saving and investment chapter 6. 2 saving, investment, and the capital market saving occurs when...

TRANSCRIPT

Saving and Investment

Chapter 6

2

Saving, Investment, and the Capital Market

• Saving occurs when households choose not to spend part of their income.

• Investment occurs when firms purchase new capital equipment.

• A mechanism for channeling funds from savers to investors is the capital market.

3

Smoothness

• Standard Deviation: the average difference from the average.

• Formula: 2/1

1

2

1

n

xxn

ii

x

4

Consumption and GDP in the United States

Figure 6.1A

©2002 South-Western College Publishing

5

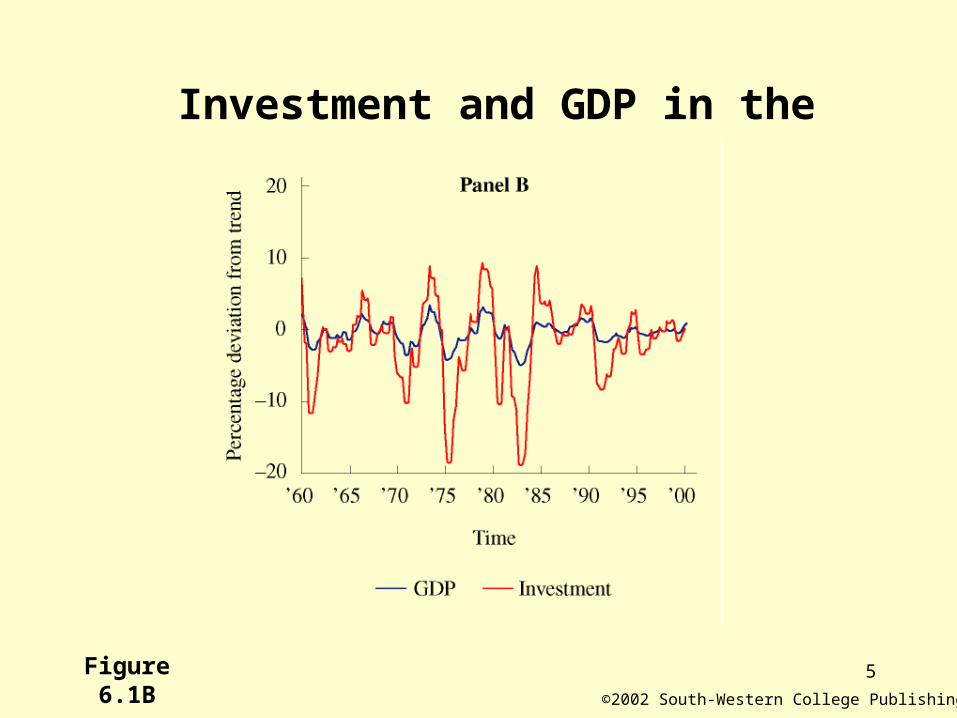

Investment and GDP in the United States

Figure 6.1B©2002 South-Western College Publishing

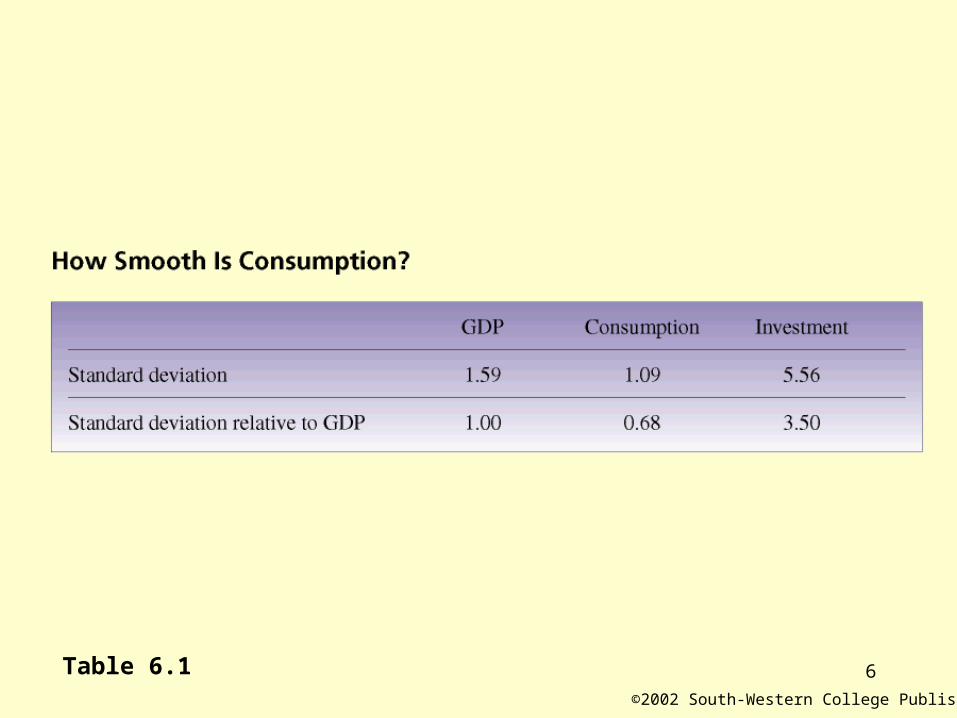

6Table 6.1©2002 South-Western College Publishing

7

Why Is Investment So Volatile?

• Fundamental Explanation (Classical):

Investment fluctuates because firms respond to changes in technology.

Ex. New Invention.

• This is the basis for the RBC school.

8

Why Is Investment So Volatile?

• Animal Spirit (Keynesian) : Highly volatile investment represents changes

in the mass psychology of investors. Belief: It could be avoided if investment were

more efficiently coordinated. They favors the implementation of

government policies to stabilize the business cycle.

Different Names: Self-fulfilling, Sunspots, Irrational Exuberance.

9

Consumption Smoothing

• Households borrow and lend in the capital market in an effort to redistribute their income more evenly over time.

• A convex intertemporal utility function.

• Ex. Robinson Crusoe

• Both Keynesian and Classical economists agree this reason.

10

11

Borrowing Constraints

• Keynesian economists agree that the capital market is used by H.H. to smooth income, but not that the market works well.

• Some economists point out that although aggregate consumption is smoother than income, it is not as smooth as it could be.

• RBC model predicts that consumption should be less volatile than it actual is.

12

Borrowing Constraints

• Many people have low incomes early in life and high incomes later in life.

• We often attempt to borrow more money than we are able to when young.

• Reason: It is hard for banks to enforce repayment later on.

13

How Does the Borrowing Constraints Alter the Classical Theory

• Suppose some H.H.s prefer to consume more than their income and opt to repay their loan later in life.

• If the credit market is imperfect, they are constrained.

• The presence of credit constrained individuals implies that aggregate consumption will fluctuate more.

14

15

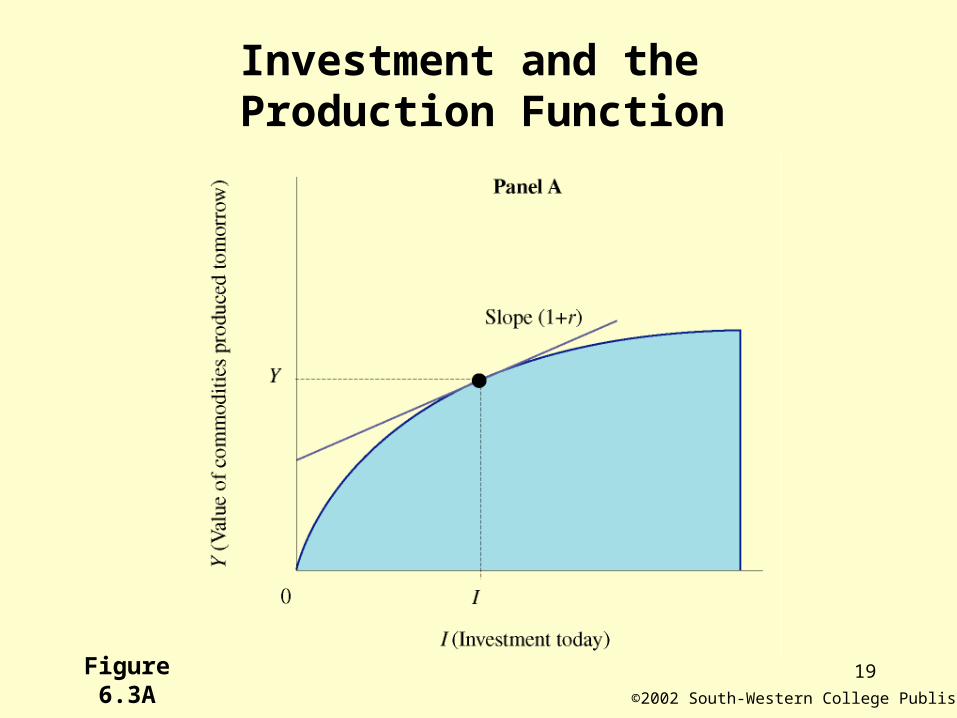

Investment

• How would Robinson make decisions if he were both a producer and a consumer?

• We illustrate the options available to Robinson Crusoe with a production possibility set in which inputs and outputs occur at different points in time.

• Robinson must decide how to allocate his produced commodities between consumption goods and investment goods.

16

Intertemporal Production Possibility Set

• The opportunities of investment is represented as intertemporal production possibility set. (Figure 6.2)

• The production possibility set has an upward-slopping frontier because the more present investment leads to more future income.

• In a modern industrial society, diminishing returns to investment applies because the stock of people is fixed.

17Figure 6.2

©2002 South-Western College Publishing

The Intertemporal Production Possibilities Set

18

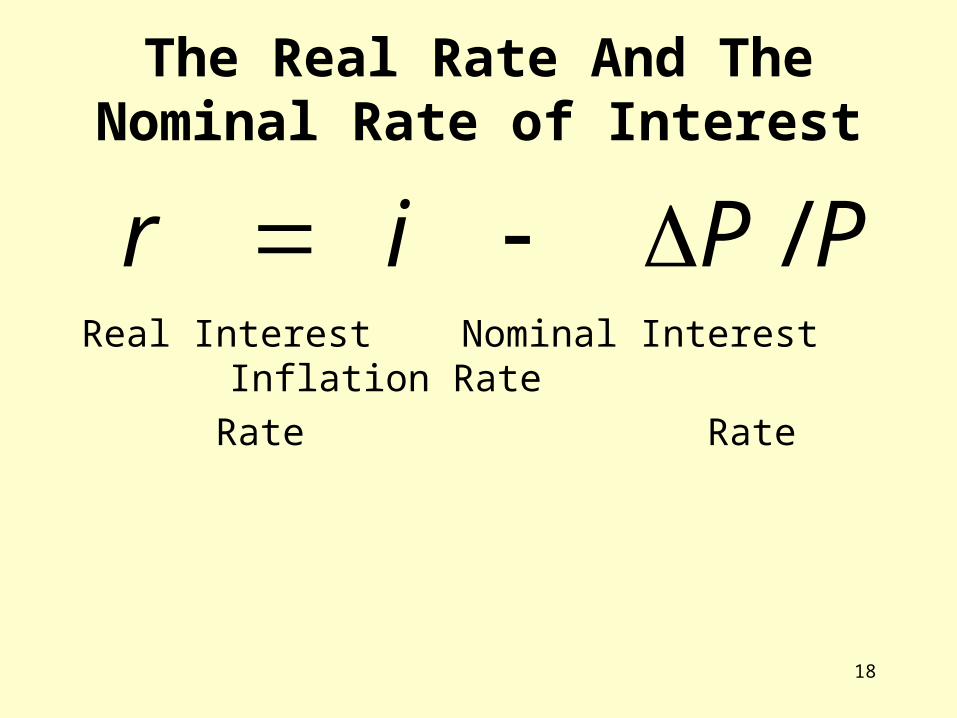

The Real Rate And The Nominal Rate of Interest

Real Interest Nominal Interest Inflation Rate

Rate Rate

PPir /

19

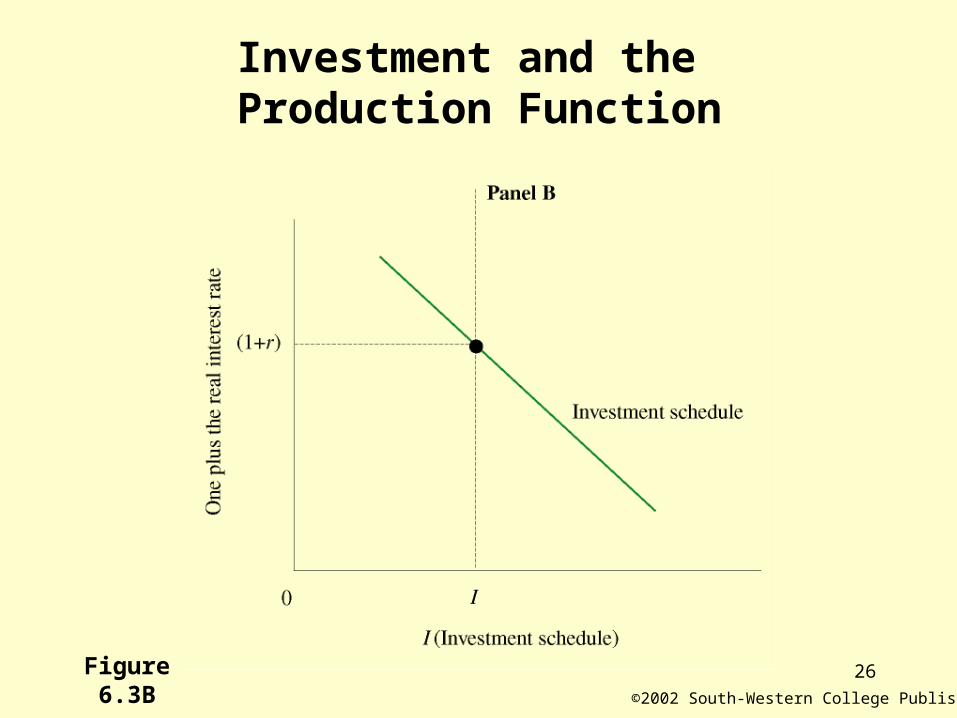

Investment and the Production Function

Figure 6.3A©2002 South-Western College Publishing

20

Maximizing Profits• The classical theory of production assumes that

markets are competitive.

• Classical theory assumes that firms choose how much labor to demand in order to maximize profits, so the same logic is applied to the decision about how much to invest.

• A firm’s profit is the value of its produced output minus the accrued principal and interest on loans needed to purchase current investment goods.

21

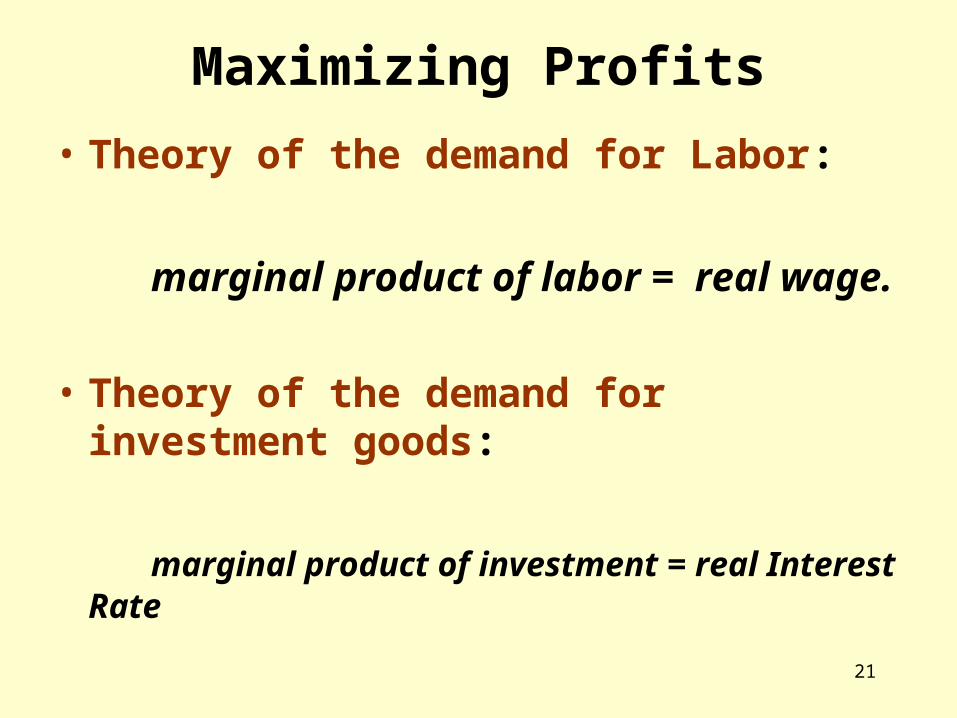

Maximizing Profits

• Theory of the demand for Labor:

marginal product of labor = real wage.

• Theory of the demand for investment goods:

marginal product of investment = real Interest Rate

22

Borrowing and the Investment Schedule

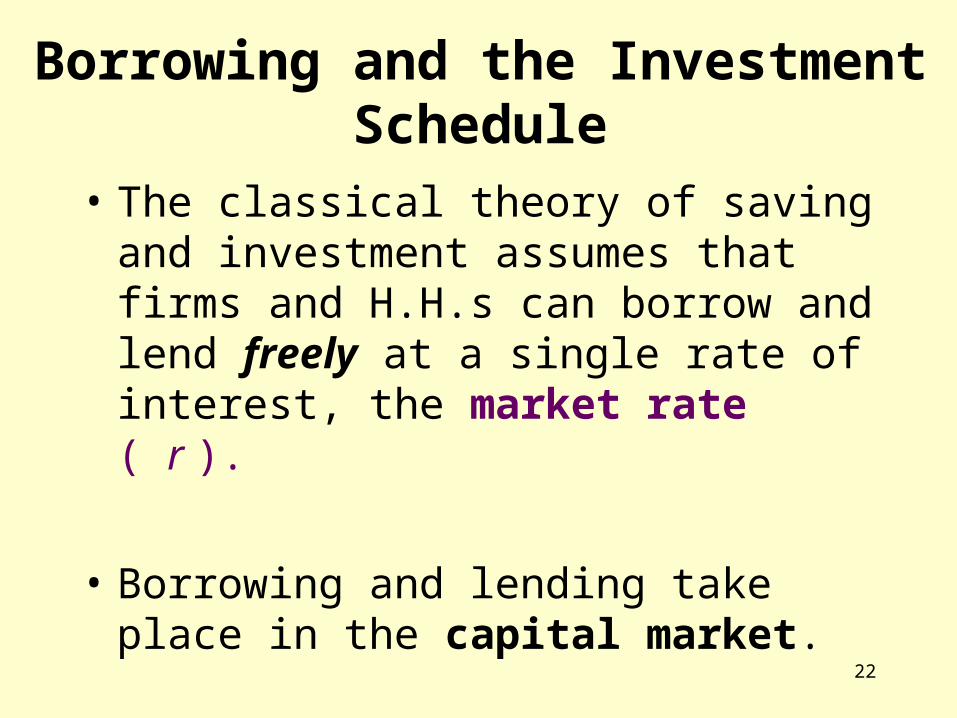

• The classical theory of saving and investment assumes that firms and H.H.s can borrow and lend freely at a single rate of interest, the market rate ( r ).

• Borrowing and lending take place in the capital market.

23

Borrowing and the Investment Schedule

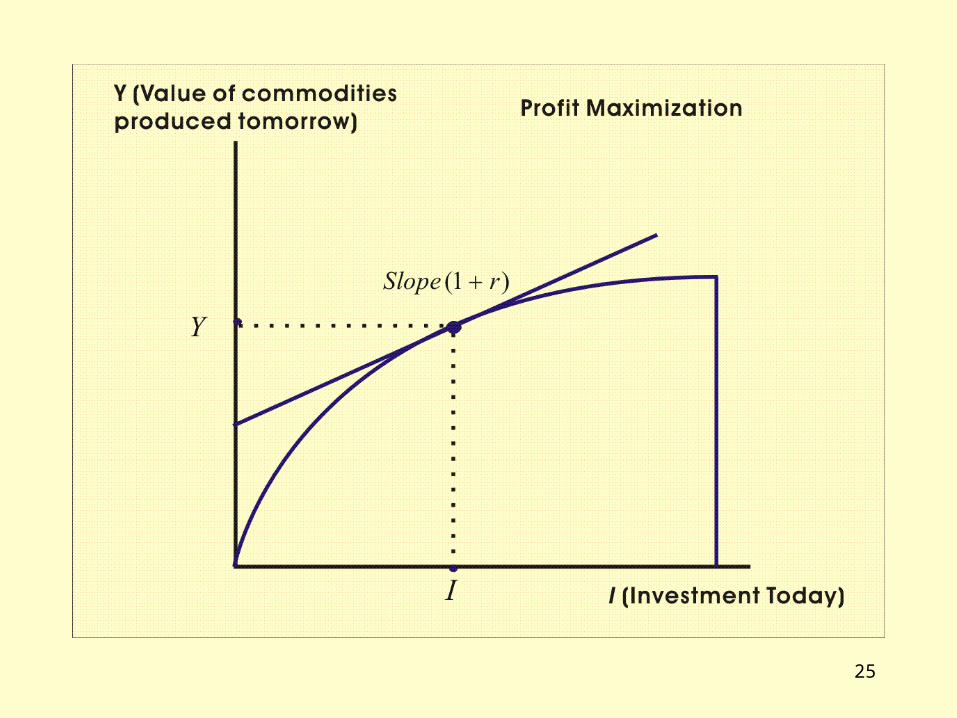

• Suppose firm can produce output tomorrow of value Y from an investment of I resources.

• Profit Value of future sales Cost of Borrowing

IrY )1(

24

Profit Maximization

F.O.C.

marginal product of investment = 1 + real Interest Rate

The investment demand curve slopes downward.

.)1()(

)1(

IrIG

IrY

)1()(' rIG

25

26

Investment and the Production Function

Figure 6.3B©2002 South-Western College Publishing

27

Deriving the Investment Schedule

• The boundary of the intertemporal production possibility set:

• Max

• F.O.C.

Marginal Product Marginal Cost

of Investment

2)2/1( IIAY S

).1( rIA

IrIAI )1()2/1( 2

28

29

Households and the Saving Supply Curve

• The application of the theory of marginal utility to the problem of saving is called the intertemporal utility theory.

• Intertemporal utility theory argues that, given the choice, families would prefer that consumption be evenly distributed over time.

• Preferences for consumption at different points in time are represented by utility.

30

The Intertemporal Budget Constraint

• Suppose the household puts its income into the capital market by lending to another household or firm.

• In return, the household receives future resources with interest.

• The rate of interest is the price at which present consumption can be exchanged for future consumption.

31

Present Value• When you borrow against future income, the

amount you can borrow is its present value.

• Example:

John will inherit $10000 next year when he turns 21 years old. He would like to spend his inheritance on a used car and is impatient and unable to wait until next year.

If he buy the car right away, bank manager will lend him:

.9901100001.01

1

)1(

1

Y

r

32

Borrowing and Lending to Smooth Consumption

• Y1: present income C1: present consumption • Y2: future income C2: future consumption• Intertemporal Budget Constraint places a

bound on the amount of consumption that is available over a household’s lifetime.

present present value of current present value of consumption future consumption resources future resources

2121 )1(

1

)1(

1Y

rYC

rC

33

Borrowing and Lending to Smooth Consumption

Left Side: Sum of the values of present and future consumption.

Right Side:Sum of the values of present and future income.

The price of future consumption is 1/(1+r) , where r is the interest rate.

2121 )1(

1

)1(

1Y

rYC

rC

34

The Saving Supply Curve

• Households maximize utility lead to a relationship between the real interest rate and the quantity of saving, called saving supply curve.

Two Effects when r varies:

1. Substitution Effect

2. Wealth Effect

35

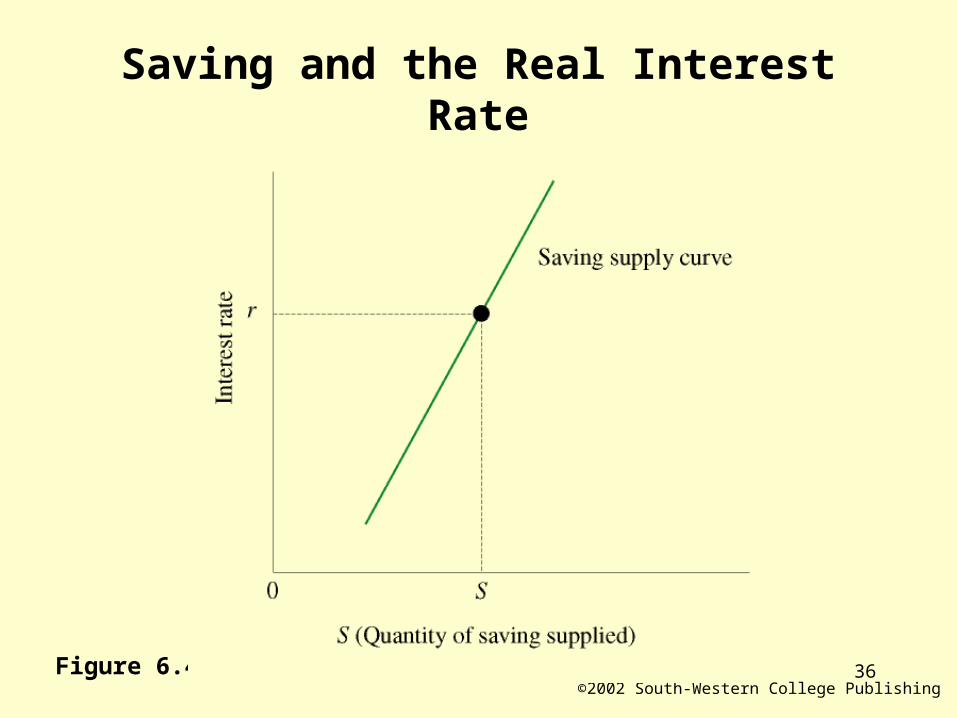

The Saving Supply Curve

• Substitution Effect (S.E.): As r goes up, current consumption becomes

relatively more expensive, and makes the household want to substitute consumption today for consumption tomorrow.

• Wealth Effect (W.E.): An increase in r makes the household

wealthier.Neoclassical theory assumes the supply of saving slopes upward, i.e. S.E.>W.E. .

36Figure 6.4©2002 South-Western College Publishing

Saving and the Real Interest Rate

37

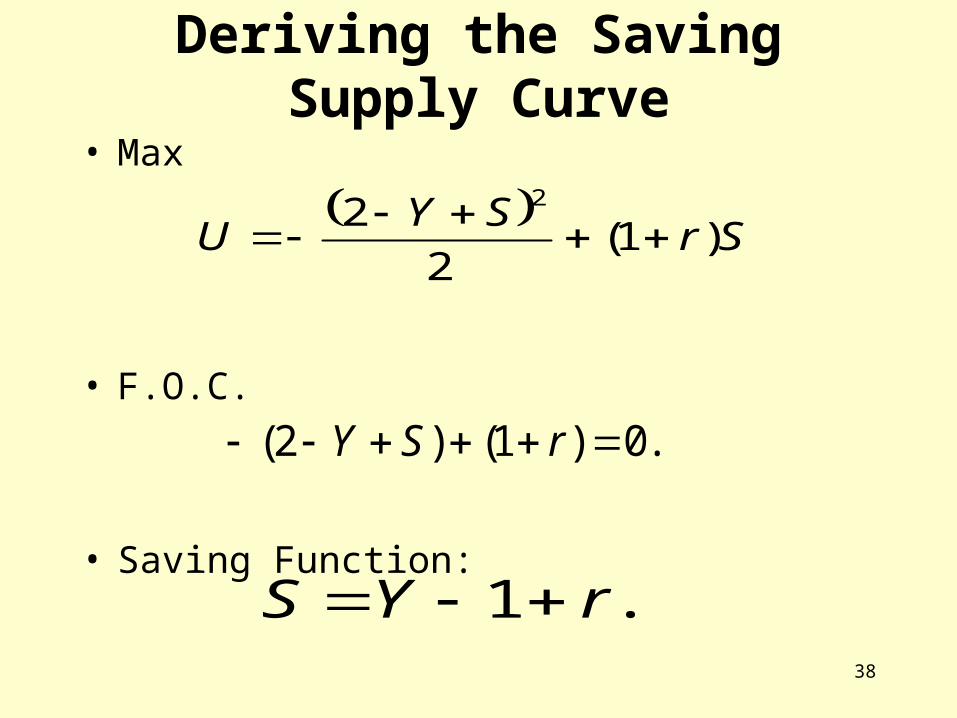

Deriving the Saving Supply Curve

• Utility function

• In current period, H.H. saves S from its income Y and consumes C1:

• In the second period (old age), H.H. consumes the principal and interest on its saving (1+r)S. We assume that H.H. has no income in old age.

1CYS

SrC )1(2

2

21

2

2C

CU

38

Deriving the Saving Supply Curve

• Max

• F.O.C.

• Saving Function:

.0)1()2( rSY

.1 rYS

Sr

SYU )1(

2

2 2

39

40

Saving and Investment in a Closed Economy

• Figure 6.5 shows how the interest rate, saving and investment are simultaneously determined.

• The saving supply curve represents the funds that are flowing into the capital market from H.H.

• The investment curve represents the funds flowing out of the market to firms that borrow the money to build new factories and machines.

41

Saving and Investment in a Closed Economy

• At r1, H.H.s supply S1 and firms want to borrow I1 to finance investment projects;

I > S.• At r2, H.H.s supply S2 and firms want to

borrow I2 to finance investment projects; I < S.• Only when r = rE does saving equal

investment. Then the capital market is in equilibrium and I = S = IE.

42Figure 6.5

©2002 South-Western College Publishing

Capital Market Equilibrium

43

Equilibrium in the Capital Market

• Investment demand curve:

• Saving supply curve

• I = S,

).1( rIA

2

YAr

.12

)( AYIS

.1 rYS

44

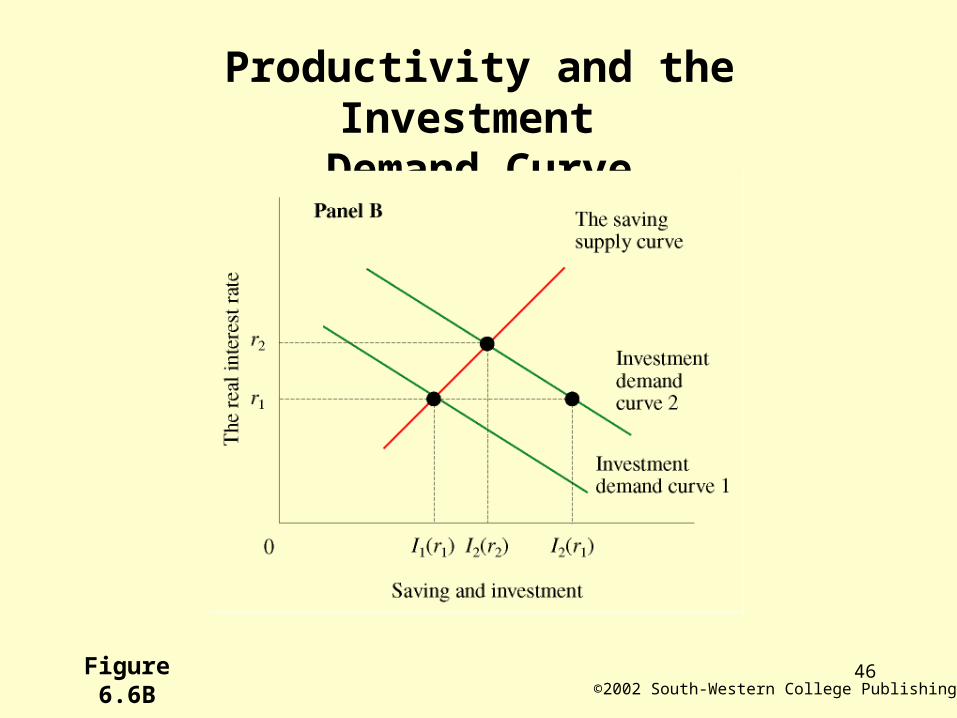

Productivity and the Investment Demand Curve

• Classical view of business cycle: Technology Shocks.

• Example: The invention of the personal computer in the 1970s.

• The new invention raise the productivity and the firm demands more investment for any given rate of interest.

45Figure 6.6A©2002 South-Western College Publishing

Productivity and the Investment Demand Curve

46Figure 6.6B©2002 South-Western College Publishing

Productivity and the Investment Demand Curve

47

Animal Spirits and the Investment Demand Curve

• Because investment and production do not take place at the same time, investors may make mistakes.

• Keynes thought that irrational swings of optimism and pessimism might be more important driving forces in the stock market than fundamentals.

48

Animal Spirits and the Investment Demand Curve

• A new technology is unproven and investments that are made on the basis of mistaken belief about future productivity have the same effect on the capital market as investments that later turn out to be profitable.

49

Animal Spirits and the Investment Demand Curve

• Is the market overvalued today?

1. We are entering a new era in which the economy will witness unprecedented growth.

2. The information age has made markets more efficient, narrowing the gap between debt and equity as more households begin to invest in the market on a daily basis.

50

Animal Spirits and the Investment Demand Curve

• Robert Shiller argues that:

1. The high value of the current market represents a “bubble” that is not justified by fundamentals.

2. He cautions that an overvalued market is, by historical standards, inherently precarious.

51

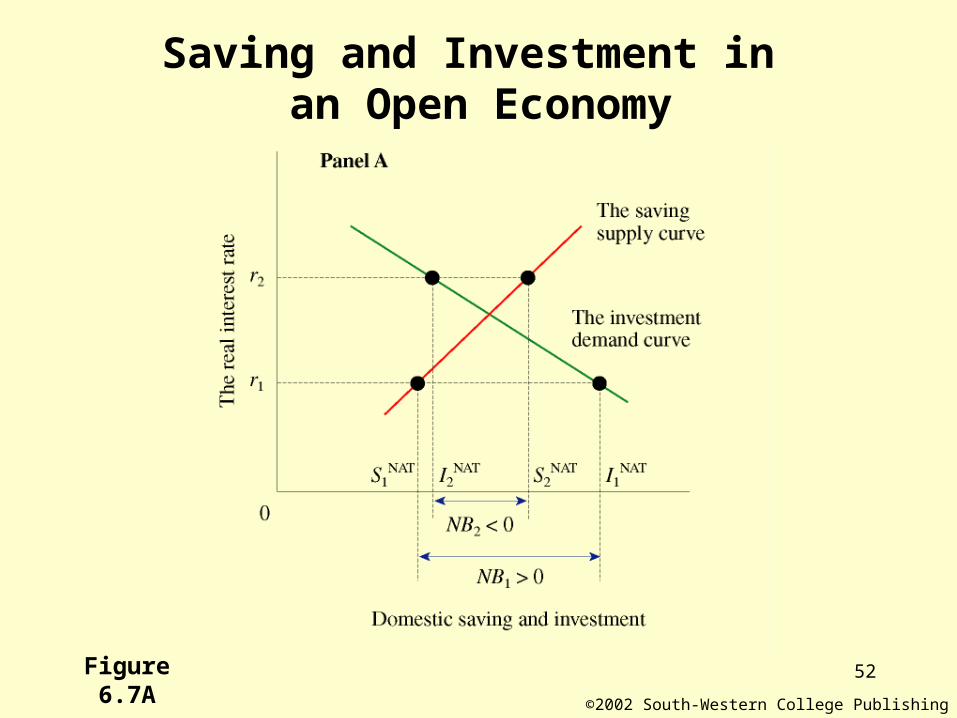

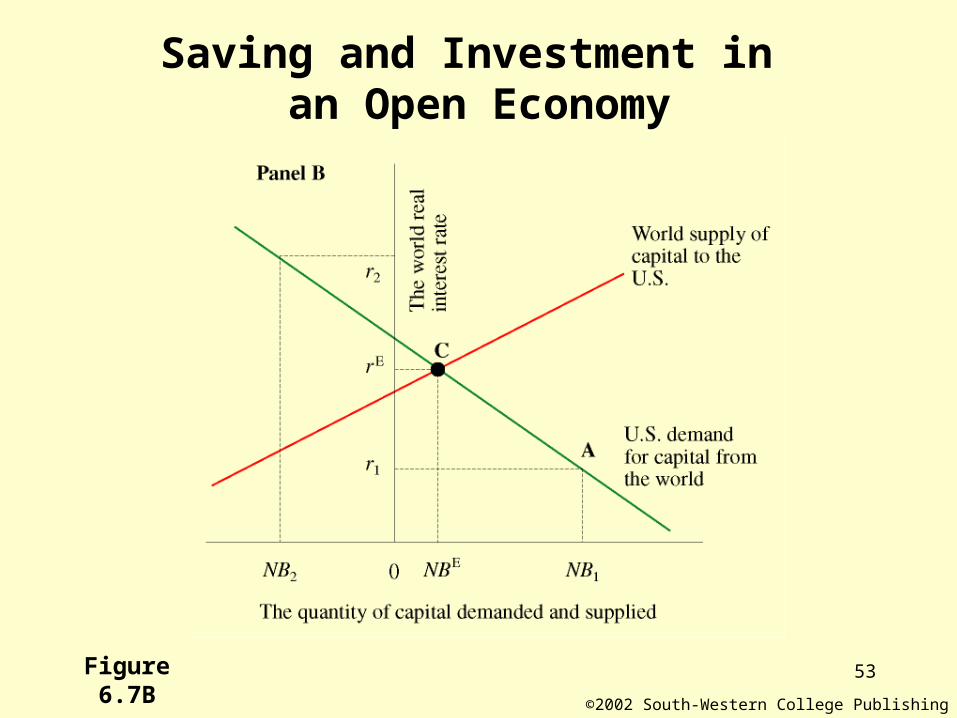

Saving and Investment in an Open Economy

• The difference between the open economy and the closed economy models is that:

In the open economy, domestic saving does not equal domestic investment;

The deficit is made up by net borrowing from abroad.

52Figure 6.7A

©2002 South-Western College Publishing

Saving and Investment in an Open Economy

53Figure 6.7B

©2002 South-Western College Publishing

Saving and Investment in an Open Economy

54

Homework

Question 1, 4, 7, 12

END