russia rebalances its economic focus _ update 16 may 2016

TRANSCRIPT

follow us onThis material contains confidential and/or official information. The terms and conditions governing its use can be found at www.iesingapore.gov.sg/Terms-of-Use.

RUSSIA REBALANCES ITS

ECONOMIC FOCUS:

Opportunities And Strategies To Enter The Market

Gwyneth TanCentre Director, Moscow Overseas Centre

16 May 2016, Sapphire Room, Lotte Hotel, Moscow, Russian Federation

HOUSEKEEPING

Presentation slides

Acrobat files of the slides will be sent to you after this

week.

Hyperlinks are embedded in logos and images used

throughout the deck. Click on the logo or image to go to the

website for more information.

OUTLINE

RUSSIA REBALANCES ITS ECONOMIC FOCUS:

Opportunities and Strategies to Enter the Market

A word about IE Moscow

Snapshot of Russia

Why still Russia? Why not Russia?

Opportunities in adversity

Succeeding in the Russian marketplace

Summing it up

Questions?

A word about IE Moscow

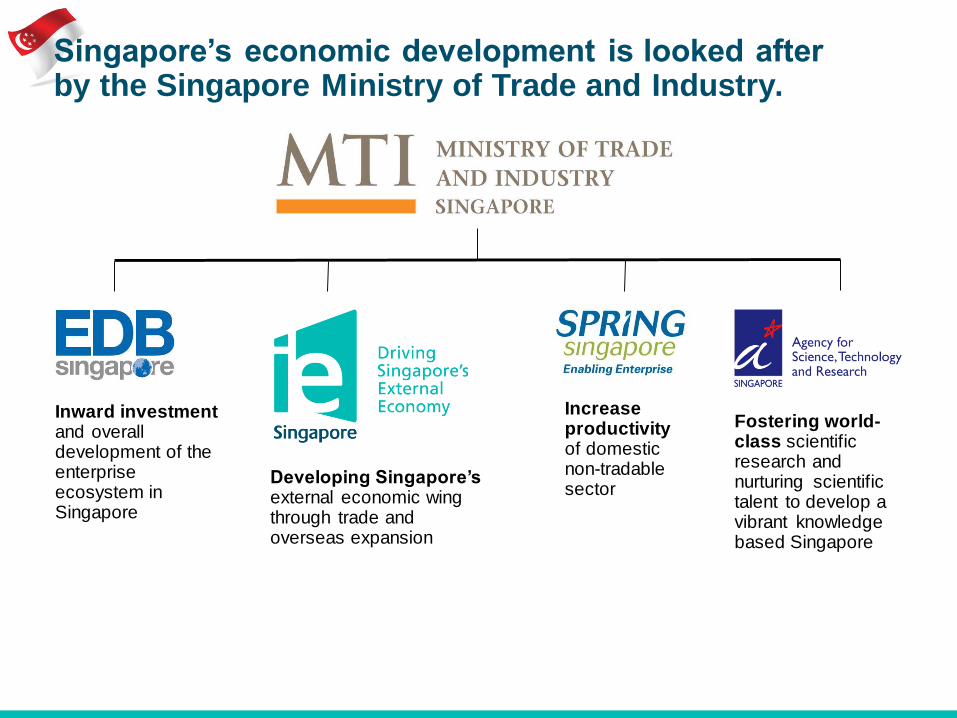

Singapore’s economic development is looked after by the Singapore Ministry of Trade and Industry.

Inward investment and overall development of the enterprise ecosystem in Singapore

Increase productivity of domestic non-tradable sector

Fostering world-class scientific research and nurturing scientific talent to develop a vibrant knowledge based Singapore

Developing Singapore’s external economic wing through trade and overseas expansion

Our Mission

To promote overseas growth ofSingapore-based enterprisesand international trade

Our Vision

A thriving business hub withglobally competitive enterprisesand leading international traders

IE Singapore serves our economy through our global network

AMERICAS

Los Angeles

Mexico City

New York

São Paulo

Singapore HQ + 39 offices worldwide

EUROPE

Frankfurt

Istanbul

London

Moscow

MIDDLE EAST

& AFRICA

Accra

Abu Dhabi

Doha

Dubai

Jeddah

Johannesburg

Riyadh

CHINA

North China

Beijing

Dalian

Qingdao

South China

Guangzhou

Wuhan

East China

Shanghai

West China

Chengdu

Chongqing

Xian

NORTH ASIA

& PACIFIC

Seoul

Sydney

Taipei

Tokyo

SOUTH ASIA

Chennai

Mumbai

New Delhi

SOUTHEAST

ASIA

Bangkok

Hanoi

Ho Chi Minh City

Jakarta

Kuala Lumpur

Manila

Surabaya

Yangon

Operating in Moscow since 2006:

Constitutes the Commercial Department of Singapore Embassy in Russia

Historically, operated by 1 Centre Director, 1 Business Development Manager, 1 Centre Secretary, 1 Driver.

Collaborates across Singapore ministries, agencies and NGOs to advance economic bilateral ties and cross

border business with Russia, Ukraine and Belarus

Cultivate and engages globally competitive Russian companies for anchoring in Singapore and Russian partners

to do business with Singapore companies.

Your IE Moscow team today:

IE Singapore Moscow Overseas Centre

Maxim ChulkovSenior Key Account

Manager

Artur KarlovBusiness Development

Manager

Diana BelyaevaBusiness Development

Manager

Victoria AraslanovaProtocol & Admin

Officer

Gwyneth TanCentre Director & Commercial Secretary

2013-2016

Raheed NargundRegional Director & Commercial Counsellor

2016 and beyond!

Alexander “Sasha” SertChauffeur & Logistics

Snapshot of Russia

Snapshot of Russia.

Official name:

Russian Federation

Area: 17,000,000 km2

No. of regions: 83

(Singapore does not

recognise Republic of Crimea

and Sevastopol City as part

of Russia)

Total population:

143,800,000 pax

Major cities:

Moscow (10.1 mln pax)

St Petersburg (4.7 mln pax)

Novosibirsk (1.4 mln pax)

Nizhny Novgorod (1.3 mln

pax)

Yekaterinburg (1.3 mln pax)

Current President:

Vladimir Putin

Current Prime Minister:

Dmitry Medvedev

Russia’s top banks:

Russia’s O&G + Defense + Dual-tech majors:

Snapshot of Russia.

2014 sectoral sanctions cut off Russia’s access to key Western resources for

developing and growing key sectors of its economy:

Note! Consult proper sanctions lawyers

to understand your specific case.

Snapshot of Russia.

Russia’s counter sanctions cut off a significant supply of staple food

imports which form the Russian basic diet:

• Fresh and frozen meat and smoked meat products (excluding canned

versions)

• Fresh and frozen poultry and processed poultry products (excluding

canned versions)

• Milk and dairy products

• Fresh and frozen fish and seafood

• Fresh vegetables, edible roots and tubers, fruits and nuts

Note! Consult proper sanctions lawyers

to understand your specific case.

Why still Russia? Why not Russia?

2014 2015

Interest rate: 17% 11%

GDP: US$1.86 tn US$1.2 tn

GDP growth: 0.6% -3.7%

Inflation: 7.8% 12.9%

Unemployment rate: 5.2% 5.8%

Total foreign direct investments: US$23.6 bn US$2 bn

Total exports: US$520.3 bn US$345.9 bn

Total imports: US$323.9 bn US$193 bn

Recent macroeconomic indicators of Russia:

Legend:

Green = improvement

Red = Decline

Looks like bad news… or is it?

In 2014, Western sanctions and plunging global oil prices struck a double blow to its

already slowing economy.

2010 2011 2012 2013 2014 2015

4.5% 4.3% 3.4%1.3%

0.6% Slight GDP contraction in 2015.

% growth

GDP

2010 2011 2012 2013 2014 2015

70bn55bn 50bn43bn

23bn

US$

FDIForeign direct investments

all but dried up.

US$105 US$38

Oil prices

plunged more

than 70% from

2014 to 2015.

-3.7%

2bn

In 2015, World Bank

expects Russia’s GDP

to contract over the

next 2 years.

On 11 May 2016, the EBRD expects Russia’s recession

to bottom out by end 2016 and the economy to return to

growth of around 1% in 2017 as oil prices recover.

…these?

Why not Russia? Is it because of…

Scary strong man. Scarier, stronger men. Dangerous beauty. Even more dangerous beauty.

Or these?

Realities behind top 3 perceptions of Russia. (1/3)

Perception 1: Putin is evil. As long as he is in power, we can’t do business in Russia.

Key takeaways for foreign businessmen:

A Russia ruled by a Strong Man backed by cohesive domestic support

and a fearsome military means:

No fear of social unrest – Russian citizens believe in their leader.

No fear of terrorist disruptions – Terrorists are effectively deterred.

No need for martial law – Post USSR Russia never needed it.

All the above lead to stable conditions for long-term business.

Perception 2: Russia is too corrupt. We can’t do business in Russia.

Realities behind top 3 perceptions of Russia. (2/3)

Food for thought:

Corruption is

everywhere: Out of 177

markets ranked by CPI,

only 14 or 7.8% are

developed markets

where corruption is

supposedly low or zero.

Even developed

markets export

corruption abroad.

Many developed

markets pose entry

barriers in terms of

market saturation,

established or

entrenched rival brands,

and protectionism.

Food for thought: Is it time

for Singapore businesses to

gain more sophisticated

firm-level capability for

handling corruption?

Realities behind top 3 perceptions of Russia. (3/3)

Perception 3: Russia is under sanctions. We can’t do business in Russia.

First thing Singapore should know about the sanctions:

1. EU and US sanctions on Russia are unilateral. They are not issued through UN resolution.

2. Singapore complies only with UN resolutions. Therefore the current sanctions on Russia

are not applicable to Singapore or Singapore entities.

3. Singapore does not join in unilateral sanctions imposed by one nation against another

outside of UN resolutions.

Second thing Singapore should know about the sanctions:

1. EU and US sanctions on Russia are imposed on specific Russian individuals, specific Russian

companies and specific Russian business activity, technology, know-how, and equipment.

2. EU and US sanctions do not bar everything under the sun.

Russia’s top banks:All EU & US

banks

Russia’s top enterprises:All EU & US O&G

+ dual tech

suppliers

Note! Consult

proper sanctions

lawyers to

understand your

specific case.

Tip! In Russia you need

to invest time and

resources to entertain

your customers. While

Russians like the

showiness, more

importantly they need

this to test your character

and get to know you.

Why Russia then?

Great place for business meetings: Moscow never sleeps. Today, it is a humming metropolis that

offers luxury to outlandish choices for you to entertain your customers.

Good eating and entertainment: Who says Russia doesn’t have good food?

Tip! In Russia,

dining out is about

being seen, showing

that you have

arrived. Self service

affairs are called

canteens, meant for

the poor and fast

food. Therefore, be

mindful of where you

take your guests!

Note! Russia ranks below

only 2 Asian markets and

above all African

markets!

Why Russia then?

World Bank’s Ease of Doing Business Index 2016: Russia ranks 6th out of all emerging

markets of Asia, Africa, Middle East and Latin America.

Southeast Asia 2014 2015

Malaysia 17 18

Thailand 46 49

Russia 54 51

Vietnam 93 90

Brunei 105 84

Philippines 97 103

Indonesia 120 109

Cambodia 133 127

Laos 139 134

Papua New Guinea 141 145

Timor-Leste 167 173

Myanmar 177 167

South Asia 2014 2015

Russia 54 51

Sri Lanka 113 107

India 134 130

Pakistan 136 138

Bangladesh 172 174

Emerging North Asia 2014 2015

Russia 54 51

Mongolia 59 56

Bhutan 70 71

China 83 84

Nepal 94 99

Latin America & Africa 2014 2015

Mexico 42 38

Chile 48 48

Peru 45 50

Russian Federation 54 51

Colombia 52 54

Puerto Rico 56 57

Rwanda 55 62

South Africa 69 73

Rest of Africa & Latin America 70-189 74-189

Middle East & Turkey 2014 2015

United Arab Emirates 32 31

Russian Federation 54 51

Israel 50 53

Turkey 51 55

Bahrain, Qatar, Oman, Saudi

Arabia, Kuwait, Jordan, Iran,

Lebanon, Egypt, West Bank and

Gaza, Iraq, Yemen, Syria,

Afghanistan

61-175 65-177

BRICS (Saudi / S. Africa) 2014 2015

Russian Federation 54 51

South Africa 69 73

Saudi Arabia 84 82

China 83 84

Brazil 111 116

India 134 130

Why Russia then?

Russia’s corporate tax rate is 20%: This is lower than the averages of most economic blocs.

Corporate tax rates: 20% Russia 20% in 2015 (steadily reduced from 43% in 2001)

Compare with: 20% Thailand, Cambodia, UK, Europe Average

25% Malaysia, Myanmar, Vietnam, Indonesia, China, Austria,

Netherlands, Colombia, Uraguay

26% Canada

28-29% Spain, Germany

30-31% Mexico, Philippines, Italy

33% France

34% Brazil, India

40% USA

Why Russia then?

Russia has proven itself to be capable of quickly managing financial crisis: Contrary to

popular news report, its economy did not collapse and is showing resilience to hold up under pressure.

RUB2.4 trillion

Anti-Crisis Plan

• 65% bank

recapitalisation

• 13.9% support of

enterprises which

account for 70%

of GDP

Prudent budget management:

• 10% cut in budget expenditure

for 2015

• Capping budget expenditure at

RUB15 trillion until 2017

Reserves (US$) 2014 2015 Change

RUSSIA386 bn 401 bn + 15 bn

GERMANY193 bn 194 bn + 1bn

USA132 bn 119bn - 13 bn

External Debt (US$) 2014 2015 Change

RUSSIA681 bn 515.3 bn - 165.7 bn

GERMANY3.6 tn 4.5 tn + 0.9 tn

USA17 tn 19 bn + 2 tn

Why Russia then?

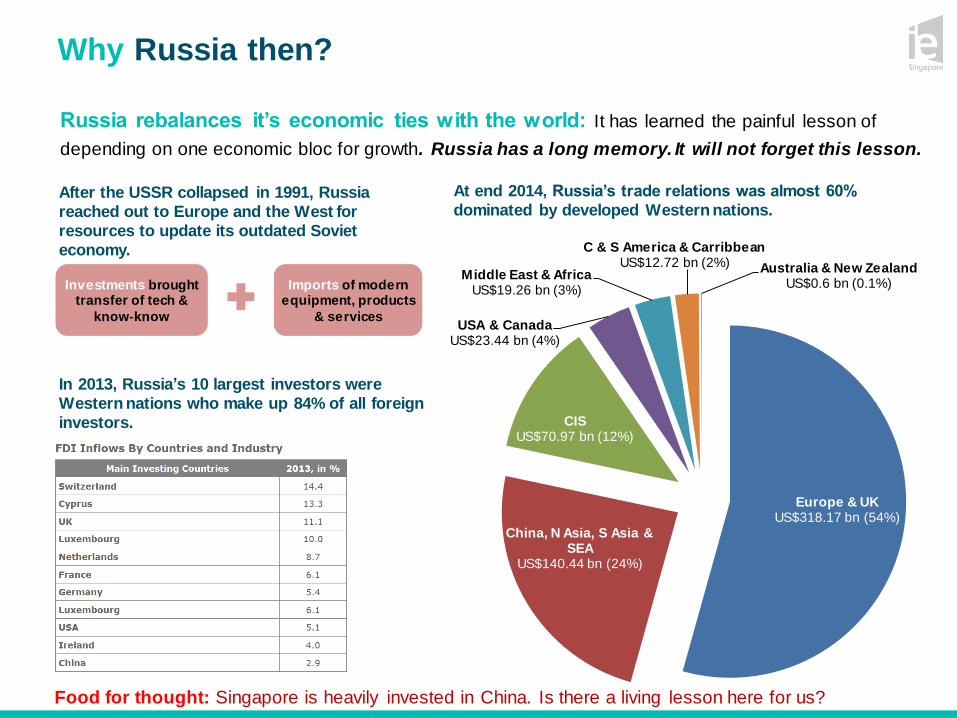

Russia rebalances it’s economic ties with the world: It has learned the painful lesson of

depending on one economic bloc for growth. Russia has a long memory. It will not forget this lesson.

Europe & UKUS$318.17 bn (54%)

China, N Asia, S Asia & SEA

US$140.44 bn (24%)

CIS US$70.97 bn (12%)

USA & CanadaUS$23.44 bn (4%)

Middle East & AfricaUS$19.26 bn (3%)

C & S America & CarribbeanUS$12.72 bn (2%) Australia & New Zealand

US$0.6 bn (0.1%)

At end 2014, Russia’s trade relations was almost 60%

dominated by developed Western nations.After the USSR collapsed in 1991, Russia

reached out to Europe and the West for

resources to update its outdated Soviet

economy.

In 2013, Russia’s 10 largest investors were

Western nations who make up 84% of all foreign

investors.

Investments brought transfer of tech &

know-know

Imports of modern equipment, products

& services+

Food for thought: Singapore is heavily invested in China. Is there a living lesson here for us?

Why Russia then?

Russia looks East. First. Russia’s rebalancing of economic ties starts with Asia first. This extends to

Singapore. This shift is unprecedented. A critical window has opened for Singapore to secure long-term

traction in the market before competition heats up.

Why Russia then?

Russian market is diversifying with new players: While many Western SMEs have pulled out,

long-time Western MNCs have expanded operations by repositioning themselves to capture rising volume of

mass market consumption in growth spots. In the meantime, China and Thailand are coming in strong.

Invested US$165 mil in cosmetics production facility.

Invested US$35 mil in auto parts production plant.

Invested US$400 mil to expand auto plant.Invested US$1 billion as at 31 December 2015 including a

US$27 mil pig-breeding farm.

Won tender to construct fibre optic

communication in Russia Far East.

Commenced building auto plant in

Tula Region.

Opportunities in adversity

Prior to 2014, 54% (US$318.2

bn) of Russia’s overseas trade

is with Europe and UK.

Only US$110.8 bn is with

China, Japan and Korea.

While US$15.8 bn is with

Southeast Asia.

There is much room to capture

more Russia-Asia trade flows

from which Singapore traders

can also benefit.

US$15.8 bn

US$110.8bnUS$110.8bnUS$110.8bn

Russia turns towards Asia for new trade flows.

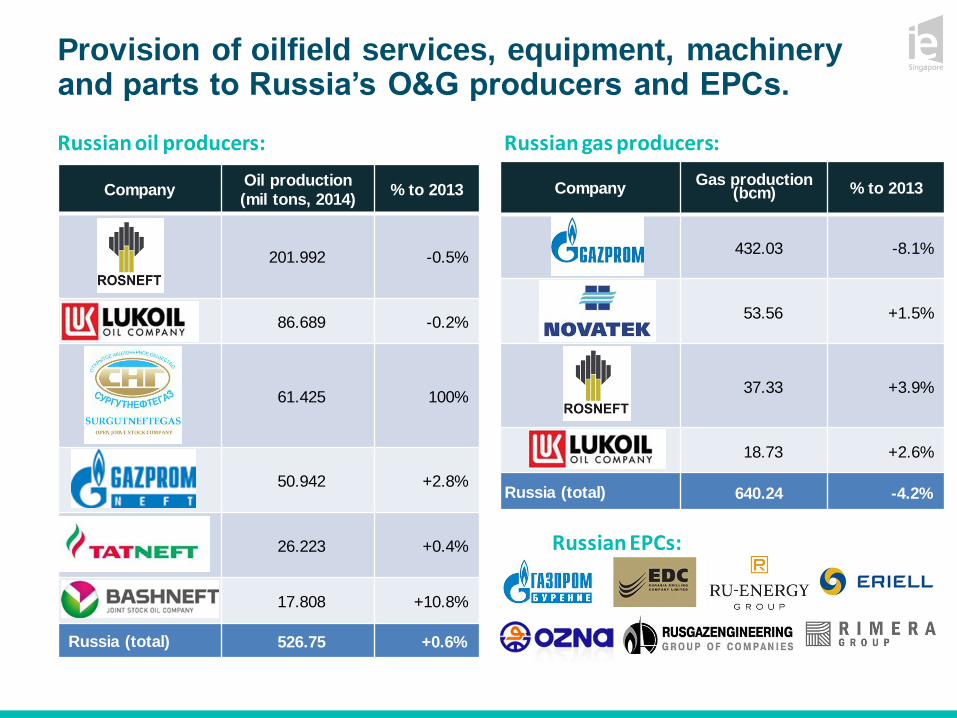

Provision of oilfield services, equipment, machinery and parts to Russia’s O&G producers and EPCs.

CompanyGas production

(bcm) % to 2013

432.03 -8.1%

53.56 +1.5%

37.33 +3.9%

18.73 +2.6%

Russia (total) 640.24 -4.2%

CompanyOil production

(mil tons, 2014)% to 2013

201.992 -0.5%

86.689 -0.2%

61.425 100%

50.942 +2.8%

26.223 +0.4%

17.808 +10.8%

Russia (total) 526.75 +0.6%

Russian oil producers: Russian gas producers:

Russian EPCs:

Staple food item Annual shortage (tonnes)

Beef (fresh, chilled and frozen) 59,050

Pork (fresh, chilled and frozen) 450,790

Poultry 338,730

Fish and seafood 457,190

Milk and dairy products 428,790

Vegetables 914,730

Fruits and nuts 1,599,570

Potential food trade as Singapore is unaffected by Russia’s import ban.

More than 50% rouble depreciation led to demand surge for mass market consumer offerings:

Russians continue to spend: Putting money away in savings is not a Russian characteristic, no

matter how bad the recession.

Domestic tourism demands:

Demand for low cost yet quality hotels, hostels, domestic destinations.

Economically priced yet hip F&B outlets:

Demand for healthy, tasty yet low cost mass market dining options.

Mass market consumer goods e.g. fast fashion:

Zara and Massimo Dutti stores giving way to Uniqlo and H&M.

Reasonably priced good quality baby products:

Russian parents would stinge on other areas to give their children the best.

Succeeding in the Russian marketplace

Tap on bilateral agreements and bilateral ties between Russia and Singapore to protect your investments and gain tax advantage.

Avoidance of Double Taxation Agreement (DTA)

Entered into force in 2009

Investment Promotion and Protection Agreement (IPPA)

Entered into force in 2012

Intergovernmental Commission (IGC)

Annual meeting co-Chaired by Russia’s 1st DPM Igor Shuvalov and Singapore’s DPM Tharman Shanmugaratnam

Next meeting in Singapore on 5 September 2016

Russia Singapore Business Forum (RSBF)

Annual flagship business forum driven by IE Singapore and graced by Russia’s 1st DPM Igor Shuvalov and Singapore’s DPM TharmanShanmugaratnam. Usually twinned with IGC.

1

Market is still

dominated by

large and complex

Russian and

Western entities

who share hard-

forged business

relationships built

over decades.

2

Recent economic

strain compels

Russia to seek

new business

partners –

window of

opportunity

opens for

Singapore to

secure hitherto

inaccessible

relationships.

3

Despite steady

improvements,

business

environment is still

complex – strong

local partners can

help navigate the

rules and market

practice.

4

Loyalty is long-

term in the

Russian business

perception – good

partners are

regarded as

friends for life.

Why? Russians do not trust easily. Hence it is very necessary to spend time to build relationships and trust with Russian business partners.

Strong relationships are paramount.

Why?

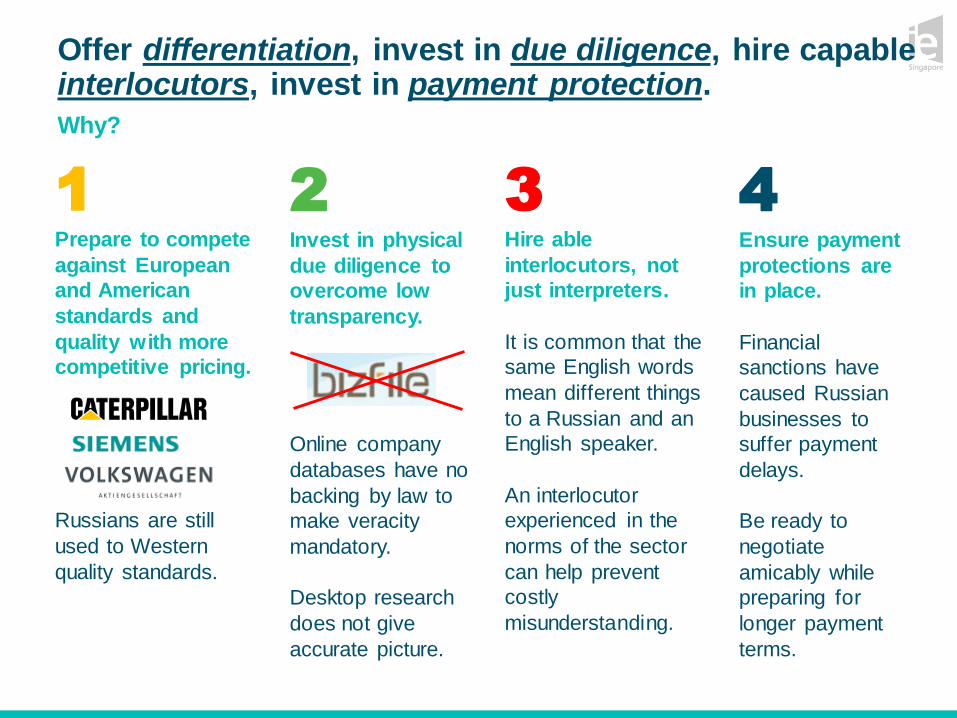

Offer differentiation, invest in due diligence, hire capable interlocutors, invest in payment protection.

4Ensure payment

protections are

in place.

Financial

sanctions have

caused Russian

businesses to

suffer payment

delays.

Be ready to

negotiate

amicably while

preparing for

longer payment

terms.

1Prepare to compete

against European

and American

standards and

quality with more

competitive pricing.

Russians are still

used to Western

quality standards.

3Hire able

interlocutors, not

just interpreters.

It is common that the

same English words

mean different things

to a Russian and an

English speaker.

An interlocutor

experienced in the

norms of the sector

can help prevent

costly

misunderstanding.

2Invest in physical

due diligence to

overcome low

transparency.

Online company

databases have no

backing by law to

make veracity

mandatory.

Desktop research

does not give

accurate picture.

Summing it up

In a nutshell:

4

Be aware of

massive

misreporting of

news about

Russia.

Balance your views

of Russia with these

other moderate

sources:

1

Russia and

businesses will

adjust to the new

environment.

Russia’s large

resource base and

highly specialised

talent pool will

provide stable

foundation for future

FDI and export

growth.

2

Singapore’s

competition in

Russia was

formerly from

Western players.

Going forward, Russia

will pay heed to maintain

diverse economic ties

with the world, not just

with the West.

There will be additional

competition soon from

China and North Asia

rivals.

3

The window period

for Singapore will

not last.

Russia’s pivot to Asia

does not mean Western

investors have left the

market place.

By end of 1Q2015, new

bargain hunters have

begun to fill the vacuum.

Over time, the Russian

marketplace is likely to

become more, not less

diverse, and more

competitive, offering

Russian customers a

wider choice of price

points and quality levels.

Questions?

Thank Youwww.iesingapore.com

This material contains confidential and/or official information. The terms and conditions governing its use can be found at www.iesingapore.gov.sg/Terms-of-Use.