royal dutch shell plc fourth quarter 2014 results analyst webcast presentation

TRANSCRIPT

1 Copyright of Royal Dutch Shell plc 29 January, 2015

FOURTH QUARTER 2014 RESULTS BALANCING GROWTH & RETURNS

29 JANUARY 2015 ROYAL DUTCH SHELL PLC

2 Copyright of Royal Dutch Shell plc 29 January, 2015

DEFINITIONS & CAUTIONARY NOTE

Reserves: Our use of the term “reserves” in this presentation means SEC proved oil and gas reserves.

Resources: Our use of the term “resources” in this presentation includes quantities of oil and gas not yet classified as SEC proved oil and gas reserves. Resources are consistent with the Society of Petroleum Engineers 2P and 2C definitions.

Organic: Our use of the term Organic includes SEC proved oil and gas reserves excluding changes resulting from acquisitions, divestments and year-average pricing impact.

Resources plays: Our use of the term ‘resources plays’ refers to tight, shale and coal bed methane oil and gas acreage.

The companies in which Royal Dutch Shell plc directly and indirectly owns investments are separate entities. In this document “Shell”, “Shell group” and “Royal Dutch Shell” are sometimes used for convenience where references are made to Royal Dutch Shell plc and its subsidiaries in general. Likewise, the words “we”, “us” and “our” are also used to refer to subsidiaries in general or to those who work for them. These expressions are also used where no useful purpose is served by identifying the particular company or companies. ‘‘Subsidiaries’’, “Shell subsidiaries” and “Shell companies” as used in this document refer to companies over which Royal Dutch Shell plc either directly or indirectly has control. Companies over which Shell has joint control are generally referred to as “joint ventures” and companies over which Shell has significant influence but neither control nor joint control are referred to as “associates”. The term “Shell interest” is used for convenience to indicate the direct and/or indirect ownership interest held by Shell in a venture, partnership or company, after exclusion of all third-party interest.

This presentation contains forward-looking statements concerning the financial condition, results of operations and businesses of Royal Dutch Shell. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Forward-looking statements include, among other things, statements concerning the potential exposure of Royal Dutch Shell to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions. These forward-looking statements are identified by their use of terms and phrases such as ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘intend’’, ‘‘may’’, ‘‘plan’’, ‘‘objectives’’, ‘‘outlook’’, ‘‘probably’’, ‘‘project’’, ‘‘will’’, ‘‘seek’’, ‘‘target’’, ‘‘risks’’, ‘‘goals’’, ‘‘should’’ and similar terms and phrases. There are a number of factors that could affect the future operations of Royal Dutch Shell and could cause those results to differ materially from those expressed in the forward-looking statements included in this presentation, including (without limitation): (a) price fluctuations in crude oil and natural gas; (b) changes in demand for Shell’s products; (c) currency fluctuations; (d) drilling and production results; (e) reserves estimates; (f) loss of market share and industry competition; (g) environmental and physical risks; (h) risks associated with the identification of suitable potential acquisition properties and targets, and successful negotiation and completion of such transactions; (i) the risk of doing business in developing countries and countries subject to international sanctions; (j) legislative, fiscal and regulatory developments including potential litigation and regulatory measures as a result of climate changes; (k) economic and financial market conditions in various countries and regions; (l) political risks, including the risks of expropriation and renegotiation of the terms of contracts with governmental entities, delays or advancements in the approval of projects and delays in the reimbursement for shared costs; and (m) changes in trading conditions. All forward-looking statements contained in this presentation are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Readers should not place undue reliance on forward-looking statements. Additional factors that may affect future results are contained in Royal Dutch Shell’s 20-F for the year ended 31 December, 2013 (available at www.shell.com/investor and www.sec.gov ). These factors also should be considered by the reader. Each forward-looking statement speaks only as of the date of this presentation, 29 January, 2015. Neither Royal Dutch Shell nor any of its subsidiaries undertake any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other information. In light of these risks, results could differ materially from those stated, implied or inferred from the forward-looking statements contained in this presentation. There can be no assurance that dividend payments will match or exceed those set out in this presentation in the future, or that they will be made at all.

We use certain terms in this presentation, such as discovery potential, that the United States Securities and Exchange Commission (SEC) guidelines strictly prohibit us from including in filings with the SEC. U.S. Investors are urged to consider closely the disclosure in our Form 20-F, File No 1-32575, available on the SEC website www.sec.gov. You can also obtain this form from the SEC by calling 1-800-SEC-0330.

3 Copyright of Royal Dutch Shell plc 29 January, 2015

BEN VAN BEURDEN CHIEF EXECUTIVE OFFICER

ROYAL DUTCH SHELL PLC

4 Copyright of Royal Dutch Shell plc 29 January, 2015

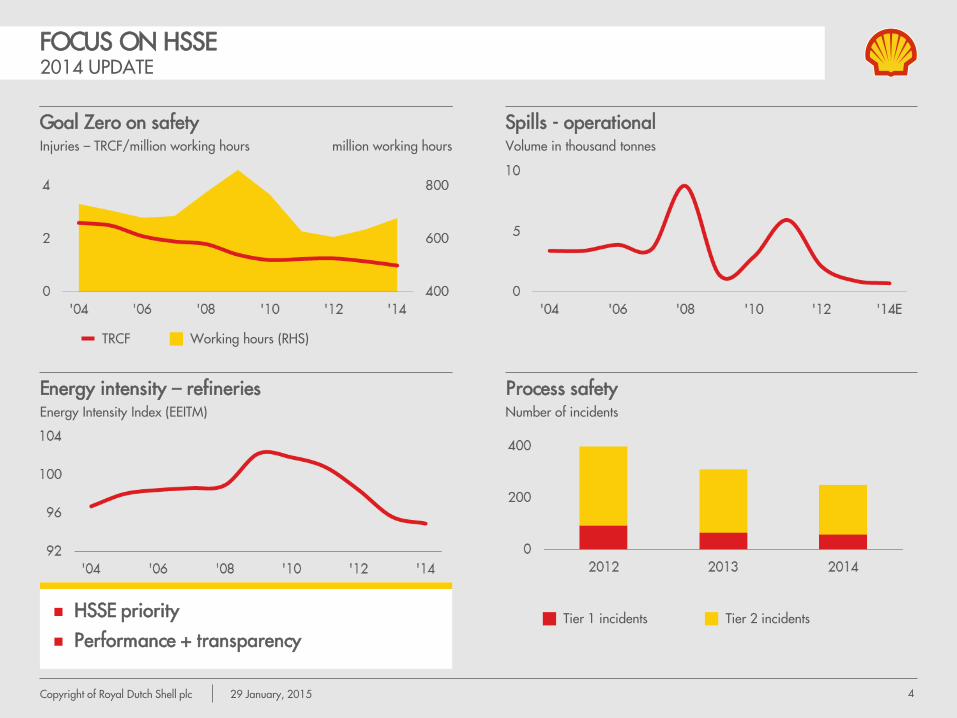

FOCUS ON HSSE 2014 UPDATE

Injuries – TRCF/million working hours

Goal Zero on safety Injuries – TRCF/million working hours

Spills - operational Volume in thousand tonnes

Energy intensity – refineries Energy Intensity Index (EEITM)

Process safety Number of incidents

million working hours

Working hours (RHS) TRCF

HSSE priority

Performance + transparency Tier 1 incidents Tier 2 incidents

5 Copyright of Royal Dutch Shell plc 29 January, 2015

EXECUTING A CONSISTENT, LONG-TERM STRATEGY

Unrelenting focus on HSSE

Technology, integration and scale

Disciplined capital investment by strategic theme

Growth in cash flow through cycle

Competitive shareholder returns

Total shareholder returns growth – 10 years Index 1/1/2005 =100

2014+ drive to rebalance growth and returns

Shell S&P500 FTSE100

6 Copyright of Royal Dutch Shell plc 29 January, 2015

2050 outlook

Population increases from 7 to 9 billion

Enabled by cheap and reliable energy

Realities

Requirement to mitigate climate change

Oil supply -70% by 2030 without new investment

Key role of gas & CCS

ENERGY TRANSITIONS

Long-term energy supply mix Million boe per day

Gas

Biomass Wind

Coal Nuclear Other renewables Solar

Shell activities Oil

Energy transitions underway

+50%

+50%

7 Copyright of Royal Dutch Shell plc 29 January, 2015

Oil market downturn

Entering 2015 with low oil prices

Requirement for $500 billion industry investment in upstream oil during 2014-20

Under-spending amplifies price spike risks

Shell response

Long-term $70 - $90 - $110 Brent oil price screens unchanged

Planning for low prices 2015+; uncertain recovery timing

Hard choices on our growth pipeline + options

Opportunity to reduce costs

OIL MARKET + SHELL RESPONSE

Source: IEA estimates

Oil supply Million barrels of oil per day

8 Copyright of Royal Dutch Shell plc 29 January, 2015

FINANCIAL PERFORMANCE 2014 DELIVERY

CCS earnings + ROACE excluding identified items

Earnings + ROACE $ billion

Cash flow $ billion

Dividend, buyback + gearing $ billion

%

%

Upstream Downstream

Corporate/Other

Dividend announced Buyback

CFFO CFFI ROACE (RHS)

Free cash flow (RHS)

Gearing (RHS)

$ billion

Gearing range

Well-positioned into oil market downturn

Asset sales delivered ahead of oil price decline

Enhanced free cash flow + lower gearing

9 Copyright of Royal Dutch Shell plc 29 January, 2015

2014 DELIVERY BALANCING GROWTH AND RETURNS

CCS earnings excluding identified items

CCS earnings $22.6 billion; CFFO $45.0 billion Dividend growth + buyback Restructuring in Oil Products + North America

resources plays

Moderated spending + growth Improved free cash flow; reduced gearing Early completion of 14-15 divestment plan

4 operated deep-water start-ups Repsol LNG integration: >$1 billion CFFO impact New options in FEED; improved exploration

Improve our financial performance

Enhance our capital efficiency

Deliver new projects

10 Copyright of Royal Dutch Shell plc 29 January, 2015

More rigorous portfolio management Taking hard choices on funnel

~140 performance units add focus

Increased shareholding requirements for management

Bottom line focus

Credible, competitive + affordable plans

Resilience

Attr

activ

enes

s

FEED FID On-stream

Identify&Assess Select Define Execute Operate ASPIRED PORTFOLIO

ATTRACTIVENESS

Growth & returns Opportunity scale

RESILIENCE

Risk, performance &

uncertainty

STRATEGIC INTENT

RESULTS & PAY-OUT

Grow

Exit

Fix/maintain

CHANGING EMPHASIS IN 2014+ SHARPER PORTFOLIO MANAGEMENT + APPRAISAL

11 Copyright of Royal Dutch Shell plc 29 January, 2015

PRIORITIES 2015+

Choices on new options

Supply chain management

Managing affordability + financial flexibility

Preserving our competitive growth pipeline in downturn

Continued ramp-up of 2014 start-ups

2015 transition year into 2016/17+ growth

Returns and cash flow

Competitive returns for shareholders

Restructuring underperforming businesses

Cost reduction programmes

Competitive financial performance

Capital efficiency Project delivery

12 Copyright of Royal Dutch Shell plc 29 January, 2015

COMPETITIVE FINANCIAL PERFORMANCE PORTFOLIO RESTRUCTURING

Optimise footprint

Integrated value capture

Selective investment in growth markets

Capital discipline and project delivery

Strong ROACE, 27% 2014

Free cash flow reduction:

Investment-heavy phase

Cost and profitability pressures

Late-life asset challenges

Resources plays

Oil Products Upstream engine

Dry gas Acquisitions LRS

NA portfolio reduction completed

2015+ reduction of International portfolio

Capital ceiling + cost reduction

Capital investment in $ billion

Asset sales (incl. MLP)

$ billion $ billion kboe per day (Shell share)

CFFO Production (RHS) Capital investment

-30%

13 Copyright of Royal Dutch Shell plc 29 January, 2015

COMPETITIVE FINANCIAL PERFORMANCE RESTRUCTURING RESOURCES PLAYS PORTFOLIO

Production excludes volumes from divestments

Production kboe per day

Capital investment $ billion

E&A On-stream

Gas Liquids Rich

Colombia

Argentina Neuquen

Ukraine

Oman Sichuan

Changbei

Arrow CBM

Changbei 2

Russia

Americas International Liquids Gas

Permian

Appalachia

W. Canada LRS

W. Canada gas

2014: North America portfolio restructured ($3.3 billion asset sales / 110 kboe/d)

2015+: International portfolio reduction

+ possible write-downs Potential to further reduce

spending

Tunisia

-30%

` Germany

Algeria Turkey

14 Copyright of Royal Dutch Shell plc 29 January, 2015

Cash flow + ROACE

COMPETITIVE FINANCIAL PERFORMANCE DOWNSTREAM ENGINE

CCS earnings excluding identified items

%

Earnings 2013 to 2014 $ billion

Operating performance % unplanned downtime

Cash flow ROACE (RHS)

Refining Chemicals

$ billion

Self-help + improved joint venture performance

Launched new cost drive at end 2014

10-12% ROACE + $10 billion p.a. CFFO potential

15 Copyright of Royal Dutch Shell plc 29 January, 2015

COMPETITIVE FINANCIAL PERFORMANCE PORTFOLIO RESTRUCTURING: OIL PRODUCTS

Equity refinery positions

Portfolio change

Resilience

Attr

activ

enes

s

Selective Growth: China LNG for transport Premium fuels + lubes Refinery crude flexibility others

Fix: Motiva Singapore fuels Pernis + Rheinland Malaysia Moerdijk others

Exit: Italy Australia Norway Denmark others

2014 asset sales + MLP: >$4 billion

Ongoing divestments

Efficiency + cost drive completed

Million b/d Refining capacity

Europe Asia, Oceania, Africa

Americas

~ -20%

# of refineries

Refineries (RHS)

16 Copyright of Royal Dutch Shell plc 29 January, 2015

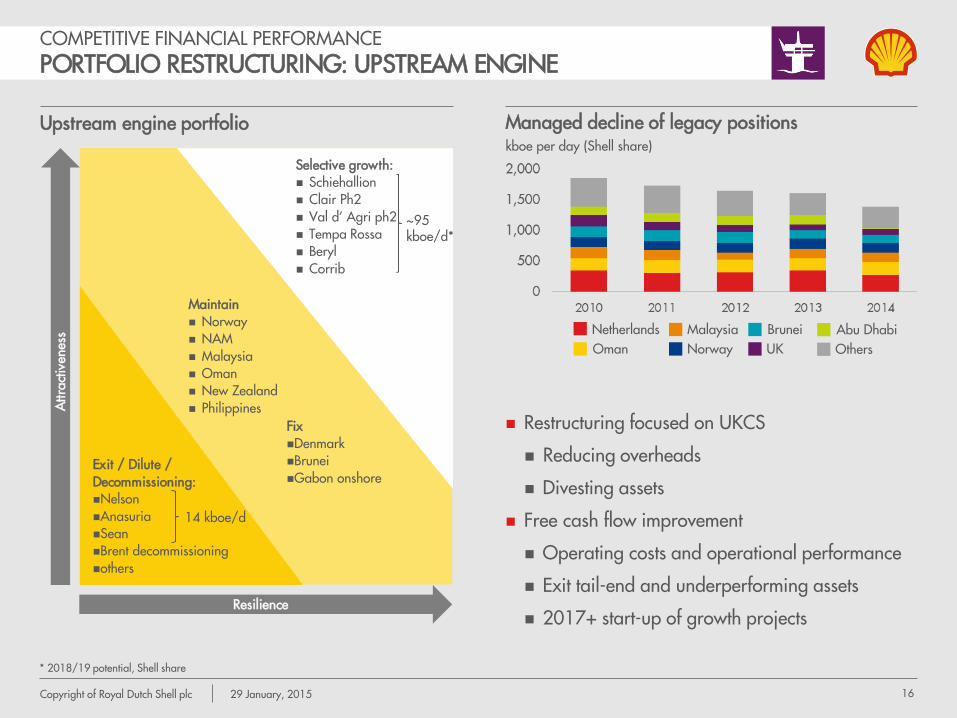

COMPETITIVE FINANCIAL PERFORMANCE PORTFOLIO RESTRUCTURING: UPSTREAM ENGINE

* 2018/19 potential, Shell share

Upstream engine portfolio

Managed decline of legacy positions kboe per day (Shell share)

Restructuring focused on UKCS

Reducing overheads

Divesting assets

Free cash flow improvement

Operating costs and operational performance

Exit tail-end and underperforming assets

2017+ start-up of growth projects Resilience

Attr

activ

enes

s

~95 kboe/d*

Selective growth: Schiehallion Clair Ph2 Val d’ Agri ph2 Tempa Rossa Beryl Corrib

Maintain Norway NAM Malaysia Oman New Zealand Philippines

Fix Denmark Brunei Gabon onshore

Exit / Dilute / Decommissioning: Nelson Anasuria Sean Brent decommissioning others

Netherlands Oman

Malaysia Norway

Brunei UK

Abu Dhabi Others

14 kboe/d

17 Copyright of Royal Dutch Shell plc 29 January, 2015

INVESTMENT PRIORITIES + PERFORMANCE

1 Iraq, Nigeria onshore (SPDC), Kazakhstan, Arctic, heavy oil

Engines (Downstream, Upstream engine)

Free cash flow businesses

Maintain competitiveness

Asset integrity + selective growth

Growth priority (Integrated Gas, deep water)

Global leadership established

High-grading our rich opportunity set

Longer term (resources plays, future opportunities1)

Major potential; managing non-technical risks

Slower pace + capital allocation

Investment choices driven on a global thematic basis Assets tested for attractiveness + resilience

ROACE (%)

CFFO in billion $

Downstream engine

Upstream engine

Integrated gas

Deep water

Resources plays Future opportunities

2014 (Brent $99/bbl)

2013 (Brent $109/bbl)

Bubble size represents year-end capital employed

18 Copyright of Royal Dutch Shell plc 29 January, 2015

COMPETITIVE, CREDIBLE + AFFORDABLE PLANS MODERATING OUR SPENDING + GROWTH OUTLOOK

2014 acquisitions: Repsol LNG

$ billion total capital investment $ billion organic capital investment

Project re-phasing / deferral

Supply chain savings

Dilutions + exits

> -15%

2015 organic spending lower than 2014

Retaining options for medium term

Flexibility to reduce further

Upstream

Downstream / Corporate

Acquisitions

2015 potential

2015 plan

19 Copyright of Royal Dutch Shell plc 29 January, 2015

ROYAL DUTCH SHELL PLC

SIMON HENRY CHIEF FINANCIAL OFFICER

20 Copyright of Royal Dutch Shell plc 29 January, 2015

ROYAL DUTCH SHELL PLC

FINANCIAL PERFORMANCE

21 Copyright of Royal Dutch Shell plc 29 January, 2015

Q4 2014 FINANCIAL HIGHLIGHTS

Earnings and ROACE on CCS basis, excluding identified items; ROACE 12 months rolling

Earnings Q4 2013 to Q4 2014 $ billion

Q4 2013

Q4 2014

$ billion UPSTREAM 2.5 1.7 DOWNSTREAM (CCS) 0.6 1.6

CORPORATE & MINORITIES (0.1) (0.0)

CCS NET EARNINGS 2.9 3.3

CCS EARNINGS, $ PER SHARE 0.46 0.52

CASH FROM OPERATIONS 6.0 9.6

ROACE (%) 8.9 10.2 SHARE BUYBACKS 1.0 1.0

DIVIDENDS 2.8 3.0

DIVIDEND, $ PER SHARE 0.45 0.47

Environment Choice

22 Copyright of Royal Dutch Shell plc 29 January, 2015

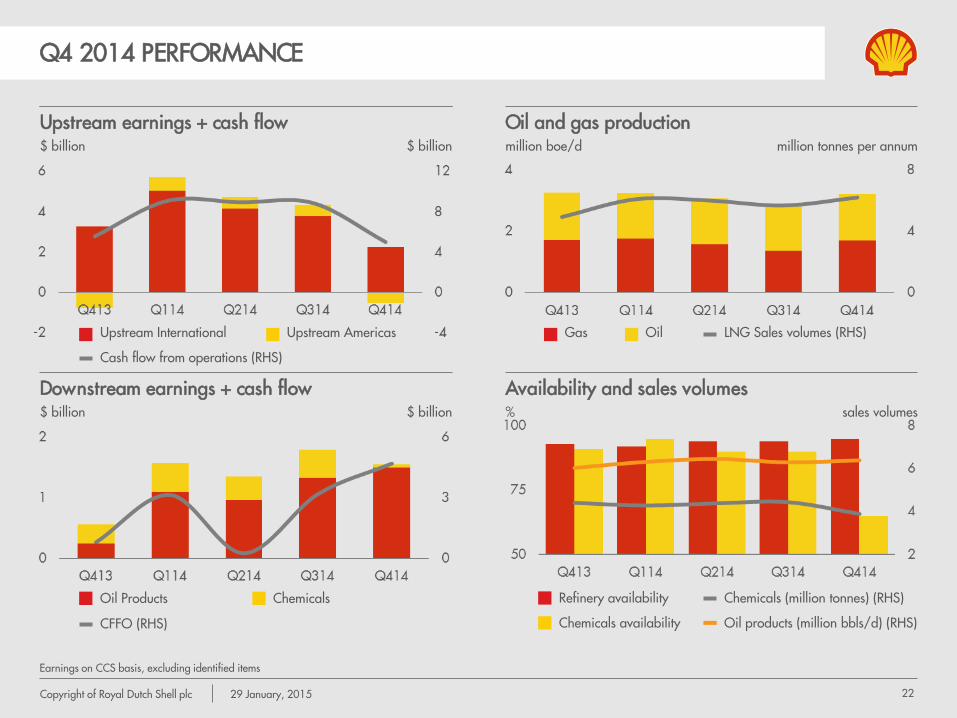

Q4 2014 PERFORMANCE

Earnings on CCS basis, excluding identified items

Upstream earnings + cash flow

$ billion

Oil and gas production

million boe/d

Downstream earnings + cash flow

$ billion

Availability and sales volumes

%

million tonnes per annum

Upstream International Upstream Americas

Cash flow from operations (RHS)

sales volumes

Refinery availability

Chemicals availability Oil products (million bbls/d) (RHS)

Chemicals (million tonnes) (RHS) Oil Products Chemicals

CFFO (RHS)

Gas Oil LNG Sales volumes (RHS)

$ billion

$ billion

23 Copyright of Royal Dutch Shell plc 29 January, 2015

PRELIMINARY RESULTS SEC PROVED RESERVES POSITION

1 Excludes acquisitions, divestments and price impacts 2 Reserves attributable to Royal Dutch Shell shareholders

2014 Reserves performance

2014 RRR 26%

2012-14 RRR 67%

Reserves life at end 2014 ~11.2 years

2012-14 Reserves average performance

Organic1 additions ~1.0 billion boe

Production ~1.2 billion boe

Organic reserves replacement 85%

Reserves Replacement

SEC proved reserves

Major reserves additions

2012-14 Reserves additions

2012-14 2014

Organic 85% 47%

Organic incl. price effects 76% 50%

SEC proved reserves2 67% 26%

(billion boe) 2012 2013 2014

Organic reserves additions 1.0 1.5 0.5

Production 1.2 1.2 1.2

SEC proved reserves2 13.6 13.9 13.1

24 Copyright of Royal Dutch Shell plc 29 January, 2015

OIL + GAS RESOURCES FUNNEL

Converting resources to production… Billion boe

Baronia EOR / Tukau Timur Bonga Main ph3 Coulomb ph2

Longer-term upside

2010 2011 2012 2013 2014

On-stream Execute (under construction)

Select/Define Production

Bonga North West Cardamom Gumusut-Kakap Mars B Petai Sabah gas KBB

Asset sales + capital ceiling

Fewer FIDs in 2014

Maintaining attractive project flow

Appomattox Browse resources plays Val d’Agri ph2 Vito others

25 Copyright of Royal Dutch Shell plc 29 January, 2015

CONVENTIONAL EXPLORATION EXECUTING A CONSISTENT AND SUCCESSFUL EXPLORATION STRATEGY

ARCTIC Long-term potential for industry

FRONTIER Build-up of acreage in under-explored basins

HEARTLANDS New plays in Shell producing basins

NEAR-FIELD High-value add-ons

Prospect size

(million boe)

Time to development

(years)

15+

10+

3+

<3 5-50

50-250

>250

>500

Spend includes acquisitions

Low-cost access to new barrels: balancing exploration risk and returns

2015 spend

Frontier / Arctic

NFE

Heartlands / Libra

26 Copyright of Royal Dutch Shell plc 29 January, 2015

EXPLORATION: 2014 PERFORMANCE

Malaysia heartlands NFE success, 3

heartland discoveries, 1 successful appraisal

~300 mmboe for Shell in 2014

Gabon deep-water frontier Sub-salt deep-water gas

discovery Shell 75%, operator

Frontier

Near-field

Frontier basin

Improved delivery in 2014

10 frontier + heartlands successes

41 near-field finds

Australia heartlands 2014: Lympstone discovery NFE success

2014 drilling success

Heartlands

GOM deep-water heartlands 2014: Rydberg, Kaikias, Power Nap

+ Gettysburg discoveries >1300 mmboe for Shell 2009+

Brazil - Libra NW1 successful appraisal C-1 well drilling Shell 20%

27 Copyright of Royal Dutch Shell plc 29 January, 2015

2015 OUTLOOK

Macro sensitivity @ $70-110/bbl Brent

2014 asset sales + license expiries (2015 vs. 2014 impact)

-100 kboe/d; -0.3 mtpa LNG

~-75 kbpd refining capacity; -145 kbpd marketing

~-$1 billion divestment tax charge impacting CFFO

Maintenance downtime / other (2015 vs. 2014 impact)

-60 kboe/d (Pearl T1, AOSP, GOM, others)

Reduced Chemicals availability (80% in 2015 vs. 85% in 2014)

Ramp-up of 2014 + 2015 start-ups

Macro

$10/bbl Brent +/- ~$3.3 billion CFFO/earnings per annum

Q1-Q1 outlook:

Maintenance -90 kboe/d (Pearl + Auger)

Divestment, license expiry, Majnoon cost recovery: ~ -200 kboe/d

Moerdijk chemicals downtime

Pearl GTL, Qatar

28 Copyright of Royal Dutch Shell plc 29 January, 2015

CAPITAL EFFICIENCY FINANCIAL FRAMEWORK AND PRIORITIES

Priorities for cash

1. Debt service

2. Dividends: growth policy

3. Capital investment: disciplined through-cycle growth

4. Return surplus cash: buybacks

Cash performance

Investment

Balance sheet

CFFO

Pay-out

Cash dividend Buyback

Gearing

CFFI

$ billion

%

$ billion

$ billion

$ billion

Net debt

Balancing cash in / cash out across cycle

Maintaining strong balance sheet

29 Copyright of Royal Dutch Shell plc 29 January, 2015

Short term Medium term Strategic

long term

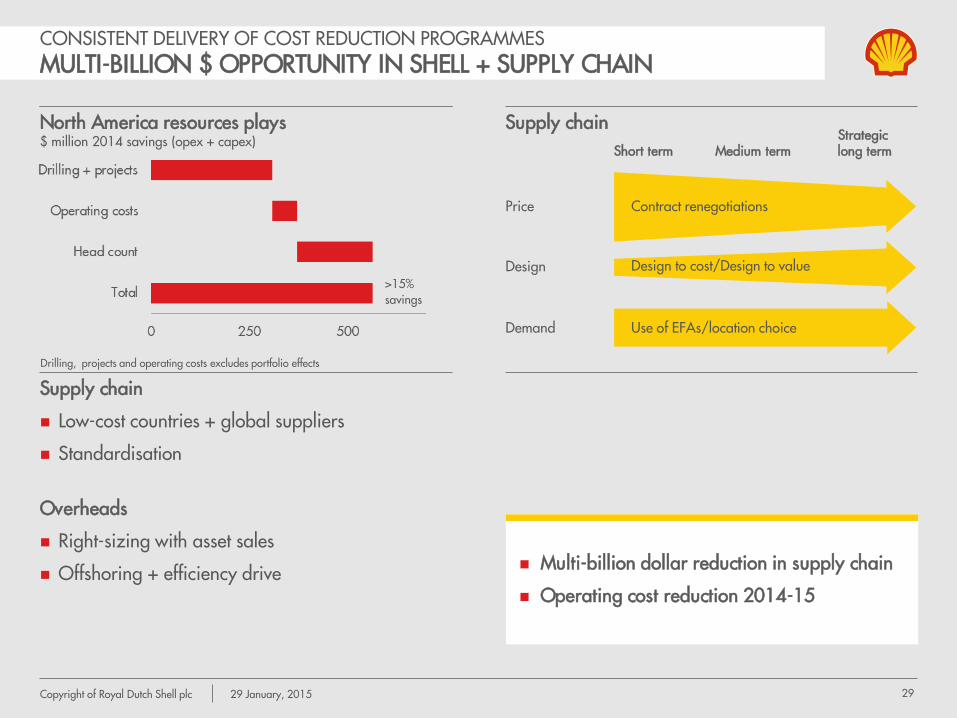

CONSISTENT DELIVERY OF COST REDUCTION PROGRAMMES MULTI-BILLION $ OPPORTUNITY IN SHELL + SUPPLY CHAIN

North America resources plays $ million 2014 savings (opex + capex)

Supply chain

Drilling, projects and operating costs excludes portfolio effects

Contract renegotiations

Design to cost/Design to value

Use of EFAs/location choice

Price

Design

Demand

>15% savings

Supply chain

Low-cost countries + global suppliers

Standardisation

Overheads

Right-sizing with asset sales

Offshoring + efficiency drive

Multi-billion dollar reduction in supply chain

Operating cost reduction 2014-15

30 Copyright of Royal Dutch Shell plc 29 January, 2015

2014

Woodside 9.5%

Wheatstone LNG

Australia downstream

Italy downstream

US midstream MLP

NA non-core LRS

Pinedale + Haynesville dry gas

BC-10 dilution

ADCO license expiry

Nigeria onshore

315 kboe/d oil + gas

~120,000 b/d refining capacity

240,000 b/d marketing

0.6 mtpa LNG

CAPITAL EFFICIENCY EARLY DELIVERY OF 2014-15 $15 BILLION DIVESTMENT PLAN

Divestment/exit Asset sales add focus $ billion

Asset sales + MLP proceeds

$5-6 billion p.a. ongoing divestment

2015 divestments likely lower pace

Early delivery of 2014-15

target Australia upstream refocus

Monetise non-core Oil Products

Resources plays reduction

ongoing footprint reduction

31 Copyright of Royal Dutch Shell plc 29 January, 2015

PORTFOLIO CHOICES DRIVING PROFITABILITY

Upstream CFFO* $ billion

Production

million boe per day

Enhancing profitability

+25%

* CFFO excludes working capital + oil & gas price effects

Underlying +2%

32 Copyright of Royal Dutch Shell plc 29 January, 2015

Growth priorities unchanged

Driving competitive cash flow

CAPITAL EFFICIENCY INVESTMENT PRIORITIES

1 Resources plays, Majnoon, infill drilling

Organic capital investment Investment themes

Growth priorities: 40%

Longer term: 25%

Engines: 35%

2015 organic capital

investment

50%

10%

40%

Pre-FID large project options

Base

Short-cycle projects1

Post-FID large projects

Conventional exploration

2015 organic capital

investment CFFO impact

of 2015 investment

’15-’16 ’17-’18

‘19+

33 Copyright of Royal Dutch Shell plc 29 January, 2015

CASH PERFORMANCE + PAY-OUT

Cash flow $ billion

Cash flow from operations Cash flow from investments1

2014 dividend and buyback $15 billion

2015 dividend ~$12 billion

Buybacks in 2015 subject to oil prices

Gearing likely to increase in 2015

$ billion Gearing and pay-out

Dividend track record

$ billion

Dividends announced

2012-2014 2014

Dividend Free cash flow

%

Gearing (RHS) Buybacks

Pay-out

Dividend is dividend announced

1 Includes MLP proceeds

34 Copyright of Royal Dutch Shell plc 29 January, 2015

BEN VAN BEURDEN CHIEF EXECUTIVE OFFICER

ROYAL DUTCH SHELL PLC

35 Copyright of Royal Dutch Shell plc 29 January, 2015

ROYAL DUTCH SHELL PLC

PROJECT DELIVERY

36 Copyright of Royal Dutch Shell plc 29 January, 2015

BC-10 ph3 Bonga Main ph3 Corrib Erha North ph2 Forcados Yokri Gbaran-Ubie ph2 Gorgon LNG ML South NA LRS/tight gas Stones

2017-19 2015-16

PROJECTS UNDER CONSTRUCTION

Production

kboe per day (Shell share) million tonnes per annum

>700 kboe/d + 7.5 mtpa LNG under construction

High-margin production

Growth uptick 2017+

2015-16 start-ups 2014 start-ups LNG volume (RHS) 2017-19 start-ups

Mars B Bonga NW Cardamom

Baronia /Tukau Timur Carmon Creek Clair ph2 Coulomb Kashagan ph1 Malikai MMLS LNG (Elba) Prelude FLNG Rabab Harweel Schiehallion Southern Swamp Tempa Rossa TNP loopline

Gumusut-Kakap Petai Sabah gas KBB

2014

Shell-operated started up

37 Copyright of Royal Dutch Shell plc 29 January, 2015

PROJECT DELIVERY MANAGING OUR OPPORTUNITY SET

2015-16 FID options 17 potential FIDs 2015-16

>$15 billion spending mitigation planned 2015-17:

Re-phasing / deferral

Supply chain

Dilutions + exits

Downstream Upstream

Options deferred / cancelled

FID choices 2015-16

FUTURE OPPORTUNITIES

Carmon Creek ph3+4 postponed

Majnoon full field

RESOURCES PLAYS

World-wide restructuring Canada, Lower 48, Argentina, other

DEEP WATER

Deferral of FIDs Slower pace in Nigeria

Appomattox Vito Bonga South West Libra pilot FPSO vessel

INTEGRATED GAS

Asia Pacific slow-down Arrow LNG greenfield cancelled

Elba LNG (site) LNG Canada T1+2 Browse LNG

UPSTREAM ENGINE

Selected base projects Val d’Agri ph2 Bokor

DOWNSTREAM ENGINE

Al Karaana chemicals cancelled Selected base projects

Pennsylvania chem. Geismar alpha olefins China chemicals Debottleneck projects

> 700 kboe/d ~12 mtpa LNG 2.7 mtpa chemicals

38 Copyright of Royal Dutch Shell plc 29 January, 2015

COMPETITIVE PERFORMANCE: BALANCING GROWTH AND RETURNS

Free cash flow: cash flow from operations less cash used in investing activities ROACE underlying: European companies: CCS basis excluding identified items. US companies: reported earnings excluding special non-operating items

Cash flow from operations $ billion

Free cash flow $ billion

ROACE – underlying %

Total shareholder return (2012-2014) %

Shell Peer group

Shell competitors

39 Copyright of Royal Dutch Shell plc 29 January, 2015

PRIORITIES 2015+

Choices on new options

Supply chain management

Managing affordability + financial flexibility

Preserving our competitive growth pipeline in downturn

Continued ramp-up of 2014 start-ups

2015 transition year into 2016/17+ growth

Returns and cash flow

Competitive returns for shareholders

Restructuring underperforming businesses

Cost reduction programmes

Competitive financial performance

Capital efficiency Project delivery

40 Copyright of Royal Dutch Shell plc 29 January, 2015

QUESTIONS & ANSWERS FOURTH QUARTER 2014 RESULTS

41 Copyright of Royal Dutch Shell plc 29 January, 2015

KEY UPSTREAM PROJECTS UNDER CONSTRUCTION

Deep water Integrated gas

Resources plays Future opportunities

Upstream engine

42 Copyright of Royal Dutch Shell plc 29 January, 2015

PRE-FID OPTIONS POTENTIAL 2015-2016 FEEDS AND FIDS

Deep water Integrated gas

Resources plays Future opportunities

Downstream engine Upstream engine

43 Copyright of Royal Dutch Shell plc 29 January, 2015

2014 CONVENTIONAL EXPLORATION: EXAMPLES

Frontier: Gabon deep water Heartland: GOM NFE: Oman, Lekhwair campaign

Noble Globetrotter 2 Exploration drilling in North Oman

Leopard sub-salt gas discovery

Multi-TCF potential

New gas play

Shell 75%

4 deep-water oil discoveries

Rydberg oil discovery in Norphlet ~110 million boe (Shell 57%)

Kaikias oil discovery ~35 million boe (Shell 100%)

Assessing new Power Nap + Gettysburg finds

11 wells drilled in 2014

~150 million barrels oil (100%)

Further potential Greater Lekhwair area

Shell 34%

Mars

Kaikias

Nakika

Vito

Appomattox

Mars B Rydberg

Ram Powell

Ursa

On-stream FEED 2014 exploration success

Brutus

100 km

Power Nap

Gettysburg

44 Copyright of Royal Dutch Shell plc 29 January, 2015

DELIVER NEW PROJECTS PROJECT MANAGEMENT

Upstream project status Construction time elapsed %

Oversight and accountability

Track record

Construction time elapsed %

photo

Corrib gas: national grid into Bellanaboy facility

45 Copyright of Royal Dutch Shell plc 29 January, 2015

2014 $ billion CCS earnings CFFO

2014 organic capital

investment

Capital employed ROACE

Engi

nes DOWNSTREAM

ENGINE

6 11 6 49 11%

UPSTREAM ENGINE

5 8 7 18 27%

Gro

wth

Prio

ritie

s

INTEGRATED GAS

10 13 6 58 18%

DEEP WATER

3 6 7 24 12%

Long

er T

erm

RESOURCES PLAYS

(2) 0 4 20 (9)%

FUTURE

OPPORTUNITIES1

1 5 5 30 2%

DECONSTRUCTING OUR PORTFOLIO

Mature + drives free cash flow

Profitable + growing

Returns impacted by growth spend

CCS earnings excluding identified items; ROACE based on CCS earnings excluding identified items 1 Iraq, Nigeria onshore (SPDC), Kazakhstan, Arctic, heavy oil

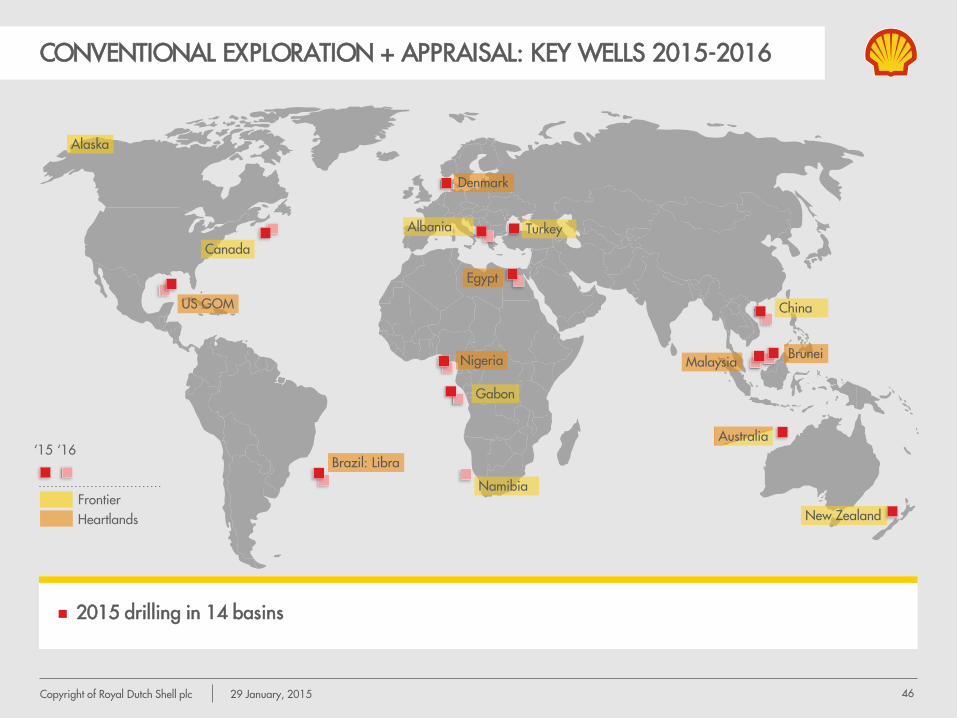

46 Copyright of Royal Dutch Shell plc 29 January, 2015

CONVENTIONAL EXPLORATION + APPRAISAL: KEY WELLS 2015-2016

‘15 ‘16

Frontier Heartlands

2015 drilling in 14 basins

Albania

US GOM

Brunei Nigeria

Australia

Gabon

Turkey

China

Malaysia

Namibia

Canada

Denmark

Egypt

Brazil: Libra

Alaska

New Zealand

47 Copyright of Royal Dutch Shell plc 29 January, 2015

FOURTH QUARTER 2014 RESULTS BALANCING GROWTH & RETURNS

29 JANUARY 2015 ROYAL DUTCH SHELL PLC