the disruptive trends in oe and aftermarket - clepa.eu · source: frost & sullivan. 3...

TRANSCRIPT

The Disruptive Trends in OE

and Aftermarket

9th CLEPA Aftermarket Conference

“We Accelerate Growth”

21.03.2017 to 22.03.2017 - Belgium, Brussels

Presentation by: Franck Leveque, Partner and

Business Unit Leader, Mobility Group

2

Vehicles are Changing…

COMPLEXITY

OF SERVCE

LONGER SERVICE

INTERVALS

AGEING

VEHICLES

ALTERNATIVE MOBILITY

OPTIONS DECREASING

MILES DRIVEN

CONNECTED &

AUTONOMOUS

VEHICLES

ALTERNATIVE

POWERTRAIN VEHICLES

TECHNICIAN SKILL GAP

SERVICE INEFFICIENCY

Source: Frost & Sullivan

3

Personalised

Experience

Convenience is Key Seamless Journey

Options beyond

Ownership

Digital Expectations

So are Customer Expectations in Ownership …

4

Mega Trends Impacting Automotive Aftermarket in FutureTraditional aftermarket to face strong headwinds due to the changing nature of cars; industry should move

away from “parts & service” to “aftersales vehicle management”

AUTONOMOUS

VEHICLES

ELECTRIC

VEHICLES

CONNECTED

VEHICLES

60-80% of vehicle parc

in North America to have

ADAS/Autonomous

capabilities by 2025

Up to 20%-30% reduction in collision

repair business by 2030

6-9m BEVsin EU car parc by 2025

5.5-7m BEVsin US car parc by 2025

~95% reduction in number

of moving par;

40-50% Penetration in Europe (Parc)

55-57% Penetration

in North America (Parc)

$10-15b Telematics

$18-20b Feature on Demand

10-20% Warranty Cost

15-20% Repair TimeCUSTOMER LOYALTY

Source: Frost & Sullivan

5

Aftersales - Key Impact Areas and TrendsConvergence of business models from various impact areas will create the strongest value propositions for

customers in the future.

Source: Frost & Sullivan

• eCommerce

• Marketplaces

• Aggregators

• In-vehicle Sales

Channels

• Telematics /

Connected Car

• 3-D Printing

• Augmented Reality

• Big Data

• In-store Technology

Technology

• Subscription

• Remote

• Mobile/express

• Participatory

• Predictive

Service

• Urban Store

• Formats

• Glocalization

(Expansion to

BRIC markets)

Geography

• B2B (for eRetailers)

• Women Drivers

• Gen Y

Customers

• Electronics/

• software

• Private Labels /

Economy Parts / All Makes

• Service contracts / loyalty

Products 1

2

3

6

5

4

6

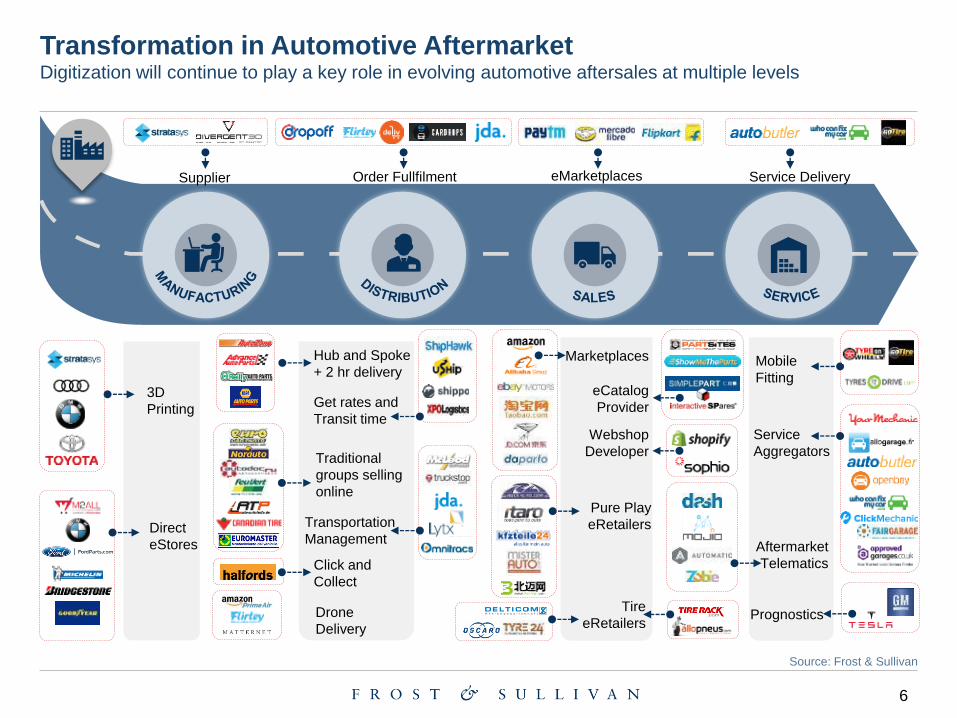

Transformation in Automotive AftermarketDigitization will continue to play a key role in evolving automotive aftersales at multiple levels

3D

Printing

Direct

eStores

Hub and Spoke

+ 2 hr delivery

Traditional

groups selling

online

Click and

Collect

Get rates and

Transit time

Transportation

Management

Mobile

Fitting

Service

Aggregators

Prognostics

Aftermarket

Telematics

Drone

Delivery

Marketplaces

eCatalog

Provider

Webshop

Developer

Pure Play

eRetailers

Tire

eRetailers

Supplier Order Fullfilment eMarketplaces Service Delivery

Source: Frost & Sullivan

7

Automotive Aftermarket - eRetailing Overview.

Automotive Aftermarket: eRetailing

Revenue, Global, 2015 and 2022

Automotive Aftermarket: eRetailing Growth

Opportunity Areas, Global, 2015–2022

Automotive Aftermarket: Top 3 eRetailing

Market Revenues, Global, 2015 and 2022

Total: $24.75

Billion

Total: $50.80

Billion 10–15%

growth forecast

15–30%

growth forecast

>30% growth

forecast

North America Germany France

North America China Germany

2015

2022

Source: Frost & Sullivan

0,0

10,0

20,0

30,0

40,0

50,0

60,0

2017 2022

Reve

nu

e (

$ B

illi

on

)

8

Aftermarket eRetailing Penetration by 2022North America and Western Europe will continue to lead in eRetailing penetration levels globally by 2022.

France

12-14%

Spain

6-7%

5-6%

China

3-4%

Mexico

India

2-3%

Brazil

4-5%

Germany

11-12%

Russia

6-7%

Italy

5-6%

North America

9-10%

UK

10-11%

Source: Frost & Sullivan

9

Parts Preference Map by Category (B2C market)While Do-it-yourself (DIY) components and accessories are most popular online, the market for DIFM

replacement part categories will grow, as sellers adopt smarter fulfilment models

Brake PartsTires

Wiper Blades

AccessoriesLubricants

Steering and Suspension Components

Filters

Heating, Ventilation, and Air

Conditioning (HVAC) Components

Body Parts

Lighting

Batteries

Starters and Alternators

Exhaust Components

Collision Body Parts

DIY to low-level labor-intensive

parts

Medium- to high-level labor-

intensive parts

Popular product categories

sold online

Not-so-popular product

categories online

Source: Frost & Sullivan

10

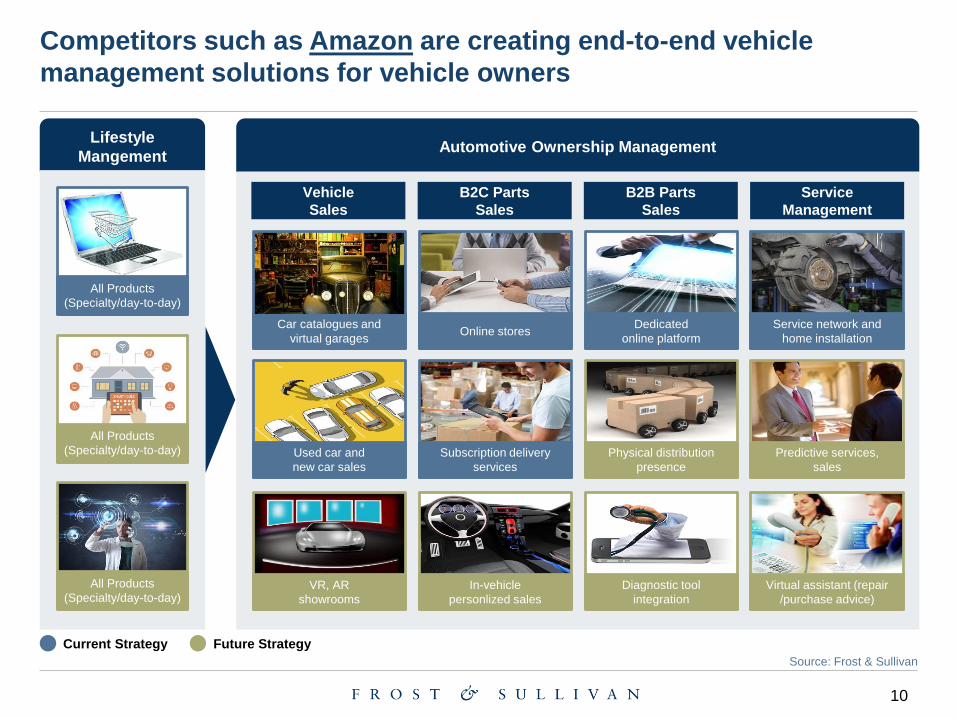

Competitors such as Amazon are creating end-to-end vehicle

management solutions for vehicle owners

Automotive Ownership ManagementLifestyle

Mangement

All Products

(Specialty/day-to-day)

All Products

(Specialty/day-to-day)

All Products

(Specialty/day-to-day)

Vehicle

Sales

B2C Parts

Sales

B2B Parts

Sales

Service

Management

Car catalogues and

virtual garagesOnline stores

Dedicated

online platform

Service network and

home installation

Used car and

new car sales

Subscription delivery

services

Physical distribution

presence

Predictive services,

sales

VR, AR

showrooms

In-vehicle

personlized sales

Diagnostic tool

integration

Virtual assistant (repair

/purchase advice)

Current Strategy Future Strategy

Source: Frost & Sullivan

11

Market Share of OES by Country – EU5The OES channel is expected to lose market share in all countries; losses in Germany and France are

likely to be lower when compared to other countries.

Source: Frost & Sullivan

Strategic Analysis of the OES Channel: Country Outlook, Europe, 2015 and 2022

OES Share (%) and

Revenue in €B in 2015OES Share (%) and

Revenue in €B in 2022 Key Areas of Impact

• Brexit could slow new vehicle sales

• OEM telematics penetration

• Service aggregation tie-ups

• Strength of franchised and authorised

networks

• Ageing vehicles

• High DIY activity

• High OES channel loyalty

• Strong DIFM market

• Ageing vehicles

• Impact of eCommerce

• Low OES channel loyalty

• Strong DIY market

• Highest in ageing vehicles

• Average vehicle age is 10 years, the

2nd-highest in the top 5 European

markets

24.8%

€ 4.01

34.9%

€ 5.68

40.5%

€ 9.05

24.7%

€ 2.83

31.8%

€ 6.01

21.3%

€ 3.98

33.5%

€ 6.15

39.1%

€ 10.01

21.2%

€ 2.74

28.3%

€ 5.99

increase in OES channel share decrease in OES channel share

12

OEM Adoption of New Business Models and Trends

PART/ACCESSORIES E-STORES

Direct:

Market

place: SOFTWARE UPDATES

AFTERSALES LOYALTY/

GIFT CARDS

MOBILE SERVICE

NEW SERVICE MODELS

Service

While You Fly

Fixed Price

Servicing

SERVICE

AGGREGATOR

/ MARKETPLACES*

ECONOMY

PARTS/ALL MAKES

Ford

(Omnicraft),

Renault

(Motrio)

VW - TPS

DIGITAL SERVICE

Online/app

booking

Digital

advisors (w/tablets)

*PSA invested in Autobutler.dk in 2015

Openbay and whocanfixmycar is popular among most OEM dealerships Source: Frost & Sullivan

13

What is Service Aggregation?Exhibit: WhoCanFixMyCar.com

Connects car owners with IAM garages and dealerships. 500 Ford dealers joined the

website, Shell selling lubricants + offering access to specialized technical support

Source: whocanfixmycar.com, Frost & Sullivan

14

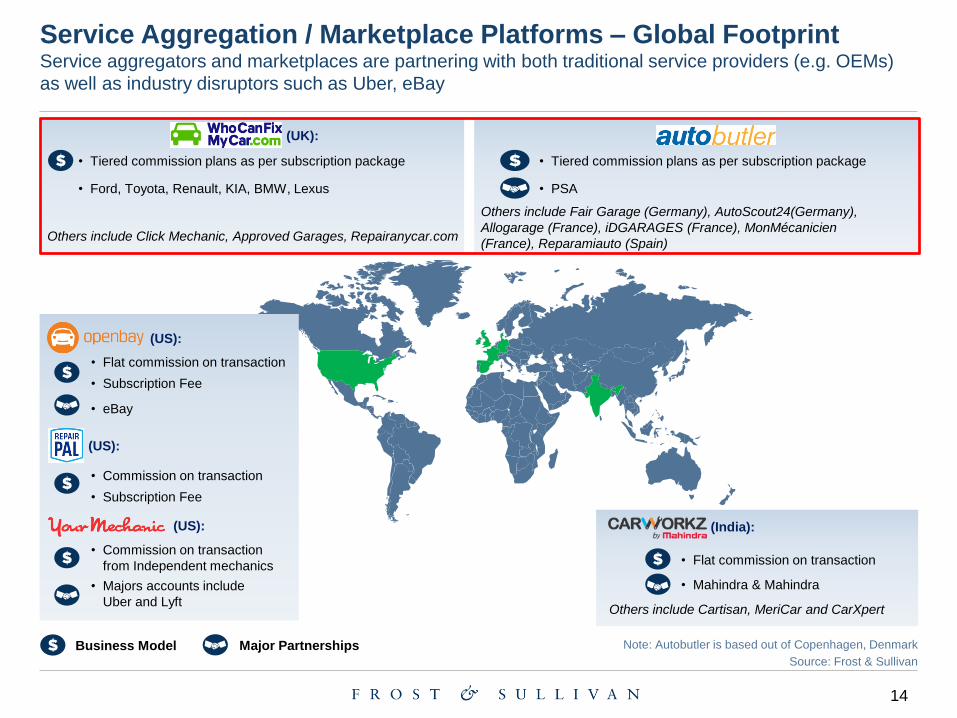

Service Aggregation / Marketplace Platforms – Global FootprintService aggregators and marketplaces are partnering with both traditional service providers (e.g. OEMs)

as well as industry disruptors such as Uber, eBay

Source: Frost & Sullivan

Note: Autobutler is based out of Copenhagen, Denmark

(US):

• Flat commission on transaction

• Subscription Fee

• eBay

(US):

• Commission on transaction

• Subscription Fee

(US):

• Commission on transaction

from Independent mechanics

• Majors accounts include

Uber and Lyft

Business Model Major Partnerships

(India):

• Flat commission on transaction

• Mahindra & Mahindra

Others include Cartisan, MeriCar and CarXpert

• Tiered commission plans as per subscription package

Others include Click Mechanic, Approved Garages, Repairanycar.com

(UK):

• Ford, Toyota, Renault, KIA, BMW, Lexus

• Tiered commission plans as per subscription package

• PSA

Others include Fair Garage (Germany), AutoScout24(Germany),

Allogarage (France), iDGARAGES (France), MonMécanicien

(France), Reparamiauto (Spain)

15

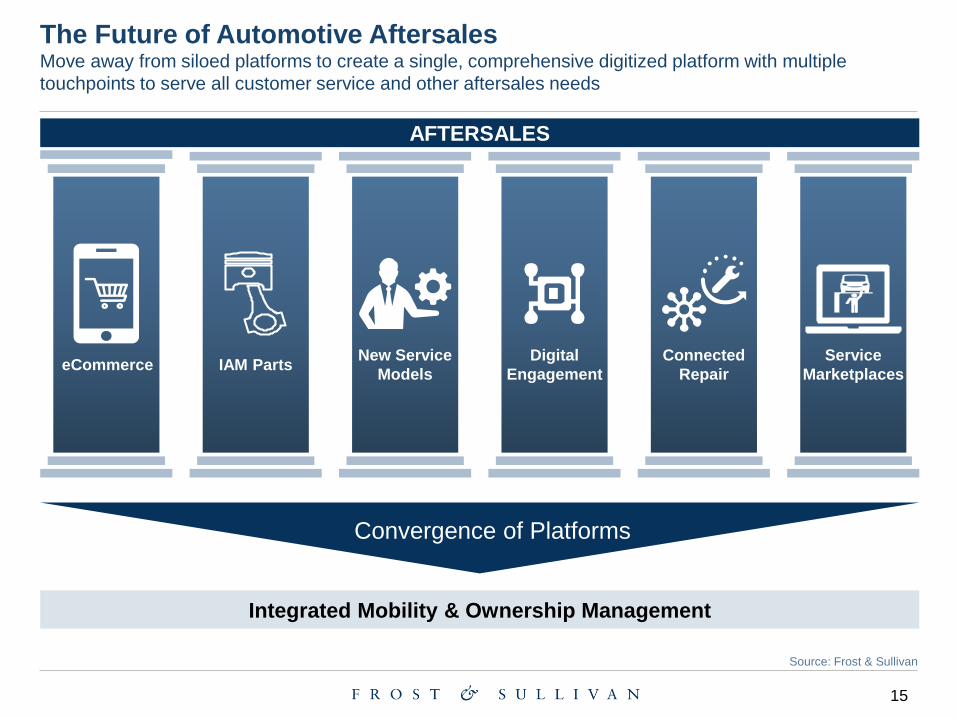

The Future of Automotive AftersalesMove away from siloed platforms to create a single, comprehensive digitized platform with multiple

touchpoints to serve all customer service and other aftersales needs

eCommerce IAM PartsNew Service

Models

Digital

Engagement

Connected

Repair

Service

Marketplaces

AFTERSALES

Integrated Mobility & Ownership Management

Convergence of Platforms

Source: Frost & Sullivan

16

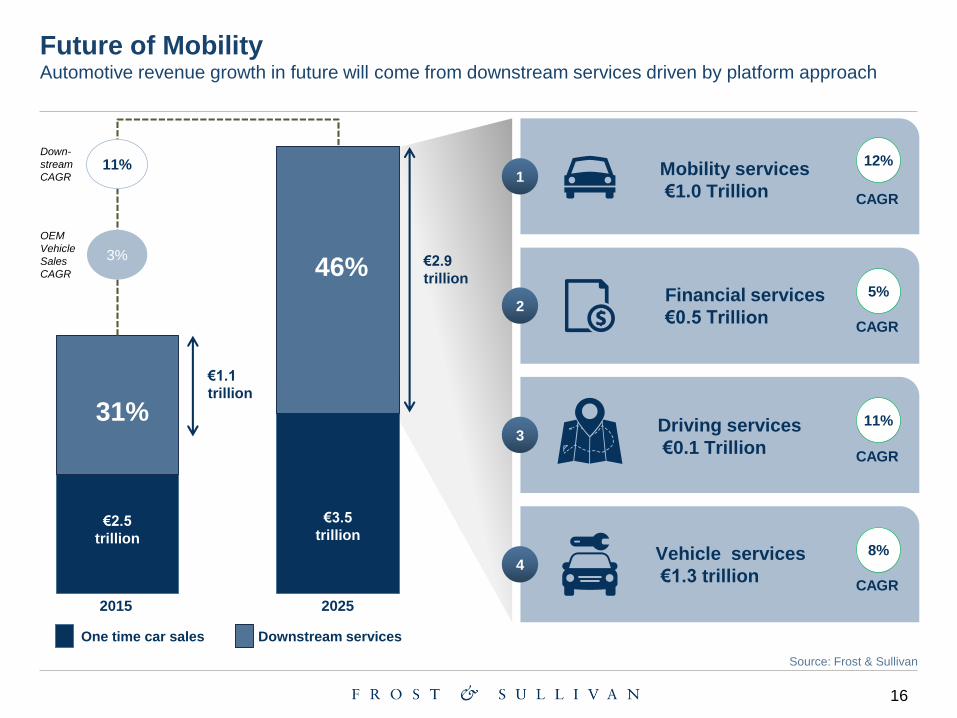

Future of MobilityAutomotive revenue growth in future will come from downstream services driven by platform approach

Financial services

€0.5 Trillion

Driving services

€0.1 Trillion

Mobility services

€1.0 Trillion

One time car sales Downstream services

Vehicle services

€1.3 trillion

2015 2025

31%

46%

€1.1

trillion

€2.9

trillion

1

2

3

4

€2.5

trillion

€3.5

trillion

12%

CAGR

5%

CAGR

11%

CAGR

8%

CAGR

11%Down-

stream

CAGR

3%

OEM

Vehicle

Sales

CAGR

Source: Frost & Sullivan

17

Join Our Mobility and Mega Trend

Groups On LinkedIn

Follow Frost & Sullivan`s series on Mega

Trends by Sarwant Singh on Forbes.comhttp://www.forbes.com/sites/sarwantsingh/

Mega Trends: Strategic

Planning and Innovation

Based on Frost & Sullivan

Research

Published Book:

New Mega Trends

Implications for our

Future Lives

By Sarwant Singh

FRANCK LEVEQUE

Partner & Business Unit Leader

Automotive & Transportation

Direct: +49 (0)69 770 33 21

Mobile: +49 (0)151 27 67 08 24

Email: [email protected]

www.frost.com

Learn More About “Digitalization

of the Automotive Industry”