singapore - · pdf filesingapore regularly updates its legislation, judicial decisions and...

TRANSCRIPT

A Stone Forest CompanyPayrollServe ®

InternationalGlobally Connected

SINGAPORE

2014 EDITION

© Copyright 2014 Stone Forest Accountserve Pte Ltd 1

Overview ......................................................................................................................4

• Disclaimer ...........................................................................................................4

• Human Resource & Payroll Administration ................................................ 5

Payroll Processing Cycle ..........................................................................................8

• Step 1: Collecting Information ........................................................................ 9

• Step 2: Information Cut-off ...........................................................................10

• Step 3: Process Payroll .................................................................................... 11

• Steps 4 & 5: Generate Payroll Reports and Approval ............................. 13

• Step 6: Processing Salary Credit and Bank Processing .........................14

• Step 7: Month-end Reporting ........................................................................ 17

Employment Act .......................................................................................................20

• Contract of Service .........................................................................................21

• Salaries .............................................................................................................22

– Definition of Salary ................................................................................22

– Frequency of Salary Payment ..............................................................23

– Authorised Salary Deductions .............................................................23

– Maximum Amount of Deduction .........................................................24

– Deduction during Termination .............................................................24

– Monthly Variable Component (MVC) ..................................................25

• Wage Definition ...............................................................................................26

– Monthly Basic Rate of Pay ....................................................................26

– Monthly Gross Rate of Pay ................................................................... 27

– Incomplete Monthly Wages .................................................................. 27

COnTEnTS

The HR Practitioners’ Guide to Key Employment Legislation2

• Hours of Work ..................................................................................................29

– Contractual Hours of Work ...................................................................29

– Maximum Hours Allowed .....................................................................29

• Overtime ..........................................................................................................30

– Overtime Computation ........................................................................... 31

• Leave & Holidays.............................................................................................35

– Public Holidays ........................................................................................35

– Annual Leave ........................................................................................... 37

– Unpaid Leave .......................................................................................... 40

– Sick Leave ................................................................................................ 40

– Government-paid Leave Schemes ......................................................42

• Termination ......................................................................................................43

– Termination Process ..............................................................................43

– notice Period & Payments ....................................................................43

– Annual Leave & Payments ....................................................................43

– Commission Payments ......................................................................... 44

– Dismissal .................................................................................................. 44

– Misconduct .............................................................................................. 44

Central Provident Fund (CPF) ...............................................................................49

• Calculation of CPF Contributions ...............................................................49

• Definition of Wages in CPF Contributions ................................................49

• Types of Wages in CPF Contributions ....................................................... 50

• Limits on CPF Contributions .........................................................................51

• A General Guide to Payments that Attract CPF Contributions ............53

COnTEnTS

© Copyright 2014 Stone Forest Accountserve Pte Ltd 3

• Common CPF Reporting Mistakes Made by Employers .........................59

Statutory Donations ................................................................................................67

• Chinese Development Assistance Council (CDAC) Fund .......................67

• Singapore Indian Development Association (SInDA) Fund ..................67

• Mosque Building and Mendaki Fund (MBMF) ...........................................67

• Eurasian Community Fund (ECF) ............................................................... 68

• SHARE Programme Donations .................................................................. 68

Employment of Foreign Manpower .......................................................................71

• Types of Employment Passes (Accurate as at 1 January 2014) ............71

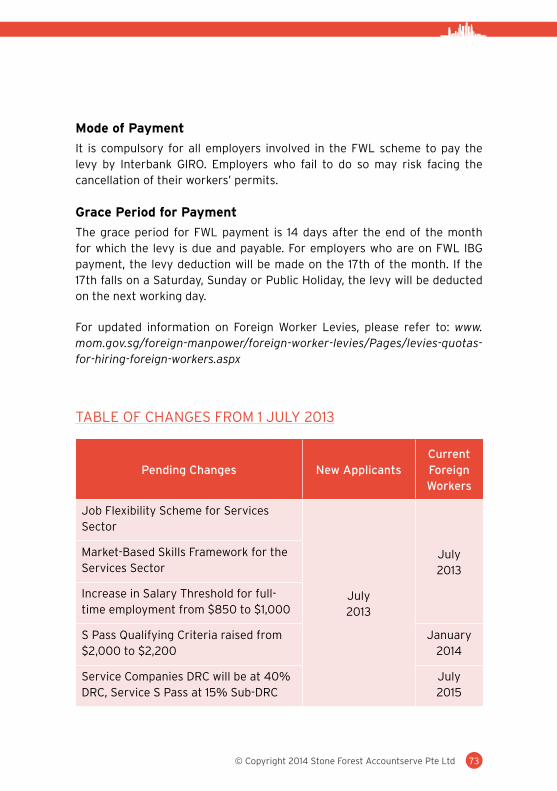

• Foreign Worker Levy (FWL) .......................................................................... 72

• Table of Changes from 1 July 2013 ............................................................. 73

Other Regulations .................................................................................................... 77

• Skills Development Levy (SDL).................................................................... 77

• national Service Make Up Pay (MUP) ........................................................ 77

Tax Reporting for Employee’s Remuneration ....................................................81

• Year-end Reporting .........................................................................................81

– Forms of Submission ...............................................................................81

– Types of Tax Forms ..................................................................................81

– Common Mistakes Made by Employers .............................................82

• Tax Clearance ..................................................................................................85

– What is Tax Clearance? ..........................................................................85

– When to Seek Tax Clearance ................................................................85

– What to Do pending Tax Clearance .................................................... 86

– FAQs on Tax Clearance ......................................................................... 86

The HR Practitioners’ Guide to Key Employment Legislation4

DISCLAIMER

This Guide is only intended to provide a general understanding of Singapore’s human resource and payroll processes and policies.

Singapore regularly updates its legislation, judicial decisions and administrative guidelines. Because this presentation is based on laws and regulations in Singapore that are subject to change at any time, possibly even on a retroactive basis, any such change could adversely affect the contents of this Guide.

no reader should act solely upon any information contained in this Guide in their fulfilment of regulatory obligations whether within or outside Singapore. nothing mentioned in these pages are binding on Singapore government authorities.

Professional advice should always be sought before taking any action on specific issues and making any significant payroll decisions. While every effort has been made to ensure the accuracy of the information contained herein, PayrollServe shall not be responsible for any errors, inaccuracies or omissions.

The information provided in this Guide is accurate as of 1 January 2014, though some details may have changed since then. For additional and more current information, please refer to www.PayrollServe.com.sg.

OvERviEw

OVERVIEW

© Copyright 2014 Stone Forest Accountserve Pte Ltd 5

HUMAn RESOURCE & PAYROLL ADMInISTRATIOn

What is Human Resource?

Human Resource is the management process of an organisation’s workforce, or human resources. It is responsible for the attraction, selection, training, assessment, and rewarding of employees, as well as overseeing organisational leadership and culture and ensuring compliance with employment and labour laws.

What is Payroll?

In a company, payroll accounting is the sum of money paid to employees, e.g. wages, bonuses and deductions, for the services they provided during a certain period of time.

Payroll plays a major role in a company for several reasons. From an accounting point of view, payroll is crucial because payroll and payroll taxes considerably affect the net income of most companies and they are subject to laws and regulations.

From an ethics-in-business viewpoint, payroll is a critical department as employees are responsive to payroll errors and irregularities: good employee morale requires timely and accurate payroll processing.

Objective of this Guide

This Guide is a compilation of information extracted/adapted from the CPF Board, IRAS, nS and MOM websites. Its purpose is to serve as a handy and easy reference for Business Executives who are unfamiliar with Payroll Regulations in Singapore.

Who is PayrollServe?

We specialise in meeting basic to complex payroll and HR administration needs of hundreds of MnCs, SMEs and small businesses in Asia. We are the Payroll Outsourcing Firm of Choice for SMEs in Asia and beyond.

A Stone Forest CompanyPayrollServe ®

InternationalGlobally Connected

Details on

Next Page

PAYROLL & BENEFITS ADMINISTRATION�

OUTSOURCING

Payroll Management

Expense Claims

ManagementLeave

Management

A Stone Forest CompanyPayrollServe ®

InternationalGlobally Connected

PAYROLL & BENEFITS ADMINISTRATION�

OUTSOURCINGPayroll ManagementOutsourcing payroll administration lets your HR team focus on improving business operations rather than managing existing ones.

Leave ManagementOur online leave management solution enables your organisation to stay on top of all leave requests and lets you effectively manage leave approvals from wherever you are.

Expense Claims ManagementOur expense claims management solution streamlines your entire claim process and provides in-depth visibility of global spending.

www.PayrollServe.com.sg

Or call us at +65 6336 0600

Learn More

The HR Practitioners’ Guide to Key Employment Legislation8

There are usually eight steps in a normal payroll cycle. In this chapter, we will take a closer look at some of the steps in detail and their implications for the company.

To ensure punctuality of the payday, the company has to find the appropriate cut-off date for each step. We will explore more on how to derive a proper time frame later in this chapter.

PayROLL PROcEssinG cycLE

PAYROLL PROCESSInG CYCLE

step 1:Collecting

Information

step 5:Payroll

Approval

step 4:Generate Payroll Reports

step 2:Information

Cut-off

step 3:Process Payroll

Pay Day

step 6:Process

Salary Credit & Pay Slips

step 7:Month-end

Reports

© Copyright 2014 Stone Forest Accountserve Pte Ltd 9

STEP 1: COLLECTInG InFORMATIOn

A payroll professional will usually need to collect and compile all data to process the following payments/deductions during a payroll cycle:

• Overtime / Undertime

In order to keep track of hours worked, companies either purchase a time management system where the employees can clock in and out, or keep a manual timesheet.

The timesheets collated are usually verified or approved by the employees’ respective supervisors before they are sent to the payroll department for processing.

(More information regarding the Employment Act regulation on Overtime Payment and Calculation can be found on Page 30.)

• attendance / Leave

To track leave taken, the company can choose to either use a leave management system or manual leave application form.

The payroll administrator will check for unpaid leave deductions or annual leave payments when processing the payroll.

(More information regarding the Employment Act regulation on Leave Entitlements and Calculations can be found on Page 37.)

• Reimbursements / claims

Reimbursements may refer to expenses borne by the employee for business purposes, e.g. clients’ entertainment, office stationery, travelling claims, transport claims, etc.

Reimbursements have to be supported by both receipts and the supervisor’s approval before payroll processing. Companies are required to keep 7 years of reimbursement records in case of a Statutory Board audit.

The HR Practitioners’ Guide to Key Employment Legislation10

Claims usually refer to staff benefits, e.g. medical and dental expense, gymnasium memberships, etc. A company may choose to tie up with an insurance company to offer the above benefits.

• commissions / incentives

The payment depends on the employee’s employment contract or company policies.

(More information regarding the Employment Act regulation on Commission Payment after Termination can be found on Page 44.)

STEP 2: InFORMATIOn CUT-OFF

To work out the appropriate time frame, the company will estimate the time needed for each step. This is illustrated in the example below:

steps Days needed Date

Information Cut-off

Process Payroll 2-3 Working Days

Generate Payroll Reports 1 Working Day

Approval Process 1-2 Working Days

Process Salary Credit & Payslips 1 Working Day

Bank Processing Date 2 Working Days

Payday 28th

PAYROLL PROCESSInG CYCLE

© Copyright 2014 Stone Forest Accountserve Pte Ltd 11

After determining the time needed for each step, the company will be able to set the information cut-off date. For planning, it is recommended that the company should take into consideration weekends and public holidays. This is illustrated in the example below:

steps Days needed Date

Information Cut-off 12th

Process Payroll 2-3 Working Days 17th

Generate Payroll Reports 1 Working Day 18th

Approval Process 1-2 Working Days 20th

Process Salary Credit & Payslips 1 Working Day 24th

Bank Processing Date 2 Working Days 25th

Payday 28th

STEP 3: PROCESS PAYROLL

There are 3 common methods by which the company can handle its payroll processes.

TypesManual Payroll Processing

system Payroll Processing

Outsourcing Payroll

Methods Payroll is usually calculated with Microsoft Excel.

Payroll is done in-house using payroll software.

Payroll is done by an external party.

The HR Practitioners’ Guide to Key Employment Legislation12

TypesManual Payroll Processing

system Payroll Processing

Outsourcing Payroll

Benefits Money saved on purchasing payroll system and maintenance.

Payroll calculations — such as CPF deductions and prorated salaries — can be completed in a fraction of the time required for manual payroll processing.

Year-end reporting is also usually automated, and both payslips and annual reports are archived in case copies are needed later.

Compliance with tax rules and government regulations is the responsibility of your vendor. Punctual and accurate payroll processing gives employer peace of mind.

The company’s payroll will not be affected should its payroll personnel decide to leave the company.

Challenges Faced

Company is usually heavily reliant on a single individual’s expertise and diligence for calculation and Statutory Board compliance.

The person who is in charge of payroll will have to ensure that the system is updated regularly in accordance with any Statutory Board changes.

Finding a reliable Payroll Vendor that can ensure privacy and security.

PAYROLL PROCESSInG CYCLE

© Copyright 2014 Stone Forest Accountserve Pte Ltd 13

STEPS 4 & 5: GEnERATE PAYROLL REPORTS AnD APPROVAL

In order to ensure accountability and accuracy, most companies will assign a different person to check and approve the payroll. This is usually the Human Resource Manager or Company Director.

Common reports generated for checking and approval include:• Payroll Register;

• Timecard Reports (For Overtime/Undertime/Leave);

• Payments and Deductions Report;

• CPF Contribution Report;

• Payment Breakdown Reports (Bank Transfer, Cheque); and

• Variance Reports

The HR Practitioners’ Guide to Key Employment Legislation14

STEP 6: PROCESSInG SALARY CREDIT AnD BAnk PROCESSInG

There are two common methods for salary credit. One is by cheque payment. The other method, which is highly encouraged by the Singapore Government, is by bank transfer or GIRO.

The table below is a list of banks commonly used in Singapore and their bank details for transfer.

Bank name

Bank code

Bank code

account no. (E.g.)

Remarks

UOB 7375 030 9102031012 • 10-digit Account no.

• Use first 3 digits of Account no. and refer to http://www.uob.com.sg/assets/pdfs/global/achcode.pdf to retrieve the corresponding Branch Code

FEB 7199 004 5041920123 • 10-digit Account no.

• Use first 3 digits of Account no. and refer to http://www.uob.com.sg/assets/pdfs/global/achcode.pdf to retrieve the corresponding Branch Code

PAYROLL PROCESSInG CYCLE

© Copyright 2014 Stone Forest Accountserve Pte Ltd 15

Bank name

Bank code

Bank code

account no. (E.g.)

Remarks

DBS 7171 005 0052312891 • 10-digit Account no.

• Use first 3 digits of Account no. as the Branch Code

e.g. For account 0052312891, the Branch Code will be 005. (Account No. will remain as

0052312891.)

POSBank 7171 081 084102395 • 9-digit Account no.

• Use 081 as Branch Code for all POSBank accounts

OCBC 7339 550 1089550 • Length of Account no. varies

• Use first 3 digits of Account no. as Branch Code

• Drop first 3 digits of Account no. for the Account no. field

e.g. for account 5501089550, the Branch Code will be 550 and the Account No. will be 1089550.

The HR Practitioners’ Guide to Key Employment Legislation16

Bank name

Bank code

Bank code

account no. (E.g.)

Remarks

HSBC 7232 146 172002492 • Length of Account no. varies

• Use first 3 digits of Account no. as Branch Code

• Drop first 3 digits of Account no. for the Account no. field e.g. for account 146172002492, the Branch Code will be 146 and the Account No. will be 172002492.

StandardChartered

7144 018 1803645852 • 10-digit Account no.

• Use ‘0’ + 1st two digits of Account no. as Branch Code

• Account no.: the full 10-digit Account no.

Source: www.uob.com.sg/assets/pdfs/global/achcode.pdf

PAYROLL PROCESSInG CYCLE

© Copyright 2014 Stone Forest Accountserve Pte Ltd 17

STEP 7: MOnTH-EnD REPORTInG

Month-end reports can be divided into 2 different types — Statutory and Company Reports.

Examples of common month-end company reports are Payroll General Ledger and Fund Movements Reports.

The month-end Statutory Report usually refers to the Central Provident Fund (CPF) Report.

(More information on the Central Provident Fund can be found on Page 49.)

A Stone Forest CompanyPayrollServe ®

InternationalGlobally Connected

Details on

Next Page

PAYDAY! HRMS

Employee Self-Service

(ESS)

Human Resource

Information System (HRIS)

Payroll Expense ClaimsLeave

A Stone Forest CompanyPayrollServe ®

InternationalGlobally Connected

PAYDAY! HRMS

www.PayrollServe.com.sg

Or call us at +65 6336 0600

Learn More

Reports

Alerts

CostCentre

ImportExport

HRIS

Payroll Leave

ESS ExpenseClaims

HRMS

HRMS is a web-based application designed to allow HR/Payroll personnel to update employees’ details and perform payroll processing from anywhere, anytime.

The standard Human Resource Management modules are:■ Payroll Module■ Leave Module■ Expense Claims Module■ Human Resource

Information System (HRIS) Module

■ Employee Self-Service (ESS) Module

The payroll, leave and claims management modules can each be adopted as a stand-alone system or partially/fully integrated with the other modules.

The HR Practitioners’ Guide to Key Employment Legislation20

EMPLOyMEnT acT

EMPLOYMEnT ACT

The computations and regulations mentioned in this section apply to employees who are covered by the Employment Act.

The Employment Act covers every employee (regardless of nationality) who is under a contract of service with an employer except:

1. Managers and executives (however, those earning basic monthly salaries of $4,500 and below are covered partially on payment of salaries only)

2. Seaman

3. Domestic worker

4. Person employed by a Statutory Board or the Government

Effective from 1 April 2014

1. Managers and executives earning a basic monthly salary not exceeding $4,500 will be covered under the Employment Act, except for the provisions in Part IV.

2. non-workmen employees earning a basic monthly salary not exceeding $2,500 will be covered under Part IV of the Employment Act.

Information in this section is extracted/adapted from www.mom.gov.sg.

new

© Copyright 2014 Stone Forest Accountserve Pte Ltd 21

COnTRACT OF SERVICE

A contract of service is defined by Ministry of Manpower (MOM) as any written or verbal agreement (expressed or implied) that establishes an employer-employee relationship.

The employer under the law is not allowed to change the terms and conditions of employment unless the employee agrees to it. Terms or conditions that are less favourable than provisions under the Employment Act are illegal, null and void. Essential clauses of contracts of service are:

• Commencement of employment;

• Appointment – job title and job scope;

• Hours of work;

• Probation period (if any);

• Remuneration;

• Employee’s benefits (e.g. sick leave, annual leave, maternity leave);

• Termination of contract – notice period; and

• Code of conduct

Types of Contract of Service

• Full-time : not less than 35 hours per week

• Part-time : Less than 35 hours per week

• Casual or Relief: Ad hoc work arrangements

Itemised Payslips and Employment Records

A set of Tripartite Guidelines has been released to encourage and guide employers to issue itemised payslips for all their employees. The Government will closely monitor the adoption of the guidelines, before phasing in the requirements over time.

Since 1 April 2014, a range of user-friendly tools, for example, simple payslip booklets, download templates and funding support for customised solutions, has been made available on MOM’s website.

new

The HR Practitioners’ Guide to Key Employment Legislation22

EMPLOYMEnT ACT

SALARIES

DEfInITIOn Of SAlARy

Salary refers to all remuneration, e.g. base salary, allowances, bonuses, commissions and incentives, payable to an employee with respect to work done under the contract of service.

It does not include:

• Allowances for travelling, housing, utilities, medical and other amenities

• Pension or CPF funds contributed by employer

• Reimbursements to employee for expenses incurred by him/her in the course of employment

• Retrenchment benefits

• Goodwill payment or gratuity payable on discharge or retirement

There is no minimum wage law in Singapore. However, there may be certain wage criteria that must be fulfilled in some situations.

Salary is subject to negotiation and mutual agreement between the employer and employee.

new Wage Rules under Environmental Public Health Bill

Companies in the cleaning and security sectors will soon be subject to new rules that require them to set basic salaries for workers.

• Under the Environmental Public Health Bill, from September 2014, the entry-level pay for cleaners will be set at S$1,000 monthly, 20 per cent higher than today’s median basic wage for the sector.

• Details for the security sector are still being worked out.

new

© Copyright 2014 Stone Forest Accountserve Pte Ltd 23

fREquEnCy Of SAlARy PAymEnT

An employee must be paid a minimum frequency of once a month.

In general, all salary components must be paid within 7 days after the end of the salary period. The following are exceptions:

situation salary must be paid

Overtime work within 14 days after the end of the salary period

Dismissal/Termination by Employer On the last day of employment or within 3 working days from the date of dismissal/termination

The employee terminates the contract by resigning and has served the required notice period.

On the last day of employment

The employee terminates the contract by leaving employment without notice or without serving the required notice period.

Within 7 working days of the last day of employment

AuTHORISED SAlARy DEDuCTIOnS

1. Absence from work.

2. For damage to or loss of goods/money that an employee is accountable for. no deductions are to be made until an inquiry is held by the employer. The total amount of such deductions must not exceed 25% of the employee’s one month’s salary, and may only be made on a once-off basis.

3. Cost of meals supplied by the employer at the request of the employee.

4. Accommodation or for amenities and services supplied by the employer and accepted by the employee.

The HR Practitioners’ Guide to Key Employment Legislation24

5. Recovery of advances, loans or adjustment of overpayments of salary. Advances may be recovered in instalments not exceeding 25% of the salary due for the period and spread over not more than twelve months.

6. Income tax payment and CPF contributions.

7. Contributions to superannuation scheme or provident fund or any other scheme, approved by the Commissioner of Labour, at the request of the employee in writing.

8. Payments to any registered co-operative society with the written consent of the employee.

9. For any other purpose that may be approved upon application from time to time by the Minister for Manpower.

mAxImum AmOunT Of DEDuCTIOn

The maximum deduction amount in respect of any one salary period is 50% of the total salary. IT DOES nOT InCLUDE deductions made for:

1. Absence from work;

2. Payment of income tax;

3. Recovery of advances/loans; and

4. Payments with the consent of the employee to registered co-operative society in respect of subscriptions, entrance fees, instalment of loans, interest and other dues payable.

DEDuCTIOn DuRInG TERmInATIOn

However, when the contract of service is terminated, the deduction from the employee’s last payment of salary may exceed 50%. This is to enable the employer to recover any sum of money owed by an employee to him.

EMPLOYMEnT ACT

© Copyright 2014 Stone Forest Accountserve Pte Ltd 25

Effective from 1 April 2014

25% sub-cap will be imposed for deductions for accommodation, amenity and services (Within the existing 50% total cap)

mOnTHly VARIABlE COmPOnEnT (mVC)

MVC is a flexible and performance-based wage system.

It is part of monthly basic salary and should be included in computing overtime payment and CPF contribution.

For MVC to be an effective mechanism for wage adjustment, it is recommended that MVC should form 10% of monthly basic salary. The percentage of MVC should be the same for all levels of employees.

Purpose of mVC

• When the company is doing well, it enables the company to reward its employees by enhancing their monthly salaries.

• During severe business downturns, it serves as a “standby” component that can be used to bring down wage costs in order for the company to survive and save jobs.

new

Authorised Deductions(50% of total salary)

T O T a L s a L a R y

The HR Practitioners’ Guide to Key Employment Legislation26

WAGE DEFInITIOn

mOnTHly BASIC RATE Of PAy

1. The basic rate of pay includes wage adjustments and increments that an employee is entitled to under his/her contract of service, but excludes:

• Additional payments, e.g., Overtime, Bonus, Annual Wage Supplements;

• Any sum paid to the employee for reimbursement of special expenses incurred by him/her in the course of employment;

• Productivity incentive payments; and

• Any allowance however described

2. Basic rate of pay is used to calculate:

• Pay for work on a Rest Day or Public Holiday

• Overtime Pay

3. For a monthly-rated employee, the basic rate of pay for one day is calculated as follows:

12 x Monthly Basic Rate of Pay

52 x average number of days an employeeis required to work in a week

EMPLOYMEnT ACT

© Copyright 2014 Stone Forest Accountserve Pte Ltd 27

mOnTHly GROSS RATE Of PAy

1. Refers to the total amount of money including allowances payable to an employee for working for one month, but excludes:

• Additional payments, e.g. Overtime, Bonus, Annual Wage Supplements;

• Any sum paid to the employee for reimbursement of special expenses incurred by him/her in the course of employment;

• Productivity incentive payments; and

• Travelling, food or housing allowances

2. The “Gross Rate of Pay” is used to calculate payment of:

• Salary in lieu of notice of termination;

• Deduction of pay for absence from work;

• Paid holidays; and

• Paid leave

InCOmPlETE mOnTHly WAGES

For the purpose of calculating salary, a ‘month’ or ‘complete month’ refers to any month in the calendar year.

When to prorate?

• Starts work after the first day of the month

• Leaves employment before the last day of the month

• Takes no-pay leave of one day or more during the month

The HR Practitioners’ Guide to Key Employment Legislation28

How to prorate?

Salary payable to a monthly-rated employee for an incomplete month of work is calculated using the formula below:

salary payable for incomplete month of work

=Monthly gross rate of pay

xactual days worked

Total number of working days in that month*

* Excludes rest days and non-working days but includes public holidays

Example:Sharon joined Company ABC Ltd on 8 August 2011.

Her monthly basic salary is $2,000, and her fixed monthly transport allowance is $300. She is working on a 5-day week.

What is her monthly wage for August 2011?

solution Monthly Gross Rate of Pay:Basic Salary ($2,000) + Fixed Monthly Allowance ($300) = $2,300

Working days in August*: 23 working days

Actual Working Days : 18 days

august 2011 Monthly wage: ($2,300/23 days) x 18 days = $1,800

* Excludes rest days and non-working days but includes public holidays

EMPLOYMEnT ACT

© Copyright 2014 Stone Forest Accountserve Pte Ltd 29

HOURS OF WORk

COnTRACTuAl HOuRS Of WORk

MOM defines “hours of work” as the period during which the employee is expected to carry out duties assigned by the employer, excluding rest and meal breaks. Under the Employment Act, an employee is not allowed to work more than 12 hours a day or more than 44 hours a week.

LunchHours worked

for the DayHours worked for the week

(assuming 5.5-day week)

1 hour 8 hours 8 x 5.5 = 44 hours

If the number of hours worked is less than 44 hours every alternate week, the limit of 44 hours a week may be exceeded in the other week. However, this must be stated in the contract of service and is subject to a maximum of 48 hours in one week or 88 hours in any continuous two-week period.

Generally, employees are not required to work more than 6 consecutive hours without a break, up to a maximum of 8 consecutive hours. As stipulated by MOM, breaks should be no less than 45 minutes.

mAxImum HOuRS AllOWED

An employee is not allowed to work:

1. More than 12 hours within a day except in the following circumstances:

a. Accident or threat of accident;

b. Work that is essential to the life of the community, national defence or security;

c. Urgent work to be done to machinery or plant; or

d. An interruption of work that was impossible to foresee.

The HR Practitioners’ Guide to Key Employment Legislation30

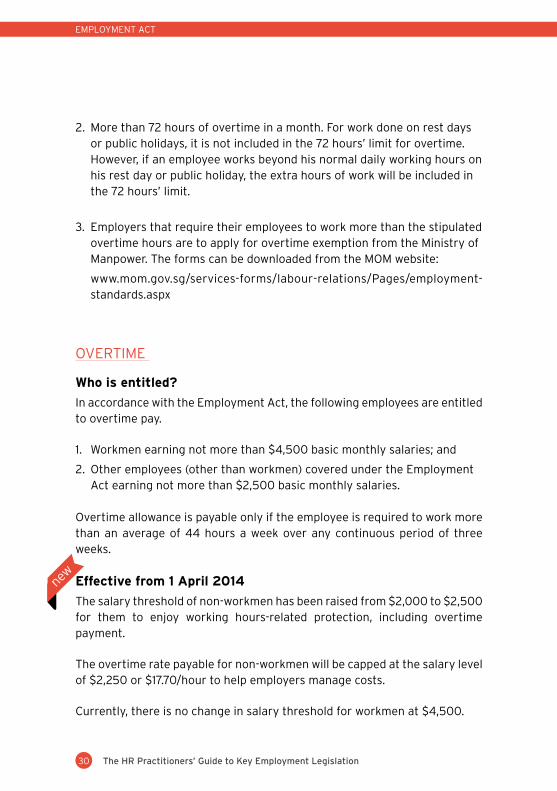

2. More than 72 hours of overtime in a month. For work done on rest days or public holidays, it is not included in the 72 hours’ limit for overtime. However, if an employee works beyond his normal daily working hours on his rest day or public holiday, the extra hours of work will be included in the 72 hours’ limit.

3. Employers that require their employees to work more than the stipulated overtime hours are to apply for overtime exemption from the Ministry of Manpower. The forms can be downloaded from the MOM website:

www.mom.gov.sg/services-forms/labour-relations/Pages/employment-standards.aspx

OVERTIME

Who is entitled?

In accordance with the Employment Act, the following employees are entitled to overtime pay.

1. Workmen earning not more than $4,500 basic monthly salaries; and

2. Other employees (other than workmen) covered under the Employment Act earning not more than $2,500 basic monthly salaries.

Overtime allowance is payable only if the employee is required to work more than an average of 44 hours a week over any continuous period of three weeks.

Effective from 1 April 2014

The salary threshold of non-workmen has been raised from $2,000 to $2,500 for them to enjoy working hours-related protection, including overtime payment.

The overtime rate payable for non-workmen will be capped at the salary level of $2,250 or $17.70/hour to help employers manage costs.

Currently, there is no change in salary threshold for workmen at $4,500.

EMPLOYMEnT ACT

new

© Copyright 2014 Stone Forest Accountserve Pte Ltd 31

OVERTImE COmPuTATIOn

• For a monthly-rated employee, his hourly basic rate of pay is computed as follows:

12 x Monthly Basic Rate of Pay

52 x 44

• For a daily-rated employee, his hourly basic rate of pay is computed as follows:

Daily Pay at the Basic Rate

working Hours Per Day

• For a piece-rated employee, his hourly basic rate of pay is computed as follows:

Total weekly Pay at the Basic Rate of Pay

Total number of Hours worked in the week

Based on the hourly basic rate of pay, the overtime pay for the 3 categories of employees is to be calculated as follows:

Hourly Basic Rate of Pay x 1.5 x number of Hours of Overtime worked

The HR Practitioners’ Guide to Key Employment Legislation32

Example 1:In September, Alicia clocked 30 hours of overtime work.

Her monthly basic salary is $2,000.

How much should she receive for her overtime?

solution Basic Rate of Pay : $2,000

Hourly Basic Rate of Pay: ($2,000 x 12) / (52 x 44) = $10.4895

OT Payable : $10.4895 x 1.5 x 30 = $472.03

Example 2:Brenda clocked 20 hours of overtime work.

Her monthly basic salary is $1,800 and her fixed monthly transport allowance is $400.

How much should she receive for her overtime?

solution Basic Rate of Pay* : $1,800

Hourly Basic Rate of Pay: ($1,800 x 12) / (52 x 44) = $9.4406

OT Payable : $9.4406 x 1.5 x 20 = $283.22

* Basic Rate of Pay does not include fixed monthly allowances

Effective from 1 April 2014

The overtime rate payable to non-workmen earning up to $2,500 basic monthly salary will be capped at the basic monthly salary level of $2,250.

EMPLOYMEnT ACT

new

© Copyright 2014 Stone Forest Accountserve Pte Ltd 33

salary per

MonthFormula for Hourly Rate

Hourly Rate

(Before 1 april 2014)

Hourly Rate

(From 1 april 2014)

$1,60012 x Monthly Basic Rate of Pay

52 x 448.40 x 1.5 = $12.59

(no Change)

$2,00012 x Monthly Basic Rate of Pay

52 x 4410.485 x 1.5 = $15.73

(no Change)

$2,10012 x Monthly Basic Rate of Pay

52 x 44

not covered for Overtime

Pay

11.01 x 1.5 = $16.52

$2,25012 x Monthly Basic Rate of Pay

52 x 4411.80 x 1.5 =

$17.70

$2,50012 x Monthly Basic Rate of Pay

52 x 44

$17.70(OT

Capped)

Rest Day Work

The rest day can be on a Sunday or any other day. The employer must inform the employee before the beginning of each month.

It is not a paid day.

The longest allowable interval between two rest days is 12 days.

How is payment for work done on a rest day calculated?

1. Work done at employer’s request:

• One day’s salary when the employee works up to half the normal daily working hours

• Two days’ salary when the employee works more than half the normal daily working hours

The HR Practitioners’ Guide to Key Employment Legislation34

2. Work done at employee’s request:

• Half day’s salary when the employee works up to half the normal daily working hours

• One day’s salary when the employee works more than half the normal daily working hours

If an employee works beyond the normal daily working hours on a rest day, he/she should be paid at least 1.5 times the hourly basic rate of pay.

Example:Gwen’s monthly basic salary is $2,000, and her fixed monthly transport allowance is $300.

She works a 5-day week, 8 hours each day.

She was asked by her boss to work 10 hours on her rest day.

How much should she receive for her overtime?

solution Rest Day Pay : [($2,000 x 12) / (52 x 5)] x 2 = $184.62

Extra OT Hours : 10 – 8 = 2

OT Payable : [($2,000 x 12) / (52 x 44)] x 1.5 x 2 = $31.47

Total Rest Day work Payable: $184.62 + $31.47 = $216.09

EMPLOYMEnT ACT

© Copyright 2014 Stone Forest Accountserve Pte Ltd 35

LEAVE & HOLIDAYS

PuBlIC HOlIDAyS

All employees covered by the Employment Act are entitled to 11 paid public holidays in a year. The 11 gazetted public holidays are:

1. new Year’s Day

2. 1st Day of Chinese new Year

3. 2nd Day of Chinese new Year

4. Hari Raya Puasa

5. Hari Raya Haji

6. Good Friday

7. Labour Day

8. Vesak Day

9. national Day

10. Deepavali

11. Christmas Day

The employer and employee may mutually agree to substitute a public holiday for any other day.

unpaid public holiday

The employee is not entitled to Public Holiday pay if he is on:

• Unauthorised leave on the day immediately before or after a holiday

• Approved no pay leave immediately before and after a holiday

The HR Practitioners’ Guide to Key Employment Legislation36

Public holiday work

Employers may sometimes require an employee to work on a public holiday. If so, the employee should be paid:

• An extra day’s salary at the basic rate of pay for working on the public holiday; and

• The gross rate of pay for that holiday.

If the employee works beyond normal working hours on a public holiday, the rate of overtime payment must be at least 1.5 times the employee’s hourly basic rate of pay.

Absence before or after a public holiday

A monthly-rated employee who works on a public holiday but absents without reason on the working day immediately before or after the holiday is not entitled to the holiday pay that is already included in his monthly gross salary.

His employer can therefore deduct one day’s pay at the gross rate for the holiday pay from his monthly gross salary. However, his employer has to pay him one day’s pay at the basic rate of pay for working on the public holiday.

Example:Aaron’s monthly basic salary is $2,000 and his fixed monthly transport allowance is $300.

He works a 5-day week, 8 hours each day.

He was asked by his boss to work 10 hours on a public holiday.

How much should he receive for his public holiday work?

EMPLOYMEnT ACT

© Copyright 2014 Stone Forest Accountserve Pte Ltd 37

solution Public Holiday Pay: Gross Rate of Pay ($2,000 x 12) / (52 x 5) = $92.31

Extra OT Hours : 10 – 8 = 2

OT Payable : [($2,000 x 12) / (52 x 44)] x 1.5 x 2 = $31.47

Total Public Holiday work Payable: $92.31 + $31.47 = $123.78

Effective from 1 April 2014

Professionals, Managers and Executives earning a basic monthly salary of up to $4,500 will receive the following protection.

Before 1 april 2014 Effective 1 april 2014

not covered under Employment act

Entitled to 11 paid public holidays in a year

not covered under Employment act

Employers will be allowed to grant time off in-lieu for those who are required to work on public holidays, subject to mutual agreement.At least 1/2 day off in-lieu has to be granted in the absence of mutual agreement.

AnnuAl lEAVE

Entitlement

An employee is entitled to annual leave if he/she has worked for at least three months.

new

The HR Practitioners’ Guide to Key Employment Legislation38

An employee’s annual leave entitlement under Part IV of the Employment Act is as follows:

years of service annual Leave Entitlement

1 7

2 8

3 9

4 10

5 11

6 12

7 13

8 and above 14

An employee’s year of service begins from the day he/she started work with the employer.

The following applies to employees who have worked less than a year:

1. His/her annual leave should be prorated using the following formula:

(no. of months in service/12) x 7

2. Periods of no-pay leave should not be included when computing annual leave entitlement.

Encashing annual leave

Annual leave may be encashed under the following circumstances:

1. Termination of employment by either the employer or the employee

2. At the discretion of the employer

3. Contractual agreement between employer and employee

EMPLOYMEnT ACT

© Copyright 2014 Stone Forest Accountserve Pte Ltd 39

formula to calculate annual leave:

12 x Monthly Gross Rate of Pay x annual Leave Balance

52 x average number of days an employee is required to work in a week

Example:Michelle’s monthly basic salary is $2,000 and her fixed monthly shift allowance is $200.

She works a 5-day week, 8 hours each day.

Calculate how much the company needs to pay her if it allows her to encash 4 days of annual leave.

solution Gross Rate of Pay : $2,000 + $200 = $2,200

Average working days in a week: 5 days

Annual Leave (Encashed Amount)

[(12 x $2,200) / (52 x 5)] x 4 days = $406.15

Effective from 1 April 2014

Professionals, Managers and Executives earning a basic monthly salary of up to $4,500 will receive the following protection.

Before 1 april 2014 Effective 1 april 2014

not covered under Employment act

Entitled to annual leave

new

The HR Practitioners’ Guide to Key Employment Legislation40

unPAID lEAVE

In the event where the employee has no annual leave left, the employer may allow him to take unpaid leave.

The formula for deducting unpaid leave for a monthly-rated worker is:

Monthly Gross Rate of Pay x number of Unpaid Leave Taken

number of working Days in a Month

Example:Sherry’s monthly basic salary is $2,000 and her fixed shift transport allowance is $200. She works a 5-day week, 8 hours each day.

Calculate how much the company needs to deduct if she goes on 4 days of unpaid leave in August 2011.

solution Gross Rate of Pay : $2,000 + $200 = $2,200

number of working days in August 2011: 23(inclusive of paid public holidays)

Unpaid Leave Deduction: ($2,200 / 23) x 4 days = $382.61

SICk lEAVE

An employee covered by the Employment Act is entitled to paid sick leave, including medical leave issued by a dentist if:

• The employee has served the employer for at least three months.

• The employee has informed or attempted to inform the employer of his/her absence within 48 hours. Otherwise, the employee will be deemed to be absent from work without permission or reasonable excuse.

• The sick leave is certified by the company’s doctor, or by a government doctor (including doctors from approved public medical institutions).

EMPLOYMEnT ACT

© Copyright 2014 Stone Forest Accountserve Pte Ltd 41

The number of days of paid sick leave a new employee is entitled to depend on his service period:

Months of service completed by anew employee

Paid outpatientnon-hospitalisation

leave (days)

Paid hospitalisation leave (days)

3 months 5 15

4 months 5 + 3 = 8 15 + 15 = 30

5 months 8 + 3 = 11 30 + 15 = 45

6 months 11 + 3 = 14 45 + 15 = 60

thereafter 14 60

If an employee has worked for at least three months, his employer is legally obliged to bear the medical consultation fee. For other medical costs, such as medication, treatment or ward charges, the employer is obliged to bear such costs depending on the medical benefits provided for in the employee’s employment contract or the collective agreement signed between the company and the union.

Sick leave taken on a half working day

Sick leave taken on a half working day (e.g. Saturday) should be considered as one day’s sick leave.

Effective from 1 April 2014

• Employers will not be required to grant paid sick leave and bear the medical consultation fees for employees seeking or undergoing medical treatment for cosmetic purposes.

• Professionals, Managers and Executives earning a basic monthly salary of up to $4,500 will be covered under the Employment Act for sick leave benefits.

new

The HR Practitioners’ Guide to Key Employment Legislation42

GOVERnmEnT-PAID lEAVE SCHEmES

Government-paid leave schemes were introduced under the Child Development Co-Savings Act to cover parents of Singapore Citizen children, including managerial, executive and confidential staff. This is to foster an overall pro-family environment in Singapore.

An employee will be entitled to the following leave schemes if he/she is covered under the Child Co-Savings Act and fulfils all conditions required for each leave type.

Marriage & Parenthood package (Effective since 1 January 2009)

Type For Must be Taken Duration

Childcare Leave BothWhen child is below

7 years old6 Days

Maternity Leave MotherWithin 12 months after the birth

of the child16 Weeks

Unpaid Infant Care Leave

BothWhen child is below

2 years old6 Days

Enhanced Marriage & Parenthood package (Effective since 1 May 2013)

Type For Must be Taken Duration

Extended Childcare Leave

BothWhen child is from 7 to 12 years

old (inclusive)2 Days

Paternity Leave Father

Within 16 weeks from the birth of the child, or 12 months from the birth of the child (subject to mutual agreement between

employer and employee)

1 Week

Shared Paternal Leave

Father When child is below 1 year of age 1 Week

Adoption Leave Mother When child is below 1 year of age 4 Weeks

EMPLOYMEnT ACT

© Copyright 2014 Stone Forest Accountserve Pte Ltd 43

TERMInATIOn

TERmInATIOn PROCESS

Termination of a contract of service can be effected either by the employer or employee. An employer cannot reject an employee’s resignation. Employees have the right to resign at any time by serving the required notice period or compensating the employer with salary in lieu of notice.

nOTICE PERIOD & PAymEnTS

• The party who intends to terminate the contract must give notice to the other party in writing.

• The notice period to be given depends on what is agreed in the written contract. If there is no such period previously agreed upon, the following shall apply:

Length of service notice Period

Less than 26 weeks 1 day

26 weeks to less than 2 years 1 week

2 years to less than 5 years 2 weeks

5 years and above 4 weeks

• Formula to calculate short notice payment:

12 x Monthly Gross Rate of Pay x short notice Days

52 x average number of days an employee is requiredto work in a week

AnnuAl lEAVE & PAymEnTS

• The employer cannot force the employee to go on leave during the period of notice, unless the employee consents to it. Any unconsumed annual leave can be encashed by the employee.

The HR Practitioners’ Guide to Key Employment Legislation44

• An employee can use his annual leave to offset the notice period for termination of contract. By bringing forward his last day of employment with the company, he is no longer considered an employee of the company and can start work immediately with his new company after that date.

COmmISSIOn PAymEnTS

An employee’s entitlement to commission payment and the time of commission payment would depend on what is stated in the employment contract or existing policies/practices. If the contract is silent, it is subject to negotiation or mutual agreement between the employee and the employer.

DISmISSAl

Dismissal is the termination of the contract of service of an employee by his employer, with or without notice.

It may or may not be due to the employee’s misconduct.

mISCOnDuCT

An employer may, after an inquiry, terminate an employee’s services without notice if the employee is found guilty of misconduct.

Misconduct refers to a breach of duty or discipline that is inconsistent with the conditions of an employee’s contract of service. Examples of misconduct are theft or dishonesty, disorderly or immoral conduct at work, and wilful insubordination.

If the employee has committed an act of misconduct, the employer should conduct an inquiry before deciding whether to dismiss the employee or to take other forms of disciplinary action. The entire process should be properly documented for possible Ministry of Manpower audits.

EMPLOYMEnT ACT

© Copyright 2014 Stone Forest Accountserve Pte Ltd 45

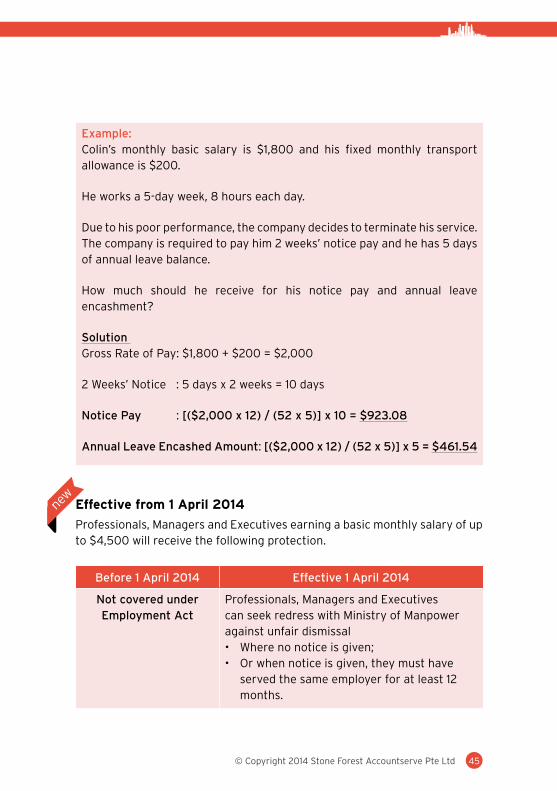

Example:Colin’s monthly basic salary is $1,800 and his fixed monthly transport allowance is $200.

He works a 5-day week, 8 hours each day.

Due to his poor performance, the company decides to terminate his service. The company is required to pay him 2 weeks’ notice pay and he has 5 days of annual leave balance.

How much should he receive for his notice pay and annual leave encashment?

solution Gross Rate of Pay: $1,800 + $200 = $2,000

2 Weeks’ notice : 5 days x 2 weeks = 10 days

notice Pay : [($2,000 x 12) / (52 x 5)] x 10 = $923.08

annual Leave Encashed amount: [($2,000 x 12) / (52 x 5)] x 5 = $461.54

Effective from 1 April 2014

Professionals, Managers and Executives earning a basic monthly salary of up to $4,500 will receive the following protection.

Before 1 april 2014 Effective 1 april 2014

not covered under Employment act

Professionals, Managers and Executives can seek redress with Ministry of Manpower against unfair dismissal• Where no notice is given;• Or when notice is given, they must have

served the same employer for at least 12 months.

new

The HR Practitioners’ Guide to Key Employment Legislation46

Effective from 1 April 2015

Before 1 april 2015 Effective 1 april 2015

Employees with less than 3 years of service with the same employer are not entitled to retrenchment benefits.

Employees with less than 2 years of service with the same employer are not entitled to retrenchment benefits.

EMPLOYMEnT ACT

new

Details on

Next Page

No Payroll Knowledge

Required

Itemised Payslips

100% Accurate & Compliant

24/7 Access Anywhere Anytime

No Setup Fees &

Contracts

Pay-As-You- Use

Software as a Service (SaaS)

PayDay! is an easy-to-use, 100% compliant and 24/7 online payroll solution. It helps to run payroll in three easy steps with no payroll knowledge required, replacing manual payroll processing.

www.PayDay.com.sg

Or call us at +65 6336 8686

Learn More

Run Payroll in 3 Easy Steps

No payroll knowledge required

No minimum contract period and setup fee. No maintenance fees

Bank GIRO file is easily generated in seconds

Automatic generation of CPF and IRAS e-submission or PATLINE files

Your data is 100% safe

100% accurate and compliant with MOM, CPF and IRAS

Itemised payslips via mobile app or any web browsers

24/7 access anytime, anywhere

Get StartedEnter your company

payroll policies, employees & salaries

Process PayrollReview salary &

allowances & process your monthly payroll

And You’re DoneInstant reports, files &

payslips are available for viewing & download

Software as a Service (SaaS)

© Copyright 2014 Stone Forest Accountserve Pte Ltd 49

CEnTRAL PROVIDEnT FUnD (CPF)

cEnTRaL PROviDEnT FUnD (cPF)

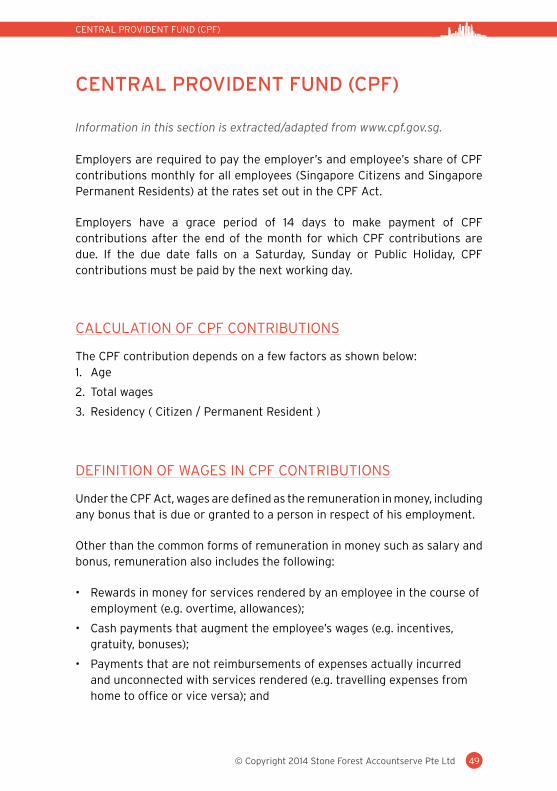

Information in this section is extracted/adapted from www.cpf.gov.sg.

Employers are required to pay the employer’s and employee’s share of CPF contributions monthly for all employees (Singapore Citizens and Singapore Permanent Residents) at the rates set out in the CPF Act.

Employers have a grace period of 14 days to make payment of CPF contributions after the end of the month for which CPF contributions are due. If the due date falls on a Saturday, Sunday or Public Holiday, CPF contributions must be paid by the next working day.

CALCULATIOn OF CPF COnTRIBUTIOnS

The CPF contribution depends on a few factors as shown below:1. Age

2. Total wages

3. Residency ( Citizen / Permanent Resident )

DEFInITIOn OF WAGES In CPF COnTRIBUTIOnS

Under the CPF Act, wages are defined as the remuneration in money, including any bonus that is due or granted to a person in respect of his employment.

Other than the common forms of remuneration in money such as salary and bonus, remuneration also includes the following:

• Rewards in money for services rendered by an employee in the course of employment (e.g. overtime, allowances);

• Cash payments that augment the employee’s wages (e.g. incentives, gratuity, bonuses);

• Payments that are not reimbursements of expenses actually incurred and unconnected with services rendered (e.g. travelling expenses from home to office or vice versa); and

The HR Practitioners’ Guide to Key Employment Legislation50

• Payments that are not genuine pre-estimates of expenses necessarily incurred on behalf of the employer (e.g. fixed amounts of broadband internet charges for home use).

An employee may be rewarded with benefits other than salary. Such employee benefits may be in kind or in money. All remunerations given in money to an employee will require CPF contributions. Some common benefits given in money to an employee include provisions of meal/food allowances, commuted leave pay, commissions/incentives for meeting sales targets, and festive allowances.

CPF contributions are not required for benefits given in kind. Some common benefits that are given in kind to employees include provision of a place of residence, a car, and free or subsidised medical/dental care.

TYPES OF WAGES In CPF COnTRIBUTIOnS

• Ordinary Wages (OW) are wages due or granted wholly and exclusively in respect of an employee’s employment in that month and payable before the due date for payment of CPF contributions for that month.

• Additional Wages (AW) are wages not granted wholly and exclusively for the month. Examples include annual bonus, leave pay, incentives and other payments made at intervals of more than a month.

• Total Wages (TW) — The total amount of an employee’s wages for any calendar month is the sum of his OW for the month and the AW paid to him in that month.

CEnTRAL PROVIDEnT FUnD (CPF)

OW AW TW

© Copyright 2014 Stone Forest Accountserve Pte Ltd 51

LIMITS On CPF COnTRIBUTIOnS

Ordinary Wage (OW) Ceiling

• From 1 January 2011 to 31 August 2011, the OW Ceiling was $4,500 monthly.

• From 1 September 2011, the OW Ceiling has been revised to $5,000 monthly.

Additional Wage (AW) Ceiling

• An employee’s AW Ceiling is computed on a per employer basis.

• The formula for calculating the AW Ceiling for 2011 and 2012 is as follows:

scenarios additional wage ceiling

Employee whose last day of employment is before 1 Sep 2011

$76,500 – Total OW subject to CPF for 2011

Employee whose last day of employment falls within the period from 1 Sep to 31 Dec 2011

$79,333 – Total OW subject to CPF for 2011

Employee in employment from 1 Jan 2012 $85,000 – Total OW subject to CPF for 2012

Example 1:Marcus’s monthly basic salary is $5,500 and his fixed monthly transport allowance is $200. Calculate his AW ceiling for Y2013.

solution Jan 2013 — Dec 2013

Ordinary Wage Ceiling: ($5,500 + $200) > $5,000

Based on Ow ceiling of $5,000 Additional Wage Ceiling: $85,000 – ($5,000 x 12) = $25,000

The HR Practitioners’ Guide to Key Employment Legislation52

Example 2:Jamie’s monthly basic salary is $2,300. Calculate her AW ceiling for Y2013.

solution Jan 2013 — Dec 2013

Ordinary Wage Ceiling: $2,300 < $5,000

Based on Ow ceiling of $5,000 Additional Wage Ceiling: $85,000 – ($2,300 x 12) = $57,400

Example 3:Mick’s monthly basic salary is $5,000, and his fixed monthly transport allowance is $300. Calculate his AW ceiling if his last day with the company is 30 September 2013.

solution Jan 2013 — Sep 2013

Ordinary Wage Ceiling: ($5,000 + $300) > $5,000

Based on Ow ceiling of $5,000 Additional Wage Ceiling: $85,000 – ($5,000 x 9) = $40,000

Example 4:Sam’s monthly basic salary is $2,000. His last day with the company is August 2013. Calculate his AW ceiling.

solution Jan 2013 — Aug 2013

Ordinary Wage Ceiling: $2,000 < $5,000

Based on Ow ceiling of $5,000 Additional Wage Ceiling: $85,000 – ($2,000 x 8) = $69,000

CEnTRAL PROVIDEnT FUnD (CPF)

© Copyright 2014 Stone Forest Accountserve Pte Ltd 53

A GEnERAL GUIDE TO PAYMEnTS THAT ATTRACT CPF COnTRIBUTIOnS

Type of Paymentis cPF

payable?

attendance allowance

Payment to employees for good work and attendance Yes

anniversary cash award

Payment to employees on company’s anniversary Yes

annual wage supplement/bonus

Payment to employees at the end of the financial year Yes

commission

Payment to employees based on percentage of sales achieved Yes

cost of living allowance

Payment to employees as part of employees’ wages Yes

Dirt allowance

Payment to employees for performing field duties Yes

Education allowance

Contractual payment for education of employee’s children. Yes

Payment to employees for employees’ self-improvement programmes no

Education/training reimbursement

Reimbursement for course and examination fees as part of employee’s training programme no

Entertainment expenses

Reimbursement for entertaining company’s clients no

The HR Practitioners’ Guide to Key Employment Legislation54

Type of Paymentis cPF

payable?

Extra duty allowance

Payment to employees for extra work done, e.g. night duty, overtime, public holiday, acting allowance, etc. Yes

Festive allowance

Cash gift (e.g. hongbao) given to employees during festive season Yes

Flexi-benefit expenses

Payments for expenses not necessarily incurred by employer, e.g. employee’s groceries, home renovations, etc. Yes

Reimbursement for expenses necessarily incurred on behalf of the employer, e.g. holiday facilities, professional publications, etc.

no

Finder introduction fees

Payment to employees for introducing workers to company no

Gifts in kind

Award in kind, e.g. token gifts no

Gratuity

Payment to employees for good service while still in employment Yes

Payment to employees upon termination of employment, i.e. compensative in nature no

Grooming and hair cut allowance

Payment to employees for enhancement of appearance Yes

CEnTRAL PROVIDEnT FUnD (CPF)

© Copyright 2014 Stone Forest Accountserve Pte Ltd 55

Type of Paymentis cPF

payable?

Handphone and pager expenses

Payment of handphone and pager allowances to employees Yes

Payment of handphone and pager charges directly to third party, e.g. service provider no

Reimbursement for actual handphone and pager expenses incurred for official purposes no

Holiday expenses

Fixed payment to employees for vacation Yes

Variable sum given as reimbursement for holiday expenses incurred by employees no

Housing/rental expenses

Payment to employees for housing rent Yes

Payment of rent directly to third party e.g. landlord no

incentive allowance

Cash payment incentive Yes

Incentive in kind, e.g. token gifts no

Laundry expenses

Payment to employees for laundry expenses of personal clothing Yes

Reimbursement for laundry expenses to uniformed employees no

Leave pay

Payment in lieu of leave Yes

The HR Practitioners’ Guide to Key Employment Legislation56

Type of Paymentis cPF

payable?

Long-service award

1. Cash award given to employees with less than 5 years’ service and every subsequent period of less than 5 years’ service.

Yes2. Cash award given to employees with at least 5 years’

service and every subsequent period of not less than 5 years’ service (i.e. 5, 10, 15 and so on), and the cash award exceeds the employee’s Ordinary Wages for the month in which it is given. CPF is payable on the amount in excess of the Ordinary Wages.

Cash award given to employees with at least 5 years’ service and every subsequent period of not less than 5 years’ service (i.e. 5, 10, 15 and so on), and the cash award does not exceed the employee’s Ordinary Wages for the month in which it is given.

no

Maternity allowance

Payment to female employees during confinement and in addition to monthly salaries Yes

Maternity subsidy

Reimbursement paid under company’s maternity expenses scheme no

Meal expenses

Monthly lump sum payment for meals to employees Yes

Meal reimbursement for staying beyond working hours, i.e. overtime no

Per diem allowance

Daily allowance given as reimbursement for defraying the cost of an overseas (i.e. out of Singapore) assignment no

CEnTRAL PROVIDEnT FUnD (CPF)

© Copyright 2014 Stone Forest Accountserve Pte Ltd 57

Type of Paymentis cPF

payable?

Personal clothing allowance

Payment to employees to enhance appearance Yes

Probation period pay

Wages for employees on probation Yes

Productivity award

Cash award for staff productivity Yes

sales performance award

Payment to employees for attaining sales target Yes

service charge

Collection by hotels/restaurants and distributed as part of wages to employees Yes

share option

Cash proceeds for the share options given to the employee Yes

Sales proceeds if the shares options have been exercised and the shares are held in the employee’s name

noPayments granted in kind to employees where no cash payments are payable to employees

staff welfare benefits

Gifts in kind to employees on their marriage or birth of their children no

stand-by duty allowance

Payment to employees for stand-by duties Yes

The HR Practitioners’ Guide to Key Employment Legislation58

Type of Paymentis cPF

payable?

Termination benefits

Retirement gratuity, retrenchment pay, ex-gratia payment, salary in lieu of notice, severance pay, compensation for loss of employment

no

Temporary lay-off benefits Yes

Tips

Cash collected from customers to augment wages of hotel and restaurant employees Yes

Transport expenses

Payment to employees for transport subsidies Yes

1. Reimbursement for travel in the line of official duty

no

2. Reimbursement for travel between home and workplace beyond normal working hours e.g. rest days and public holidays

3. Reimbursement for travel from home/office to the place of assignment (not the normal place of work)

4. Reimbursement for actual transport expenses where the employer is obliged to provide transport for employees and where the transport is not available

work injury compensation

Payment to employees for injuries under the Work Injury Compensation Act. no

Source: http://mycpf.cpf.gov.sg/Employers/Employers_Guide_to_CPF/Existing_Employer/ee_Find_out_if_CPF_contributions_are_payable/ExistingEmployer_Find_out_if_CPF_con_payable_which_allowances_and_payments.htm

CEnTRAL PROVIDEnT FUnD (CPF)

© Copyright 2014 Stone Forest Accountserve Pte Ltd 59

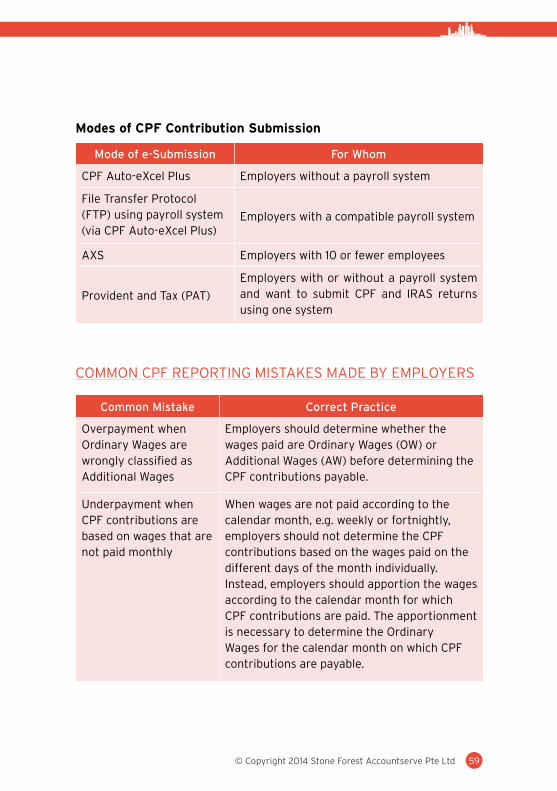

modes of CPf Contribution Submission

Mode of e-submission For whom

CPF Auto-eXcel Plus Employers without a payroll system

File Transfer Protocol (FTP) using payroll system (via CPF Auto-eXcel Plus)

Employers with a compatible payroll system

AXS Employers with 10 or fewer employees

Provident and Tax (PAT)

Employers with or without a payroll system and want to submit CPF and IRAS returns using one system

COMMOn CPF REPORTInG MISTAkES MADE BY EMPLOYERS

common Mistake correct Practice

Overpayment when Ordinary Wages are wrongly classified as Additional Wages

Employers should determine whether the wages paid are Ordinary Wages (OW) or Additional Wages (AW) before determining the CPF contributions payable.

Underpayment when CPF contributions are based on wages that are not paid monthly

When wages are not paid according to the calendar month, e.g. weekly or fortnightly, employers should not determine the CPF contributions based on the wages paid on the different days of the month individually.Instead, employers should apportion the wages according to the calendar month for which CPF contributions are paid. The apportionment is necessary to determine the Ordinary Wages for the calendar month on which CPF contributions are payable.

The HR Practitioners’ Guide to Key Employment Legislation60

common Mistake correct Practice

Underpayment/ Overpayment when wrong CPF contribution rates are applied

Employers should check the CPF contribution rates applicable for their employees before determining the CPF contributions payable, especially when:i. the employee’s total wage is less than

$1,500ii. the employee has crossed over to the next

age group

Underpayment/Overpayment when wrong CPF contribution rates for Singapore Permanent Residents are applied

Employers should check the date employees obtain their Singapore Permanent Resident (SPR) status at the point of employment before determining the CPF contributions payable.

The first-year rate is payable from the day the employee obtains his SPR status. The day he obtains the SPR status refers to the date indicated on the entry permit (Form 5/5A) that is issued by the Immigration and Checkpoints Authority of Singapore. The second- and third-year rates are payable from the month following the anniversary of the employee’s conversion to a SPR.

Overpayment when CPF contributions for Ordinary Wages (OW) are paid above the OW Ceiling

Employers should pay CPF contributions for Ordinary Wages (OW) up to the OW Ceiling of $5,000.

CEnTRAL PROVIDEnT FUnD (CPF)

© Copyright 2014 Stone Forest Accountserve Pte Ltd 61

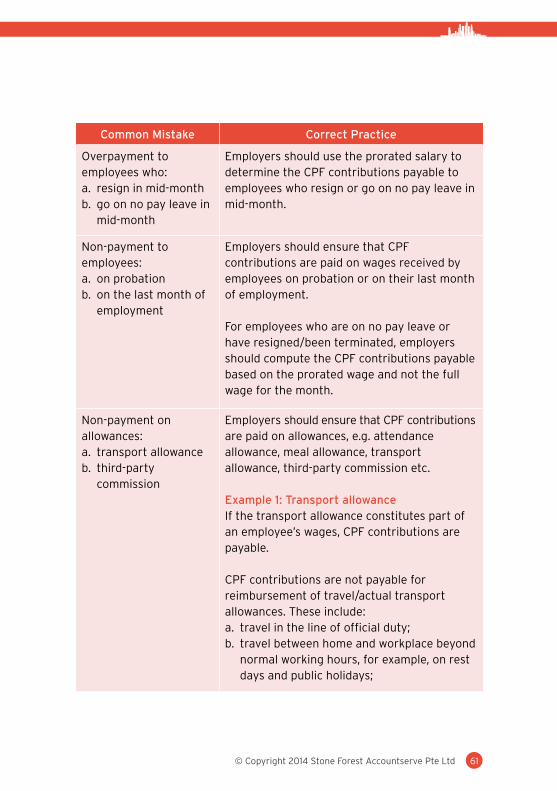

common Mistake correct Practice

Overpayment to employees who:a. resign in mid-monthb. go on no pay leave in

mid-month

Employers should use the prorated salary to determine the CPF contributions payable to employees who resign or go on no pay leave in mid-month.

non-payment to employees:a. on probationb. on the last month of

employment

Employers should ensure that CPF contributions are paid on wages received by employees on probation or on their last month of employment.

For employees who are on no pay leave or have resigned/been terminated, employers should compute the CPF contributions payable based on the prorated wage and not the full wage for the month.

non-payment on allowances:a. transport allowanceb. third-party

commission

Employers should ensure that CPF contributions are paid on allowances, e.g. attendance allowance, meal allowance, transport allowance, third-party commission etc.

Example 1: Transport allowanceIf the transport allowance constitutes part of an employee’s wages, CPF contributions are payable.

CPF contributions are not payable for reimbursement of travel/actual transport allowances. These include:a. travel in the line of official duty;b. travel between home and workplace beyond

normal working hours, for example, on rest days and public holidays;

The HR Practitioners’ Guide to Key Employment Legislation62

common Mistake correct Practice

c. travel from home/office to the place of assignment; and

d. actual transport expenses where the employer is obliged to provide transport and where transport is not available.

Example 2: Third-party commissionCPF contributions are payable on third-party commissions as long as the commissions are money for services rendered by the employee during his employment. Third-party commissions are commissions that an employee earns from third parties for services rendered by him by virtue of his employment.

Arrangement to pay commissions can be formal or informal and CPF contributions are payable on third-party commissions whether the employer earns a commission or whether such commissions are stated in the employment contract.

For instance, Ivan is a salesperson and has to recommend his customers to financial institutions listed by his employer for car insurance. For any insurance he sells, he would be paid a commission from the financial institution. CPF contributions are payable on such commissions.

CEnTRAL PROVIDEnT FUnD (CPF)

© Copyright 2014 Stone Forest Accountserve Pte Ltd 63

common Mistake correct Practice

non-payment for employees under a contract of service

Employers should ensure that CPF contributions are paid for all employees under a contract of service.

Example:Jill employs a part-time receptionist, who comes to work a few days each month. There is neither a written agreement nor a need to serve termination notice.

Jill has to pay CPF contributions for her temporary, part-time or permanent employees as long as there are wages due and payable to these employees.

Source: http://mycpf.cpf.gov.sg/Employers/Employers_Guide_to_CPF/Existing_Employer/determining+_CPF_con.htm

Effective from 1 January 2015

Employers to Face Higher cPF contribution RatesEmployers will face higher Medisave and older worker CPF contribution rates with effect from 1 January 2015, as announced in the FY2014 Budget Statement.

Employers’ CPF contribution rates to the Medisave Account will be raised by 1 percentage point. In addition, the CPF contribution rates for workers aged above 50 years to 65 years will also be increased. The overall impact of these increases for an employee’s monthly wage of $750 and above is shown in Table 1 on the next page:

new

The HR Practitioners’ Guide to Key Employment Legislation64

Table 1

age (years)

current Effective 1 Jan 2015

Employer’s

CPF

Employee’s

CPF

Total

CPF

Employer’s

CPF

Employee’s

CPF

Total

CPF

50 andbelow

16% 20% 36% 17% 20% 37%

Above50 – 55

14% 18.5% 32.5% 16% 19% 35%

Above55 – 60

10.5% 13% 23.5% 12% 13% 25%

Above60 – 65

7% 7.5% 14.5% 8.5% 7.5% 16%

Above65

6.5% 5% 11.5% 7.5% 5% 12.5%

CEnTRAL PROVIDEnT FUnD (CPF)

A Stone Forest CompanyPayrollServe ®

InternationalGlobally Connected

Details on

Next Page

PAYROLL & HR TRAINING

Legislation Updates

MS Excel for Payroll

Specialists

Advanced Payroll

Masterclass for HR

Professionals

Insights into HR in China

HR Masterclass for Business

Owners

A Stone Forest CompanyPayrollServe ®

InternationalGlobally Connected

For over 25 years, we have been delivering highly effective payroll services and training. Our unrivalled in-house team of expert payroll practitioners facilitates all workshops, backed by extensive practical experience in the payroll environment. Every single workshop is specially designed for specific roles: whether you are new to payroll, have been in the industry for years, keeping your skills up to date, or simply looking for a refresher course.

PayrollServe Academy provides a wide range of Payroll and HR-related training:■ Advanced Payroll Masterclass for HR Professionals■ HR Masterclass for Business Owners■ Latest Legislation Updates & Highlights■ Insights into HR in China − Today’s Challenges and Practices■ MS Excel for Payroll Specialists■ Individual Tax Filing Information Session■ Payroll Year-end Tax Returns Workshop

www.PayrollServe.com.sg

Or call us at +65 6336 0600

Learn More

PAYROLL & HR TRAINING

© Copyright 2014 Stone Forest Accountserve Pte Ltd 67

CHInESE DEVELOPMEnT ASSISTAnCE COUnCIL (CDAC) FUnD

All Chinese employees who are either citizens of Singapore or Singapore permanent residents may contribute monthly to the CDAC, according to the wage levels indicated below:

wage Level Monthly contribution

Less than $2,000 $0.50

$2,000 or more $1.00

SInGAPORE InDIAn DEVELOPMEnT ASSOCIATIOn (SInDA) FUnD

All working Indians except foreign workers on the FWL scheme in Singapore may contribute monthly to the SInDA Fund, according to the wage levels indicated below:

wage Level Monthly contribution

Up to $600 $1.00

Above $600 to $1,500 $3.00

Above $1,500 to $2,500 $5.00

Above $2,500 $7.00

MOSQUE BUILDInG AnD MEnDAkI FUnD (MBMF)

All working Muslim Singapore citizens, Singapore permanent residents and foreign workers are required to contribute to the MBMF monthly, according to the wage levels indicated on the next page:

STATUTORY DOnATIOnS

sTaTUTORy DOnaTiOns

The HR Practitioners’ Guide to Key Employment Legislation68

wage Level Monthly contribution

$200 and below nil

Above $200 to $1,000 $2.00

$1,001 to $2,000 $3.50

$2,001 to $3,000 $5.00

$3,001 to $4,000 $12.50

$4,001 and above $16.00

EURASIAn COMMUnITY FUnD (ECF)

All working Eurasian Singapore citizens and Singapore permanent residents may contribute to the ECF monthly, according to the wage levels indicated below:

wage Level Monthly contribution

Up to $1,000 $2.00

Above $1,000 to $1,500 $4.00

Above $1,500 to $2,500 $6.00

Above $2,500 to $4,000 $8.00

Above $4,000 $10.00

SHARE PROGRAMME DOnATIOnS

The CPF Board collects SHARE donations on behalf of the Community Chest, a division of the national Council of Social Service. Donations by the employees are voluntary and deducted from the employees’ wages.

STATUTORY DOnATIOnS

2-Day Seminar

InternationalGlobally Connected

A Stone Forest CompanyPayrollServe ® Academy

HR Masterclass for Business OwnersAligning Business Objectives with Employment Law Updates

The Ministry of Manpower has introduced significant changes to labour legislations in recent years. These changes mainly focus on employment standards and benefits, moderating the growth of foreign manpower, enhancing productivity and more importantly, ensuring that Singaporeans remain the core of our workforce.

Besides having a profound impact on the continued employment and management of people in various business sectors / industries, these changes also inevitably affect companies’ profit margins.

Our speaker, JANARTHANAN SELVARAJOO, is currently a HR Chief Consultant in private practice. He spent 11 years in the Ministry of Manpower (MOM) and his diverse portfolio includes that of Assistant Commissioner for Labour, Head of Labour Court, Director of Employment Inspectorate, and Deputy Controller of Work Permit.

Find out how employers can STAY COMPETITIVE AND COMPLIANT with employment law updates at the same time.

Details on

Next Page

Programme OutlineHR Masterclass for Business OwnersAligning Business Objectives with Employment Law Updates