shai even - content.equisolve.net

TRANSCRIPT

Shai Even

Senior Vice President & Chief Financial Officer

Citi 2015 MLP/Midstream Infrastructure Conference – August 2015

Forward-Looking Statements

2

All statements contained in or made in connection with this presentation that are not statements of historicalfact are forward-looking statements intended to be covered by the safe harbor provisions of the Securities Actof 1933 or the Securities Exchange Act of 1934. The words “believe”, “intend”, “plan”, “expect”, “should”,“estimate”, “anticipate”, “potential”, “future”, “will” and similar terms and phrases identify forward-lookingstatements. Forward-looking statements reflect the current expectations of the management of Alon USAPartners, LP (“Alon”) regarding future events, results or outcomes. These expectations may or may not berealized and actual results could differ materially from those projected in forward-looking statements. Alon’sbusinesses and operations involve numerous risks and uncertainties, many of which are beyond our control,which could result in the expectations reflected in forward-looking statements not being realized or which mayotherwise affect Alon’s financial condition, results of operations and cash flows. These risks and uncertaintiesinclude, among other things, changes in price or demand for our products; changes in the availability or cost ofcrude oil and other feedstocks; changes in market conditions; actions by governments, competitors, suppliersand customers; operating hazards, natural disasters or other disruptions at our or third-party facilities; and thecosts and effects of compliance with current and future state and federal regulations. For more informationconcerning factors that could cause actual results to differ from those expressed in forward-looking statements,see Alon’s most recently filed Form 10-Q which has been filed with the Securities and Exchange Commissionand is available on the company’s web site at www.alonpartners.com. Alon undertakes no obligation to updateor publicly release the results of any revisions to any forward-looking statements that may be made to reflectevents or circumstances that occur, or that we become aware of, after the date of this presentation or to reflectthe occurrence of unanticipated events.

Alon USA Energy Overview

Alon USA Energy, Inc. (NYSE: ALJ) owns 81.6% of the limited partner interests in Alon USA Partners, LP (NYSE: ALDW), a variable distribution MLP, which owns an oil refinery in Big Spring, TX. Alon USA Energy is composed of three segments: refining and marketing, asphalt and retail.

Corporate Structure Alon USA Energy Asset Base

3

100% GP81.6% LP

Alon USA Partners Overview

4

The 73,000 bpd Big Spring refinery processes oil from the Permian Basin into finished products such as gasoline, diesel, jet fuel and petrochemicals, which are marketed primarily in West Texas, Central Texas, Oklahoma, New Mexico and Arizona through its wholesale distribution network to both Alon USA Energy’s

retail convenience stores and other third-party distributors.

Our Strategic Advantages

» Strategically located refinery in the heart of the prolific Permian Basin

» High quality asset with low operating costs

» Physically integrated refining and marketing system

» Strong liquidity position and flexibility provided by supply & offtakeagreement at the refinery

» Focus on operational excellence and organic growth opportunities

5

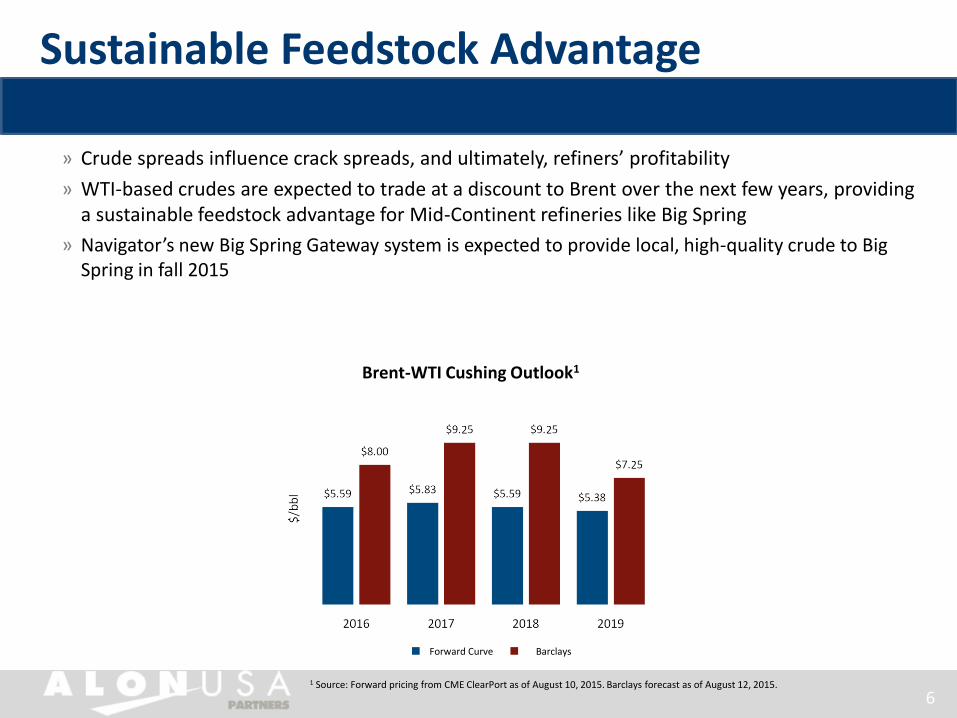

» Crude spreads influence crack spreads, and ultimately, refiners’ profitability

» WTI-based crudes are expected to trade at a discount to Brent over the next few years, providing a sustainable feedstock advantage for Mid-Continent refineries like Big Spring

» Navigator’s new Big Spring Gateway system is expected to provide local, high-quality crude to Big Spring in fall 2015

Brent-WTI Cushing Outlook1

1 Source: Forward pricing from CME ClearPort as of August 10, 2015. Barclays forecast as of August 12, 2015.

Sustainable Feedstock Advantage

n Forward Curve n Barclays

6

1 Source: Baker Hughes, RigData; Rig map as of August 7, 20152 Source: EIA Drilling Productivity Report August 20153 Source: Simmons & Company; Tudor, Pickering, Holt & Company; Raymond James Research

Texas Permian Basin Activity Overview 1

Oil Rig

Big Spring: In the Heart of the Permian Basin

» Several rigs concentrated in the proximity of the refinery

» Permian rig count has increased by 23 rigs since bottoming in late June 2015; rig count has risen to 254 rigs as of August 7, 20151

» Permian oil production still increasing; EIA forecasts a small sequential increase in September production2

» The Permian has been the most resilient of the major U.S. oil shale plays

Permian Oil Production Outlook3

7

1,710 1,726

1,900

2,167

2,491

2,844

1,628

1,815 1,848

2,199

2,606

2,910 3,026

1,771

1,977 2,163

1,000

1,500

2,000

2,500

3,000

3,500

2014 2015 2016 2017 2018 2019 2020

TPH Raymond James Simmons

MB

pd

66,03367,10368,946 73,934

Big Spring Refinery Overview

Refinery Operating Margin1

Refinery Throughput (bpd)1Refinery Product Yield1,2

n Big Spring Operating Margin – – – Gulf Coast 321 Crack Spread

n WTS crude n WTI crude n Blendstocksn Gasoline n Diesel/jet n Asphalt n Other

1 Refinery Operating Margin, Refinery Throughput and Refinery Product Yield for 2014 were negatively impacted by the major turnaround at Big Spring in 2Q 2014. Pro forma for the turnaround in 2Q 2014, Adjusted EBITDA would be higher by $55-65 million.2 Product yield percentages based on total production. Liquid recovery shown at top of column. Some numbers may not add due to rounding.

» Big Spring refinery:

› 73,000 bpd (~26 MMbbl/year) sour crude cracking refinery

› 10.5 Nelson Complexity

› Processes 100% Midland-priced crude

» Integrated wholesale fuels marketing business supplies ~640 branded sites, including substantially all of Alon’s retail sites

› In 2014, Alon’s retail gasoline and diesel sales represented 27% and 8%, respectively, of Big Spring’s gasoline and diesel production

8

How Big Spring Made Money – 1H 2015

1 Some numbers may not add due to rounding. “Other” includes costs relating to RINs, pipeline fees, supply related costs and other raw materials purchased at the refinery.

Chart is not to scale. Chart reflects liquid recovery of 100.4%.

Product Yields Crude / Blendstocks Refining Operating Margin1

9

» Big Spring achieved low operating expense of $3.56 per barrel in 1H 2015

Per bbl Per bbl Per bbl

Gasoline

10.08$ $20.16

Gasoline Sour

50.0% Crude

50.3%

Jet

$19.72

Jet

5.1%

Diesel

$23.36

Diesel Sweet

31.5% Crude

45.9% (2.28)$ Wholesale & Other ($0.35)

Asphalt

3.9% Asphalt

Other (15.65)$

9.9% Blendstock

3.8%

$69.43 $51.48 $15.56

$71.86

$71.43

$75.07

$36.06

$51.35

1.01$

7.36$

(0.61)$

Highly Efficient Operations – Solomon Results

Source: Solomon Associates. 1 Rank is out of 14 refineries with kEDC of 800 – 1,399. Big Spring’s kEDC is 819. 2 Rank is out of 10 refineries in the Lower Mid-Continent.Survey conducted every other year.

U.S.

84 refineries

Capacity Peer Group1

14 refineries

Regional Peer Group2

10 refineries

Mechanical Availability 0 0 0

Net Cash Margin (Rack Pricing) 2 15 0

Maintenance Cost Efficiency 32 26 10

2014 Solomon Percent Rankings (0 Represents Best)

Maintenance Cost Efficiency

Mechanical Availability

Net Cash Margin (Rack Pricing)

» Big Spring led U.S. Solomon Survey participants in mechanical availability in 2014 and led its regional peer group in net cash margin

10

2010 2012 2014

Q-1

Q-2

Q-3

Q-4

BSR

2010 2012 2014

Q-1

Q-2

Q-3

Q-4

BSR

2010 2012 2014

Q-4

Q-3

Q-2

Q-1

BSR

Integrated Wholesale Marketing

Legend:

Branded license agreement and payment card location

Branded company-operated and distributor location

Unbranded supply available

Wichita Falls

Tucson

Phoenix

Abilene

El Paso Big Spring

» Integrated wholesale fuels marketing business supplies ~640 branded sites, including substantially all of Alon’s retail sites

» In 2014, approximately 85% of gasoline and over 90% of diesel produced at Big Spring was transferred to our wholesale business, including branded and unbranded marketing

» In 2014, wholesale gasoline and diesel sales volumes totaled 819 million gallons, including volumes sold to Alon USA’s retail locations

» Entered premium Phoenix market in 2Q 2015

› Sold ~6,000 bpd in the premium Arizona market (Phoenix and Tucson) in June 2015

› Capture additional RINs with Arizona sales – another benefit of selling into Arizona instead of the Group

11

Business Opportunities

» Capitalizing on crude slate flexibility by running lowest cost inputs / highest margin outputs

» Continuing to evaluate low-risk projects to enhance gross margin with payback periods of less than two years; projects focused on LPG recovery, increased aromatics recovery, producing chemical-grade propylene

» Leveraging integrated wholesale marketing business to expand product deliveries in Texas and Arizona

» Evaluating project to increase refinery’s ability to process WTI Midland

» Evaluating potential for significant expansion of the refinery

» Looking at alternatives to unlock value from existing logistics assets

12

Guidance and RINs Information

13

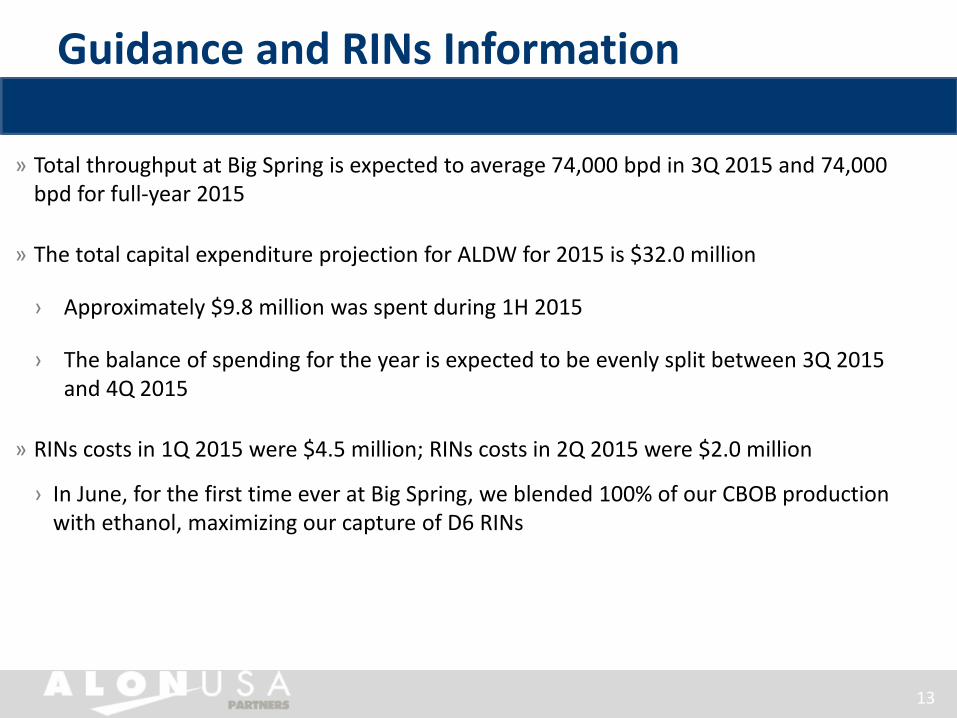

» Total throughput at Big Spring is expected to average 74,000 bpd in 3Q 2015 and 74,000 bpd for full-year 2015

» The total capital expenditure projection for ALDW for 2015 is $32.0 million

› Approximately $9.8 million was spent during 1H 2015

› The balance of spending for the year is expected to be evenly split between 3Q 2015 and 4Q 2015

» RINs costs in 1Q 2015 were $4.5 million; RINs costs in 2Q 2015 were $2.0 million

› In June, for the first time ever at Big Spring, we blended 100% of our CBOB production with ethanol, maximizing our capture of D6 RINs

Crude Differentials & Crack Spread Trends

¹ 5 Year Average of 2010 to 2014* All crude differentials above are based on trade-month pricing, except Brent- WTI Cushing 14

» The Gulf Coast 3-2-1 crack spread averaged $24.46 per barrel in July 2015

Brent

West Texas

Intermediate - Cushing

("WTI")

West Texas Sour ("WTS") WTI Midland

WTI 5 Year Average¹--$91.94

2014 ---$93.10 YTD 2015 ---$53.20 Q2 2015---$57.86

GC321 5 Year Average --$18.54

2014 ---$14.52 YTD 2015 ---$18.73Q2 2015---$19.71

GC321(Brent) 5 Year Average --$8.22

2014 ---$8.36 YTD 2015 ---$14.19Q2 2015---$16.05

WTI Cushing - WTS 5 Year Average --$3.63

2014 ---$6.04 YTD 2015 ---$0.76Q2 2015 ---$(0.21)

WTI Cushing - WTI Midland 5 Year Average --$2.63

2014 ---$6.93 YTD 2015 ---$1.27 Q2 2015 ---$0.60

Brent - WTI Cushing 5 Year Average --$10.32

2014 ---$6.16 YTD 2015 ---$4.54Q2 2015 ---$3.66

Financial Summary

15

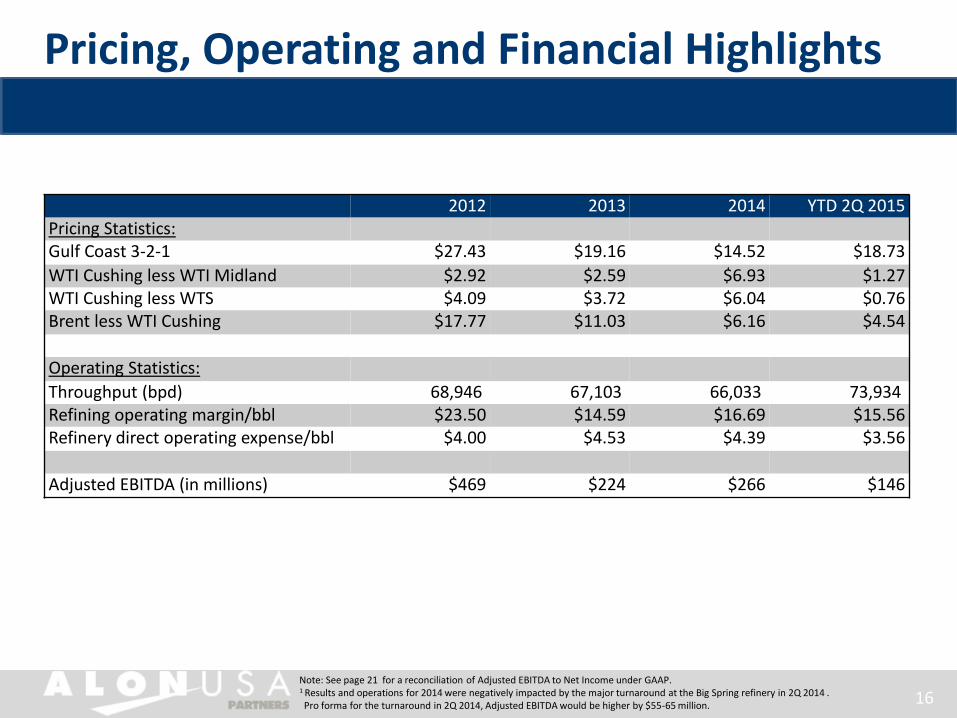

Pricing, Operating and Financial Highlights

Note: See page 21 for a reconciliation of Adjusted EBITDA to Net Income under GAAP.1 Results and operations for 2014 were negatively impacted by the major turnaround at the Big Spring refinery in 2Q 2014 .Pro forma for the turnaround in 2Q 2014, Adjusted EBITDA would be higher by $55-65 million. 16

2012 2013 2014 YTD 2Q 2015Pricing Statistics:Gulf Coast 3-2-1 $27.43 $19.16 $14.52 $18.73

WTI Cushing less WTI Midland $2.92 $2.59 $6.93 $1.27WTI Cushing less WTS $4.09 $3.72 $6.04 $0.76Brent less WTI Cushing $17.77 $11.03 $6.16 $4.54

Operating Statistics:

Throughput (bpd) 68,946 67,103 66,033 73,934Refining operating margin/bbl $23.50 $14.59 $16.69 $15.56Refinery direct operating expense/bbl $4.00 $4.53 $4.39 $3.56

Adjusted EBITDA (in millions) $469 $224 $266 $146

Distributions 2014 - Current

171 Results for 2Q 2014 were negatively impacted by the major turnaround at the Big Spring refinery. Pro forma for the turnaround in 2Q 2014, Adjusted EBITDA would be higher by $55-65 million.

(dollars in thousands, except per unit data) 1Q 2014 2Q 20141 3Q 2014 4Q 2014 1Q 2015 2Q 2015

Net income 42,241 7,802 76,993 42,099 36,451 59,426

Interest expense 11,324 11,569 11,584 12,229 11,693 10,847

State income tax expense (benefit) 485 240 1,060 999 350 (395)

Depreciation and amortization 10,067 9,508 13,852 14,067 13,993 13,591

Adjusted EBITDA 64,117 29,119 103,489 69,394 62,487 83,469

less: Maintenance/growth capital expenditures 4,162 7,277 2,492 2,133 2,321 5,465

less: Major and non-major turnaround and catalyst replacement capital expenditures 14,465 10,982 23,703 9,586 1,484 520

add: Major turnaround and catalyst replacement capital expenditures previously reserved (11,989) (11,011) — — — —

less: Major turnaround reserve for future years 1,150 1,500 1,500 1,500 1,500 1,500

less: Principal payments 625 625 625 625 625 625

less: State income tax expense 485 240 1,060 342 350 341

less: Interest paid in cash 12,097 11,106 10,542 11,203 11,539 10,236

Cash available for distribution $ 43,122 $ 8,400 $ 63,567 $ 44,005 $ 44,668 $ 64,782

Common units outstanding (in 000’s) 62,502 62,507 62,507 62,507 62,507 62,510

Cash available for distribution per unit $ 0.69 $ 0.13 $ 1.02 $ 0.70 $ 0.71 $ 1.04

Balance Sheet

18

(In $000's) June 30, December 31,

(2015 INFORMATION IS UNAUDITED) 2015 2014

ASSETS

Current assets:

Cash and cash equivalents $ 149,884 $ 106,325

Accounts and other receivables, net 81,842 68,545

Accounts and other receivables, net - related parties 11,888 9,466

Inventories 43,189 45,162

Prepaid expenses and other current assets 8,256 9,163

Total current assets 295,059 238,661

Property, plant, and equipment, net 436,407 445,706

Other assets, net 76,291 85,879

Total assets $ 807,757 $ 770,246

LIABILITIES AND PARTNERS’ EQUITY

Current liabilities:

Accounts payable $ 252,862 $ 186,156

Accrued liabilities 39,531 54,566

Current portion of long-term debt 2,500 2,500

Total current liabilities 294,893 243,222

Other non-current liabilities 37,779 38,746

Long-term debt 278,920 299,876

Total liabilities 611,592 581,844

Common unitholders - 62,510,039 and 62,506,550 units issued and outstanding at June 30, 2015 and December 31, 2014, respectively 196,165 188,402

Total partners’ equity 196,165 188,402

Total liabilities and partners' equity $ 807,757 $ 770,246

Statement of Operations

19

(In $000's, except per unit data) For the Six Months Ended

(ALL INFORMATION IS UNAUDITED) June 30, 2015 June 30, 2014

STATEMENT OF OPERATIONS DATA:

Net sales $ 1,167,506 $ 1,582,312

Operating costs and expenses:

Cost of sales 957,717 1,424,444

Direct operating expenses 47,701 54,093

Selling, general and administrative 16,118 11,152

Depreciation and amortization 27,584 19,575

Total operating costs and expenses 1,049,120 1,509,264

Operating income 118,386 73,048

Interest expense (22,540) (22,893)

Other income (loss), net (14) 613

Income before income tax expense (benefit) 95,832 50,768

State income tax expense (benefit) (45) 725

Net Income 95,877 50,043

Earnings per unit $ 1.53 $ 0.80

Weighted average common units outstanding (in thousands) 62,508 62,504

Cash distribution per unit $ 1.41 $ 0.87

Statement of Cash Flows

20

(In $000's) For the Six Months Ended(ALL INFORMATION IS UNAUDITED) June 30, 2015 June 30, 2014Cash flows from operating activities:Net income $ 95,877 $ 50,043Adjustments to reconcile net income to cash provided by operating activities:

Depreciation and amortization 27,584 19,575Unit-based compensation 20 —Deffered income taxes (736) —Amortization of debt issuance costs 1,098 1,018Amortization of original issuance discount 294 272

Changes in operating assets and liabilities:Accounts and other receivables, net (13,297) 37,608Accounts and other receivables, net - related parties (2,422) (1,021)Inventories 1,973 (21,300)Prepaid expenses and other current assets 907 (11,033)Other assets, net 1,500 (1,053)Accounts payable 36,571 (26,977)Accrued liabilities (14,740) (10,959)Other non-current liabilities (231) 9,059

Net cash provided by operating activities 134,398 45,232Cash flows from investing activities:

Capital expenditures (7,786) (11,439)

Capital expenditures for turnarounds and catalysts (2,004) (25,447)Net cash used in investing activities (9,790) (36,886)

Cash flows from financing activities:Revolving credit facility, net (20,000) —Distributions paid to unitholders – Alon Energy (71,910) (44,370)Distributions paid to unitholders (16,224) (10,010)Inventory agreement transactions 30,135 (25,200)Payments on long-term debt (1,250) (1,250)Deferred debt issuance costs (1,800) —

Net cash used in financing activities (81,049) (80,830)Net increase (decrease) in cash and cash equivalents 43,559 (72,484)Cash and cash equivalents, beginning of period 106,325 153,583Cash and cash equivalents, end of period $ 149,884 $ 81,099

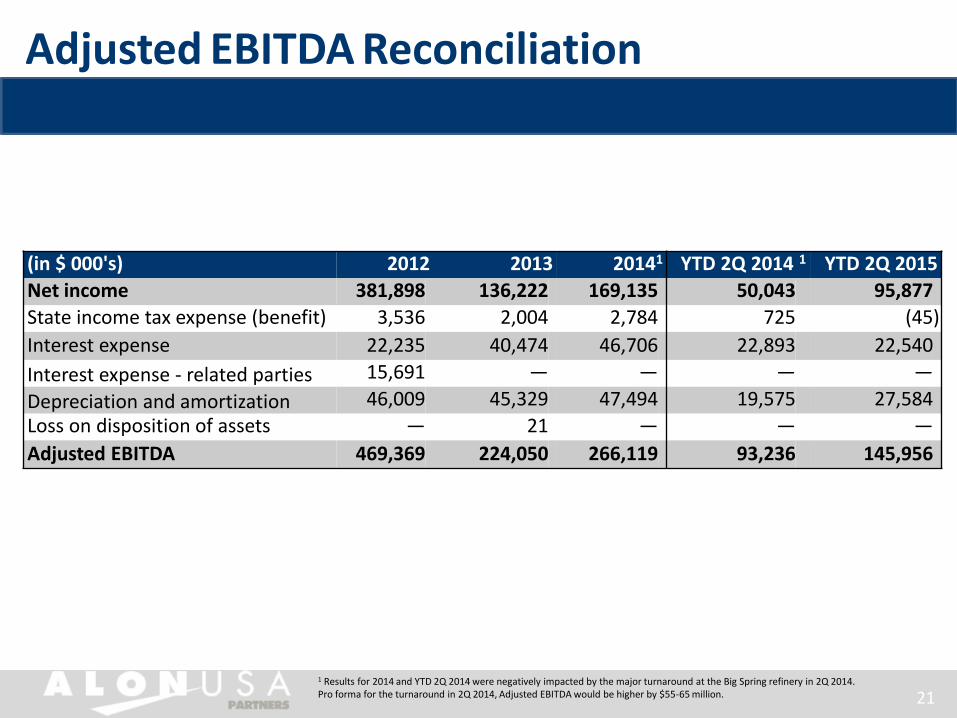

Adjusted EBITDA Reconciliation

1 Results for 2014 and YTD 2Q 2014 were negatively impacted by the major turnaround at the Big Spring refinery in 2Q 2014. Pro forma for the turnaround in 2Q 2014, Adjusted EBITDA would be higher by $55-65 million. 21

(in $ 000's) 2012 2013 20141 YTD 2Q 2014 1 YTD 2Q 2015

Net income 381,898 136,222 169,135 50,043 95,877

State income tax expense (benefit) 3,536 2,004 2,784 725 (45)

Interest expense 22,235 40,474 46,706 22,893 22,540

Interest expense - related parties 15,691 — — — —

Depreciation and amortization 46,009 45,329 47,494 19,575 27,584

Loss on disposition of assets — 21 — — —

Adjusted EBITDA 469,369 224,050 266,119 93,236 145,956

Appendix – Alon USA Energy

22

23

Krotz Springs Refinery Overview

» 74,000 bpd sweet crude residual cracking refinery

» 8.3 Nelson Complexity

» Historically processed a mix of LLS and HLS type crudes

» Transporting 30,000 bpd of WTI Midland-priced crude through the AMDEL pipeline to process at KrotzSprings

» High liquid recovery of approximately 102%

» One of the newest refineries in the U.S. (1980)¹ with industry low operating costs

» High distillate yield capability of over 40%

» Evaluating several growth projects, including adding an alkylation unit

¹ Source: EIA2 Product yield percentages based on total production. Liquid recovery shown at top of column. Some numbers may not add due to rounding.

Refinery Operating Margin

Refinery Throughput (bpd)

Refinery Product Yield2n WTI crude n Gulf Coast Sweet Crude n Blendstocks

n Gasoline n Diesel/jet n Other

67,877 64,705 70,345 74,745

n Krotz Springs Operating Margin – – – Gulf Coast 211 (LLS) Crack Spread

24

How Krotz Springs Made Money – 1H 2015

Product Yields Crude / Blendstocks Refining Operating Margin1

1 Some numbers may not add due to rounding. “Other” includes costs relating to RINs, pipeline fees, supply related costs and other raw materials purchased at the refinery.

Charts are not to scale. Chart reflects liquid recovery of 102.2%.

» Krotz Springs achieved low operating expense of $3.64 per barrel in 1H 2015

Per bbl Per bbl Per bbl

Gasoline $11.74

WTI

Gasoline 40.0%

46.9%

Jet

$13.43

Jet Diesel

20.7% $9.74

Light Sweet

Diesel Crude

21.5% 55.0% Other

($19.78)

Other

13.1% Blendstock 5.0%

$65.69 $56.81 $8.71

$69.80

$71.49

$67.81

$38.29

5.50$

2.79$

2.10$

(1.68)$

25

Physically Integrated Retail Network

» Largest 7-Eleven licensee in the U.S. with 294 stores (~50% fee owned) in Central/West Texas and New Mexico1

» Remodel program continues to progress

» Expanding store count through purchase of 14 retail gas stations in Albuquerque (not included in table)

» In 2014, Alon’s retail gasoline and diesel sales represented 27% and 8%, respectively, of Big Spring’s gasoline and diesel production

» Record operating results, fuel volumes and merchandise sales in 2014

Locations in High Growth Markets1

Location Total

Big Spring, Texas 7

Wichita Falls, Texas 11

Waco, Texas 9

Midland, Texas 17

Lubbock, Texas 21

Albuquerque, New Mexico 24

Odessa, Texas 35

Abilene, Texas 40

El Paso, Texas 82

Other locations in Central and West Texas 48

Total Stores 294

1 Store count does not include 14 stores in Albuquerque that were purchased in August 2015.

New Large-Format Store Opened in Rio Rancho, NM in May 2015

26

Improving the Asphalt Business

» In 2014, U.S. asphalt demand was down 40% from the peak in 2005; PADD V demand was down 52% from 20051

» Asphalt demand is largely driven by federal, state and local spending

» The country’s highways and bridges require capital investment of $120 billion annually over six years to meet current demand, but only $83 billion is currently being invested2

» Underinvestment in infrastructure is driving pent-up demand that will eventually spur a recovery

Steps Alon is taking to improve profitability:

» Focusing on premium products with better margins (recycled ground tire rubber blends)

» Working with suppliers to improve sourcing

» Right-sizing terminal system and leased railcar fleet

» Targeting $12 million reduction in direct operating costs in 2015 vs. 2014

Alon is positioned well when asphalt demand inevitably recovers1 Source: EIA2 Source: The American Association of State Highway and Transportation Officials and the American Public Transportation Association’s “2015 Bottom Line Report”

Krotz Springs

Phoenix

Elk Grove

(Sacramento)Bakersfield

Mojave

Fernley

(Reno)

Paramount /

Long Beach

Big Spring

Richmond Beach

(Seattle)

Refineries

Asphalt terminals

Legend

Flagstaff

27

Key Financial Metrics – Alon USA Energy

Adjusted EBITDA1

» Increase in capital expenditures in 2014 and 2015 relates to the turnaround and vacuum tower project at Big Spring in 2Q 2014 and the planned turnaround at Krotz Springs in 4Q 2015

» Alon has low sustaining capex requirements –Big Spring and Krotz Springs combined require ~$50 million in sustaining and regulatory spending and ~$20 million for turnarounds annually

$ m

illio

ns

Capital Expenditures & Turnarounds

1 See page 28 for a reconciliation of Adjusted EBITDA to Net Income under GAAP. Pro forma for the turnaround in 2Q2014, 2014 Adjusted EBITDA would be higher by $55-65 million.

$ m

illio

ns

Net Leverage (Net Debt/Adjusted EBITDA)2

$ m

illio

ns

28

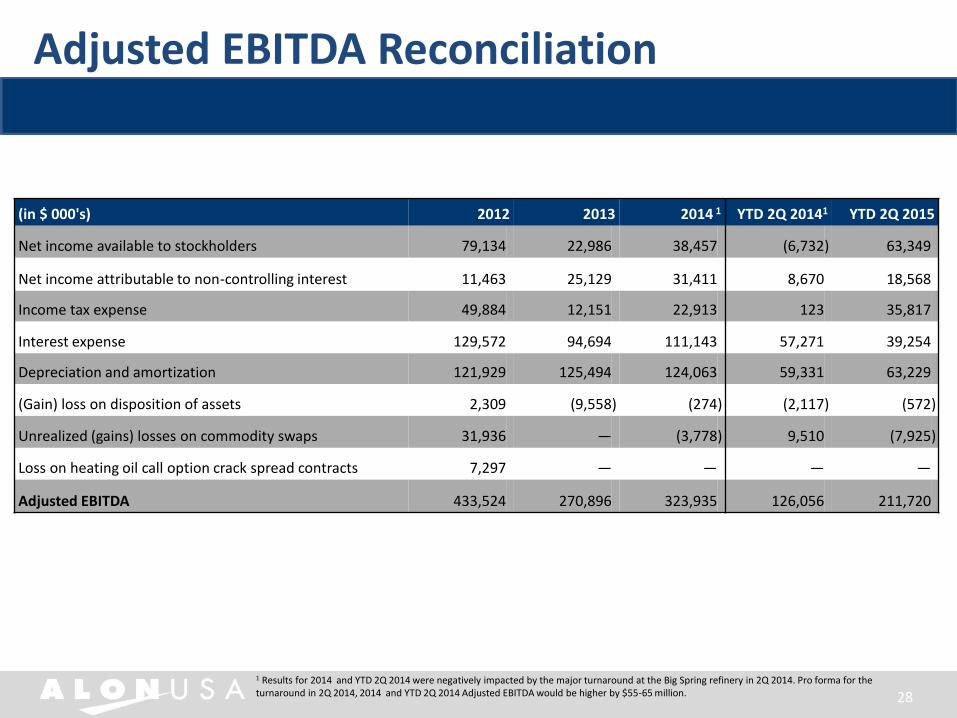

Adjusted EBITDA Reconciliation

1 Results for 2014 and YTD 2Q 2014 were negatively impacted by the major turnaround at the Big Spring refinery in 2Q 2014. Pro forma for the turnaround in 2Q 2014, 2014 and YTD 2Q 2014 Adjusted EBITDA would be higher by $55-65 million.

(in $ 000's) 2012 2013 2014 1 YTD 2Q 20141 YTD 2Q 2015

Net income available to stockholders 79,134 22,986 38,457 (6,732) 63,349

Net income attributable to non-controlling interest 11,463 25,129 31,411 8,670 18,568

Income tax expense 49,884 12,151 22,913 123 35,817

Interest expense 129,572 94,694 111,143 57,271 39,254

Depreciation and amortization 121,929 125,494 124,063 59,331 63,229

(Gain) loss on disposition of assets 2,309 (9,558) (274) (2,117) (572)

Unrealized (gains) losses on commodity swaps 31,936 — (3,778) 9,510 (7,925)

Loss on heating oil call option crack spread contracts 7,297 — — — —

Adjusted EBITDA 433,524 270,896 323,935 126,056 211,720