session 2. saving and investment. the real interest rate. 2.pdf · saving, investment investment...

TRANSCRIPT

1

Macroeconomics in the Global Economy Antonio Fatás

Session 2. Saving and Investment. The Real Interest Rate.

v National Accounting Identity

v Consumption and Saving

v Investment

v Equilibrium and the real interest rate

v Applications: Farewell to cheap capital?

Macroeconomics in the Global Economy Antonio Fatás

The expenditure approach to measuring GDP:

GDP = C + I + G + NX

C = Private Consumption (Households expenditures excluding housing)

I = Private Investment (Infrastructure, Structures, Equipment, Housing)

G = Government Spending (Purchases of Goods and Services by Government, excludes Transfers)

NX = Net Exports (Exports – Imports)

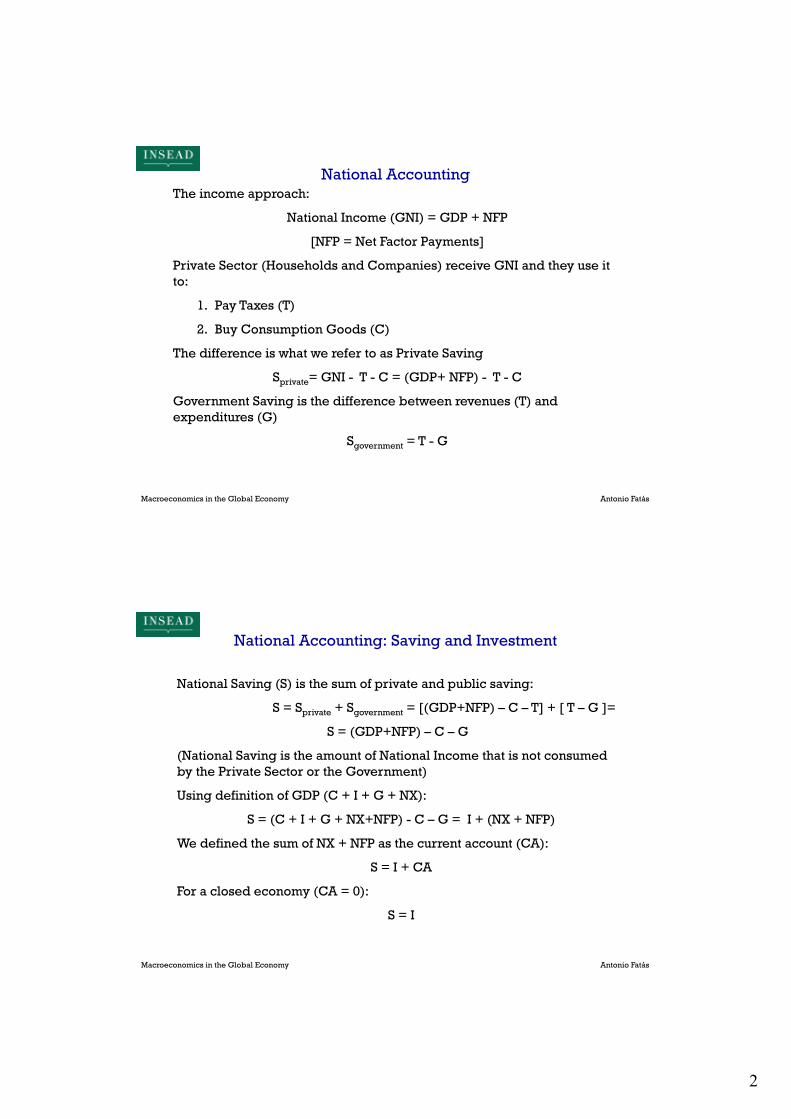

National Accounting

2

Macroeconomics in the Global Economy Antonio Fatás

The income approach:

National Income (GNI) = GDP + NFP

[NFP = Net Factor Payments]

Private Sector (Households and Companies) receive GNI and they use it to:

1. Pay Taxes (T)

2. Buy Consumption Goods (C)

The difference is what we refer to as Private Saving

Sprivate= GNI - T - C = (GDP+ NFP) - T - C

Government Saving is the difference between revenues (T) and expenditures (G)

Sgovernment = T - G

National Accounting

Macroeconomics in the Global Economy Antonio Fatás

National Saving (S) is the sum of private and public saving:

S = Sprivate + Sgovernment = [(GDP+NFP) – C – T] + [ T – G ]=

S = (GDP+NFP) – C – G

(National Saving is the amount of National Income that is not consumed by the Private Sector or the Government)

Using definition of GDP (C + I + G + NX):

S = (C + I + G + NX+NFP) - C – G = I + (NX + NFP)

We defined the sum of NX + NFP as the current account (CA):

S = I + CA

For a closed economy (CA = 0):

S = I

National Accounting: Saving and Investment

3

Macroeconomics in the Global Economy Antonio Fatás

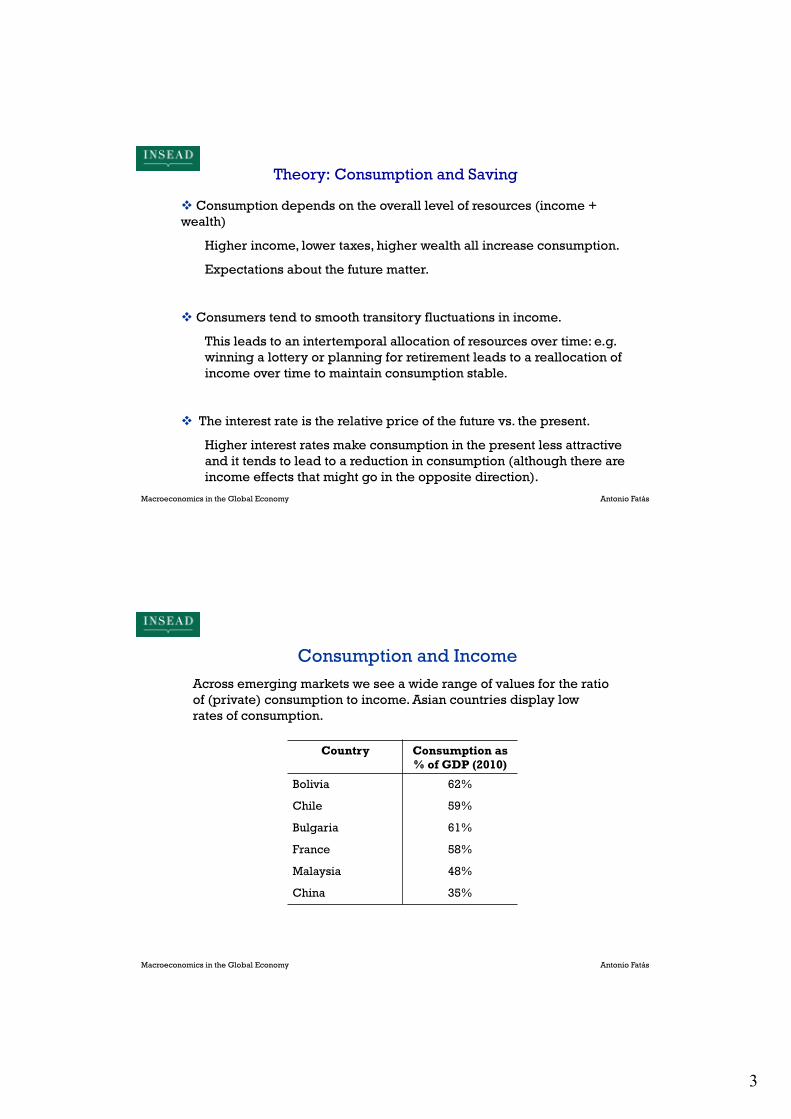

v Consumption depends on the overall level of resources (income + wealth)

Higher income, lower taxes, higher wealth all increase consumption.

Expectations about the future matter.

v Consumers tend to smooth transitory fluctuations in income.

This leads to an intertemporal allocation of resources over time: e.g. winning a lottery or planning for retirement leads to a reallocation of income over time to maintain consumption stable.

v The interest rate is the relative price of the future vs. the present.

Higher interest rates make consumption in the present less attractive and it tends to lead to a reduction in consumption (although there are income effects that might go in the opposite direction).

Theory: Consumption and Saving

Macroeconomics in the Global Economy Antonio Fatás

Across emerging markets we see a wide range of values for the ratio of (private) consumption to income. Asian countries display low rates of consumption.

Consumption and Income

Country Consumption as % of GDP (2010)

Bolivia 62%

Chile 59%

Bulgaria 61%

France 58%

Malaysia 48%

China 35%

4

Macroeconomics in the Global Economy Antonio Fatás

Assignment

54 61 61

58 35

75 58

75 57

59 78

65 58

37 59

0 10 20 30 40 50 60 70 80 90

Australia Brazil

Bulgaria Canada

China Egypt

France Greece

India Japan

Lebanon Mexico

New Zealand Singapore

South Africa

Consumption (C) as % of GDP

2010

Macroeconomics in the Global Economy Antonio Fatás

Assignment

18 21

16 22

13 11

25 18

12 20

12 12

21 11

21

0 5 10 15 20 25 30

Australia Brazil

Bulgaria Canada

China Egypt

France Greece

India Japan

Lebanon Mexico

New Zealand Singapore

South Africa

Government Consumption (G) as % of GDP

2010

5

Macroeconomics in the Global Economy Antonio Fatás

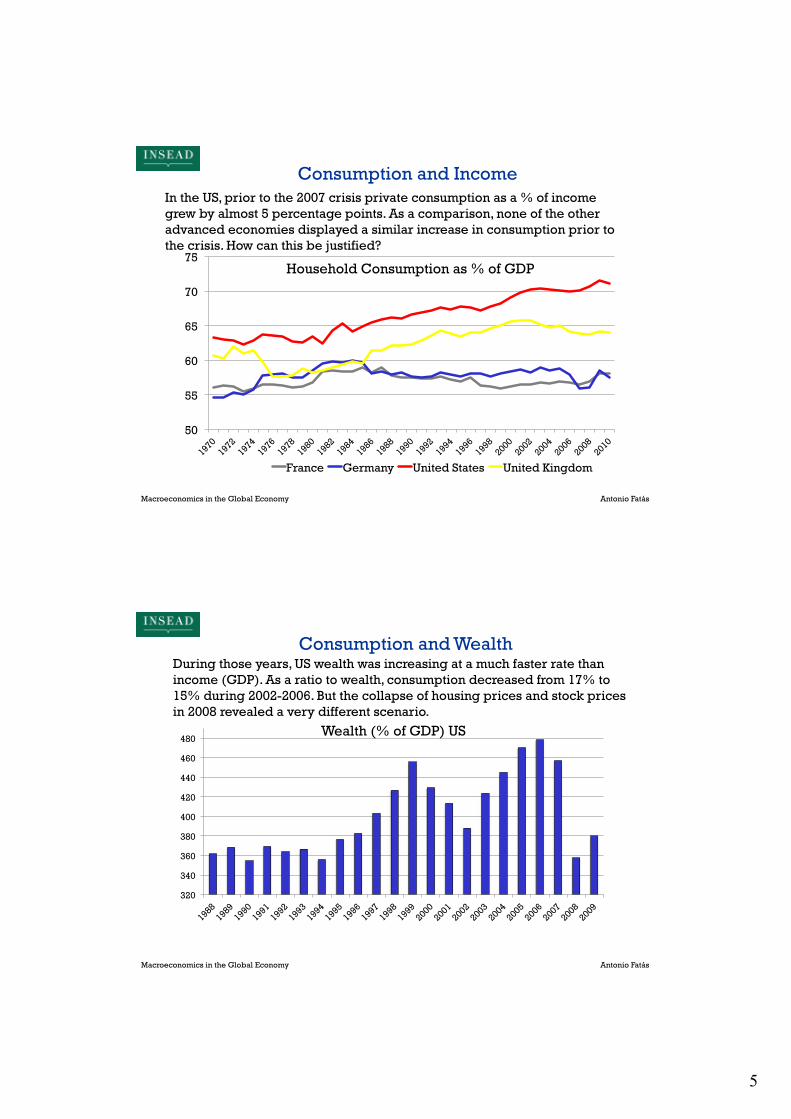

In the US, prior to the 2007 crisis private consumption as a % of income grew by almost 5 percentage points. As a comparison, none of the other advanced economies displayed a similar increase in consumption prior to the crisis. How can this be justified?

Consumption and Income

50

55

60

65

70

75 Household Consumption as % of GDP

France Germany United States United Kingdom

Macroeconomics in the Global Economy Antonio Fatás

Consumption and Wealth During those years, US wealth was increasing at a much faster rate than income (GDP). As a ratio to wealth, consumption decreased from 17% to 15% during 2002-2006. But the collapse of housing prices and stock prices in 2008 revealed a very different scenario.

320

340

360

380

400

420

440

460

480 Wealth (% of GDP) US

6

Macroeconomics in the Global Economy Antonio Fatás

r

Saving

Real Interest Rate

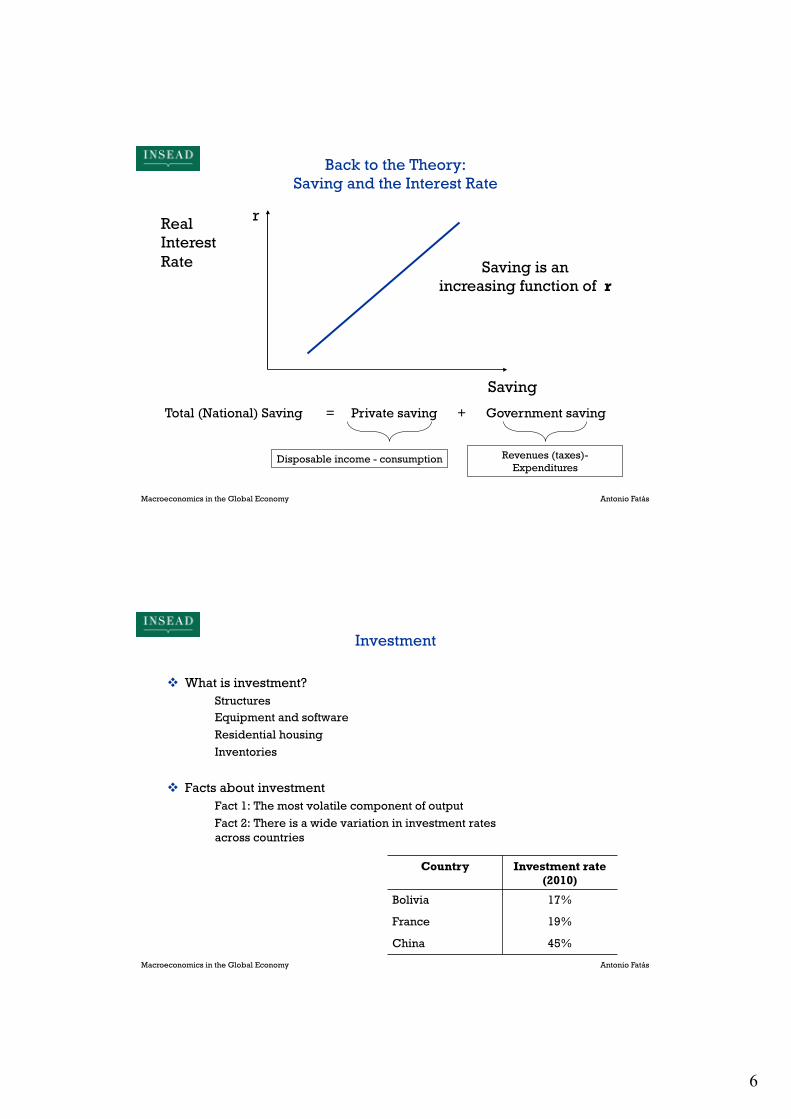

Back to the Theory: Saving and the Interest Rate

Saving is an increasing function of r

Total (National) Saving = Private saving + Government saving

Disposable income - consumption Revenues (taxes)- Expenditures

Macroeconomics in the Global Economy Antonio Fatás

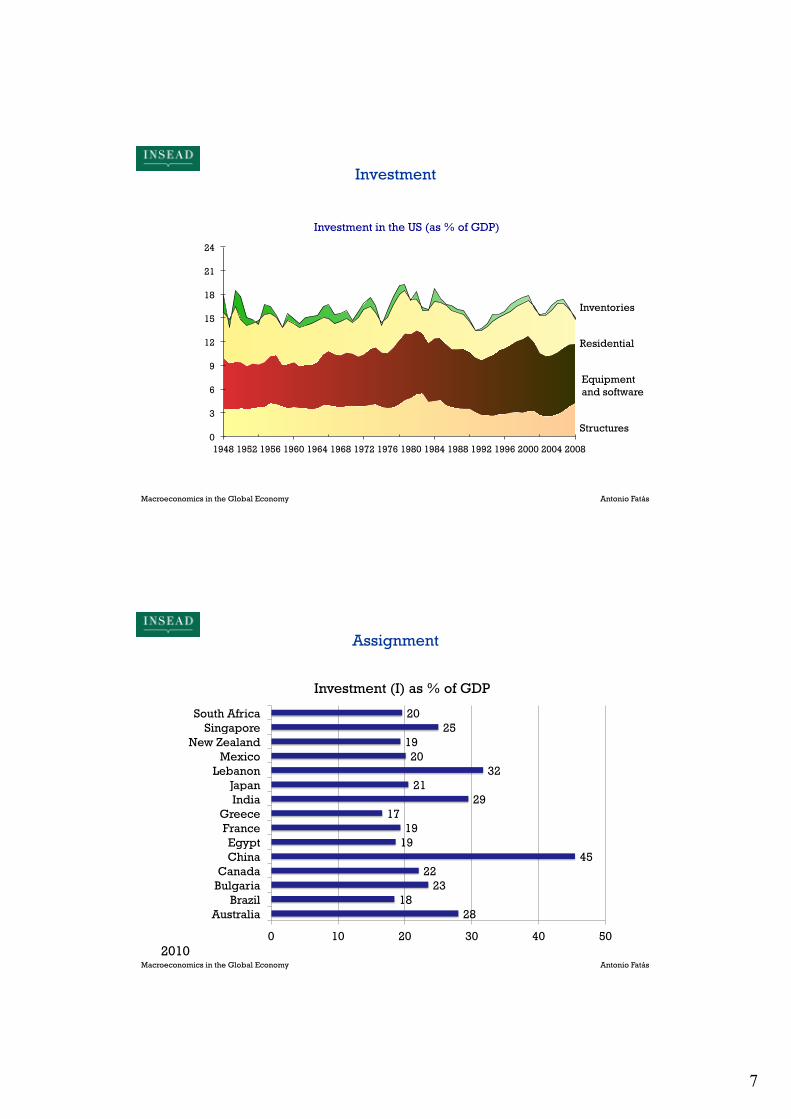

Investment

v What is investment? Structures Equipment and software Residential housing Inventories

v Facts about investment Fact 1: The most volatile component of output Fact 2: There is a wide variation in investment rates across countries

Country Investment rate (2010)

Bolivia 17%

France 19%

China 45%

7

Macroeconomics in the Global Economy Antonio Fatás

Investment

0

3

6

9

12

15

18

21

24

1948 1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

Investment in the US (as % of GDP)

Structures

Equipment and software

Residential

Inventories

Macroeconomics in the Global Economy Antonio Fatás

Assignment

28 18

23 22

45 19 19

17 29

21 32

20 19

25 20

0 10 20 30 40 50

Australia Brazil

Bulgaria Canada

China Egypt

France Greece

India Japan

Lebanon Mexico

New Zealand Singapore

South Africa

Investment (I) as % of GDP

2010

8

Macroeconomics in the Global Economy Antonio Fatás

Assignment

100 100 100 102

94 104

102 109

98 99

122 97 98

73 101

0.0 20.0 40.0 60.0 80.0 100.0 120.0 140.0

Australia Brazil

Bulgaria Canada

China Egypt

France Greece

India Japan

Lebanon Mexico

New Zealand Singapore

South Africa

C+I+G as % of GDP

2010

Macroeconomics in the Global Economy Antonio Fatás

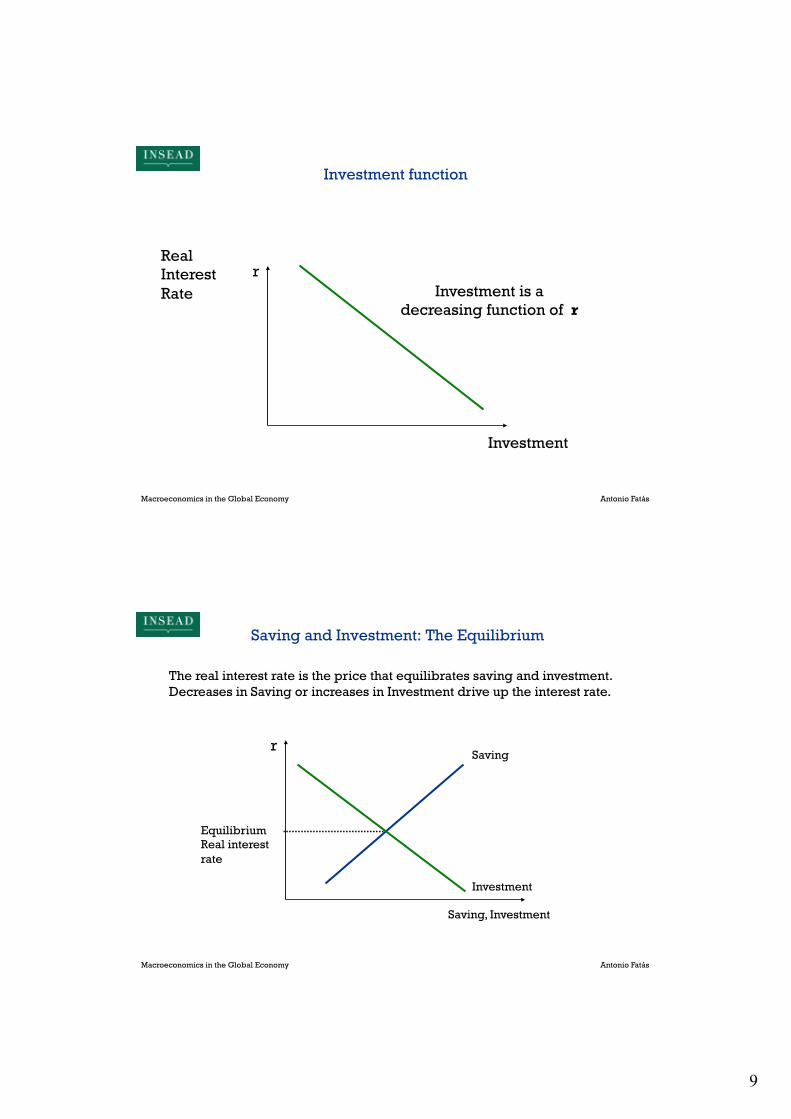

Theory: Investment and the interest rate

v Investment depends negatively on real interest rate, the nominal interest rate corrected for inflation.

v The real interest rate reflects:

the cost of borrowing the opportunity cost of using one’s own funds to finance investment

spending.

So, ↑↑r ⇒⇒ ↓↓I v In addition: Investment is affected by expected future profitability of

capital (productivity, taxes)

9

Macroeconomics in the Global Economy Antonio Fatás

Investment is a decreasing function of r

r

Investment

Real Interest Rate

Investment function

Macroeconomics in the Global Economy Antonio Fatás

r

Saving, Investment

Investment

Saving

Equilibrium Real interest rate

Saving and Investment: The Equilibrium

The real interest rate is the price that equilibrates saving and investment. Decreases in Saving or increases in Investment drive up the interest rate.

10

Macroeconomics in the Global Economy Antonio Fatás

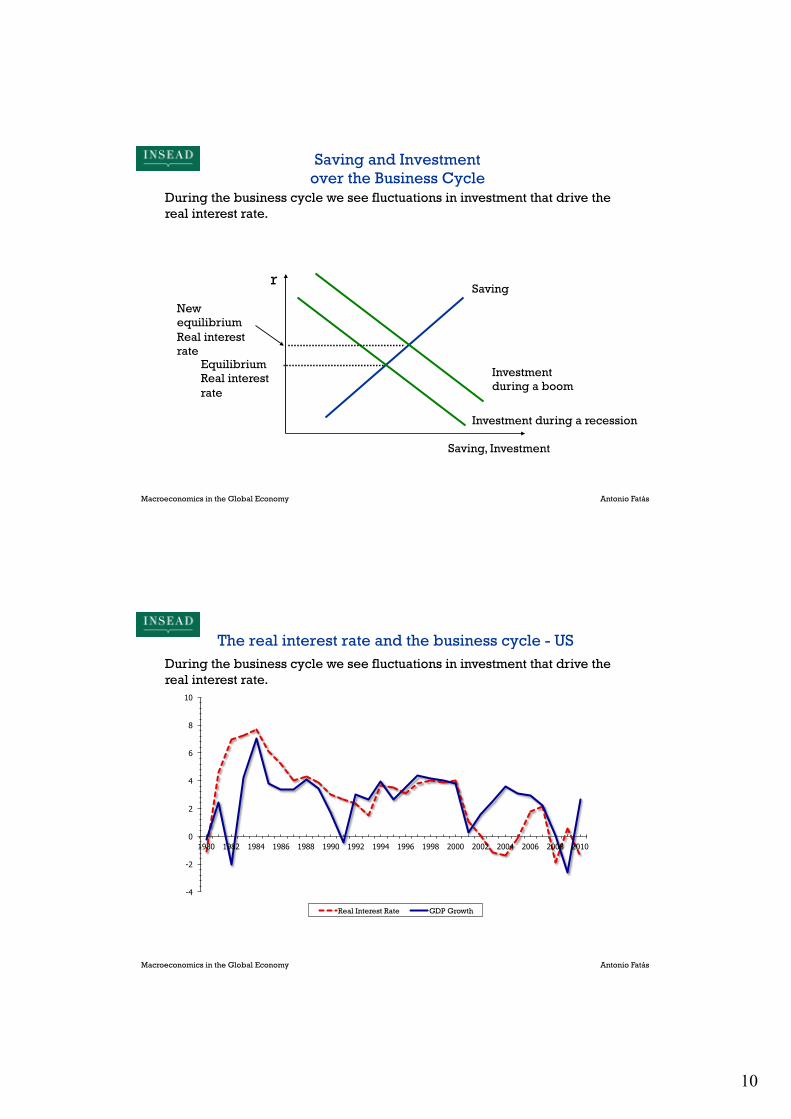

r

Saving, Investment

Investment during a recession

Saving

Equilibrium Real interest rate

New equilibrium Real interest rate

Investment during a boom

Saving and Investment over the Business Cycle

During the business cycle we see fluctuations in investment that drive the real interest rate.

Macroeconomics in the Global Economy Antonio Fatás

The real interest rate and the business cycle - US

-4

-2

0

2

4

6

8

10

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Real Interest Rate GDP Growth

During the business cycle we see fluctuations in investment that drive the real interest rate.

11

Macroeconomics in the Global Economy Antonio Fatás

r

Saving, Investment

Investment

Saving (1990s)

Equilibrium Real interest rate

Saving Glut

“To be more specific, I will argue that over the past decade a combination of diverse forces has created a significant increase in the global supply of saving--a global saving glut--which helps to explain the relatively low level of long-term real interest rates in the world today” Ben Bernanke, March 10, 2005.

Saving (2000s)

Macroeconomics in the Global Economy Antonio Fatás

r

Saving, Investment

Investment

Saving

Equilibrium Real interest rate

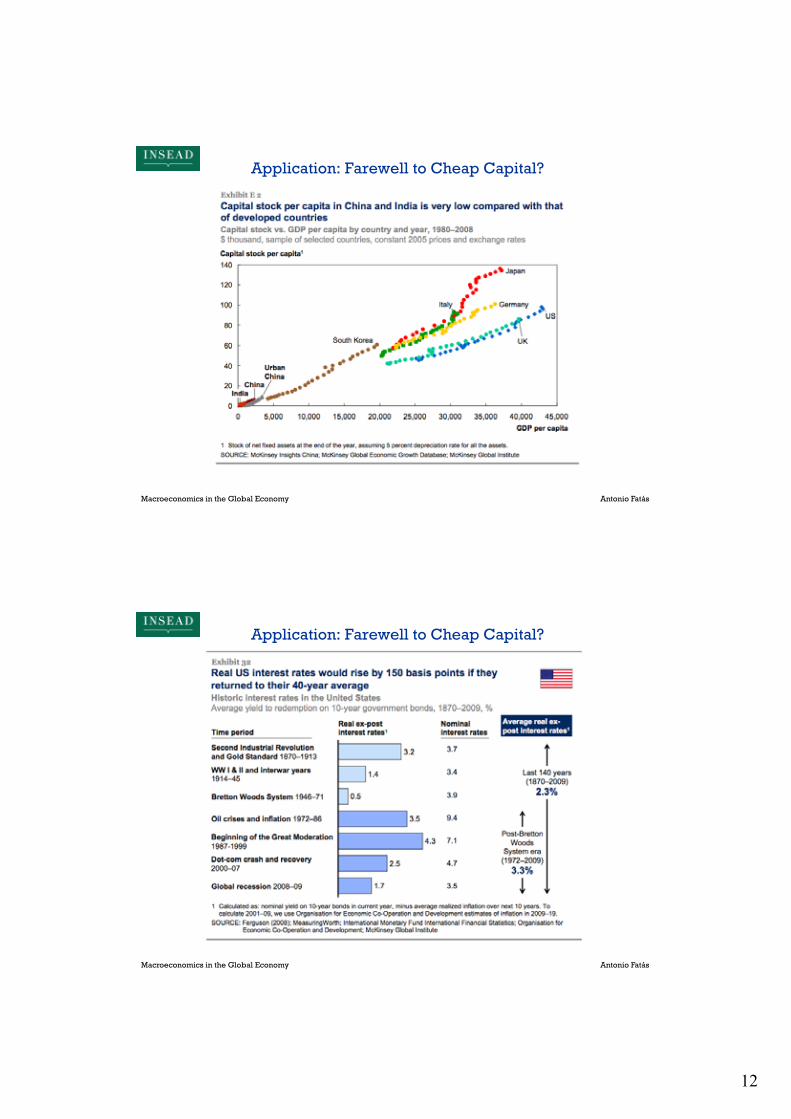

Application: Farewell to Cheap Capital?

Going forward we might see increases in investment in emerging countries, possibly combined with increases in consumption in China (lower saving). Among advanced economies we see a trend towards deleveraging (higher saving), but looking beyond the next 5 years we will see an increasing number of workers reaching retirement and using their savings to fund their consumption. What will world (real) interest rates do?

12

Macroeconomics in the Global Economy Antonio Fatás

Application: Farewell to Cheap Capital?

Macroeconomics in the Global Economy Antonio Fatás

Application: Farewell to Cheap Capital?

13

Macroeconomics in the Global Economy Antonio Fatás

Session 2. Summary

Saving curve is shifted to the right if:

Investment curve is shifted to the right if:

1. Current output increases 2. Expected future output decreases 3. Wealth decreases 4. Taxes increase 5. Government spending decreases

1. (Expected) productivity increases. 2. Taxes on capital decrease.

v Saving depends positively on interest rates: If interest rates increase people save more.

v Investment depends negatively on interest rates: If interest rates increase, companies invest less.

v The Real Interest Rate is the price that ensures that Saving = Investment

Macroeconomics in the Global Economy Antonio Fatás

Appendix: Consumption and the interest rate

v Income effect If consumer is a saver, a higher interest rate makes him/her better off, which tends to increase consumption today and in the future.

v Substitution effect An increase in the interest rate increases the opportunity cost of current consumption, which tends to reduce today’s consumption and increase future consumption.

v Both effects lead to increase in future consumption Whether today’s consumption increases or falls depends on the relative size of the income & substitution effects.

14

Macroeconomics in the Global Economy Antonio Fatás

r

Saving, Investment

Investment

New equilibrium real rate

Saving

Equilibrium real rate

War

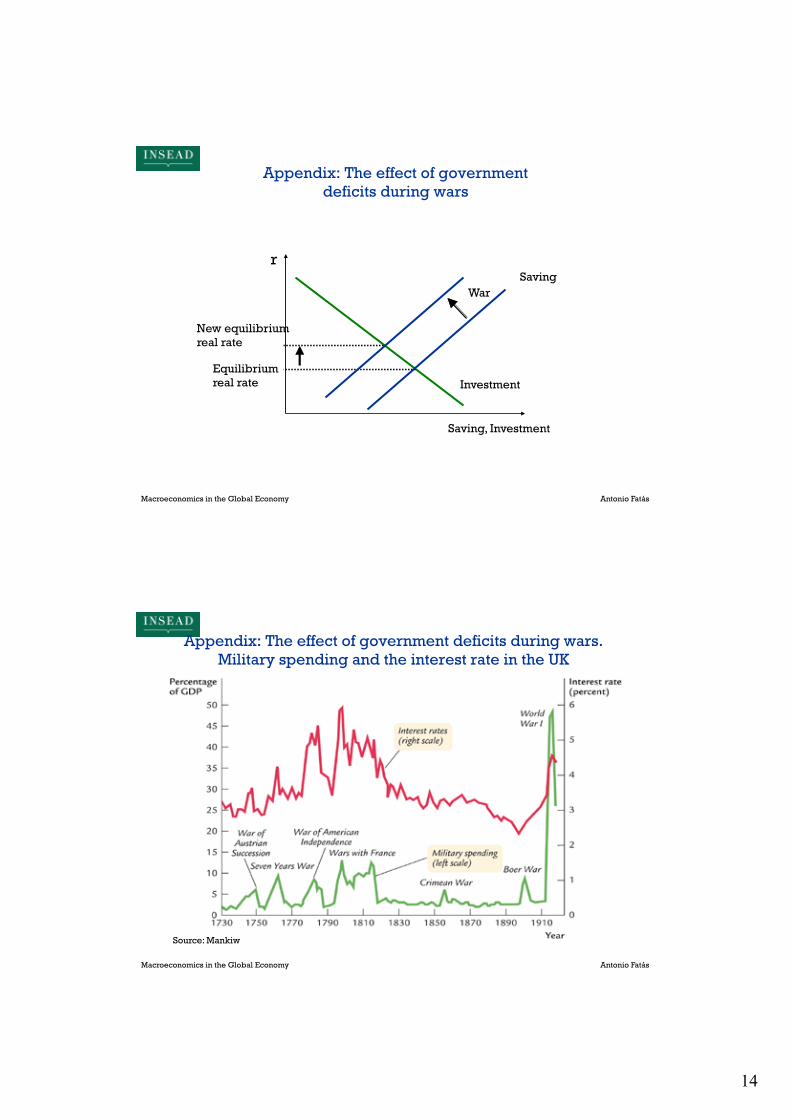

Appendix: The effect of government deficits during wars

Macroeconomics in the Global Economy Antonio Fatás

Appendix: The effect of government deficits during wars. Military spending and the interest rate in the UK

Source: Mankiw

15

Macroeconomics in the Global Economy Antonio Fatás

A builds a house that he sells to B. The value of the

house is $1,000. B sells food to A for a total of $500. To be able to pay for the house, B borrows $500 from

his bank. A’s income for the year is $1000 out of which she

spends $500on food. She keeps the rest ($500) on her bank account. Calculate: GDP, Consumption, Investment and Saving for each individual and for the economy. Is saving equal to investment?

Exercise: Making sure that investment = saving (in a closed economy)