secrets of profitable cloud resellers

TRANSCRIPT

CAPTURING THE SMB CLOUD

OPPORTUNITY AND

UNCOVERING SECRETS FOR

PARTNER PROFITABILITY

AMI-Partners546 Fifth Avenue, New York

New York, Houston, Singapore, Bangalore, Kolkata, London, Tokyo

www.ami-partners.com

Source: AMI-Partners (www.ami-partners.com) 2014

AMI Background

Capturing the SMB Cloud Opportunity

Benchmarking Against Best-in-Class Cloud Partners

Q&A

2

Agenda

Source: AMI-Partners (www.ami-partners.com) 2014 3

Actionable Global Market Intelligence, GTM Strategy & Implementation Support- 18+ Year History -

AMI Tracking Surveys Cover Countries Driving over 90% of WW SMB IT/Telecom Spending

(SB = 1-99 Employees, MB = 100-999 Employees)

SMB End User Tracking

Channel Partner Tracking

Global IT/Telecom Market Sizing

Actionable Market Segmentation Model & Predictive Analytics

Go-to-Market Consulting

Strong Global Presence Across Americas, Europe & APAC

AMI: Extensive Global Footprint

Source: AMI-Partners (www.ami-partners.com) 2014

We must understand SMBs’ needs, mindsets, and challenges:

Internal Constraints: Managing Cash flow, Talent/HR, Weak Economy

External Environment: Pricing/Competitive Issues, Response Time, Savvier Customers

Key IT Purchase Drivers: Affordable, Simplicity, Productivity, High Performing, Ensure Customer Loyalty

Position our solutions and messaging to address SMBs’ needs and challenges.

How Can We Capture the SMB

Opportunity?

SMB = Companies with 1-999 employees

Source: AMI-Partners (www.ami-partners.com) 2014

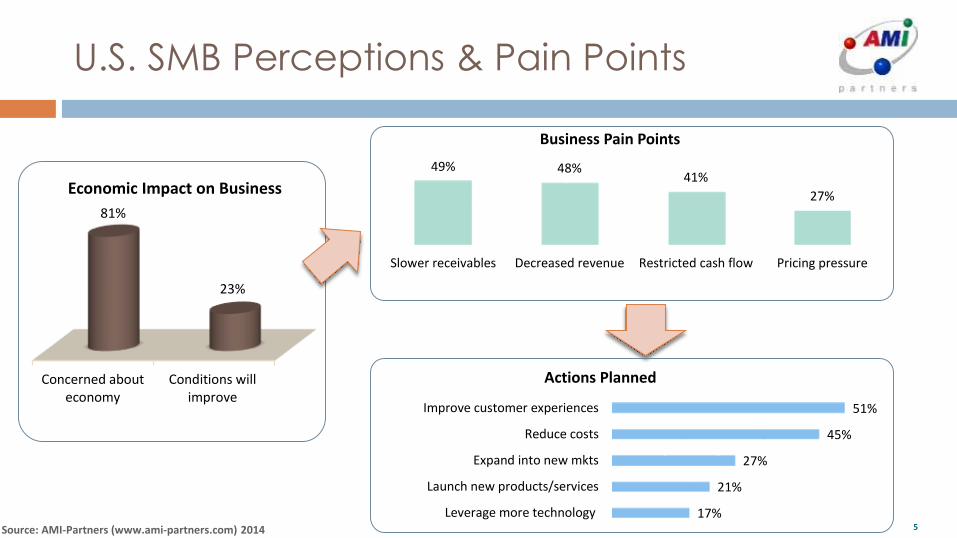

Concerned abouteconomy

Conditions willimprove

81%

23%

Economic Impact on Business

49% 48%41%

27%

Slower receivables Decreased revenue Restricted cash flow Pricing pressure

Business Pain Points

51%

45%

27%

21%

17%

Improve customer experiences

Reduce costs

Expand into new mkts

Launch new products/services

Leverage more technology

Actions Planned

5

U.S. SMB Perceptions & Pain Points

Source: AMI-Partners (www.ami-partners.com) 2014

Small Business Medium Business

71%

59%

45%

40%

39%

37%

37%

Improving bandwidth

On-premise data back-up & disasterrecovery solutions

On-premise data security & privacyfor PCs/network

Security for mobile devices

Data Loss Prevention (DLP) solutions

CRM (Customer RelationshipManagement)

Hosted data back-up & disasterrecovery solutions

ApplicationsConnectivity/

CommunicationsIT Infrastructure Mobility

Source: AMI ICT Tracking Studies6

74%

74%

73%

72%

71%

68%

68%

Improving bandwidth

On-premise data back-up & disaster recoverysolutions

Security for mobile devices

Server virtualization

On-premise data security & privacy forPCs/network

IT systems mgt tools

Data Loss Prevention (DLP) solutions

SMB Strategic IT Imperatives and InvestmentsTechnology remains a strategic focal point for SMBs

Source: AMI-Partners (www.ami-partners.com) 2014

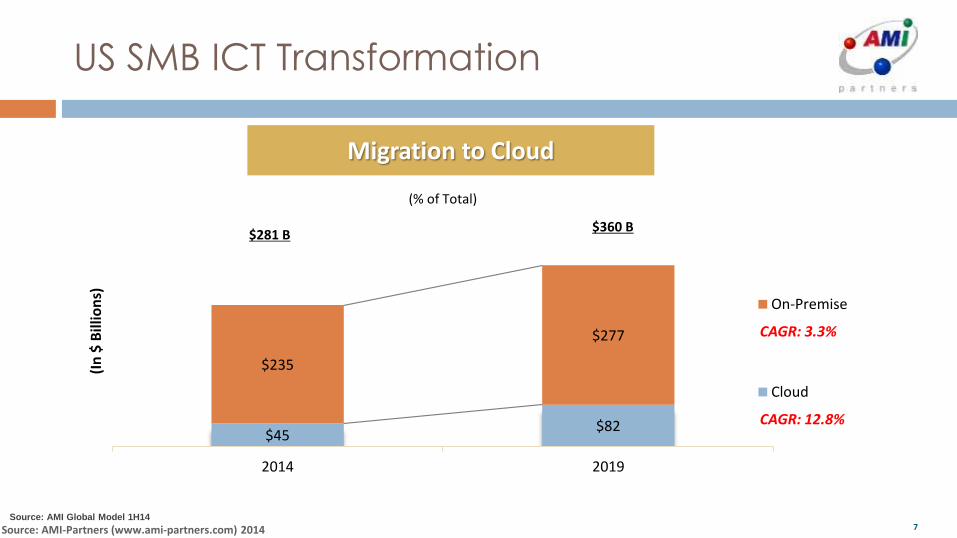

$45 $82

$235

$277

2014 2019

(In

$ B

illio

ns)

On-Premise

Cloud

Migration to Cloud

$281 B$360 B

CAGR: 12.8%

CAGR: 3.3%

(% of Total)

7Source: AMI Global Model 1H14

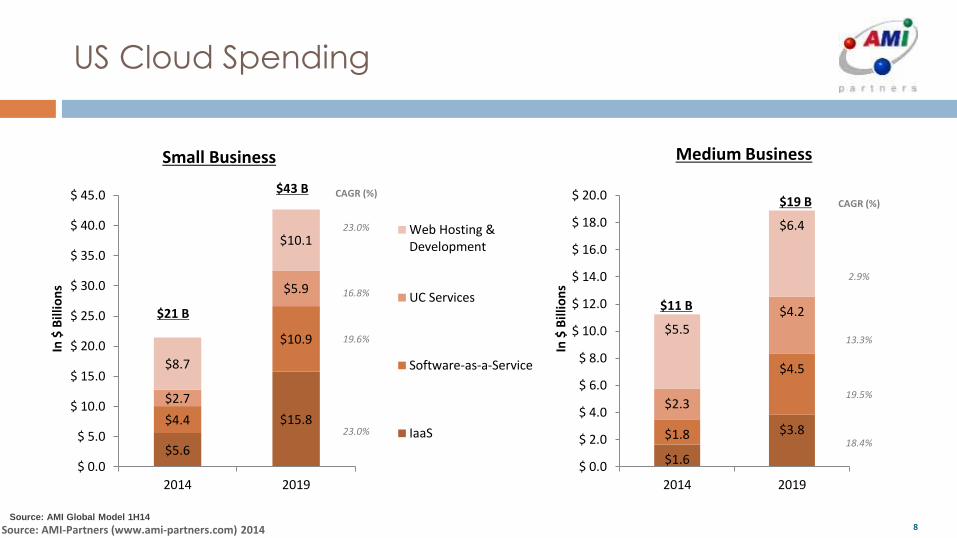

US SMB ICT Transformation

Source: AMI-Partners (www.ami-partners.com) 2014

Small Business Medium Business

8

$5.6

$15.8$4.4

$10.9

$2.7

$5.9

$8.7

$10.1

$ 0.0

$ 5.0

$ 10.0

$ 15.0

$ 20.0

$ 25.0

$ 30.0

$ 35.0

$ 40.0

$ 45.0

2014 2019

In $

Bill

ion

s

Web Hosting &Development

UC Services

Software-as-a-Service

IaaS

$21 B

$43 B

$1.6

$3.8$1.8

$4.5

$2.3

$4.2

$5.5

$6.4

$ 0.0

$ 2.0

$ 4.0

$ 6.0

$ 8.0

$ 10.0

$ 12.0

$ 14.0

$ 16.0

$ 18.0

$ 20.0

2014 2019

In $

Bill

ion

s

CAGR (%)

2.9%

13.3%

19.5%

18.4%

CAGR (%)

23.0%

16.8%

19.6%

23.0%

$11 B

$19 B

Source: AMI Global Model 1H14

US Cloud Spending

Source: AMI-Partners (www.ami-partners.com) 2014

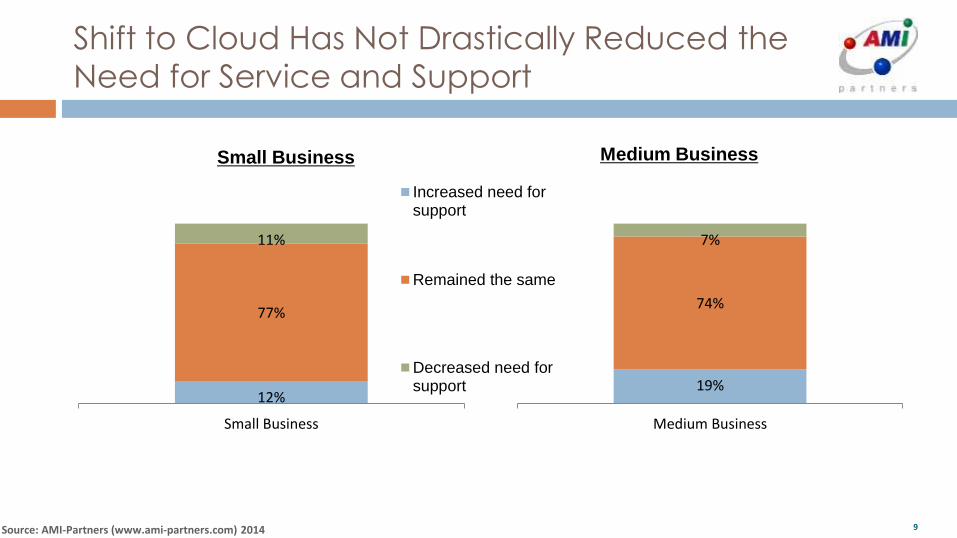

12%

77%

11%

Small Business

Small Business Medium Business

19%

74%

7%

Medium Business

Increased need forsupport

Remained the same

Decreased need forsupport

9

Shift to Cloud Has Not Drastically Reduced the

Need for Service and Support

Source: AMI-Partners (www.ami-partners.com) 2014

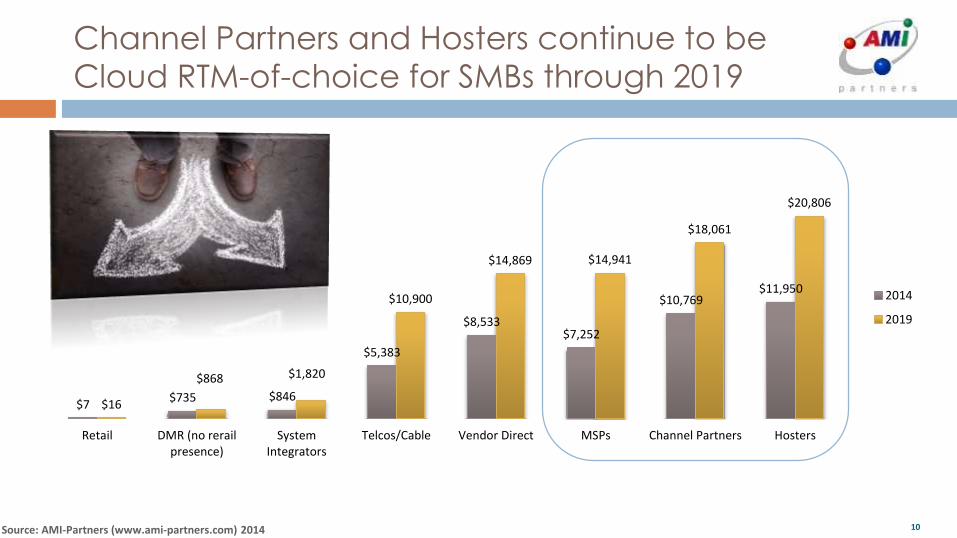

$7$735 $846

$5,383

$8,533$7,252

$10,769$11,950

$16

$868 $1,820

$10,900

$14,869 $14,941

$18,061

$20,806

Retail DMR (no rerailpresence)

SystemIntegrators

Telcos/Cable Vendor Direct MSPs Channel Partners Hosters

2014

2019

10

Channel Partners and Hosters continue to be

Cloud RTM-of-choice for SMBs through 2019

Source: AMI-Partners (www.ami-partners.com) 2014

We have quantified the addressable opportunity and uncovered the challenges faced by SMBs.

How do we target and segment these end-users?

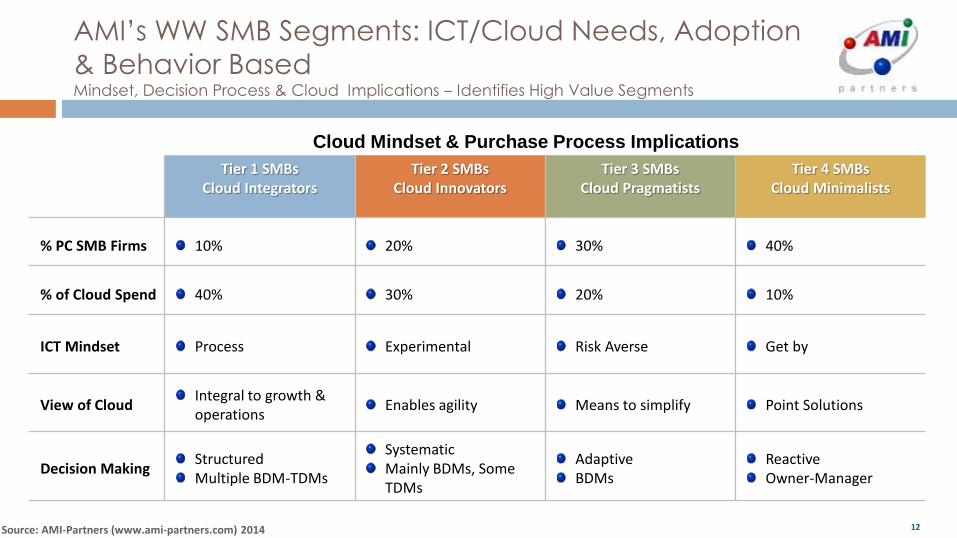

Introducing AMIs SMB Segmentation Model… Allows us to uncover who the key decision makers are and how we can connect

with high value customers.

Targeting High Value Customers

Source: AMI-Partners (www.ami-partners.com) 2014

Tier 1 SMBsCloud Integrators

Tier 2 SMBsCloud Innovators

Tier 3 SMBsCloud Pragmatists

Tier 4 SMBsCloud Minimalists

% PC SMB Firms 10% 20% 30% 40%

% of Cloud Spend 40% 30% 20% 10%

ICT Mindset Process Experimental Risk Averse Get by

View of CloudIntegral to growth & operations

Enables agility Means to simplify Point Solutions

Decision MakingStructuredMultiple BDM-TDMs

SystematicMainly BDMs, Some TDMs

AdaptiveBDMs

ReactiveOwner-Manager

Cloud Mindset & Purchase Process Implications

12

AMI’s WW SMB Segments: ICT/Cloud Needs, Adoption

& Behavior Based Mindset, Decision Process & Cloud Implications – Identifies High Value Segments

Source: AMI-Partners (www.ami-partners.com) 2014

Tier 1 Tier 2 Tier 3 Tier 4

SaaS

Acctg/Financials

Payroll

HR

CRM

ERP

Proj Mgt.

Bus Intel/analytics

IaaS

Storage

Servers

Security

UC

Audio Conf.

Video Conf.

Web Conf.

Hosted VoIP

IM

25%

48%

22%

37%

13%

25%

28%

39%

34%

56%

75%

48%

64%

24%

73%

21%

33%

3%

8%

1%

3%

2%

32%

14%

28%

43%

18%

23%

37%

59%

6%

7%

2%

1%

4%

13%

8%

15%

18%

17%

12%

7%

57%

3%

9%

1%

1%

1%

5%

3%

12%

26%

25%

17%

7%

34%13

Cloud Applications/Services Usage – Tiers

1 and 2 are Principal Drivers

Source: AMI-Partners (www.ami-partners.com) 2014

What steps are partners taking to drive success & profitability in the cloud and what metrics should we track to benchmarkourselves against them?

AMI has segmented and benchmarked partners based on how far they are along the cloud transformation journey.

How to Measure Yourself Against Best in

Class Partners?

Source: AMI-Partners (www.ami-partners.com) 2014

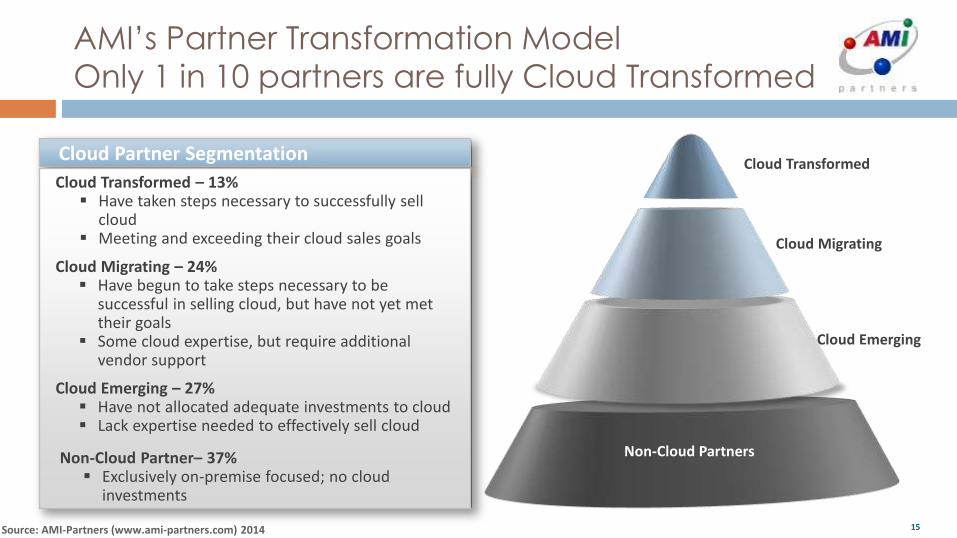

Cloud Partner SegmentationCloud Transformed

Cloud Migrating

Cloud Emerging

Cloud Emerging – 27% Have not allocated adequate investments to cloud Lack expertise needed to effectively sell cloud

Cloud Migrating – 24% Have begun to take steps necessary to be

successful in selling cloud, but have not yet met their goals

Some cloud expertise, but require additional vendor support

Cloud Transformed – 13% Have taken steps necessary to successfully sell

cloud Meeting and exceeding their cloud sales goals

15

AMI’s Partner Transformation Model

Only 1 in 10 partners are fully Cloud Transformed

Non-Cloud Partner– 37% Exclusively on-premise focused; no cloud

investments

Non-Cloud Partners

Source: AMI-Partners (www.ami-partners.com) 2014

Cloud Partner Metrics

Sales Expertise

Technical Expertise

Cloud Revenue Model

Marketing Expertise

Vendor Engagement

Customer Engagement

Cloud Sales Goals

Cloud dedicated sales staff

Cloud marketing activities

Cloud certified emps

Cloud biz. modelsCustomer Sat.

Customer demand

Cloud vendor partnerships

Marketing funds for cloud

Cloud Models Offered

% of revenue from cloud

Cloud Partner Benchmarking Metrics

16

Partner Benchmarking Approach & MetricsThere are several business areas that are key for partner transformation

Source: AMI-Partners (www.ami-partners.com) 2014

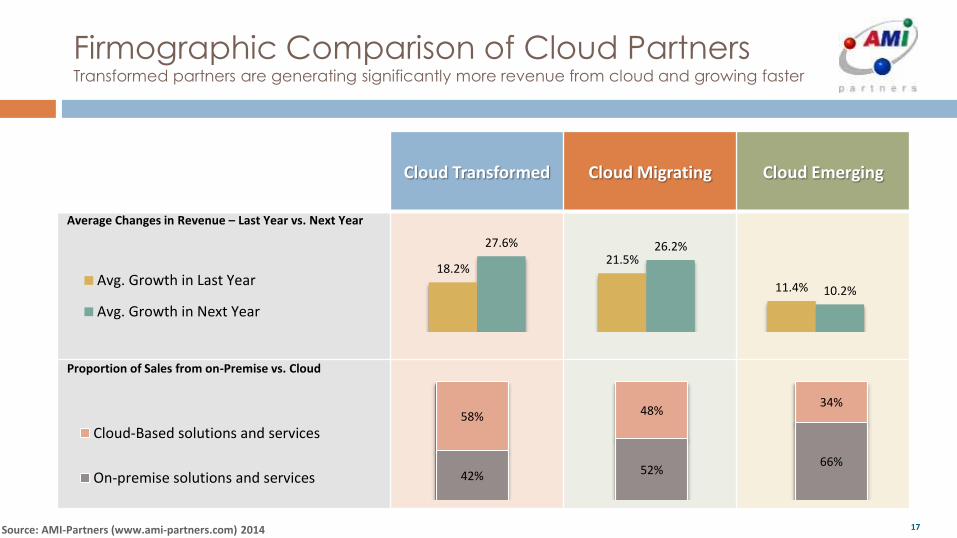

Cloud Transformed Cloud Migrating Cloud Emerging

Average Changes in Revenue – Last Year vs. Next Year

Proportion of Sales from on-Premise vs. Cloud

18.2%21.5%

11.4%

27.6% 26.2%

10.2%Avg. Growth in Last Year

Avg. Growth in Next Year

42% 52%66%

58% 48%34%

Cloud-Based solutions and services

On-premise solutions and services

17

Firmographic Comparison of Cloud PartnersTransformed partners are generating significantly more revenue from cloud and growing faster

Source: AMI-Partners (www.ami-partners.com) 2014 18

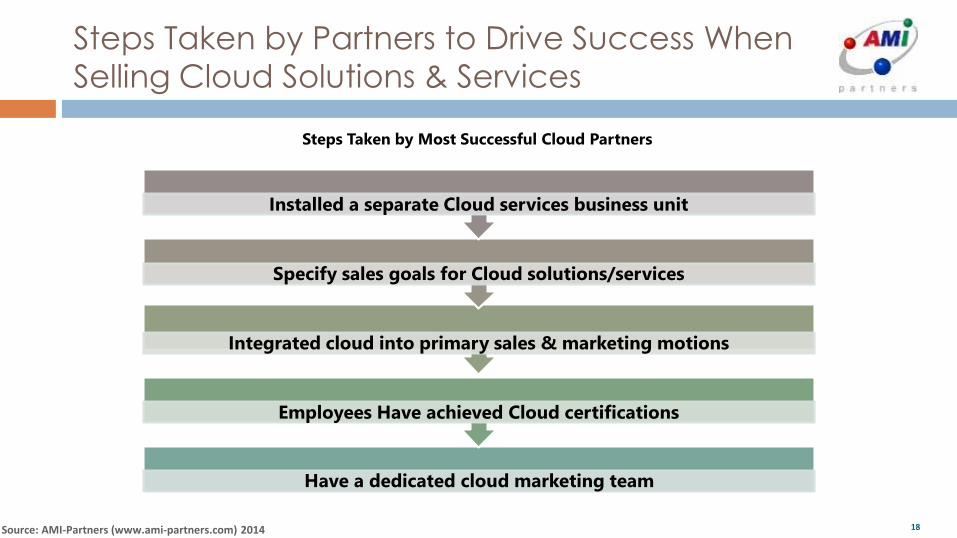

Steps Taken by Partners to Drive Success When

Selling Cloud Solutions & Services

Have a dedicated cloud marketing team

Employees Have achieved Cloud certifications

Integrated cloud into primary sales & marketing motions

Specify sales goals for Cloud solutions/services

Installed a separate Cloud services business unit

Steps Taken by Most Successful Cloud Partners

Source: AMI-Partners (www.ami-partners.com) 2014

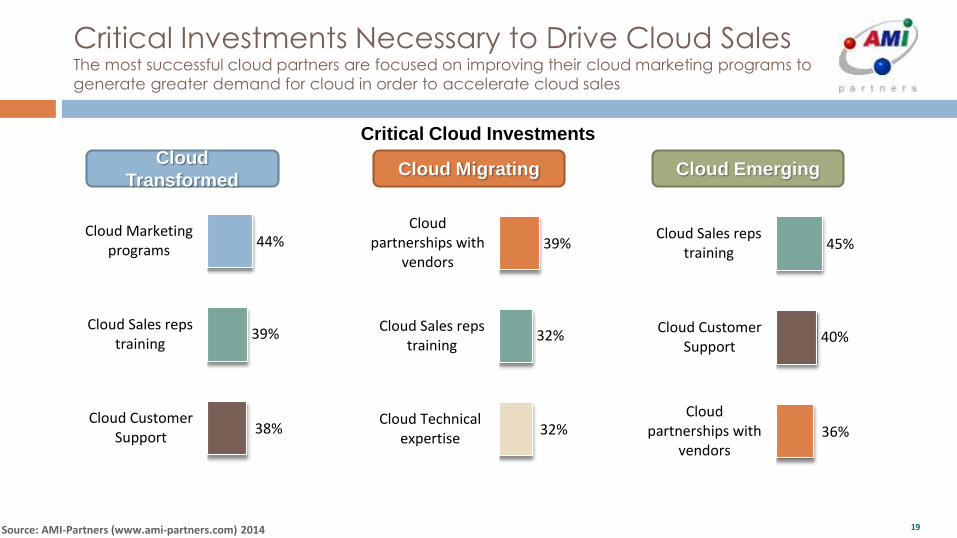

44%

39%

38%

Cloud Marketingprograms

Cloud Sales repstraining

Cloud CustomerSupport

39%

32%

32%

Cloudpartnerships with

vendors

Cloud Sales repstraining

Cloud Technicalexpertise

45%

40%

36%

Cloud Sales repstraining

Cloud CustomerSupport

Cloudpartnerships with

vendors

Cloud

TransformedCloud Migrating Cloud Emerging

19

Critical Cloud Investments

Critical Investments Necessary to Drive Cloud SalesThe most successful cloud partners are focused on improving their cloud marketing programs to

generate greater demand for cloud in order to accelerate cloud sales

Source: AMI-Partners (www.ami-partners.com) 2014

Cloud

TransformedCloud Migrating Cloud Emerging

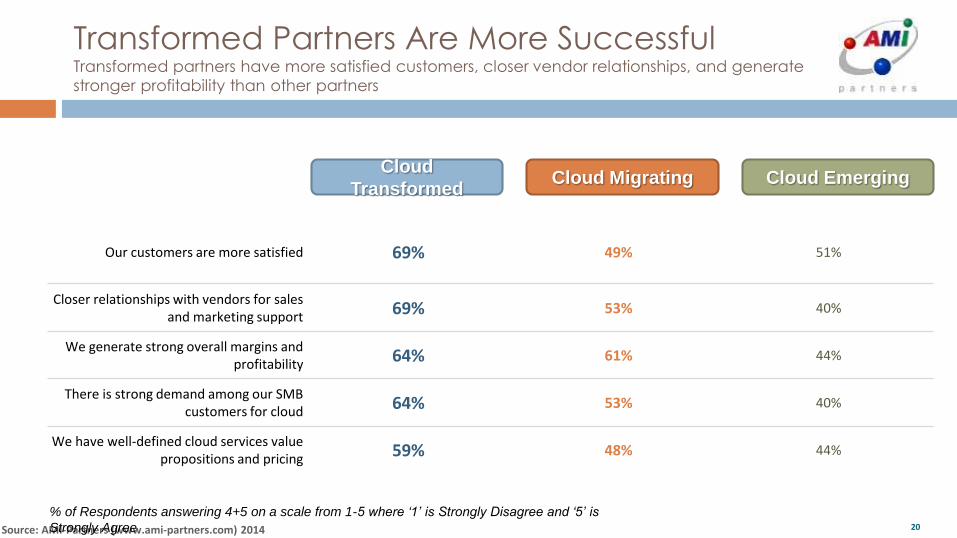

Our customers are more satisfied 69% 49% 51%

Closer relationships with vendors for sales and marketing support 69% 53% 40%

We generate strong overall margins and profitability 64% 61% 44%

There is strong demand among our SMB customers for cloud 64% 53% 40%

We have well-defined cloud services value propositions and pricing 59% 48% 44%

20

% of Respondents answering 4+5 on a scale from 1-5 where ‘1’ is Strongly Disagree and ‘5’ is

Strongly Agree

Transformed Partners Are More SuccessfulTransformed partners have more satisfied customers, closer vendor relationships, and generate

stronger profitability than other partners

Source: AMI-Partners (www.ami-partners.com) 2014

Perform Marketing Activities On a Daily

Basis

20+% Marketing Budget Dedicated to

Cloud

Work with IT Vendors for Marketing

Has a Dedicated Cloud Sales & Marketing

Team

Marketing Approach

21

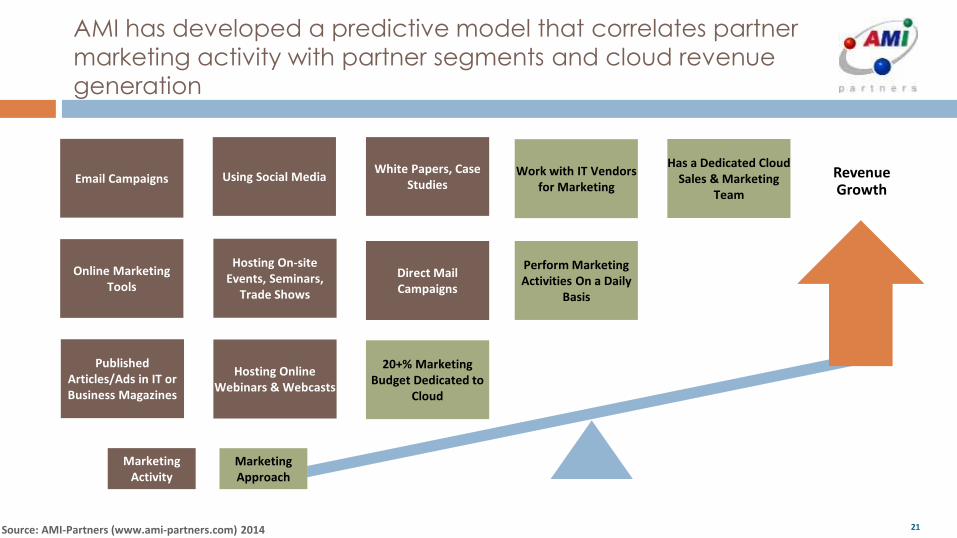

AMI has developed a predictive model that correlates partner

marketing activity with partner segments and cloud revenue

generation

Source: AMI-Partners (www.ami-partners.com) 2014

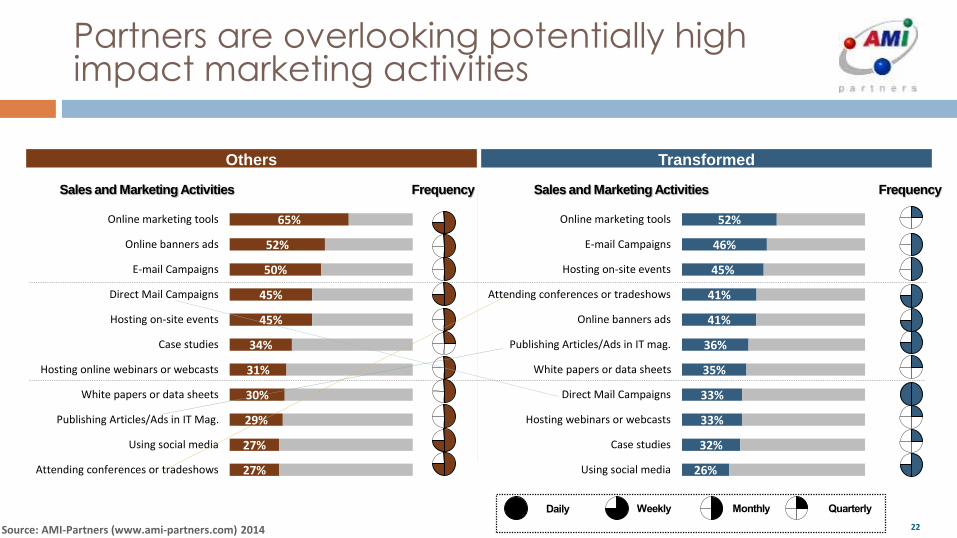

52%

46%

45%

41%

41%

36%

35%

33%

33%

32%

26%

Online marketing tools

E-mail Campaigns

Hosting on-site events

Attending conferences or tradeshows

Online banners ads

Publishing Articles/Ads in IT mag.

White papers or data sheets

Direct Mail Campaigns

Hosting webinars or webcasts

Case studies

Using social media

65%

52%

50%

45%

45%

34%

31%

30%

29%

27%

27%

Online marketing tools

Online banners ads

E-mail Campaigns

Direct Mail Campaigns

Hosting on-site events

Case studies

Hosting online webinars or webcasts

White papers or data sheets

Publishing Articles/Ads in IT Mag.

Using social media

Attending conferences or tradeshows

Sales and Marketing Activities Generate Strong Success

Frequency

Others

Sales and Marketing Activities Frequency

Transformed

22

Partners are overlooking potentially high impact marketing activities

Source: AMI-Partners (www.ami-partners.com) 2014 23

Cloud Transformed Cloud Migrating Cloud Emerging

Direct/Face-to-face Via Field Salesforce

67% 49% 55%

Direct Through Telesales 56% 52% 50%

Indirect via other channel partners/resellers

36% 42% 44%

Indirect via App Stores/ Aggregators/Brokers

28% 37% 36%

Via our website 47% 50% 48%

% of Respondents answering 4+5 on a scale from 1-5 where ‘1’ is Not at all Effective and ‘5’ is Very

Effective

Top Cloud Sales MethodsTransformed partners are self-reliant whereas other partners prefer indirect sales tactics

Source: AMI-Partners (www.ami-partners.com) 2014 24

Cloud ConnexMaking Money Just Got Easier – Resell Private-Labeled, Cloud-Based Services

Extend

Customer Opps

NEW

Revenue Sources

Minimal

Investment

Increase

Profit Margins

NEW

Portfolio Products

Combine or Sell

Standalone

Source: AMI-Partners (www.ami-partners.com) 2014 25

Cloud ConnexEasily and Affordably Resell and Deliver Your Own Branded Cloud Solutions

Source: AMI-Partners (www.ami-partners.com) 2014 26

Cloud ConnexAvailable Services

Reseller

Customers

Q & A?