strategic acquisition of alexander dennis · key adl statistics key adl financials (£ mm)(1) adl...

TRANSCRIPT

STRATEGIC ACQUISITION OF ALEXANDER DENNIS

May 28, 2019

Alexander Dennis is a Scotland headquartered global leader of lightweight single and double deck buses and motor coaches

1

Business Description

Key ADL Statistics Key ADL Financials (£ mm)(1)

ADL is a leading global manufacturer of double deck and single deck buses and motor coaches. Headquartered in Larbert, Scotland with international offices in Hong Kong, Singapore, Malaysia, New Zealand, Europe,

Canada, the United States and Mexico.

More than 120 years of British engineering heritage. In 1995 Mayflower Corporation bought Scottish bus-maker Walter Alexander (founded 1924) and in 1998 English bus-maker

Dennis Group (founded 1895). Mayflower joined Henlys Group in a JV rolling Alexander, Dennis and Henlys' Plaxton (founded 1907) into one company called TransBus International. The JV was not successful and Mayflower collapsed in 2004.

Alexander Dennis was incorporated in 2004 as a private consortium to buy a major portion of the collapsed Mayflower Corporation. Henlys' Plaxton was taken over by management and operated under the ownership of Plaxton Holdings until 2007 when it was bought by Alexander Dennis.

Propulsion expertise includes Clean Diesel, CNG, Hybrid and Battery-Electric. ADL is the UK electric bus leader (on BYD chassis) with international electric models launching in 2019

ADL provides aftermarket services in all of its markets including parts, maintenance and servicing

Company Overview

2017 2018 GrowthUnits Sold 2,345 2,533 (3% EV) 8.0%

Revenue £576 £631 9.5%

Adjusted EBITDA / % Margin £40 / 7% £44 / 7% 10.0%

Free Cashflow (2) £6.6 £18.1 175%

Number of employees 2,587

Buses in Service 31,600

Assembly Facilities Scotland (3), England (1), US (1), Canada (1)

Service and Parts Distribution locations

England (3), New Zealand (1), Singapore (1), Malaysia (1), Canada (1), USA (1)

1. All financial information regarding ADL contained in this presentation has been derived from ADL’s financial statements which are prepared in accordance with UK Generally Accepted Accounting Principles (“GAAP”). NFI prepares its financial statements in accordance with International Financial Reporting Standards (“IFRS”). UK GAAP differs in certain material respects from IFRS. Adjusted EBITDA is a non-IFRS and non-UK GAAP measure. See “Non-IFRS measures” under cautionary statements at the end of this press release.

TRANSACTIONHIGHLIGHTS

FINANCING AND PRO FORMA

LEVERAGE

Transaction Highlights

£320 million (US$405 million), transaction value funded through a combination of cash and shares– Transaction signed and closed on day of announcement (no regulatory approvals)– ADL’s primary shareholders and ADL’s CEO and CFO have elected to receive in aggregate 1.47 million NFI shares

(approx. 10% of the transaction value) issued at $31.94 per share– Equating to 2% of NFI shares outstanding following completion of the transaction

ADL management team to remain in place and will continue executing its growth strategy

Purchase price multiple of approximately 7.3x 2018 (for the 12 months ended Dec 30, 2018) Adjusted EBITDA (1)

Immediately accretive to earnings per share and free cash flow per share(1) (before potential synergies)

2

The cash consideration paid pursuant to the transaction was financed with a new US$300 mm credit facility with the remainder funded from NFI’s existing syndicated credit facility

– New credit facility has substantially the same terms as NFI’s existing syndicated credit facility

NFI pro forma total debt to estimated combined Adjusted EBITDA(1) of approximately 2.9x as at December 30, 2018

Significant deleveraging is expected over the next 18 months (to within target leverage of 2.0x to 2.5x total debt / Adjusted EBITDA) similar to the MCI transaction

NFI maintains dividend policy presently at $1.70 per share annually, paid quarterly

1. See footnote on slide 1 and “Non-IFRS measures” under cautionary statements at the end of this presentation.2. British pounds have been converted to US dollars using an exchange rate of £1.00=US$1.2663; 2018 actual figures have been converted at an exchange rate of £1.00=US$1.3355.

MARKET LEADERSHIP

INTERNATIONAL DIVERSIFICATION

A PLATORM FOR GROWTH

ENHANCES NFIPRODUCT PORTFOLIO

COST EFFECTIVE PLATFORM

FINANCIALLY COMPELLING

STRONG CULTURAL FIT WITH

COMMITMENT TO SAFETY AND

ENVIRONMENT

Strategic Acquisition Rationale

3

ADL is the #1 UK bus manufacturer and #1 global producer of double-decker buses with a well established international presence- Significant installed base in UK, Hong Kong, Canada, USA and New Zealand

Growing North America business which augments NFI’s product breadth and customer reach Successful track record of accessing and growing in new markets globally

- Recent success in Continental Europe (Poland, Switzerland and Germany) provides a platform for further expansion into Western Europe - Operating model in Mexico to be utilized to investigate additional growth

ADL revenue split: Bus = 84% of total sales, Motor coach = 5%, and Parts/Service = 11%

Adds its class leading, internationally proven line-up of single-deck and double-deck buses Sharing of best practices, and the optimization of existing partnerships internationally Enhances NFI’s technical competencies on lightweight chassis / bodies UK’s market leading electric bus business with significant product know-how and first mover advantage

ADL operates flexible assembly model (both internal and 3rd party) with deep manufacturing and engineering talent Operates successfully in very competitive environments with cost competitive buses assembled in the UK primarily for the UK, in the US and

Canada for domestic markets and even more cost competitive in foreign markets with local sourcing and 3rd party assembly

Strong cultural alignment between NFI and ADL with longstanding relationships and mutual respect- Share similar cultures and values, especially towards quality, technology, innovation and customer experience- Clear alignment on management strategy, market outlook, and EV adoption expectations

ADL commitment to sustainable mobility and completely aligned with NFI

ADL management to remain in place and to drive performance and international growth

Immediately accretive to earnings per share and free cash flow(1)(2) per share (before synergies) Rapid deleveraging to NFI’s target range of 2.0x to 2.5x total debt to Adjusted EBITDA is expected over the next 18 months(1)

Significant acquisition whilst maintaining NFI dividend policy Potential to capture revenue and cost synergies from the sharing of best practices and a combined market approach in North America

1. See footnote on slide 1 and “Non-IFRS measures” under cautionary statements at the end of this presentation.

ADL is well aligned with NFI’s Strategy

4

1. Offer global operators the best buses, services and value in the industry Migrate from selling buses to providing solutions…that deliver best value & support for life Provide complete offering: Bus (“Workhorse of the Fleet”) supported by Parts & Service Lead market innovation with diverse propulsion offering on proven bus platforms Increased focus on Aftermarket Parts and Services (such as telematics, infrastructure, etc.)

2. Operate as a world class OEM using LEAN Principles (OpEx) & Quality Roadmap Be recognized as an Employer of Choice Excel in supply chain, strategic sourcing and appropriate in-sourcing Continuous pursuit of eliminating waste and cost reduction to improve competitiveness Excel at customer support, response and follow-up Operate as a responsible, sustainable and environmentally conscious business

3. Perform while seeking Growth and Diversification into New Markets Deliver attractive returns to shareholders through capital appreciation and dividends Operate with a prudent capital structure preserving flexibility to invest and grow the business Seek to diversify: Product (type of bus) and/or Market (Public vs. Private) and/or Geography (North America vs. International)

Market leadership, world class operations and prudent growth into new markets

NFI MISSION: To move people with leading transportation solutions that are safe, accessible, efficient, and reliable.

NFI VISION: To enable the future of mobility with innovative and sustainable solutions.

NFI STRATEGY:

5 1. Sales also include used / third-party chassis (£26 mm / 4% of total). All figures based on UK GAAP. 2. Source: UK Bus Registration Data, ADL Management estimates.

ManufacturingSingle Deck / Double Deck Buses Motor Coaches

2018A Sales(1):

£528 mm(84% of total)

Enviro400

Broad range of lightweight double deck (2 axle and 3 axle) and single deck products

Complete design offering– Proprietary in-house production and development of bus

chassis and bodies– UK EV chassis through strategic relationship with BYD

Best-in-class reliability and fuel efficiency

Leader in Green Propulsion Options Partnerships with leading technology partners and global battery

manufacturers including BYD Enviro200 electric vehicle variant best selling in the UK with 70%

market share(2)

Double deck EV variants launching in 2019 in the UK and North America (on ADL Chassis)

Panorama

2018A Sales(1):

£32 mm(5% of total)

Full range of bodies with best-in-class reliability, configurability, and fuel efficiency

Utilization of Volvo and Scania chassis

Strong UK presence with export opportunities available (Successful entrance to New Zealand market)

Aftermarket

2018A Sales(1):

£71 mm(11% of total)

Sale of body and chassis parts, engineering, maintenance, and diagnostics

Online ordering through AD24 platform

Currently UK focused with planned international expansion

Developing tech-driven aftermarket systems to develop sales, improve margins and enhance the customer experience

Product Segment Overview

PantherEnviro200EV

6

Countries with recent ADL Deliveries

Single / Double Deck Buses Motor Coaches

ADL 2018A Revenue Breakdown(1)

Global Player with Diversified Revenue Stream

ADLADL Manufacturing Location3rd Party Manufacturing LocationCountries with Operations / Sales Offices

ADL Manufacturing Footprint

1. Excludes FX adjustments.

United Kingdom

Hong Kong

Ireland

Singapore

United States

Malaysia

Canada

New Zealand

United Kingdom

Poland

Ireland

New Zealand

Mexico Switzerland

49%

27%

12%1%

11% U.K.Asia PacificNorth AmericaOther DevelopingAftermarket

Track Record of Successful International Expansion

7

2004 2007

Scottish investor group acquires former Alexander and Dennis businesses; ADL is formed

2008 2015 2016 2017 2018

Colin Robertson joins ADL as CEO

ADL acquires Plaxton (UK #1 coach body builder)

Joint Venture with Kiwi Bus Builders in New Zealand

Manufacturing alliance with Zhuhai in China

JV with New Flyer in North America

Manufacturing alliance with ABC in the United States

Multi-year order from Metrolinx in Toronto, Canada

Entry into Malaysia and Singapore markets

Supplied coach bodies to PolskiBus in Poland

Nappanee, USA facility acquired in early 2017

Entry into Mexican and Swiss market

Electric model of Enviro200launched in the UK

ADL wins contract to supply double deck fleet to BVG in Berlin

Initial sales of electric model of Enviro400 to be delivered in 2019

AD24 launched. An online portal for parts sales, training and manuals

2012

Partner in Malaysia to start production in APAC

8

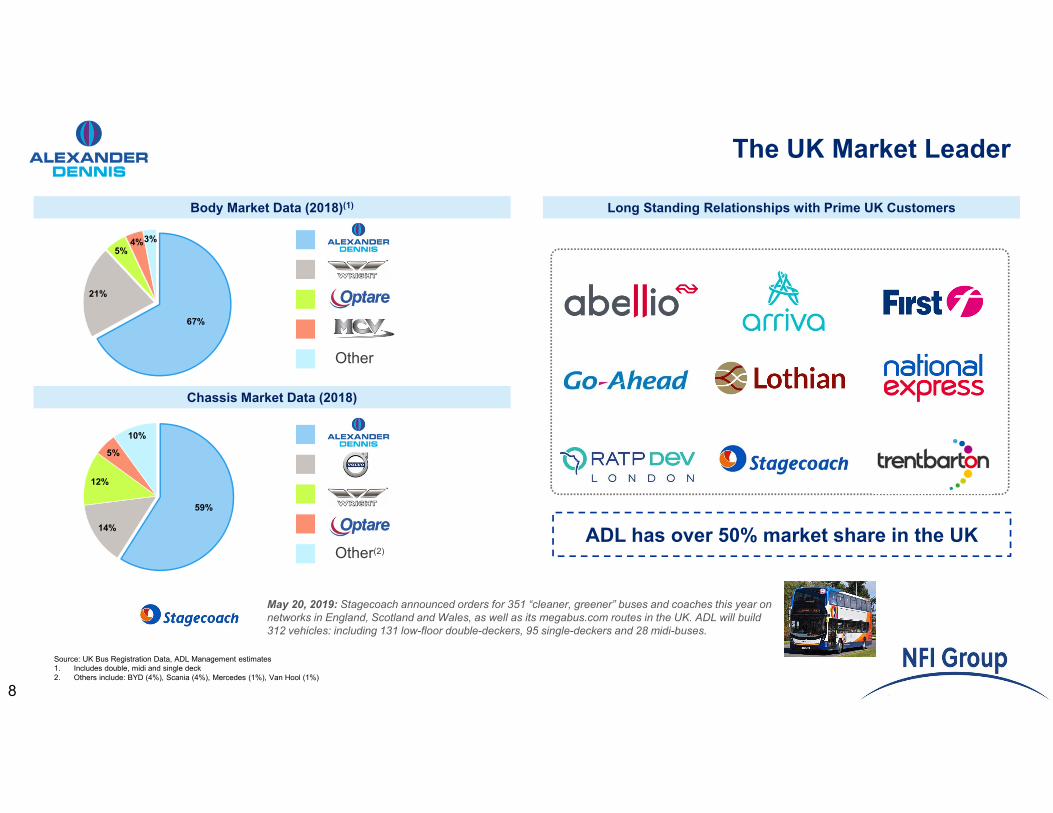

Body Market Data (2018)(1)

ADL has over 50% market share in the UK

The UK Market Leader

Source: UK Bus Registration Data, ADL Management estimates 1. Includes double, midi and single deck2. Others include: BYD (4%), Scania (4%), Mercedes (1%), Van Hool (1%)

Chassis Market Data (2018)

Long Standing Relationships with Prime UK Customers

May 20, 2019: Stagecoach announced orders for 351 “cleaner, greener” buses and coaches this year on networks in England, Scotland and Wales, as well as its megabus.com routes in the UK. ADL will build 312 vehicles: including 131 low-floor double-deckers, 95 single-deckers and 28 midi-buses.

67%

21%

5%4%3%

Other

59%

14%

12%

5%

10%

Other(2)

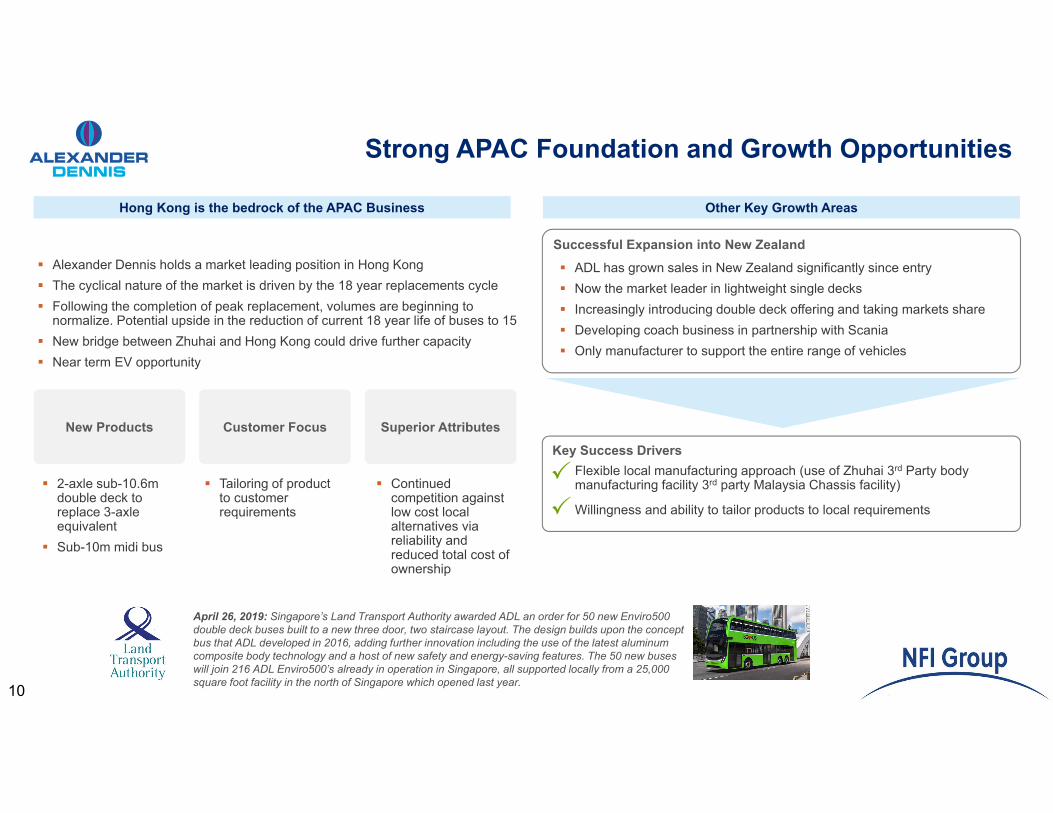

Strong APAC Foundation and Growth Opportunities

10

Hong Kong is the bedrock of the APAC Business

Alexander Dennis holds a market leading position in Hong Kong The cyclical nature of the market is driven by the 18 year replacements cycle Following the completion of peak replacement, volumes are beginning to

normalize. Potential upside in the reduction of current 18 year life of buses to 15 New bridge between Zhuhai and Hong Kong could drive further capacity Near term EV opportunity

Other Key Growth Areas

New Products Customer Focus Superior Attributes

2-axle sub-10.6m double deck to replace 3-axle equivalent

Sub-10m midi bus

Tailoring of product to customer requirements

Continued competition against low cost local alternatives via reliability and reduced total cost of ownership

Successful Expansion into New Zealand

Flexible local manufacturing approach (use of Zhuhai 3rd Party body manufacturing facility 3rd party Malaysia Chassis facility)

Key Success Drivers

Willingness and ability to tailor products to local requirements

ADL has grown sales in New Zealand significantly since entry Now the market leader in lightweight single decks Increasingly introducing double deck offering and taking markets share Developing coach business in partnership with Scania Only manufacturer to support the entire range of vehicles

April 26, 2019: Singapore’s Land Transport Authority awarded ADL an order for 50 new Enviro500 double deck buses built to a new three door, two staircase layout. The design builds upon the concept bus that ADL developed in 2016, adding further innovation including the use of the latest aluminum composite body technology and a host of new safety and energy-saving features. The 50 new buses will join 216 ADL Enviro500’s already in operation in Singapore, all supported locally from a 25,000 square foot facility in the north of Singapore which opened last year.

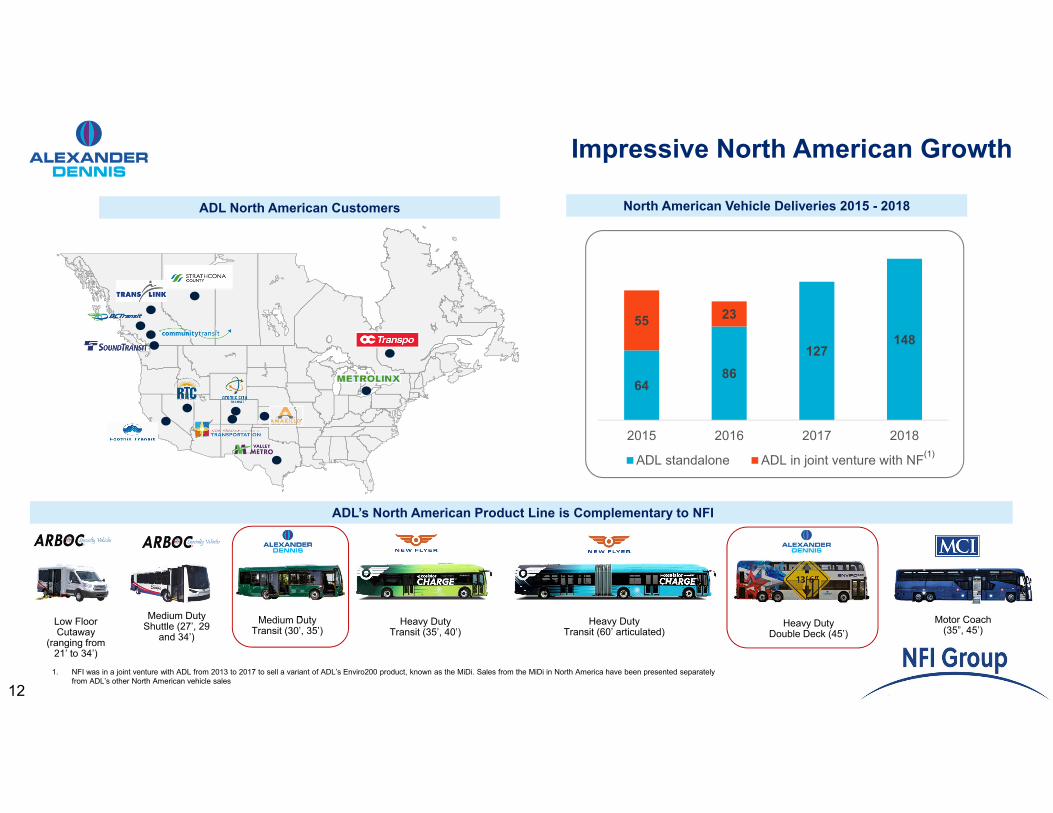

Impressive North American Growth

12

North American Vehicle Deliveries 2015 - 2018

ADL’s North American Product Line is Complementary to NFI

Low Floor Cutaway

(ranging from 21’ to 34’)

Medium DutyShuttle (27’, 29

and 34’)

Medium DutyTransit (30’, 35’)

Heavy DutyTransit (35’, 40’)

Heavy DutyTransit (60’ articulated)

Heavy DutyDouble Deck (45’)

6486

127148

55 23

2015 2016 2017 2018

ADL standalone ADL in joint venture with NF

ADL North American Customers

Motor Coach(35”, 45’)

(1)

1. NFI was in a joint venture with ADL from 2013 to 2017 to sell a variant of ADL’s Enviro200 product, known as the MiDi. Sales from the MiDi in North America have been presented separately from ADL’s other North American vehicle sales

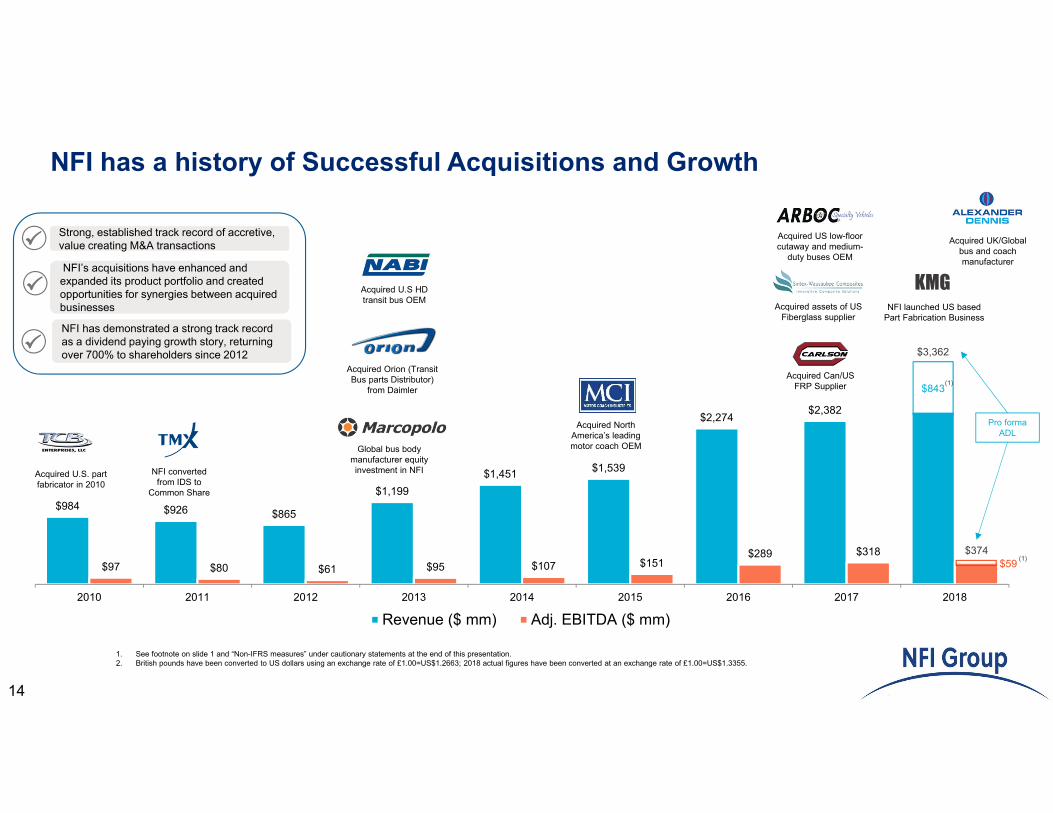

$984 $926 $865

$1,199 $1,451 $1,539

$2,274 $2,382

$97 $80 $61 $95 $107 $151 $289 $318

2010 2011 2012 2013 2014 2015 2016 2017 2018

Revenue ($ mm) Adj. EBITDA ($ mm)

14

Acquired U.S. part fabricator in 2010

NFI converted from IDS to

Common Share

Global bus body manufacturer equity investment in NFI

Acquired Orion (Transit Bus parts Distributor)

from Daimler

Acquired U.S HD transit bus OEM

Acquired North America’s leading motor coach OEM

Acquired Can/USFRP Supplier

Acquired assets of US Fiberglass supplier

Acquired US low-floor cutaway and medium-

duty buses OEM

$843

$3,362

$374$59

Acquired UK/Global bus and coach manufacturer

Pro forma ADL

(1)

(1)

NFI has a history of Successful Acquisitions and Growth

Strong, established track record of accretive, value creating M&A transactions

NFI has demonstrated a strong track record as a dividend paying growth story, returning over 700% to shareholders since 2012

NFI’s acquisitions have enhanced and expanded its product portfolio and created opportunities for synergies between acquired businesses NFI launched US based

Part Fabrication Business

KMG

1. See footnote on slide 1 and “Non-IFRS measures” under cautionary statements at the end of this presentation.2. British pounds have been converted to US dollars using an exchange rate of £1.00=US$1.2663; 2018 actual figures have been converted at an exchange rate of £1.00=US$1.3355.

15

NFI Group Leadership

Janice HarperExecutive Vice President

Human ResourcesJoined in 1998

Glenn AshamExecutive Vice President

Chief Financial OfficerJoined in 1992

David WhiteExecutive Vice President

Supply ManagementJoined in 1996

Colin PewarchukExecutive Vice President

General CounselJoined in 2006

Paul SoubryPresident & CEO

Joined in 2009

Chris StoddartPresident

Transit BusJoined in 2008

Ian SmartPresident

Motor CoachJoined in 2011

Brian DewsnupPresidentNFI Parts

Joined in 2006

Colin RobertsonCEO ADL &

President NFI InternationalJoined in 2007

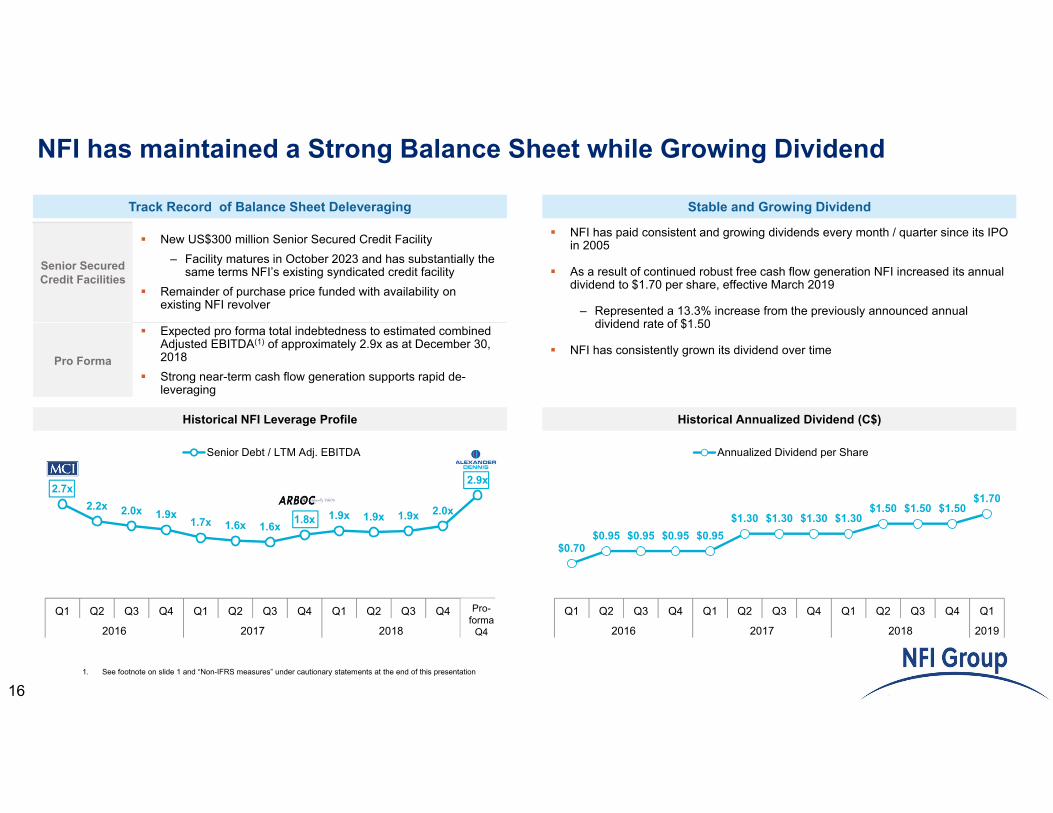

NFI has maintained a Strong Balance Sheet while Growing Dividend

16

Track Record of Balance Sheet Deleveraging Stable and Growing Dividend

Senior Secured Credit Facilities

New US$300 million Senior Secured Credit Facility– Facility matures in October 2023 and has substantially the

same terms NFI’s existing syndicated credit facility Remainder of purchase price funded with availability on

existing NFI revolver

Pro Forma

Expected pro forma total indebtedness to estimated combined Adjusted EBITDA(1) of approximately 2.9x as at December 30, 2018

Strong near-term cash flow generation supports rapid de-leveraging

Historical NFI Leverage Profile

2.7x 2.2x 2.0x 1.9x

1.7x 1.6x 1.6x 1.8x 1.9x 1.9x 1.9x 2.0x

2.9x

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018 2019

Senior Debt / LTM Adj. EBITDA

Historical Annualized Dividend (C$)

$0.70 $0.95 $0.95 $0.95 $0.95

$1.30 $1.30 $1.30 $1.30 $1.50 $1.50 $1.50

$1.70

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018 2019

Annualized Dividend per Share

NFI has paid consistent and growing dividends every month / quarter since its IPO in 2005

As a result of continued robust free cash flow generation NFI increased its annual dividend to $1.70 per share, effective March 2019

– Represented a 13.3% increase from the previously announced annual dividend rate of $1.50

NFI has consistently grown its dividend over time

1. See footnote on slide 1 and “Non-IFRS measures” under cautionary statements at the end of this presentation

Pro-forma

Q4

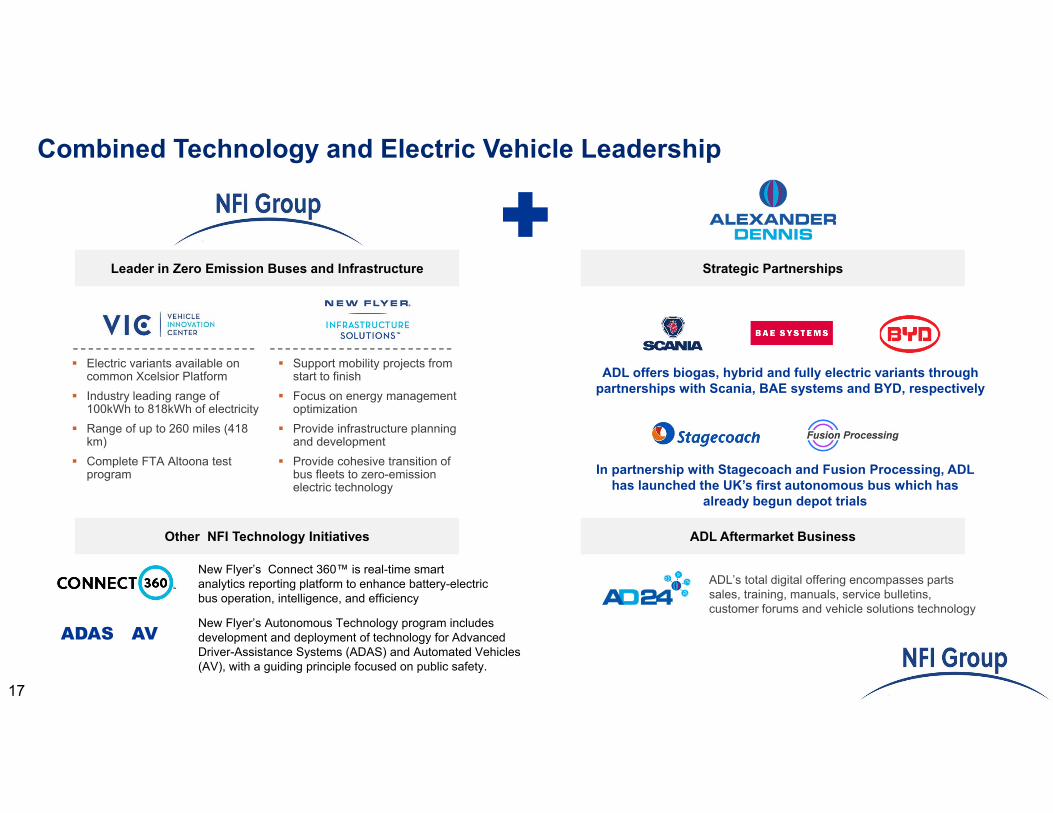

Combined Technology and Electric Vehicle Leadership

17

Leader in Zero Emission Buses and Infrastructure

Other NFI Technology Initiatives

Electric variants available on common Xcelsior Platform

Industry leading range of 100kWh to 818kWh of electricity

Range of up to 260 miles (418 km)

Complete FTA Altoona test program

Support mobility projects from start to finish

Focus on energy management optimization

Provide infrastructure planning and development

Provide cohesive transition of bus fleets to zero-emission electric technology

ADAS AV

Strategic Partnerships

ADL’s total digital offering encompasses parts sales, training, manuals, service bulletins, customer forums and vehicle solutions technology

ADL Aftermarket Business

ADL offers biogas, hybrid and fully electric variants through partnerships with Scania, BAE systems and BYD, respectively

In partnership with Stagecoach and Fusion Processing, ADL has launched the UK’s first autonomous bus which has

already begun depot trials

New Flyer’s Connect 360™ is real-time smart analytics reporting platform to enhance battery-electric bus operation, intelligence, and efficiency

New Flyer’s Autonomous Technology program includes development and deployment of technology for Advanced Driver-Assistance Systems (ADAS) and Automated Vehicles (AV), with a guiding principle focused on public safety.

Key Transaction Highlights

• Market Leadership, international diversification, and a platform for growth

• Enhances NFI product portfolio

• Cost effective platform

• Financial compelling

• Strong cultural fit with commitment to safety and environment

18

Non-IFRS measuresAll financial information regarding ADL contained in this presentation has been derived from ADL’s financial statements which are prepared in accordance with UK GAAP. NFI prepares its financial statements in accordance with IFRS. UK GAAP differs in certain material respects from IFRS.

ADL’s “Adjusted EBITDA” referred to in this press release has been calculated by ADL’s management and consists of earnings before interest, income taxes, depreciation, amortization, product development costs and other non-cash charges and certain non-recurring charges. References to “Adjusted EBITDA” are to earnings before interest, income taxes, depreciation and amortization after adjusting for the effects of certain non-recurring and/or non-operations related items as referred to in the Company’s public filings plus estimated adjustments to ADL’s Adjusted EBITDA for conversion from UK GAAP to IFRS. NFI’s free cash flow means net cash generated by operating activities adjusted as referred to in the Company’s public filings. References to ADL’s free cash flow means net cash generated by operating activities with certain adjustments, prepared on a UK GAAP basis. Management believes Adjusted EBITDA and free cash flow are useful measures in evaluating the performance of the Company. However, these terms are not recognized earnings measures under UK GAAP or IFRS and do not have standardized meanings prescribed by UK GAAP or IFRS. Readers are cautioned that these terms should not be construed as an alternative to net earnings or loss or cash flows from operating activities determined in accordance with UK GAAP or IFRS. NFI's and ADL’s method of calculating Adjusted EBITDA and free cash flow may differ materially from the methods used by other issuers and, accordingly, may not be comparable to similarly titled measures used by other issuers.

Forward-looking statementsThis press release contains forward-looking statements relating to expected future events and results, including plans for the combination and integration of the acquired business into NFI’s existing business and expected synergies, the diversification and growth of the combined businesses, the accretive effects of the transaction to revenue, earnings and cash flow of NFI and expected future financial deleveraging. Actual events and results may differ materially from management expectations as projected in such forward-looking statements for a variety of reasons, including risks related to acquisitions, joint ventures and other strategic relationships with third parties, risks related to operations in existing, new and emerging markets, the ability to implement the operational changes necessary to achieve expected or potential synergies, market and general economic conditions, political developments in the countries where the Company operates and funding availability for customers to purchase buses and coaches and to purchase parts or services, the covenants contained under NFI’s credit facilities could impact the ability of NFI to make strategic investments and fund dividends and the other risks and uncertainties discussed in the materials filed with the Canadian securities regulatory authorities and available on SEDAR at www.sedar.com. Due to the potential impact of these factors, the Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, unless required by applicable law.

Cautionary Statements

19