table of - scottsdale arizona realtor · • coordinates all information between buyer, lender,...

TRANSCRIPT

Table Of Contents:

CLOSING THE AMERICAN DREAM.

Useful Information q YOUR CONTACTSq WHO DOES WHATq WHY USE A REALTOR®

q ESCROW & TITLE

Buyer’s Guide q BUYERS TIPSq HOUSE HUNTINGq HOUSE HUNTING EVALUATIONq FOUND YOUR HOME, NOW WHAT?q WAYS TO TAKE TITLE IN ARIZONAq MISCELLANEOUS INFORMATION

Seller’s Guideq SELLING A HOMEq SHOWING A HOMEq INSPECTIONSq HOME WARRANTIESq F.A.Q.q MOVING CHECKLISTq FORMS AND DOCUMENTS

This publication is designed to provide general information provided by American Title Service Agency LLC, in regard to the subject matter covered in this Buyer/Seller Guide. It is provided free of charge with the understanding that the publisher is not engaged in rendering legal, accounting, tax, real estate related or other professional services. Although prepared by American Title Service Agency LLC, this publication should not be utilized as a substitute for paid professional services. If professional real estate assistance is required, seek the assistance of an attorney or a licensed Arizona REALTOR®.

WHO DOES WHAT?Here is some helpful information so that you may understand who your team is and what they do for you.

A BUYERS AGENT

•Representsbuyerwithpurchaseofproperty,loanandescrowprocess •Helpsbuyerengagealenderwhoinformsbuyerthemaximumloanamounttheyqualifyfor •Helpsbuyerfindsuitableproperty •Advisesbuyerandhelpsnegotiatethepriceandtermsthroughseller’sagent •Verifiesallpropertyinformationfrompreliminarytitlereports,liens,title, legal description, restrictions, easements, etc. •Coordinatesallinformationbetweenbuyer,lender,escrow,inspectionsandseller’sagent •Guidesbuyerthroughcontractprocess,loan,requiredinsurance,escrowandclosing •Takesbuyeron“walkthrough”inspectionofpropertytonoteanyproblems that need to be addressed during the inspection period •Arrangestomeetwithanyinspectorsatproperty(withorwithoutbuyerpresent) •UsuallyaccompaniesbuyertoAmericanTitleServiceAgencyforloanandescrowsigning •Deliversexistingkeystobuyerafterthepropertyrecordsfromsellertobuyer

A SELLERS AGENT

•Representssellerofproperty •Orderspropertyprofilefromtitlecompanytodetermineownership,liens,legaldescription,square footage, bedrooms, baths, roof, heat/air, or special amenities such as a pool, workshop, etc. •Doesmarketresearchandhelpsthesellerestablishthemarketvalueofthepropertyfromrecentsales •Listspropertyonmultiplelistingservice,reachingalmosteveryREALTOR® in the community •MarketstoREALTORS®, advertises, holds open houses, dispurses information about your property through the multiple listing service or other cooperative marketing networks •Overseesnecessaryrepairsofpropertyandmaintenanceduringlistingperiod •Negotiatespriceandtermsofpurchasecontractwithbuyersagentonbehalfoftheseller •Coordinatesanddisseminatesinformationbetweenbuyer’sagent,seller, escrow, property inspectors and any others involved in sale •Overseesinspectionsandanyotherrepairsagreedtoincontract •Usuallymeetswithsellertosignescrow/loandocumentsarrangespickupanddelivery of existing keys to property and instructional information on any equipment, warranties, etc.

CLOSING THE AMERICAN DREAM.

YOUR AMERICAN TITLE SERVICE AGENCY ESCROW OFFICER

•Coordinatesmostaspectsofpurchasecontract •Orderspreliminarytitlereportonsubjectpropertytoconfirmlegalinformationonsubjectproperty, owners of record, current taxes, deed/lien information and CC&R’S of record •Makescertainthatall“conditions”aremetasperinstructions,agreedtobybuyerandseller •Coordinatesallinformationbetweenbothagents,titledepartment,lenderandinspectors,etc. •Gathersalldocumentationregardingnewandexistingloans,inspectionreports, repairs and title requirements, etc. •Arrangesforbuyerandsellertosignallescrowandtitledocuments •Recordsalldocumentsrequiredtotransfertitlefromsellertobuyer •Disbursesallfundsnecessaryforexistingloanpayoff,inspections,demandsofpaymentsforrepairs,etc. •Arrangesforsellertoreceiveproceedsofsale

YOUR LOAN OFFICER

•Definesloanamountforborrower •Qualifiesborrower •Ordersappraisalonsubjectproperty •Submitsborrower’sinformationtounderwriterforapproval •Ordersloandocumentstobesenttoescrowforborrowers’signature •Returnsdocumentstounderwriterforfinalinspection(correctsignatures/dates) •Ordersloanfundsforpurchasewhicharesenttoescrowfordisbursementbyescrowofficer

CLOSING THE AMERICAN DREAM.

CLOSING THE AMERICAN DREAM.

WHY USE A REALTOR®?All real estate licensees are not the same. Only real estate licensees who are members of the NATIONAL ASSOCIATION OFREALTORS®areproperlycalledREALTORS®.TheyproudlydisplaytheREALTOR“®”logoontheirbusinesscard or other marketing and sales literature. REALTORS® are committed to treat all parties to a transaction honestly. REALTORS® subscribe to a strict code of ethics and are expected to maintain a higher level of knowledge of the process of buying and selling real estate. An independent survey reports that 84% of home buyers would use the same REALTOR® again.

Real estate transactions involve one of the biggest financial investments most people experience in their lifetime. Transactions today usually exceed $100,000. If you had a $100,000 income tax problem, would you attempt to deal with it without the help of a CPA? If you had a $100,000 legal question, would you deal with it without the help of an attorney? Considering the small upside cost and the large downside risk, it would be unwise to consider a purchase of real estate without the professional assistance of a REALTOR®.

But if you’re still not convinced of the value of a REALTOR®, here are a dozen more reasons to use one:

1. Your REALTOR® can help you determine your buying power; that is, your financial reserves plus your borrowing capacity. If you give a REALTOR® some basic information about your available savings, income and current debt, heorshecanreferyoutolendersbestqualifiedtohelpyou.Mostlenders,(banksandmortgagecompanies)offerlimited choices.

2. Your REALTOR® has many resources to assist you in your home search. Sometimes the property you are seeking is available but not actively advertised in the market, and it will take some investigation by your agent to find all available properties.

3. Your REALTOR® can assist you in the selection process by providing objective information about each property. Agents who are REALTORS® have access to a variety of informational resources. REALTORS® can provide local community information on utilities, zoning, schools, etc. There are two things you’ll want to know. First, will the property provide the environment I want for a home or investment? Second, will the property have resale value when I am ready to sell?

4. Your REALTOR® can help you negotiate. There are a myriad of negotiating factors, including but not limited to price, financing, terms, date of possession and often the inclusion or exclusion of repairs and furnishings or equipment. The purchase agreement should provide a period of time for you to complete appropriate inspections and investigations of the property before you are bound to complete the purchase. Your agent can advise you as to which investigations and inspections are recommended or required.

5. Your REALTOR® provides due diligence during the evaluation of the property. Depending on the area and property, this could include inspections for termites, dry rot, asbestos, faulty structure, roof condition, septic tank andwelltests,justtonameafew.YourREALTOR®canassistyouinfindingqualifiedresponsibleprofessionalsto

CLOSING THE AMERICAN DREAM.

do most of these investigations and provide you with written reports. You will also want to see a preliminary report on the title of the property. Title indicates ownership of property and can be mired in confusing status of past owners orrightsofaccess.Thetitletomostpropertieswillhavesomelimitations;forexample,easements(accessrights)for utilities. Your REALTOR®, title company or attorney can help you resolve issues that might cause problems at a later date.

6. Your REALTOR® can help you in understanding different financing options and in identifyingqualified lenders.

7. Your REALTOR® can guide you through the closing process and make sure everything flows together smoothly.

8. When selling your home, your REALTOR® can give you up-to-date information on what is happening in the marketplace and the price, financing, terms and condition of competing properties. These are key factors in getting your property sold at the best price, quickly and with minimum hassle.

9. Your REALTOR® markets your property to other real estate agents and the public. Often, your REALTOR® can recommend repairs or cosmetic work that will significantly enhance the salability of your property. Your REALTOR® markets your property to other real estate agents and the public. In many markets across the country, over 50% of real estate sales are cooperative sales; that is, a real estate agent other than yours brings in the buyer. Your REALTOR® acts as the marketing coordinator, disbursing information about your property to other real estate agents through a Multiple Listing Service or other cooperative marketing networks, open houses for agents, etc. The REALTOR® Code of Ethics requires REALTORS® to utilize these cooperative relationships when they benefit their clients.

10. Your REALTOR® will know when, where and how to advertise your property. There is a misconception that advertising sells real estate. The NATIONAL ASSOCIATION OF REALTORS® studies show that 82% of real estate sales are the result of agent contacts through previous clients, referrals, friends, family and personal contacts. When a property is marketed with the help of your REALTOR®, you do not have to allow strangers into your home. Your REALTOR® will generally prescreen and accompany qualified prospects through your property.

11. Your REALTOR® can help you objectively evaluate every buyer’s proposal without compromising your marketing position. This initial agreement is only the beginning of a process of appraisals, inspections and financing -- a lot of possible pitfalls. Your REALTOR® can help you write a legally binding, win-win agreement that will be more likely to make it through the process.

12. Your REALTOR® can help close the sale of your home.Betweentheinitialsalesagreementandclosing(orsettlement),questionsmayarise.Forexample,unexpectedrepairsarerequired toobtain financingoracloud inthe title is discovered. The required paperwork alone is overwhelming for most sellers. Your REALTOR® is the best persontoobjectivelyhelpyouresolvetheseissuesandmovethetransactiontoclosingorsettlement.

Courtesy of Realtor.com

CLOSING THE AMERICAN DREAM.

WHAT IS ESCROW?Whenfinalizingthepurchaseorsaleofahome,aneutral,3rdparty(theescrowholder,a.k.a.escrowagent/officer)isengagedtoassurethetransactionwillcloseproperlyandontime.

The escrow holder insures that all terms and conditions of the seller’s and buyer’s purchase contract/escrow agreement are met prior to the sale being finalized, including receiving funds and documents, completing required forms, and obtaining the release documents for any loans or liens that have been paid off within the transaction, assuring you clear title to the property before the purchase price is fully paid.

The documentation the escrow holder may be collecting includes:•Loandocuments•PropertyTaxInformation•Fireandotherinsurancepolicies•Titleinsurancepolicies•Termsofsaleandanyseller-assistedfinancing•Requestsforpaymentforvariousservicestobepaidoutofescrowfunds

Upon completion of all instructions of the escrow, closing can take place. All outstanding payments and fees are collected and paid at this time covering expenses such as; taxes, homeowner association transfer fees, inspection fees, real estate commissions and title insurance and escrow fees. Title to the property is then transferred from the seller to the buyer and appropriate title insurance is issued as outlined in the purchase contract and preliminary title report. At the close of escrow, payment of funds due by you shall be made in an acceptable form to the escrow holder, this is typically a Cashier’s Check or wire transfer of funds.

WHAT ESCROW NEEDS FROM THE BUYER•Yourexactname,maritalstatus,addressandcontactinformationandmanner in which you wish to acquire title.•Nameandaddressofyourproposedlender.Also,thenameandphonenumber of your loan representative.

TIPS FOR A SUCCESSFUL CLOSING

COMMUNICATEFrequentcommunicationwithallpartiesinvolved(yourREALTOR®,loanofficerandescrowofficer)iscritical.Itisextremelyimportanttocommunicateanysignificantchangesinyourlife,suchasjobchanges,newcarpurchases, and changes to your sales price, as well as if you wish to change your close of escrow date.

HOMEOWNER’S INSURANCEFailure to secure Homeowner’s Insurance in advance of closing is a leading cause of delays in the mortgage process. Insurance should be secured as soon as possible before your scheduled closing date. It is no longer always possible to secure homeowners insurance at the last minute. Be prepared to order this as soon as you can.

CHANGING JOBSYour income is a crucial part of the puzzle when determining your ability to repay the loan. The underwriter looks atthestabilityofyourjobandshouldyouchangejobsduringtheloanprocess,itpotentiallycouldcreatesomeinstability in your loan profile. Contact your Loan Officer prior to making any career changes.

DEBTPaying off debt may sound like the right thing to do, but the additional liquid assets you have may have been a determining factor in your loan approval. Contact your Loan Officer before making any significant changes to your debt structure. Also avoid allowing payments to be late between now and closing.

PROVIDE DOCUMENTATION WHEN REQUESTEDAny delay in receiving requested information may postpone the approval and closing process. Provide all requested information in a timely manner.

LARGE PURCHASESYourdebtsandcashreserveshavealreadybeenassessed.Anychangestothesecouldjeopardizeyourapproval.Contact your Loan Officer prior to making any significant purchases.

AVOID MAKING MOVING PLANS TOO TIGHTTry to allow a 5-7 day overlap between closing date and move date. If the closing date is moved for any reason, unbudgeted expenses could occur.

FINANCIAL RECORDSOccasionally, your mortgage company will have to verify information from previous bank account statements or pay check stubs such as large deposits or bonus checks. Save all of these items during the loan process as well as the paper trails on any deposits that are not income, such as tax refunds or 401k loans. When you pack, remember to keep all financial information in a convenient place. Do not put this information in storage or let movers take it.

ALLOW TIME TO GO TO THE BANK ON CLOSING DAYThe cashier’s check or wired funds for closing should be made out to American Title Service Agency. Assuming your loan process went exactly as planned, you will receive your final closing figures from the title company prior to your closing.

CLOSING THE AMERICAN DREAM.

CLOSING THE AMERICAN DREAM.

UNDERSTANDING TITLE INSURANCEIn Arizona, it is common for a title company to issue two title insurance policies:

1)TheOwner’sPolicy2)TheLender’sPolicy

Each plays a vital role in the home buying process, though the homeowner only benefits from the Owners Policy of title insurance.

The “ALTA” Homeowner’s title insurance policy(whichstandsfortheAmericanLandTitleAssociation),isanextended title insurance policy that protects the homeowner from any undetected clouds or defects of title that did not show up in the title search and up to 34 other potential issues. Generally, the premium for this policy is paid by the seller of the home for the buyer. This title insurance policy is based upon the sales price of the home.

The second type of policy is issued by American Title Service Agency to protect the lender from any clouds or defects should they have to foreclose upon the homeowner. Often referred to as an “ALTA” loan policy, this policy protects lenders of all types who are making loans of their depositors’, investors’ or employees’ funds and must obtain the security of a real property to protect the investment. To obtain title insurance for its investment, alenderneedsavalid,enforceablemortgagelienthathaspriority(alsoknownasafirstmortgage)overanyknown or unknown interests or claims to the property that is used as security for the note. Title insurance provides the assurance which the lender needs by insuring that the homeowner actually has title to the property and that no other entity or person has an interest that will affect the lender’s security. This title insurance policy is based upon the buyer’s loan amount.

These types of policies provide for indemnity against loss or damage for undisclosed interests, ownerships, defects, liens or encumbrances on or affecting the property, or because of a lack of access to or from the property or for an alleged or actual un-marketability of title to the property. In addition to insurance of the title, the ALTA loan policy insures the validity, enforceability and priority of the mortgage against the home.

WHY DO I NEED TITLE INSURANCE?Purchasing a home is probably the single biggest investment you will ever make. Before closing on the house, you’ll want to know that no other individual or entity has a right, lien or claim to the property.

Delivering a clear title from a seller to a buyer is achieved through the issuance of a Title Insurance Policy. Title insuranceprovidescoverage forownersof realproperty (real estate) and lenderswhouse realproperty assecurity for a loan by protecting them against claims against the property.

CLOSING THE AMERICAN DREAM.

TITLE INSURANCE = PEACE OF MINDResearching a property’s title history generally uncovers the most obscure claims against a home. However, therecouldbe“hiddenrisks”thatcouldthreatenthehomeowner’sclaimtoownershipofahome.Matterssuchas forgery, incompetency or incapacity of the parties, fraudulent impersonation, and unknown errors in the recordsareexamplesof“hiddenrisks”thatcouldprovidebasisforaclaimafterahomeownerhaspurchaseda property.

For a modest, one-time title insurance premium, you will receive continuous title insurance protection in an amount equal to the purchase price of the property or its current market value. There are seperate premiums for your owners policy as well as your lenders policy. When issued simultaneously, the lenders policy premium is provided at a discounted rate.

One of the marked advantages of title insurance is that prior to a policy being issued, American Title Service Agency completes extensive research into relevant public records, maps and documents to trace ownership of the property and determine if anyone other than you has an interest in the property. Through its research, American Title Service Agency can usually identify any title problems that may arise and have these problems cleared-up prior to closing.

Your title insurance owner’s policy will describe the property and outline any recorded limitations onyour ownership. It will also set forth the underwriters responsibilities should any claim covered by the policy terms arise. Typically your title insurance will protect you from loss:

•Ifsomeonecontestsyourtitleinacivilactionthetitleinsurancecompanywilldefendthetitle atnoexpensetoyousubjecttopolicylimitationsanddeductibles. •Ifthereisatitledefectthatcannotbeeliminatedyourtitlepolicywillprotectyoufromfinancialloss based on policy limitations and deductibles up to the amount of the policy.

CLOSING THE AMERICAN DREAM.

NOTES...

CLOSING THE AMERICAN DREAM.

Buyer’s Guide

CLOSING THE AMERICAN DREAM.

BUYERS TIPSSO YOU ARE GETTING READY TO BUY... Now is the time to assess your situation, motivation and bank account to determine how you can accomplish your goal of getting into your first home or moving into a different home. You will need to consider many things including your employment history, income, credit history and current debt, what you can afford and how much it will cost you to get into a home... and that’s before you even think about your wants and needs in a home.

FIRST THINGS FIRST... PREPARATIONIn this day and age we are prone to wanting instant gratification. Due to this, many potential homebuyers go looking at homes first, then contact the REALTOR® to view a few that have caught their eye. Then they figure out how to pay for the new home. This can be self-defeating! The best and least stressful method of buying a home goes in this order:

•FINDAREALTOR® •DECIDEYOURWANTSAND NEEDS IN A HOME •SHOPFORAMORTGAGELENDER •CHECKYOURCREDIT •CALCULATEYOURDOWNPAYMENTAND CLOSING COSTS •SHOPFORHOMES

DECIDE YOUR WANTS AND NEEDS IN A HOMEWhat do you need in a home? What do you want in a home? What are you willing to compromise on? A family of 5 for example might need 4 bedrooms, one for the parents and one for each child, however, you might want anextrabedroomjustincaseAuntieEmcomestovisitortouseasahomeoffice/gym.Sonopointshoppingfor 3 bedroom homes - however it would be nice to shop for 4 and 5 bedroom homes in case you find one with the extra bedroom that you want. If school districts are important to you, make it a non-negotiable need. You’d lovetohaveapool(want)butwouldsettleforahomewithoutoneifitofferedeverythingelseyouneeded.You’dpreferahome(want)onthecorner,butit’snottheendoftheworldifyoudon’tfindit(youdon‘tneedit).Listyourwantsononesideandyourneeds(musthaves)ontheothersideofourhandyWantsandNeedsListforaneasy‘shopping’guide.

SHOP FOR A MORTGAGE LENDERNot all loan professionals are created equal and so shopping for a good mortgage professional is important. Ask your REALTOR®, friends, family and co-workers for referrals to professionals they have used with positive

HELPFUL HINTS: What is EARNEST MONEY?

Earnest money is a deposit that is presented with an offer as a show of the buyer’s good faith. If the contract is accepted the earnest money is deposited with a neutral third party preferably American Title Service Agency and credited to the buyer at closing.

CLOSING THE AMERICAN DREAM.

results. Some lending companies can only offer a few loan programs while others have unlimited access. Ask about their charges for giving you a loan too; this can affect your closing costs. Some loan companies charge higher origination fees and or points but can get lower interest rates while others charge a small origination fee and no points but your payment might be a bit higher. Know what is important to you, what you can afford and ask questions. Having slightly higher closing costs up front might be more attractive to you than paying a higher house payment each month or paying a few dollars more each month might help to lower your closing costs. When you know what you can afford to buy, shopping for a home is so much simpler.

CHECK YOUR CREDITKnowing your credit score and catching errors or misunderstandings on your report before applying for a loan is a smart move. Look at your income versus your monthly expenses, make sure you remember to include thingssuchaschildcare,groceries,homemaintenanceandautomobilecosts(payment/gas/insuranceetc)whencalculating your debt load. Knowing how much money each month you can safely afford for a house payment along with how much you have saved for a down payment and closing costs is probably the easiest way to determine how much you can spend. When you contact a lender they can assist you with this analysis.

THE THREE MAJOR CREDIT BUREAUS YOU CAN REQUEST YOUR CREDIT REPORT FROM ARE:Trans Union 1-888-503-0048 - Equifax 1-800-685-1111 - Experian 1-888-EXPERIAN (397-3742)

DOWN PAYMENTA down payment is usually between 3% and 20% of the total cost of the home. The amount of the down payment depends on your credit history, income, the cost of the home, and the type of mortgage you choose. Some lenders also have loan options that allow for no down payment at all. PMI is insurance you pay to protect the bank if you don’t repay your loan in full. PMI is added to your closing and monthly mortgage costs. When you apply for a home loan, in addition to the down payment funds, many mortgages require you to also have at least two months worth of mortgage payments saved, called reserves. However, there are mortgages that do not require reserves. Most lenders want to know the source of your down payment and have restrictions about how much can come from gifts from your relatives. In most cases, these gifts will need to be documented. Ask your lender for more information.

CLOSING COSTSClosing, or settlement, costs are fees you pay when you actually get your loan from your financial institution. These include points, taxes, title insurance, escrow fees, financing costs, items that must be prepaid or escrowed, and other settlement costs. You’ll receive an estimate from your lender after you apply for a mortgage. You must pay these costs at the time you close on your loan.

CLOSING THE AMERICAN DREAM.

house huntingSHOP FOR HOMESAfter your REALTOR® has seen a copy of your wish list, they will compile a list of homes to show you. Allow plenty of time to view the homes, use our handy Property Evaluation Forms to keep track of the features in the homes you see and, when ready, make a strong competitive offer! Of course your REALTOR® can compile a list of homes for you without the Wants and Needs list – but the more you know about what you want and what you really need, the easier it is on all of you! *Note in this market, it is highly likely that the home you are interested in could have other offers being submitted on the same day. Making your offer with the least amount ofcontingencies,showingyouareaqualifiedbuyerandofferingasubstantialearnestmoneydeposit(whichcanbeusedtowardyourdownpayment)mightjustgetyourofferplacedonthetopofthepile!Bepreparedtowritea contract on a different home if your offer is not accepted and/or be ready to look at different homes. The right homeisalwaysoutthere,sometimesitjusttakespatienceandperseverancetofindit.

NEW OR RESALE?As you search for your dream home, you’ll probably hear a variety of opinions on whether you should purchase anewlybuilthome(newbuild)ora resalehome(purchase frompreviousowner).Thereareadvantages toboth new builds and resales, but your individual needs, not the age of the structure, should be foremost in deciding which is best for you. For a better idea of which type may be more suited to your needs, let’s look at the advantages of both new and resale homes.

WHY BUY A RESALE HOME, BANK OWNED OR SHORT SALE?(PreviouslyOwned)Housing styles have changed with time, and you might favor more traditional layouts and features. Older houses and neighborhoods may have more character and charm. The trees are full-grown, and the neighbors can tell you all about your new hometown. Here are some other advantages:

•Resalehomesmayprovidemoreopportunitiesforhomeimprovements•Theytypicallyhavemorelandthannewerpropertiesduetochangesinland-usepatterns•Thehomesareofteninolder,moreconvenientmetroareasratherthanoutlyingsuburbs•Youcanusetheexistinghomeasabaseforbuildingauniqueproperty through modernization or expansion•Resalestendtobelessexpensivethannewpropertiesandmorelikelytocomecompletewithitemsthat may cost extra with a new home such as blinds, landscaping, built-ins, etc.•Sometimesresalehomesmayhavelowerpropertytaxrates–checkwithyourREALTOR®•Ownersusuallyaren’trequiredtopayforthelocalbondsthataresometimesassociatedwith new development, such as for schools, parks, or road or transportation improvements•Thesehomesoftenhavemoretraditionallayouts,whichmayincludesuchareas as formal living and dining rooms•Buyerscanmostlikelypurchasealargerhomeforthesamemoneywitha resale than with new construction

CLOSING THE AMERICAN DREAM.

WHY BUY A NEW HOME?Perhaps you love the idea that you can be a home’s very first owner. Everything is new and shiny, the neighbors areprobablyalsojustmovingin,andyoucancustomizethefloorplanandcolors.Buyinganewhomecanbefun and exciting. Here are some other advantages:

• New homes are built with new materials and appliances, so less maintenance is typically required than with resale homes

• They often possess more safety features and fewer health hazards to conform to today’s building codes

• Many homebuilders offer warranties in case certain problems develop over time• Thehome’smajorappliancesandsystemsalsotypicallyincludemanufacturers’warranties• They typically feature modern architecture and layout such as great rooms, bigger closets, and

additional bathrooms, which often replace the formal dining and/or living rooms of older homes • New homes are usually well-insulated due to better windows, more efficient heating and cooling

equipment, and greater use of insulation• The homes are often made with materials requiring less maintenance, such as aluminum siding,

vinyl windows, and pressure-treated wood decks that resist rot and insects• They can be easier to customize than resale homes since you can choose many details ranging

from floor plans and paint colors to faucets and light fixtures• New homes are more apt to be wired with new technologies in mind, such as being pre-wired for

multiple phone lines, high-speed Internet connections, extra cable or satellite outlets and surround sound speaker systems

As you can see, both new homes and resale homes offer significant, but very different, advantages. Keep in mind that the real question shouldn’t be about whether to buy a new or used home. It’s more about finding which individual property will best meet the needs of you and your family.

CLOSING THE AMERICAN DREAM.

YOU’VE FOUND YOUR NEW HOME – NOW WHAT?After you have an accepted contract on a home, you or your REALTOR® should contact your loan officer to provide them with the following information:

1. The full property address.

2. Closing date as per contract.A legible copy of the contract and all counter offers that have the full property address and closing date specified. Get this to your lender as soon as possible – your REALTOR® should do this but if you are working without one, do this yourself.

3. If you are purchasing a property with a Home Owners Association (HOA), you should have the name of the HOA as well as the address of the specific association with a contact person, and contact number for the association.

NOTE: Not having the above information upfront can slow the registration or processing of your loan. If working with a REALTOR® they can provide this information for you.

If your loan was approved with conditions it is very important to know what the conditions of your loan are. Write down the conditions you are responsible for. Such as:

1. Asset verification.2. Income verification.3. Credit conditions.4. Any other personal conditions that you are able to provide right away.

After you have registered your loan with your loan officer you should receive a loan package within 3 business days. During that time you should have prepared the conditions you received from your loan officer and have them ready to be returned.

NOTE: Getting the information to your loan officer as quickly as possible is a major factor in getting your loan closed on time and locking in interest rates. If youwould like toorneed tochange the loan type (30year fixed,5/1ARM,etc.)atanytime,callyourloanofficerfortheirmortgageadviceandnotifyyourREALTOR® to take the steps you need to revise your existing program. Remember always get it in writing and assume the loan process could start all over again.

When you receive your loan package it is very important to return the completed package and requested information as soon as possible. Review the loan documentation thoroughly and sign where it is indicated. You should receive a copy of all documentation in the loan package for your file. Sign the documentation and input

CLOSING THE AMERICAN DREAM.

your prepared conditions and return the package to the lender. Your package will also have the name of your processor. You should contact your processor as soon as you receive the package if you have any questions. Introduce yourself and inform them of when the package will be returned.

Yourprocessorworkswithyourloanofficerforthesamemortgagecompanyanditistheprocessor’sjobtoprepare your loan to submit to underwriting. The loan processor will inform you of any additional information that is needed in order to move the process forward.

It is very important to keep your REALTOR® informed of any communication with the processor as well as your loan officer and your American Title Service Agency escrow officer. If there is a delay, your REALTOR® can assist you.

When your loan is going through the underwriting process, make sure you are available to speak with the processor throughout your underwriting process, since things can change daily and getting necessary items in a timely manner is key to getting your loan closed on time.

Finally, your closing. You should verify that you are ready for closing 10 days prior to your scheduled closing date. Make sure that the processor has scheduled the closing with American Title Service Agency and that your loan has been fully processed and underwriter reviewed. Your loan when approved for funding, gives the seller the comfort of knowing that you are totally approved for your loan. Please keep in mind failing to communicate with your lender, agent and escrow officer can cause you to lose your home and in some cases your earnest money deposit!

CLOSING THE AMERICAN DREAM.

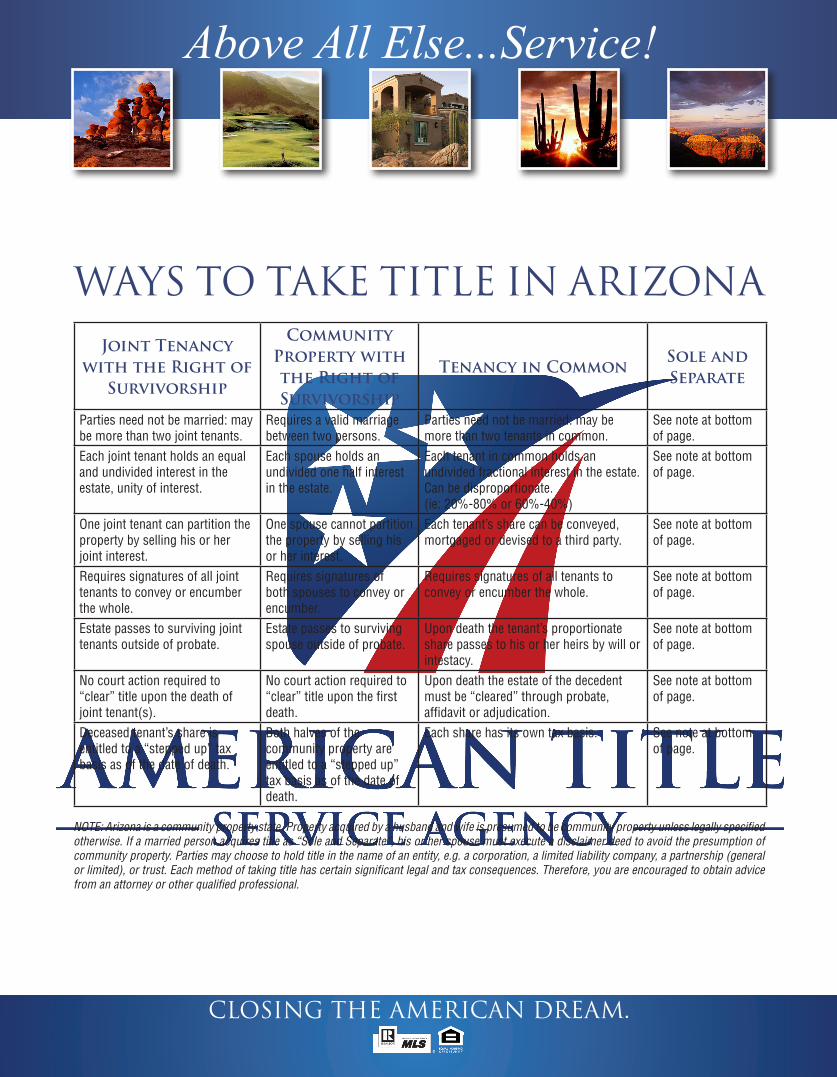

WAYS TO TAKE TITLE IN ARIZONAJoint Tenancy

with the Right ofSurvivorship

CommunityProperty with the Right ofSurvivorship

Tenancy in CommonSole andSeparate

Parties need not be married: may bemorethantwojointtenants.

Requires a valid marriage between two persons.

Parties need not be married: may be more than two tenants in common.

See note at bottomof page.

Eachjointtenantholdsanequaland undivided interest in the estate, unity of interest.

Each spouse holds an undivided one half interest in the estate.

Each tenant in common holds an undivided fractional interest in the estate. Can be disproportionate. (ie:20%-80%or60%-40%)

See note at bottomof page.

Onejointtenantcanpartitiontheproperty by selling his or herjointinterest.

One spouse cannot partition the property by selling his or her interest.

Each tenant’s share can be conveyed, mortgaged or devised to a third party.

See note at bottomof page.

Requiressignaturesofalljointtenants to convey or encumberthe whole.

Requires signatures of both spouses to convey or encumber.

Requires signatures of all tenants to convey or encumber the whole.

See note at bottomof page.

Estatepassestosurvivingjointtenants outside of probate.

Estate passes to surviving spouse outside of probate.

Upon death the tenant’s proportionate share passes to his or her heirs by will or intestacy.

See note at bottomof page.

No court action required to “clear”titleuponthedeathofjointtenant(s).

No court action required to “clear”titleuponthefirstdeath.

Upon death the estate of the decedent mustbe“cleared”throughprobate,affidavitoradjudication.

See note at bottomof page.

Deceased tenant’s share is entitledtoa“steppedup”taxbasis as of the date of death.

Both halves of the community property are entitledtoa“steppedup”tax basis as of the date of death.

Each share has its own tax basis. See note at bottomof page.

NOTE: Arizona is a community property state. Property acquired by a husband and wife is presumed to be community property unless legally specified otherwise. If a married person acquires title as “Sole and Separate”, his or her spouse must execute a disclaimer deed to avoid the presumption of community property. Parties may choose to hold title in the name of an entity, e.g. a corporation, a limited liability company, a partnership (general or limited), or trust. Each method of taking title has certain significant legal and tax consequences. Therefore, you are encouraged to obtain advice from an attorney or other qualified professional.

CLOSING THE AMERICAN DREAM.

MISCELLANEOUS INFORMATIONAPPRAISALSAn appraisal is a written estimate of a property’s market value completed by an appraiser. The value is based upon a market analysis of the prices of recent sales of similar properties in the area and the property’s physicalcondition. Usually, this requires an interior and exterior property inspection.

Why is an Appraisal Necessary?Lenders use appraisals to determine the buyer’s loan amount. The appraisal will be completed shortly after the buyer requests a mortgage.

Appraisals and Sales Prices•Iftheappraisedvalueishigherthanthesalesprice,thereisnoimpact.Thesalespricecannotberaised.•Whenthepropertyappraisesforalowervaluethanthesalesprice,thelowerappraisedvalueisusedtodetermine the loan amount. To complete the sale, the buyer may have to increase the down payment to make up the difference between the appraised value and the purchase price or you may have to negotiate a new sales price.

HOME INSPECTIONSAstandardpre-purchaseinspectioncoversahome’smajormechanicalsystems,electrical,plumbing,heating,cooling and its construction from roof to foundation, exterior to interior. Overall inspections generally do not cover soil, pools, wells, septic systems, building code violations or environmental hazards such as lead unless specifically requested.

REMEMBER REPAIRS OR REMEDIES ARE NEGOTIABLE; THEY ALSO CAN DERAIL A DEAL.

HOME WARRANTIESHome warranties offer advantages to both buyer and seller. Offering a home warranty gives the buyer a sense of security, knowing that they are protected after buying the property by paying only a deductible for certain repairsorreplacementofmajormechanicalsystemsinthehomesuchasheating,airconditioningandmajorappliances. There are a variety of plans available; we can give you information on the options, costs and providers in your specific area.

BENEFITS OF HOME WARRANTY TO THE BUYER•Warrantycoverageforyourmajorsystemsandbuiltinappliances•Protectsyourcashflow•Putsacompletenetworkofqualifiedservicetechniciansatyourservice•Lowdeductible

CLOSING THE AMERICAN DREAM.

WANTS and NEEDS ListWhile house-hunting, it is easy to get distracted if you choose to look at properties that donot meet your criteria. Stay focused on what’s most important to you.

What we WANT in a home What we NEED in a home

1.2.3.4.5.6.7.8.9.10.11.12.13.14.15.16.17.18.19.20.

CLOSING THE AMERICAN DREAM.

HOUSE HUNTING EVALUATIONVery often it is difficult to remember which house had the great kitchen, pool or master bath. We have provided this evaluation form so that you keep track of the homes you have seen and what your thoughts are on them.Youcanusethisformtopickyour“Top5”andeliminatetherest.Intoday’smarket,itisreasonabletoassumethat the seller may have another offer when you submit your offer. Keeping track of the homes that come close toyour“dreamhome”willenableyoutochangedirectionsquicklyifnecessary.

YOUR TOP FIVE PICKSUse this Evaluation Form to rate the home according to it’s benefits and features that are important to you.

features home #1 home #2 home #3 home #4 home #5PropertyAddress

ArchitecturalStyle

Living RoomDining Room

Kitchen# of Bedrooms# of Bathrooms

AdditionalRooms

Floor PlanAdditionalFeaturesGarageLot /

LandscapingUtility

InformationSuitableLocation

Does HomeMeet Needs?

CLOSING THE AMERICAN DREAM.

Seller’s Guide

CLOSING THE AMERICAN DREAM.

SELLING A HOMEIT PAYS TO WORK WITH A REALTOR® Without the professional guidance and expertise of a REALTOR®, selling a home can often entail many unnecessary complications. The following information, as prepared by the National Association of REALTORS®, best describes the many benefits of contacting a professional REALTOR® to handle all your real estate needs. The term REALTOR® is a registered, collective membership mark which identifies real estate professionals who are members of the National Association of REALTORS® and abide by its strict Code of Ethics. A REALTOR® is bound by a Code of Ethics and pledges to protect and promote the interest of their seller by providing fair treatment for all parties involved in the transaction.

Here are some ways a REALTOR® can help you sell your home:

• PROMOTION• VIEWING• NETWORKING

WORKING WITH YOU BY: •Conferringwithyouregardingwhenyouwanttoplaceyourhomeonthemarket•Establishingasalepricebasedonthefollowing: •Researchofcomparableproperties •Consideringthecurrentlocalmarketconditions•Establishingyourprobablenetproceeds•Advertisingyourhomeandmakingsuggestionsonwhatyoucandotomakeyourpropertymoresellable•Reviewingthenecessarypaperworkwithyou

NEGOTIATING THE CONTRACT BY: •Reviewingthecontractandyourobligations•Explainingcontingenciesandreleaseclauses•Explainingthelegaldisclosurerequirements•Explainingtheramificationsofpestcontrolinspections/reports•Explainingyourresponsibilitiesregardingtheconditionoftheproperty•Examiningofferscloselyandexplainingthereasonsbehindapossiblecounter-offer

MANAGING AND CLOSING ESCROW BY: •Followingcloselytheprogressofthebuyer’sloanandcoordinatingthepayoffofyourexistingloan•Facilitatingtheappraisalprocess•Stayinginconstantcommunicationwiththebuyer’sagenttoensureasmoothescrowclosing•Closelymonitoringcontingencyremovaldatesanddiscussingthesewithyou•Coordinatingthedetailsofthetransactionwiththeescrowofficer•Makingsureyougetyourcheckandsettlementdocumentspromptlyafterclosing

CLOSING THE AMERICAN DREAM.

SHOWING YOUR HOME First impressions are the most powerful sales tools. Emotion plays a tremendous part in creating an interestinyourhomefromapotentialbuyer.Makecertainyourhomeputsits“bestfootforward”andthat you follow the time-tested rules and behavior that will enhance the likelihood of a sale.

OUTSIDE • Invest in landscaping where it can be seen at first sight. A well manicured lawn, neatly clipped shrubs

and clean walks create a good first impression • An extra shot of fertilizer, in season, will make your grass look lush and green• Cut back overgrown shrubbery that looks unkempt and keeps light out of your house• Paint your house if necessary. This can probably do more for sales appeal than any other factor. If you

decide against painting, at least consider painting front shutters or window and door trim• Walks should be free of leaves, weeds, dirt and debris• Inspect the roof and gutters, and replace any missing shingles• Consider putting flowers outside the front door• Repaint or stain the front door• Put a bright coat of paint on your mailbox• Put a new doormat out front

KITCHEN

•This is the most important room in the house. Make it bright and attractive. Clean your cabinets inside and out

• Clean the vent hood, the range/oven and the sink • Scrub the kitchen floor • Remove any extra appliances and/or knickknacks on the counters that you don’t use every day

BATHROOM• Repair any dripping faucets; they discolor sinks and suggest faulty plumbing• Keep fresh towels in the bathroom• Scrub the toilet-shower, tub and caulk if necessary• Use drain opener to unclog any slow drains

LIVING AREAS • Have all drywall in good shape. Cracks and nail holes are easy to fix • Check ceiling and ceiling fans for dirt• When painting or redecorating, stick to conventional colors

CLOSING THE AMERICAN DREAM.

• Replace faded curtains or bedspreads • If you have a fireplace, clean it out and lay some logs inside • Wash your windows inside and out• Replace any broken windows• Replace or fix any torn screens • Make sure all windows open and close easily• Check all light bulbs and replace if necessary • Check light switches and plugs to make sure they work • Make sure all floors are clean• Straighten all closets; well ordered closets show space is ample • Repair sliding doors that stick• Clean the air return vents and put in new filters

GARAGE, ATTIC AND DRIVEWAY• Clean and organize the garage and attic, dispose of or donate anything you will not take with you • Repairanymajorcracksasnecessary• Clean any oil stains • Check garage door and service if necessary

WHEN YOUR HOUSE IS BEING SHOWN • Keep shades open to let in light; this makes your rooms look larger • Have your home well-lit and interior doors open for showing• At night, turn on porch light and any exterior lighting • Make sure all beds are made and rooms cleaned daily• Make sure all dirty dishes are in the dishwasher, not in the sink or on the counters • Keep toys in the kids’ room• Keep radio/stereo/TV off • Try to run some errands when the house is being shown • If you are home, do not negotiate directly with the buyers• Refer any inquiries about your home to your REALTOR®• Take your pets for a walk when your house is being shown• Let the REALTOR® show your house and do not tag along

CLOSING THE AMERICAN DREAM.

INSPECTIONSThe standard real estate purchase contract used in the State of Arizona contains a provision that allows the buyer to physically inspect the property being purchased, either by himself or by a professional inspector or inspectors, during the time frame as described in your purchase contract. It is the seller’s obligation to provide the buyer access to the property during this inspection period for whatever inspections the buyer requires. Below is a list of common types of inspections.

STRUCTURAL PEST CONTROL •Todetermineanyactiveinfestationbywooddestroyingorganisms.•Todeterminewhetherthereisanyearthtowoodcontact, cellulose debris or faulty grades on the property.

PHYSICAL INSPECTION •This inspectioncanencompass inspectionof the roof, plumbing, electrical, heatingandanyother accessible area of the property. •Adetailedreportorreportswillbewrittenbytheinspectororinspectorswithrecommendationsfor repairs, and same will be delivered to the buyer. Subsequently the buyer will request of the seller any repairs that the buyer wishes the seller to be responsible for. If the seller agrees to the repairs, they would need to be completed prior to the close of escrow.

OTHER COMMON INSPECTIONS MIGHT INCLUDE: •WellandSeptic•Hazardousmaterials•Chimney•HeatingandCooling•Survey•ZoningandBuildingpermitcompliance•StructuralEngineering

HOME WARRANTIES Home Warranties are insurance policies designed to protect a seller during the listing period and a buyer for oneyearafterthecloseofescrow,againstrepaircostsformechanicalsystemsandmajorappliances.Thecostof a home warranty policy is a one time fee which either the buyer or the seller can pay at the close of escrow and which is renewable annually. There are a variety of home warranty companies and plans. The plans vary according to the optional coverage chosen by the insured which might include, but not be limited to heating, air conditioning, dishwasher, washer, dryer, refrigerator, garbage disposals, pool and/or spa equipment. A few of the benefits of a home warranty are listed as follows:

•Replacementorrepairofmajororminorplumbing,heatingorelectricalproblems during the policy period at a nominal service fee per incident. •Afullnetworkofqualifiedtechniciansatyourservice.•Protectionofyourbudgetagainstunexpectedexpensesforrepairsorreplacementsof systems in your home for the first year of ownership or subsequent years if renewed.

CLOSING THE AMERICAN DREAM.

THE SELLER’S EIGHT MOST FREQUENTLY ASKED QUESTIONS Q. When do I get my proceeds check?A. On the date of recording, you may request that your escrow officer either issue a check for your

proceeds or wire the funds directly into your bank account.Q. Why do I have to pay interest on my loan pay-off past the day of recording?A. Your lender continues to accrue interest to the date that they post your loan as being paid in full. Q. When do I get a refund from my impound account?A. After your escrow officer sends your pay-off check to your existing lender, you can expect to get

impoundaccountbackdirectfromyourlenderwithin30-60days.Ifyouhaveanyquestionsafterthattime, we suggest calling your lender.

Q. When do I cancel homeowners/fire insurance?A. Please do not cancel your insurance until you have confirmed with your escrow officer that your

transaction has closed.Q. Why does my escrow officer require that I complete a 1099 form?A. A 1099 form is the reporting form adopted by the IRS for submitting the information required by law.

Under guidelines established by the IRS, sellers of real property are required to have their sales price reported on the 1099 form.

Q. What is a Statement of information?A. Statements of information provide title companies with the information they need to distinguish the

buyers and sellers of real property from others with similar names, for the issuance of title insurance at close of escrow. After identifying the true buyers and sellers, title companies may disregard the judgements,liensorothermattersonthepublicrecordsundersimilarnames.

Q. I don’t understand tax pro-rations. How do they work?A. Each year on January 1st, the lien of that year’s property taxes attach to the land, pursuant to Arizona

Law. However, the lien is not due and payable until October 1st of that year for the first half of that year’s bill and the second half of that year’s bill is not due until March 1st of the following year. Pro-rations are done to reimburse the buyer for the portion of the year that the seller has owned the property and has not yet paid taxes.

Q. What will I need to take with me to American Title Service Agency to signmy documents for closing?

A. Take one of the following: Arizona Drivers License, Arizona ID card, Military ID or Passport.

CLOSING THE AMERICAN DREAM.

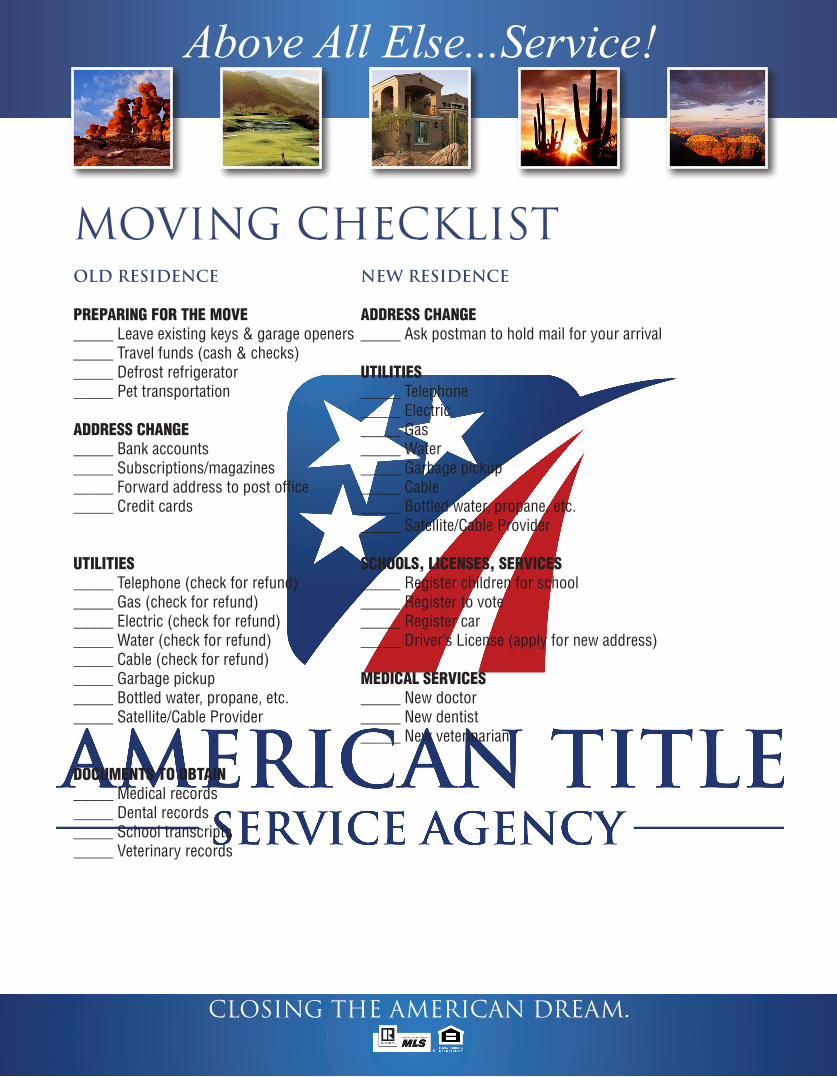

MOVING CHECKLISTOLD RESIDENCE NEW RESIDENCE

PREPARING FOR THE MOVE ADDRESS CHANGE_____ Leave existing keys & garage openers _____ Ask postman to hold mail for your arrival_____Travelfunds(cash&checks)_____ Defrost refrigerator UTILITIES_____ Pet transportation _____ Telephone _____ ElectricADDRESS CHANGE _____ Gas_____ Bank accounts _____ Water_____ Subscriptions/magazines _____ Garbage pickup _____ Forward address to post office _____ Cable_____ Credit cards _____ Bottled water, propane, etc. _____ Satellite/Cable Provider

UTILITIES SCHOOLS, LICENSES, SERVICES_____Telephone(checkforrefund) _____Registerchildrenforschool_____Gas(checkforrefund) _____Registertovote_____Electric(checkforrefund) _____Registercar_____Water(checkforrefund) _____Driver’sLicense(applyfornewaddress)_____Cable(checkforrefund)_____ Garbage pickup MEDICAL SERVICES_____ Bottled water, propane, etc. _____ New doctor_____ Satellite/Cable Provider _____ New dentist _____ New veterinarian

DOCUMENTS TO OBTAIN _____ Medical records_____ Dental records_____ School transcripts_____ Veterinary records

CLOSING THE AMERICAN DREAM.

NOTES...

CLOSING THE AMERICAN DREAM.

FORMS & DOCUMENTSThe AAR purchase contract used for the purchase of resale homes is included on the following pages.

CLOSING THE AMERICAN DREAM.

SAMPLE

Page 1 of 9

Buyer Attachment • Updated: February 2011Copyright © 2011 Arizona Association of REALTORS®. All rights reserved.

ATTENTION BUYER!You are entering into a legally binding agreement.

1. Read the entire contract before you sign it.

2. Review the Residential Seller’s Property Disclosure Statement (See Section 4a). • This information comes directly from the Seller. • Investigate any blank spaces, unclear answers or any other information that is important to you.

3. Review the Inspection Paragraph (see Section 6a).If important to you, hire a qualified:

• Mold inspector • Roof inspector • Pest inspector • Pool inspector • Heating/cooling inspector

Verify square footage (see Section 6b)Verify the property is on sewer or septic (see Section 6f)

4. Confirm your ability to obtain insurance and insurability of the propertyduring the inspection period with your insurance agent (see Sections 6a and 6e).

5. Apply for your home loan now, if you have not done so already, and provideyour lender with all requested information (see Section 2f).It is your responsibility to make sure that you and your lender deliver the necessary funds to escrow insufficient time to allow escrow to close on the agreed upon date. Otherwise, the Seller may cancel the contract.

6. Read the title commitment within five days of receipt (see Section 3c).

7. Read the CC&R’s and all other governing documents within five days of receipt(see Section 3c), especially if the home is in a homeowner’s association.

8. Conduct a thorough final walkthrough (see Section 6m). If the property is unacceptable, speak up. After the closing may be too late.

You can obtain information through the Buyer’s Advisory at http://www.aaronline.com.

Remember, you are urged to consult with an attorney, inspectors, and experts of your choice in any areaof interest or concern in the transaction. Be cautious about verbal representations, advertising claims, andinformation contained in a listing. Verify anything important to you.

Document updated:February 2011BUYER ATTACHMENT

This attachment should be given to the Buyer prior to the submissionof any offer and is not part of the Residential Resale Real Estate PurchaseContract’s terms.

Buyer’s Check List4

CLOSING THE AMERICAN DREAM.

Residential Resale Real Estate Purchase Contract • Updated: February 2011Copyright © 2011 Arizona Association of REALTORS®. All rights reserved.

Page 1 of 9

>>

1a.

1b.

1c.

1d.

1e.

1f.

1g.

1. PROPERTY

BUYER: BUYER’S NAME(S)

SELLER: or n as identified in section 9c.SELLER’S NAME(S)

Buyer agrees to buy and Seller agrees to sell the real property with all improvements, fixtures, and appurtenances thereon or incidental thereto, plus the personal property described herein (collectively the “Premises”).

Premises Address: Assessor’s #:

City: County: AZ, Zip Code:

Legal Description:

$ Full Purchase Price, paid as outlined below

$ Earnest money

$

$

Close of Escrow: Close of Escrow (“COE”) shall occur when the deed is recorded at the appropriate county recorder’s office. Buyerand Seller shall comply with all terms and conditions of this Contract, execute and deliver to Escrow Company all closing documents,and perform all other acts necessary in sufficient time to allow COE to occur on , 20 (“COE Date”). If Escrow Company or recorder’s office is closed on COE Date,

MONTH DAY YEAR

COE shall occur on the next day that both are open for business.

Buyer shall deliver to Escrow Company a cashier’s check, wired funds or other immediately available funds to pay any downpayment, additional deposits or Buyer’s closing costs, and instruct the lender, if applicable, to deliver immediately available funds toEscrow Company, in a sufficient amount and in sufficient time to allow COE to occur on COE Date.

Possession: Seller shall deliver possession, occupancy, existing keys and/or means to operate all locks, mailbox, security system/alarms, and all common area facilities to Buyer at COE or n .Broker(s) recommend that the parties seek appropriate counsel from insurance, legal, tax, and accounting professionals regardingthe risks of pre-possession or post-possession of the Premises.

Addenda Incorporated: n AS IS n Additional Clause n Assumption and Carryback n Buyer Contingency n Domestic Water Well

n H.O.A. n Lead-Based Paint Disclosure n On-site Wastewater Treatment Facility n Short Sale

n Other:

Fixtures and Personal Property: Seller agrees that all existing fixtures on the Premises, and any existing personal propertyspecified herein, shall be included in this sale, including the following:

• free-standing range/oven • light fixtures • draperies and other window coverings• ceiling fans • towel, curtain and drapery rods • shutters and awnings• attached floor coverings • flush-mounted speakers • water-misting systems • window and door screens, sun screens • storm windows and doors • solar systems • garage door openers and controls • attached media antennas/ • mailbox• outdoor landscaping, fountains, and lighting satellite dishes • central vacuum, hose, and attachments• pellet, wood-burning or gas-log stoves • attached fireplace equipment • built-in appliances • storage sheds • timers

1.

2.

3.4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.16.17.

18.

19.

20. 21.22.

23.24.25.26.

27.28.29.

30.31.32.33.34.35.36.37.38.39.

PAGE 1 of 2

Document updated:February 2011

RESIDENTIAL RESALE REAL ESTATEPURCHASE CONTRACT

Page 1 of 9

SAMPLE

CLOSING THE AMERICAN DREAM.

Residential Resale Real Estate Purchase Contract >>

Page 2 of 9

Residential Resale Real Estate Purchase Contract • Updated: February 2011Copyright © 2011 Arizona Association of REALTORS®. All rights reserved.

Page 2 of 9

>>

If owned by the Seller, the following items also are included in this sale: • pool and spa equipment (including any mechanical or other cleaning systems)• security and/or fire systems and/or alarms • water softeners • water purification systems

Additional existing personal property included in this sale (if checked): n refrigerator n washer n dryer as described:

n Other:

Additional existing personal property included shall not be considered part of the Premises and shall be transferred with no monetaryvalue, and free and clear of all liens or encumbrances.

Fixtures and leased items NOT included:

IF THIS IS AN ALL CASH SALE, GO TO SECTION 3.

2. FINANCING Pre-Qualification: A completed AAR Pre-Qualification Form n is n is not attached hereto and incorporated herein by reference.

Loan Contingency: Buyer’s obligation to complete this sale is contingent upon Buyer obtaining loan approval for the loan describedin the AAR Loan Status Update (“LSU”) form without Prior to Document (“PTD”) conditions no later than three (3) days prior to theCOE Date. If Buyer is unable to obtain loan approval without PTD conditions, Buyer shall deliver a notice of the inability to obtainloan approval without PTD conditions to Seller or Escrow Company no later than three (3) days prior to the COE Date.

Unfulfilled Loan Contingency: This Contract shall be cancelled and Buyer shall be entitled to a return of the Earnest Money if afterdiligent and good faith effort, Buyer is unable to obtain loan approval without PTD conditions no later than three (3) days prior to theCOE Date. Buyer acknowledges that prepaid items paid separately from earnest money are not refundable.

Interest Rate / Necessary Funds: Buyer agrees that (i) the inability to obtain loan approval due to the failure to lock the interestrate and “points” by separate written agreement with the lender during the Inspection Period or (ii) the failure to have the downpayment or other funds due from Buyer necessary to obtain the loan approval without conditions and close this transaction is notan unfulfilled loan contingency.

Loan Status Update: Buyer shall deliver to Seller the LSU with at a minimum lines 1-40 completed describing the current statusof the Buyer’s proposed loan within five (5) days after Contract acceptance and instruct lender to provide an updated LSU toBroker(s) and Seller upon request.

Loan Application: Unless previously completed, during the Inspection Period, Buyer shall (i) complete, sign and deliver to thelender a loan application and grant lender permission to access Buyer’s Trimerged Residential Credit Report; and (ii) provideto lender all initial requested signed disclosures and Initial Requested Documentation listed in the LSU on lines 32-35.

Loan Processing During Escrow: Buyer agrees to diligently work to obtain the loan and will promptly provide the lender with alladditional documentation required. Buyer shall sign all loan documents no later than three (3) days prior to the COE Date.

Type of Financing: n Conventional n FHA n VA n USDA n Assumption n Seller Carryback n (If financing is to be other than new financing, see attached addendum.)

Loan Costs: All costs of obtaining the loan shall be paid by the Buyer, unless otherwise provided for herein.

Seller Concessions (If Any): In addition to the other costs Seller has agreed to pay herein, Seller agrees to pay up to %of the Purchase Price or $ for Buyer’s loan costs including pre-paids, impounds and Buyer’s title / escrow closing costs.

VA Loan Costs: In the event of a VA loan, Seller agrees to pay the escrow fee and up to $ of loan costs notpermitted to be paid by the Buyer, in addition to the other costs Seller has agreed to pay herein, including Seller’s Concessions.

Changes: Buyer shall immediately notify Seller of any changes in the loan program, financing terms, or lender described in thePre-Qualification Form if attached hereto or LSU provided within five (5) days after Contract acceptance and shall only make anysuch changes without the prior written consent of Seller if such changes do not adversely affect Buyer’s ability to obtain loanapproval without PTD conditions, increase Seller’s closing costs, or delay COE.

Appraisal Contingency: Buyer’s obligation to complete this sale is contingent upon an appraisal of the Premises acceptable to lender forat least the purchase price. If the Premises fail to appraise for the purchase price in any appraisal required by lender, Buyer has five (5)days after notice of the appraised value to cancel this Contract and receive a refund of the Earnest Money or the appraisal contingencyshall be waived.

Appraisal Fee(s): Appraisal Fee(s), when required by lender, shall be paid by n Buyer n Seller n Other Appraisal Fee(s) n are n are not included in Seller Concessions, if applicable.

40.41.42.43.44.

45.

46.

47.

48.

49.50.51.

52.

53.

54.

55.56.57.58.

59.60.61.

62.63.64.65.

66.67.68.

69.70.71.

72.73.

74.75.

76.

77.78.

79.80.

81.82.83.84.

85.86.87. 88.

89.90.

2a.

2b.

2c.

2d.

2e.

2f.

2g.

2h.

2i.

2j.

2k.

2l.

2m.

2n.

SAMPLE

CLOSING THE AMERICAN DREAM.

Residential Resale Real Estate Purchase Contract >>

Page 3 of 9

Residential Resale Real Estate Purchase Contract • Updated: February 2011Copyright © 2011 Arizona Association of REALTORS®. All rights reserved.

Page 3 of 9

>>

3. TITLE AND ESCROW Escrow: This Contract shall be used as escrow instructions. The Escrow Company employed by the parties to carry out theterms of this Contract shall be:

“ESCROW/TITLE COMPANY”

ADDRESS CITY STATE ZIP

EMAIL PHONE FAX

Title and Vesting: Buyer will take title as determined before COE. Taking title may have significant legal, estate planning and taxconsequences. Buyer should obtain legal and tax advice.

Title Commitment and Title Insurance: Escrow Company is hereby instructed to obtain and deliver to Buyer and Seller directly,addressed pursuant to 8t and 9c or as otherwise provided, a Commitment for Title Insurance together with complete and legible copiesof all documents that will remain as exceptions to Buyer’s policy of Title Insurance (“Title Commitment”), including but not limited toConditions, Covenants and Restrictions (“CC&Rs”); deed restrictions; and easements. Buyer shall have five (5) days after receipt of theTitle Commitment and after receipt of notice of any subsequent exceptions to provide notice to Seller of any items disapproved. Sellershall convey title by warranty deed, subject to existing taxes, assessments, covenants, conditions, restrictions, rights of way, easementsand all other matters of record. Buyer shall be provided at Seller’s expense an American Land Title Association (“ALTA”) Homeowner’sTitle Insurance Policy, or if not available, an ALTA Residential Title Insurance Policy (“Plain Language”/“1-4 units”) or, if not available, aStandard Owner’s Title Insurance Policy, showing title vested in Buyer. Buyer may acquire extended coverage at Buyer’s own additionalexpense. If applicable, Buyer shall pay the cost of obtaining the ALTA Lender Title Insurance Policy.

Additional Instructions: (i) Escrow Company shall promptly furnish notice of pending sale that contains the name and address of theBuyer to any homeowner’s association in which the Premises is located. (ii) If the Escrow Company is also acting as the title agencybut is not the title insurer issuing the title insurance policy, Escrow Company shall deliver to the Buyer and Seller, upon deposit offunds, a closing protection letter from the title insurer indemnifying the Buyer and Seller for any losses due to fraudulent acts or breachof escrow instructions by the Escrow Company. (iii) All documents necessary to close this transaction shall be executed promptly bySeller and Buyer in the standard form used by Escrow Company. Escrow Company shall modify such documents to the extentnecessary to be consistent with this Contract. (iv) Escrow Company fees, unless otherwise stated herein, shall be allocated equallybetween Seller and Buyer. (v) Escrow Company shall send to all parties and Broker(s) copies of all notices and communicationsdirected to Seller, Buyer and Broker(s). (vi) Escrow Company shall provide Broker(s) access to escrowed materials and informationregarding the escrow. (vii) If an Affidavit of Disclosure is provided, Escrow Company shall record the Affidavit at COE.

Tax Prorations: Real property taxes payable by the Seller shall be prorated to COE based upon the latest tax information available.

Release of Earnest Money: In the event of a dispute between Buyer and Seller regarding any Earnest Money deposited withEscrow Company, Buyer and Seller authorize Escrow Company to release Earnest Money pursuant to the terms and conditions ofthis Contract in its sole and absolute discretion. Buyer and Seller agree to hold harmless and indemnify Escrow Company againstany claim, action or lawsuit of any kind, and from any loss, judgment, or expense, including costs and attorney fees, arising from orrelating in any way to the release of Earnest Money.

Prorations of Assessments and Fees: All assessments and fees that are not a lien as of the COE, including homeowner’sassociation fees, rents, irrigation fees, and, if assumed, insurance premiums, interest on assessments, interest on encumbrances, and service contracts, shall be prorated as of COE or n Other:

Assessment Liens: The amount of any assessment, other than homeowner’s association assessments, that is a lien as of the COE, shall be n paid in full by Seller n prorated and assumed by Buyer. Any assessment that becomes a lien after COE is the Buyer’s responsibility.

IRS and FIRPTA Reporting: Seller agrees to comply with IRS reporting requirements. If applicable, Seller agrees to complete, sign,and deliver to Escrow Company a certificate indicating whether Seller is a foreign person or a non-resident alien pursuant to theForeign Investment in Real Property Tax Act (“FIRPTA”). Buyer and Seller acknowledge that if the Seller is a foreign person, theBuyer must withhold a tax equal to 10% of the purchase price, unless an exemption applies.

91.92.

93.

94.

95.

96.97.

98.99.

100.101.102.103.104.105.106.107.

108.109.110.111.112.113.114.115.116.117.

118.

119.120.121.122.123.

124.125.126.

127.128.129.

130.131.132.133.

3a.

3b.

3c.

3d.

3e.

3f.

3g.

3h.

3i.SAMPLE

CLOSING THE AMERICAN DREAM.

Residential Resale Real Estate Purchase Contract >>

Page 4 of 9

Residential Resale Real Estate Purchase Contract • Updated: February 2011Copyright © 2011 Arizona Association of REALTORS®. All rights reserved.

Page 4 of 9

>>

4. DISCLOSURE Seller Property Disclosure Statement (“SPDS”): Seller shall deliver a completed AAR Residential SPDS form to the Buyerwithin five (5) days after Contract acceptance. Buyer shall provide notice of any SPDS items disapproved within the InspectionPeriod or five (5) days after receipt of the SPDS, whichever is later.

Insurance Claims History: Seller shall deliver to Buyer a written five-year insurance claims history regarding Premises (or a claimshistory for the length of time Seller has owned the Premises if less than five years) from Seller’s insurance company or an insurancesupport organization or consumer reporting agency, or if unavailable from these sources, from Seller, within five (5) days after Contractacceptance. (Seller may obscure any reference to date of birth or social security number from the document). Buyer shall providenotice of any items disapproved within the Inspection Period or five (5) days after receipt of the claims history, whichever is later.

Lead-Based Paint Disclosure: If the Premises were built prior to 1978, the Seller shall: (i) notify the Buyer of any known lead-basedpaint (“LBP”) or LBP hazards in the Premises; (ii) provide the Buyer with any LBP risk assessments or inspections of the Premises inthe Seller’s possession; (iii) provide the Buyer with the Disclosure of Information on Lead-based Paint and Lead-based PaintHazards, and any report, records, pamphlets, and/or other materials referenced therein, including the pamphlet “Protect Your Familyfrom Lead in Your Home” (collectively “LBP Information”). Buyer shall return a signed copy of the Disclosure of Information on Lead-Based Paint and Lead-Based Paint Hazards to Seller prior to COE.

n LBP Information was provided prior to Contract acceptance and Buyer acknowledges the opportunity to conduct LBP risk assessments or inspections during Inspection Period.

n Seller shall provide LBP Information within five (5) days after Contract acceptance. Buyer may within ten (10) daysor days after receipt of the LBP Information conduct or obtain a risk assessment or inspection of the Premises for the presence of LBP or LBP hazards (“Assessment Period”). Buyer may within five (5) days after receipt of the LBP Information or five(5) days after expiration of the Assessment Period cancel this Contract.

Buyer is further advised to use certified contractors to perform renovation, repair or painting projects that disturb lead-based paint inresidential properties built before 1978 and to follow specific work practices to prevent lead contamination.

If Premises were constructed prior to 1978, (BUYER’S INITIALS REQUIRED) BUYER BUYER

If Premises were constructed 1978 or later, (BUYER’S INITIALS REQUIRED) BUYER BUYER

Affidavit of Disclosure: If the Premises is located in an unincorporated area of the county, and five or fewer parcels of propertyother than subdivided property are being transferred, the Seller shall deliver a completed Affidavit of Disclosure in the form requiredby law to the Buyer within five (5) days after Contract acceptance. Buyer shall provide notice of any Affidavit of Disclosure itemsdisapproved within the Inspection Period or five (5) days after receipt of the Affidavit of Disclosure, whichever is later.

Changes During Escrow: Seller shall immediately notify Buyer of any changes in the Premises or disclosures made herein, inthe SPDS, or otherwise. Such notice shall be considered an update of the SPDS. Unless Seller is already obligated by Section 5aor otherwise by this Contract or any amendments hereto, to correct or repair the changed item disclosed, Buyer shall be allowedfive (5) days after delivery of such notice to provide notice of disapproval to Seller.

5. WARRANTIES Seller Warranties: Seller warrants and shall maintain and repair the Premises so that at the earlier of possession or COE: (i) allheating, cooling, mechanical, plumbing, and electrical systems (including swimming pool and/or spa, motors, filter systems, cleaningsystems, and heaters, if any), free-standing range/oven, and built-in appliances will be in working condition; (ii) all other agreed uponrepairs and corrections will be completed pursuant to Section 6j; (iii) the Premises, including all additional existing personal propertyincluded in the sale, will be in substantially the same condition as on the date of Contract acceptance; and (iv) all personal propertynot included in the sale and all debris will be removed from the Premises.

Warranties that Survive Closing: Seller warrants that Seller has disclosed to Buyer and Broker(s) all material latent defects andany information concerning the Premises known to Seller, excluding opinions of value, which materially and adversely affect theconsideration to be paid by Buyer. Prior to the COE, Seller warrants that payment in full will have been made for all labor,professional services, materials, machinery, fixtures, or tools furnished within the 150 days immediately preceding the COE inconnection with the construction, alteration, or repair of any structure on or improvement to the Premises. Seller warrants that theinformation regarding connection to a sewer system or on-site wastewater treatment facility (conventional septic or alternative) iscorrect to the best of Seller’s knowledge.

Buyer Warranties: Buyer warrants that Buyer has disclosed to Seller any information that may materially and adversely affect theBuyer’s ability to close escrow or complete the obligations of this Contract. At the earlier of possession of the Premises or COE,Buyer warrants to Seller that Buyer has conducted all desired independent inspections and investigations and accepts the Premises.Buyer warrants that Buyer is not relying on any verbal representations concerning the Premises except disclosed as follows:

134.135.136.

137.138.139.140.141.

142.143.144.145.146.147.

148.149.

150.151.152.153.

154.155.

156.

157.

158.159.160.161.

162.163.164.165.

166.167. 168.169.170.171.

172.173.174.175.176.177.178.

179. 180.181.182.

183.184.

4a.

4b.

4c.

4d.

4e.

5a.

5b.

5c.SAMPLE

CLOSING THE AMERICAN DREAM.

Residential Resale Real Estate Purchase Contract >>

Page 5 of 9

Residential Resale Real Estate Purchase Contract • Updated: February 2011Copyright © 2011 Arizona Association of REALTORS®. All rights reserved.

Page 5 of 9

>>

6. DUE DILIGENCE Inspection Period: Buyer’s Inspection Period shall be ten (10) days or days after Contract acceptance. During theInspection Period Buyer, at Buyer’s expense, shall: (i) conduct all desired physical, environmental, and other types of inspectionsand investigations to determine the value and condition of the Premises; (ii) make inquiries and consult government agencies,lenders, insurance agents, architects, and other appropriate persons and entities concerning the suitability of the Premises and thesurrounding area; (iii) investigate applicable building, zoning, fire, health, and safety codes to determine any potential hazards,violations or defects in the Premises; and (iv) verify any material multiple listing service (“MLS”) information. If the presence of sexoffenders in the vicinity or the occurrence of a disease, natural death, suicide, homicide or other crime on or in the vicinity is amaterial matter to the Buyer, it must be investigated by the Buyer during the Inspection Period. Buyer shall keep the Premises freeand clear of liens, shall indemnify and hold Seller harmless from all liability, claims, demands, damages, and costs, and shall repairall damages arising from the inspections. Buyer shall provide Seller and Broker(s) upon receipt, at no cost, copies of all inspectionreports concerning the Premises obtained by Buyer. Buyer is advised to consult the Arizona Department of Real Estate BuyerAdvisory provided by AAR to assist in Buyer’s due diligence inspections and investigations.

Square Footage: BUYER IS AWARE THAT ANY REFERENCE TO THE SQUARE FOOTAGE OF THE PREMISES, BOTH THEREAL PROPERTY (LAND) AND IMPROVEMENTS THEREON, IS APPROXIMATE. IF SQUARE FOOTAGE IS A MATERIALMATTER TO THE BUYER, IT MUST BE INVESTIGATED DURING THE INSPECTION PERIOD.

Wood-Destroying Organism or Insect Inspection: IF CURRENT OR PAST WOOD-DESTROYING ORGANISMS OR INSECTS(SUCH AS TERMITES) ARE A MATERIAL MATTER TO THE BUYER, THESE ISSUES MUST BE INVESTIGATED DURING THEINSPECTION PERIOD. The Buyer shall order and pay for all wood-destroying organism or insect inspections performed during theInspection Period. If the lender requires an updated Wood-Destroying Organism or Insect Inspection Report prior to COE, it will beperformed at Buyer’s expense.

Flood Hazard: Flood hazard designations or the cost of flood hazard insurance shall be determined by Buyer during theInspection Period. If the Premises are situated in an area identified as having any special flood hazards by any governmentalentity, the lender may require the purchase of flood hazard insurance. Special flood hazards may also affect the ability toencumber or improve the Premises.

Insurance: IF HOMEOWNER’S INSURANCE IS A MATERIAL MATTER TO THE BUYER, BUYER SHALL APPLY FOR ANDOBTAIN WRITTEN CONFIRMATION OF THE AVAILABILITY AND COST OF HOMEOWNER’S INSURANCE FOR THEPREMISES FROM BUYER’S INSURANCE COMPANY DURING THE INSPECTION PERIOD. Buyer understands that anyhomeowner’s, fire, casualty, or other insurance desired by Buyer or required by lender should be in place at COE.

Sewer or On-site Wastewater Treatment System: The Premises are connected to a:

n sewer system n septic system n alternative system

IF A SEWER CONNECTION IS A MATERIAL MATTER TO THE BUYER, IT MUST BE INVESTIGATED DURING THEINSPECTION PERIOD. If the Premises are served by a septic or alternative system, the AAR On-site Wastewater TreatmentFacility Addendum is incorporated herein by reference.

(BUYER’S INITIALS REQUIRED) BUYER BUYER

Swimming Pool Barrier Regulations: During the Inspection Period, Buyer agrees to investigate all applicable state, county, andmunicipal Swimming Pool barrier regulations and agrees to comply with and pay all costs of compliance with said regulations prior tooccupying the Premises, unless otherwise agreed in writing. If the Premises contains a Swimming Pool, Buyer acknowledges receiptof the Arizona Department of Health Services approved private pool safety notice.

(BUYER’S INITIALS REQUIRED) BUYER BUYER