rim mobility in retail

TRANSCRIPT

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 1/21

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 2/21© Copyright Forbes 2010

Riding the chairlit at o a major western ski resort, a

customer o The North Face pulls out a smartphone

and clicks on the retailer’s specialty application, Summit

Signals. The mobile sotware uses GPS technology to

determine the skier’s location, and the customer sees

eedback on this specic mountain’s terrain and recom-

mendations on how to approach its trails. The outdoor

apparel retailer uses this same technology to provide

similar location-specic content or bikers, alpine hik-

ers, rock climbers, runners, and kayakers.Walking through the pet ood section o a major dis-

count chain, a customer receives a text message with a

digita l coupon good or 20% o Iams dog ood. In this pilot

program, the store has detected the shopper’s presence in

the pet ood aisle, and knows that this particular shopper

generally purchases Purina Beneul. For the retailer’s mar-

keting partners, th is provides a chance to encourage a brand

switch. For the retailer, it enhances loyalty rom a customer

who has opted in to participate in the mobile program.

Two teenaged girls rie through the racks o tops i

major department store chain’s juniors section. Stopping

one she likes, one girl takes out her phone and takes a p

ture o the shirt’s bar code. On the screen o her phone s

sees product reviews rom other shoppers, and also get

special oer on a pair o shoes to complete the outt.

As he jockeys to make his ight at Houston’s airpor

New York-bound traveler realizes he’s orgotten to pack

laptop’s power cord. He turns to his cell phone and brin

up Best Buy’s wireless website. He orders a replacem

cord, nds the store location closest to his Manhattan ho

and picks it up on his way to check in.These are just a handul o customer interactio

taking place—today—in the mobile commerce (m-co

merce) channel. In each instance, a retailer uses mobile

a way to enhance customer engagement and loyalty. A

it is the ubiquity o cell phones, smartphones, and oth

mobile devices that is leading a growing number o reta

ers to explore what additional opportunities await in t

mobile space. But how are these initiatives aring, a

what do the early results rom these eorts have to

about the way orward?

Key Findings Retailers are actively pursuing the mobile channel, with nearly three out o our having some kind o mobile initiative•

in place today.

Nearly hal o retailers say they want to capture “frst-mover advantage” as their customers go mobile.•

Retailers are at varying levels o sophistication in terms o their mobile eorts. Fundamental tools such as mobile ads•

and mobile websites are the most common. Others are moving into more transaction-based and customer service-oriented applications. The most sophisticated are putting in place location- and context-based apps.

For many retailers, mobile is much more than a “scaled-back” version o the Internet, as they take advantage o the•

ubiquity o cell phones and smartphones to create location-specifc experiences.

Retailers are determining which mobile devices and operating systems to support, relying primarily on the device’s•

current and potential market share and the demographics o the device’s user base.

Retailers appear satisfed with their mobile eorts, with six out o ten saying their mobile channel returns are either•

meeting or exceeding expectations.

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 3/21© Copyright Forbes 2010

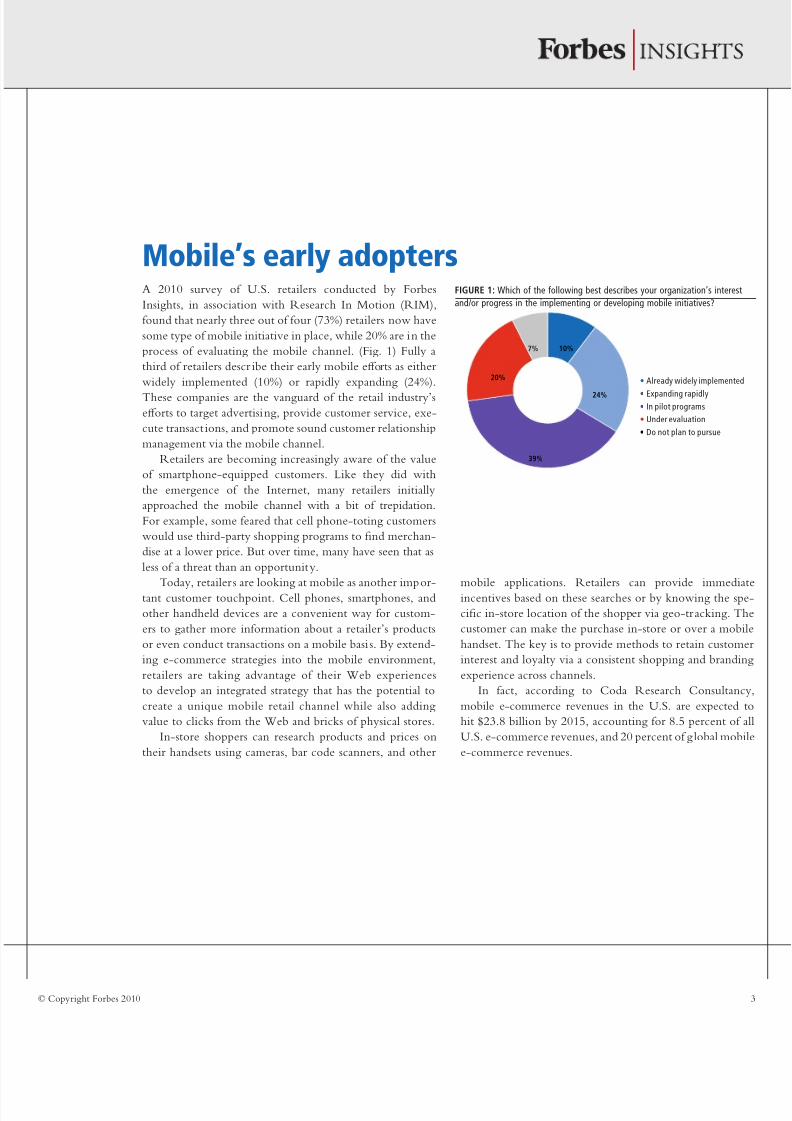

A 2010 survey o U.S. retailers conducted by Forbes

Insights, in association with Research In Motion (RIM),

ound that nearly three out o our (73%) retailers now have

some type o mobile initiative in place, while 20% are in the

process o evaluating the mobile channel. (Fig. 1) Fully a

third o retailers descr ibe their early mobile eorts as either

widely implemented (10%) or rapidly expanding (24%).

These companies are the vanguard o the retail industry’s

eorts to target advertising, provide customer service, exe-

cute transact ions, and promote sound customer relationship

management via the mobile channel.

Retailers are becoming increasingly aware o the value

o smartphone-equipped customers. Like they did with

the emergence o the Internet, many retailers initially

approached the mobile channel with a bit o trepidation.

For example, some eared that cell phone-toting customers

would use third-party shopping programs to nd merchan-

dise at a lower price. But over time, many have seen that as

less o a threat than an opportunity.

Today, retailers are looking at mobile as another impor-

tant customer touchpoint. Cell phones, smartphones, and

other handheld devices are a convenient way or custom-

ers to gather more inormation about a retailer’s products

or even conduct transactions on a mobile basi s. By extend-

ing e-commerce strategies into the mobile environment,

retailers are taking advantage o their Web experiences

to develop an integrated strategy that has the potential to

create a unique mobile retail channel while also adding

value to clicks rom the Web and bricks o physical stores.

In-store shoppers can research products and prices on

their handsets using cameras, bar code scanners, and other

mobile applications. Retailers can provide immedi

incentives based on these searches or by knowing the sp

cic in-store location o the shopper via geo-tracking. T

customer can make the purchase in-store or over a mob

handset. The key is to provide methods to retain custom

interest and loyalty via a consistent shopping and brandi

experience across channels.

In act, according to Coda Research Consultan

mobile e-commerce revenues in the U.S. are expected

hit $23.8 billion by 2015, accounting or 8.5 percent o

U.S. e-commerce revenues, and 20 percent o g lobal mob

e-commerce revenues.

FIGURE 1: Which o the ollowing best describes your organization’s interest

and/or progress in the implementing or developing mobile initiatives?

• Already widely implemented

• Expanding rapidly• In pilot programs

• Under evaluation

• Do not plan to pursue

10%

24%

39%

20%

7%

M’ r r

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 4/21© Copyright Forbes 2010

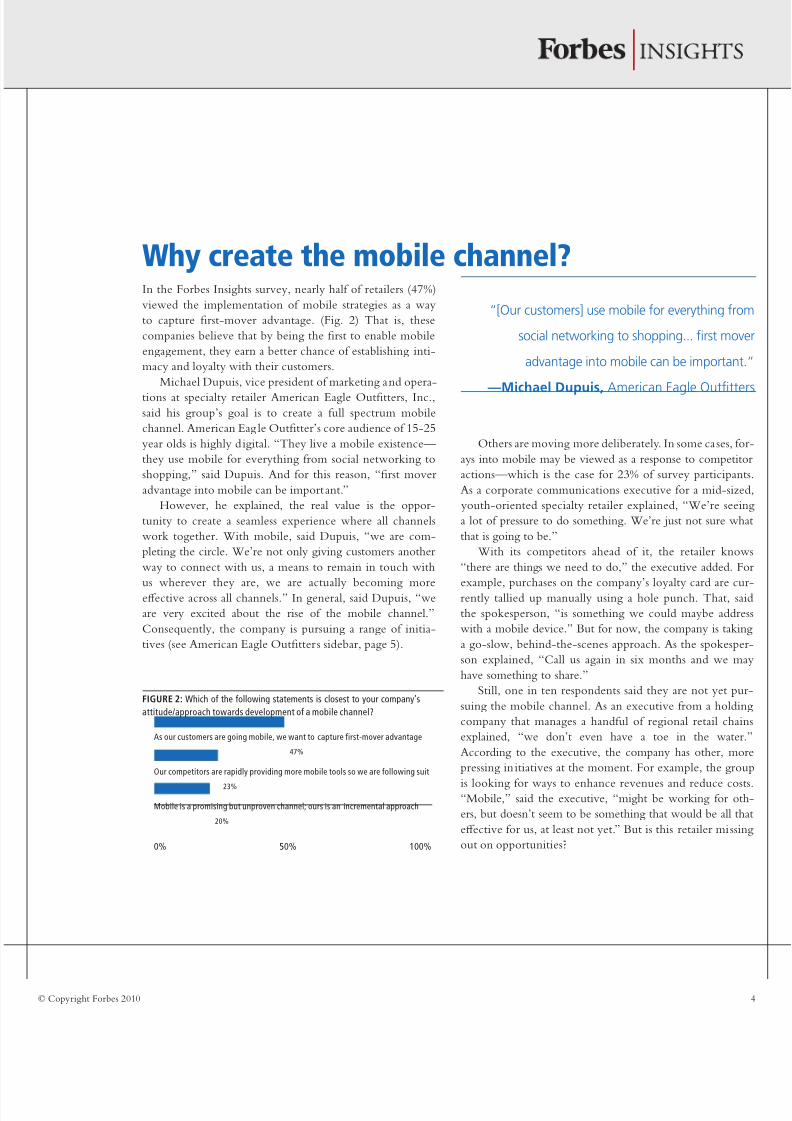

In the Forbes Insights survey, nearly hal o retailers (47%)

viewed the implementation o mobile strategies as a way

to capture rst-mover advantage. (Fig. 2) That is, these

companies believe that by being the rst to enable mobile

engagement, they earn a better chance o establishing inti-

macy and loyalty with their customers.

Michael Dupuis, vice president o marketing and opera-

tions at specialty retailer American Eagle Outtters, Inc.,

said his group’s goal is to create a ull spectrum mobile

channel. American Eag le Outtter’s core audience o 15-25

year olds is highly digital. “They live a mobile existence—

they use mobile or everything rom social networking to

shopping,” said Dupuis. And or this reason, “rst mover

advantage into mobile can be important.”

However, he explained, the real value is the oppor-

tunity to create a seamless experience where all channels

work together. With mobile, said Dupuis, “we are com-

pleting the circle. We’re not only giving customers another

way to connect with us, a means to remain in touch with

us wherever they are, we are actually becoming more

eective across all channels.” In general, said Dupuis, “we

are very excited about the rise o the mobile channel.”

Consequently, the company is pursuing a range o initia-

tives (see American Eagle Outtters sidebar, page 5).

Others are moving more deliberately. In some cases,

ays into mobile may be viewed as a response to competi

actions—which is the case or 23% o survey participan

As a corporate communications executive or a mid-siz

youth-oriented specialty retailer explained, “We’re seei

a lot o pressure to do something. We’re just not sure w

that is going to be.”

With its competitors ahead o it, the retailer kno

“there are things we need to do,” the executive added. F

example, purchases on the company’s loyalty card are cu

rently tallied up manually using a hole punch. That, s

the spokesperson, “is something we could maybe addr

with a mobile device.” But or now, the company is taki

a go-slow, behind-the-scenes approach. As the spokesp

son explained, “Call us again in six months and we m

have something to share.”

Still, one in ten respondents said they are not yet pu

suing the mobile channel. As an executive rom a holdi

company that manages a handul o regional retail cha

explained, “we don’t even have a toe in the wate

According to the executive, the company has other, m

pressing in itiatives at the moment. For example, the gro

is looking or ways to enhance revenues and reduce co“Mobile,” said the executive, “might be working or o

ers, but doesn’t seem to be something that would be all t

eective or us, at least not yet.” But is this retailer missi

out on opportunities?

“[Our customers] use mobile or everything ro

social networking to shopping... frst mov

advantage into mobile can be important

—Michael Dupuis, American Eagle Outftte

FIGURE 2: Which o the ollowing statements is closest to your company’s

attitude/approach towards development o a mobile channel?

0% 50% 100%

As our customers are going mobile, we want to capture irst-mover advantage

Our competitors are rapidly providing more mobile tools so we are ollowing suit

Mobile is a promising but unproven channel; ours is an incremental approach

47%

23%

20%

Wh cr h m ch?

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 5/21© Copyright Forbes 2010

t r mThE FUndamEnTal Tools: mobIlE ads and

mobIlE wEbsITEs

A cynic might describe the mobile channel as the Internet

delivered at slower speeds on smaller screens. But in act,

mobile communications are something entirely dierent,

and the opportunity exists to nd out what works within

the context o this new tool. The key advantages o mobile

devices relative to the Internet are their portability and

ubiquity. Cell phones and mobile devices are in the pocket

or on the ear o nearly every customer or prospect. So the

question becomes: given mobile’s unique attributes, which

capabilities should a retailer develop?

The simplest place to begin is with mobile advertising.

As with the Internet, this is essentially a pay-to-play strat-

egy. Retailers can buy space on other mobile websites or can

pay or prominent placement on various mobile search terms.

The question though is what happens when a mobile device

user clicks on that banner ad or the search term’s results?

Advertising is one thing, but a company needs to be ready or

interaction within the context o the mobile environment.

Some early adopters and their advisers suggest starting

with two essential and complementary elements: a mobile

website and an appropriate set o customized, downloadable

applications. Newcomers to mobile oten ask i one is more

important than the other. But i the goal is to create an in

grated experience or the customer—i the goal is indeed

mobile channel—a retai ler may need to create both.

A mobile website can be a slimmed-down version

a company’s Internet site, optimized or mobile browsin

This might mean reducing the capability o the mobile s

relative to the Internet site or even reducing the number

viewable items. Many get their start in m-commerce w

just such an approach.

However, according to Kelly O’Neill, d irector o pro

uct marketing at ATG, whose sotware ocuses on onli

and cross-channel commerce, the ultimate goal “is to p

vide an integrated experience between mobile, the Intern

physical stores, call centers—al l points o customer inter

tion.” In other words, a mobile website can be launch

with limited unctionality relative to the Internet, but t

near-term endgame should be that anything customers c

do on the Web, they should also be able to do with mob

The two sites should be connected and customers should

able to shop and browse across both. When deciding how

mobile site and website might dier, O’Neill suggested th

merchants should consider elements that are most appr

priate to that channel—GPS or barcode scanning or

mobile shopper, or example.

amERIcan EaGlE oUTFITTERs: an EaRly adopTER sTIll movInG FoRwaRd

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 6/21© Copyright Forbes 2010

That’s also why many retailers simultaneously create

native applications. With their smaller screens and largely

“mouse-less” interaces, mobile devices require signi-

icantly more work to accomplish similar tasks. Enter the

native, or branded application. Retailers can enhance the

mobile experience by giving customers downloadable tools

that reduce the number o actions required to obtain and

internet-comparable experience in a mobile environment.

Matt Johnston, vice president o marketing and commu-

nity at the crowd-sourcing sotware testing company Utest,

explained, “Good native applications have considerable intel-

ligence and customization built-in. The customer downloads

the application onto his or her own device, and now has a

quick way to go where they need to go. Do they want to

place an order, nd a store, see their account, grab a coupon?

Whatever they need, with a good app, it’s right there.”

InTERmEdIaTE applIcaTIons: mobIlE commERcE and

cUsTomER sERvIcE

Beyond mobile websites and native applications, pioneers

in m-commerce are building a broad array o additional

capabilities.

Basic native applications might include a store nder or

an “order now” capability. More advanced applications are

being developed to enhance both the mobile and the in-

store experience. For instance, a mobile device’s camera can

“Do they want to place an order, fnd a stor

see their account, grab a coupon? Whatever the

need, with a good app, it’s right there.

—Matt Johnston, Ute

TaRGET: GETTInG bEyond TExT mEssaGEs

be used to take a picture o a product’s barcode. Once t

product is identied, the mobile device can become a co

duit or a wide range o possibilities.

For example, in a urniture store, a customer mig

swipe the barcode o a couch. Now the application allo

the user to view this same couch covered in a variety

abrics. Or alternatively, in a clothing store, the same b

code could launch a program that shows an item in a ran

o colors or paired with suitable, complementary items

the item is out o stock in this location, the applicati

might be able to check inventory in other stores or in iti

a purchase or home delivery.

Similarly, such a scan could provide the option o us

the mobile device to view a product demonstration or wh

ever enhanced content the retailer believes will be relev

to the customer or prospect. Or the customer might be a

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 7/21© Copyright Forbes 2010

to use the scan to execute an in-store purchase or alert a sales

associate or assistance, similar to what Target is doing (see

Target sidebar, page 6).

There’s literally no end to the possibilities. For exam-

ple, at Kroger, pilot programs are up and running to embed

the store’s loyalty card into customers’ mobile devices. A

similar initiative at Ace Hardware sends coupons and other

special oers to customers.

advancEd Tools: locaTIon and conTExT TRackInGFurther on the horizon, a number o retailers are experiment-

ing with GPS-enabled proximity-marketing capabilities.

(Fig. 3) Note that in each case the customers are aware their

location is known to the retailer in question and that they

have chosen to opt-in to the services.

An essential component o this type o app is relevance,

and it is here that mobile commerce could potentially

expand customer intimacy beyond location to also incorpo-

rate time, weather or other actors. Imagine i a retailer was

able to detect not only a customer’s location but could also

iner his or her likely interests based on context—a coee

coupon or an early ri sing commuter (now being tested by

Sonic) or a discount on a soundtrack recording or a person

coming home rom a musical theater perormance.

One company working in this space is location-based

advertising startup Placecast. A critical goal or retailers,

said the rm’s CEO Alistair Goodman, “is getting cus-

tomers into the stores.” Placecast is attempting to assist

retailers and others in th is regard by detecting customers

and prospects as they enter variously dened “geo-ences.”

Highly relevant text messages are then delivered—again

strictly on an opt-in basis—based on time, place, and

other contextual variables.

O note, said Goodman, is that such marketing has

both immediate and longer-term benets. “Location” and“context” are very powerul tools. A customer may not be

o a mind to act on the SMS communication at the time

it’s received. But, said Goodman, people oten remem-

ber where they were when an idea entered their minds. As

such, said Goodman, the customer may not immediately

respond, but “they make a mental note, then go back” at a

later date.

FIGURE 3: What mobile tactics are you using today—and plan to be using in

one year?

0% 50% 100%

Mobile website

Mobile Web content

Mobile coupons

Paid mobile search

Mobile advertising

Downloadable applications

SMS outbound

Proximity marketing

Downloadable brand-related content

• Today • In one year

36%

35%

34%

33%

29%

27%

24%

24%

18%

40%

41%

36%

44%

39%

29%

32%

23%

25%

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 8/21

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 9/21© Copyright Forbes 2010

A key challenge or retailers will be building integration

between their physical stores, Internet presence, call cen-

ters, and now mobile centers. Customers requently have a

single view o their relationship with a retailer. That is, no

matter which channel the customer chooses, the expectation

is that the retailer wil l know the history o the relationship.

Moreover, this inormation should ow seamlessly rom

channel to channel. For example, i a customer creates a

wish li st on a website, that customer’s r iends should be able

to access that same registry rom any mobile device.

Largely owing to lessons learned during the devel-

opment o the Internet, many retail executives already

understand the need to coordinate across channels. So this

time around, explained Daniel May, marketing manager at

convenience store giant 7-Eleven, “Maybe things are going

a bit smoother.” (See 7-Eleven sidebar, page 11)

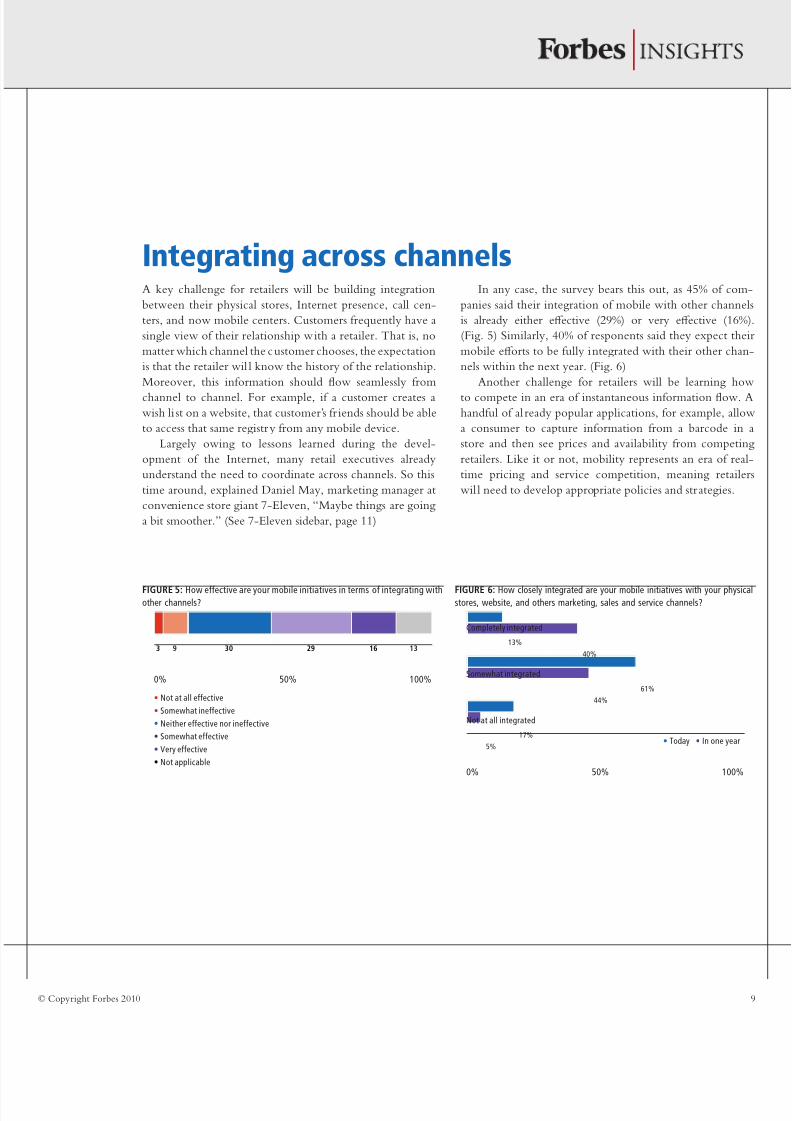

In any case, the survey bears this out, as 45% o com

panies said their integration o mobile with other chann

is already either eective (29%) or very eective (16%

(Fig. 5) Similarly, 40% o responents said they expect th

mobile eorts to be ully integrated with their other cha

nels within the next year. (Fig. 6)

Another challenge or retailers will be learning h

to compete in an era o instantaneous inormation ow

handul o al ready popular applications, or example, all

a consumer to capture inormation rom a barcode in

store and then see prices and availability rom compet

retailers. Like it or not, mobility represents an era o re

time pricing and service competition, meaning retail

wil l need to develop appropriate policies and strategies.

3 9 30 29 16 13

FIGURE 5: How eective are your mobile initiatives in terms o integrating withother channels?

0% 50% 100%

• Not at all eective

• Somewhat ineective

• Neither eective nor ineective

• Somewhat eective

• Very eective

• Not applicable

FIGURE 6: How closely integrated are your mobile initiatives with your physstores, website, and others marketing, sales and service channels?

0% 50% 100%

Completely integrated

Somewhat integrated

Not at all integrated

• Today • In one year

13%

61%

17%

40%

44%

5%

ir cr ch

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 10/21© Copyright Forbes 2010

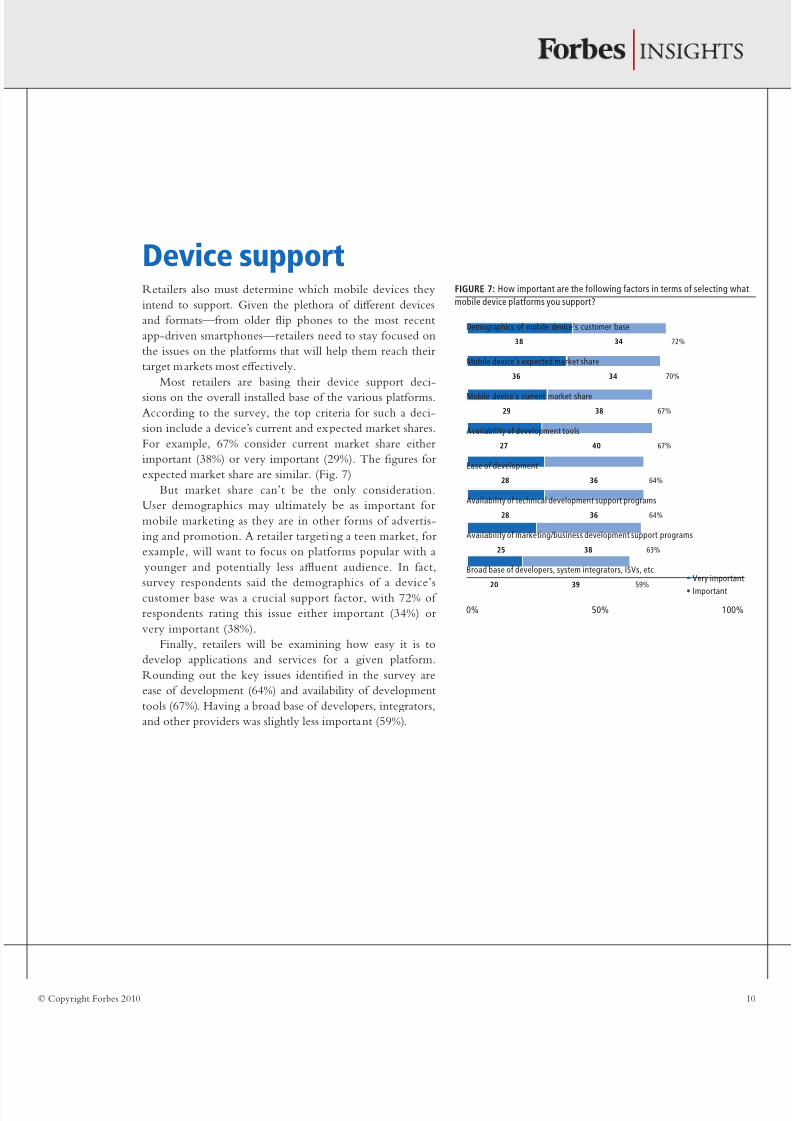

dc urRetailers also must determine which mobile devices they

intend to support. Given the plethora o dierent devices

and ormats—rom older ip phones to the most recent

app-driven smartphones—retailers need to stay ocused on

the issues on the platorms that will help them reach their

target markets most eectively.

Most retailers are basing their device support deci-

sions on the overall installed base o the various platorms.

According to the survey, the top criteria or such a deci-

sion include a device’s current and expected market shares.

For example, 67% consider current market share either

important (38%) or very important (29%). The gures or

expected market share are similar. (Fig. 7)

But market share can’t be the only consideration.

User demographics may ultimately be as important or

mobile marketing as they are in other orms o advertis-

ing and promotion. A retailer targeting a teen market, or

example, will want to ocus on platorms popular with a

younger and potentially less auent audience. In act,

survey respondents said the demographics o a device’s

customer base was a crucial support actor, with 72% o

respondents rating this issue either important (34%) or

very important (38%).

Finally, retailers will be examining how easy it is to

develop applications and services or a given platorm.

Rounding out the key issues identied in the survey are

ease o development (64%) and availability o development

tools (67%). Having a broad base o developers, integrators,

and other providers was slightly less important (59%).

FIGURE 7: How important are the ollowing actors in terms o selecting wh

mobile device platorms you support?

0% 50% 100%

Mobile device’s current market share

Mobile device’s expected market share

Demographics o mobile device’s customer base

Availability o development tools

Availability o technical development support programs

Availability o marketing/business development support programs

Broad base o developers, system integrators, ISVs, etc.

20 39

25 38

28 36

27 40

28 36

38 34

36 34

29 38

• Very importan

• Important

67%

70%

72%

64%

67%

64%

63%

59%

Ease o development

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 11/21© Copyright Forbes 2010

7-ElEvEn: RElaTInG To mIllEnnIals

g rRetailers need to think in terms o how ar and how ast

their competing priorities will allow them to pursue this

ast-evolving channel.

For those retailers seeking “rst mover” advantage, the

decision to pursue mobile was almost lightning ast. As

American Eagle Outtters’ Dupuis explained, “The oppor-

tunity in our case was airly obvious—this was something

our customers wanted and needed and so we just had to go

about getting it done.”

A key challenge or others may be obtaining manage-

ment buy-in along with the necessary development and

operating budgets. Here, the news is both bad and good.

The bad news: any organization that isn’t already well on

its way to developing mobile capabilities may already be

behind. But the good news: early adopters have been doing

their share o pathnding. As such, the way orward or

those yet to begin the journey or just launching pilot pro-

grams is signicantly clearer.

There’s even more good news. Many o the most

demanding challenges have already been ironed out. For

example, today, mobile websites can address the vast major-

ity o smart devices by providing compatibility with a small

and well-established array o mobile browsers. Also, a year

or so ago, the universe o mobile-aware IT expertise—both

in-house and external—was airly thin. Today, thou

the sheer volume o activity makes or a competitive m

ketplace, there are many more proven resources a

development paths.

In the majority o cases, the push or mobile strateg

begins with interna l marketing executives—the case at 7

o companies surveyed. However, IT executives also pla

leading role in initiating such strategies—the case at 59%

those surveyed.

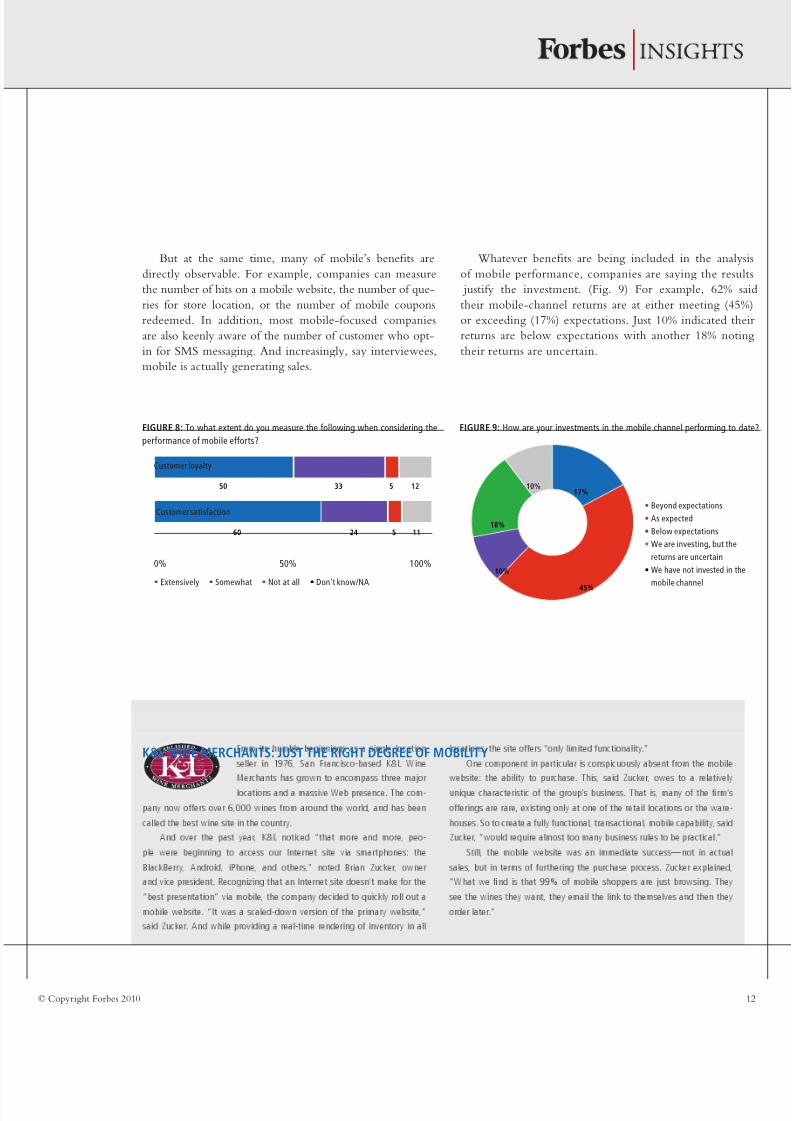

In terms o ROI, many o the returns are intangib

For example, it would likely be difcult to gauge mobi

impact on the quality o customer service or customer s

isaction in general. Still, organizations are making t

eort. According to the survey, 83% o companies that ha

invested in mobile are measuring its impact on custom

loyalty, with 50% describing the eort a s extensive. (Fig

Similarly, 84% are measuring the impact on customer sa

action, 60% extensively.

“Mobile coupons defnitely drive visit

— Daniel May, 7-Elev

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 12/21© Copyright Forbes 2010

But at the same time, many o mobile’s benets are

directly observable. For example, companies can measure

the number o hits on a mobile website, the number o que-

ries or store location, or the number o mobile coupons

redeemed. In addition, most mobile-ocused companies

are also keenly aware o the number o customer who opt-

in or SMS messaging. And increasingly, say interviewees,

mobile is actually generating sales.

Whatever benets are being included in the analy

o mobile perormance, companies are saying the resu

justiy the investment. (Fig. 9) For example, 62%

their mobile-channel returns are at either meeting (45

or exceeding (17%) expectations. Just 10% indicated th

returns are below expectations with another 18% not

their returns are uncertain.

FIGURE 9: How are your investments in the mobile channel perorming to d

• Beyond expectations

• As expected

• Below expectations

• We are investing, but the

returns are uncertain

• We have not invested in th

mobile channel

17%

10%

45%

18%

10%

k&l wInE mERchanTs: JUsT ThE RIGhT dEGREE oF mobIlITy

60

50

24

33

5

5

11

12

FIGURE 8: To what extent do you measure the ollowing when considering the

perormance o mobile eorts?

Customer loyalty

0% 50% 100%

Customer satisaction

• Extensively • Somewhat • Not at all • Don’t know/NA

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 13/21© Copyright Forbes 2010

Many retailers are at a crossroads in approaching the mobile

channel. Early adopters are raising the bar in terms o cus-

tomer expectations across a range o activities. From product

availability and pricing to sales and customer service, i a

retailer can’t provide a mobile option, the business will l ikely

migrate to a competitor. At nearly light speed, mobile capa-

bilities have moved rom nice to have to essential.

Retailers today need to maintain a viable mobile web-

site i or no other reason than to be visible on product

and location searches. It is also advisable to pursue mobile

advertising and to provide native applications. Such tools

can provide a range o benets or end users, such as

streamlined mobile keystrokes or perorming searches or

transactions on a retailer’s mobile website. And because

such applications are relatively inexpensive to create, retail-

ers can barely aord overlooking any o the most popular

mobile devices.

In all o this, outbound marketing messages, taking the

orm o text messages, can be a key component. Companies

mEThodoloGy

chRIsTIaan RIzy

dirECtor

sTUaRT FEIl

EditoriAl dirECtor

bREnna snIdERman

rESEArCh dirECtor

bIll mIllaR

WritEr

can consider the most advanced capabilities, such as lo

tion-based or contextual messaging, or they can st

to the undamentals. But whether choosing glitz or t

tried and true, it wi ll be important to always obtain iro

clad customer buy-in, and then monitor and control t

number and degree o messages to avoid overstepping t

boundaries o any customer relationship.

Yes, the mobile channel is still in its inancy. A

undoubtedly it will evolve in surprising, occasionally disa

pointing, but generally increasingly eective ways. Alrea

customers are embracing mobility as a means o interacti

with preerred and secondary brands and product o

ings. Retailers should similarly embrace mobility, nd

the means to incorporate its advantages within the cont

o physical stores, Web presences, and related unctions a

activities.

In short, mobile represents a proound opportunity. T

challenge today is nding its optimal implementation

any given brand and its accompanying customers.

conclUsIon:

tm h c

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 14/21© Copyright Forbes 2010

appEndIx a

a ur f

Over the next 12 months, what are your top marketing and channel priorities?

0% 50% 100%

Directing customers to the appropriate service channel

Leveraging the mobile channel

Achieving an integrated, cross-channel view o the customer

Taking better advantage o social media

Remerchandising stores

Integrating in-store and technology-enabled channels

Reining our Web strategy

Maximizing the in-store experience

Improving customer service

45%

33%

26%

20%

45%

27%

25%

20%

14%

While leveraging the mobile channel does

not rate as a chie concern, many o the top

priorities—such as improving customer

service or taking advantage o social media—

are intrinsically linked to mobile.

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 15/21© Copyright Forbes 2010

Which o these groups is primarily responsible or initiating your mobile channel

strategies?

0% 50% 100%

Other external partners

External marketing partners/agencies

Other internal executives

External IT partners

Suppliers and vendors

Internal IT executives

Internal marketing executives

72%

59%

4%

21%

22%

13%

1%

What is your company’s approach to managing its mobile initiatives?

• We manage all phases in-house

• We manage the majority o

the program in-house, but

use some external services

providers

• We use external service

providers to a signifcant

degree, but do some work

in-house

• We rely exclusively on external

service providers

• Don’t know/not applicable

31%11%

11%

45%

2%

Internal stakeholders still drive mobile

eorts or retail; strategies are set by internal

marketing and IT teams...

...while ongoing management is driven by

in-house teams with some support rom

external providers.

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 16/21© Copyright Forbes 2010

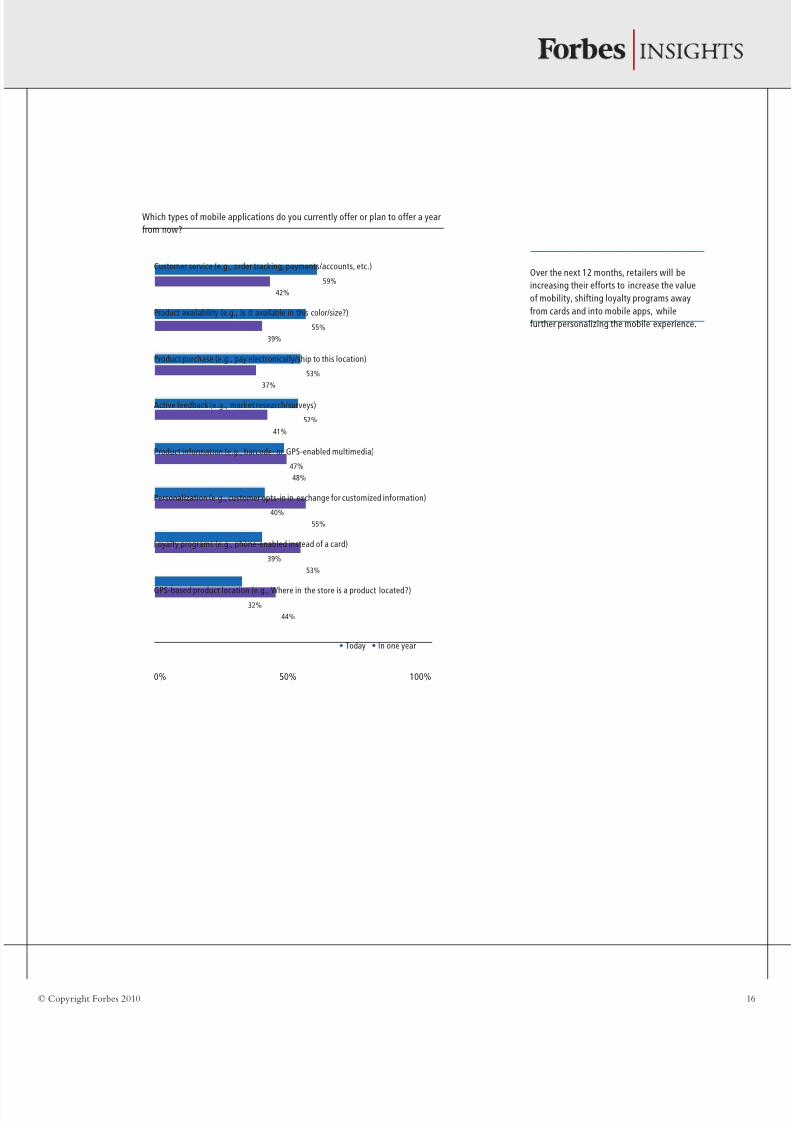

Which types o mobile applications do you currently oer or plan to oer a year

rom now?

0% 50% 100%

Loyalty programs (e.g., phone-enabled instead o a card)

GPS-based product location (e.g., Where in the store is a product located?)

Active eedback (e.g., market research/surveys)

Personalization (e.g., customer opts-in in exchange or customized inormation)

Product inormation (e.g., barcode- or GPS-enabled multimedia)

Product purchase (e.g., pay electronically/ship to this location)

Product availability (e.g., Is it available in this color/size?)

Customer service (e.g., order tracking, payments/accounts, etc.)

59%

55%

53%

52%

47%

40%

39%

32%

42%

39%

37%

41%

48%

55%

53%

44%

• Today • In one year

Over the next 12 months, retailers will be

increasing their eorts to increase the value

o mobility, shiting loyalty programs away

rom cards and into mobile apps, while

urther personalizing the mobile experience.

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 17/21© Copyright Forbes 2010

What do you see as the top challenges to integrating mobile initiatives with

other customer/marketing programs?

0% 50% 100%

Challenges o integrating multiple customer inormation databases

Customer privacy issues

Device compatibility

Incompatibility with existing enterprise applications

Incompatibility with existing CRM/ERP applications

Complex/ast-evolving technologies

Complexity o customer interaction

Discerning customer needs/preerences

Lack o interest/cooperation between other customer-acing unctions

Resistance rom other customer-acing unctions

35%

33%

29%

20%

16%

34%

30%

24%

17%

15%

Although integrating mobile, Internet, phone,

and in-store channels is a top priority or

retailers, many challenges still exist.

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 18/21© Copyright Forbes 2010

How much o your total marketing budget is allocated to mobile initiatives?

• 0-10%

• 11-20%

• 20+%

100%

0%

What is your total budget or mobile marketing in 2010?

• Under $1 million

• $1-5 million

• $6-10 million

• $11-15 million• $16-25 million

• Over $25 million

34%

14%

25%

15%

5%

9%

Today 1 year rom now 3 years rom now

66%

47%

31%

26%

39% 38%

8%

14%

31%

Over the next three years, mobile will get

a signifcantly greater share o retailers’

marketing budgets.

Although mobile is not yet a top marketing

budget item, nearly one-in-ten retailers is

spending in excess o $25 million on mobile

this year.

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 19/21© Copyright Forbes 2010

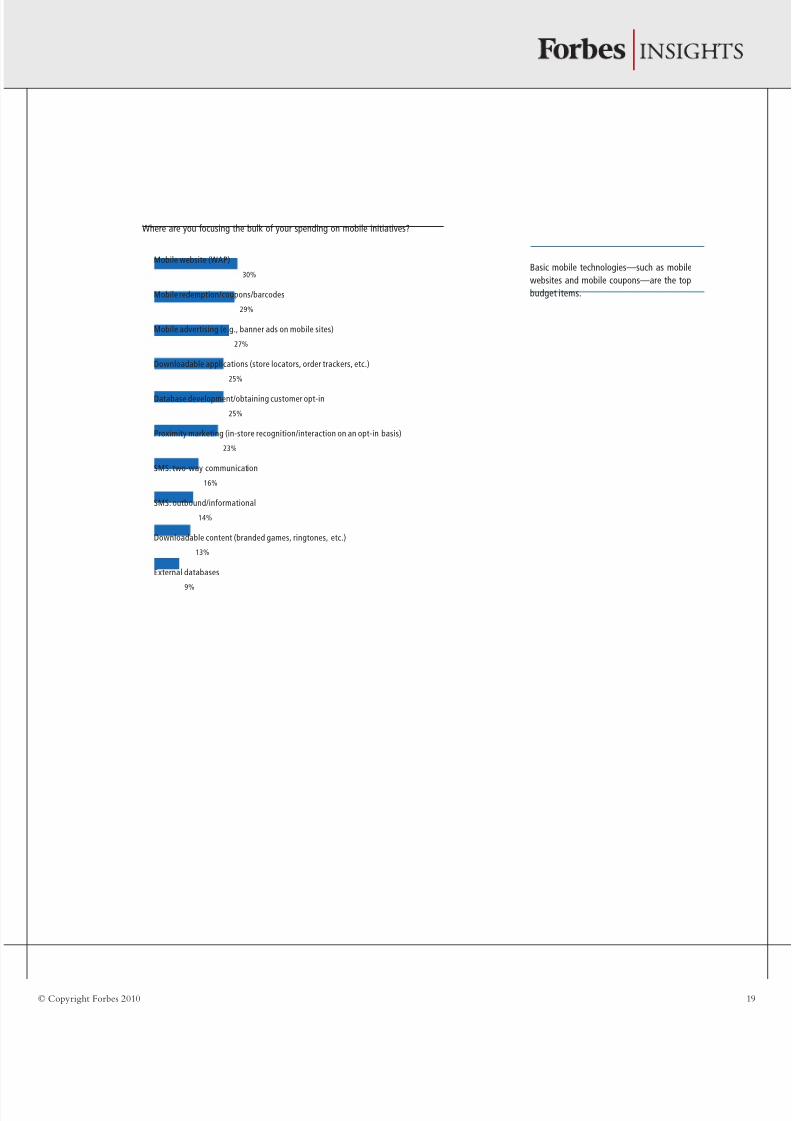

Where are you ocusing the bulk o your spending on mobile initiatives?

Mobile website (WAP)

Mobile advertising (e.g., banner ads on mobile sites)

Database development/obtaining customer opt-in

SMS: two-way communication

Downloadable content (branded games, ringtones, etc.)

Mobile redemption/coupons/barcodes

Downloadable applications (store locators, order trackers, etc.)

Proximity marketing (in-store recognition/interaction on an opt-in basis)

SMS: outbound/inormational

External databases

30%

27%

25%

16%

13%

29%

25%

23%

14%

9%

Basic mobile technologies—such as mobile

websites and mobile coupons—are the top

budget items.

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 20/21© Copyright Forbes 2010

In which retail industry segment does your company belong?

What are your company’s annual revenues?

• Specialty sot goods

• Specialty hard goods

• Department store

• Chain store/mass merchandiser/

discounter

• Supermarket/drug store

• Other

• $100 million to $249.9 million

• $250 million to $499.9 million

• $500 million to $999.9 million

• $1 billion - $4.9 billion

• $5 billion - $10 billion

• More than $10 billion

21%

10%

11%

29%

19%

10%

How many stores does your company operate?

• 2-10

• 11-25

• 26-50

• 51-100

• 101-200

• 201-500

• more than 500

7%

8%

9%

6%

13%

12%

45%

6%

21%13%

12%

24%

24%

appEndIx b

sur dmrhc

Responses were split among the major

retail segments.

Most responding retailers operate chains o

more than 100 locations.

More than 60% o responding retailers have

revenues o $1 billion-plus.

8/6/2019 RIM Mobility in Retail

http://slidepdf.com/reader/full/rim-mobility-in-retail 21/21

60 Ff Aveue, new yk, ny 10011 | 212-367-2662