sharpening our focus -...

TRANSCRIPT

Sharpening Our Focus

2

Forward-Looking Statements

We want to remind everyone that our comments may contain certain forward-looking statements that are inherently subject to uncertainties. We caution everyone to be guided in their analysis of Dover Corporation by referring to our Form 10-K for a list of factors that could cause our results to differ from those anticipated in any such forward-looking statement.

We would also direct your attention to our internet site, www.dovercorporation.com, where considerably more information can be found.

3

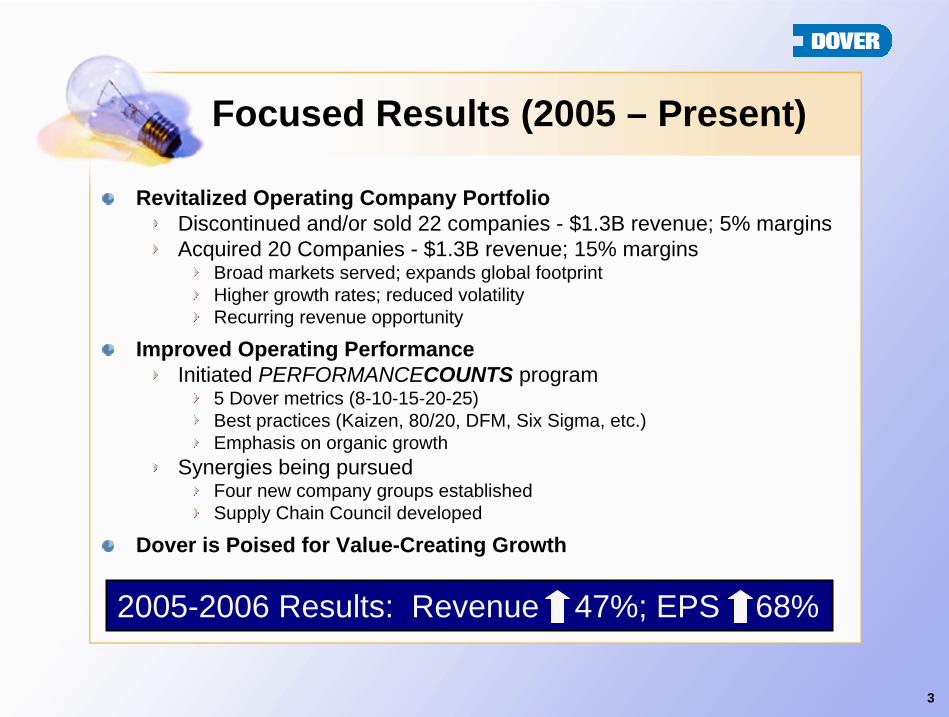

Focused Results (2005 – Present)

Revitalized Operating Company Portfolio Discontinued and/or sold 22 companies - $1.3B revenue; 5% marginsAcquired 20 Companies - $1.3B revenue; 15% margins

Broad markets served; expands global footprintHigher growth rates; reduced volatilityRecurring revenue opportunity

Improved Operating PerformanceInitiated PERFORMANCECOUNTS program

5 Dover metrics (8-10-15-20-25)Best practices (Kaizen, 80/20, DFM, Six Sigma, etc.)Emphasis on organic growth

Synergies being pursuedFour new company groups establishedSupply Chain Council developed

Dover is Poised for Value-Creating Growth

2005-2006 Results: Revenue 47%; EPS 68%

4

Sustainable Growth

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

2002 2003 2004 2005 2006

Rev

enue

$0

$100

$200

$300

$400

$500

$600

$700

Earn

ings

Revenue Earnings

5-YR REVENUE CAGR: 13.5% 5-YR EARNINGS CAGR: 24.2%

$ in millions

Results reflect continuing operations

5

Recent Successes

Expanding Our Growth PlatformsSuccessful acquisitions in Product ID, Material Handling and Electronic Technologies

Generating Strong Cash FlowGenerated $1.1B free cash flow (2005 – 2006)

9.6% of revenueDisciplined acquisition process in challenging marketFocus on capital allocation

$500M share repurchase in process52nd consecutive year of dividend increase

Driving Performance Through Shared Best PracticesKaizen, 80/20, DFM, Six Sigma, etc.

6

Double Digit EPS Growth

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Continuing Earnings Per Share

2004

$1.72

$2.12

$2.88

2005 20072006

YTD$1.49

7

Evolution of Our Structure

19551985

20042007

Direct ReportingDirect Reporting

Autonomous operating companies.

4 Subsidiaries4 Subsidiaries

Delegated oversight of companies to

Subsidiary CEO’s.

6 Subsidiaries6 Subsidiaries

Broadened management structure and deepened executive talent base.

4 Segments 4 Segments –– 6 Platforms6 Platforms• Organized into logical

business groupings. • Provides framework to

increase synergies.• Increases clarity for investors.

8

Our Previous Structure

.DIVERSIFIED RESOURCES

ELECTRONICS SYSTEMS

INDUSTRIES TECHNOLOGIES

9

Our New Structure

INDUSTRIALPRODUCTS

ENGINEEREDSYSTEMS

FLUIDMANAGEMENT

ELECTRONICTECHNOLOGIES

MaterialHandling

MobileEquipment

Product ID

EngineeredProducts

Energy

Fluid Solutions

10

New Segment Rationale

Match Organization to “New” PortfolioAlign similar businesses focused on broad end-

marketsDevelop platform management teams

Set strategic platform directionCoordinate best practices sharingAdditional acquisition capacitySupport for segment leaders

Expand executive opportunitiesCreate leaders of tomorrowDevelop deeper platform expertise

11

New Segment Rationale (continued)

Enhance Synergy OpportunitiesIdentify and capture synergiesExpand global sourcing/supply chain opportunitiesBuild leading market share positions

Leverage global operations expertise Focus on developing market trends

Focus Acquisition ProcessFocus investments on key platforms

Opportunistically pursue new platformsStrengthen position as “acquirer of choice”

12

Improve Clarity

Simplify Dover for InvestorsPrior subsidiary names had limited external meaningNew names convey end-market focus

Greater TransparencyMore meaningful data points to be reported“Pure play” platforms identified

Potential Catalyst for New InvestorsMakes analysis easierBusiness focus more intuitiveImproves market liquidity

13

New Reporting Segments

INDUSTRIALPRODUCTS

ENGINEEREDSYSTEMS

ELECTRONICTECHNOLOGIES

FLUIDMANAGEMENT

JUNE 2007 YTD REVENUE

14

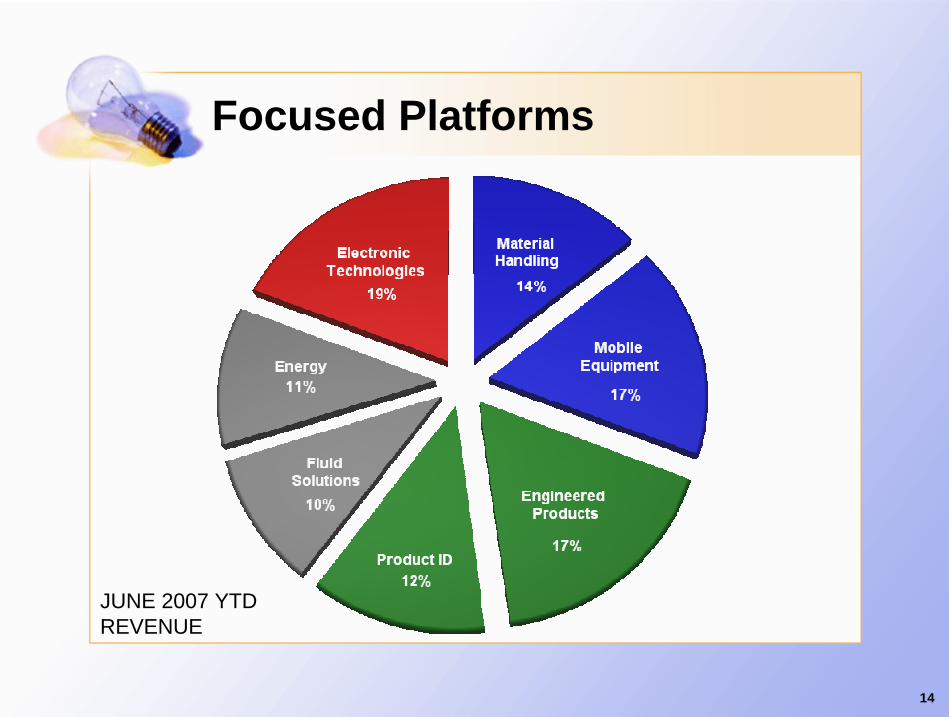

Focused Platforms

JUNE 2007 YTD REVENUE

15

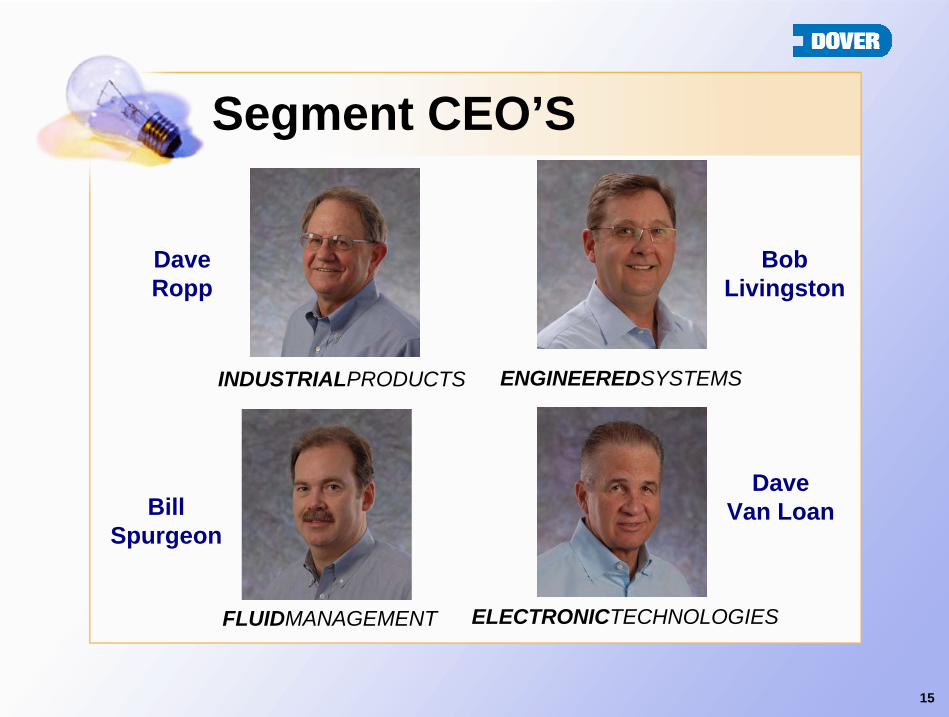

Segment CEO’S

INDUSTRIALPRODUCTS ENGINEEREDSYSTEMS

FLUIDMANAGEMENT ELECTRONICTECHNOLOGIES

Dave Ropp

Dave Van Loan

BobLivingston

Bill Spurgeon

16

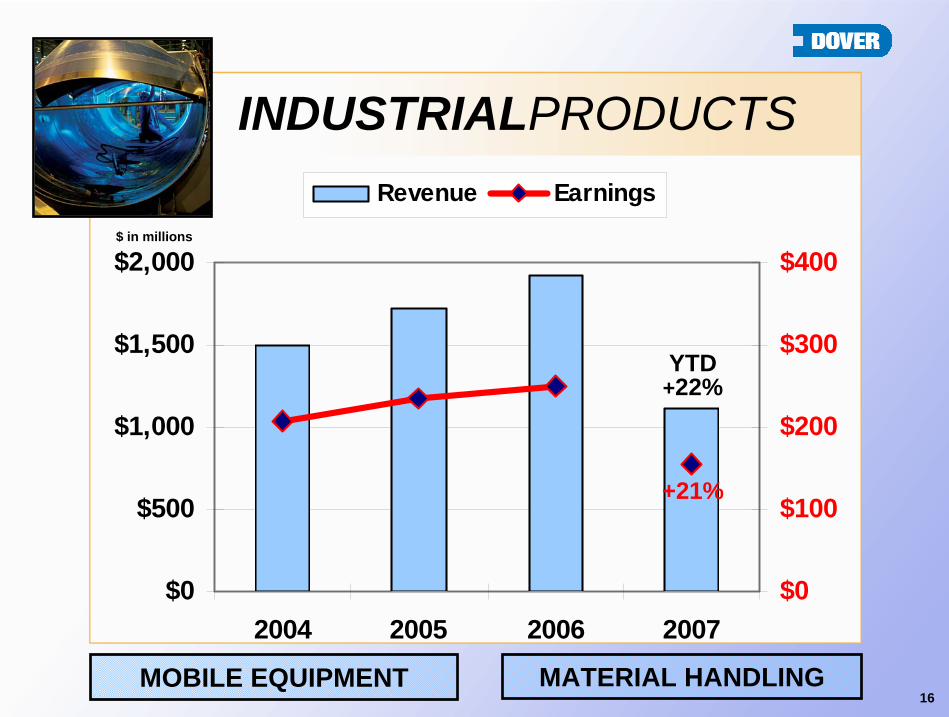

INDUSTRIALPRODUCTS

MOBILE EQUIPMENT MATERIAL HANDLING

$0

$500

$1,000

$1,500

$2,000

2004 2005 2006 2007$0

$100

$200

$300

$400

Revenue Earnings

YTD+22%

+21%

$ in millions

17

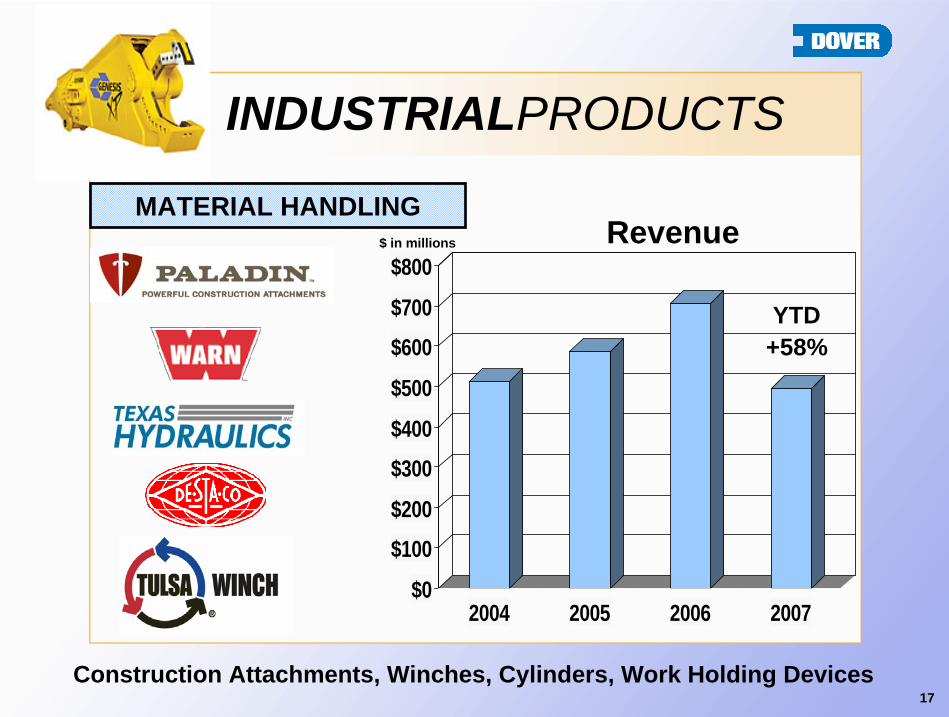

INDUSTRIALPRODUCTS

MATERIAL HANDLING

$0$100$200$300$400$500$600$700$800

2004 2005 2006 2007

Revenue

Construction Attachments, Winches, Cylinders, Work Holding Devices

+58%YTD

$ in millions

18

INDUSTRIALPRODUCTS

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

2004 2005 2006 2007

RevenueMOBILE EQUIPMENT

Refuse Equipment, Fuel/Bulk Trailers, Aerospace Components, Powersports Components, Automotive Aftermarket Equipment

+3%

$ in millions

YTD

19

ENGINEEREDSYSTEMS

PRODUCT IDENTIFICATION ENGINEERED PRODUCTS

$0

$400

$800

$1,200

$1,600

$2,000

2004 2005 2006 2007$0

$60

$120

$180

$240

$300

Revenue Earnings

YTD+29%

+4%

$ in millions

20

ENGINEEREDSYSTEMS

PRODUCT IDENTIFICATION

$0

$100

$200

$300

$400

$500

$600

2004 2005 2006 2007

Revenue

Product Marking Equipment, Stationary and Portable Printers and related consumables

+71%

$ in millions

YTD

21

ENGINEERED PRODUCTS

$0

$200

$400

$600

$800

$1,000

$1,200

2004 2005 2006 2007

Revenue

Refrigerated Display Cases, Heat Exchangers, Food Equipment, ATM’s

ENGINEEREDSYSTEMS

+10%

$ in millions

YTD

22

FLUIDMANAGEMENT

ENERGY FLUID SOLUTIONS

$0

$300

$600

$900

$1,200

$1,500

2004 2005 2006 2007$0

$60

$120

$180

$240

$300

Revenue Earnings

YTD+12%

+10%

$ in millions

23

ENERGY

$0

$100

$200

$300

$400

$500

$600

$700

2004 2005 2006 2007

Revenue

Oilfield Drill Bit Inserts, Sensors, Sucker Rods, Gas Compression, Specialty Bearings

FLUIDMANAGEMENT

+17%

$ in millions

YTD

24

FLUID SOLUTIONS

$0

$100

$200

$300

$400

$500

$600

$700

2004 2005 2006 2007

Revenue

Service Station Equipment, Hydraulic Pumps and Valves, Dispensing Equipment

FLUIDMANAGEMENT

+8%

$ in millions

YTD

25

ELECTRONICTECHNOLOGIES

$0

$300

$600

$900

$1,200

$1,500

2004 2005 2006 2007$0

$60

$120

$180

$240

$300

Revenue Earnings

YTD-5%

-24%

$ in millions

26

$0

$300

$600

$900

$1,200

$1,500

2004 2005 2006 2007

Bookings

Acoustic, Microwave, Ceramic, Frequency Control Components; Electronic Test, Material Deposition and Soldering Tools

ELECTRONICTECHNOLOGIES

-11%YTD

$ in millions

27

Public Disclosure

Segment (Quarterly & Annual)Revenue, earnings, bookings, backlog , operating marginsGrowth components: organic, acquisitions, currency

Platform (Quarterly & Annual)Revenue, bookings, backlogComparative earnings trends

High Level Qualitative CommentaryAcquisition and Divestiture Activity

INDUSTRIALPRODUCTS ENGINEEREDSYSTEMS FLUIDMANAGEMENT ELECTRONICTECHNOLOGIES

28

Sharpening Our FocusNew Organizational Structure Will Make a Difference

Operational improvementsFacilitates expanded synergies & best practicesFocuses acquisition activityExpanded oversight provides advancement opportunitiesProvides clarity and simplifies Dover for investors

Performance improvementsPERFORMANCECOUNTS is driving world-class improvements

Unique Culture Will be RetainedSource of competitive advantageAllow experts to run their business

Synergistic Activities Expected to Improve Operational Earnings 4% - 6% Over Two-Year Period

29

Refining Our Structure to Refining Our Structure to Enhance Our PerformanceEnhance Our Performance