spiceworks: the 2015 it budget report

TRANSCRIPT

1Where IT goes to work.

FREE IT REPORTS ON TODAY’S HOTTEST TECH TOPICS AND TRENDS.

AS TECH BUDGETS LEVEL OFF IN 2015, MARKETERS NEED TO COACH THEIR BUYERS TO THE FINISH LINE.

2

TABLE OF CONTENTS

3

00

THE STARTING LINE

01

IT BUDGETS: SLOW &

STEADY

02

TECH HURDLES ON

THE HORIZON

03

HOW TO BECOME A

MARKETING CHAMP

04

CLOSING CEREMONIES

4

00CHAPTER

5

ON YOUR MARK... Why can’t Pete, IT manager, get approval for

those sweet new SSDs? And what’s the hold-up

with those company-wide software upgrades?

It looks like budgets in 2015 will be slow to

react to the starting gun.

Fortunately, there’s plenty marketers can do to

adjust their 2015 campaigns and coach buyers

to the “purchase” finish line. But what exactly

is causing sluggish budget growth? Let’s travel

back in time…

MEET PETE, IT MANAGER

Early 2014. A weak start to the year. While

athletes were winning gold at the Winter

Olympics, most IT budgets... seemed to

miss the starting gun. Couple that with

global economic uncertainty leading into

2015. What’s it all mean? You guessed it:

Restrained global IT budgets over the

coming 12 months.

For tech marketers, it ’s a challenging reali-

ty to face: Selling to IT pros with shoestring

budgets that are slowing their purchase

potential. But don’t throw in the towel just

yet; Spiceworks’ tech marketing experts

are here to help. We suggest focusing your

marketing strategies on cost savings and

productivity gains for tech buyers in 2015.

It will take hard work and training, but

marketers and IT pros alike can still go

for the gold.Only a third of IT pros expect their budgets to pick up speed in 2015.

KEY HIGHLIGHTSGIVE ME THE 30 SEC RE-CAP

Over half of IT pros surveyed

said their company’s revenue would

increase in 2015. Unfortunately, the

same can’t be said for IT budgets that

are still running at their 2014 pace.

Only a third of IT pros surveyed

expect their budgets to pick up speed

in 2015. This is a decrease from the 42%

who indicated a budget increase in our

State of IT survey published in Q2 2014.

In addition, only one quarter of IT pros

said their IT department would add

new employees.

IT is cramping up: Aging hardware

and software will force many IT pros

to spend more on IT refreshes vs. new

projects. Over half of PCs on the Spice-

works anonymized aggregate network

are more than four years old (in tech

years, that’s ancient).

Further, more than a third of respondents

will need to migrate from Windows Server

2003 due to its end of life in July 2015,

making upgrades a top priority for many

IT pros.

Tech marketers can go from passive viewer

to interactive instructor. A few strategic tips

and you’ll be sharing a place on the podium

with IT buyers.

1

2

3

6

01CHAPTER

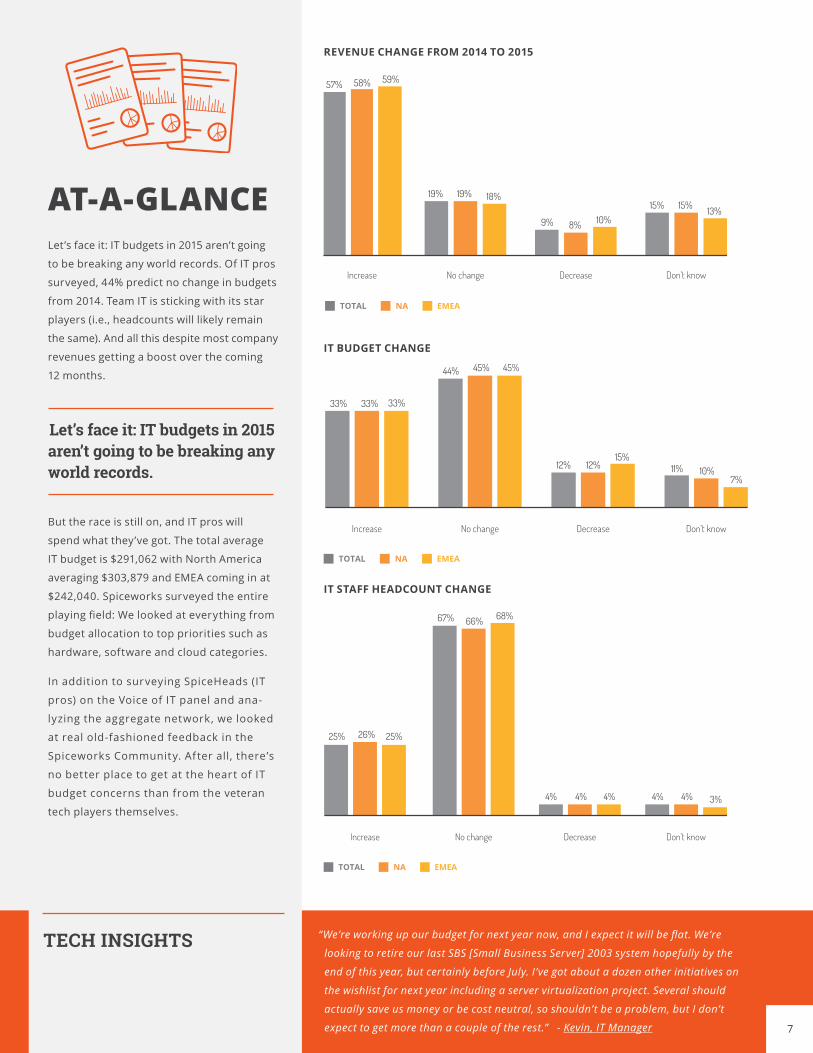

AT-A-GLANCE Let’s face it: IT budgets in 2015 aren’t going

to be breaking any world records. Of IT pros

surveyed, 44% predict no change in budgets

from 2014. Team IT is sticking with its star

players (i.e., headcounts will likely remain

the same). And all this despite most company

revenues getting a boost over the coming

12 months.

But the race is still on, and IT pros will

spend what they’ve got. The total average

IT budget is $291,062 with North America

averaging $303,879 and EMEA coming in at

$242,040. Spiceworks surveyed the entire

playing field: We looked at everything from

budget allocation to top priorities such as

hardware, software and cloud categories.

In addition to surveying SpiceHeads (IT

pros) on the Voice of IT panel and ana-

lyzing the aggregate network, we looked

at real old-fashioned feedback in the

Spiceworks Community. After all, there’s

no better place to get at the heart of IT

budget concerns than from the veteran

tech players themselves.

REVENUE CHANGE FROM 2014 TO 2015

IT BUDGET CHANGE

Let’s face it: IT budgets in 2015 aren’t going to be breaking any world records.

IT STAFF HEADCOUNT CHANGE

“We’re working up our budget for next year now, and I expect it will be flat. We’re

looking to retire our last SBS [Small Business Server] 2003 system hopefully by the

end of this year, but certainly before July. I’ve got about a dozen other initiatives on

the wishlist for next year including a server virtualization project. Several should

actually save us money or be cost neutral, so shouldn’t be a problem, but I don’t

expect to get more than a couple of the rest.” - Kevin, IT Manager

TECH INSIGHTS

TOTAL NA EMEA

57% 58% 59%

19% 19% 18%

9% 8% 10%15%15% 13%

Increase No change Decrease Don’t know

Increase No change Decrease Don’t know

33% 33% 33%

44% 45% 45%

12% 12%15%

11% 10%7%

TOTAL NA EMEA

Increase No change Decrease Don’t know

25% 26% 25%

67% 66% 68%

4% 4% 4% 4% 4% 3%

TOTAL NA EMEA

7

8

FOCUS ON SPEND(ING) Where are IT pros focusing their spend

in 2015? Client hardware still takes the

gold (41%) with software projects in the

silver position (33%). Hosted/cloud-

based services projects and managed

services get the bronze.

It ’s no surprise that the top priorities for

2015 IT budgets are laptops/desktops

(44%) and software (42%) – which aligns

with plans for IT budget allocation for

2015. And the final standings are…

ALLOCATION OF 2015 ANNUAL IT BUDGET

It’s no surprise that the top priorities for 2015 IT budgets are laptops/ desktops and software.

TOP IT BUDGET PRIORITIES IN 2015

Hardware projects Software projects Hosted/cloud-based services projects

Don’t know

41%

Managed servicesprojects

42%39%

33% 34% 33%

12% 12% 13%10% 9%

12%

3% 3% 3%

TOTAL NA EMEA

Software

Laptop/Desktop

Storage

Virtualization

Networking

Mobile

Cloud-based servers

Security

Physical servers

44%

42%

46%

42%

40%

48%

35%

33%

36%

34%

34%

32%

32%

35%

26%

13%

14%

10%

29%

21%

23%

21%

30%

27%

29%

32%

31%

TOTAL NA EMEA

9

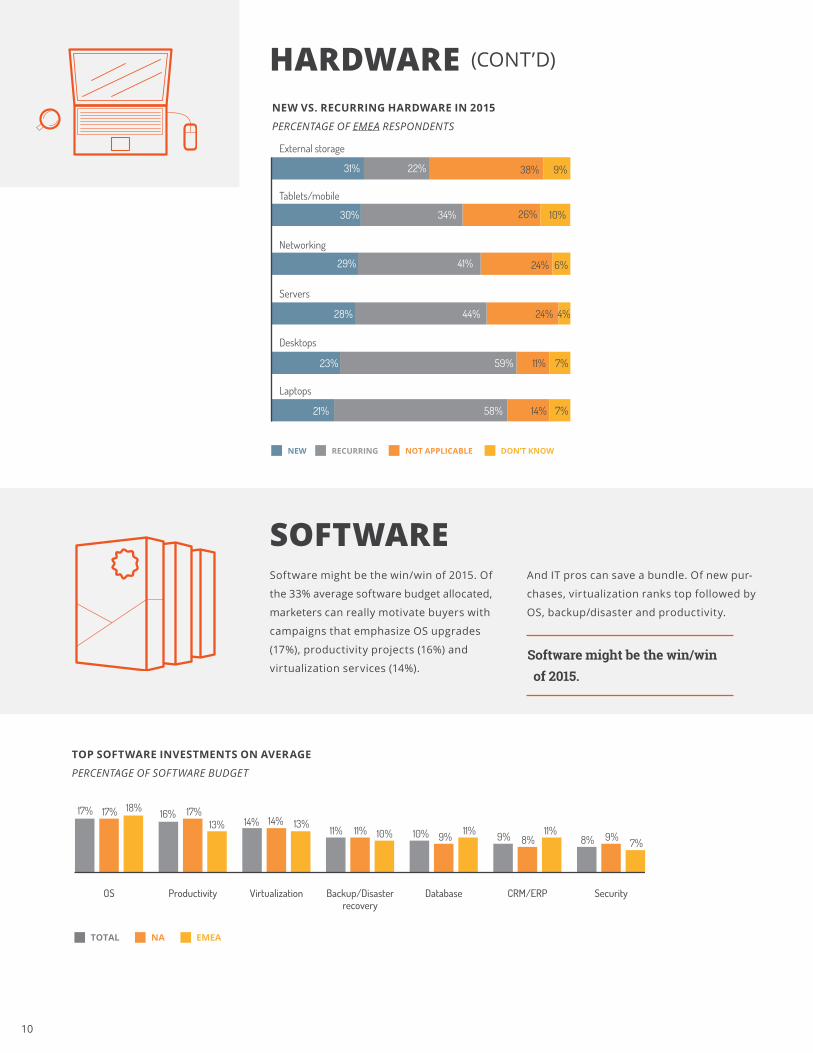

HARDWARE Steady budget pace? Sure. But good

old-fashioned hardware is still in Pete’s

purchase arena. Of the 41% average

hardware budget allocated, desktops

(19%) get top ranking followed by servers

(18%), laptops (14%) and networking (9%).

Servers top the chart for new

purchases followed by networking

(wireless, routers, switches), tablets/

mobile devices, and external storage.

Servers top the chart for new purchases followed by networking mobile devices, and external storage.

TOP HARDWARE INVESTMENTS ON AVERAGE

PERCENTAGE OF HARDWARE BUDGET

NEW VS. RECURRING HARDWARE IN 2015

PERCENTAGE OF TOTAL RESPONDENTS

External storage(SAN, NAS, etc.)

Networking(wireless, routers,

switches)

LaptopsServersDesktops

20% 19%22%

19% 20%17% 15% 15% 14%

10% 10% 9% 8% 7% 9%

Tablets/mobile

7% 7% 8%

TOTAL NA EMEA

Servers

37% 37% 19%

Networking

Tablets/mobile

External storage

Desktops

Laptops

7%

33% 38% 21% 8%

9%26% 33%32%

10%35%25%30%

29% 52% 13% 6%

26% 53% 14% 7%

RECURRING NOT APPLICABLE DON’T KNOWNEW

NEW VS. RECURRING HARDWARE IN 2015

PERCENTAGE OF NORTH AMERICA RESPONDENTS

5%

Servers

Networking

Tablets/mobile

External storage

Desktops

Laptops

18%35%42%

35% 38% 19% 8%

33% 23% 36% 8%

32% 50% 14% 4%

30% 27% 33% 10%

29% 51% 14% 6%

RECURRING NOT APPLICABLE DON’T KNOWNEW

What factors do IT pros like Pete take into consideration before the hardware purchase

gun even fires? According to respondents, the top considerations are reliability, value

and service/support.

PURCHASE STRETCH #1

10

TOP SOFTWARE INVESTMENTS ON AVERAGE

PERCENTAGE OF SOFTWARE BUDGET

HARDWARE (CONT’D) NEW VS. RECURRING HARDWARE IN 2015

PERCENTAGE OF EMEA RESPONDENTS

SOFTWARESoftware might be the win/win of 2015. Of

the 33% average software budget allocated,

marketers can really motivate buyers with

campaigns that emphasize OS upgrades

(17%), productivity projects (16%) and

virtualization services (14%).

And IT pros can save a bundle. Of new pur-

chases, virtualization ranks top followed by

OS, backup/disaster and productivity.

Software might be the win/win of 2015.

OS

17%

Productivity Virtualization Backup/Disasterrecovery

Database CRM/ERP Security

17% 18% 16% 17%13% 14% 14% 13%

11% 11% 10% 10% 9% 11% 9% 8%11%

8% 9% 7%

TOTAL NA EMEA

External storage

Tablets/mobile

Networking

Servers

Desktops

Laptops

31%

30%

29%

28%

23%

21%

22%

34%

41%

44%

59%

58%

38%

26%

24%

24%

11%

14%

9%

10%

6%

4%

7%

7%

RECURRING NOT APPLICABLE DON’T KNOWNEW

11

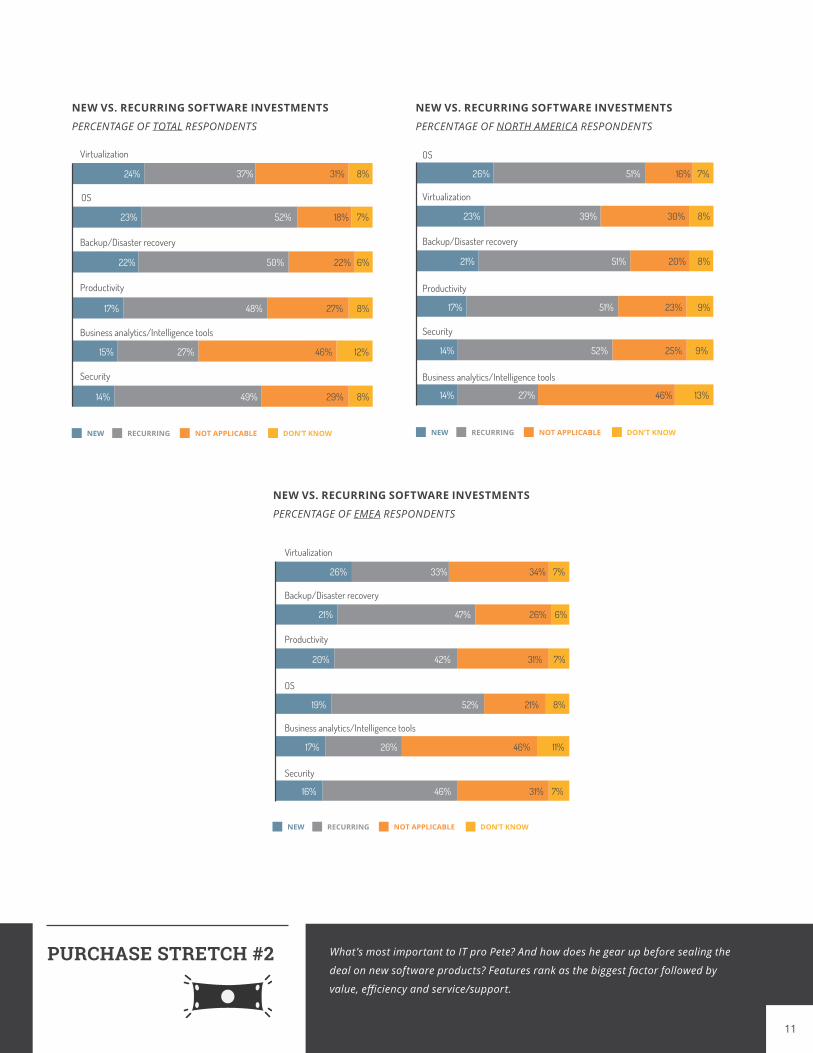

Virtualization

OS

Backup/Disaster recovery

Productivity

Business analytics/Intelligence tools

Security

24%

23%

22%

17%

15%

14%

37%

52%

50%

48%

27%

49%

31%

18%

22%

27%

46%

29% 8%

12%

8%

6%

7%

8%

RECURRING NOT APPLICABLE DON’T KNOWNEW

NEW VS. RECURRING SOFTWARE INVESTMENTS

PERCENTAGE OF TOTAL RESPONDENTS

NEW VS. RECURRING SOFTWARE INVESTMENTS

PERCENTAGE OF NORTH AMERICA RESPONDENTS

NEW VS. RECURRING SOFTWARE INVESTMENTS

PERCENTAGE OF EMEA RESPONDENTS

OS

Virtualization

Backup/Disaster recovery

Productivity

Security

Business analytics/Intelligence tools

26%

23%

21%

9%

9%

8%

8%

7%

25%

23%

20%

30%

16%

52%

51%

51%

39%

51%

17%

14%

14% 13%46%27%

RECURRING NOT APPLICABLE DON’T KNOWNEW

26%

11%

8%

7%

6%

7%

7%

46%

21%

31%

26%

34%

31%

26%

52%

42%

47%

33%

46%

17%

19%

20%

21%

16%

Virtualization

OS

Backup/Disaster recovery

Productivity

Business analytics/Intelligence tools

Security

RECURRING NOT APPLICABLE DON’T KNOWNEW

What’s most important to IT pro Pete? And how does he gear up before sealing the

deal on new software products? Features rank as the biggest factor followed by

value, efficiency and service/support.

PURCHASE STRETCH #2

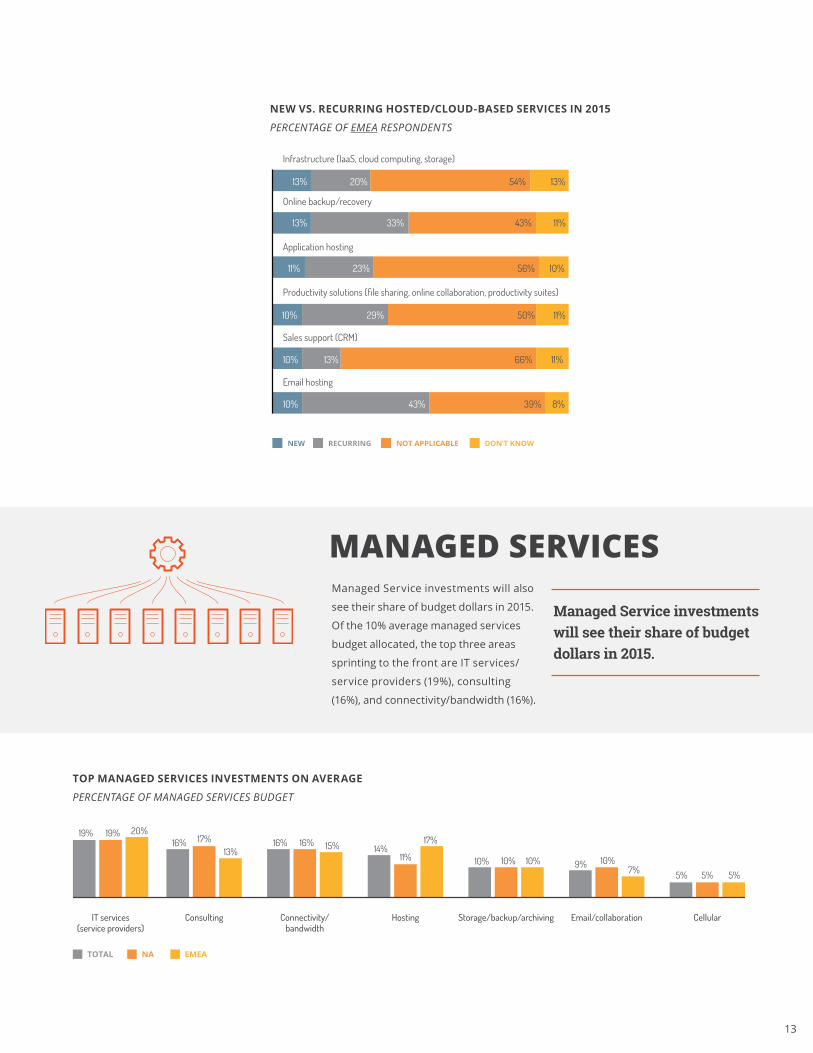

CLOUD As IT pros circle the track, cloud floats onto the purchase field. Of the

12% average cloud/hosting services budget allocated, email hosting

(18%), web hosting (16%) and online backup/recovery (13%) are all mak-

ing the rounds in the IT Budget Stadium in 2015.

When it comes to new purchases for cloud-based projects, online back-

up/recovery is out ahead followed by productivity solutions

and email hosting.

When it comes to new purchases for cloud-based projects, online backup/recovery is out ahead.

TOP HOSTED/CLOUD-BASED SERVICES INVESTMENTS ON AVERAGE

PERCENTAGE OF HOSTED/CLOUD-BASED BUDGET

What factors does Pete keep top of mind when researching services?

Support is #1 followed by value, reliability and features/functionality.PURCHASE STRETCH #3

Email hosting Web hosting Online backup/recovery Productivity solutions Application hosting Industry-specific applications

18%16%

19%16% 14%

21%

13% 14%12%

9% 10%8% 7% 8%

5% 6% 6%4%

TOTAL NA EMEA

NEW VS. RECURRING HOSTED/CLOUD-BASED

SERVICES IN 2015 / PERCENTAGE OF TOTAL RESPONDENTS

NEW VS. RECURRING HOSTED/CLOUD-BASED SERVICES IN 2015

PERCENTAGE OF NORTH AMERICA RESPONDENTS

Online backup/recovery

Productivity solutions (file sharing, online collaboration, productivity suites)

Infrastructure (IaaS, cloud computing, storage)

Email hosting

Sales support (CRM)

Application hosting

10%

10%

7%

11%

9%

9%42%

46%

58%

37%

63%

55%

35%

35%

23%

48%

20%

28%

14%

10%

8%

8%

7%

7%

RECURRING NOT APPLICABLE DON’T KNOWNEW

Online backup/recovery

Productivity solutions (file sharing, online collaboration, productivity suites)

Email hosting

Infrastructure (IaaS, cloud computing, storage)

Sales support (CRM)

Application hosting

10%

8%

10%

6%

7%

9%40%

44%

34%

58%

61%

55%

37%

39%

52%

26%

25%

30%

14%

10%

8%

6%

6%

5%

RECURRING NOT APPLICABLE DON’T KNOWNEW

13

MANAGED SERVICES Managed Service investments will also

see their share of budget dollars in 2015.

Of the 10% average managed services

budget allocated, the top three areas

sprinting to the front are IT services/

service providers (19%), consulting

(16%), and connectivity/bandwidth (16%).

Managed Service investments will see their share of budget dollars in 2015.

TOP MANAGED SERVICES INVESTMENTS ON AVERAGE

PERCENTAGE OF MANAGED SERVICES BUDGET

NEW VS. RECURRING HOSTED/CLOUD-BASED SERVICES IN 2015

PERCENTAGE OF EMEA RESPONDENTS

NEW VS. RECURRING HOSTED/CLOUD-BASED SERVICES IN 2015

PERCENTAGE OF NORTH AMERICA RESPONDENTS

Infrastructure (IaaS, cloud computing, storage)

Online backup/recovery

Application hosting

Productivity solutions (file sharing, online collaboration, productivity suites)

Sales support (CRM)

Email hosting

13%

13%

11%

10%

10%

10%

20%

33%

23%

29%

13%

43%

54%

43%

56%

50%

66%

39% 8%

11%

11%

10%

11%

13%

RECURRING NOT APPLICABLE DON’T KNOWNEW

IT services(service providers)

Consulting Connectivity/bandwidth

Hosting Storage/backup/archiving Email/collaboration Cellular

19% 19% 20%16% 17%

13%16% 16% 15% 14%

11%

17%

10% 10% 10% 9% 10%7% 5% 5% 5%

TOTAL NA EMEA

14

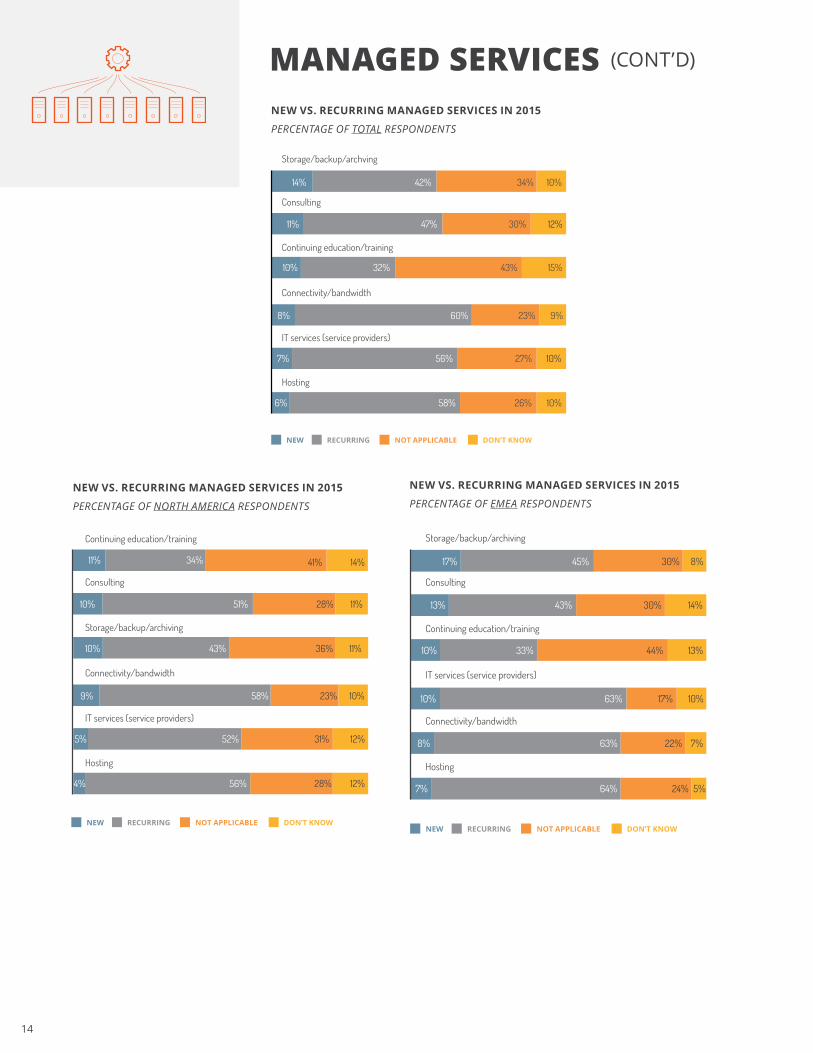

MANAGED SERVICES (CONT’D) NEW VS. RECURRING MANAGED SERVICES IN 2015

PERCENTAGE OF TOTAL RESPONDENTS

NEW VS. RECURRING MANAGED SERVICES IN 2015

PERCENTAGE OF NORTH AMERICA RESPONDENTS

NEW VS. RECURRING MANAGED SERVICES IN 2015

PERCENTAGE OF EMEA RESPONDENTS

0 20 40 60 80 100

Storage/backup/archving

Consulting

Continuing education/training

Connectivity/bandwidth

IT services (service providers)

Hosting

10%34%42%

12%30%47%

15%

11%

14%

43%32%10%

8% 60% 23% 9%

7% 56% 27% 10%

6% 58% 26% 10%

RECURRING NOT APPLICABLE DON’T KNOWNEW

Continuing education/training

Consulting

Storage/backup/archiving

Connectivity/bandwidth

IT services (service providers)

Hosting

14%

11%

11%

23%

36%

31% 12%

10%

28% 12%

58%

52%

56%

43%

51% 28%

34% 41%11%

10%

10%

9%

5%

4%

RECURRING NOT APPLICABLE DON’T KNOWNEW

17%

13%

10%

10%

8%

7%

45%

43%

33%

63%

63%

64%

30%

30%

44%

17%

22%

24% 5%

7%

10%

13%

14%

8%

Storage/backup/archiving

Consulting

Continuing education/training

IT services (service providers)

Connectivity/bandwidth

Hosting

RECURRING NOT APPLICABLE DON’T KNOWNEW

15

02CHAPTER

17

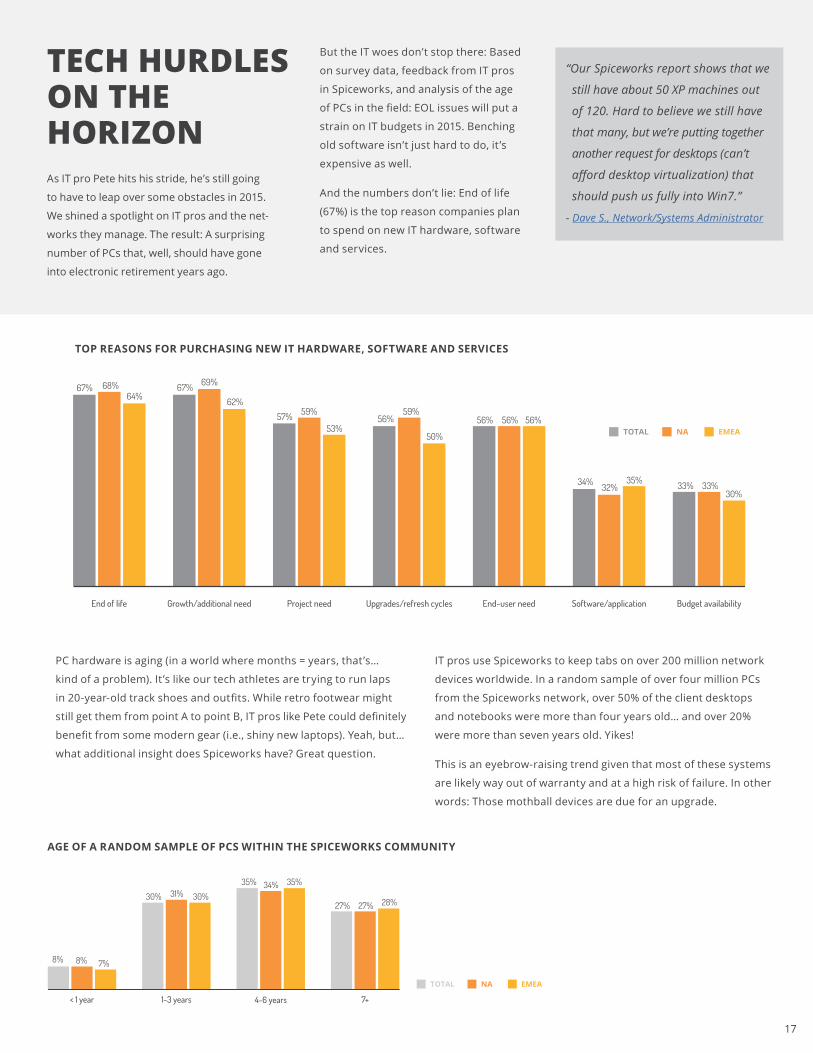

TECH HURDLES ON THE HORIZON As IT pro Pete hits his stride, he’s still going

to have to leap over some obstacles in 2015.

We shined a spotlight on IT pros and the net-

works they manage. The result: A surprising

number of PCs that, well, should have gone

into electronic retirement years ago.

But the IT woes don’t stop there: Based

on survey data, feedback from IT pros

in Spiceworks, and analysis of the age

of PCs in the field: EOL issues will put a

strain on IT budgets in 2015. Benching

old software isn’t just hard to do, it ’s

expensive as well.

And the numbers don’t lie: End of life

(67%) is the top reason companies plan

to spend on new IT hardware, software

and services.

“Our Spiceworks report shows that we

still have about 50 XP machines out

of 120. Hard to believe we still have

that many, but we’re putting together

another request for desktops (can’t

afford desktop virtualization) that

should push us fully into Win7.”

- Dave S., Network/Systems Administrator

PC hardware is aging (in a world where months = years, that’s…

kind of a problem). It ’s like our tech athletes are trying to run laps

in 20-year-old track shoes and outfits. While retro footwear might

still get them from point A to point B, IT pros like Pete could definitely

benefit from some modern gear (i.e., shiny new laptops). Yeah, but…

what additional insight does Spiceworks have? Great question.

IT pros use Spiceworks to keep tabs on over 200 million network

devices worldwide. In a random sample of over four million PCs

from the Spiceworks network, over 50% of the client desktops

and notebooks were more than four years old… and over 20%

were more than seven years old. Yikes!

This is an eyebrow-raising trend given that most of these systems

are likely way out of warranty and at a high risk of failure. In other

words: Those mothball devices are due for an upgrade.

TOP REASONS FOR PURCHASING NEW IT HARDWARE, SOFTWARE AND SERVICES

AGE OF A RANDOM SAMPLE OF PCS WITHIN THE SPICEWORKS COMMUNITY

67%

TOTAL NA EMEA

End of life Growth/additional need Project need Upgrades/refresh cycles End-user need Software/application Budget availability

68%64%

67% 69%

62%

57% 59%

53%56%

59%

50%

56% 56% 56%

34% 32%35% 33% 33%

30%

TOTAL NA EMEA

< 1 year 1-3 years 4-6 years 7+

8% 8% 7%

30% 31% 30%

35% 34% 35%

27% 27% 28%

18

Server software is also getting a little… geriatric. More than

a third of survey respondents indicated they’d need to move

off of Windows Server 2003 next year. Analysis of aggregated

Spiceworks network data confirmed this trend. In fact, 65%

of companies sampled in NA & EMEA within the Spiceworks

network had at least one installation of Windows Server 2003.

As a result, many companies will be racing to migrate off of

WS2003 in advance of Microsoft’s end of life for the OS on

July 14, 2015. After that, IT teams will be living dangerously

and on their own in the event of an OS injury… with no new

patches in sight.

IMPACT OF WINDOWS SERVER 2003 END OF LIFE

OF RESPONDENTS WITH WINDOWS SERVER 2003

“Hardware: I’ve been scrooging all year long so that I can replace some of my aging servers at the end of the year

when I still have money left in the budget. Software: We’re actually in good shape for this. I’m replacing the last

three XP machines this week. Everything else is Win7 / Win8. Of course, Win2003 is still heavy in my environment,

but I’ve still got a little time.” - David R., IT Director

CONCLUSIONIn short, Pete’s got some budget barriers to navigate around in 2015. And that’s where you, coach marketer, can help guide

him (and your campaigns) to victory…

TOTAL NA EMEA

We will need to upgrade software

We will need to buy new servers

We will need to purchase new

software

We will spend on service to assist with Windows Server

2003 migration

We will spend to host workloads formerly

running on Windows 2003 in the Cloud

25% 23%

29%

17% 18% 16% 14% 14%17%

8%7%7%3% 2% 4%

19

20

03CHAPTER

HOW TO BECOME A MARKETING CHAMP Uh-oh. We can already see the worry lines

creeping across your brow as you watch

buyers plod around the track. But before

you break down in a fit of “holy-cow-what-

now” despair (happens to the best of us),

we’ve got some good news: There are real,

concrete measures you can take to transform

2015 from the Year of the Anxious Athlete to

the Year of the Successful Superstar.

“ As you’re hitting your stride and heading to the finish line to meet your market-

ing goals in 2015, demand more of yourself. Demand more of your marketing.

Why? Because IT buyers do.”

- Jon Pafk, Senior Marketing Communications Manager

Armed with the insights from this report, you (Coach/Tech Marketer) might want to focus

your game plan on the following tactics. After all, Pete needs some guidance and a little

extra help in this less than ideal economic climate. Winning new business won’t be easy,

but it’s certainly possible to hit campaign goals… despite IT pro woes:

Virtualization Vendors:

Hone in on the cost-saving message

of replacing old WS2003 servers with

newer OSes running on VMs.

Hardware Vendors:

Focus on refresh promotions and

warranty renewals.

Backup/Recovery Vendors:

Provide “peace of mind” for aging

PCs with backup/recovery solutions.

All Tech Vendors:

Define your vertical social network

strategy to engage customers across

all touch points of the lifecycle.

1

2

3

Consider this quick cheat sheet a fast track to continued business success. IT pro purchases

will endure the marathon (and your campaigns can guide them to the finish line).

4

Check out The Spicy Marketer, our new marketing blog, for marketing tips, up-to-date news, and a ton of tech marketing mojo.

BONUS BOOST

21

22

04CHAPTER

23

CLOSING CEREMONIES The 2015 IT Budget Games are under way: IT

pros will need to adjust their tech buying hab-

its due to budget constraints that will cramp

their purchase pace. With aging hardware

and software and Windows Server 2003 EOL,

you’ll need to meet your buyers halfway by

adjusting your campaign messaging.

In short, there will be no shortage of

hurdles for IT pros and marketers alike

in 2015. But there’s also going to be tons

of opportunity to hit campaign goals (a little

course correction now will help

you go the distance).

With the right amount of prep, endurance

and focus, Olympic Gold is within your reach.

And the best part: IT buyers will thank you...

in the long run.

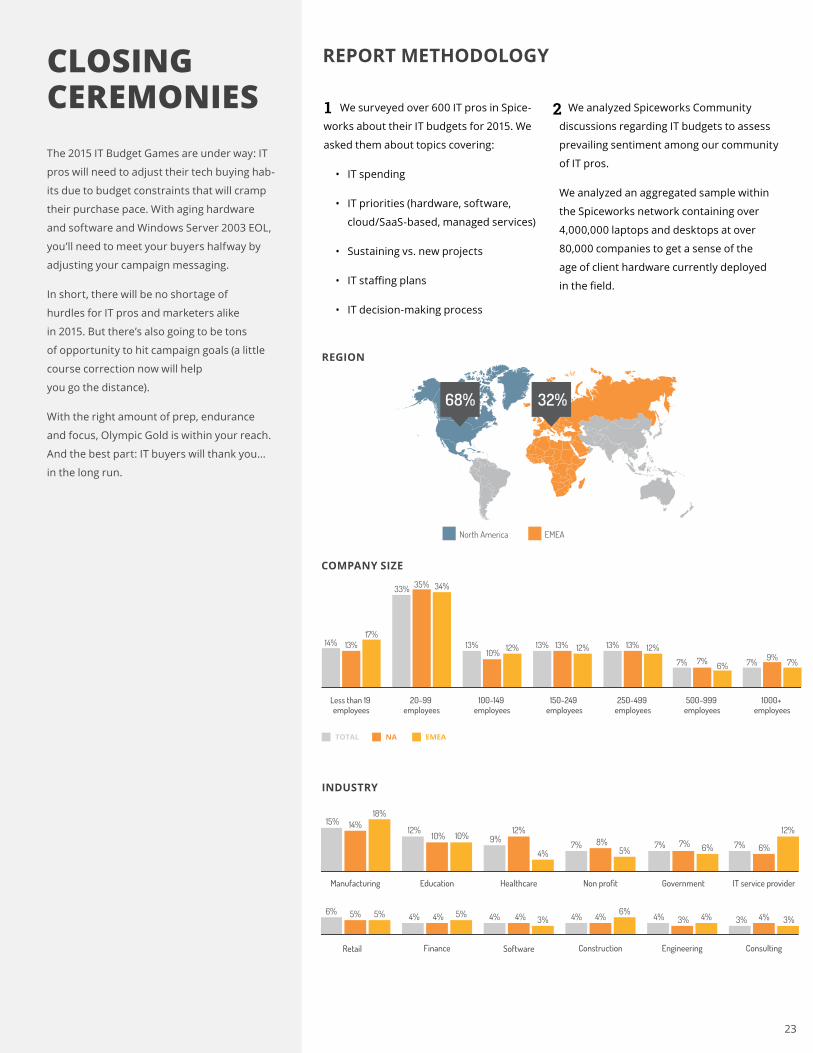

REPORT METHODOLOGY

We surveyed over 600 IT pros in Spice-

works about their IT budgets for 2015. We

asked them about topics covering:

• IT spending

• IT priorities (hardware, software,

cloud/SaaS-based, managed services)

• Sustaining vs. new projects

• IT staffing plans

• IT decision-making process

We analyzed Spiceworks Community

discussions regarding IT budgets to assess

prevailing sentiment among our community

of IT pros.

We analyzed an aggregated sample within

the Spiceworks network containing over

4,000,000 laptops and desktops at over

80,000 companies to get a sense of the

age of client hardware currently deployed

in the field.

1 2

INDUSTRY

COMPANY SIZE

REGION

68% 32%

North America EMEA

Manufacturing Education Healthcare Non profit Government IT service provider

Retail Finance Software Construction Engineering Consulting

TOTAL NA EMEA

15% 14%18%

6% 5% 5%

12%

4% 4% 5%

10% 10%

4% 4% 3% 4% 4%6%

4%3%4% 3% 4% 3%

12%

6%7%6%7%7%5%

8%7%4%

12%9%

TOTAL NA EMEA

Less than 19 employees

20-99 employees

100-149 employees

150-249 employees

250-499 employees

500-999 employees

1000+ employees

14% 13%17%

33% 35% 34%

13%10% 12% 13% 13% 12% 13% 13% 12%

7% 7% 6% 7% 9% 7%

24

25

Spiceworks photo credits:

Jon Pafk, Senior Marketing Communications Manager (as the IT Team “Coach”)

Peter Tsai, IT Content Marketing Manager (as the “Pete, IT Manager”)

Drew Sollberger, Manager of Demand Generation (as himself)

Emily Perdue, Email Marketing Coordinator (as a “Sales Manager”)

Tracy Peto, Custom Research Specialist (as a “Sales Manager”)

Jennifer Faulk, PR & Social Media Specialist (as a “Marketing Manager”)

Design:

Kevan Lin, Graphic Designer (Interative design, photography and art direction)

Clarice Bajkowski, Graphic Designer (Photography art direction, print design)

Marivi Delgado, Junior Graphic Designer (Photography)

The contents in this report are a result of primary research performed by Spiceworks. Unless otherwise noted, the entire contents distributed as part of this report are copyrighted by Spiceworks. As such any information made available by any means in this report may not be copied, reproduced, duplicated, published, displayed, transmitted, distributed, given, sold, traded, resold, marketed, offered for sale, modified to create derivative works or otherwise exploited for valuable consideration without prior written consent by Spiceworks. For more information visit www.spiceworks.com/voice-of-it/terms.

This report contains information of fact relating to parties other than Spiceworks. Although the information has been obtained from, and is based on sources that Spiceworks believes to be reliable, Spiceworks does not guarantee the accuracy, and any such information might be incomplete or condensed. Any estimates included in this report constitute Spiceworks’ judgment as of the date of compilation, and are subject to change without notice. This report is for information purposes only. All responsibility for any interpretations or actions based on the information or commentary contained within this report lie solely with the recipient. All rights reserved. 2014.

About Spiceworks Voice of IT®

The Spiceworks Voice of IT market insights program publishes statistics, trends and opinions collected from IT professionals worldwide. More than 620,000 IT professionals in over 100 countries have joined the program to share information and feedback on the technology issues important to them.

About Spiceworks

Spiceworks is the professional network 6 million IT professionals use to connect withone another and over 3,000 technology brands. The company simplifies how ITprofessionals discover, buy and manage more than $600 billion in technology productsand services each year. Headquartered in Austin, Texas, Spiceworks is backed byAdams Street Partners, Austin Ventures, Institutional Venture Partners (IVP), GoldmanSachs, Shasta Ventures and Tenaya Capital. For more information www.spiceworks.com

Follow Spiceworks on Twitter and connect with Spiceworks on Facebook.

Voice of IT ®

26

Where IT goes to work.