teekay shipping shipping jefferies tanker ... crude oil tankers product carriers specialized ice...

TRANSCRIPT

www.teekay.com

T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ®

SM

Jefferies Tanker Conference

Teekay Shipping

Jefferies Tanker Conference

September 15, 2005

Teekay Shipping Teekay Shipping

Jefferies Tanker Jefferies Tanker ConferenceConference

September 15, 2005September 15, 2005

TEEKAY SHIPPING

2 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

Forward Looking StatementsForward Looking StatementsThis presentation contains forward-looking statements (as defined in Section 21E of the Securities Exchange Act of 1934, as amended) which reflect management’s current views with respect to certain future events and performance, including statements regarding the Company’s future growth prospects; tanker market fundamentals, including the balance of supply and demand in the tanker market and sources of incremental oil production, and spot tanker charter rates; LNG shipping demand fundamentals; and the valuation of the Company. The following factors are among those that could cause actual results to differ materially from the forward-looking statements, which involve risks and uncertainties, and that should be considered in evaluating any such statement: changes in production of or demand for oil, petroleum products and LNG, either generally or in particular regions; greater or less than anticipated levels of tanker newbuilding orders or greater or less than anticipated rates of tanker scrapping; changes in trading patterns significantly affecting overall tanker tonnage requirements; changes in applicable industry laws and regulations and the timing of implementation of new laws and regulations; changes in the typical seasonal variations in tanker charter rates; changes in the offshore production of oil; the potential for early termination of long-term contracts and inability of the Company to renew or replace long-term contracts; shipyard production delays; and other factors discussed in Teekay’s filings from time to time with the SEC, including its Report on Form 20-F for the fiscal year ended December 31, 2004. The Company expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in theCompany’s expectations with respect thereto or any change in events, conditions or circumstances on which any such statement is based.

TEEKAY SHIPPING

3 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

Investment HighlightsInvestment Highlights

Conventional crude oil tankersLiquefied natural gas carriersRefined product tankersShuttle TankersFloating Storage Units

Teekay is the only publicly traded shipping company with the following complement of assets:

Diverse Portfolio of Assets

Large spot in-chartered fleet provides additional operating leverage while minimizing capital employed

Large owned spot tanker fleet provides significant operating leverage

Unique Business MixFixed-rate contract portfolio provides for positive earnings in nearly any tanker

cycle

Teekay’s Business Model Appeals to CustomersTeekay is the only publicly traded shipping company that moves the three most

important commodities:Liquefied Natural Gas Crude Oil Refined Products

TEEKAY SHIPPING

4 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

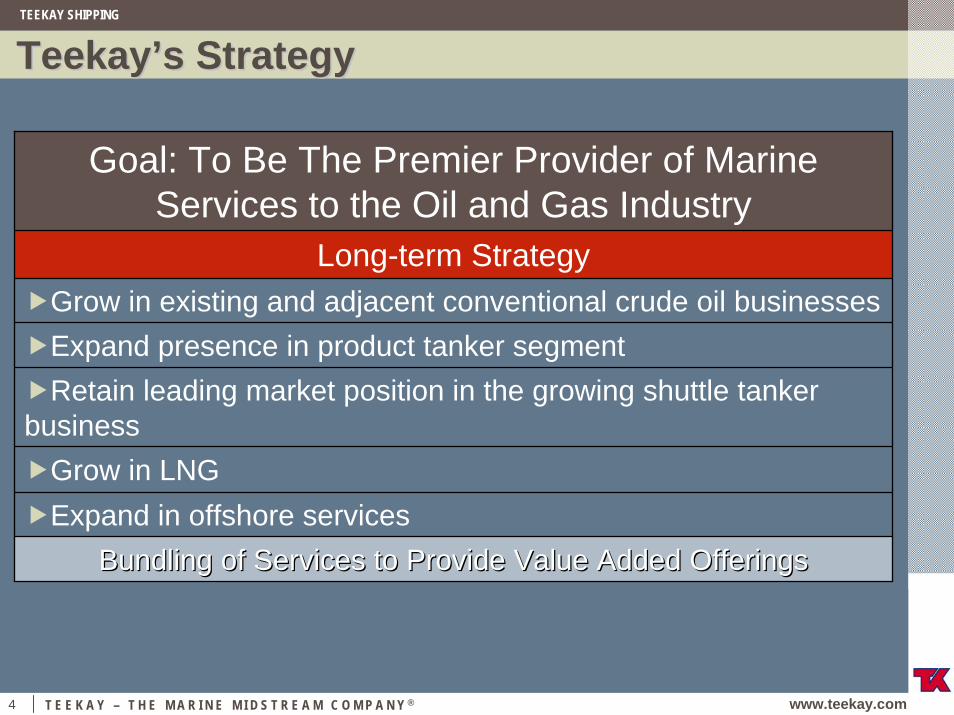

TeekayTeekay’’s Strategys Strategy

Goal: To Be The Premier Provider of Marine Services to the Oil and Gas Industry

Long-term StrategyGrow in existing and adjacent conventional crude oil businessesExpand presence in product tanker segmentRetain leading market position in the growing shuttle tanker

businessGrow in LNGExpand in offshore services

Bundling of Services to Provide Value Added OfferingsBundling of Services to Provide Value Added Offerings

TEEKAY SHIPPING

5 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

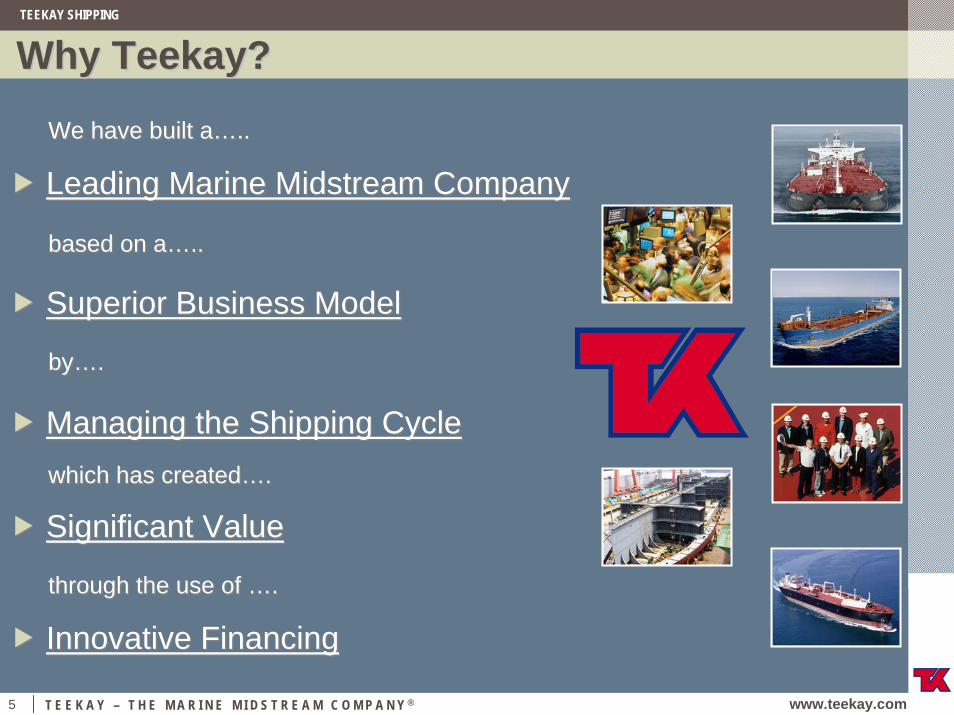

Why Teekay?Why Teekay?

We have built a…..We have built a…..

Leading Marine Midstream CompanyLeading Marine Midstream Company

based on a…..based on a…..

Superior Business ModelSuperior Business Model

by….by….

Managing the Shipping CycleManaging the Shipping Cyclewhich has created….which has created….

Significant ValueSignificant Value

through the use of ….through the use of ….

Innovative FinancingInnovative Financing

TEEKAY SHIPPING

6 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

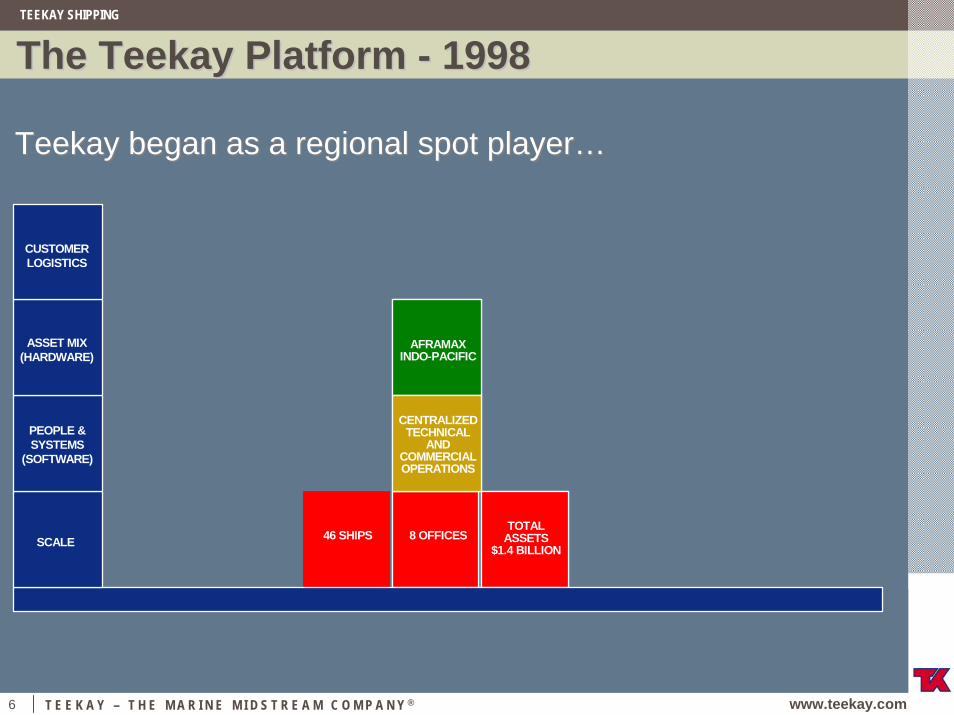

The Teekay Platform The Teekay Platform -- 19981998

Teekay began as a regional spot player…Teekay began as a regional spot player…

TOTAL ASSETS

$1.4 BILLION46 SHIPS 8 OFFICES

TOTAL ASSETS

$1.4 BILLION46 SHIPS 8 OFFICESSCALE

PEOPLE & SYSTEMS

(SOFTWARE)

ASSET MIX (HARDWARE)

CUSTOMER LOGISTICS

AFRAMAX INDO-PACIFIC

AFRAMAX INDO-PACIFIC

CENTRALIZED TECHNICAL

AND COMMERCIAL OPERATIONS

CENTRALIZED TECHNICAL

AND COMMERCIAL OPERATIONS

TEEKAY SHIPPING

7 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

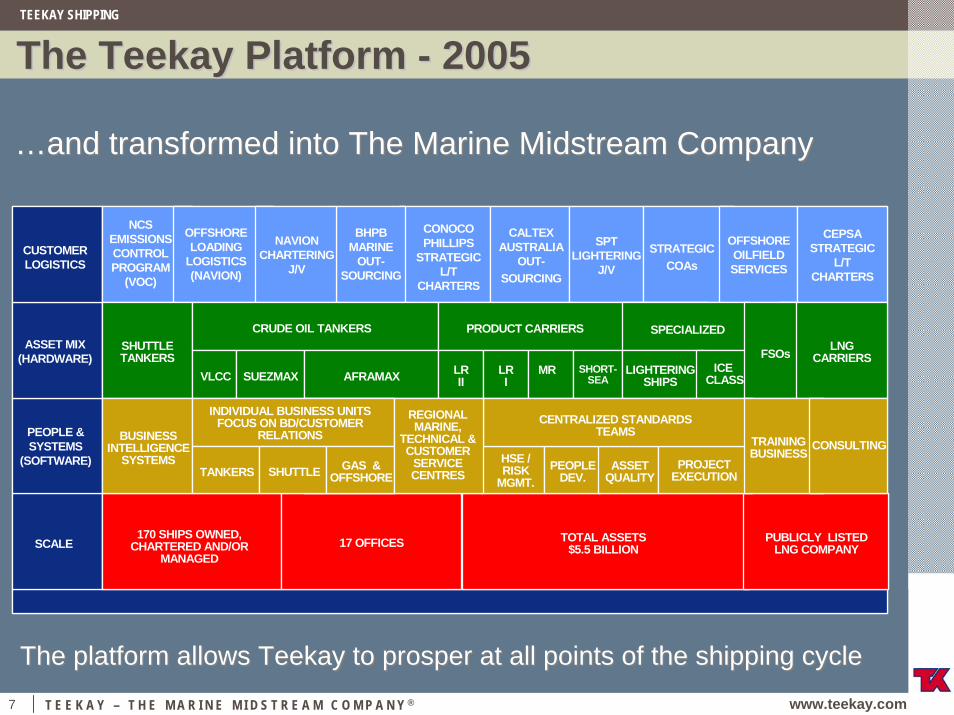

The Teekay Platform The Teekay Platform -- 20052005

…and transformed into The Marine Midstream Company…and transformed into The Marine Midstream Company

SCALE

PEOPLE & SYSTEMS

(SOFTWARE)

ASSET MIX (HARDWARE)

CUSTOMER LOGISTICS

SCALE

PEOPLE & SYSTEMS

(SOFTWARE)

ASSET MIX (HARDWARE)

CUSTOMER LOGISTICS

17 OFFICES170 SHIPS OWNED,

CHARTERED AND/ORMANAGED

PUBLICLY LISTED LNG COMPANY

TOTAL ASSETS$5.5 BILLION17 OFFICES

170 SHIPS OWNED, CHARTERED AND/OR

MANAGED

PUBLICLY LISTED LNG COMPANY

TOTAL ASSETS$5.5 BILLION

NCSEMISSIONS CONTROL PROGRAM

(VOC)

OFFSHORE LOADING

LOGISTICS (NAVION)

NAVION CHARTERING

J/V

BHPB MARINE

OUT-SOURCING

CONOCO PHILLIPS

STRATEGIC L/T

CHARTERS

CALTEX AUSTRALIA

OUT-SOURCING

SPT LIGHTERING

J/V

OFFSHORE OILFIELD SERVICES

CEPSA STRATEGIC

L/T CHARTERS

STRATEGICCOAs

NCSEMISSIONS CONTROL PROGRAM

(VOC)

OFFSHORE LOADING

LOGISTICS (NAVION)

NAVION CHARTERING

J/V

BHPB MARINE

OUT-SOURCING

CONOCO PHILLIPS

STRATEGIC L/T

CHARTERS

CALTEX AUSTRALIA

OUT-SOURCING

SPT LIGHTERING

J/V

OFFSHORE OILFIELD SERVICES

CEPSA STRATEGIC

L/T CHARTERS

STRATEGICCOAs

VLCC SUEZMAX

FSOsSHUTTLETANKERS

AFRAMAX

CRUDE OIL TANKERS PRODUCT CARRIERS SPECIALIZED

ICECLASS

LNG CARRIERS

LRII

LRI

MR SHORT-SEA

LIGHTERING SHIPSVLCC SUEZMAX

FSOsSHUTTLETANKERS

AFRAMAX

CRUDE OIL TANKERS PRODUCT CARRIERS SPECIALIZED

ICECLASS

LNG CARRIERS

LRII

LRI

MR SHORT-SEA

LIGHTERING SHIPS

BUSINESSINTELLIGENCE

SYSTEMS

INDIVIDUAL BUSINESS UNITS FOCUS ON BD/CUSTOMER

RELATIONS

TANKERS SHUTTLE GAS & OFFSHORE

REGIONAL MARINE,

TECHNICAL & CUSTOMER

SERVICE CENTRES

CENTRALIZED STANDARDS TEAMS

HSE /RISK

MGMT.PEOPLE

DEV.ASSET

QUALITYPROJECT

EXECUTION

TRAINING BUSINESS

CONSULTINGBUSINESS

INTELLIGENCESYSTEMS

INDIVIDUAL BUSINESS UNITS FOCUS ON BD/CUSTOMER

RELATIONS

TANKERS SHUTTLE GAS & OFFSHORE

REGIONAL MARINE,

TECHNICAL & CUSTOMER

SERVICE CENTRES

CENTRALIZED STANDARDS TEAMS

HSE /RISK

MGMT.PEOPLE

DEV.ASSET

QUALITYPROJECT

EXECUTION

TRAINING BUSINESS

CONSULTING

The platform allows Teekay to prosper at all points of the shipping cycleThe platform allows Teekay to prosper at all points of the shipping cycle

TEEKAY SHIPPING

8 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

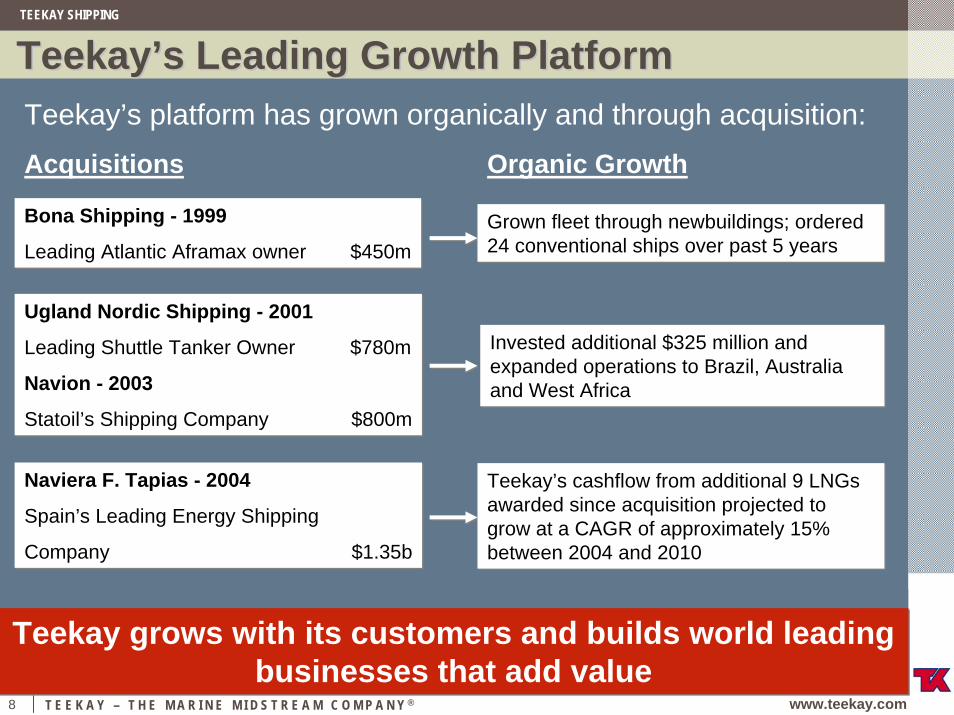

TeekayTeekay’’s Leading Growth Platforms Leading Growth PlatformTeekay’s platform has grown organically and through acquisition:Acquisitions Organic Growth

Bona Shipping - 1999

Leading Atlantic Aframax owner $450m

Bona Shipping - 1999

Leading Atlantic Aframax owner $450m

Ugland Nordic Shipping - 2001

Leading Shuttle Tanker Owner $780m

Navion - 2003

Statoil’s Shipping Company $800m

Ugland Nordic Shipping - 2001

Leading Shuttle Tanker Owner $780m

Navion - 2003

Statoil’s Shipping Company $800m

Grown fleet through newbuildings; ordered 24 conventional ships over past 5 yearsGrown fleet through newbuildings; ordered 24 conventional ships over past 5 years

Invested additional $325 million and expanded operations to Brazil, Australia and West Africa

Invested additional $325 million and expanded operations to Brazil, Australia and West Africa

Naviera F. Tapias - 2004

Spain’s Leading Energy Shipping

Company $1.35b

Naviera F. Tapias - 2004

Spain’s Leading Energy Shipping

Company $1.35b

Teekay’s cashflow from additional 9 LNGsawarded since acquisition projected to grow at a CAGR of approximately 15% between 2004 and 2010

Teekay’s cashflow from additional 9 LNGsawarded since acquisition projected to grow at a CAGR of approximately 15% between 2004 and 2010

Teekay grows with its customers and builds world leading businesses that add value

Teekay grows with its customers and builds world leading businesses that add value

TEEKAY SHIPPING

9 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

SHUTTLE TANKER

OFFSHORE DRILLINGFSO

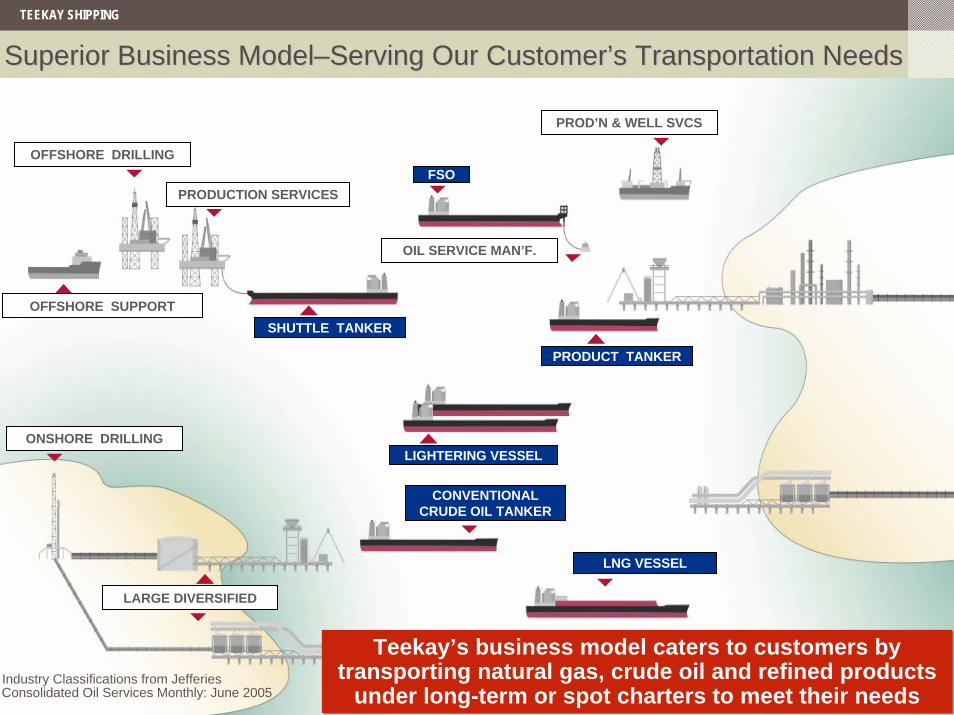

Superior Business ModelSuperior Business Model––Serving Our CustomerServing Our Customer’’s Transportation Needss Transportation Needs

OFFSHORE SUPPORT

PRODUCTION SERVICES

ONSHORE DRILLING

LARGE DIVERSIFIED

PROD’N & WELL SVCS

OIL SERVICE MAN’F.

LIGHTERING VESSEL

PRODUCT TANKER

CONVENTIONAL CRUDE OIL TANKER

LNG VESSEL

Industry Classifications from Jefferies Consolidated Oil Services Monthly: June 2005

Teekay’s business model caters to customers by transporting natural gas, crude oil and refined products

under long-term or spot charters to meet their needs

Teekay’s business model caters to customers by transporting natural gas, crude oil and refined products

under long-term or spot charters to meet their needs

TEEKAY SHIPPING

10 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

TeekayTeekay’’ss Spot Tanker BusinessSpot Tanker BusinessLargest spot operator of medium-sized tankers

Shipped close to 1.5 billion barrels in 2004

Unique global organization

Maintaining high in-charter activity

0

20

40

60

Teeka

y

MISCAfra

max In

t'lGen

marNovo

ship

# of

Afr

amax

es

existing vessels newbuildings

Higher operating leverage than typical shipowner

Portfolio of strategic contracts with blue chip customer base

High Capacity Utilization + Scale = Unique Competitive Advantage

High Capacity Utilization + Scale = Unique Competitive Advantage

TEEKAY SHIPPING

11 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

TeekayTeekay’’ss Spot Tanker BusinessSpot Tanker Business

Strong Platform for Future GrowthStrong Platform for Future GrowthListen to the customer –replicate mid-size tanker franchise in other segments

Expand into new areas of the customers’ logistic chain

Able to consolidate or grow organically using large platform of conventional tankers

Growth not dependent on owning the assets

TEEKAY SHIPPING

12 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

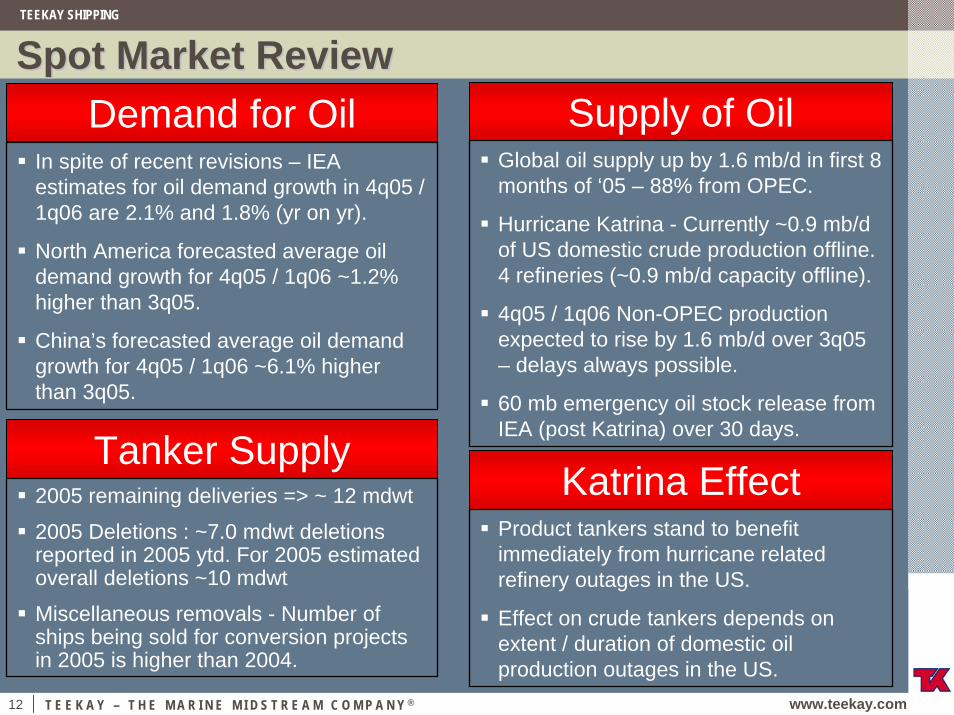

Spot Market ReviewSpot Market ReviewDemand for Oil Supply of Oil

Tanker SupplyKatrina Effect

In spite of recent revisions – IEA estimates for oil demand growth in 4q05 / 1q06 are 2.1% and 1.8% (yr on yr).

North America forecasted average oil demand growth for 4q05 / 1q06 ~1.2% higher than 3q05.

China’s forecasted average oil demand growth for 4q05 / 1q06 ~6.1% higher than 3q05.

Global oil supply up by 1.6 mb/d in first 8 months of ‘05 – 88% from OPEC.

Hurricane Katrina - Currently ~0.9 mb/d of US domestic crude production offline. 4 refineries (~0.9 mb/d capacity offline).

4q05 / 1q06 Non-OPEC production expected to rise by 1.6 mb/d over 3q05 – delays always possible.

60 mb emergency oil stock release from IEA (post Katrina) over 30 days.

Product tankers stand to benefit immediately from hurricane related refinery outages in the US.

Effect on crude tankers depends on extent / duration of domestic oil production outages in the US.

2005 remaining deliveries => ~ 12 mdwt

2005 Deletions : ~7.0 mdwt deletions reported in 2005 ytd. For 2005 estimated overall deletions ~10 mdwt

Miscellaneous removals - Number of ships being sold for conversion projects in 2005 is higher than 2004.

TEEKAY SHIPPING

13 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

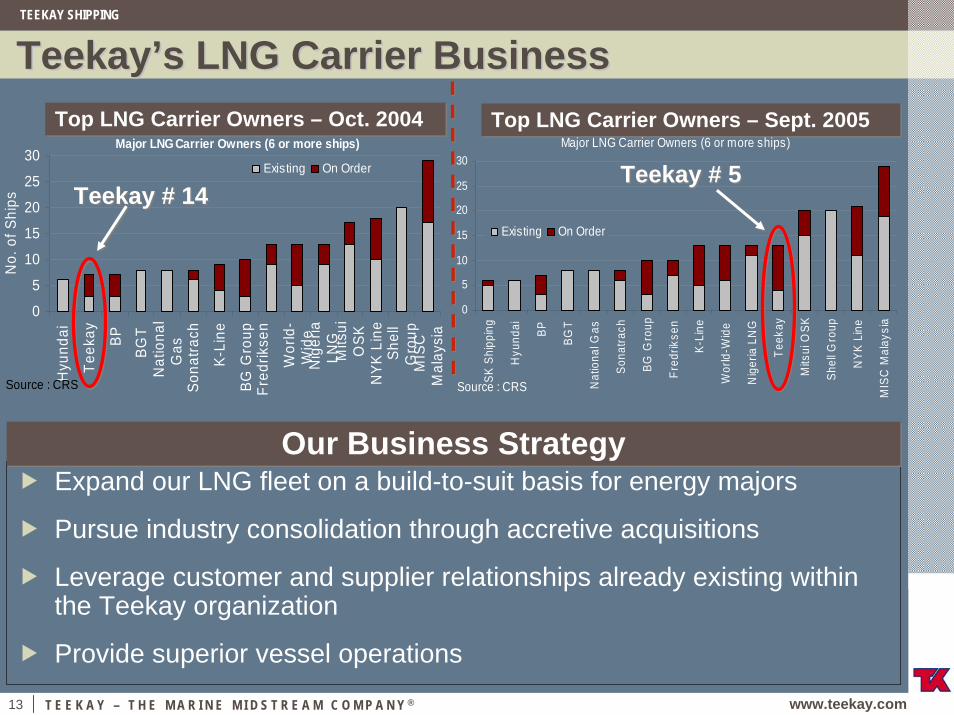

TeekayTeekay’’ss LNG Carrier BusinessLNG Carrier Business

Major LNG Carrier Owners (6 or more ships)

0

5

10

15

20

25

30

Hyu

ndai

Teek

ay BP

BGT

Nat

iona

lG

as

Sona

trach

K-Li

ne

BG G

roup

Fred

rikse

n

Wor

ld-

Wid

e N

iger

iaLN

G

Mits

uiO

SKN

YK L

ine

Shel

lG

roup

MIS

CM

alay

sia

Source : CRS

No.

of S

hips

Existing On Order

Top LNG Carrier Owners – Oct. 2004Top LNG Carrier Owners – Oct. 2004 Top LNG Carrier Owners – Sept. 2005Top LNG Carrier Owners – Sept. 2005

Teekay # 14Teekay # 14

Major LNG Carrier Owners (6 or more ships)

0

5

10

15

20

25

30

SK S

hipp

ing

Hyu

ndai

BP

BGT

Nat

iona

l Gas

Sona

trach

BG G

roup

Fred

rikse

n

K-Li

ne

Wor

ld-W

ide

Nig

eria

LN

G

Teek

ay

Mits

ui O

SK

Shel

l Gro

up

NYK

Lin

e

MIS

C M

alay

sia

Source : CRS

Existing On Order

Teekay # 5Teekay # 5

Expand our LNG fleet on a build-to-suit basis for energy majors

Pursue industry consolidation through accretive acquisitions

Leverage customer and supplier relationships already existing within the Teekay organization

Provide superior vessel operations

Our Business StrategyOur Business Strategy

TEEKAY SHIPPING

14 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

Delivery Schedule of Delivery Schedule of NewbuildingNewbuilding LNG CarriersLNG Carriers

RASGAS HULL #2238

RASGAS HULL #1643

RASGAS HULL #1644

RASGAS HULL #1645

RASGAS HULL #1646

Tangguh HULL #1780

Tangguh HULL #S298

RASGAS HULL #2239

RASGAS HULL #2240

2006 2007 2008LNG CARRIER FLEETSept.2005 2009

Ship DeliveryShip Delivery

Teekay’s share of the LNG orderbook ~$930 million Teekay’s share of the LNG orderbook ~$930 million

TEEKAY SHIPPING

15 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

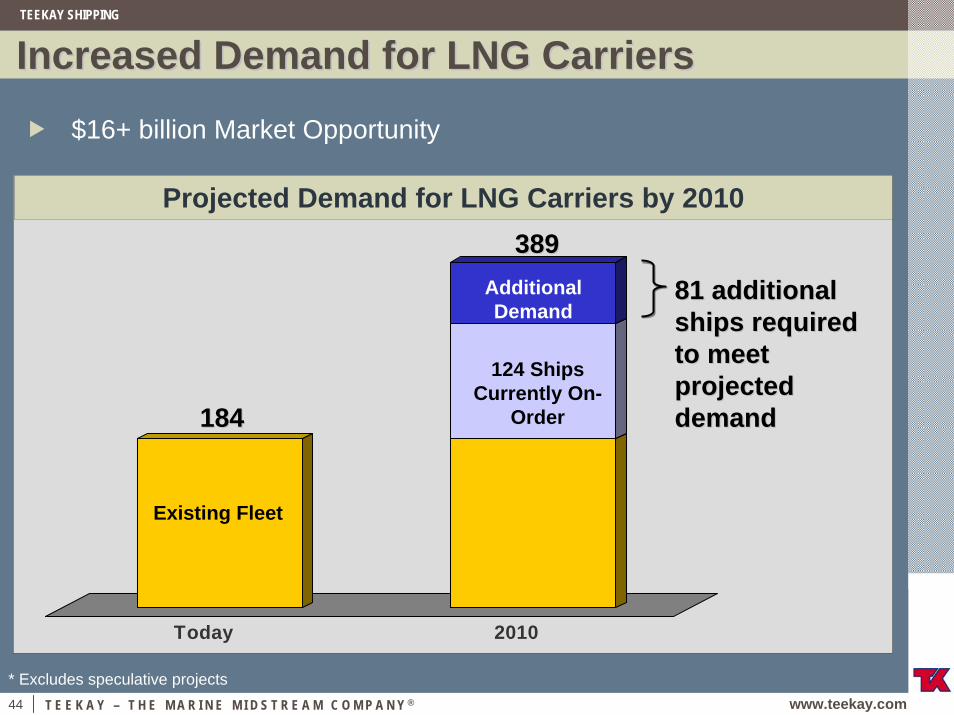

Increased Demand for LNG CarriersIncreased Demand for LNG Carriers

Today 2010

$16+ billion Market Opportunity

Projected Demand for LNG Carriers by 2010

Existing Fleet

124 Ships Currently On-

Order

81* additional 81* additional ships required ships required to meet to meet projected projected demanddemand

Additional Demand

389 389

184184

* Excludes speculative projects, Company Estimates

TEEKAY SHIPPING

16 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

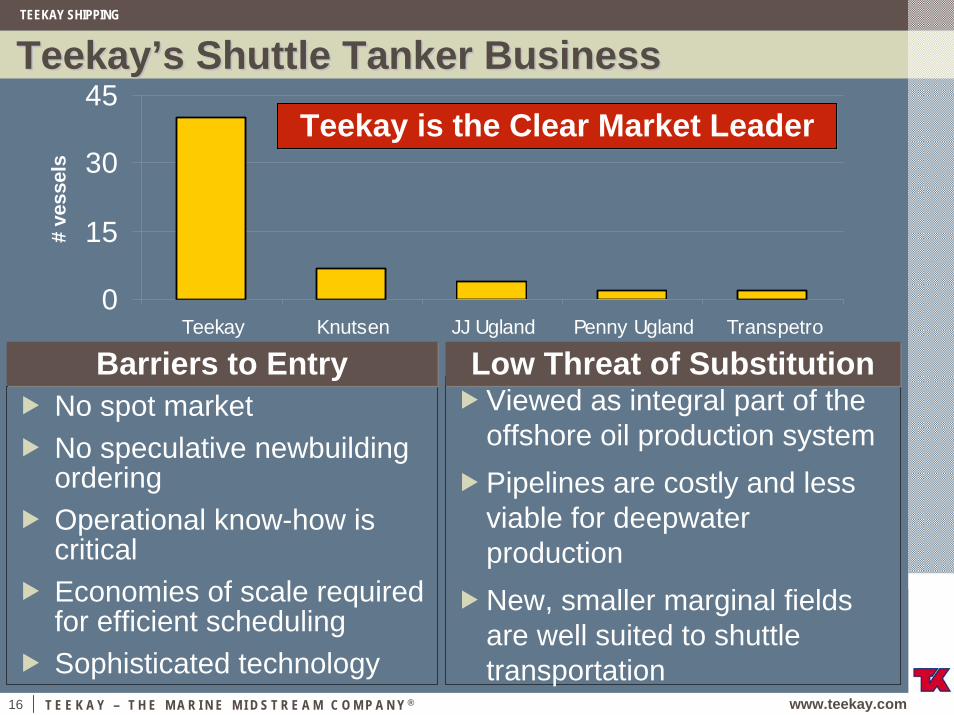

TeekayTeekay’’ss Shuttle Tanker BusinessShuttle Tanker Business

No spot market No speculative newbuildingorderingOperational know-how is criticalEconomies of scale required for efficient schedulingSophisticated technology

Barriers to EntryBarriers to EntryViewed as integral part of the offshore oil production systemPipelines are costly and less viable for deepwater production New, smaller marginal fields are well suited to shuttle transportation

Low Threat of SubstitutionLow Threat of Substitution

0

15

30

45

Teekay Knutsen JJ Ugland Penny Ugland Transpetro

# ve

ssel

s

Teekay is the Clear Market LeaderTeekay is the Clear Market Leader

TEEKAY SHIPPING

17 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

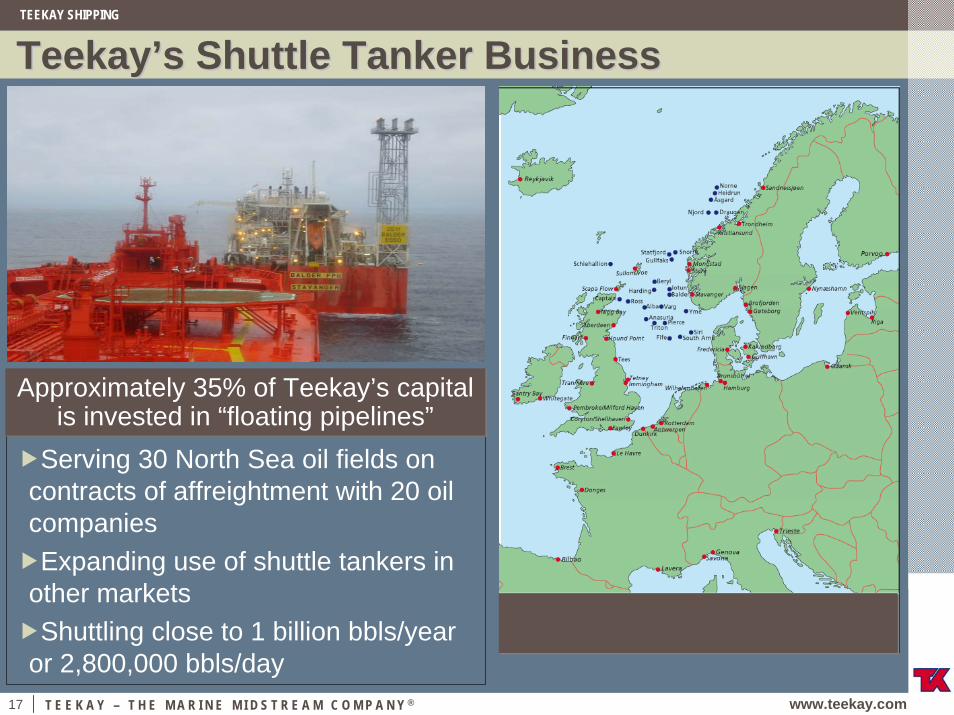

TeekayTeekay’’ss Shuttle Tanker BusinessShuttle Tanker Business

Serving 30 North Sea oil fields on contracts of affreightment with 20 oil companiesExpanding use of shuttle tankers in

other marketsShuttling close to 1 billion bbls/year

or 2,800,000 bbls/day

Approximately 35% of Teekay’s capital is invested in “floating pipelines”

Approximately 35% of Teekay’s capital is invested in “floating pipelines”

TEEKAY SHIPPING

18 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

TeekayTeekay’’ss Shuttle Tanker SegmentShuttle Tanker Segment

Rapid growth in deepwater explorationContinued development of core North Sea marketUpside in Brazil marketOther opportunities:

East Coast of CanadaGulf of MexicoWest AfricaAustralia

Significant Growth Potential in Offshore Oil……Significant Growth Potential in Offshore Oil……

……especially at $60+ oil……especially at $60+ oil

19 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

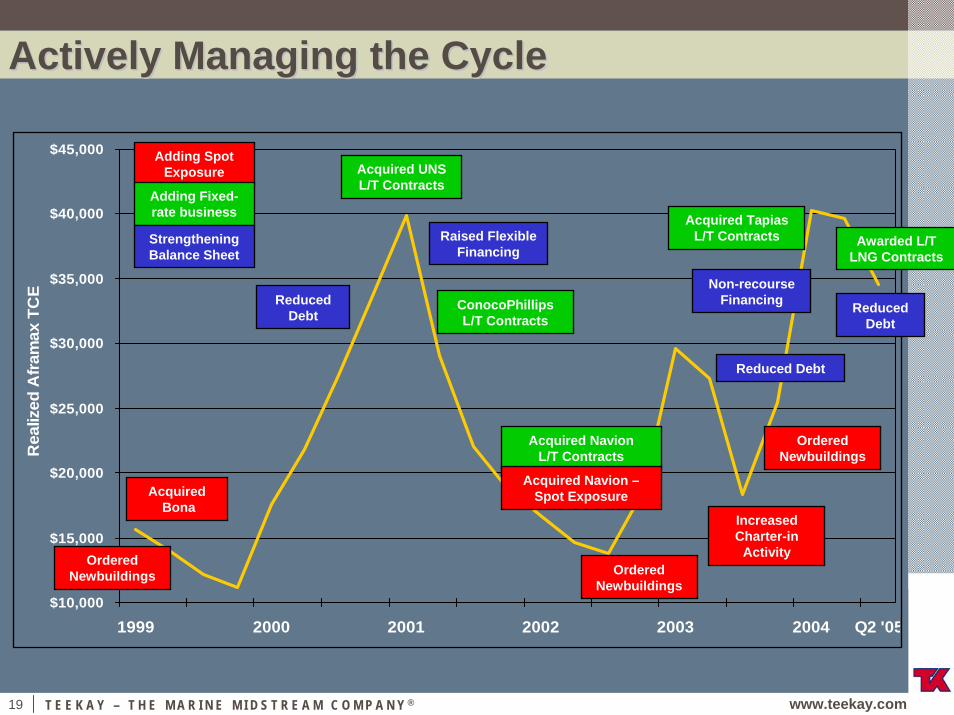

Actively Managing the CycleActively Managing the Cycle

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

1999 2000 2001 2002 2003 2004 Q2 '05

Rea

lized

Afra

max

TC

E

Acquired Navion L/T Contracts

Acquired UNS L/T Contracts

Raised Flexible Financing

Reduced Debt

Ordered Newbuildings

AcquiredBona

Ordered Newbuildings

Acquired Navion –Spot Exposure

ConocoPhillips L/T Contracts

Reduced Debt

Ordered Newbuildings

Acquired Tapias L/T Contracts

Adding Spot Exposure

Adding Fixed-rate business

Strengthening Balance Sheet

Non-recourse Financing

Increased Charter-in

Activity

Awarded L/T LNG Contracts

Reduced Debt

TEEKAY SHIPPING

20 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

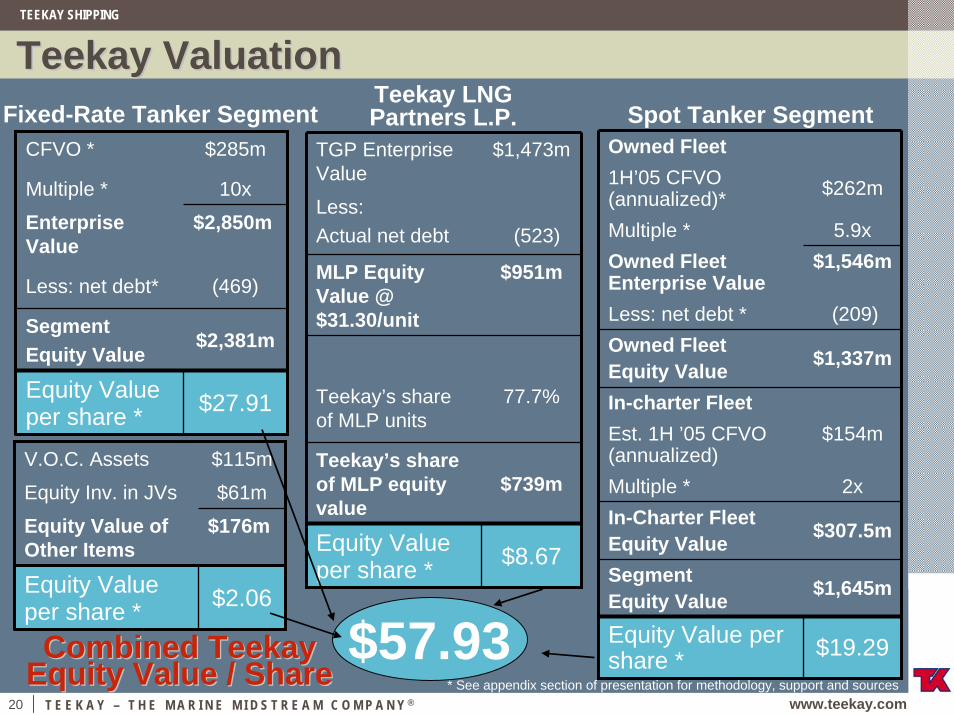

Teekay ValuationTeekay Valuation

CFVO * $285m

Multiple * 10x

Enterprise Value

$2,850m

Less: net debt* (469)

Segment Equity Value

$2,381m

Equity Value per share * $27.91

TGP Enterprise Value

$1,473m

Less: Actual net debt (523)

MLP Equity Value @ $31.30/unit

$951m

Teekay’s share of MLP units

77.7%

Teekay’s share of MLP equity value

$739m

Equity Value per share * $8.67

Teekay LNG Partners L.P.Fixed-Rate Tanker Segment

Owned Fleet1H’05 CFVO (annualized)* $262m

Multiple * 5.9xOwned Fleet Enterprise Value

$1,546m

Less: net debt * (209)Owned Fleet Equity Value $1,337m

In-charter FleetEst. 1H ’05 CFVO (annualized)

$154m

Multiple * 2xIn-Charter FleetEquity Value $307.5m

Segment Equity Value $1,645m

Equity Value per share * $19.29

Spot Tanker Segment

$57.93Combined Teekay Combined Teekay Equity Value / ShareEquity Value / Share * See appendix section of presentation for methodology, support and sources

V.O.C. Assets $115m

Equity Inv. in JVs $61m

Equity Value of Other Items

$176m

Equity Value per share * $2.06

TEEKAY SHIPPING

21 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

Financial HighlightsFinancial HighlightsNet income of $383m or $4.42 per share in 1H 2005

Reduced leverage from 42% to 34% in last 6 months

~ $300m or 6.9 million shares repurchased since Nov. ’04 => present authorization for additional $305m or 6.8 million shares

Dividend increased three times in past three years

When completed, over 16% of o/s

shares repurchased since Nov. ‘04

When completed, over 16% of o/s

shares repurchased since Nov. ‘04

Increased 93% in three years

Increased 93% in three years

ROE of ~20%ROE of ~20%

Near low end of target range

Near low end of target range

TEEKAY SHIPPING

22 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$10,0

00

$15,0

00

$20,0

00

$25,0

00

$30,0

00

$35,0

00

$40,0

00

$45,0

00

$50,0

00

$55,0

00

$60,0

00

Aframax Rates ($ per day)

Qua

rter

ly E

arni

ngs

Per S

hare

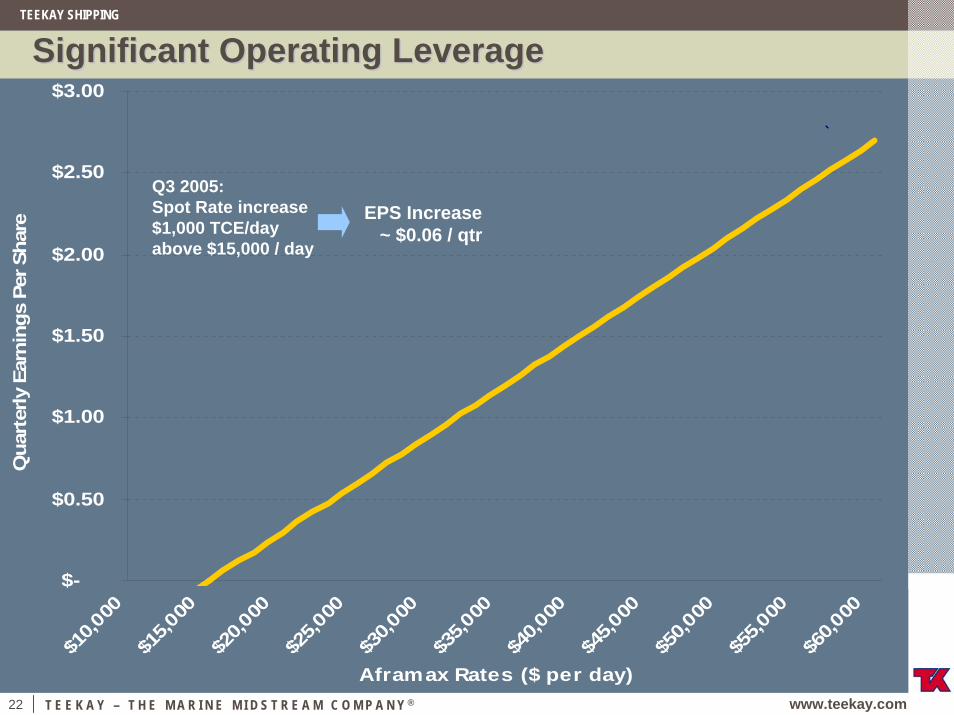

Significant Operating LeverageSignificant Operating Leverage

Q3 2005:Spot Rate increase $1,000 TCE/day above $15,000 / day

EPS Increase~ $0.06 / qtr

TEEKAY SHIPPING

23 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

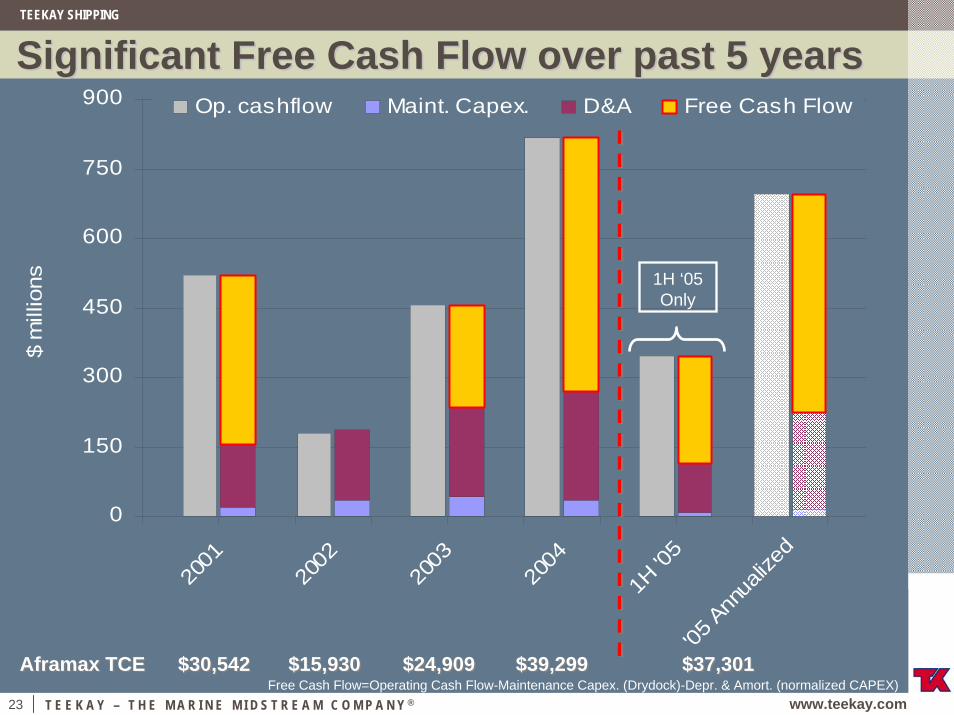

Significant Free Cash Flow over past 5 yearsSignificant Free Cash Flow over past 5 years

0

150

300

450

600

750

900

2001

2002

2003

2004

1H '0

5'05

Ann

ualiz

ed

$ m

illio

ns

Op. cashflow Maint. Capex. D&A Free Cash Flow

1H ‘05 Only

Aframax TCEAframax TCE $30,542$30,542 $15,930$15,930 $24,909$24,909 $39,299$39,299 $37,301$37,301Free Cash Flow=Operating Cash Flow-Maintenance Capex. (Drydock)-Depr. & Amort. (normalized CAPEX)

TEEKAY SHIPPING

24 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

Investment HighlightsInvestment Highlights

Teekay’s Business Model Appeals to Customers

Diverse Portfolio of Assets

Unique Business Mix

www.teekay.com

T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ®

SM

AppendixAppendixTanker Market Slides

Teekay LNG Partners L.P.

Sum-of-parts Valuation Support

Fleet Breakdown

Non-GAAP Reconciliation

TEEKAY SHIPPING

26 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

Crude Tanker Spot MarketCrude Tanker Spot Market

0

25,000

50,000

75,000

100,000

125,000

150,000

175,0001q

99

3q99

1q00

3q00

1q01

3q01

1q02

3q02

1q03

3q03

1q04

3q04

1q05

3q05

ytd

Source: CRS

US$

per

Day

Aframax Suezmax VLCC

TEEKAY SHIPPING

27 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

Product Tanker Spot MarketProduct Tanker Spot Market

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,0001q

99

3q99

1q00

3q00

1q01

3q01

1q02

3q02

1q03

3q03

1q04

3q04

1q05

3q05

ytd

Source: CRS

US

$ pe

r Day

LR2 LR1 MR

TEEKAY SHIPPING

28 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

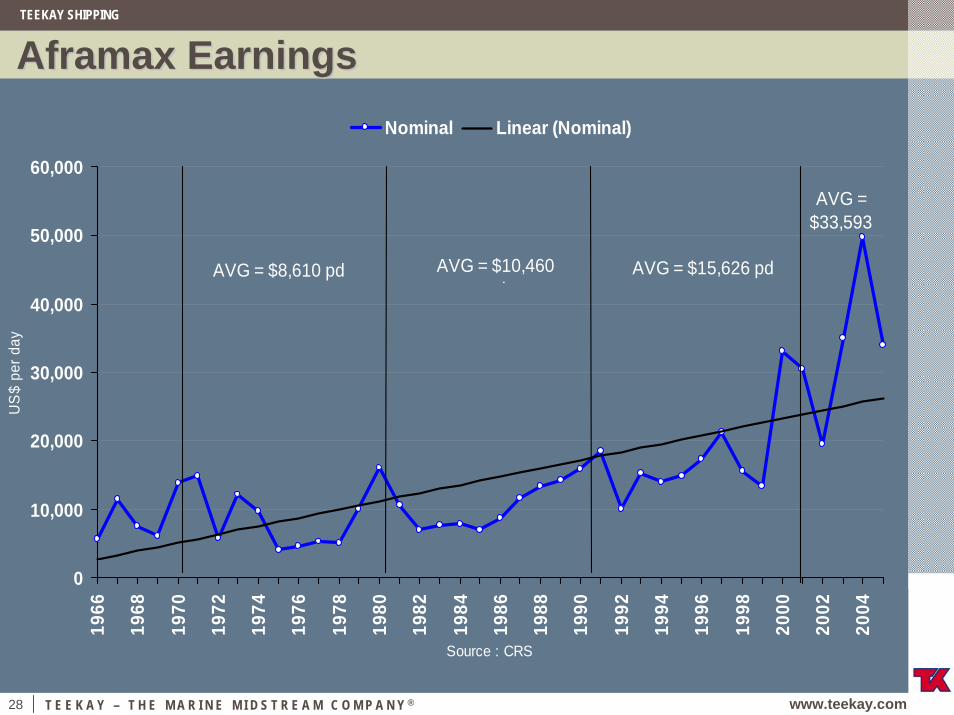

Aframax EarningsAframax Earnings

0

10,000

20,000

30,000

40,000

50,000

60,000

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Source : CRS

US

$ pe

r day

Nominal Linear (Nominal)

AVG = $8,610 pd AVG = $10,460 d

AVG = $15,626 pd

AVG = $33,593

TEEKAY SHIPPING

29 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

1 Year TC Rates for Modern Tankers1 Year TC Rates for Modern Tankers

0

20,000

40,000

60,000

80,0001q

00

3q00

1q01

3q01

1q02

3q02

1q03

3q03

1q04

3q04

1q05

3q05

ytd

Source : CRS

US

$ pe

r day

VLCC TC Suezmax TC Aframax TC MR TC

TEEKAY SHIPPING

30 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

Oil Demand Growth Estimate Oil Demand Growth Estimate

64

70

76

82

88

94

1q02

3q02

1q03

3q03

1q04

3q04

1q05

3q05

E

1q06

E

3q06

E

Source : IEA

Oil

Dem

and

/ Sup

ply-

MB

/D

500

800

1,100

1,400

1,700

2,000

OEC

D In

dust

ry S

tock

s - M

ill. B

bl.

World oil demand OECD Industry Stocks World oil supply

Estimated winter oil demand is 3.0 mb/d higher

than 3q05 demandInventory growth forms part of OPEC strategy to

meet 4q05 peak oil demand

2006 Forecast: 2.1% oil demand growth

TEEKAY SHIPPING

31 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

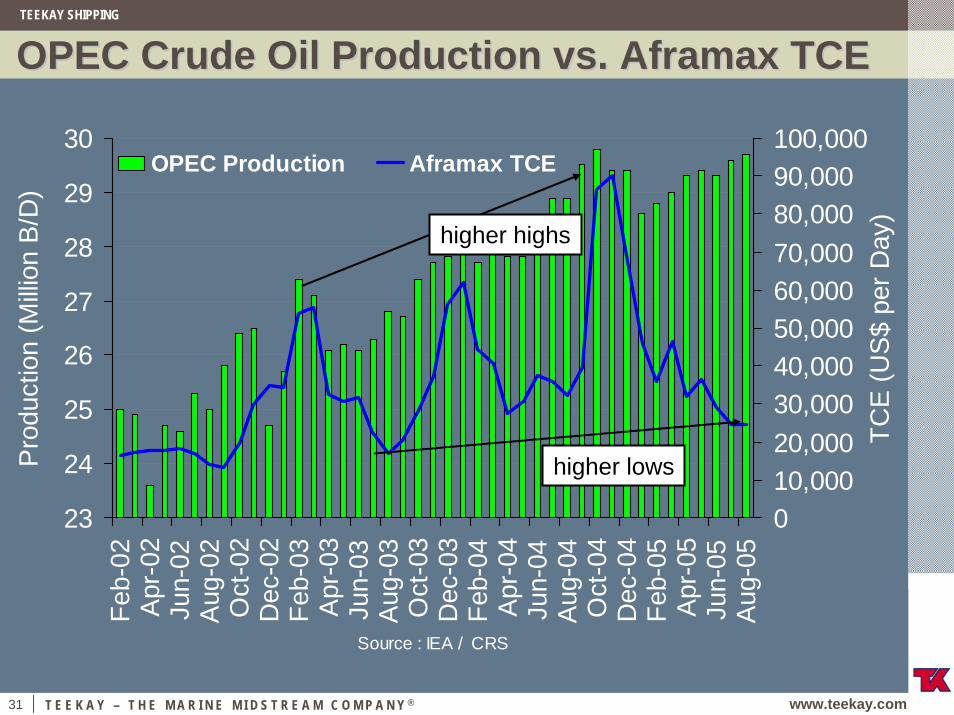

OPEC Crude Oil Production vs. Aframax TCEOPEC Crude Oil Production vs. Aframax TCE

23

24

25

26

27

28

29

30Fe

b-02

Apr

-02

Jun-

02Au

g-02

Oct

-02

Dec

-02

Feb-

03A

pr-0

3Ju

n-03

Aug-

03O

ct-0

3D

ec-0

3Fe

b-04

Apr

-04

Jun-

04Au

g-04

Oct

-04

Dec

-04

Feb-

05A

pr-0

5Ju

n-05

Aug-

05

Source : IEA / CRS

Pro

duct

ion

(Milli

on B

/D)

010,00020,00030,00040,00050,00060,00070,00080,00090,000100,000

TCE

(US$

per

Day

)

OPEC Production Aframax TCE

higher highs

higher lows

TEEKAY SHIPPING

32 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

OPEC Crude Output vs. Aframax TCEOPEC Crude Output vs. Aframax TCE’’ss

23

24

25

26

27

28

29

30

1q99

3q99

1q00

3q00

1q01

3q01

1q02

3q02

1q03

3q03

1q04

3q04

1q05

3q05

ytd

Source : IEA/CRS

Mill

ion

Bbl

s/D

ay

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

US

$/D

ay

OPEC crude prod. Aframax Average

TEEKAY SHIPPING

33 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

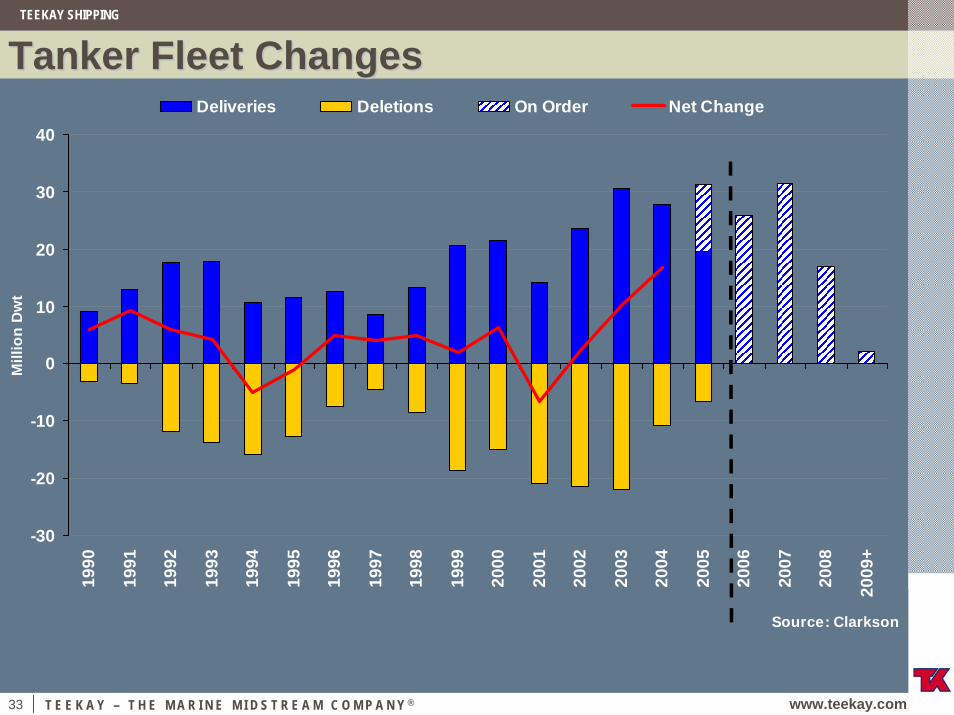

Tanker Fleet ChangesTanker Fleet Changes

-30

-20

-10

0

10

20

30

40

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

+

Source: Clarkson

Mill

ion

Dw

t

Deliveries Deletions On Order Net Change

TEEKAY SHIPPING

34 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

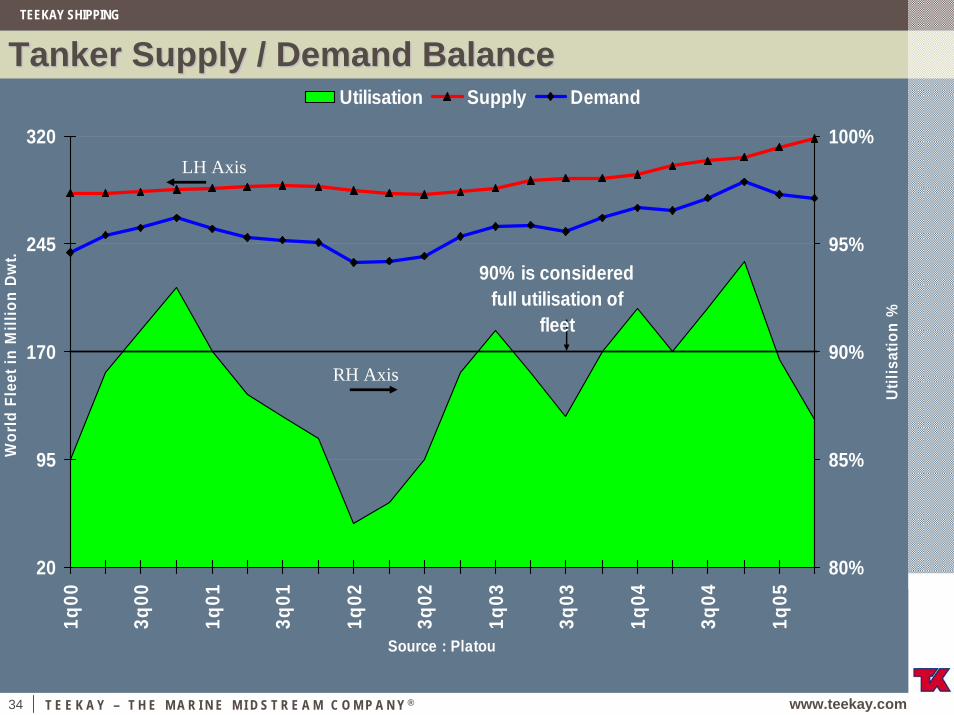

Tanker Supply / Demand BalanceTanker Supply / Demand Balance

20

95

170

245

320

1q00

3q00

1q01

3q01

1q02

3q02

1q03

3q03

1q04

3q04

1q05

Source : Platou

Wor

ld F

leet

in M

illio

n D

wt.

80%

85%

90%

95%

100%

Util

isat

ion

%

Utilisation Supply Demand

90% is considered full utilisation of

fleet

LH Axis

RH Axis

TEEKAY SHIPPING

35 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

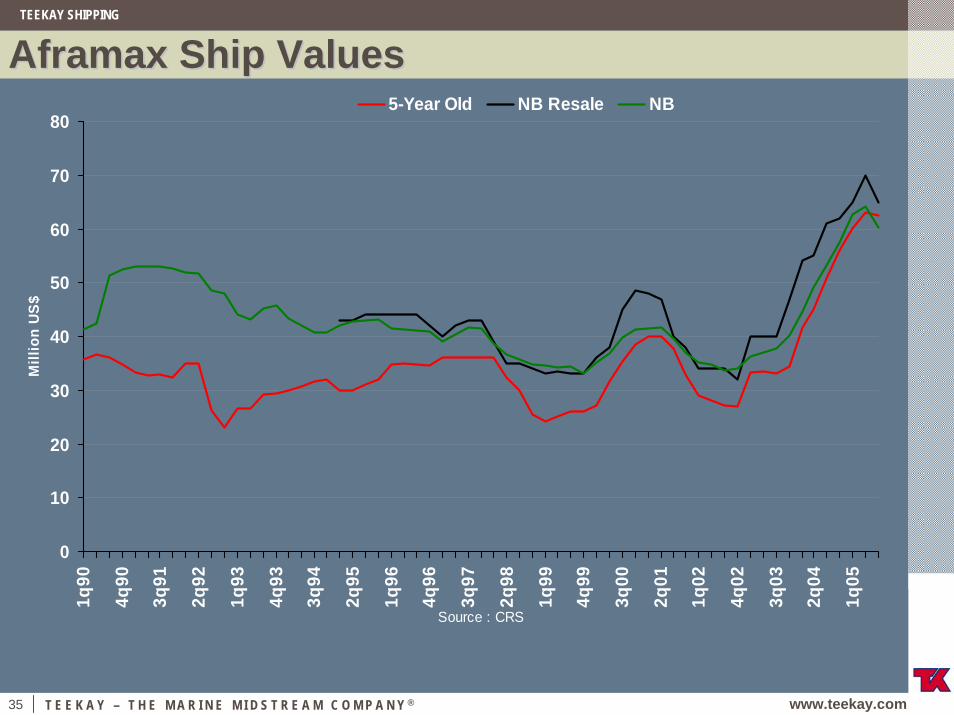

Aframax Ship ValuesAframax Ship Values

0

10

20

30

40

50

60

70

80

1q90

4q90

3q91

2q92

1q93

4q93

3q94

2q95

1q96

4q96

3q97

2q98

1q99

4q99

3q00

2q01

1q02

4q02

3q03

2q04

1q05

Source : CRS

Mill

ion

US$

5-Year Old NB Resale NB

www.teekay.com

T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ®

SM

TEEKAY LNG PARTNERS L.P.TEEKAY LNG TEEKAY LNG PARTNERS L.P.PARTNERS L.P.

TEEKAY SHIPPING

37 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

TeekayTeekay’’ss LNG Carrier OverviewLNG Carrier Overview

Teekay Shipping CorporationEnterprise Value = $5.0 billion

Teekay Shipping CorporationEnterprise Value = $5.0 billion

Teekay GP L.L.C.(General Partner)

Teekay GP L.L.C.(General Partner)

Public Unitholders

Public Unitholders75.7%75.7%

22.3%22.3%

100%100%

2.0%2.0% Teekay LNG Partners L.P.

9 Vessels

Current LNG Fleet

Current Oil Tanker Fleet

LNG Carriers On-Order

5 Vessels4 Vessels

TEEKAY SHIPPING

38 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

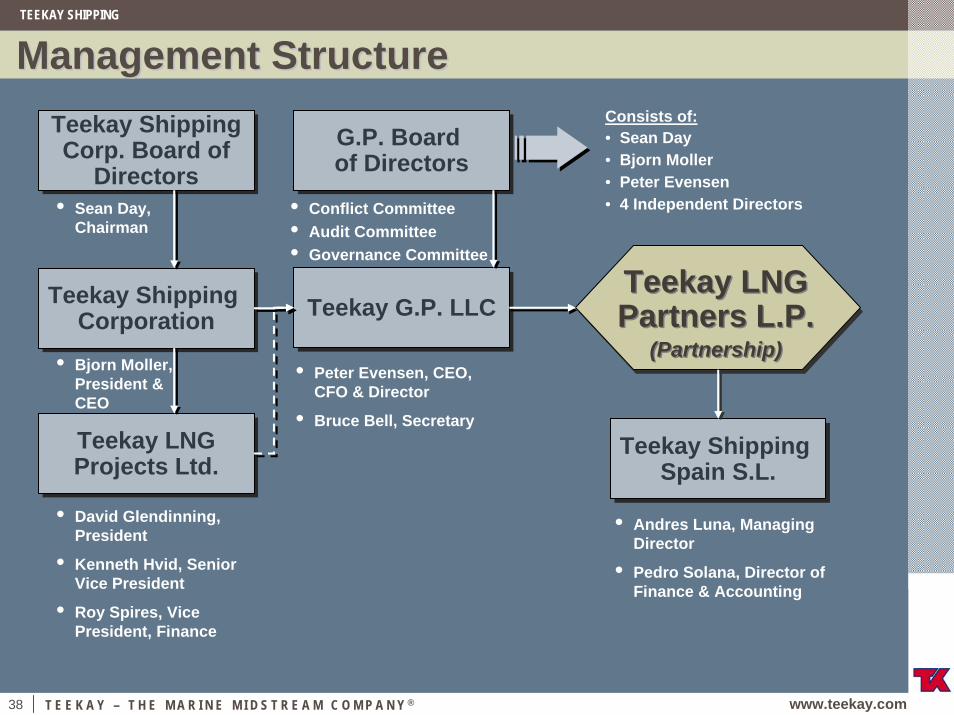

Management StructureManagement StructureConsists of:• Sean Day• Bjorn Moller• Peter Evensen• 4 Independent Directors

Teekay Shipping Corp. Board of

Directors

Teekay Shipping Corp. Board of

Directors

Teekay LNG Partners L.P.

(Partnership)

Teekay LNG Partners L.P.

(Partnership)

G.P. Board of DirectorsG.P. Board of Directors

Teekay Shipping Corporation

Teekay Shipping Corporation Teekay G.P. LLCTeekay G.P. LLC

Teekay LNGProjects Ltd.Teekay LNGProjects Ltd.

Teekay Shipping Spain S.L.

Teekay Shipping Spain S.L.

• Peter Evensen, CEO, CFO & Director

• Bruce Bell, Secretary

• Conflict Committee• Audit Committee• Governance Committee

• Bjorn Moller, President & CEO

• Sean Day, Chairman

• David Glendinning, President

• Kenneth Hvid, Senior Vice President

• Roy Spires, Vice President, Finance

• Andres Luna, Managing Director

• Pedro Solana, Director of Finance & Accounting

TEEKAY SHIPPING

39 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

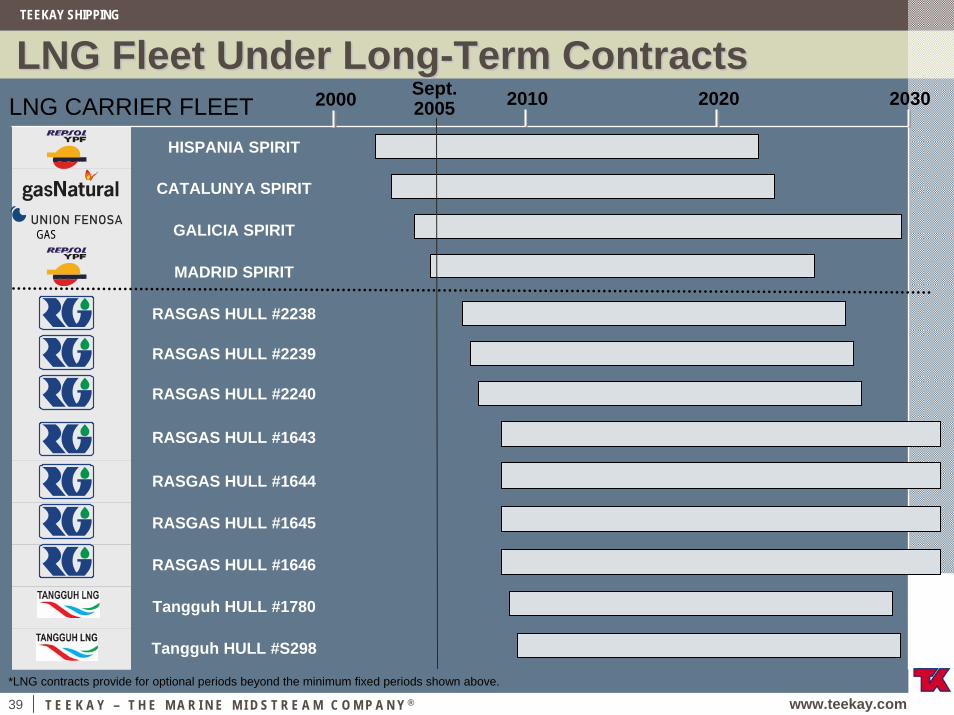

LNG Fleet Under LongLNG Fleet Under Long--Term ContractsTerm Contracts

HISPANIA SPIRIT

RASGAS HULL #1643

RASGAS HULL #1644

RASGAS HULL #1645

RASGAS HULL #1646

Tangguh HULL #1780

Tangguh HULL #S298

CATALUNYA SPIRIT

GALICIA SPIRIT

MADRID SPIRIT

RASGAS HULL #2238

RASGAS HULL #2239

RASGAS HULL #2240

2010 2020 2030

GAS

2000 Sept.2005LNG CARRIER FLEET

*LNG contracts provide for optional periods beyond the minimum fixed periods shown above.

TEEKAY SHIPPING

40 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

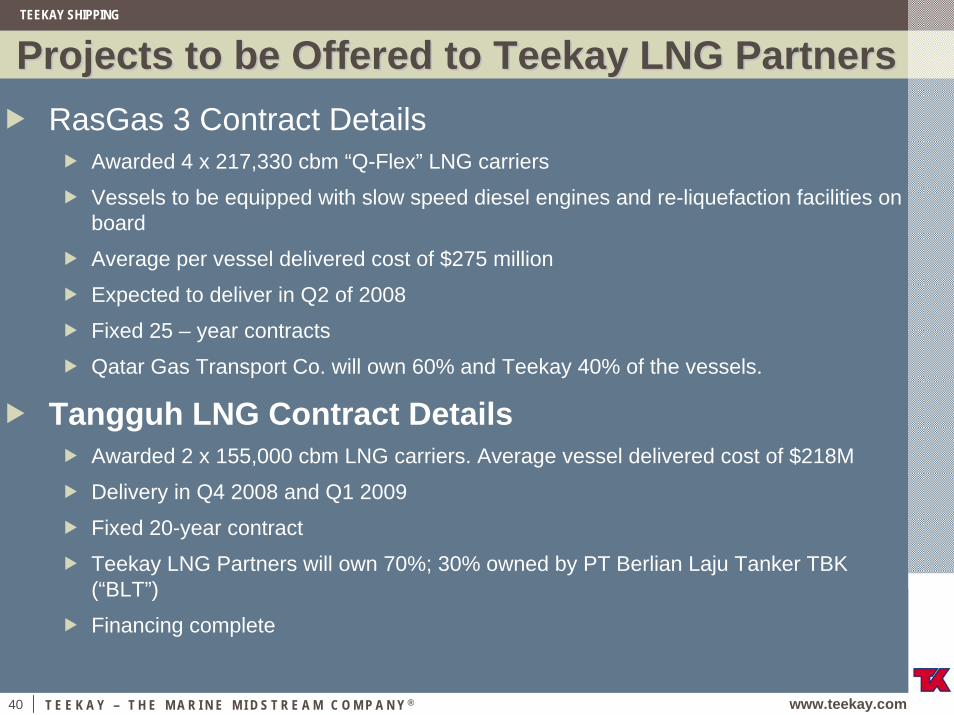

Projects to be Offered to Teekay LNG PartnersProjects to be Offered to Teekay LNG PartnersRasGas 3 Contract Details

Awarded 4 x 217,330 cbm “Q-Flex” LNG carriers

Vessels to be equipped with slow speed diesel engines and re-liquefaction facilities on board

Average per vessel delivered cost of $275 million

Expected to deliver in Q2 of 2008

Fixed 25 – year contracts

Qatar Gas Transport Co. will own 60% and Teekay 40% of the vessels.

Tangguh LNG Contract DetailsAwarded 2 x 155,000 cbm LNG carriers. Average vessel delivered cost of $218M

Delivery in Q4 2008 and Q1 2009

Fixed 20-year contract

Teekay LNG Partners will own 70%; 30% owned by PT Berlian Laju Tanker TBK (“BLT”)

Financing complete

TEEKAY SHIPPING

41 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

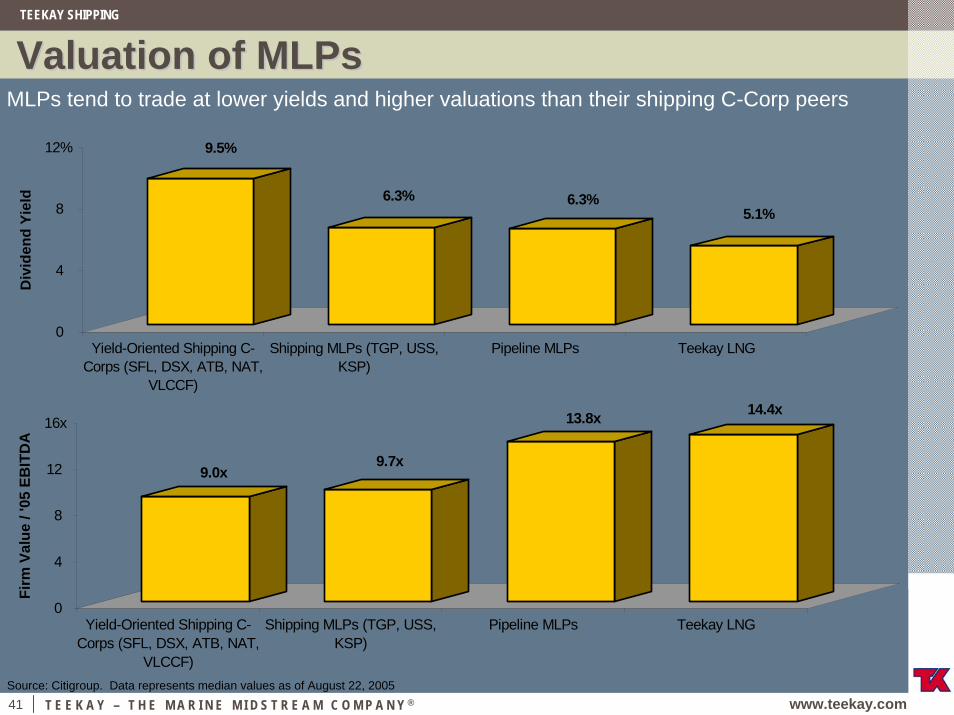

Valuation of Valuation of MLPsMLPsMLPs tend to trade at lower yields and higher valuations than their shipping C-Corp peers

9.5%

6.3% 6.3%5.1%

0

4

8

12%

Div

iden

d Yi

eld

Yield-Oriented Shipping C-Corps (SFL, DSX, ATB, NAT,

VLCCF)

Shipping MLPs (TGP, USS,KSP)

Pipeline MLPs Teekay LNG

9.0x9.7x

13.8x 14.4x

0

4

8

12

16x

Firm

Val

ue /

'05

EBIT

DA

Yield-Oriented Shipping C-Corps (SFL, DSX, ATB, NAT,

VLCCF)

Shipping MLPs (TGP, USS,KSP)

Pipeline MLPs Teekay LNG

Source: Citigroup. Data represents median values as of August 22, 2005

www.teekay.com

T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ®

SM

NEW LNG PROJECTSNEW LNG NEW LNG PROJECTSPROJECTS

TEEKAY SHIPPING

43 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

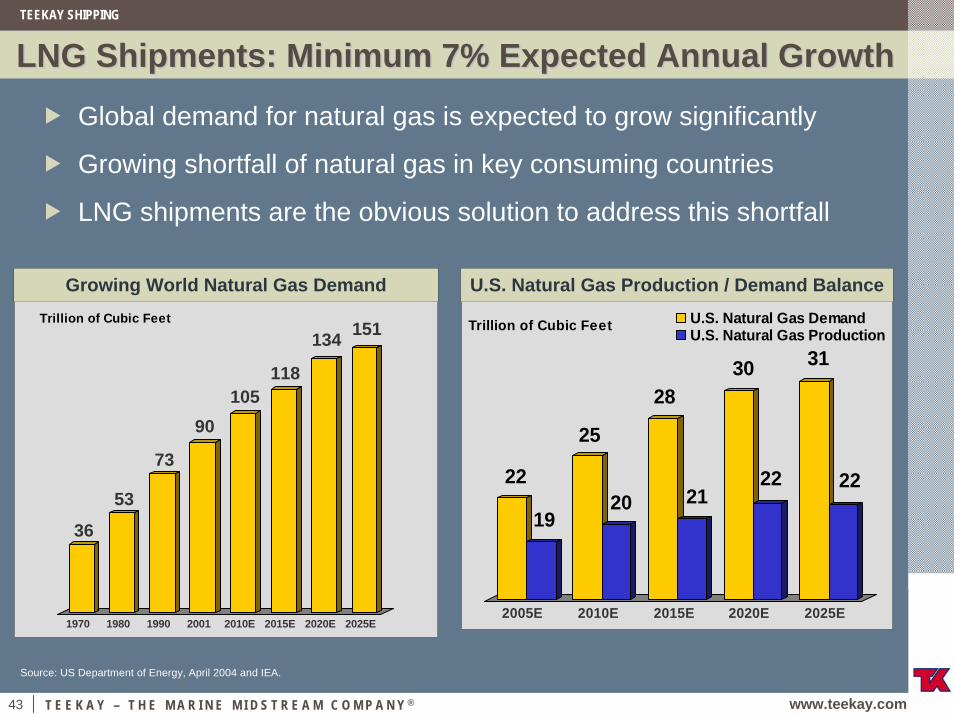

LNG Shipments: Minimum 7% Expected Annual GrowthLNG Shipments: Minimum 7% Expected Annual Growth

Global demand for natural gas is expected to grow significantly

Growing shortfall of natural gas in key consuming countries

LNG shipments are the obvious solution to address this shortfall

36

53

73

90105

118

134 151

1970 1980 1990 2001 2010E 2015E 2020E 2025E

Trillion of Cubic Feet

Growing World Natural Gas Demand U.S. Natural Gas Production / Demand Balance

22

19

25

20

28

21

30

22

31

22

2005E 2010E 2015E 2020E 2025E

Trillion of Cubic Feet U.S. Natural Gas DemandU.S. Natural Gas Production

Source: US Department of Energy, April 2004 and IEA.

TEEKAY SHIPPING

44 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

Increased Demand for LNG CarriersIncreased Demand for LNG Carriers

Today 2010

$16+ billion Market Opportunity

Projected Demand for LNG Carriers by 2010

Existing Fleet

124 Ships Currently On-

Order

81 additional 81 additional ships required ships required to meet to meet projected projected demanddemand

Additional Demand

389 389

184184

* Excludes speculative projects

TEEKAY SHIPPING

45 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

Securing Our Share of the Market OpportunitySecuring Our Share of the Market Opportunity

$16+ billion LNG Market

OpportunityCost of CapitalCost of Capital

Ship Yard Relationships

Ship Yard Relationships

Customer Relationships

Customer Relationships

Operational Excellence

Operational Excellence

Industry ReputationIndustry

Reputation

Technical Expertise

Technical Expertise

Project Management

Project Management

Operating Cost Competitiveness

Teekay LNG has a winning formulaTeekay LNG has a winning formula

TEEKAY SHIPPING

46 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

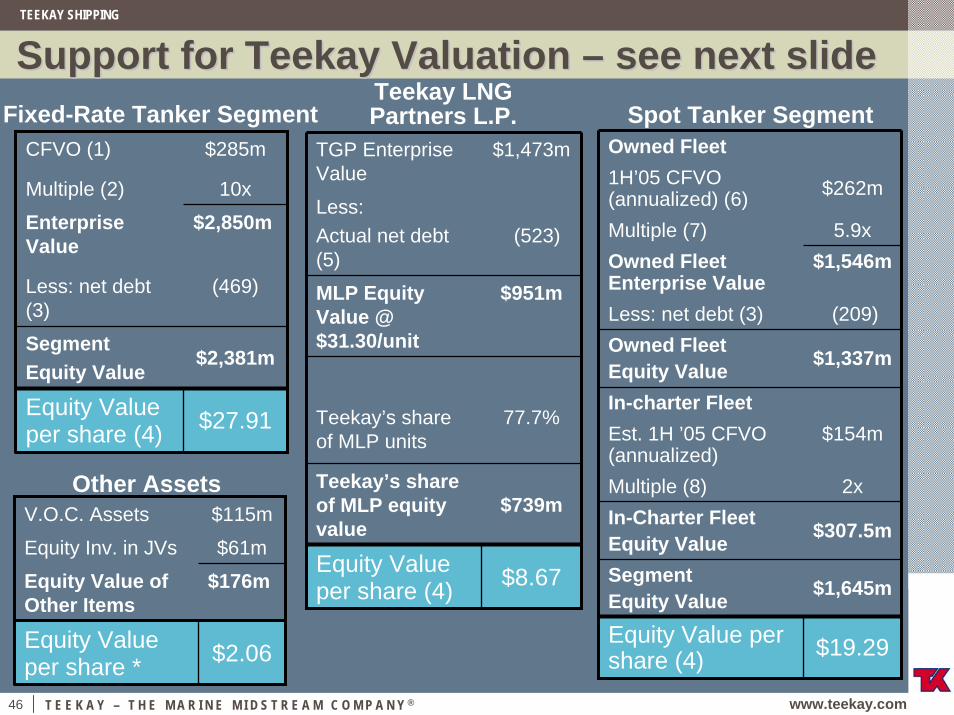

Support for Teekay Valuation Support for Teekay Valuation –– see next slidesee next slideTeekay LNG Partners L.P.Fixed-Rate Tanker Segment Spot Tanker Segment

CFVO (1) $285m

Multiple (2) 10x

Enterprise Value

$2,850m

Less: net debt (3)

(469)

Segment Equity Value

$2,381m

Equity Value per share (4) $27.91

TGP Enterprise Value

$1,473m

Less: Actual net debt (5)

(523)

MLP Equity Value @ $31.30/unit

$951m

Teekay’s share of MLP units

77.7%

Teekay’s share of MLP equity value

$739m

Equity Value per share (4) $8.67

Owned Fleet1H’05 CFVO (annualized) (6) $262m

Multiple (7) 5.9xOwned Fleet Enterprise Value

$1,546m

Less: net debt (3) (209)Owned Fleet Equity Value $1,337m

In-charter FleetEst. 1H ’05 CFVO (annualized)

$154m

Multiple (8) 2xIn-Charter FleetEquity Value $307.5m

Segment Equity Value $1,645m

Equity Value per share (4) $19.29

V.O.C. Assets $115m

Equity Inv. in JVs $61m

Equity Value of Other Items

$176m

Equity Value per share * $2.06

Other Assets

TEEKAY SHIPPING

47 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

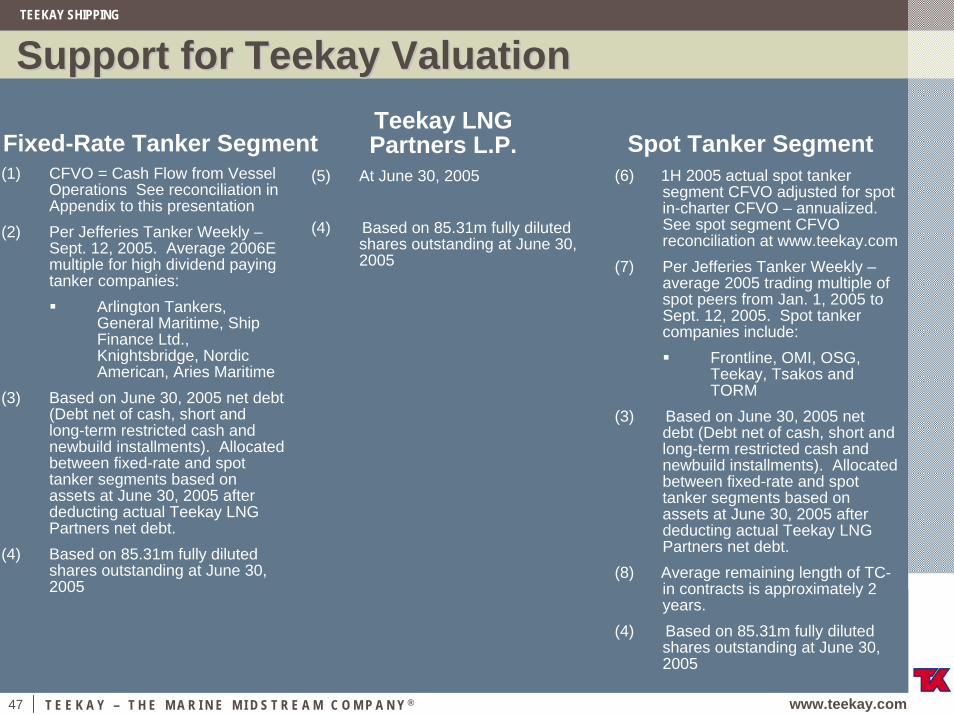

Support for Teekay ValuationSupport for Teekay Valuation

Fixed-Rate Tanker SegmentTeekay LNG Partners L.P. Spot Tanker Segment

(1) CFVO = Cash Flow from Vessel Operations See reconciliation in Appendix to this presentation

(2) Per Jefferies Tanker Weekly –Sept. 12, 2005. Average 2006E multiple for high dividend paying tanker companies:

Arlington Tankers, General Maritime, Ship Finance Ltd., Knightsbridge, Nordic American, Aries Maritime

(3) Based on June 30, 2005 net debt (Debt net of cash, short and long-term restricted cash and newbuild installments). Allocated between fixed-rate and spot tanker segments based on assets at June 30, 2005 after deducting actual Teekay LNG Partners net debt.

(4) Based on 85.31m fully diluted shares outstanding at June 30, 2005

(5) At June 30, 2005

(4) Based on 85.31m fully diluted shares outstanding at June 30, 2005

(6) 1H 2005 actual spot tanker segment CFVO adjusted for spot in-charter CFVO – annualized. See spot segment CFVO reconciliation at www.teekay.com

(7) Per Jefferies Tanker Weekly –average 2005 trading multiple of spot peers from Jan. 1, 2005 to Sept. 12, 2005. Spot tanker companies include:

Frontline, OMI, OSG, Teekay, Tsakos and TORM

(3) Based on June 30, 2005 net debt (Debt net of cash, short and long-term restricted cash and newbuild installments). Allocated between fixed-rate and spot tanker segments based on assets at June 30, 2005 after deducting actual Teekay LNG Partners net debt.

(8) Average remaining length of TC-in contracts is approximately 2 years.

(4) Based on 85.31m fully diluted shares outstanding at June 30, 2005

TEEKAY SHIPPING

48 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

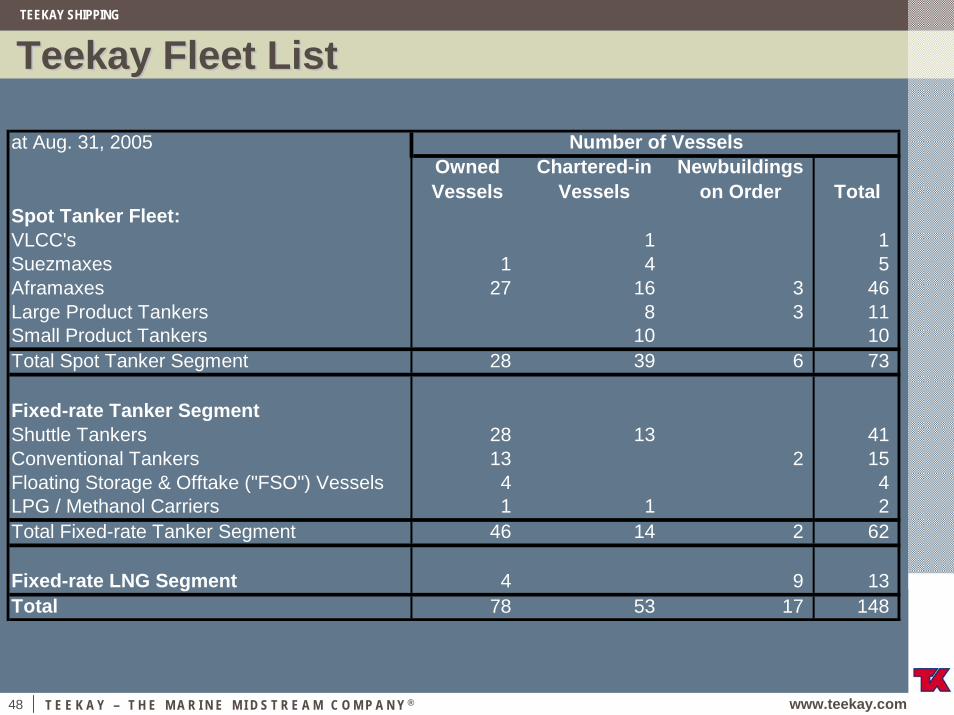

Teekay Fleet ListTeekay Fleet List

at Aug. 31, 2005Owned Vessels

Chartered-in Vessels

Newbuildings on Order Total

Spot Tanker Fleet:VLCC's 1 1 Suezmaxes 1 4 5 Aframaxes 27 16 3 46 Large Product Tankers 8 3 11 Small Product Tankers 10 10 Total Spot Tanker Segment 28 39 6 73

Fixed-rate Tanker SegmentShuttle Tankers 28 13 41 Conventional Tankers 13 2 15 Floating Storage & Offtake ("FSO") Vessels 4 4 LPG / Methanol Carriers 1 1 2 Total Fixed-rate Tanker Segment 46 14 2 62

Fixed-rate LNG Segment 4 9 13 Total 78 53 17 148

Number of Vessels

TEEKAY SHIPPING

49 T E E K A Y – T H E M A R I N E M I D S T R E A M C O M P A N Y ® www.teekay.com

NonNon--GAAP ReconciliationGAAP ReconciliationCash flow from vessel operations represents income from vessel operations before depreciation and amortization expense and vessel write-downs/(gain) loss on sale of vessels. Cash flow from vessel operations is a non-GAAP financial measure used by certain investors to measure the financial performance of shipping companies. Cash flow from operations is not required by accounting principles generally accepted in the United States and should not be considered as an alternative to net income or any other indicator of the Company's performance required by accounting principles generally accepted in the United States. The following table reconciles this non-GAAP measure as used in this presentation to the most directly comparable GAAP financial measure for the periods presented.

Year Ended

Dec. 31, 2005

Projection for Fixed-rate Tanker Segment

Income From Vessel Operations 160,000

Depreciation and Amortization 125,000

Cash flow from vessel operations 285,000