the desirability of the arm’s length

TRANSCRIPT

The desirability of the arm’s length

principle in the 21st century.

J. Pleune

ANR: 666258

Master thesis

International Business Tax Economics, Tilburg School of

Economics and Management, Tilburg University

Supervisors:

dr. C.A.T. Peters

Prof. dr. P.H.J. Essers

June - 2017

Acknowledgement

There are some people I would like to thank for making this thesis possible. Their help and support have

made the process of writing a lot easier, and this thesis would not have been the same without them.

First of all, I would like to thank my thesis advisor, dr. Cees Peters of the School of Economics and

Management. You allowed this thesis to be my own work, but steered me in the right direction whenever

you thought I needed it. I appreciated the honesty of the advice when certain things might have been

interesting to add to my research, but might not work out the way I anticipated. This really helped me to

stay within the scope of the subject of this thesis. Moreover, I learned to look at issues from different

perspectives, which has been an important tool in order to increase the framework of my thinking. Moreover,

thank you for the time reading the draft versions and to discuss your observations and critical notes,

especially in the final stages of the process.

Additionally, I want to thank my fellow students at Tilburg University. While this thesis has been an

individual project, it has greatly benefited from your knowledge and assistance. The best of luck and many

thanks go out to Rens de Zwart, Reno Nabben, and Charis Papalampros for your help and advice on the

thesis. I am glad you were there to listen whenever I ran into issues or whenever I had a question about my

thesis. I hope I have returned the favor. I wish you all the best in your professional lives.

Finally, I would like to express my gratitude to my parents and brothers for providing me the support and

continues encouragement throughout my years of studying at Tilburg University. Your confidence in me

has made this accomplishment possible. Thank you.

Jelle Pleune, Tilburg, June 19, 2017

Table of Contents 1. Introduction ................................................................................................................................... 1

2. Transfer pricing ............................................................................................................................. 5

2.1 Introduction ............................................................................................................................. 5

2.2 Transfer Pricing Goals ............................................................................................................. 7

2.3 Transfer Pricing Mismatches .................................................................................................... 8

2.4 Functions of taxation ................................................................................................................ 8

2.4.1 Function 1: Revenue ......................................................................................................... 9

2.4.2 Function 2: Distribution .................................................................................................... 9

2.4.3 Function 3: Regulation ................................................................................................... 10

2.4.4 Function 4: Simplification .............................................................................................. 10

2.4.5 Function 5: Robustness ................................................................................................... 11

2.5 Summary ............................................................................................................................... 11

3. The Arm’s Length Principle ........................................................................................................ 12

3.1 Introduction ........................................................................................................................... 12

3.2 The origin of the arm’s length principle .................................................................................. 13

3.3 Separate entity approach ........................................................................................................ 14

3.4 Comparability analysis ........................................................................................................... 15

3.4.1 Commercial and financial relations ................................................................................. 15

3.4.2 Comparable transactions ................................................................................................. 17

3.5 Transfer pricing methods ........................................................................................................ 17

3.5.1 Traditional transaction methods ...................................................................................... 18

3.5.2 Transactional profit methods .......................................................................................... 18

3.6 Criticism on the arm’s length principle ................................................................................... 19

3.6.1 Reflecting economic reality: comparability ..................................................................... 19

3.6.2 Reflecting economic reality: integration .......................................................................... 20

3.6.3 Feasibility ...................................................................................................................... 21

3.6.4 Opinion OECD ............................................................................................................... 22

3.7 The Benchmark ...................................................................................................................... 22

3.7.1 Benchmarking the arm’s length principle ........................................................................ 24

3.8 Summary ............................................................................................................................... 25

4. Intangibles .................................................................................................................................... 26

4.1. Introduction ........................................................................................................................... 26

4.2 Defining Intangibles ............................................................................................................... 26

4.3 Intangibles at arm’s length ..................................................................................................... 27

4.4 Typical IP Structures .............................................................................................................. 29

4.4.1 Mobility ......................................................................................................................... 30

4.4.2 The basic structure .......................................................................................................... 30

4.5 The Double Irish Dutch Sandwich .......................................................................................... 31

4.5.1 The complex structure .................................................................................................... 32

4.5.2 Low tax payment on the initial IP transfer ....................................................................... 33

4.5.3 Setting high royalty payments ......................................................................................... 33

4.6 New Guidance ....................................................................................................................... 33

4.6.1 Information asymmetry .................................................................................................. 34

4.6.2 Cost approach ................................................................................................................. 35

4.6.3 Benchmarking the DEMPE-method ................................................................................ 37

4.7 Summary ............................................................................................................................... 38

5. Alternative approaches ................................................................................................................ 39

5.1. Introduction ........................................................................................................................... 39

5.2. Destination-based cash flow tax ............................................................................................. 39

5.2.1 Criticism ........................................................................................................................ 41

5.2.2 Benchmarking ................................................................................................................ 42

5.3. Formulary of apportionment ................................................................................................... 43

5.3.1. Criticism ........................................................................................................................ 44

5.3.2. Benchmarking ................................................................................................................ 45

6. Conclusion and recommendations............................................................................................... 47

Reference list ....................................................................................................................................... 49

1

1. Introduction

Big multinational corporations are often named and shamed by NGO’s, journalists and news channels for

not paying their fair share.1 These multinational corporations are blamed for having an immoral and non-

transparent strategy that consists of reducing the global tax burden of the group. By transferring profits

from one country to the other, multinational enterprises (MNEs) are notorious for allocating profits to

countries that levy less or no corporate tax.

The role of international companies in world trade has increased a lot in the last two decades.2 This increase

of globalization has also increased the number of transactions between entities belonging to the same

multinational group, as they become more integrated with one another.3 This increase of intercompany

transactions, in turn, leads to an increase of complexity of issues regarding the allocation of profits that

derive from their intercompany transactions.4 Due to this increased complexity of group structures, a group

structure may be exposed to certain risks associated with the taxation of corporate income. The worst risk

for an MNE is that the same income may be taxed twice in different jurisdictions. On the other hand, a

group structure may also offer great opportunities for tax planning, where for instance income may be not

taxed at all.

In order to make use of this double non-taxation, MNEs use transfer pricing within their tax policies. This

means that MNEs use intercompany trade to shift money between parents, subsidiaries, and affiliates

operating in different countries.5 Governments try to counter this behavior, so that profits derived from

these intercompany transactions are allocated in a fair manner. However, as globalization tends to increase

the complexity of transfer pricing, and because of the lack of harmonization between countries,

governments have a hard task to achieve a fair allocation of taxing rights. Therefore, transfer pricing

implications of business structures and supply chains have been a focus area of recent public debate.6 In

fact, today, there are few issues more controversial than international transfer pricing.7

It may be hard to grasp the size of transfer pricing issues at first, but its size is enormous. According to

UNCTAD8, in the early 1990s, there were about 37,000 international companies with 175.000 foreign

subsidiaries. In 2004 these numbers increased to 64,000 and 870,000 respectively. 9 Moreover, the US

1 See for example Devereux & Fella (2014) p. 11. 2 OECD (2015) Action 8-10 final reports, p.9. 3 Lohse et al. (2012) p.2. 4 Radolović (2012) p.30. 5 Baker (2005) p.30. 6 Beer & Loeprich (2015). 7 Mura et al. (2013) p. 483. 8 UNCTAD is a permanent intergovernmental body established by the United Nations General Assembly. 9 The Economist (2004).

2

Consensus Bureau reported that in 2014, 51% of the goods imported in the US came from related

companies.10 The trade that these MNEs conduct with related parties is highly sensitive to transfer pricing.11

It is expected that cross-border trade between related companies will continue to increase both in absolute

numbers and as a percentage of world trade.12 Moreover, for many MNEs, exaggerated transfer pricing is

standard procedure and forms a major part of the global strategy to minimize taxes.13 Transfer pricing

manipulation has been said to be one of the easiest ways to avoid taxation and is, therefore, one of the most

common techniques of tax avoidance.14 Other recent studies also suggest that a major fraction of income

shifting is achieved specifically in MNE’s that hold intangible property.15 Especially in times of recession,

countries are afraid to lose tax revenue and aim to counter tax avoidance by MNEs by implementing stricter

regulation.16 However, as transfer pricing often involves many jurisdictions, this issue challenges the tax

systems worldwide.17 Therefore, an adequate solution may not be easy to achieve.

The current transfer pricing legislation is based on a principle that looks at companies within an MNE in a

separate and independent manner. This may have suited the economic reality of a century ago, but as a

consequence of globalization, European integration, the rise of MNEs, and the increased value of intangible

assets the world of a century ago has changed significantly.18 However, the issue is that the current principle,

which was developed in the 1920s, is still governing the allocation of taxable profits today. Especially as a

consequence of globalization and the fact that intangible assets of MNE’s have gained so much in value, I

argue that reconsideration of the foundations of the current transfer pricing regime is necessary.19 Due to

more globalization, we cannot simply rely on the foundations that have been laid a century ago. As a

consequence, I believe the international tax regime to be in dire need of reform.20

Therefore, in this thesis, I have tried to explore the reasons for the current transfer pricing regulation and

see whether its foundations are still adequate in the current global economy. The research question that has

10 See US Census Bureau (2014) 11 Cools et al. (2008). 12 See for example: Oguttu (2006) p.41; Becker (1996). 13 Baker (2005) p.30. 14 Schoueri (2015) p.690; Auerbach et al. (2017) p. 27. 15 Tran et al. (2016) p.28. 16 Lohse & Riedel (2013) p.2: Ever more countries require corporations to submit detailed documentation to the tax

authorities to justify their intracompany prices and the profit distribution amongst affiliated companies. Failure to

provide adequate documentation would trigger penalties in many countries. The authors find that profit shifting is

reduced with about 50% when countries tighten transfer pricing documentation. 17 Lohse et al. (2012). 18 De Wilde (2015) p.5. 19 See for example for the effects of intangible assets in MNEs: Adams (2015) page 91; Auerbach et al. (2017) p. 27. 20 Devereux & Vella (2014) p. 11.

3

been my starting point is: What shortcomings does the arm’s length principle have regarding the

valuation of intangibles and which alternatives might be desirable?

The objective of this thesis is twofold. First, I will explain the flaws of the foundation of transfer pricing

regulation in the well-developed and high-tech 21st century. Secondly, by focusing more specifically on

intangible property, I will investigate whether there may be other approaches that would be more desirable

as a foundation for transfer pricing regulation.

To conduct my research I had to look at transfer pricing from several perspectives, specifically from a legal

and economic perspective. There is a strong interrelationship between these two fields regarding transfer

pricing. The economic consequences of the transfer pricing practices by MNEs have led to reactions of

regulatory bodies, and regulation has led to change in transfer pricing policies of MNEs. Therefore, I believe

it is imperative to combine both perspectives in this thesis in order to address the issue of transfer pricing.

By focusing on practical problems and the regulatory solutions to these problems, I will argue whether or

not the arm’s length principle is still the most appropriate basis for transfer pricing. By means of a

systematic review, I have collected and critically analyzed the literature on the matter. Moreover, I have

used the arguments obtained in my review to establish a benchmark. This benchmark was used accordingly

to test the desirability of the arm’s length principle and the alternative approaches. This has provided me

with sufficient knowledge of the current literature relevant to be able to answer my research question.

Thus, this thesis will deliver a contribution to the current discussion on base erosion and profit shifting

(BEPS), especially by focusing more on the current globalized world, in which intangible assets are

becoming an ever-more important value driver for MNEs. By focusing on the strengths and weaknesses of

transfer pricing approaches in light of the 21st century, I believe this thesis contributes to developing a new

international tax system. In this line of reasoning, I argue that the current transfer pricing regulation should

be reconsidered.

The limitation of this thesis is that it relies heavily on academic literature and there is a lack of empirical

data to substantiate my point. Even though I have tried to support my arguments with data, this data was

not obtained by myself but gathered from existing sources. Therefore, the economic effects of my proposed

policy recommendations are uncertain and have to be researched further. Furthermore, I focus on the basis

of transfer pricing regulation and not so much on the documentation requirements as recently imposed by

the OECD member countries. However, I do believe that a bottom-up approach for transfer pricing

regulation is much more useful than a top-down approach, as I believe that the foundation of transfer pricing

regulation is on shaky ground due to the increased importance of intangible assets. Therefore, it is not my

goal to come up with a well-defined alternative international tax regime. Instead, I have sought to discover

4

the flaws of the current system and tried to provide an alternative framework to base transfer pricing

regulation on.

In order to answer my research question in a logical order, this thesis is divided into 6 chapters, with the

introduction of the subject being the first chapter. In Chapter 2, the concept of transfer pricing is thoroughly

explained. This chapter shows the logical development of distrust in the current international tax system as

the functions of taxation are in danger as a consequence of mismatches that exist between countries. Whilst

Chapter 2 has a more economic and descriptive approach, Chapter 3 will deal with the legal basis of transfer

pricing regulation; the arm’s length principle and the separate entity approach. In Chapter 3, special focus

is given to the rules initiated by the OECD member countries. After discussing the arm’s length principle

in Chapter 3, I have developed a benchmark in this Chapter based on the strengths and weaknesses of the

arm’s length principle. This benchmark will be used to compare the alternative approaches of Chapter 5

with. Chapters 4 and 5 form the core of my thesis. These chapters focus more on the current globalized

world and the practical complications of the arm’s length principle concerning intangibles and the flaws of

international taxation in this context. Moreover, in Chapter 5, attention will be given to alternative

approaches of the arm’s length principle, and their desirability will be tested against the benchmark formed

in Chapter 3. Finally, in Chapter 6, my research is concluded and policy recommendations regarding the

foundations of transfer pricing regulation will be made.

5

2. Transfer pricing

2.1 Introduction First, I believe some knowledge on the basis of transfer pricing is required. A transfer price is a price that

is charged for a cross-border transfer of goods and services. Transfer pricing only deals with international

transactions within the same Multinational Enterprise (MNE). An MNE consists of at least a parent

company in one country and one subsidiary in another country (see the figure below).

Figure: Basic figure of an MNE, with Parent company (P) in one country and subsidiary 1, 2 and 3 in another country.

In order for there to be possible transfer pricing issues, two requirements have to be fulfilled. First, transfer

pricing issues can only occur in international situations. Transfer pricing between subsidiaries of an MNE

which are all resident of one jurisdiction usually poses little to nihil tax avoidance problems since the

relevant national law is the same for all these subsidiaries.21 Think of the following domestic example based

on the figure above. Entity S1 and S2 are both located in the Netherlands and conduct business with each

other. S1 sells semi-final goods to S2 for a price of EUR 10, with the costs of goods sold of EUR 5. In a

fair market, the selling price of this semi-final good would be EUR 15. S2 then sells these goods onwards

to a third party in another country for EUR 20. Therefore, S1 receives a profit of EUR 5 (EUR 10 – EUR

5), and S2 receives a profit of EUR 10 (EUR 20 – EUR 10). The total profit that will be taxed in the

Netherlands is EUR 5 + EUR 10 = EUR 15, regardless of the fair market price of the semi-final good. From

a Dutch tax perspective, therefore, it does not matter how the profits are allocated between entities in a

purely domestic situation.22

21 Oguttu (2006) p. 138. 22 It only matters to the extent that two companies can make use of the lower corporate rate twice, instead of once.

See for example Article 22 of the Dutch Corporation Income Tax 1969.

6

However, internationally it does matter, as states wish to execute their rights of taxation based on the

allocation of jurisdictions.23 Picture the following example where company P is established in Germany

and Company S1 is established in the Netherlands and both companies belong to the same group. Company

P sells goods to Company S1. When company P sells goods for a price that is much higher than normal

market prices, the effect is that profits of Company P are increased and so are the costs of company S1.

This also means that Germany can tax over a higher tax base, whereas the Netherlands is left with a smaller

piece of the pie. Therefore, transfer pricing issues may occur in international situations.24

The second requirement for transfer pricing issues is that it only concerns affiliated companies.25 The ratio

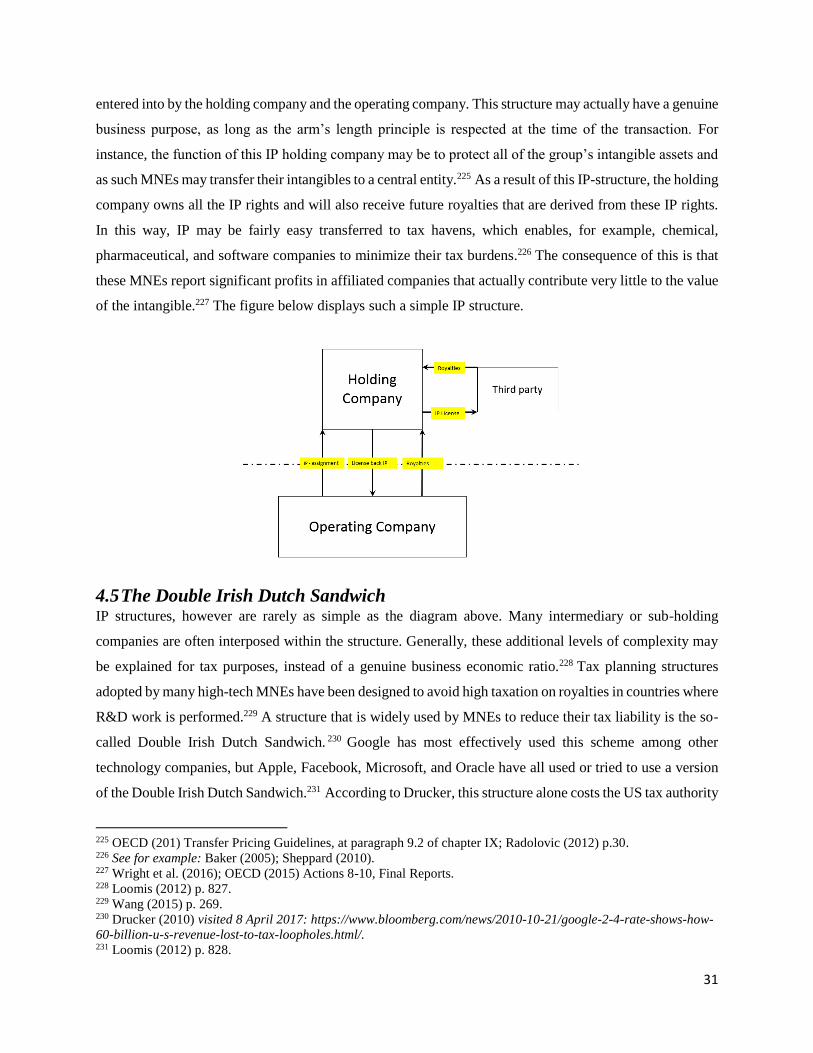

behind the requirement of affiliation is that there is wide consensus in economic literature that independent

parties would never conduct trade that would be disadvantageous to them. 26 In the example above,

Company P owns 100% of the shares of its subsidiaries. Such ownership makes it possible for the

shareholder to influence the decisions made by the subsidiary. This means that, as a consequence of the

relationship between the two entities, the price of the goods may be set at higher or lower prices compared

to the market price. Or as Schoueri puts it correctly:

“Taxpayers carrying out a controlled transaction have sufficient power to misprice the operation,

thereby jeopardizing the taxation of income. This would lead to a situation in which the entities of an

MNE were taxed less than independent parties would be, even if they undertook the same transaction.”27

In the above example, when tax rates would have been lower in Germany and higher in the Netherlands,

MNEs would like to have as much profit taxed in Germany instead of the Netherlands, in order to reduce

their total tax bill.28 Affiliated companies within an MNE group may, therefore, have an incentive to use

transfer pricing in a way to manipulate profits to have most of the profits taxed in countries with lower tax

rates and thereby reducing their tax burden.29 However, this leads to international transfer pricing issues, as

countries wish to execute their power of sovereignty and make sure that profits are not shifted outside their

jurisdiction and to keep their tax base from being eroded.30

23 De Wilde (2015) p.51; Graetz (2001) p.278. 24 See for example Palmer (1989) p.3: the author says that the difficulty lies in specifying the income over which a

nation should have jurisdiction. 25 Parties are seen as associated parties when an entity directly or indirectly holds capital, management or oversight

in another entity. The first mentioned entity must be able to influence the other entity. I.e. the entity must have

sufficient control to influence the prices set in associated transaction (>50% of the voting rights). 26 See for example Avi-Yonah (2007) p. 17; OECD Transfer Pricing Guidelines (2010) paragraph 1.38. 27 Schoueri (2015) p. 695. 28 Baker (2005) p.30; Tran et al. (2016) p.28. 29 Oguttu (2006) p. 140. 30 OECD (2015). BEPS Final Reports, Action 1 – 15.

7

2.2 Transfer Pricing Goals Transfer pricing is becoming ever-more important to MNEs in a globalized economy where their operations

involve countries with different tax regimes and regulations.31 The main goals for an efficient transfer

pricing policy are to maximize consolidated profits and to minimize tax liabilities.32 By maximizing

expenses in a high-tax jurisdiction and maximizing income in a low-tax jurisdiction, the overall tax bill is

logically reduced.33 Another study shows that the effective tax rate of MNEs that focus on minimizing taxes

is on average 6.6% lower compared to an MNE that is more focused on tax compliance instead.34 Therefore,

it seems that transfer pricing strategies pay off.35

Research shows that differences in tax rates between tax jurisdictions play a significant role in an MNE’s

strategy when setting transfer prices.36 Other tax-related objectives for transfer pricing may be to utilize

other attributes, such as tax incentives, subsidies or the use of losses that would otherwise expire after a

certain number of years.37 An opinion that exists in literature is that tax can also be seen as a normal cost

of doing business, and as businesses are constantly looking to increase revenue and save costs, naturally a

good manager will try to manage the tax bill as well as any other bill.38

It must be noted that transfer pricing is not only driven by tax incentives, simplicity is also a very important

argument for MNEs to commence transfer pricing. It is easy to have all the supporting functions, financing,

IT, know-how etc. centralized in one entity, instead of being spread out across many companies. Other

objectives of designing efficient transfer pricing policies may be to increase the market share and reduce

the impact of economic constraints.39 Therefore, transfer pricing is not always driven by tax economic

reasons but may be justified by business economic reasons as well.

31 Baker (2005) p.30; Cools et al. (2008) p. 605. 32 Sikka and Wilmott (2010) p.7. 33 PwC (2009). 34 Klassen et al. (2016) p. 455. 35 Baker (2005) p.30. 36 See for example Behrens et al. (2014) p.652; Tran et al. (2016) p.41: the authors have proven that companies set

low transfer prices when the foreign tax rate is larger than the home tax rate, and the reverse is also true. 37 Kobetsky (2008). 38 Sikka and Wilmott (2010) p.7. 39 Radolovic (2012) p.30

8

2.3 Transfer Pricing Mismatches In the previous paragraphs, we have seen that the effects of transfer pricing can be very advantageous for

MNEs.40 However, there is another – darker – side of the same coin. When transfer pricing does not reflect

market forces, the expenses and revenues, and as consequence, the profit and tax liabilities of the affiliated

companies could be distorted.41 Or how Malesky puts it:

“Transfer pricing becomes a concern when it is incorrectly applied to lower profits in a division of an

enterprise that is located in a high-tax jurisdiction and to raise profits in a country that levies no or low

taxes.” 42

This ‘artificial’ transfer pricing leads to mismatches and leaves countries with the perception that the most

valuable links in the value chains of MNEs are ‘missing’. Therefore, it is believed that these artificial

schemes and abusive transfer pricing policies are to blame for the lack of tax revenue in jurisdictions.43

Especially in times of recessions or depressions or when developing countries are concerned, such blaming,

naming and shaming finds global political appeal. 44 Therefore, tax authorities in many countries are

modernizing their legislation in order to safeguard the collection of a fair amount of tax in their

jurisdiction.45 Viewed in this context, transfer pricing rules have been regarded as a necessary tool to stop

MNEs from easily avoiding or reducing taxation by shifting profits to low-tax jurisdictions. 46 As a

consequence, transfer pricing has become a very controversial topic and ever-more professionals and public

officials are engaged in establishing and revising the rules of transfer pricing.47

2.4 Functions of taxation This political reaction to tax avoidance seems logical when taking into account the fact that transfer pricing

directly affects the taxes a jurisdiction may levy upon corporate profits.48 The revenue of these taxes is used

to finance public expenses, which explains the aversion of the society when people read about MNEs that

might not pay their fair share of taxes.49 Therefore, paying corporate tax can be seen as a contribution to

40 Klassen et al. (2016) p. 455. 41 OECD (2010) Transfer Pricing Guidelines. Page 32. 42 Malesky (2015). 43 Tavares and Owens (2015) p. 591. 44 For example in Papua New Guinea in the forestry business alone, it is estimated that in 1999, between $ 9 million

and $ 17 million was lost in tax revenues due to transfer pricing practices. This amount far exceeds the country’s

education and healthcare budget. These are lost revenues that are vital for the economic development of developing

countries. This shows that transfer pricing mismatches can seriously harm the economic development of countries

and that these mismatches have to be countered. Christian-Aid (2008). 45 Elliott and Emmanuel (2000) p. 216. 46 Brauner (2008). 47 It is a complex game with many actors; MNEs, lawyers, accountants, consultants, tax authorities, governments,

the OECD, the UN, NGO’s etc. 48 Sikka and Wilmott (2010) pp. 3-4. 49 See for example: Escribano (2017) p.250.

9

social development or as a return on the investment made by the jurisdiction to facilitate business

activities.50 Below I will briefly describe the most important functions of taxation. For each of the functions,

I will indicate whether or not I believe the function is important from a transfer pricing perspective.

Moreover, the useful functions will be used in the next chapter to develop a benchmark in order to test

transfer pricing regulation against.

2.4.1 Function 1: Revenue

The first and foremost goal of taxation is to raise revenue in order to fund the necessary governmental

functions, such as providing public goods or services.51 Even though people tend to disagree about what

functions of government are truly necessary, and what size of government is appropriate, there is a

widespread agreement that a government is indeed needed.52 I believe that the revenue function of taxation

is very important, as a government simply needs the money to function. However, I do not consider it to be

of major importance in the context of transfer pricing. The reason is that transfer pricing as such, is not a

tax, and therefore it cannot create wealth for a government. Based hereon I consider this revenue function

to be a secondary goal from a transfer pricing perspective. In my opinion, transfer pricing regulation should

merely make sure the corporate income tax laws are executed in a fair manner.

2.4.2 Function 2: Distribution

The second function of taxation is to redistribute wealth, especially to reduce the unequal distribution

between the poor and the rich. According to Vogel, this distributive function can be viewed from two

perspectives.53 First of all, the tax burden has to be fairly distributed among the taxpayers of a jurisdiction.

The ability-to-pay-concept has been regarded as an acceptable standard for the fair distribution of tax

burdens within a jurisdiction.54 States often believe a citizen’s income is the key figure to calculate one’s

ability to pay.55

However, as discussed, transfer pricing is a purely international issue, and therefore the collection of tax

has to be distributed between states as well. 56 The competence of states to tax the profits of MNEs does not

extend beyond the borders of a country. In other words, the fiscal sovereignty which states need to levy tax

50 Countries invest in infrastructure, education, healthcare etc. which are factors businesses directly benefit of. This

benefit principle is a very important principle in taxation. 51 Herrington & Lowell (2017) p. 5. The authors say that the budget of each jurisdiction in which an MNE conducts

business operations incurs expense for providing public services, such as safety, fire and police protection, roads,

hospitals, national defense, and education. 52 Dennis (2002) p.3. 53 Vogel (1977). 54 Schoeuri (2015) p.695. 55 Schoeuri (2015) p.695. 56 Vogel (1977).

10

is limited to economic activities that take place within their territory.57 Therefore, the principles upon which

countries agree upon to allocate tax revenues are critical for the global tax environment.58 I believe that the

latter is very important when designing transfer pricing approaches. Especially as today’s world economy

is ever-more globalized and dominated by MNEs, I believe that there must be harmony in the distribution

of tax jurisdictions. 59

2.4.3 Function 3: Regulation

The third goal of taxation is its regulatory function. Taxation can be used to steer the activities of the private

sector in the directions that are desired by governments.60 For example, by encouraging or discouraging

certain behavior, and to correct market imperfections, taxation is used to give direction to the society.61 De

Wilde believes this function is irrelevant as far as corporate taxation is concerned. He argues that the sole

purpose of corporate taxation should be to fund government spending, and not to steer business decisions,

not in a positive, nor negative way.62 I agree with him and I believe this function to be less relevant from a

transfer pricing perspective.

2.4.4 Function 4: Simplification

According to Klaus Vogel, a fourth function should be added to the levying of taxes. He calls it the

Vereinfachungsfunktion, i.e. the simplification of the tax system.63 This encompasses that the system should

be able to comprehend so that taxpayers can figure out how much time and effort they have to invest in

complying with the tax system.64 Personally, I believe that rules should be clear, and any uncertainty should

be minimized. In the absence of clear rules, neither the taxpayer or tax authority can know in advance the

likelihood of the tax burden and tax revenue, respectively.65 An efficient system should not contain a

complexity of exemptions, deductions, and tax credits.66 However, in the current tax environment, MNEs

are surrounded by transfer pricing risks due to uncertainties, and these uncertainties have to be managed

within the MNE.67 I believe taxes should impact business decisions as little as possible, and every distortion

should be minimized.68 Therefore, I believe this fourth function to be very important from a transfer pricing

57 De Wilde (2015) p.51 58 Herrington & Lowell (2017) p.6. 59 De Wilde (2015) p.51; Herrington & Lowell (2017) p.6. 60 Avi-Yonah (2006) p. 3 61 See for example: Bird and Zolt (2005) p. 1630. 62 De Wilde (2015) p.37 63 Vogel (1977); see also: Avi-Yonah (1996): The structure of International taxation: A proposal for simplification. 64 Rabuschka (2000) p. 4. 65 Avi-Yonah (2007) p.25. 66 Rabuschka (2000) p. 4. 67 Rossing (2013) p. 177. 68 De Wilde (2015) p. 54: the author says it basically requires the tax system produces as little red tape as possible.

11

perspective. Especially considering the fact that every country should be able to implement the regulation,

and every MNE should be able to understand the rules.

2.4.5 Function 5: Robustness

I would like to add a fifth function as I believe that the possibility of abuse should be kept at a minimal

level when introducing new rules concerning taxation. The European Commission argues that the world

has treated tax planning as a legitimate practice, but that over time, structures are becoming too aggressive.69

As mentioned in my introduction, transfer pricing has indeed become standard procedure for the tax

planning activities of many MNEs.70 Moreover, combatting tax avoidance through affiliated companies

was one of the original motives to enact transfer pricing rules in the first place.71 Also, Eden says that the

main purpose of transfer pricing regulation is to combat tax avoidance by MNEs.72 However, regulation

cannot be effective if either creates profit shifting incentives or if fails to combat tax avoidance. For these

reasons, I believe that this fifth function is very important to keep in mind when designing transfer pricing

policies.

2.5 Summary In this chapter, I introduced the concept of transfer pricing. The main goals for MNEs to commence efficient

transfer pricing policies are to maximize consolidated profits and minimizing tax liabilities. However,

transfer pricing is not always driven by tax economic reasons but may be justified by business economic

reasons as well. Unfortunately, transfer pricing has become a concern for jurisdictions, because transfer

pricing is incorrectly applied in order to artificially reduce taxation. Therefore, governments by

implementing transfer pricing regulation. In order for this regulation to be effective, I argued that regulation

should distribute taxing rights in a fair manner, rules must be easy to understand, and tax avoidance should

be minimized.

Having introduced the concept of transfer pricing in this chapter, I will now focus more on the arm’s length

principle, currently being the underlying principle of transfer pricing regulation.

69European Commission (2012) Recommendation on Aggressive Tax Planning, C(2012) 8806 Final, p. 2. 70 See for example: Barker (2017); Baker (2005) p.30; Bartelsman & Beetsma (2003). 71 See Avi-Yonah (2007) p. 3. He refers to the direct predecessor of Section 482 of the Code which dates back to

1921, when the IRS was authorized to consolidate the accounts of affiliated corporations "for the purpose of making

an accurate distribution or apportionment of gains, profits, income, deductions, or capital between or among such

related trades or business."; OECD (2010) Transfer Pricing Guidelines, at page 31. 72 Eden (1998) p.104.

12

3. The Arm’s Length Principle

3.1 Introduction As discussed in the previous chapter, transfer pricing policies of MNEs may be detrimental to the execution

of the taxing rights of states. Firms may achieve income shifting results by using prices for intragroup sales

that depart from fair market conditions, by for example agreeing on; excessive management or overhead

fees, or costs for IT services, that an independent party would never agree upon.73 The fact that differential

tax regimes exist among states, gives MNEs the incentive to engage in income shifting by means of transfer

pricing.74 The distribution of taxing rights has, therefore, become one of the most important functions of

international taxation.

In order to distribute taxing rights, the arm’s length principle was introduced a century ago and still, lies at

the basis of transfer pricing legislation.75 It was first defined in US corporate tax legislation in 1935 as a

standard that an uncontrolled taxpayer would always deal at arm’s length with another uncontrolled

taxpayer.76 This principle provides an international yardstick to judge whether transfer prices are correct

from a tax perspective. As Brauner correctly describes in my opinion, this principle is still the “…heart,

spirit and foundation of the current international transfer pricing system”.77 OECD countries have agreed

upon this principle and it is used to counter income shifting, tax base erosion and double taxation. 78

However, the arm’s length principle should not be mistaken for an anti-tax avoidance rule. 79 Indeed, it is

merely a means to base anti-tax avoidance rules on; it is not an objective as such.80

The OECD has adopted the principle in Article 9 of the OECD Model Convention.81 In the wording of the

OECD, we can conclude that prices affiliated companies charge to each other should be the same as when

two unrelated parties would transact with one another. In other words, sales between affiliated enterprises

should represent fair market prices. From the same article of the OECD Model Convention, we can also

conclude that it is the foundation for the comparability analysis because it initiated the requirement of:

73 Weichenrieder (2009) p.2. 74 Cools et al. (2008) p. 605. 75 De Wilde (2015) p.6: “In these early days of international taxation the League of Nations, as the ‘predecessor’ of

the United Nations and the OECD, drafted the first Model Tax Conventions on Income and Capital.” 76 Eden (200) p. 675. 77 Brauner (2008) p.96. 78 Wittendorff (2011) p.227. 79 Pankiv (2016) p.463 80 See Schoeuri (2015) p. 704: The mere fact that over 4,000 tax treaties are currently in force that adopt the arm’s

length principle, makes this principle important for tax avoidance purposes. 81 See Schoeuri (2015) p. 704: over 4,000 tax treaties based on the OECD Model Tax Convention are currently in

force that adopt the arm’s length principle.

13

“A comparison between conditions (including but not only prices) made or imposed between associated

enterprises and those which would be made between independent enterprises, in order to determine

whether the determination of profits is at arm’s length.”82

Although the arm’s length principle has been used to provide for fairness in the distribution of tax revenues

among countries, its original intent was the need for equality between affiliated and unrelated firms, as can

be concluded from the wording of the OECD.83 By doing so, it aims to avoid creating tax advantages that

would distort the relative competitive positions of either type of entity.84 The ratio behind the comparing

against independent enterprises is that when independent parties deal with each other, the conditions of the

transactions ordinarily are determined by market forces. Due to opposing interest of both parties, one may

expect a fair market price will rule the transaction. On the other hand, when affiliated companies deal with

each other, the conditions of the transactions may be not directly affected by market forces in their dealings

with each other.85

3.2 The origin of the arm’s length principle There is some doubt as to where the arm’s length principle found its origin, but the principle has originated

from the domestic laws of each state. 86 The OECD has developed the Transfer Pricing Guidelines

(hereafter: the Guidelines) in the past three decades to standardize these different national interpretations

in order to make the principle more suitable for international use.87 Nowadays, however, domestic rules are

reshaped in order to align them with the Guidelines. Today, the Guidelines represent a new way for

regulating global tax issues to correct the problems that arise when unilateral approaches are unable to solve

transfer pricing issues.88 Already in 2011, there were more than 60 countries which had implemented laws

and regulations regarding transfer pricing, based on the Guidelines. By 2016, over 85 countries

implemented transfer pricing regulation.89

The general idea behind the arm’s length principle is to allocate the profits to each part of the value chain

that attributes to the value of the chain. This should ultimately lead to the point where each country in the

value chain can levy a tax based on a tax base, which is equivalent to the actual value created in that specific

country.90 Therefore, the arm’s length principle is believed to serve the distributive function very well.

82 OECD (2010) Transfer Pricing Guidelines, at p. 34, paragraph 1.7. 83 Schoueri (2015) p. 695. 84 OECD (2010) Transfer Pricing Guidelines, at paragraph 1.8, p. 34. 85 OECD (2010) Proposed revisions of Chapters I-III of the Transfer Pricing Guidelines; or for the reasons

mentioned in paragraph 2.2. 86 See for example Calderón, J. (2007) p.8. 87 OECD (2010) Transfer Pricing Guidelines. 88 See for example Rossing, P.R. (2013) p. 176 or Eden, L (1998); Calderón (2007) p.12. 89 According to KPMG (2016) Global Transfer Pricing Review. 90 OECD (2015) Actions 8-10, Final Report, at p. 10.

14

3.3 Separate entity approach The OECD member countries have selected the separate entity approach as the most appropriate way to

achieve fair allocation results.91 Generally, this means that each enterprise within an MNE group is treated

as a separate entity. The objective of this approach is to identify the taxable entity that has affected

transactions, even if those transactions are undertaken within a single MNE.92

OECD countries believe that this approach is the most reasonable means for achieving the best result for

the allocation of tax bases between nations and minimizing the risk of double taxation.93 When applying

this approach, each group member is the subject of profit taxation that arises in that specific company. This

means that each company is treated as a separate taxable subject, irrespective of their function within an

integrated group. As a result of this, transactions undertaken between affiliated companies are also

recognized for tax purposes.94 This might seem an ideal situation in theory, but the risk of this approach is

that it creates an incentive to increase profit shifting, as an MNE may allocate profits to the countries where

its entities are located.95 This profit shifting is believed by the OECD to be corrected by the functioning of

the arm’s length principle.96

As MNEs have become more prominent in the global economy, and ever-more integrated, it is not that easy

to adequately use the separate entity approach anymore.97 In other words: members of an MNE group

cannot always be seen as separate economic actors in the 21st century. Financial accounting already ignores

affiliates and treats the MNE group as a single entity, in the sense that it only has to make one consolidated

financial statement. According to Vann, this is a strong argument that transfer pricing should also evolve

from a transactional to a more “whole of the enterprise approach”.98

From a tax perspective, it may also be argued that the separate entity approach may be losing its

significance. Hafkenscheid argues that countries apply an extensive set of rules already to circumvent the

unwanted side-effects of the separate entity approach.99 For example, controlled foreign company (CFC)

rules that require the parent company of a CFC to treat the income as fictitiously distributed to the parent,

91 OECD (2010) Transfer Pricing Guidelines, at p. 33. 92 De Wilde (2017) p.8. 93 See OECD (2010) Transfer Pricing Guidelines, at p. 18. 94 De Wilde (2017) p.8. 95 Escribana (2017) p. 253; Avi-Yonah (2009). 96 OECD Transfer Pricing Guidelines (2010) p. 18. 97 Radolovic (2012) p.30; Lohse et al. (2012) p.2. 98 Vann (2003) p.134. 99 Hafkenscheid (2017) p. 21.

15

or rules that subject the consolidation of corporate profits into the parent’s profit.100 These rules show that

the separate entity approach is not always the norm anymore for taxation purposes.

Moreover, the whole point of integration within an MNE is that the group is seen as a group instead of

separate entities. Not even MNEs regard each subsidiary as a separate entity that must trade with other

subsidiaries on an arm’s length basis. The very existence of integrated MNEs may be evidence that the

arm’s length principle does not reflect economic reality. This argument is based on the fact that MNEs try

to achieve economies of scale, something that cannot be achieved by separate economic actors.101

3.4 Comparability analysis Based on the separate entity approach, affiliated companies should act in the same manner as independent

companies do. Therefore, an affiliated company should be comparable to an independent entity. As

mentioned earlier in Paragraph 3.1, the comparability analysis finds its foundation in the OECD Model

Convention.102 This comparability analysis lies at the heart of the arm’s length principle.103 The ratio is that

independent enterprises will only enter into a transaction if they believe the transaction is not going to make

them worse off than their next best option.104

To analyze the comparison between affiliated and independent companies, two aspects are of major

importance. First, the commercial and financial relations between the affiliated companies within an MNE

group and the relevant economic circumstances have to be clearly defined. The second aspect is to find

comparable transactions between independent enterprises on the open market and to compare these

conditions and circumstances with the transactions of affiliated companies.105

3.4.1 Commercial and financial relations

Before comparing the transaction between affiliated companies with a comparable situation of unrelated

entities, it is vital to identify the relevant characteristics of the transaction. 106 The OECD lists five

comparability factors, which are seen as most important to accurately define the controlled transaction.

First, the contractual terms of the transactions have to be identified. A transaction is often formalized in a

100 See for example: the US Treasury Regulations under sec. 1501 Internal Revenue Code and arts. 15-15aj Dutch

Corporation Tax Act 1969. 101 Avi-Yonah (2007) p.24. 102 See OECD Model Convention On Income and Capital (2014) Paragraph 1 of Article 9: A comparison between

conditions (including but not only prices) made or imposed between associated enterprises and those which would

be made between independent enterprises, in order to determine whether the determination of profits is at arm’s

length. 103 OECD Transfer Pricing Guidelines (2010) paragraph 1.6 104 OECD Transfer Pricing Guidelines (2010) paragraph 1.38. 105 OECD Transfer Pricing Guidelines (2010) paragraph 1.33. 106 OECD (2010) Transfer Pricing Guidelines, at paragraph 1.36.

16

contract, covering the responsibilities, obligation, and rights of both parties.107 However, contracts alone

often do not provide all the relevant information for an adequate transfer pricing analysis. Additionally, the

OECD requires a functional analysis to be made. This analysis seeks to identify the significant activities

performed, the assets used in the process and the material risks assumed by the parties of the transaction.108

In practice, this analysis may be difficult or even impossible, especially when it comes to intellectual

property (IP). According to Picciotto, IP and risks are spread throughout the entity as a whole, and therefore

very hard to delineate to a certain entity.109 Moreover, BASF, a multinational chemical company responded

to this functional analysis approach of the OECD and concluded that it is often very hard indeed to identify

who ‘controls’ the relevant functions within an MNE. The chemical company says that decision-making is

multi-layered and can often not be delineated as such. Especially relating to intangible returns, BASF

believes the functional analysis should not be decisive.110

As can be concluded from the Guidelines, risk delineation forms a significant part of the functional

analysis.111 However, this may create new profit shifting possibilities instead of combatting tax avoidance.

By ‘simply’ shifting risks, profits may be shifted to low-tax jurisdictions.112 Therefore, risk allocation has

become an important aspect of tax planning from MNEs, especially because from an economic perspective,

the transfer of risk has little consequence for the MNE as a whole.113

As a third comparability factor, differences in the characteristics of the product or service transferred often

account for differences in the value of the product or service in the open market. It depends on the transfer

pricing method chosen by the MNE, whether or not this factor should be given much weight.114 Four,

economic circumstances may be relevant as arm’s length prices may differ across markets even when the

107 OECD (2010) Transfer Pricing Guidelines, at paragraph 1.42. 108 OECD (2010) Transfer Pricing Guidelines, at paragraph 1.52-1.58: The significant activities performed reflects

the actual physical contributions of each party. The assets used should contain the use of valuable intangibles,

financial assets, plants, and equipment etc. In an open market; the material risks assumed would usually be

compensated by an increase in expected return. 109 Picciotto (2015) p. 755. 110 BASF (2013) submission on the Revised Discussion Draft on Transfer Pricing Aspects of Intangibles. 111 OECD (2010) Transfer Pricing Guidelines, at p.239: An examination of the allocation of risks between associated

enterprises is an essential part of the functional analysis. 112 Devereux & Vella (2014) p.7. 113 Durst (2012). 114 OECD (2010) Transfer Pricing Guidelines, at paragraph 1.107The CUP-method heavily relies on the

comparability of characteristics. For the transactional profit methods, this comparability factor plays a less

significant role.

17

exact same property or service is transferred.115 And finally, the OECD requires business strategies to be

examined when defining the transaction and determining the level of comparability.116

3.4.2 Comparable transactions

Once a comparability analysis has been completed, the second step is to find adequate comparable

independent companies in the market. The search for comparable companies plays an important role to

guarantee that independent companies enjoy the same market, level of technology and levels of efficiency

that are similar to the ‘tested’ associated company. This information can often be obtained from commercial

databases.117 However, it might not always be easy to establish these fair market prices. For raw materials,

where prices are established by the global market, prices may easily be obtained from the commodities

exchange markets. Or if other highly comparable goods exist on the global market, comparable prices may

be fairly easily obtained. However, for many goods, prices are harder to obtain, as market prices for intra-

group transfers, due to their unique nature, rarely exist. 118 This comparability analysis therefore,

immediately poses a threat to intangible assets. The market-based comparability approach will most likely

only provide an adequate outcome if transactions are highly comparable. Developed, high-tech markets

usually have no or very little comparable transactions, and therefore comparability is a major issue.119

3.5 Transfer pricing methods Based on the comparability analysis, the OECD has described methods that can be used to establish whether

the conditions imposed between affiliated enterprises are consistent with the arm's length principle.120 I will

not go into too much detail regarding the various methods, as I regard it to be of minor importance for this

thesis, however, some understanding is fruitful.

In principle, the OECD requires an MNE to select the most appropriate transfer pricing method to the

circumstances of the case.121 In principle thus, the taxpayer seems to be free to choose a method of his

115 OECD (2010) Transfer Pricing Guidelines, at paragraph 1.110: Economic circumstances that may be relevant to

compare markets include: the geographical location, the level of competition, the size of the market, the levels of

supply and demand, and consumer purchasing power, etc. 116 OECD (2010) Transfer Pricing Guidelines, at paragraph 1.14: Business strategies would include: innovation, the

degree of diversification, risk aversion, duration of arrangements, etc. 117 OECD (2010) Transfer Pricing Guidelines, at p. 115: commercial databases have been developed by editors who

compile accounts filed by companies with the relevant administrative bodies and present them in an electronic

format suitable for searches and statistical analysis. Care must be exercised with respect to whether and how these

databases are used, given that they are compiled and presented for non-transfer pricing purposes. 118 Rossing (2013) p. 176. 119 Brauner (2008) p. 105; OECD, Actions 8-10 Final Reports, at paragraph 6.35: The OECD acknowledges this and

says that the use or transfer of intangibles may indeed challenge the comparability analysis. 120 OECD (2010) Transfer Pricing Guidelines, at p. 59. 121 OECD (2010) Transfer Pricing Guidelines, at paragraph 2.76.

18

liking. The methods prescribed by the OECD fall in either of two categories; traditional transaction methods

and transactional profit methods, both will be briefly described in the paragraphs below.

3.5.1 Traditional transaction methods

Traditional transaction methods can be regarded as the most direct means of establishing the at arm’s length

conditions of a certain transaction. These traditional methods were first implemented in the US tax

legislation in 1968.122 The traditional transaction methods are predominantly used for transactions that are

simpler of nature.123 Therefore, one may wonder how applicable the methods are for transactions involving

intangible assets, as they are complex per definition. The OECD admits that from a practical point of view

it is very hard to find a transaction between independent enterprises that is similar enough to a transaction

between affiliated companies.124 In practice, many times these methods are indeed rejected because they

cannot match one of the comparability criteria as established in the previous paragraphs.125

3.5.2 Transactional profit methods

If the traditional transaction methods are rejected, the transactional profit methods may be used instead. In

cases where each of the parties makes unique and valuable contributions in relation to the controlled

transaction, or where different group members are all related in highly integrated activities, a transactional

profit method may be more appropriate.

Another reason for adopting the profit method is the lack of available data on open-market prices, which is

required for a comparability analysis.126 As the most intellectual property is unique, reliable comparables

may not exist in the world.127 The transactional profit methods were originally given the name “basic arm’s

length return method”, which means that arm’s length principle does not only focus the prices of

transactions as such but that the principle may be applied through the examination of profits as well.128 This

means that the determination of an arm’s length price or result may be justified without direct reference to

the comparability analysis.129

122 Eden (2000) p.676. 123 Hughes & Nicholls (2011). 124 OECD (2010) Transfer Pricing Guidelines, at paragraph 2.15. 125 See for example Hughes & Nicholls (2010). 126 See Hughes & Nicholls (2010); and paragraph 3.4.1. 127 Rossing (2013) p. 176. 128 Mura et al. (2013). 129 Robillard (2015) pp. 447-448.

19

3.6 Criticism on the arm’s length principle I believe that no approach for transfer pricing can be perfect, as transfer pricing is not an exact science. 130

However, as may be concluded from the paragraphs above, applying the arm’s length principle seems to be

imperfect, and not easy to administer. Transfer pricing policies of MNEs are often based on judgments

made from by the MNE as well as the tax authority on how the arm’s length principle should be applied.131

One can also wonder about the name ‘arm’s length principle’ itself. The wording already constitutes

ambiguity, i.e. how long is an arm, really? Because of this ambiguity, tax authorities in different countries

may differ in regulatory standards and the way these standards should be interpreted and applied by MNEs.

However, the main objections to the arm’s length principle can be categorized into two groups. First, the

principle has been criticized for not reflecting economic reality and second, its feasibility has come under

great scrutiny.132 Regarding the economic reality, scholars argue that the arm’s length principle may not be

adequate anymore to determine the geographic location of a business activity and as a consequence.

Moreover, it is believed that the principle does not achieve anymore what it was designed to do, which is

to allocate taxing rights in a fair manner.133

3.6.1 Reflecting economic reality: comparability

It may be argued how adequately the arm’s length principle reflects the economic reality, especially in the

current economic environment, where intangibles are becoming an ever-more dominant value driver for

MNEs.134 First of all, the arm’s length principle is a legal fiction, as controlled transactions are deemed to

have been dealt with in accordance with the arm’s length principle.135 This means that the OECD depends

on a comparable transaction with independent entities. However, most of the intellectual property is unique,

and as such, reliable comparables may not exist in the world.136 Indeed, there may be a lack of third-party

comparables and a lack of comparability between the intangibles in question. Moreover, the legal ownership

of intangibles might be separated within the MNE and there is difficulty in isolating the impact of a

particular intangible on the MNE group’s income.137

Especially from 1975 onwards, reliable comparables were becoming harder to find in the market and

disputes between tax authorities and taxpayers concerning transfer pricing were becoming more common.

I believe that this increase in litigation may already constitute an indication that the arm’s length principle

130 OECD (2010)Transfer Pricing Guidelines p. 29. 131 Rossing, C. (2013) p. 176. 132 Schoeuri (2015) p. 698. 133 See for example: Avi-Yonah & Benshalom (2011); Fleming et al. (2014). 134 Adams (2015) p 91. 135 Schoueri (2015) p.697; Actions 8-10 Final Reports, at paragraph 2.88. 136 Rossing (2013) p. 176. 137 See Actions 8-10 Final Reports, at paragraph 6.33.

20

might not be practical anymore.138 As a consequence of the changed world-market, inadequate comparables

may be used for the application transfer pricing. Therefore, the arm’s length principle may actually lead to

very unrealistic results from an economic perspective. 139

There is a wide consensus among scholars that the fact that no independent party would never transfer

intangibles to an unrelated party without any payment. However, any attempt to find a proper royalty rate

may be very hard as no reliable comparables may exist.140 For example in the Bausch & Lomb transfer

pricing case concerning intangibles, the court judged a 5% royalty rate based on net sales too low. However,

the court was unable to find a “sufficiently similar transaction involving an unrelated party” and it

consequently constructed an arm’s length itself, arriving at a 20% royalty rate instead.141

3.6.2 Reflecting economic reality: integration

Moreover, affiliated companies and independent companies are very much different from each other by

definition.142 The reason is that MNEs may be created because they tend to generate greater returns by

combining entities than can be obtained from separate market transactions. The arm’s length principle does

not take into account these synergies effects of a group. I believe that a group of companies may pursue a

goal that does not directly benefit each member of the MNE separately but does benefit the MNE as a

whole.143 Therefore, I believe that an MNE group may not simply be divided into separate entities but has

to be seen as a whole.144

Hence, the arm’s length principle cannot define what the costs would be when unrelated parties would have

transacted with one another because the goal of setting up an MNE was to save costs by avoiding such

unrelated party transactions.145 The following example may illustrate things more clearly. It is very likely

that unrelated parties would have more distrust towards one another compared to affiliated companies and

as a consequence, independent parties would spend much more hours on meetings, or on their legal advisors

when drafting up important agreements. Therefore, there is an immediate profit when trade is conducted

amongst affiliated companies, something that the arm’s length principle doesn’t take into account. MNEs

138 Avi-Yonah (2007) p.10. 139 Avi-Yonah (2007) p.10. 140 Avi-Yonah (2007) p. 17 141 See Bausch & Lomb, Inc. v. Commissioner, 92 T.C. 525, 582 (1989). 142 Avi-Yonah & Benshalom (2011) p. 379. 143 Fleming et al. (2014) p.3. 144 See for example: Vann (2003) p.134. 145 Avi-Yonah & Benshalom (2011) p. 379.

21

especially flourish in those industries where the ability to integrate functions in different countries enables

them to reduce certain costs146 by taking advantage of synergy benefits.147

In the Guidelines, the OECD does try to take these synergies into account. However, the burden lies with

the taxpayer, as the OECD states that taxpayers would have to document these anticipated synergies when

applying the arm’s length principle.148 Then there remains another problem. When affiliates realize a

synergy gain from integration, such gain cannot be attributed to either of the affiliated companies in

isolation. Even if the synergy rents are well documented and the taxpayer is able to isolate the added value

of the synergy, it is theoretically still defensible to make any allocation of the surplus at will.149 Therefore,

I believe it to be not pragmatic, or even impossible to identify and determine an adequate key allocating

such synergy profits once these synergy profits are isolated.

3.6.3 Feasibility

Next to the belief that the arm’s length principle does not reflect economic reality, the feasibility of the

arm’s length principle may be questioned as well. For one there is the challenge of finding meaningful

comparable transactions amongst unrelated parties.150 Moreover, the process of finding comparable data

required for taxpayers, and the evaluation by tax authorities can be very burdensome, as may also be

concluded from Paragraphs 3.4 and 3.5.151 Scholars argue that very elaborate regulation and enforcement

measures have been implemented to counter tax avoidance, but those attempts seem to be futile against the

administrative burden it produces.152 This compliance burden results from the need to apply the arm’s

length principle on a factual, case-by-case basis and there is a lack of general rules.153 Therefore, when a

transfer pricing case goes to court, it is often very burdensome, time-consuming and expensive for all parties

involved; i.e. there is no clear winner, just losers.

For example, in 1993, Chevron delivered 1.3 million pages of documents to the IRS.154 This resulted in

huge enforcement costs for the tax authority. Therefore, even though the arm’s length principle actually

imposes a limited degree of restraint on income shifting and tax avoidance, it does so by putting a substantial

burden on both taxpayers and tax authorities. Moreover, the amount of restraint achieved is somewhat

146 These costs include research and development costs, transactions costs, information-obtaining costs, managerial

costs and finance costs. 147 Avi-Yonah & Benshalom (2011) p. 379. 148 OECD (2010) Transfer Pricing Guidelines, at paragraph 9.57. p.254. 149 Kane (2015) p.292. 150 Avi-Yonah & Benshalom (2011) p.377. 151 Schoueri (2015) p.705. 152 Devereux & Auerbach (2017). 153 Avi-Yonah (2007) p.25. 154 See Bureau of National Affairs, Tax Management Transfer Pricing Report, 135-36 (July 7, 1993).

22

modest.155 This cannot be the intention of policy makers, as I believe this is very much in contrast with the

beliefs of Adam Smith. This great economist namely said that the collection of taxes should involve the

lowest cost possible for the taxpayer.156 Therefore, I believe this administrative burden to be undesirable as

the application of the arm’s length principle may go beyond the understanding of most tax directors. This

can force taxpayers to use resources to employ economists or statisticians for example, instead of focusing

on their core business. Thus, the arm’s length principle has lost its feasibility in my opinion and poses a

threat the simplification function, which I believe to be one of the most important functions of transfer

pricing regulation.157

3.6.4 Opinion OECD

Despite the challenges formulated above, the OECD believes that applying the arm’s length principle can

in most cases, yield an appropriate allocation of returns, even for intangible property. And therefore, OECD

member countries continue to use the arm’s length principle to govern the evaluation of transfer pricing

between associated enterprises.158 The OECD considers that the experience from the application of the

arm’s length principle has become sufficiently broad and sophisticated to establish a substantial body of

common understanding. Furthermore, the OECD says that this experience should elaborate the arm’s length

principle further in order to refine and improve its functioning.159

As a consequence, the OECD says that other methods other than the arm’s length principle would not be

acceptable in theory, implementation, or in practice. It says that no legitimate or realistic alternative has yet

emerged.160 However, the application of the arm’s length principle is heavily debated by scholars, especially

regarding the inability to control tax-motivated transfer pricing with respect to the shifting of intangibles

within an MNE.161 Therefore, I believe that this principle needs to be reevaluated in the light of the 21st

century. In order to reevaluate the adequacy of the arm’s length principle, I derived a benchmark. In the

next paragraph, I will lay out the benchmark based on the strengths of the arm’s length principle on the one

hand and the criticism on the other hand.

3.7 The Benchmark I believe there are five very important aspects of a transfer pricing approach, which can be deduced from

this chapter and the previous.162 First and foremost, the measure must reflect the economic reality. We

155 Fleming et al. (2014) p.36. 156 Smith (2010) Chapter 2. 157 See paragraph 2.4.4. 158 OECD (2010) Transfer Pricing Guidelines, at p. 36, paragraph 1.14. 159 OECD (2010) Transfer Pricing Guidelines, at p. 36, paragraph 1.15. 160 OECD (2010) Transfer Pricing Guidelines, at p. 36, paragraph 1.15. 161 Fedusiv (2016) p. 483. 162 My criteria are not based on the criteria Auerbach et al. (2017) but it does show similarities with the authors’

criteria. See p.4. The authors test the destination based cash flow taxation against five criteria: (1) economic

23

currently live in a developed world where MNEs are becoming ever-more integrated. Moreover, the

economy has shifted from an in industrial era to a knowledge era.163 The fact that the value of intangible

assets has increased so much in the past decade, proves that we are indeed moving towards an era based on

knowledge. 164 Also, the world is dynamic and changing at such a rapid pace, which makes it quite

impossible to predict the future. Therefore, I believe it is imperative for transfer pricing regulation to be up-

to-date and to be able to cope with economic progress. Once transfer pricing fails to represent the economic

reality, a rule should be amended or replaced to once again reflect the economic reality.

Secondly, the administrative burden for taxpayers and enforcement costs for tax authorities should be

marginal. That tax compliance costs and the risk of double taxation have become a cause for great

concern.165 In order for compliance costs to be acceptable, I believe the rules should be clear and as simple

as possible.166 Complex rules will put a heavy burden on taxpayers as well as tax authorities, with high

costs as a result for both parties. 167 While it is understandable that especially in times of economic

recession, transfer pricing regulation may be tightened, a major drawback of this stricter regulation may be

that it involves high administrative costs for tax authorities and taxpayers. Therefore, the effectiveness of

such administrative burden depends on the level of income shifting it prevents.168 Once a measure creates

disproportionate administrative burdens, I believe it distorts the business decisions as businesses would

have to relocate their resources towards tax compliance. Based hereon, I believe that administrative burdens

should be kept at a low level in order to affect business decisions as little as possible.169

Three, the measure should result in a fair allocation of taxing rights between countries. Tax authorities in

many countries are modernizing their legislation in order to safeguard the collection of a fair amount of tax

in their jurisdiction.170 However, the fiscal sovereignty which states need to levy tax is limited to economic

activities that take place within their territory.171 Therefore, transfer pricing mismatches cannot be solved

unilaterally. As transfer pricing is a purely international issue, transfer pricing has to be able to allocate

taxing rights between states. 172 Theoretically, this could be achieved when nations would mutually

efficiency, (2) robustness to tax avoidance and evasion, (3) ease of administration, (4) fairness, (5) stability. Note,

however, that my criteria are more focused on transfer pricing. 163 Adams (2015) p. 87. 164 Adams (2015) p 91. 165 Schreiber & Fell (2017) p. 11. 166 See paragraph 2.4.4. 167 Avi-Yonah & Benshalom (2011) p.379. 168 Lohse & Riedel (2013) p. 2. 169 This is in line with the beliefs of Adam Smith; De Wilde (2015) p.12. 170 Elliott and Emmanuel (2000) p. 216; According to KPMG (2016): By 2016, over 85 countries implemented

transfer pricing regulation. 171 De Wilde (2015) p.5. 172 Vogel (1977).

24

coordinate their tax systems.173 Viewed in this context, I believe transfer pricing rules are necessary to help

allocate profits to jurisdictions, especially as the tax sovereignty of states is limited to the boundaries of its

own territory.

Four, the approach should be resilient to tax avoidance. In the past, abusive tax practices and the risk of

base erosion and profit shifting was virtually absent.174 However, in the 21st century, transfer pricing

manipulation has been said to be one of the easiest ways to avoid taxation and is, therefore, one of the most

common techniques of tax avoidance.175 Especially in this knowledge era, income shifting may be fairly