synergies in banking m&a: let’s play - home page-dip ... · exploit global operating ... the...

TRANSCRIPT

Copyright © 2009 Accenture All Rights Reserved, Accenture, its logo, and High Performance Delivered are trademarks of Accenture,Copyright © 2009 Accenture All Rights Reserved, Accenture, its logo, and High Performance Delivered are trademarks of Accenture,

Synergies in Banking M&A:Let’s play

Verona, 18 maggio 2009

Copyright © 2009 Accenture All Rights Reserved, 22

� Pre deal - Danilo Troncarelli

- M&A Trend

- Synergies in Banking M&A

- Golden Rules

� Post deal - Andrea Dalla Vedova

- Integration approach

- Action Plan

- Golden Rules

Agenda

Copyright © 2009 Accenture All Rights Reserved, 3

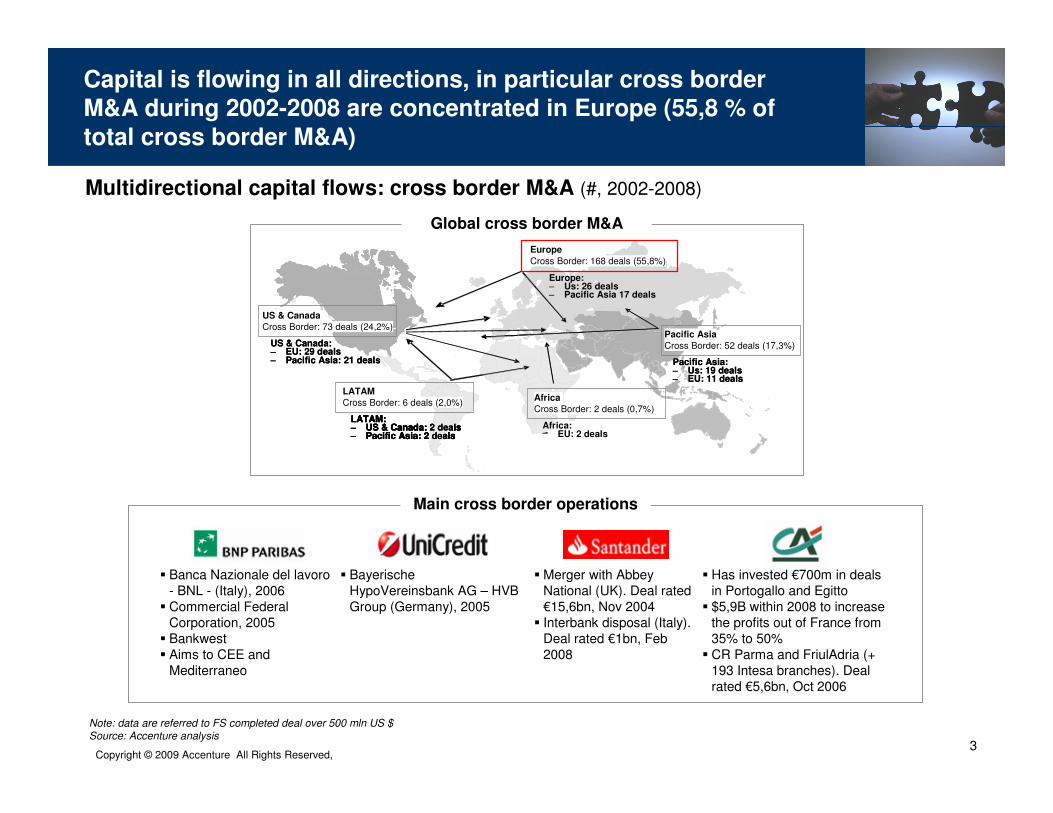

Capital is flowing in all directions, in particular cross borderM&A during 2002-2008 are concentrated in Europe (55,8 % of

total cross border M&A)

Multidirectional capital flows: cross border M&A (#, 2002-2008)

Note: data are referred to FS completed deal over 500 mln US $Source: Accenture analysis

Europe

Cross Border: 168 deals (55,8%)

Europe:– Us: 26 deals – Pacific Asia 17 deals

Pacific Asia

Cross Border: 52 deals (17,3%)

Pacific Asia:– Us: 19 deals – EU: 11 deals

US & Canada:– EU: 29 deals – Pacific Asia: 21 deals

LATAM

Cross Border: 6 deals

LATAM:– US & Canada: 2 deals – Pacific Asia: 2 deals

LATAM

Cross Border: 6 deals (2,0%)

LATAM:– US & Canada: 2 deals – Pacific Asia: 2 deals

Africa

– EU: 2 deals

Europe

Cross Border: 168 deals (55,8%)

Europe:– Us: 26 deals – Pacific Asia 17 deals

Pacific Asia

Cross Border: 52 deals (17,3%)

Pacific Asia:– Us: 19 deals – EU: 11 deals

US & Canada:– EU: 29 deals – Pacific Asia: 21 deals

LATAM

Cross Border: 6 deals

LATAM:– US & Canada: 2 deals – Pacific Asia: 2 deals

LATAM

Cross Border: 6 deals (2,0%)

LATAM:– US & Canada: 2 deals – Pacific Asia: 2 deals

Africa

Cross Border: 2 deals (0,7%)

–Africa:

� Merger with AbbeyNational (UK). Deal rated€15,6bn, Nov 2004

� Interbank disposal (Italy). Deal rated €1bn, Feb2008

� BayerischeHypoVereinsbank AG – HVB Group (Germany), 2005

� Has invested €700m in dealsin Portogallo and Egitto

� $5,9B within 2008 to increasethe profits out of France from35% to 50%

� CR Parma and FriulAdria (+ 193 Intesa branches). Deal rated €5,6bn, Oct 2006

� Banca Nazionale del lavoro - BNL - (Italy), 2006

� Commercial FederalCorporation, 2005

� Bankwest� Aims to CEE and

Mediterraneo

Main cross border operations

US & Canada

Cross Border: 73 deals (24,2%)

Global cross border M&A

Copyright © 2009 Accenture All Rights Reserved, 4

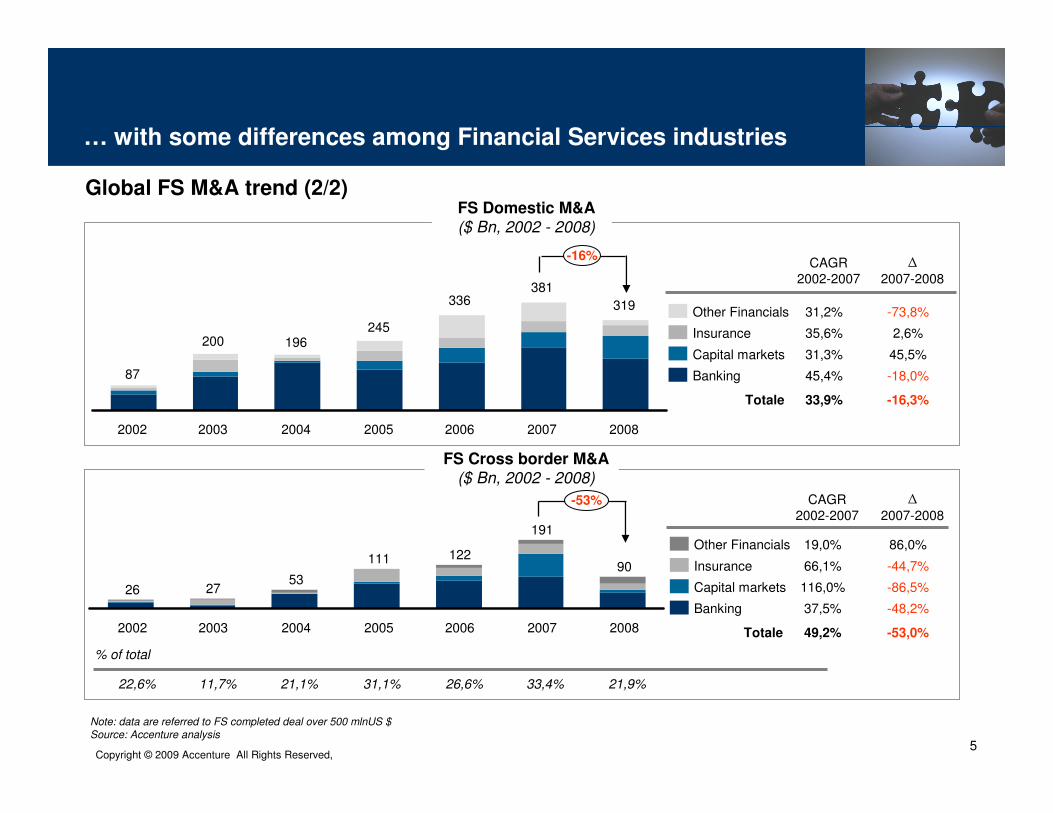

The global FS M&A trend shows a significantly reduction in the 2008 (compared with 2007) after a long period of a high growth

rate. 2008 in any case is positioning itself between 2005-06 …

Global FS M&A trend (1/2)

FS M&A($ Bn, 2002 - 2008)

% of cross border

22,6% 11,7% 21,1% 31,1% 26,6% 21,9%33,4%

319381

336

245196200

87 90

191

122111532726

2008200720062005200420032002

33,9%

-53%

-16%

Cross border

Domestic

CAGR 2002-2007 domestic

CAGR 2002-2007 cross border

49,2%

∆ (pp) 2007-2008

Average ‘02-’07

24,4%

Year

11,5%

Note: data are referred to FS completed deal over 500 mln US $Source: Accenture analysis

Copyright © 2009 Accenture All Rights Reserved, 5

… with some differences among Financial Services industries

FS Domestic M&A($ Bn, 2002 - 2008)

FS Cross border M&A($ Bn, 2002 - 2008)

Global FS M&A trend (2/2)

Note: data are referred to FS completed deal over 500 mlnUS $Source: Accenture analysis

Other Financials

Insurance

Capital markets

Banking

Insurance

Capital markets

Banking

Other Financials

% of total

20052002 20042003

381

196245

2008

336

2006 2007

319

87

200

-16%

22,6%

2005 2008

191

2007

90

26

2002

27

2003

53

2004

111 122

2006

11,7% 21,1% 31,1% 26,6% 21,9%33,4%

CAGR 2002-2007

35,6%

31,3%

45,4%

31,2%

Totale 33,9%

CAGR 2002-2007

Totale

66,1%

116,0%

37,5%

19,0%

49,2%

∆

2007-2008

2,6%

45,5%

-18,0%

-73,8%

-16,3%

-44,7%

-86,5%

-48,2%

86,0%

-53,0%

-53%

∆

2007-2008

Copyright © 2009 Accenture All Rights Reserved, 6

In any case, 2008 is different compared with all the previous years and waves. Now is a matter of “super-consolidation” that

is opening a period of operating model transformation

� BofA / Merrill Lynch

� Barclays / Lehman, Nomura / Lehman

� JP Morgan Chase / Washington Mutual

� Commerzbank / Dresdner Bank

� Wells Fargo / Wachovia

� Lloyds TSB / HBOS

� BNP Paribas / Fortis

� JPM/ Bear Sterns

� Westpac/ St. George Bank

� JPMorgan / Chase (2000)

� Barclays / Absa (2004)

� Santander / Abbey (2004)

� Danske Bank / NIB, NB (2005)

� RBS / ABN AMRO (2007)

� UBS / SBC (1997/8)

� Citi / Travelers (1998)

� BofA / Nationsbank (1998)

� RBS / Natwest (2000)

� Intesa / Sanpaolo (2006)

� Unicredit / Capitalia (2007)

Examples

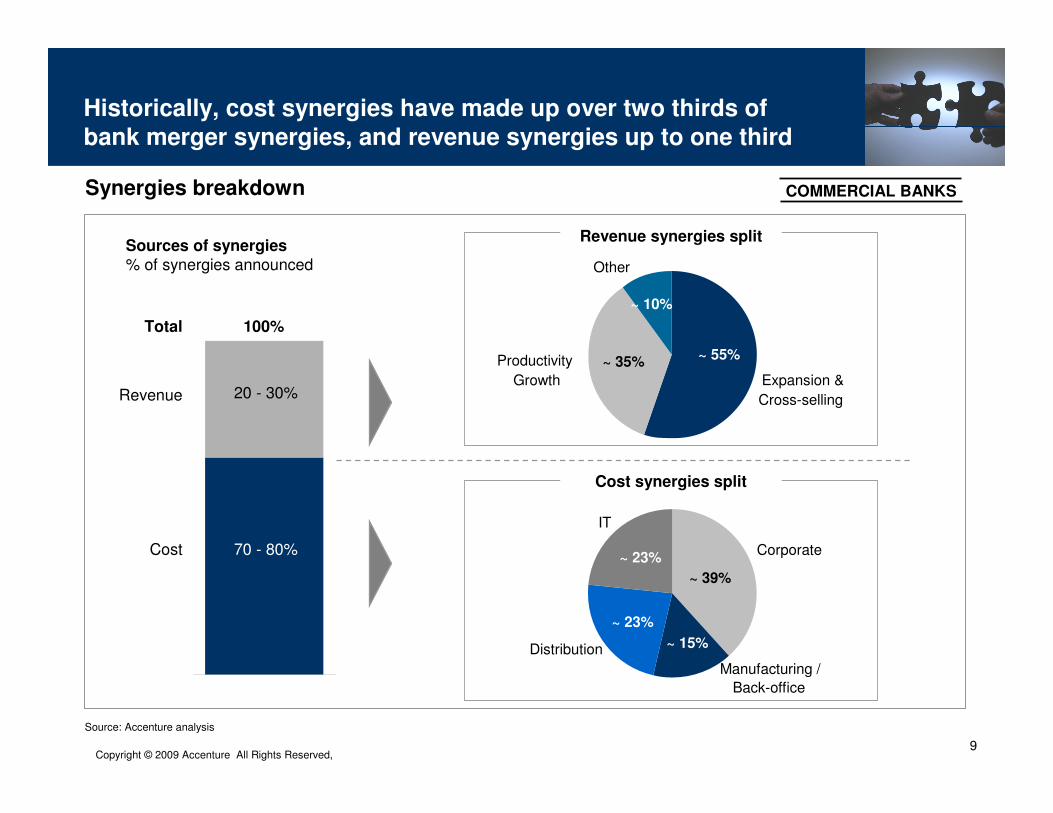

Cost: 70-80%

Revenue: 20-30%

Cost: 50-70%

Revenue: 30-50%

Synergies

announced

Fall 2008 up today1997 – 2007Timeframe

Super-consolidation

� Operating model transformation

� Strategic cost reduction

� Best practice transfer

� Local / regional de-duplication

� Next wave of M&A

� Market growth

� Product factories

� Best practice transfer

� Regional de-duplication

� Market growth

� Enlarged customer base

� Better market penetration and pricing

� Local de-duplication

� Branch consolidation

� Cost reduction

Sources of Value

� Economic slowdown

� Market discontinuity

� Regulatory intervention / “shot gun weddings”

� Uncertain outlook – risk of toxic assets, low confidence

� Asset divestitures

� Overcapitalization

� Undervalued assets

� Economies of scale

� Desire for regional / global footprint

� Overcapitalization

� Need for sustainable local market share and geographic footprint

� Cross-sell opportunities

Market

environment

Capability-basedExpansion

Domestic Consolidation

FS M&A waves

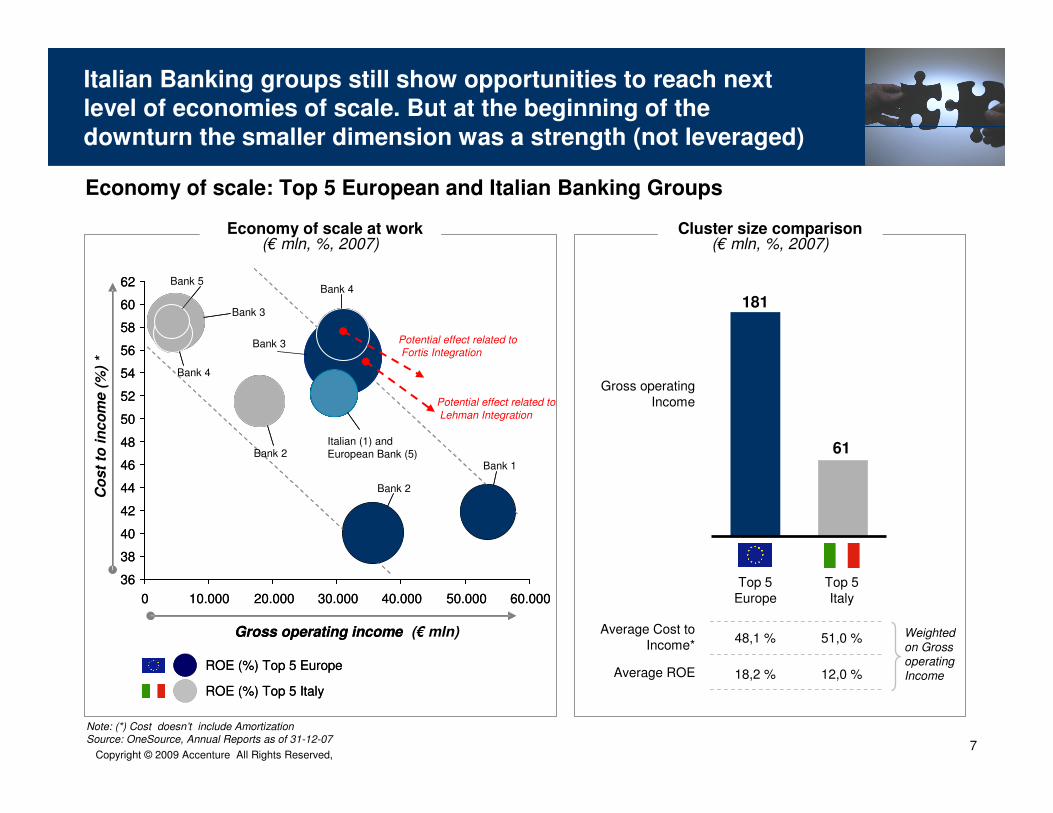

Copyright © 2009 Accenture All Rights Reserved, 7

181

61

Top 5Europe

Top 5Italy

Average Cost to Income*

Average ROE

48,1 % 51,0 %

18,2 % 12,0 %

Note: (*) Cost doesn’t include Amortization Source: OneSource, Annual Reports as of 31-12-07

Italian Banking groups still show opportunities to reach next level of economies of scale. But at the beginning of the

downturn the smaller dimension was a strength (not leveraged)

Economy of scale at work(€ mln, %, 2007)

Cluster size comparison(€ mln, %, 2007)

Gross operating income

ROE (%) Top 5 Europe

ROE (%) Top 5 Italy

+

+

Gross operating income (€ mln)

ROE (%) Top 5 Europe

ROE (%) Top 5 Italy

Economy of scale: Top 5 European and Italian Banking Groups

36

38

40

42

44

46

48

50

52

54

56

58

60

62

0 10.000 20.000 30.000 40.000 50.000 60.000

Bank 4

Italian (1) andEuropean Bank (5)

Unicredit

Bank 3

Bank 4

Bank 5

Co

st

to in

co

me (

%)

*

36

38

40

42

44

46

48

50

52

54

56

58

60

62

0 10.000 20.000 30.000 40.000 50.000 60.000

Bank 2

Bank 3

Bank 2

Gross operating Income

Weighted on Gross operating Income

Potential effect related toFortis Integration

Potential effect related toLehman Integration

Bank 1

Copyright © 2009 Accenture All Rights Reserved, 8

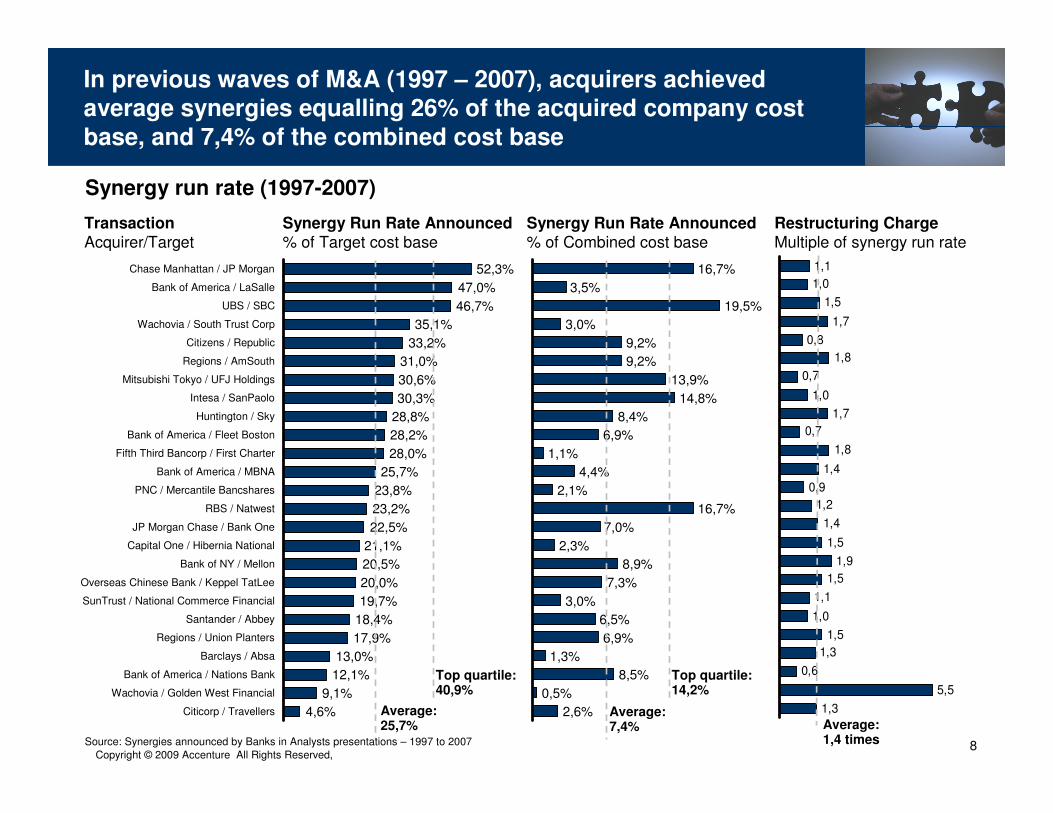

In previous waves of M&A (1997 – 2007), acquirers achieved average synergies equalling 26% of the acquired company cost

base, and 7,4% of the combined cost base

Synergy Run Rate Announced

% of Target cost baseSynergy Run Rate Announced

% of Combined cost baseTransaction

Acquirer/Target

Average:1,4 times

Citicorp / Travellers

9,1%Wachovia / Golden West Financial

12,1%Bank of America / Nations Bank

13,0%Barclays / Absa

17,9%Regions / Union Planters

18,4%Santander / Abbey

19,7%SunTrust / National Commerce Financial

20,0%Overseas Chinese Bank / Keppel TatLee

20,5%Bank of NY / Mellon

21,1%Capital One / Hibernia National

22,5%JP Morgan Chase / Bank One

23,2%RBS / Natwest

23,8%PNC / Mercantile Bancshares

25,7%Bank of America / MBNA

28,0%Fifth Third Bancorp / First Charter

28,2%Bank of America / Fleet Boston

28,8%

4,6%

46,7%

47,0%

52,3%

33,2%

Regions / AmSouth

UBS / SBC

Wachovia / South Trust Corp

Intesa / SanPaolo

31,0%

Bank of America / LaSalle

35,1%

30,3%

Mitsubishi Tokyo / UFJ Holdings

Chase Manhattan / JP Morgan

Citizens / Republic

Huntington / Sky

30,6%

Average:25,7%

Top quartile:40,9%

16,7%

3,5%

19,5%

3,0%

9,2%

9,2%

13,9%

14,8%

8,4%

6,9%

1,1%

4,4%

2,1%

16,7%

7,0%

2,3%

8,9%

7,3%

3,0%

6,9%

8,5%

2,6%

6,5%

1,3%

0,5%

Average:7,4%

Top quartile:14,2%

1,3

5,5

0,6

1,3

1,5

1,0

1,1

1,5

1,9

1,5

1,4

1,2

0,9

1,4

1,8

0,7

1,7

1,0

0,7

1,8

0,8

1,7

1,5

1,0

1,1

Restructuring Charge

Multiple of synergy run rate

Synergy run rate (1997-2007)

Source: Synergies announced by Banks in Analysts presentations – 1997 to 2007

Copyright © 2009 Accenture All Rights Reserved, 9

Productivity

Growth Expansion &

Cross-selling

Other

Sources of synergies% of synergies announced

100%

Revenue 20 - 30%

Cost

Total

70 - 80%

Revenue synergies split

~ 55%~ 35%

~ 10%

Cost synergies split

Source: Accenture analysis

~ 8%

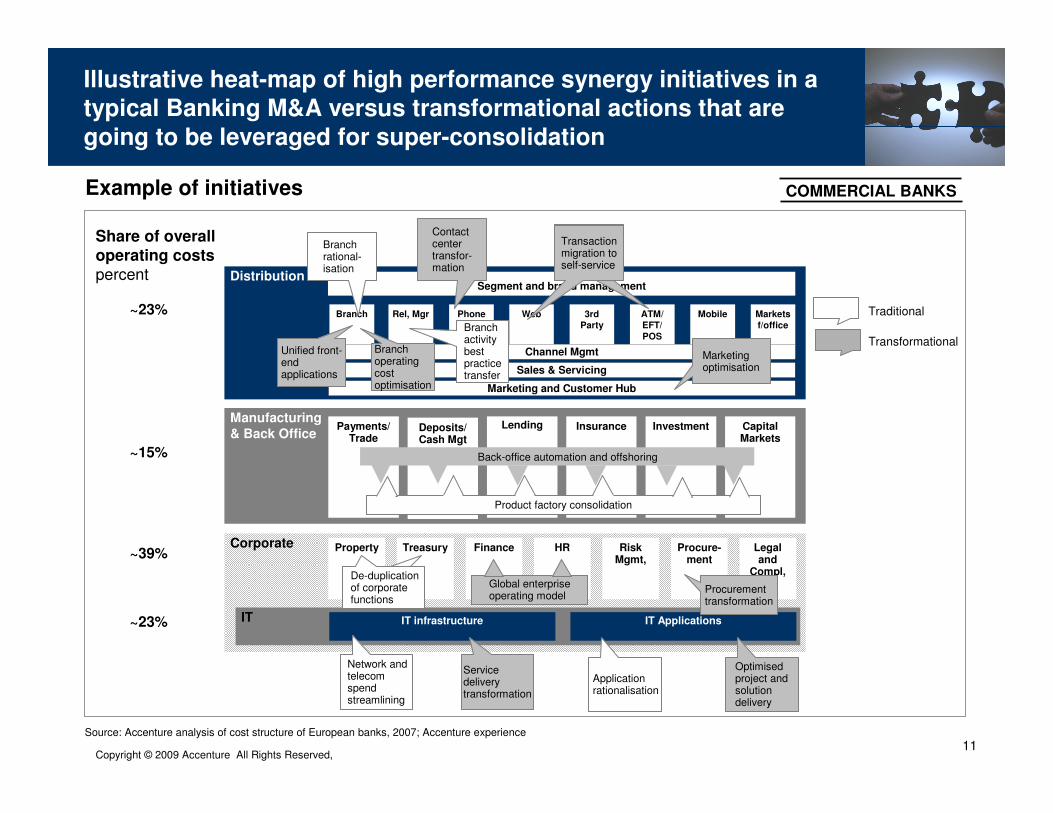

COMMERCIAL BANKS

Historically, cost synergies have made up over two thirds of

bank merger synergies, and revenue synergies up to one third

Synergies breakdown

Corporate

IT

~ 39%

~ 23%

~ 23%

~ 15%

Manufacturing /

Back-office

Distribution

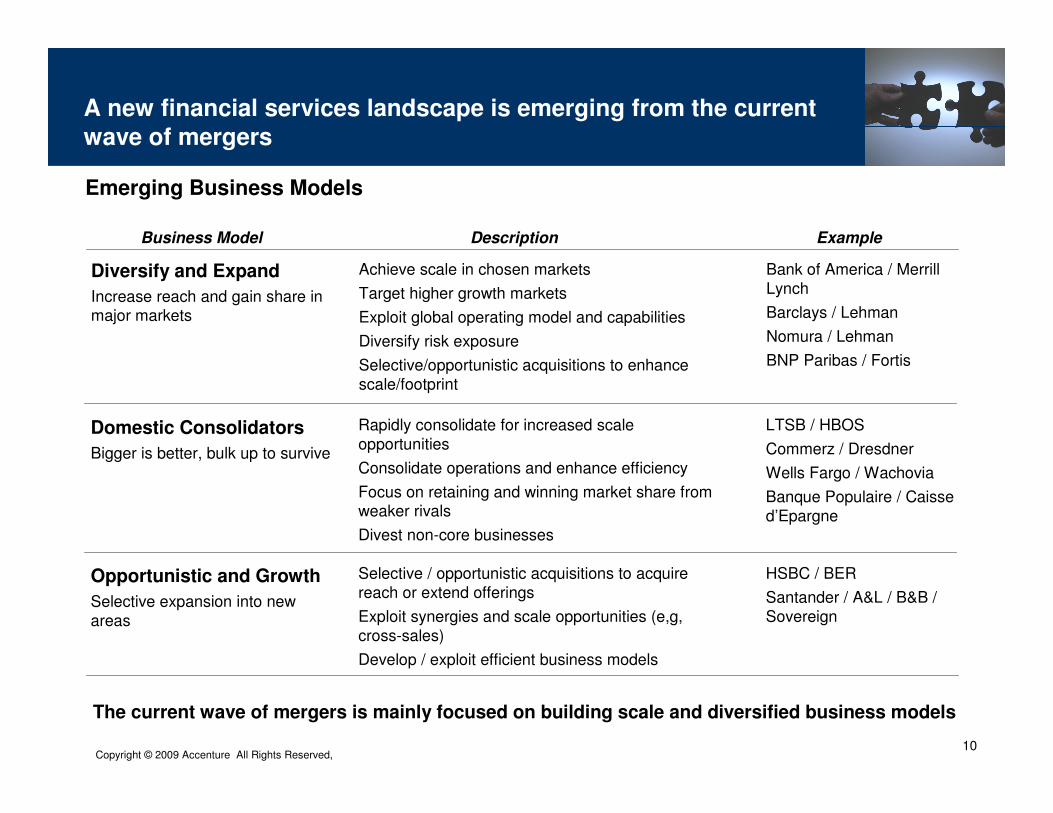

Copyright © 2009 Accenture All Rights Reserved, 10

Achieve scale in chosen markets

Target higher growth markets

Exploit global operating model and capabilities

Diversify risk exposure

Selective/opportunistic acquisitions to enhance scale/footprint

Diversify and Expand

Increase reach and gain share in major markets

Domestic Consolidators

Bigger is better, bulk up to survive

Rapidly consolidate for increased scale opportunities

Consolidate operations and enhance efficiency

Focus on retaining and winning market share from weaker rivals

Divest non-core businesses

Opportunistic and Growth

Selective expansion into new areas

Selective / opportunistic acquisitions to acquire reach or extend offerings

Exploit synergies and scale opportunities (e,g, cross-sales)

Develop / exploit efficient business models

Bank of America / Merrill Lynch

Barclays / Lehman

Nomura / Lehman

BNP Paribas / Fortis

LTSB / HBOS

Commerz / Dresdner

Wells Fargo / Wachovia

Banque Populaire / Caissed’Epargne

HSBC / BER

Santander / A&L / B&B / Sovereign

The current wave of mergers is mainly focused on building scale and diversified business models

A new financial services landscape is emerging from the current

wave of mergers

Emerging Business Models

Business Model Description Example

Copyright © 2009 Accenture All Rights Reserved, 11

Distribution

Manufacturing

& Back Office

Corporate

Segment and brand management

Branch Rel, Mgr Web ATM/

EFT/

POS

3rd

Party

Phone Mobile Markets

f/office

Deposits/Cash Mgt

Lending InvestmentPayments/ Trade

Insurance Capital Markets

Finance HR Risk Mgmt,

Procure-ment

Legal and

Compl,

Property Treasury

IT IT infrastructure IT Applications

Channel Mgmt

Sales & Servicing

~65%

Marketing and Customer Hub

Share of overall operating costspercent

~23%

~15%

~23%

~39%

Branch rational-isation

Contact center transfor-mation

Transaction migration to self-service

Optimisedproject and solution delivery

Application rationalisation

Service delivery transformation

Network and telecom spend streamlining

De-duplication of corporate functions

Marketing optimisation

Traditional

Transformational

Global enterprise operating model

Product factory consolidation

Back-office automation and offshoring

Transaction migration to self-service

De-duplication of corporate functions

Branch operating cost optimisation

Unified front-end applications

Branch activity best practice transfer

Procurement transformation

Illustrative heat-map of high performance synergy initiatives in a typical Banking M&A versus transformational actions that are

going to be leveraged for super-consolidation

Example of initiatives

Source: Accenture analysis of cost structure of European banks, 2007; Accenture experience

COMMERCIAL BANKS

Copyright © 2009 Accenture All Rights Reserved, 12

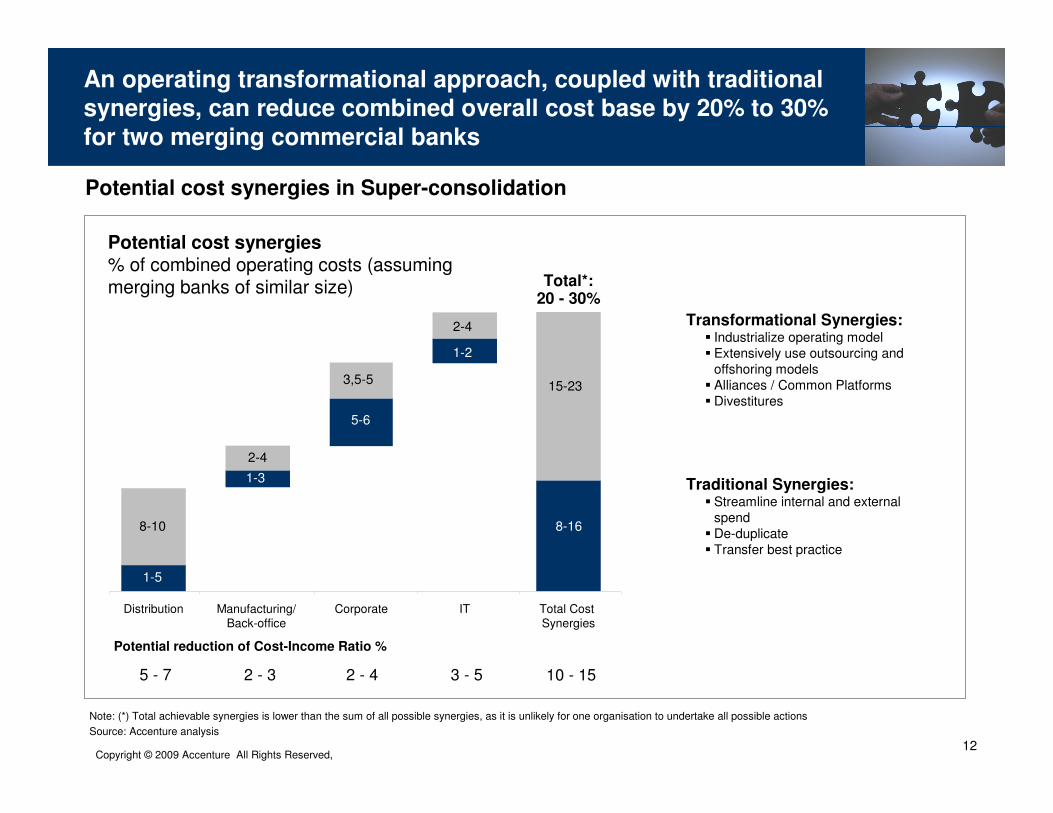

Potential cost synergies% of combined operating costs (assuming merging banks of similar size)

Traditional Synergies:� Streamline internal and external

spend� De-duplicate� Transfer best practice

Total*:20 - 30%

Transformational Synergies:� Industrialize operating model� Extensively use outsourcing and

offshoring models� Alliances / Common Platforms� Divestitures

10 - 153 - 52 - 42 - 35 - 7

Potential reduction of Cost-Income Ratio %

Note: (*) Total achievable synergies is lower than the sum of all possible synergies, as it is unlikely for one organisation to undertake all possible actions

Source: Accenture analysis

An operating transformational approach, coupled with traditionalsynergies, can reduce combined overall cost base by 20% to 30%

for two merging commercial banks

8-16

15-23

1-5

8-10

1-3

2-4

5-6

3,5-5

Distribution Manufacturing/Back-office

Corporate Total CostSynergies

Potential cost synergies in Super-consolidation

1-2

2-4

IT

Copyright © 2009 Accenture All Rights Reserved, 13

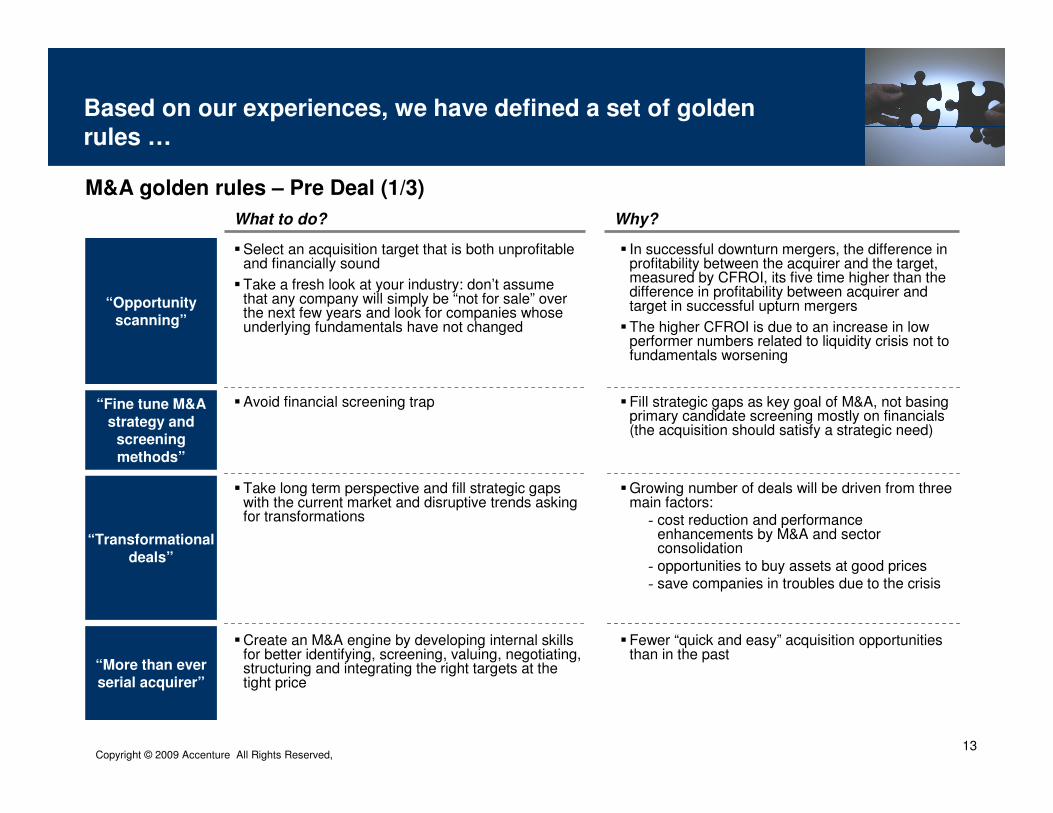

“Opportunity scanning”

“Fine tune M&A

strategy and screening

methods”

“Transformational

deals”

What to do? Why?

�Select an acquisition target that is both unprofitable and financially sound

�Take a fresh look at your industry: don’t assume that any company will simply be “not for sale” over the next few years and look for companies whose underlying fundamentals have not changed

� In successful downturn mergers, the difference in profitability between the acquirer and the target, measured by CFROI, its five time higher than the difference in profitability between acquirer and target in successful upturn mergers

�The higher CFROI is due to an increase in low performer numbers related to liquidity crisis not to fundamentals worsening

�Avoid financial screening trap �Fill strategic gaps as key goal of M&A, not basing primary candidate screening mostly on financials (the acquisition should satisfy a strategic need)

�Take long term perspective and fill strategic gaps with the current market and disruptive trends asking for transformations

�Growing number of deals will be driven from three main factors:- cost reduction and performance

enhancements by M&A and sector consolidation- opportunities to buy assets at good prices- save companies in troubles due to the crisis

Based on our experiences, we have defined a set of golden

rules …

�Create an M&A engine by developing internal skills for better identifying, screening, valuing, negotiating, structuring and integrating the right targets at the tight price

�Fewer “quick and easy” acquisition opportunities than in the past

“More than ever serial acquirer”

M&A golden rules – Pre Deal (1/3)

Copyright © 2009 Accenture All Rights Reserved, 14

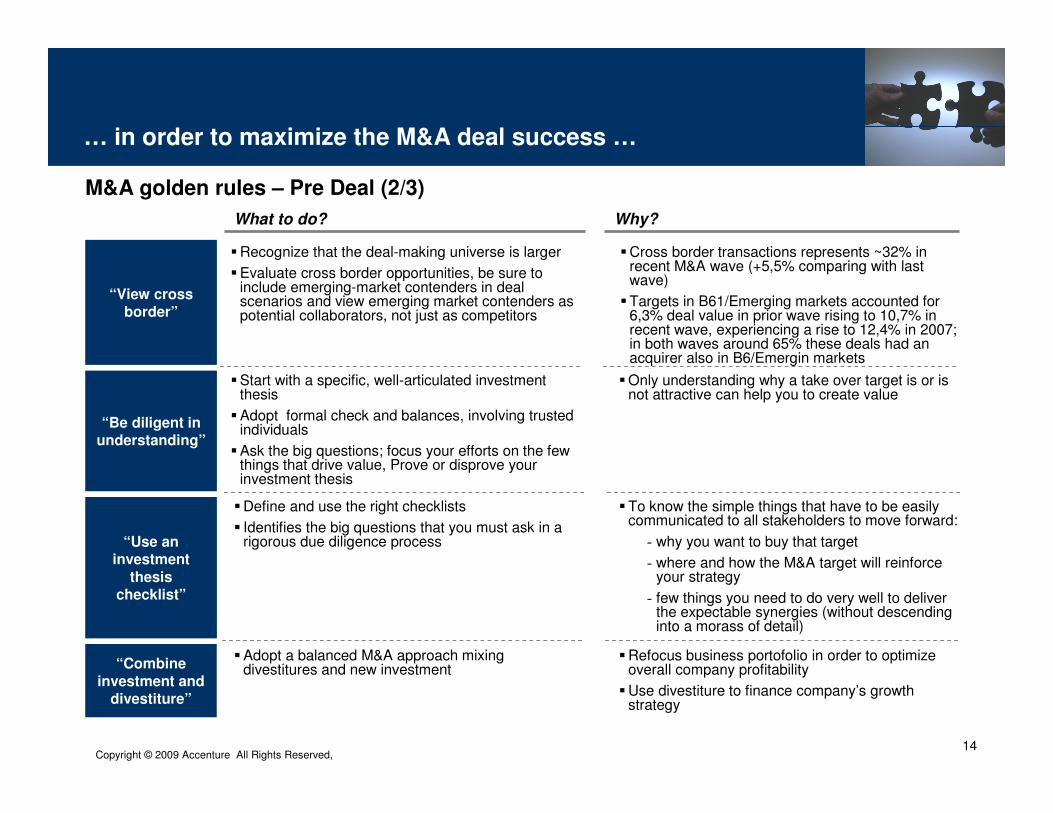

�Start with a specific, well-articulated investment thesis

�Adopt formal check and balances, involving trusted individuals

�Ask the big questions; focus your efforts on the few things that drive value, Prove or disprove your investment thesis

�Only understanding why a take over target is or is not attractive can help you to create value

“Be diligent in understanding”

�Define and use the right checklists

� Identifies the big questions that you must ask in a rigorous due diligence process

�To know the simple things that have to be easily communicated to all stakeholders to move forward:

- why you want to buy that target

- where and how the M&A target will reinforce your strategy

- few things you need to do very well to deliver the expectable synergies (without descending into a morass of detail)

“Use an investment

thesis checklist”

… in order to maximize the M&A deal success …

�Adopt a balanced M&A approach mixing divestitures and new investment“Combine

investment and divestiture”

�Refocus business portofolio in order to optimize overall company profitability

�Use divestiture to finance company’s growth strategy

M&A golden rules – Pre Deal (2/3)

�Recognize that the deal-making universe is larger

�Evaluate cross border opportunities, be sure to include emerging-market contenders in deal scenarios and view emerging market contenders as potential collaborators, not just as competitors

“View cross border”

What to do? Why?

�Cross border transactions represents ~32% in recent M&A wave (+5,5% comparing with last wave)

�Targets in B61/Emerging markets accounted for 6,3% deal value in prior wave rising to 10,7% in recent wave, experiencing a rise to 12,4% in 2007; in both waves around 65% these deals had an acquirer also in B6/Emergin markets

Copyright © 2009 Accenture All Rights Reserved, 15

… and understand even if it is not the case to move forward with

the deal

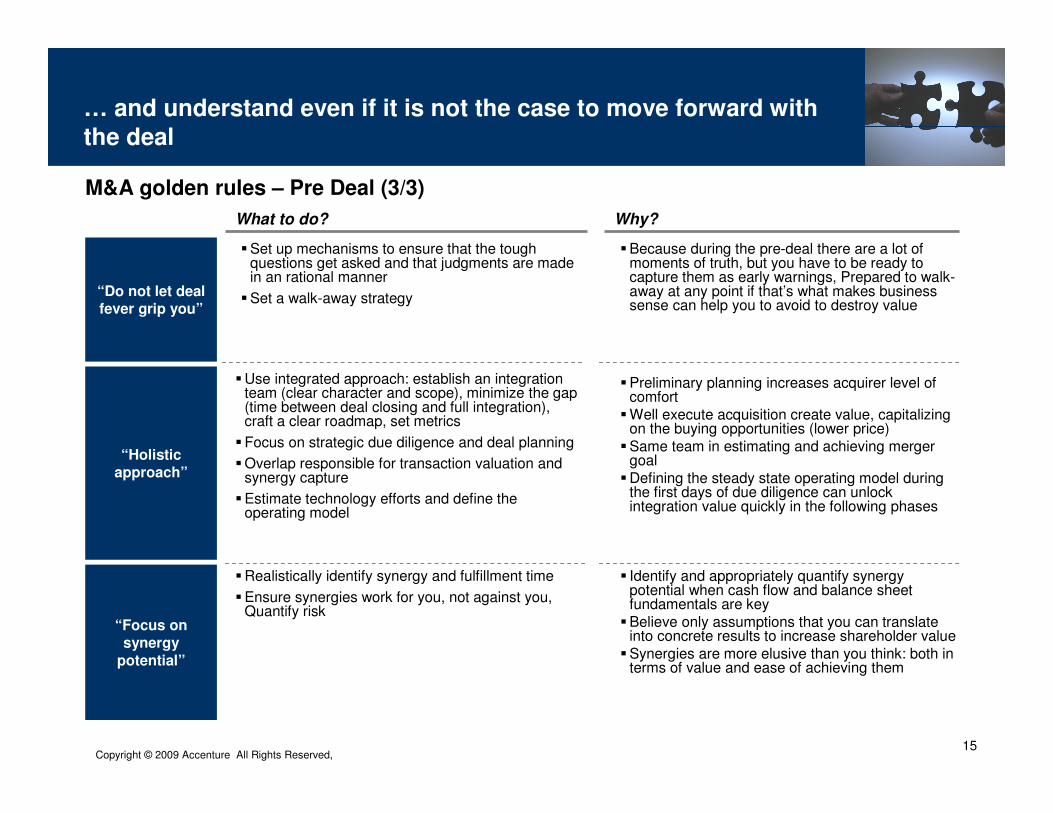

�Use integrated approach: establish an integration team (clear character and scope), minimize the gap (time between deal closing and full integration), craft a clear roadmap, set metrics

�Focus on strategic due diligence and deal planning

�Overlap responsible for transaction valuation and synergy capture

�Estimate technology efforts and define the operating model

“Holistic approach”

�Realistically identify synergy and fulfillment time

�Ensure synergies work for you, not against you, Quantify risk

“Focus on synergy

potential”

� Identify and appropriately quantify synergy potential when cash flow and balance sheet fundamentals are key

�Believe only assumptions that you can translate into concrete results to increase shareholder value

�Synergies are more elusive than you think: both in terms of value and ease of achieving them

M&A golden rules – Pre Deal (3/3)

What to do? Why?

�Set up mechanisms to ensure that the tough questions get asked and that judgments are made in an rational manner

�Set a walk-away strategy

�Because during the pre-deal there are a lot of moments of truth, but you have to be ready to capture them as early warnings, Prepared to walk-away at any point if that’s what makes business sense can help you to avoid to destroy value

“Do not let deal fever grip you”

�Preliminary planning increases acquirer level of comfort

�Well execute acquisition create value, capitalizing on the buying opportunities (lower price)

�Same team in estimating and achieving merger goal

�Defining the steady state operating model during the first days of due diligence can unlock integration value quickly in the following phases

Copyright © 2009 Accenture All Rights Reserved, 1616

Agenda

� Pre deal - Danilo Troncarelli

- M&A Trend

- Synergies in Banking M&A

- Golden Rules

� Post deal - Andrea Dalla Vedova

- Integration approach

- Action Plan

- Golden Rules

Copyright © 2009 Accenture All Rights Reserved, 17

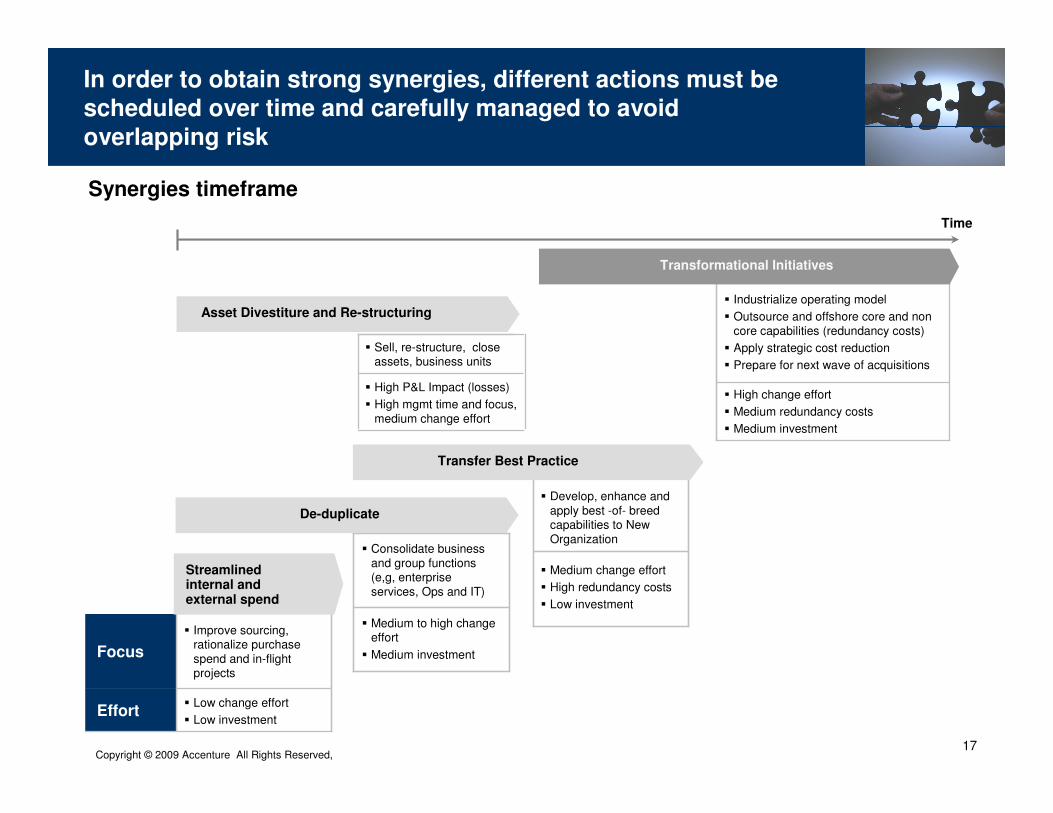

Effort

Focus

Transfer Best Practice

De-duplicate

Time

Transformational Initiatives

Asset Divestiture and Re-structuring

Synergies timeframe

In order to obtain strong synergies, different actions must be scheduled over time and carefully managed to avoid

overlapping risk

� Sell, re-structure, close assets, business units

� High P&L Impact (losses)

� High mgmt time and focus, medium change effort

� Industrialize operating model

� Outsource and offshore core and non core capabilities (redundancy costs)

� Apply strategic cost reduction

� Prepare for next wave of acquisitions

� High change effort

� Medium redundancy costs

� Medium investment

� Develop, enhance and apply best -of- breed capabilities to New Organization

� Medium change effort

� High redundancy costs

� Low investment

� Medium to high change effort

� Medium investment

� Consolidate business and group functions (e,g, enterprise services, Ops and IT)

� Low change effort

� Low investment

� Improve sourcing, rationalize purchase spend and in-flight projects

Streamlined internal and external spend

Copyright © 2009 Accenture All Rights Reserved, 18

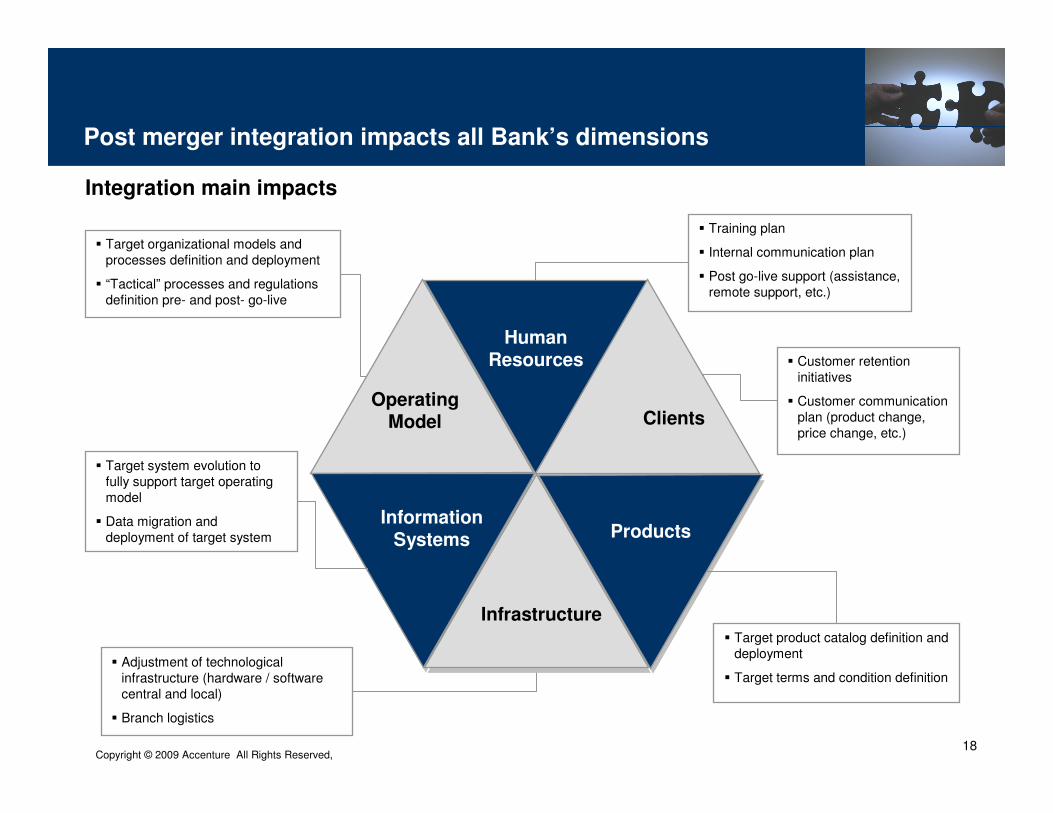

Information Systems

Human Resources

Operating Model

� Training plan

� Internal communication plan

� Post go-live support (assistance, remote support, etc.)

� Customer retention initiatives

� Customer communication plan (product change, price change, etc.)

� Target product catalog definition and deployment

� Target terms and condition definition� Adjustment of technological

infrastructure (hardware / software central and local)

� Branch logistics

� Target organizational models and processes definition and deployment

� “Tactical” processes and regulations definition pre- and post- go-live

� Target system evolution to fully support target operating model

� Data migration and deployment of target system

Clients

Products

Infrastructure

Post merger integration impacts all Bank’s dimensions

Integration main impacts

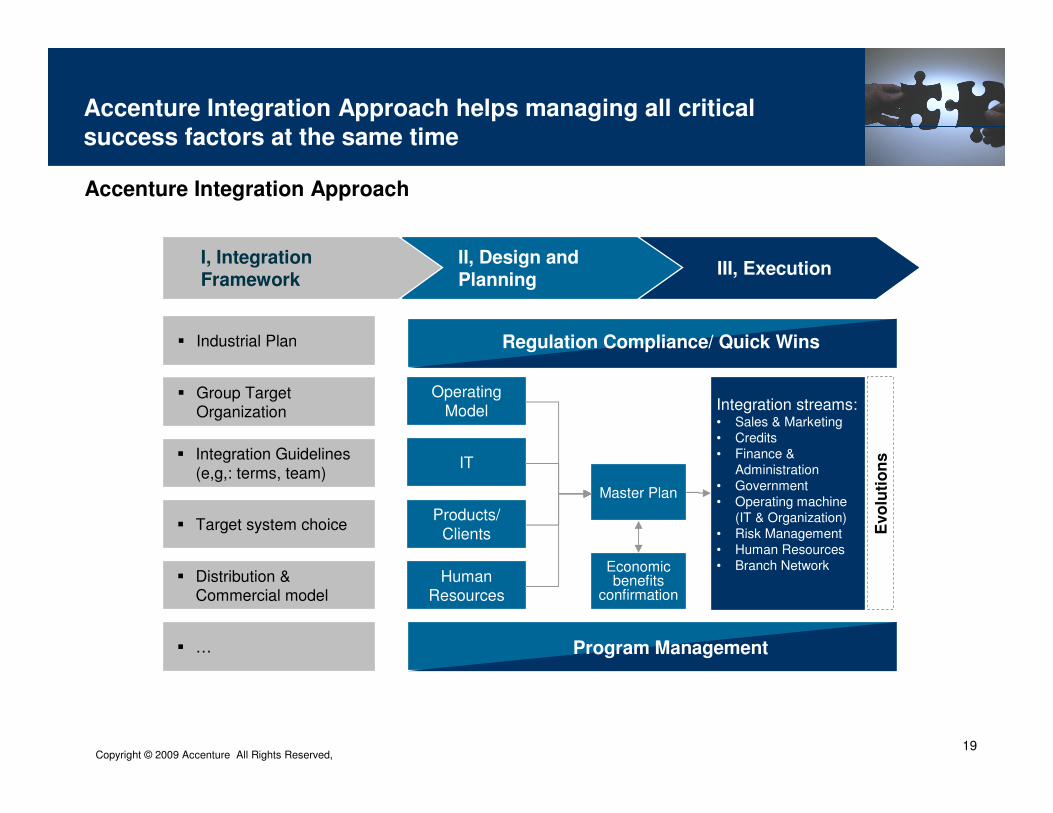

Copyright © 2009 Accenture All Rights Reserved, 19

Accenture Integration Approach helps managing all critical

success factors at the same time

Accenture Integration Approach

� Industrial Plan

III, ExecutionII, Design and Planning

I, Integration Framework

Operating Model

Evo

luti

on

sIT

Products/ Clients

Human Resources

Master Plan

Economic benefits

confirmation

Integration streams:• Sales & Marketing • Credits• Finance &

Administration• Government• Operating machine

(IT & Organization)• Risk Management• Human Resources• Branch Network

Program Management

Regulation Compliance/ Quick Wins

� Group Target Organization

� Integration Guidelines (e,g,: terms, team)

� Target system choice

� Distribution & Commercial model

� …

Copyright © 2009 Accenture All Rights Reserved, 20

Distribution

Group Operations

Op

era

tio

ns

Pro

du

cts

&

M

ark

ets

Sa

les

&

Se

rvic

eS

up

po

rt

C&G Cards SW

3rd

Parties

Group Operations

CA GIBusiness

Migration

to Gp

Ops

Underway

CardsC&GSavingsLendingCurrent

Accounts

Enterprise Shared Services

Distribution

Group OperationsOp

era

tio

ns

Pro

du

cts

&

M

ark

ets

Sa

les

&

Se

rvic

eS

up

po

rt

C&G

Central Operations

CA

Ops

Underway

Enterprise Shared Services

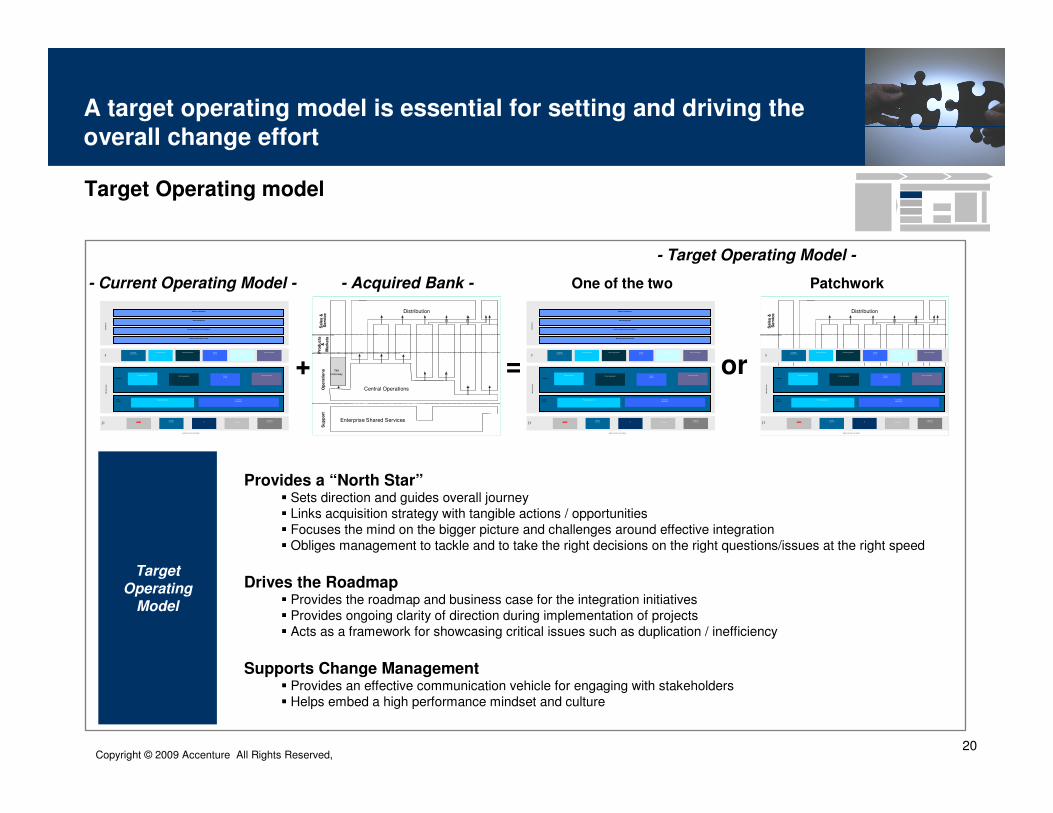

- Acquired Bank -- Current Operating Model -

- Target Operating Model -

+

Provides a “North Star”� Sets direction and guides overall journey� Links acquisition strategy with tangible actions / opportunities� Focuses the mind on the bigger picture and challenges around effective integration� Obliges management to tackle and to take the right decisions on the right questions/issues at the right speed

Drives the Roadmap� Provides the roadmap and business case for the integration initiatives � Provides ongoing clarity of direction during implementation of projects� Acts as a framework for showcasing critical issues such as duplication / inefficiency

Supports Change Management� Provides an effective communication vehicle for engaging with stakeholders� Helps embed a high performance mindset and culture

Target

Operating Model

Target Operating model

= or

One of the two Patchwork

A target operating model is essential for setting and driving the

overall change effort

Dis

trib

uti

on

Hu

bM

an

ufa

ctu

rin

g

Co

rp

co

re

Knowledgemanagement

Products

Crossproduct

Product development

Ser vice integrationCustomermanagement

Customer pricing Product aggregation Third partymanagement

Productpricing

Segment manag ement

Brand management

Marketin g, sales and servicing

Channel integration and man agement

Finance

Humanresources IT Purchasing

Legal andcompliance

SIMPLIFIED ON THE INSIDE

Customer pricingProduct aggregation Product

pricing

Ser vice integration

Dis

trib

uti

on

Hu

bM

an

ufa

ctu

rin

g

Co

rp

co

re

Knowledgemanagement

Products

Crossproduct

Product development

Ser vice integrationCustomermanagement

Customer pricing Product aggregation Third partymanagement

Productpricing

Segment management

Brand management

Marketing, sales and servicing

Channel integration and management

Finance

Humanresources IT Purchasing

Legal andcompliance

SIMPLIFIED ON THE INSIDE

Customer pricingProduct aggregation Product

pricing

Ser vice integration

Distribution

Pro

du

cts

&

M

ark

ets

Sa

les

&

Se

rvic

e

C&G Cards SW

3rd

Parties

CA GIBusiness CardsC&GSavingsLendingCurrent

Accounts

Distribution

Sa

les

&

Se

rvic

e

C&GCA

Hu

bM

an

ufa

ctu

rin

g

Co

rp

co

re

Knowledgemanagement

Products

Crossproduct

Product development

Ser vice integrationCustomermanagement

Customer pricing Product aggregation Third partymanagement

Productpricing

Finance

Humanresources IT Purchasing

Legal andcompliance

SIMPLIFIED ON THE INSIDE

Customer pricingProduct aggregation Product

pricing

Ser vice integration

Copyright © 2009 Accenture All Rights Reserved, 21

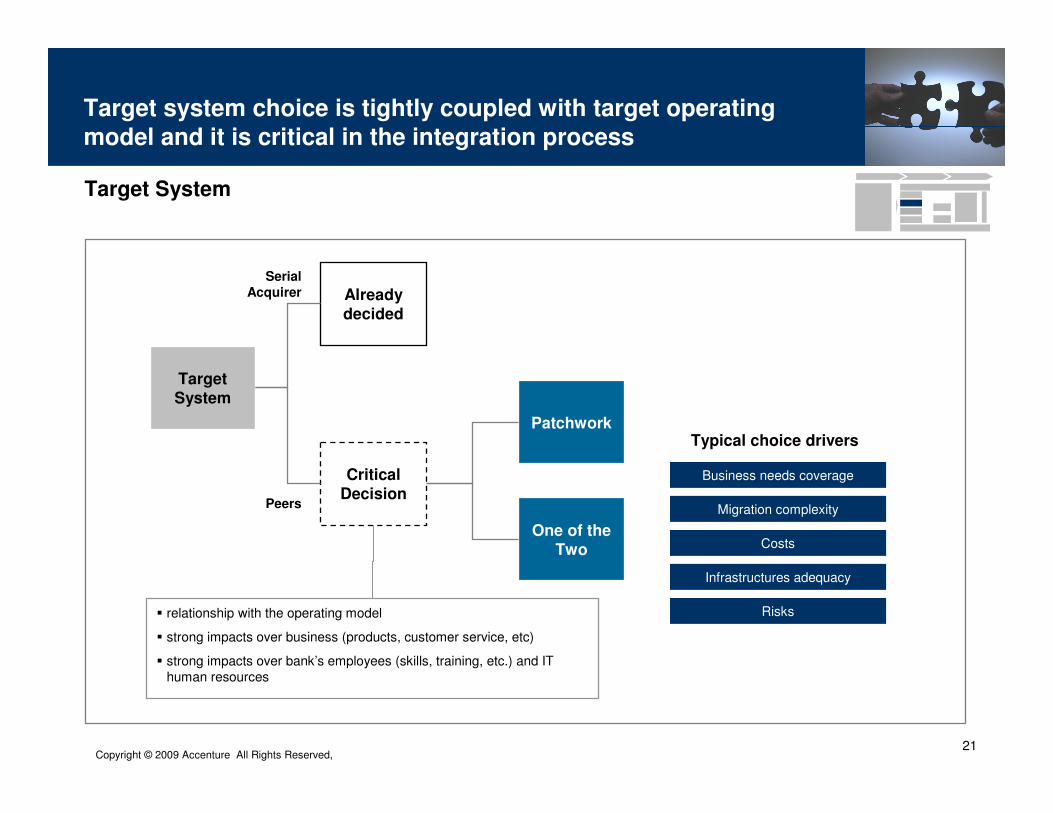

Already decided

Target System

� relationship with the operating model

� strong impacts over business (products, customer service, etc)

� strong impacts over bank’s employees (skills, training, etc.) and IT human resources

Target System

Patchwork

Critical Decision

Serial

Acquirer

Peers

One of the Two

Typical choice drivers

Business needs coverage

Migration complexity

Costs

Infrastructures adequacy

Risks

Target system choice is tightly coupled with target operating

model and it is critical in the integration process

Copyright © 2009 Accenture All Rights Reserved, 22

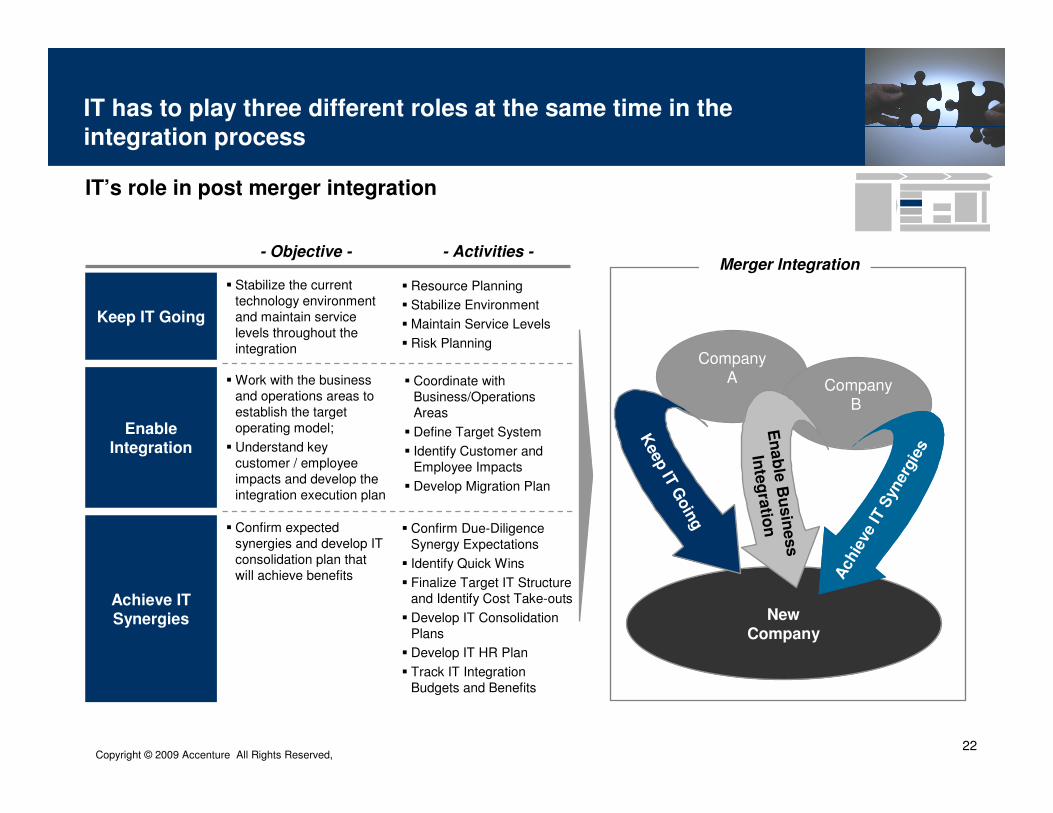

Keep IT Going

Enable Integration

Achieve IT Synergies

� Stabilize the current technology environment and maintain service levels throughout the integration

� Work with the business and operations areas to establish the target operating model;

� Understand key customer / employee impacts and develop the integration execution plan

� Confirm expected synergies and develop IT consolidation plan that will achieve benefits

- Activities -- Objective -

� Resource Planning

� Stabilize Environment

� Maintain Service Levels

� Risk Planning

� Coordinate with Business/Operations Areas

� Define Target System

� Identify Customer and Employee Impacts

� Develop Migration Plan

� Confirm Due-Diligence Synergy Expectations

� Identify Quick Wins

� Finalize Target IT Structure and Identify Cost Take-outs

� Develop IT Consolidation Plans

� Develop IT HR Plan

� Track IT Integration Budgets and Benefits

Company A

New Company

Company B

Keep IT

Goin

g

En

ab

le B

usin

ess

Inte

gra

tion

Achie

ve IT

Syn

erg

ies

Merger Integration

IT has to play three different roles at the same time in the

integration process

IT’s role in post merger integration

Copyright © 2009 Accenture All Rights Reserved, 23

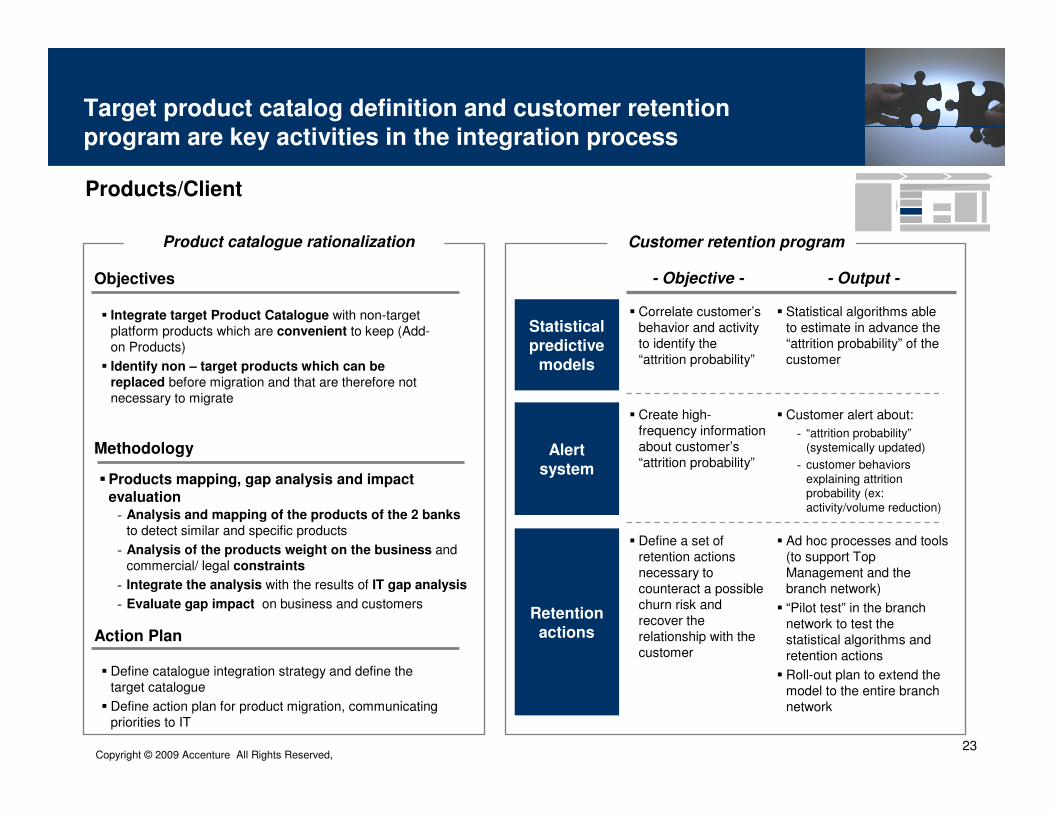

Products/Client

Statistical predictive

models

Alert system

Retention actions

� Correlate customer’s behavior and activity to identify the “attrition probability”

� Create high-frequency information about customer’s “attrition probability”

� Define a set of retention actions necessary to counteract a possible churn risk and recover the relationship with the customer

- Output -- Objective -

� Statistical algorithms able to estimate in advance the “attrition probability” of the customer

� Customer alert about:

� Ad hoc processes and tools (to support Top Management and the branch network)

� “Pilot test” in the branch network to test the statistical algorithms and retention actions

� Roll-out plan to extend the model to the entire branch network

- “attrition probability”(systemically updated)

- customer behaviors explaining attrition probability (ex: activity/volume reduction)

� Integrate target Product Catalogue with non-target platform products which are convenient to keep (Add-on Products)

� Identify non – target products which can be

replaced before migration and that are therefore not necessary to migrate

Objectives

Methodology

- Analysis and mapping of the products of the 2 banks

to detect similar and specific products

- Analysis of the products weight on the business andcommercial/ legal constraints

- Integrate the analysis with the results of IT gap analysis

- Evaluate gap impact on business and customers

Customer retention programProduct catalogue rationalization

�Products mapping, gap analysis and impact

evaluation

Action Plan

� Define catalogue integration strategy and define the target catalogue

� Define action plan for product migration, communicating priorities to IT

Target product catalog definition and customer retention

program are key activities in the integration process

Copyright © 2009 Accenture All Rights Reserved, 24

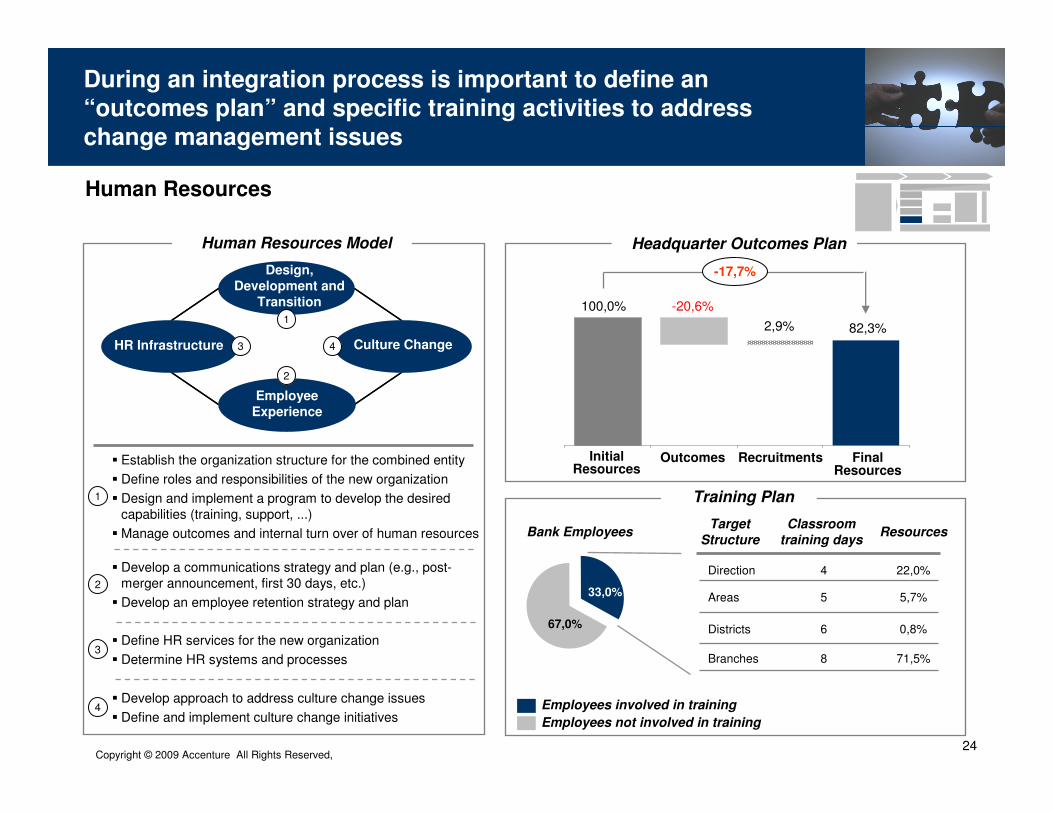

During an integration process is important to define an “outcomes plan” and specific training activities to address

change management issues

Organization

Design,

Development and

Transition

Culture Change

Employee

Experience

HR Infrastructure 3

1

4

2

1

2

3

4

4Direction

Target

Structure

Areas

Districts

Classroom

training daysResources

5

6

8Branches

22,0%

5,7%

0,8%

71,5%

� Establish the organization structure for the combined entity

� Define roles and responsibilities of the new organization

� Design and implement a program to develop the desired capabilities (training, support, ...)

� Manage outcomes and internal turn over of human resources

� Develop a communications strategy and plan (e.g., post-merger announcement, first 30 days, etc.)

� Develop an employee retention strategy and plan

� Define HR services for the new organization

� Determine HR systems and processes

� Develop approach to address culture change issues

� Define and implement culture change initiatives

100,0% -20,6%

2,9% 82,3%

OutcomesInitial Resources

Final Resources

Recruitments

Human Resources Model

Training Plan

Headquarter Outcomes Plan

-17,7%

33,0%

67,0%

Employees involved in training

Employees not involved in training

Bank Employees

Human Resources

Copyright © 2009 Accenture All Rights Reserved, 25

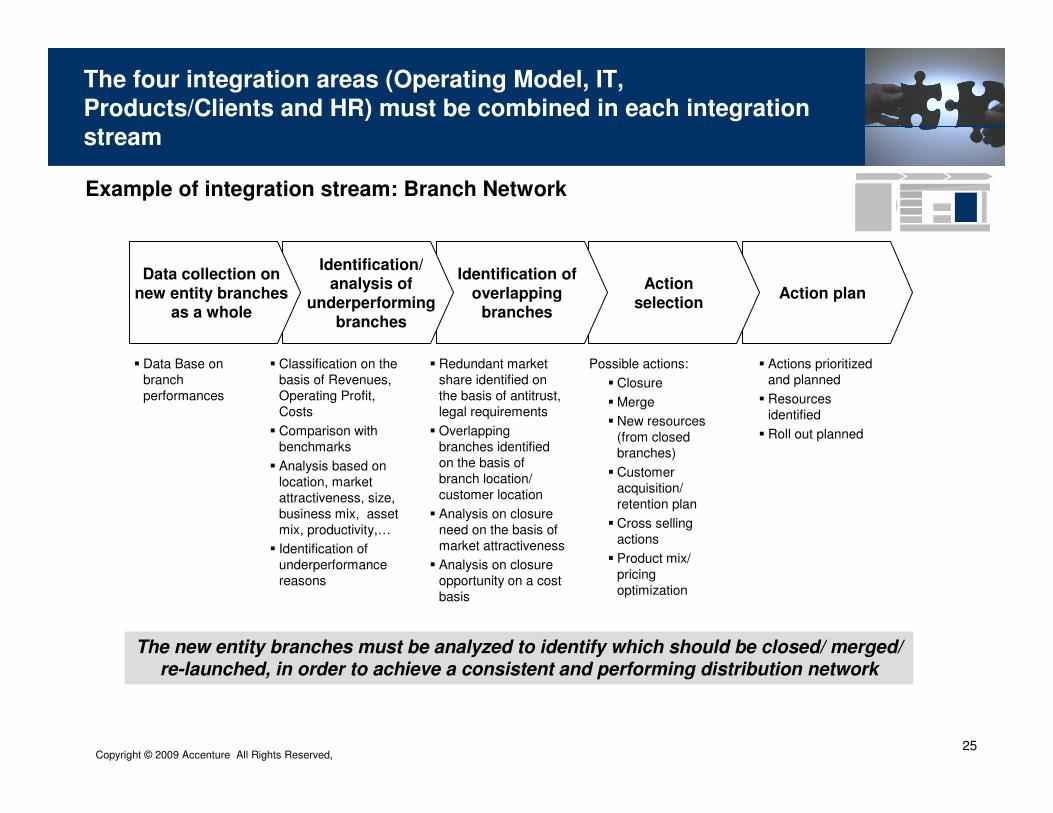

The new entity branches must be analyzed to identify which should be closed/ merged/ re-launched, in order to achieve a consistent and performing distribution network

Action planAction

selection

Identification of overlapping

branches

Identification/ analysis of

underperforming branches

Data collection on new entity branches

as a whole

� Data Base on branch performances

� Actions prioritized and planned

� Resources identified

� Roll out planned

� Classification on the basis of Revenues, Operating Profit, Costs

� Comparison with benchmarks

� Analysis based on location, market attractiveness, size, business mix, asset mix, productivity,…

� Identification of underperformance reasons

� Redundant market share identified on the basis of antitrust, legal requirements

� Overlapping branches identified on the basis of branch location/ customer location

� Analysis on closure need on the basis of market attractiveness

� Analysis on closure opportunity on a cost basis

Possible actions:

� Closure

� Merge

� New resources (from closed branches)

� Customer acquisition/ retention plan

� Cross selling actions

� Product mix/ pricing optimization

Example of integration stream: Branch Network

The four integration areas (Operating Model, IT, Products/Clients and HR) must be combined in each integration

stream

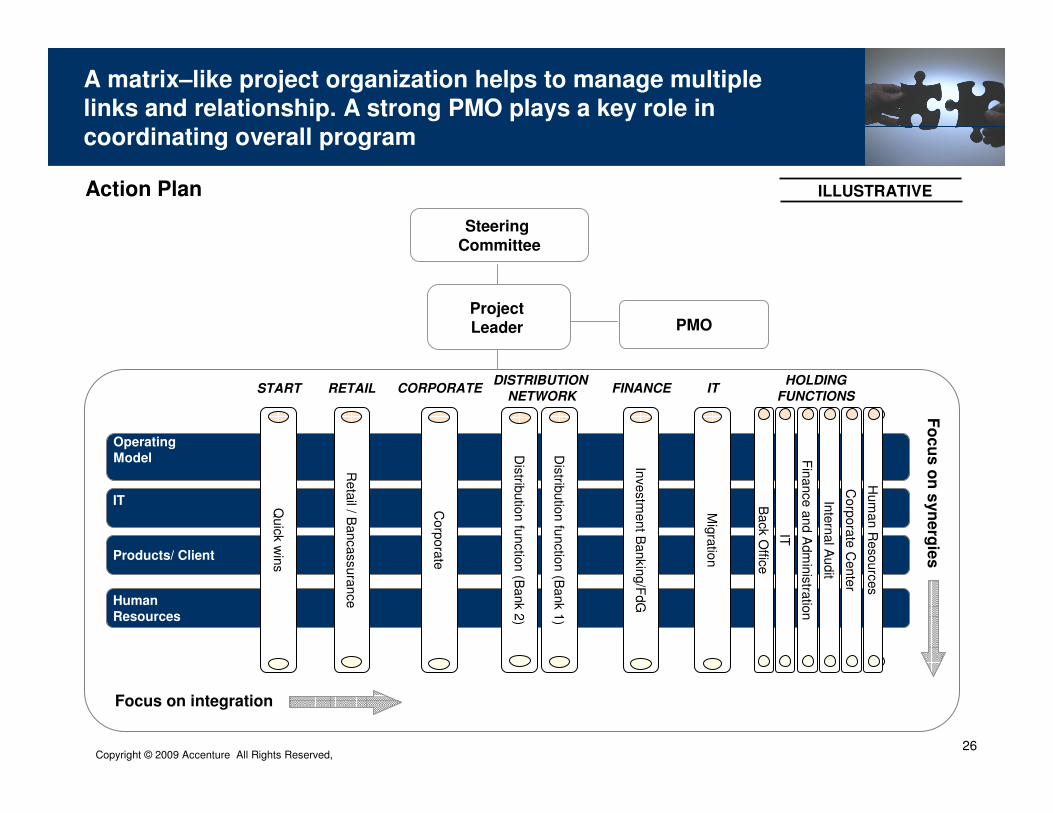

Copyright © 2009 Accenture All Rights Reserved, 26

Steering Committee

PMO

Human

Resources

Operating

Model

IT

Products/ Client

START RETAIL CORPORATEDISTRIBUTION

NETWORKFINANCE IT

HOLDING

FUNCTIONS

Mig

ratio

n

Hum

an R

eso

urc

es

Corp

ora

te C

ente

r

Inte

rnal A

udit

Fin

ance a

nd A

dm

inis

tratio

n

Corp

ora

te

Quick

win

s

Project Leader

Action Plan

A matrix–like project organization helps to manage multiple links and relationship. A strong PMO plays a key role in

coordinating overall program

Focus on integration

Fo

cu

s o

n s

yn

erg

ies

IT

Back

Offic

e

Inve

stm

ent B

ankin

g/F

dG

Dis

tributio

n fu

nctio

n (B

ank 1

)

Dis

tributio

n fu

nctio

n (B

ank 2

)

Reta

il / Bancassura

nce

ILLUSTRATIVE

Copyright © 2009 Accenture All Rights Reserved, 27

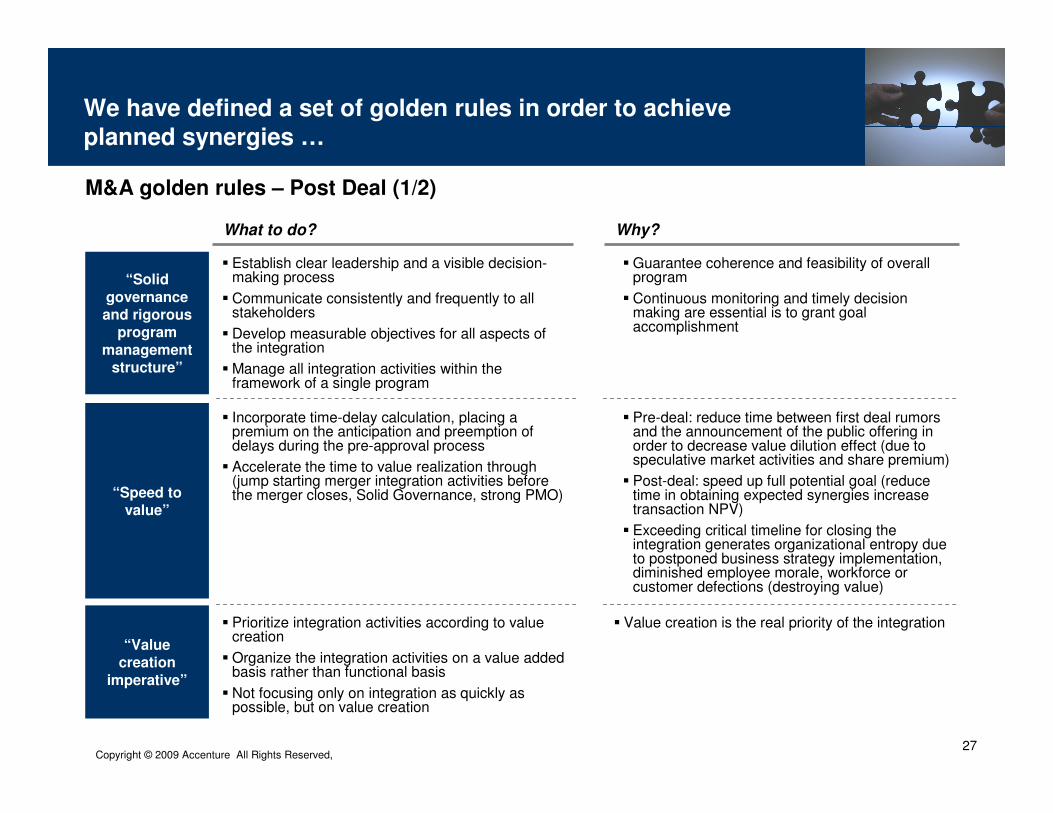

What to do? Why?

We have defined a set of golden rules in order to achieve

planned synergies …

� Establish clear leadership and a visible decision-making process

� Communicate consistently and frequently to all stakeholders

� Develop measurable objectives for all aspects of the integration

� Manage all integration activities within the framework of a single program

“Solid

governance and rigorous

program

management structure”

� Incorporate time-delay calculation, placing a premium on the anticipation and preemption of delays during the pre-approval process

� Accelerate the time to value realization through (jump starting merger integration activities before the merger closes, Solid Governance, strong PMO)“Speed to

value”

� Prioritize integration activities according to value creation

� Organize the integration activities on a value added basis rather than functional basis

� Not focusing only on integration as quickly as possible, but on value creation

� Value creation is the real priority of the integration

“Value creation

imperative”

M&A golden rules – Post Deal (1/2)

� Guarantee coherence and feasibility of overall program

� Continuous monitoring and timely decision making are essential is to grant goal accomplishment

� Pre-deal: reduce time between first deal rumors and the announcement of the public offering in order to decrease value dilution effect (due to speculative market activities and share premium)

� Post-deal: speed up full potential goal (reduce time in obtaining expected synergies increase transaction NPV)

� Exceeding critical timeline for closing the integration generates organizational entropy due to postponed business strategy implementation, diminished employee morale, workforce or customer defections (destroying value)

Copyright © 2009 Accenture All Rights Reserved, 28

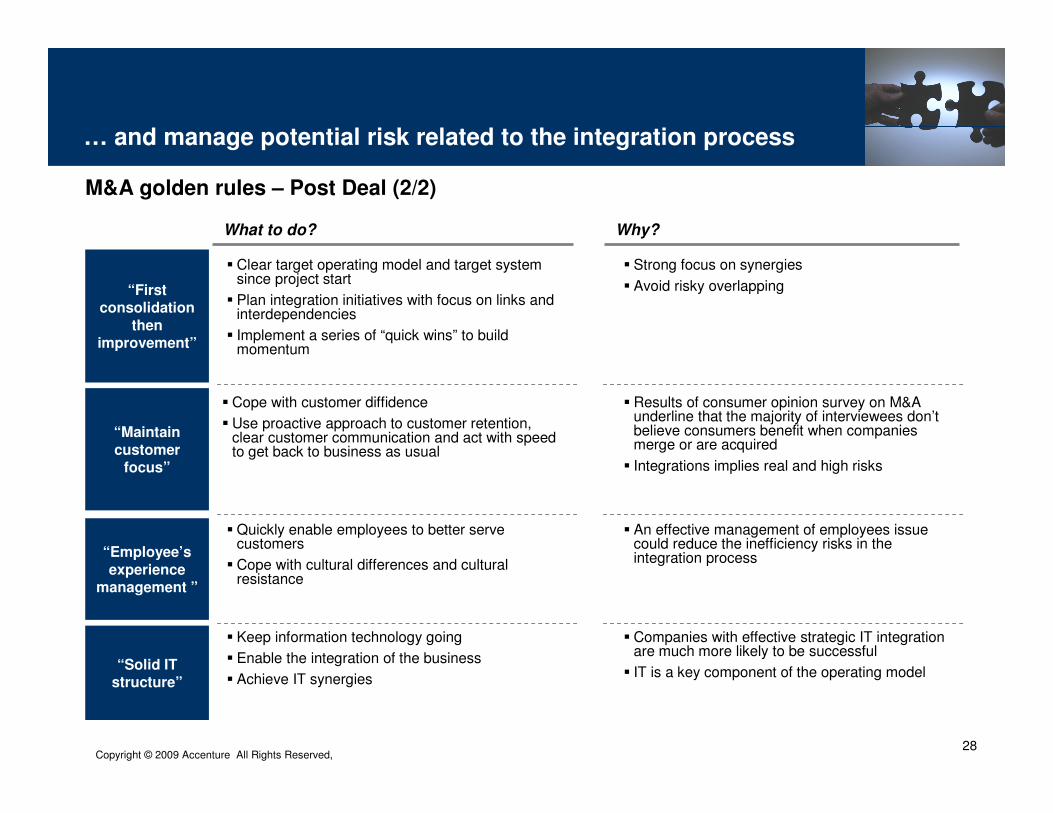

What to do? Why?

“First consolidation

then improvement”

� Cope with customer diffidence

� Use proactive approach to customer retention, clear customer communication and act with speed to get back to business as usual

� Results of consumer opinion survey on M&A underline that the majority of interviewees don’t believe consumers benefit when companies merge or are acquired

� Integrations implies real and high risks

“Maintain

customer focus”

“Employee’s

experience management ”

“Solid IT structure”

� Quickly enable employees to better serve customers

� Cope with cultural differences and cultural resistance

� An effective management of employees issue could reduce the inefficiency risks in the integration process

� Keep information technology going

� Enable the integration of the business

� Achieve IT synergies

� Companies with effective strategic IT integration are much more likely to be successful

� IT is a key component of the operating model

� Strong focus on synergies

� Avoid risky overlapping

� Clear target operating model and target system since project start

� Plan integration initiatives with focus on links and interdependencies

� Implement a series of “quick wins” to build momentum

M&A golden rules – Post Deal (2/2)

… and manage potential risk related to the integration process