lng infrastructure in philippines - the lantau group · the lantau group how does the changing fuel...

TRANSCRIPT

The Lantau Group

LNG Infrastructure in Philippines Sarah Fairhurst

The Lantau Group

What drives LNG Infrastructure?

• Economic Drivers

– The use of LNG is cheaper than some alternative fuel

• Environmental Drivers

– The use of LNG reduces emissions or other harmful outcomes

• Government Policy

– Government gives incentives or defines policy that makes LNG more attractive than other options

1

The Lantau Group

So what has changed on these in the past year?

• Economic Drivers

– Changes in the oil price are significant since the conference last year. Will this drive more LNG in

Philippines?

– Advancement of new gas-fired projects (San Gabriel phase 2 & Avion) and coal fired projects have

progressed

• Environmental Drivers

– Expansion of quotas for Renewable Energy

– No change in coal taxation; no overt moves to a “carbon tax”

• Government Policy

– No change

– Gas Master Plan, while completed, has not been published

2

The rest of the presentation will focus mainly on economic drivers

The Lantau Group

40

50

60

70

80

90

100

110

120

Da

ily B

ren

t p

ric

e, U

SD

/ba

rre

l

Jan '14 Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec '14 Jan '15 Feb

Asian LNG prices are linked to oil prices.

Brent has dropped by half from the high level in H1 2014

3 Source: ICE, Reuters, GS Global Investment Research and TLG analysis

ISIS attacked

Iraq

Price stabilized at

$100-110/barrel in

H1 2014 as Saudi

Arabia proactively

balanced the crude

market

Libya ports

re-opened

US air-

strike

on Iraq

started

1st sanction on

Russia

Saudi cut Oct

OSP priced

Saudi cut

Nov OSP

priced

Crude production in Iraq and Russia are not disrupted

while Libya supply returned despite of political turmoil

The Lantau Group

This is reflected in the spot price of LNG over the last 18 months

4

0

5

10

15

20

25

8/14/13 11/22/13 3/2/14 6/10/14 9/18/14 12/27/14 4/6/15

Daily JKM Spot Prices, $/MMBtu

Time period during which

modelling for Gas Master

Plan was carried out

The Lantau Group

But LNG is not the only fuel to have changed price. Coal prices have also

softened gradually since early 2011

5

0

20

40

60

80

100

120

140

160

180

09 08 07 06 05 04 03 02 01 16 15 14 13 12 11 2000 10

US$/MT or bbl

Source: World Bank; Macquarie

Oil (Brent)

Coal

(Newcastle)

Coal and oil monthly prices (2000-Feb 2015)

0

2

4

6

8

10

12

14

16

18

20

20

30

40

50

60

70

80

90

100

Australian Coal Prices ($/Tonne)

Asian Spot LNG prices ($/MMBtu)

Since the start of the Master Plan process

The Lantau Group

0

20

40

60

80

100

120

140

2000 2001 2003 2004 2006 2007 2009 2011 2012 2014 2015 2017 2019 2020

End 2009 future price

US$/barrel

Forward price in June 2014

End 2008 future prices

15th September 2014

Forward price on 20th Feb 2014

31th October 2014

In addition, we should not forget that the longer term has not changed as much

as the short term

• Forward price curves in recent years have been quite consistent

6

Brent forward curve

Source: ICE

Dated Brent

($/barrel)

2013 (historical) 109

2014 (historical) 99

2015 (forecast) 55

2016 (forecast) 65

2017 (forecast) 70

2018 (forecast) 75

2019 (forecast) 80

2020 (forecast) 80

The market thinks that oil (and thus LNG) prices will rise again in the medium

term

The Lantau Group

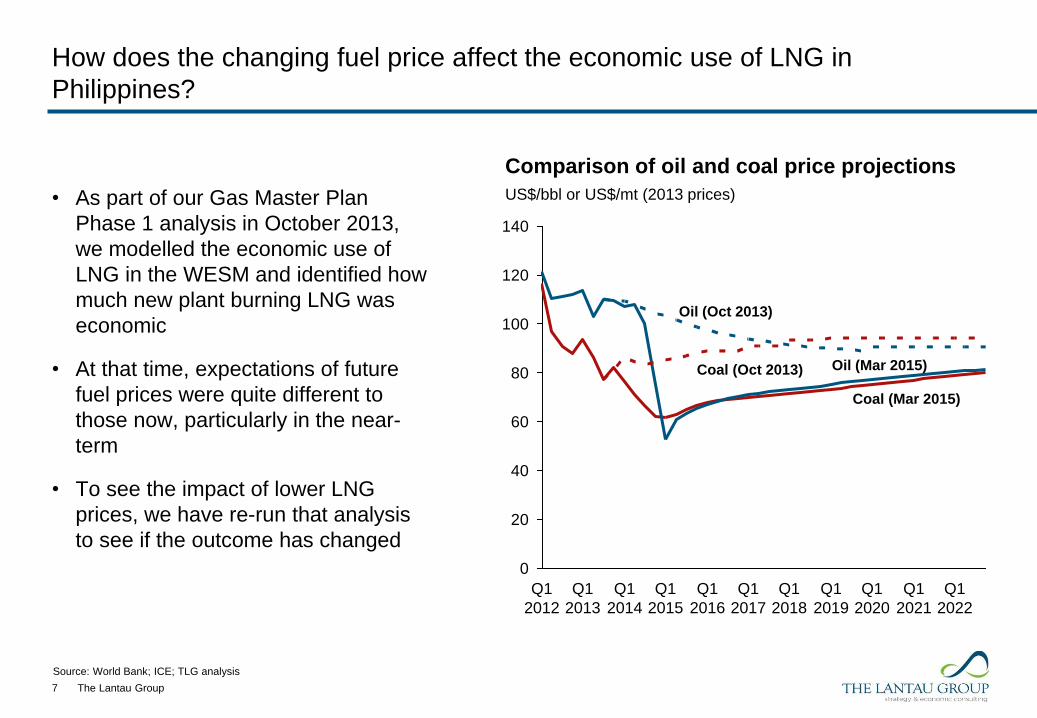

How does the changing fuel price affect the economic use of LNG in

Philippines?

• As part of our Gas Master Plan

Phase 1 analysis in October 2013,

we modelled the economic use of

LNG in the WESM and identified how

much new plant burning LNG was

economic

• At that time, expectations of future

fuel prices were quite different to

those now, particularly in the near-

term

• To see the impact of lower LNG

prices, we have re-run that analysis

to see if the outcome has changed

7

0

20

40

60

80

100

120

140

Q1

2014

Q1

2015

Q1

2013

Q1

2012

Q1

2016

Q1

2017

Q1

2018

Q1

2020

Q1

2021

Q1

2019

Q1

2022

US$/bbl or US$/mt (2013 prices)

Comparison of oil and coal price projections

Oil (Oct 2013)

Coal (Oct 2013) Oil (Mar 2015)

Coal (Mar 2015)

Source: World Bank; ICE; TLG analysis

The Lantau Group

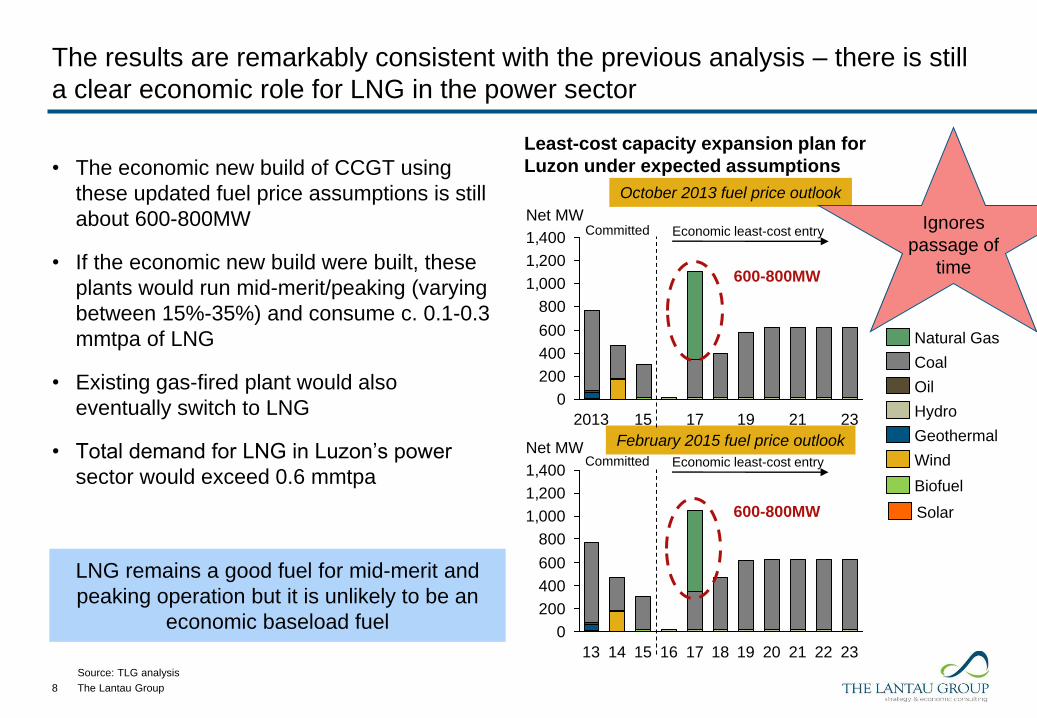

LNG remains a good fuel for mid-merit and

peaking operation but it is unlikely to be an

economic baseload fuel

• The economic new build of CCGT using

these updated fuel price assumptions is still

about 600-800MW

• If the economic new build were built, these

plants would run mid-merit/peaking (varying

between 15%-35%) and consume c. 0.1-0.3

mmtpa of LNG

• Existing gas-fired plant would also

eventually switch to LNG

• Total demand for LNG in Luzon’s power

sector would exceed 0.6 mmtpa

8

The results are remarkably consistent with the previous analysis – there is still

a clear economic role for LNG in the power sector

Least-cost capacity expansion plan for

Luzon under expected assumptions

0

200

400

600

800

1,000

1,200

1,400

23 21 18 20 22 14 16 19 17 15 13

Net MW

October 2013 fuel price outlook

February 2015 fuel price outlook

Natural Gas

Biofuel

Wind

Geothermal

Hydro

Oil

Coal

Solar 600-800MW

Economic least-cost entry Committed

0

200

400

600

800

1,000

1,200

1,400

19 17 15 2013 23 21

Net MW Economic least-cost entry Committed

600-800MW

Source: TLG analysis

Ignores

passage of

time

The Lantau Group

Taking into account the passage of time, other developments also affect the

need for more gas-fired capacity and ultimately more LNG demand

9

Least-cost capacity expansion plan for

Luzon under expected assumptions

0

200

400

600

800

1,000

1,200

1,400

19 17 15 2013 23 21

Net MW Economic least-cost entry Committed

0

200

400

600

800

1,000

1,200

1,400

15 14 13 23 22 21 20 19 18 17 16

Net MW

October 2013 outlook

Natural Gas

Biofuel

Wind

Geothermal

Hydro

Oil

Coal

Solar

• Option to use Malampaya gas supports more

gas-fired capacity

– As anticipated but not then certain, FirstGen’s San

Gabriel phase 2 and Avion have since achieved

financing and are under construction

– They plan to eventually use Malampaya gas and

ultimately LNG

– Changing the way Malampaya gas is used supports the

entry of more gas-fired capacity and ultimately more

LNG

• Additional renewable impacts on system

– Significantly more solar and wind capacity appears likely

in response to Government policies increasing total

available capacity

– More intermittent generation may require more flexible

plant in the system to respond to times when solar and

wind are unavailable

• Reduced incentives to build peaking capacity

– Lower offer price cap and new secondary price

cap decrease the incentives to build new gas-

fired capacity

600-800MW

Economic least-cost entry Committed

February 2015 outlook

400-600MW

Source: TLG analysis

500MW

The Lantau Group

Key factors that could affect economics of LNG remain uncertain

• Malampaya supplies after expiry of current GSPAs and SC38

– Quantities

– Pricing

– Degree of flexibility

• WESM offer price cap, secondary price cap and other market interventions

– Provide lower incentives for investors by seemingly reducing ability to make required returns on investment

– We are already seeing various potential investors pulling out of the market

• Regulatory framework for contracting with power offtakers

– ERC rules still under development

– Uncertainty over long-term direction of retail market (no gentailers?)

• Demand growth

– Economic expectations falling below Government targets?

10

The Lantau Group

The good news is that new LNG supplies should push down spot LNG prices in

Asia….

11

2015 2016

3.6 Mtpa PNG T1

3.6 Mtpa PNG T2

5 Mtpa Australia Gorgon T1

5 Mtpa Gorgon T2

5 Mtpa GorgonT3

4.25 Mtpa Australia (Curtis) T1

2017

4.25 Mtpa Curtis T2

7.8 Mtpa Australia Gladstone T1,2

2.1 Mtpa Indonesia Donggi-Senoro

4.5 Mtpa Australia APLNG T1

2014

= coal seam gas projects

9 Mtpa Sabine Pass LNG

train 1 and 2 from US

9 Mtpa Sabine Pass LNG train 3 and 4

The Lantau Group

…the bad news is that lower oil and LNG prices mean that some projects have

now been delayed or cancelled

For example:

• Petronas has delayed making a final investment decision on plans to export liquefied natural gas

from British Columbia

• BG Group said it was delaying a decision on the Louisiana LNG project

• Shell has cancelled plans for the Arrow LNG project in Queensland, Australia

• Woodside has delayed the investment decision on the Browse floating LNG project off Western

Australia. The Chevron-operated Gorgon project in Western Australia is also running late.

– Cost over runs are also plaguing Australian LNG projects, making new projects less certain

12

Most of these cite low LNG prices as the cause of the delay or cancellation

The Lantau Group

In summary, the message remains substantially the same as last year, despite

the large global changes in prices

• LNG is economic in the Philippines for mid-merit operation

• The volume of LNG required is modest

• There remain challenges in bringing LNG into the Philippines and incentivising the

market to build and burn the economic quantity of LNG

13

The Lantau Group

Thank You

Contact

Sarah Fairhurst [email protected]

By phone +852 2521 5501 (office)

By mail 4602-4606 Tower 1, Metroplaza

223 Hing Fong Road,

Kwai Fong, Hong Kong

Online www.lantaugroup.com

Rigour

Value

Insight

Energy Power Utilities

14

The Lantau Group

We cover the Asia Pacific region

15

End user price projections

Transmission development

Energy policy issues

Electricity and gas pricing to multiple industrial facilities

Generation opportunities (all fuel types)

Policy and regulatory developments

Retail contracting and power price

projections

Generation opportunity development

Capacity contracting

Energy price projections and impacts

Market design

Energy Market Review)

Power sector review

Gas pricing and demand

Electricity and gas pricing to multiple sites

Energy price projections

Tariff benchmarking

Natural gas entry opportunity

Energy price projections (electricity

and gas)

Regulatory developments

Tariff benchmarking and design