solar development in the philippines - the lantau grouplantaugroup.com/files/ppt_pgen16s_sf.pdf ·...

TRANSCRIPT

The Lantau Group

Solar Development in the Philippines22nd September

The Lantau Group

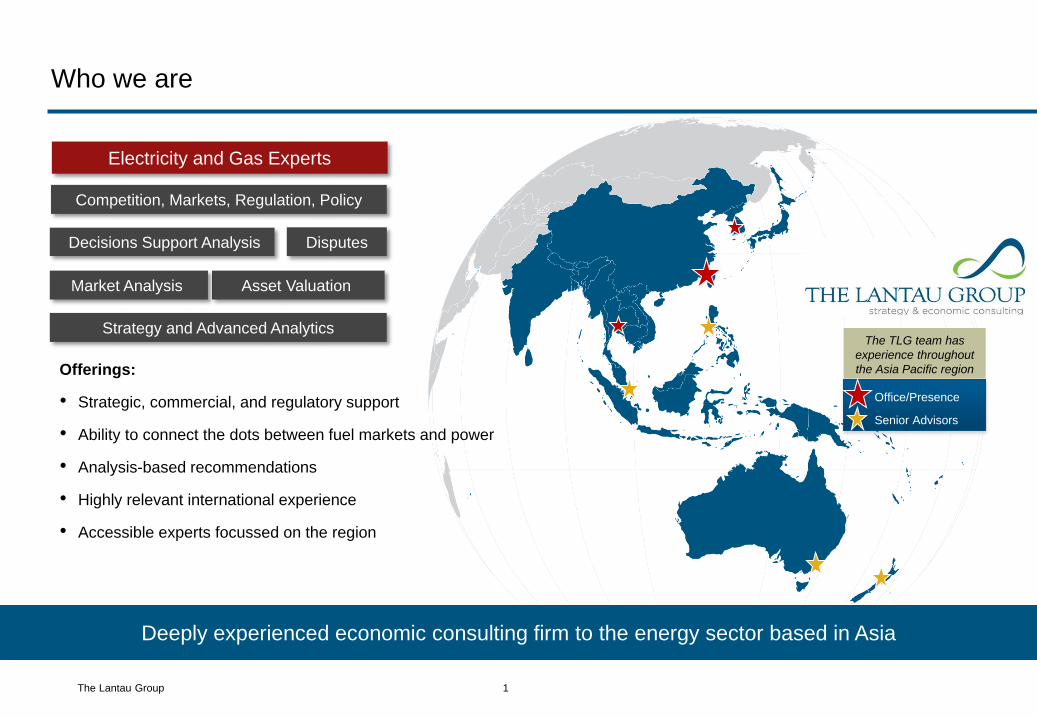

Deeply experienced economic consulting firm to the energy sector based in Asia

Who we are

Decisions Support Analysis

Asset Valuation

Strategy and Advanced Analytics

Competition, Markets, Regulation, Policy

Disputes

Market Analysis

Electricity and Gas Experts

The TLG team has

experience throughout

the Asia Pacific region

Office/Presence

Senior Advisors

Offerings:

• Strategic, commercial, and regulatory support

• Ability to connect the dots between fuel markets and power

• Analysis-based recommendations

• Highly relevant international experience

• Accessible experts focussed on the region

1

The Lantau Group

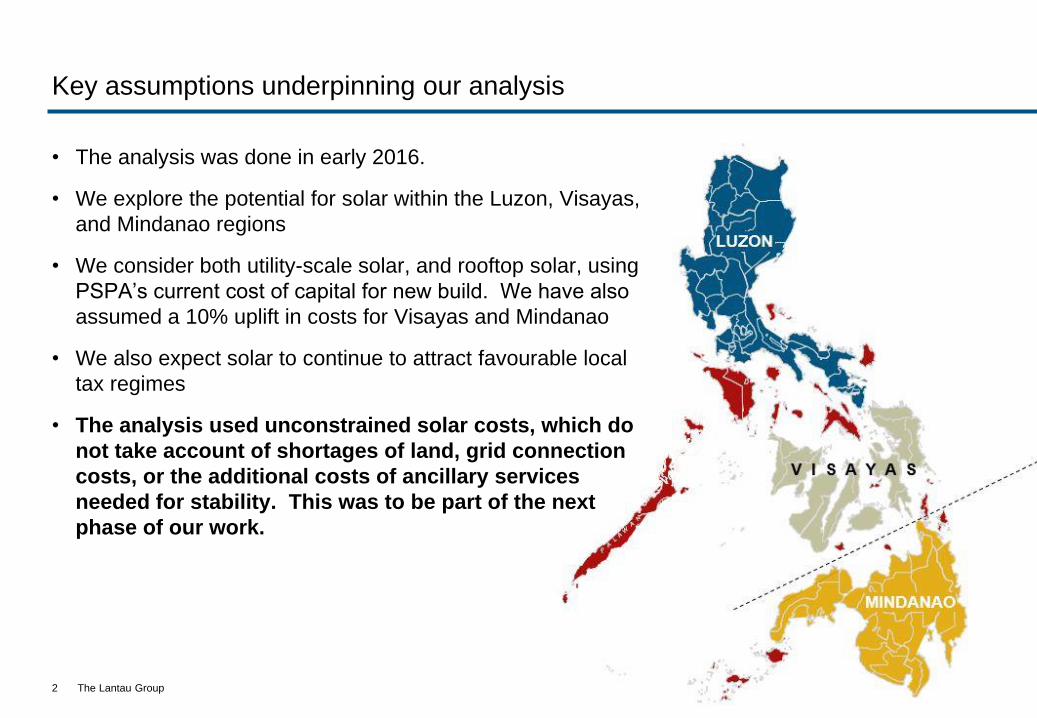

Key assumptions underpinning our analysis

• The analysis was done in early 2016.

• We explore the potential for solar within the Luzon, Visayas,

and Mindanao regions

• We consider both utility-scale solar, and rooftop solar, using

PSPA’s current cost of capital for new build. We have also

assumed a 10% uplift in costs for Visayas and Mindanao

• We also expect solar to continue to attract favourable local

tax regimes

• The analysis used unconstrained solar costs, which do

not take account of shortages of land, grid connection

costs, or the additional costs of ancillary services

needed for stability. This was to be part of the next

phase of our work.

2

The Lantau Group

0

1

2

3

4

5

6

7

8

9

10

20

30

40

50

60

70

80

90

100

Current outlook for fuel prices

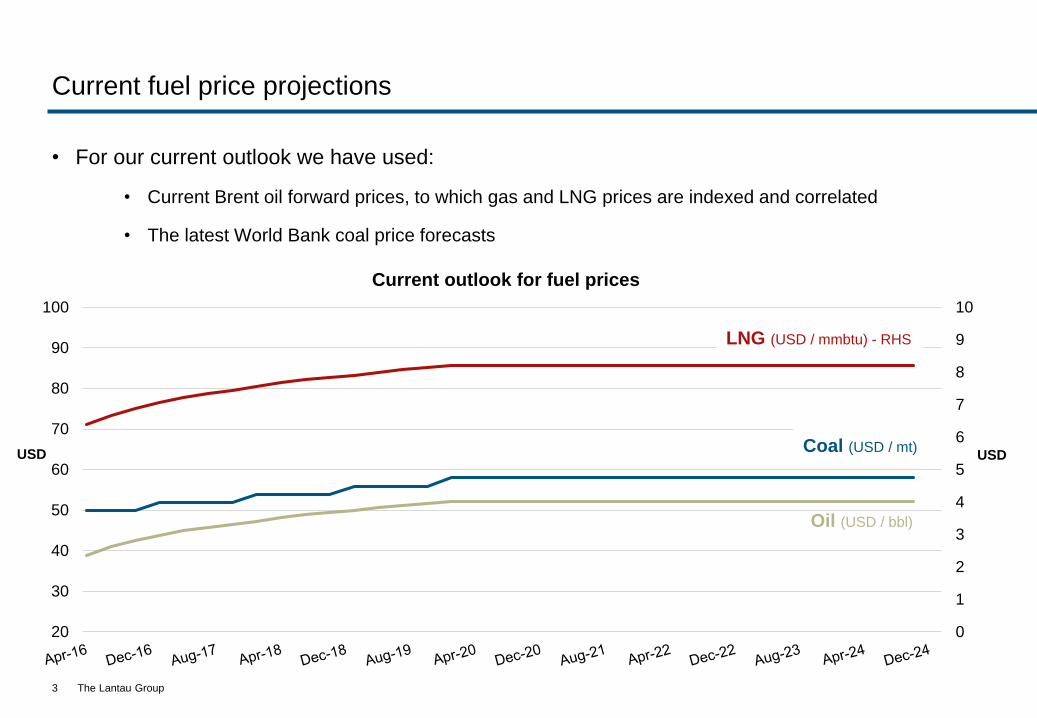

Current fuel price projections

• For our current outlook we have used:

• Current Brent oil forward prices, to which gas and LNG prices are indexed and correlated

• The latest World Bank coal price forecasts

3

USDUSD

LNG (USD / mmbtu) - RHS

Coal (USD / mt)

Oil (USD / bbl)

The Lantau Group

The demand outlook in the Philippines is supported by relatively robust

economic fundamentals with the potential for growth to accelerate

• Our assessment of macroeconomic growth and sectoral trends, alongside DOE projections,

paints a relatively strong picture for demand growth

4

Power demand in the Philippines remains relatively low compared to neighbouring nations, yet with

potential for demand growth to accelerate given the lower energy intensity per $ of GDP

(5) 0 5 10 15 20

Japan

New Zealand

Australia

Hong Kong

Singapore

Philippines

Thailand

Korea, Rep.

Myanmar

Malaysia

Indonesia

China

Vietnam

Percent

Electricity consumption annual growth

(1991-2013)

2011

1990

2005

1990

0

500

1,000

1,500

2,000

2,500

0 1 2 3 4 5 6 7

GDP per capita (2005 PPP US$)

PhilippinesIndonesiaThailandVietnamMalaysia

kWh consumption per capitaTotal consumption per capita vs. GDP per capita (1980-2013)

The Lantau Group

Our independent analysis is underpinned by sophisticated modelling of the

Philippine market, through which we are able to explore different scenarios

• QUAFU is an integrated generation dispatch modelling tool that incorporates state-of-the-art

optimisation theory grounded in proven techniques

5

The Lantau Group

Agenda

Introduction to The Lantau Group

Scope of work

• Key assumptions

• Fuel prices and demand outlook

• Analytical approach

Current projections

• Luzon

• Visayas

• Mindanao

The impact of decreasing capital costs

Fuel price scenarios and sensitivity analysis

Re-profiling solar new build and fuel cost savings

Impact on solar when assuming 30 percent gas generation

Summary and questions

6

The Lantau Group

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

0

250

500

750

1,000

1,250

1,500

1,750 PHP / MWh

Cap

acit

y a

dd

itio

ns (

MW

)

Committed Biofuel

Committed Coal

Committed Natural Gas

Committed Solar

Generic Coal

Generic Natural Gas

Generic Solar

Time-weighted Price(Luzon)

With capital costs for solar remaining at today’s levels the new build outlook for

Luzon is dominated by coal and solar

• In Luzon, an excess of committed generation coming online between 2016-2020 (largely coal and gas) suppresses

WESM prices through to around 2022

• We hit a turning point in 2023 following the expiry of ToP gas contracts from Malampaya, which sees existing

CCGT plant price off more expensive gas ( LNG) and operate more in a mid-merit / peaking role.

• The resultant increase in prices then begins to incentivise new build, in particular for coal and solar

7

Projected average price

Expiry of Malampaya gas ToP contracts: thereafter gas

generation drops from 20 TWh to around 11 TWh per year

Projected average price

(Luzon)

The Lantau Group

However the fundamental outlook in Visayas is markedly different

• In Visayas, the amount of new solar capacity that could enter the market economically is naturally much lower,

with around 400 MW projected between 2016 – 2017

• The longer-term outlook for new build (across all fuels) is suppressed by strong capacity margins of between

0.9 GW and 1.5 GW above peak demand through to 2025

8

0

500

1,000

1,500

2,000

2,500

3,000

0

100

200

300

400

500

600

700

800

PHP / MWh

Cap

acit

y a

dd

itio

ns (

MW

)

Committed Coal

Committed Natural Gas

Committed Solar

Generic Coal

Generic Natural Gas

Generic Solar

Time-weighted Price(Visayas)

Projected

average price

Committed coal and solar coming

online equates to 80% of Visayas’

peak demand in 2016-2018

Projected average price

(Visayas)

The Lantau Group

With a similar picture in Mindanao

• Similar to Visayas, prices in Mindanao are not supportive of any new build in the short to

medium-term

9

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

0

100

200

300

400

500

600

700

800

900

1,000

1,100

PHP / MWh

Cap

acit

y ad

dit

ion

s (M

W)

Committed Coal

Committed Hydro

Generic Coal

Generic Oil

Generic Solar

Time-weighted Price(Mindanao)

Committed coal coming online

equates to 80% of Mindanao’s

peak demand in 2016-2017

Projected

average price

Projected average price

(Mindanao)

The Lantau Group

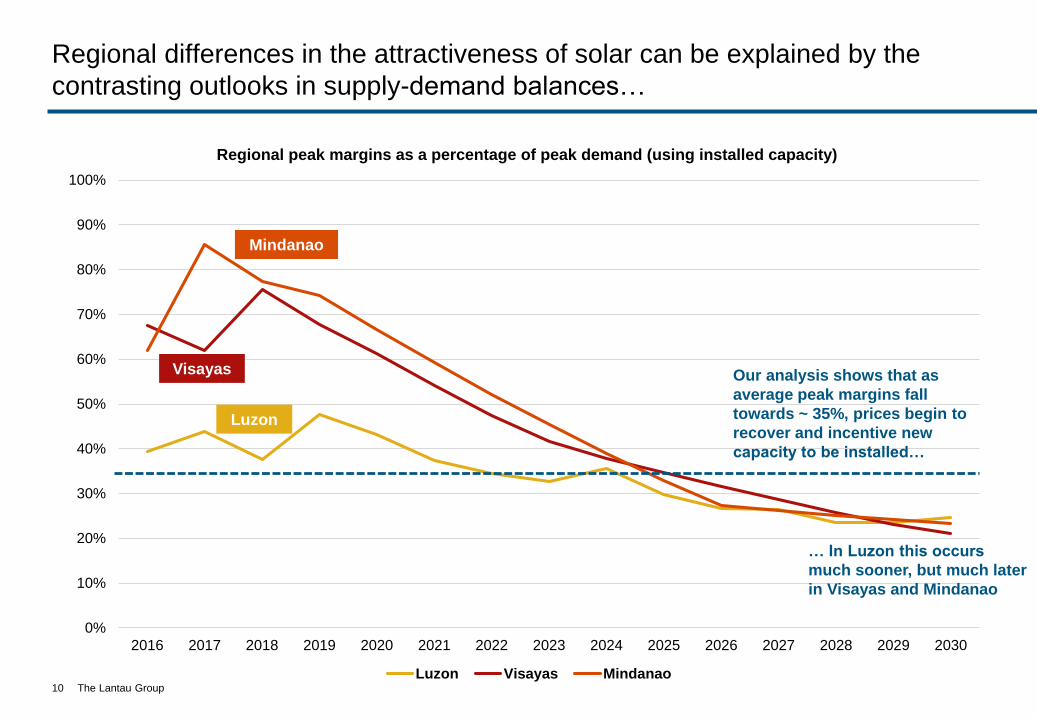

Regional differences in the attractiveness of solar can be explained by the

contrasting outlooks in supply-demand balances…

10

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Regional peak margins as a percentage of peak demand (using installed capacity)

Luzon Visayas Mindanao

Luzon

Visayas

Mindanao

Our analysis shows that as

average peak margins fall

towards ~ 35%, prices begin to

recover and incentive new

capacity to be installed…

… In Luzon this occurs

much sooner, but much later

in Visayas and Mindanao

The Lantau Group

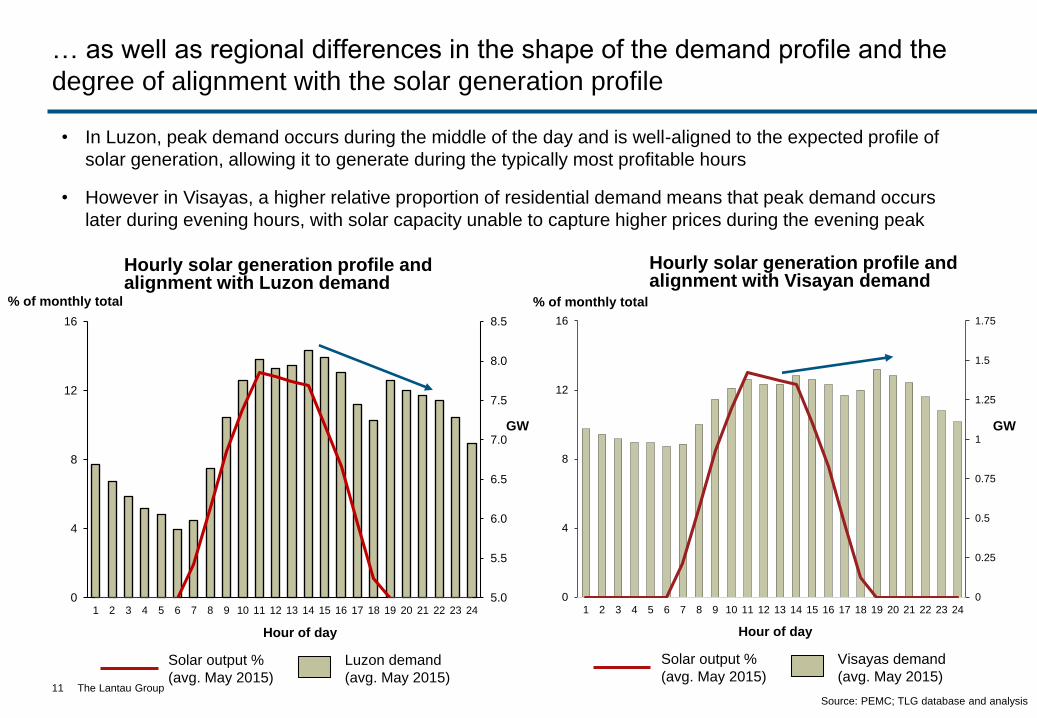

… as well as regional differences in the shape of the demand profile and the

degree of alignment with the solar generation profile

11

GW

Source: PEMC; TLG database and analysis

Solar output %

(avg. May 2015)

Luzon demand

(avg. May 2015)

% of monthly total

Hour of day

Hourly solar generation profile and alignment with Luzon demand

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

0

4

8

12

16

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

• In Luzon, peak demand occurs during the middle of the day and is well-aligned to the expected profile of

solar generation, allowing it to generate during the typically most profitable hours

• However in Visayas, a higher relative proportion of residential demand means that peak demand occurs

later during evening hours, with solar capacity unable to capture higher prices during the evening peak

GW

Hourly solar generation profile and alignment with Visayan demand

0

0.25

0.5

0.75

1

1.25

1.5

1.75

0

4

8

12

16

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

% of monthly total

Solar output %

(avg. May 2015)

Visayas demand

(avg. May 2015)

Hour of day

The Lantau Group

Agenda

Introduction to The Lantau Group

Scope of work

• Key assumptions

• Fuel prices and demand outlook

• Analytical approach

Current projections

• Luzon

• Visayas

• Mindanao

The impact of decreasing capital costs

Fuel price scenarios and sensitivity analysis

Re-profiling solar new build and fuel cost savings

Impact on solar when assuming 30 percent gas generation

Summary and questions

12

The Lantau Group

In reality the cost of new solar is highly likely to continue to fall

• Solar costs have been on a clear downward trajectory for the last 8 – 10 years, and are expected

to continue to fall, albeit at a more gradual rate

• We have prudently assumed costs fall by 1.5% pa. until 2025, and 0.75% pa. thereafter

• Solar costs fall 1.5% pa. until

• By 2030

13

2016 2020 2025 2030

2016 current costs (PSPA)US $2,290 / kW (rooftop)

US $1,400 / KW (utility-scale)

2030 projected costsUS $1,925 / kW (rooftop)

US $1,177 / KW (utility-scale)

The Lantau Group

… In turn attracting significant amounts of new build solar, albeit largely in Luzon

• A gradual decline in the cost of utility-scale solar (to $1,177 per kW by 2030) attracts an additional

7.4 GW solar build in Luzon

14

-500

0

500

1000

1500

2000

2500

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Difference in solar build between fixed and decreasing cost of capital

Luzon Visayas Mindanao

Capacity

(MW)

The Lantau Group

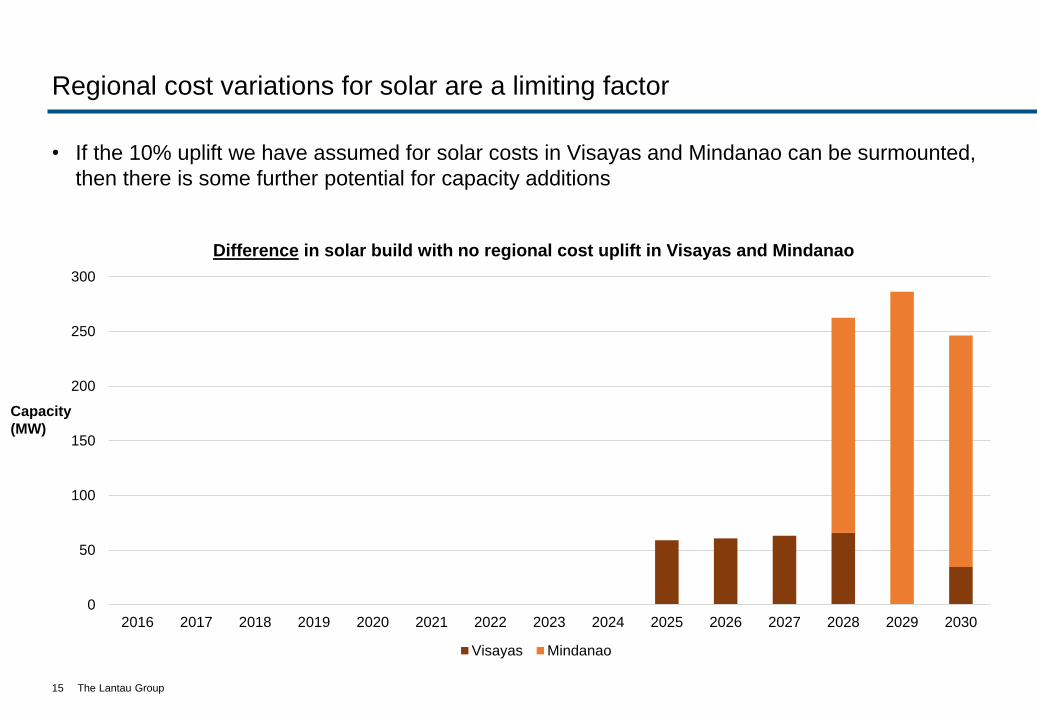

Regional cost variations for solar are a limiting factor

• If the 10% uplift we have assumed for solar costs in Visayas and Mindanao can be surmounted,

then there is some further potential for capacity additions

15

0

50

100

150

200

250

300

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Difference in solar build with no regional cost uplift in Visayas and Mindanao

Visayas Mindanao

Capacity

(MW)

The Lantau Group

Understanding the sensitivity of solar build to future fuel price dynamics is key

• We modelled a set of fuel price scenarios based around different oil price projections to 2020

16

‘Flat-Lining’ – based on current prices remaining static

‘High Fuel 2’ – based on a rise in oil prices to $85

‘High Fuel 1’ – based on a rise in oil prices to $70

‘Current Outlook’ – based on current and implied price forecasts

‘Low Fuel’ – based on a fall in oil prices to $20 by 2020

‘High Fuel 3’ – based on a rise in oil prices to $100

0

10

20

30

40

50

60

70

80

90

100

Fuel price scenarios used in this analysis

Brent

crude

(US / bbl)

The prices above are nominal and

adjusted to real terms in our modelling

The Lantau Group

In Luzon, utility-scale solar is well placed to capitalise on increasing fuel

prices, whilst also showing a high level of resilience to falling oil prices

17

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Cumulative solar build in Luzon (from 2016)

High Fuel 3 High Fuel 2 High Fuel 1 Current Outlook Flat-Lining Low Fuel

Cumulative

capacity

build (MW)

+ 4 GW

capacity

When oil prices fall below $28 we

start to see a pronounced

decrease in solar, as it becomes

displaced by new CCGT gas plant

and an increase in generation at

existing gas plant

In the most bullish scenario, solar

displaces around 16 TWh of gas

generation between 2020-2025,

rising to 40 TWh between 2026-2030

Current outlook

The Lantau Group

Rising fuel prices significantly benefit solar build, which sees a significant

increase in generation almost entirely at the expense of existing gas-fired plant

18

-10

-8

-6

-4

-2

0

2

4

6

8

10

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Change in generation mix (TWh) in Luzon between ‘Current Outlook’ and ‘High Fuel 3’ scenario

Natural Gas Coal Solar

TWh

generation

• Again, the expiry of ToP contracts from Malampaya marks a clear turning point, and thereafter

gas plant shifts further up the merit order curve

The Lantau Group

-

100

200

300

400

500

600

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Cumulative solar build in Visayas (from 2016)

High Fuel 3 High Fuel 2 High Fuel 1 Current Outlook Flat-Lining Low Fuel

In Visayas, a bearish supply-demand outlook persists with only small increases

19

Cumulative

MW

+ 150

MW

The Lantau Group

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Cumulative solar build in Mindanao (from 2016)

High Fuel 3 High Fuel 2 High Fuel 1 Current Outlook Flat-Lining Low Fuel

Whilst in Mindanao, solar is sensitive to rising fuel prices over the longer term

20

Cumulative

MW

+ 1.6

GW

• From 2024 rising fuel prices begin to support the economic build of solar, displacing what would

otherwise be new oil-fired plant additions

The Lantau Group

A recovery in the energy complex over the medium-term would provide a

unique window for Philippine industry to capitalise on the present situation

• History has shown oil prices tend to follow strong cyclical patterns, and we appear to have seen

a recent bottoming-out of oil prices

• In each of our scenarios where we forecast a rise in oil prices, the new build of solar becomes

increasingly attractive as thermal generation spreads are squeezed and new build is deterred

21

0

2

4

6

8

10

12

14

16

18

20

US

D/G

J,

20

14 r

eal te

rms

Note: Crude price 1970-1979 Saudi Arabian Light, 1979-present Brent

Source: TLG analysis

Oil price

When comparing the current

outlook for fuel prices with the

most bullish scenario, we see

an additional 5.8 GW of new

solar across Luzon, Visayas

and Mindanao by 2030

(assuming decreasing solar

costs)

The Lantau Group

Whilst staying ahead of the investment cycle of conventional generation is critical

• When oil prices are juxtaposed with fuel spreads, clear ‘windows’ exist for conventional new

build projects to be developed and come online

• Thus it is vital for solar new build to get ahead of the next window, displacing the next wave of

conventional new build that would ultimately subdue future power prices

22

Note: Crude price 1970-1979 Saudi Arabian Light, 1979-present Brent; Coal price Newcastle

Source: World Bank; TLG analysis

Coal price

Oil price

0

2

4

6

8

10

12

14

16

18

20

‘Coal window’ ‘Coal window’

US

D/G

J,

20

14 r

eal te

rm

‘Gas window’ ‘Gas window?’

Will gas or

solar win

the coming

round?

The Lantau Group

• In practice it may be unrealistic or impractical for industry to install the significant amounts of

new solar capacity within such a narrow timeframe

There may be opportunities to accelerate the addition of capacity, thereby

allowing the industry to scale and avoid future supply bottlenecks

23

Smoothing of solar capacity additions in Luzon, assuming a ‘High Fuel 3’ scenario and decreasing solar costs)

2024-2025 new build

capped at 2 GW, with

excess built early

Projected

average price

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

PHP / MWh

MW

Generic Coal

Committed Natural Gas

Committed Biofuel

Committed Coal

Generic Solar

Committed Solar

Load-weighted Price (Luzon)

Price (without early build)

The Lantau Group

• When taking into account the amount of conventional, fossil fuel generation that is displaced by

bringing forward solar new build, fuel cost savings amount to around 5%

Additionally, accelerating the new build of solar achieves wider benefits by

reducing fuel costs and ultimately the burden on consumers

24

Projected fuel

cost savings

US

D $

m (

2014 r

ea

l te

rms)

-

1,000

2,000

3,000

4,000

5,000

6,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Projected fuel costs

'High Fuel 3' scenario 'High Fuel 3' scenario with early build of solar in Luzon

The Lantau Group

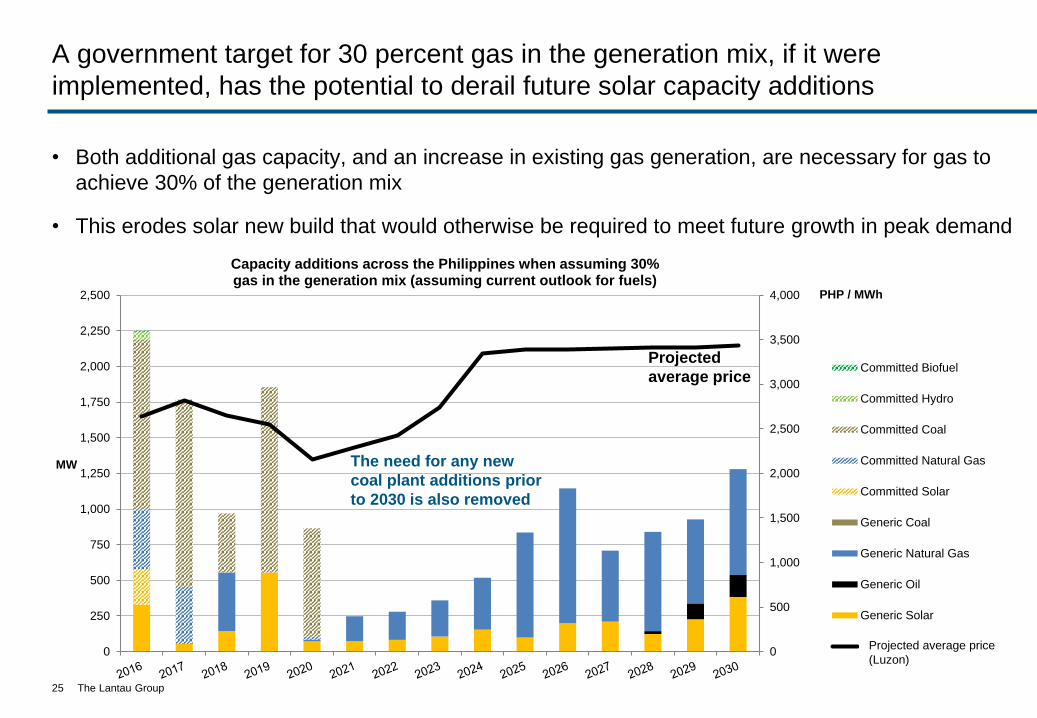

• Both additional gas capacity, and an increase in existing gas generation, are necessary for gas to

achieve 30% of the generation mix

• This erodes solar new build that would otherwise be required to meet future growth in peak demand

A government target for 30 percent gas in the generation mix, if it were

implemented, has the potential to derail future solar capacity additions

25

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500 PHP / MWh

MW

Capacity additions across the Philippines when assuming 30%gas in the generation mix (assuming current outlook for fuels)

Committed Biofuel

Committed Hydro

Committed Coal

Committed Natural Gas

Committed Solar

Generic Coal

Generic Natural Gas

Generic Oil

Generic Solar

Time-weighted Price (Luzon)Projected average price

(Luzon)

Projected

average price

The need for any new

coal plant additions prior

to 2030 is also removed

The Lantau Group

A government target for 30 percent gas in the generation mix, if it were

implemented, has the potential to derail future solar capacity additions

26

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

CumulativeMW

Cumulative new build of solar across the Philippines when comparing30% gas in the generation mix with our current outlook

Total solar build (No Min Gas) Total solar build (30% Min Gas Share)

- 7.5

GW

The Lantau Group27

Thank You.

We look forward to continue playing a key role in the

development of solar generation in the Philippines.

4602-4606 Tower 1, Metroplaza

223 Hing Fong Road

Kwai Fong, Hong Kong

Tel: +852 2521 5501

www.lantaugroup.com