rian le roux - old mutual

TRANSCRIPT

RIAN LE ROUX

SAVINGS & GROWTH GROWTH & SAVINGS

RESEARCH UPDATE EDITION 9

WHO SAVES AND WHY?

• Saving = HH’s +

Co’s + Govt

• If Saving < Investment, we rely on foreigners to plug the gap

or investment suffers

• Saving = tax

revenue > current spending

• Excess tax revenues finance physical & social

infrastructure investment

• Savings =

undistributed profits

• These retained profits used to finance

replacement & expansion

• Foregoing

current consumption to enhance future consumption

• i.e. HH’s save to

finance future big expenses & retirement

I f we save too l i t t le? I n v e s t m e n t i s a k e y d r i v e r o f g r o w t h

Households Companies Government As a Nation

1

RESEARCH UPDATE EDITION 9

A FEW IMPORTANT REMINDERS

Saving and investment

interplay

• Sufficient saving is a necessary, but not a

sufficient, prerequisite for investment

• Or, without savings, investment cannot occur (or little saving = little investment)

• But, sufficient savings do not

guarantee that investment will occur

For investment to occur, macro-

conditions must be conducive, e.g:

• Good macro-economic conditions and prospects

• A business-friendly environment, incl policy certainty

and predictability (at macro and industry levels), good infrastructure, bureaucratic efficiency, political stability, entrenched property rights, etc, etc

Excess savings over investment will

either seek a home elsewhere (abroad)

or be returned to shareholders

2

RESEARCH UPDATE EDITION 9

JULY 2014: SA’S NATIONAL INVESTMENT & SAVINGS TROUBLE HAS ARRIVED

Gap required

from foreigners

Saving/investment gap is also equal to the current account balance

Investment as % of GDP

Saving as % of GDP

Source: MacroSolutions

RESEARCH UPDATE EDITION 9

1 Current account deficit

(how will it narrow?)

2 Portfolio flows

(at risk from Fed ‘tapering’)

3 Budget deficit

(slow growth = another year of slippage?)

4 Growth

(slow & slowing)

5 Labour troubles

(more of 2012?)

6 Electricity shortages

(a short term risk and a long term bind)

7 Employment

(where will the jobs come from?)

8 Inflation

(risks from the ZAR?)

9 Politics & policy

(policy paralysis as 2014 election nears?)

10 SARB policy reaction function

(what if inflation spikes?)

JULY 2013: WHY ARE FOREIGNERS CONCERNED ABOUT SA? TALK ABOUT A PERFECT STORM…

(ZAR HAD MOVED FROM R8.25/$ TO R10.00 OVER 1 YEAR…

4

RESEARCH UPDATE EDITION 9

1 Current account deficit

Little improvement, strike(s) still to hit

2 Portfolio flows

Still positive, but slower, volatile & at risk

3 Budget deficit

Another year of slippage now very likely

4 Growth

2014 now set to be slower than 2013

5 Labour troubles

Worse, far worse, than 2012/13

6 Electricity shortages

Major blackouts avoided, bind remains

7 Employment

Weak growth & strikes = even less hope

8 Inflation

Surprisingly muted, but pressures building

9 Politics & policy

Hopes remain, but expectations are low

10 SARB policy reaction function

SARB’s position getting more difficult

WHY ARE FOREIGNERS CONCERNED ABOUT SA? ALL REMAINED BAD OR GOT WORSE OVER THE PAST YEAR, TRIGGERING A GENERAL

CONFIDENCE SLUMP AND RATINGS DOWNGRADES…

5

RESEARCH UPDATE EDITION 9

1

• All three above harm economic role

players’ ability & willingness to save

• As a lack of saving can harm investment, a self-feeding vicious circle can occur

2

• C/A financing may not always be available, forcing investment & growth lower

• Current-spending driven fiscal deficit implies:

• limited room for infrastructure

expansion

• risks crowding out private

investment

• raising Govt saving through

higher taxes will lower private

sector saving ability/willingness

• The results of both above may be same as in 1

3

• Both these are bad for growth & saving (the

latter will flee abroad)

• Yet again, the risk of a vicious circle occurs

WHAT DO THE “10 CONCERNS” HAVE TO DO WITH SAVINGS? 10 INDIVIDUAL CONCERNS BOIL DOWN TO 3 BROAD ONES…

6

Slow growth trap,

little employment,

heavy government

dependency

Big deficits Social and/or fiscal

stability at risk?

RESEARCH UPDATE EDITION 9

7

SA SEEKING A GROWTH MODEL; POTENTIAL STUCK AT LESS THAN 3% P.A. SA DID ENJOY FAST GROWTH IN THE 1950/60’S AND AGAIN IN 2003/7

0

2

4

6

8

0

2

4

6

8

50 55 60 65 70 75 80 85 90 95 00 05 10 15 20

Annual GDP growth

5 year moving average

Source: MacroSolutions

RESEARCH UPDATE EDITION 9

WHY DID THE ECONOMY GROW SO FAST IN THE 1950’S & 1960’S? BOOMING MINING STIMULATES INDUSTRY, INFRASTRUCTURE AND TRADE

Mining GDP 1950 – 1971: 5.0 % p.a

Manufacturing GDP 1950 – 1971: 7½% p.a

Construction GDP 1950 – 1971: 6% % p.a 1960 – 1975: 10% p.a.

Trade GDP 1950 – 1970: 5½% p.a.

8

Source: MacroSolutions

RESEARCH UPDATE EDITION 9

9

SA SEEKING A GROWTH MODEL POTENTIAL STUCK AT LESS THAN 3% P.A.

0

2

4

6

8

0

2

4

6

8

50 55 60 65 70 75 80 85 90 95 00 05 10 15 20

Annual GDP growth

5 year moving average

2003/7: What happened here?

1950’/60’s: Mining, Infrastructure & Manufacturing booms

Source: MacroSolutions

RESEARCH UPDATE EDITION 9

10

SA SEEKING A GROWTH MODEL POTENTIAL STUCK AT LESS THAN 3% P.A.

0

2

4

6

8

0

2

4

6

8

50 55 60 65 70 75 80 85 90 95 00 05 10 15 20

Annual GDP growth

5 year moving average

2003/7: Global, Infrastructure & Consumer Credit booms

1950’/60’s: Mining, Infrastructure & Manufacturing booms

Source: MacroSolutions

RESEARCH UPDATE EDITION 9

11

PERHAPS 3% P.A. GDP GROWTH IS NOT AS BAD AS WE THINK…

0

2

4

6

8

0

2

4

6

8

50 55 60 65 70 75 80 85 90 95 00 05 10 15 20

Annual GDP growth

5 year moving average

Annual population growth

3% GDP growth with 1% population growth is as good as 5% GDP growth with 3% population growth

Source: MacroSolutions

RESEARCH UPDATE EDITION 9

12

SO, REAL DISPOSABLE INCOME PER CAPITA HAS RISEN SOLIDLY

SINCE 1995 AND AT THE SAME PACE AS IN THE 1950’S & ‘60’S

12500

15000

17500

21000

10000

25500

12500

15000

17500

21000

10000

25500

50 60 70 80 90 00 10 20

Up 44% since 1995, or some 2% p.a.,

same as in the period 1950’s to early-’70’s

3% GDP growth with 1% population growth

is as good as 5% GDP growth with 3% population growth

Source: MacroSolutions

RESEARCH UPDATE EDITION 9

13

BUT A HUGE BACKLOG HAS OPENED UP DURING 2 DECADES

OF STAGNATION

14000

17500

25000

35000

10000

45000

17500

25000

35000

10000

45000

Had we continued to grow at the rate of the 1950’s & ‘60’s,

overall living standards would have been 50% higher today

and unemployment likely a lot lower

Failure to close the gap risks social-,

financial, fiscal- & policy instability

14000

50 60 70 80 90 00 10 20

Source: MacroSolutions

RESEARCH UPDATE EDITION 9

14

AND, WE HAVE MADE NO PROGRESS WITH UNEMPLOYMENT…

Unemployment rate 4.6m cannot find work

40

35

30

25

20

15

40

35

30

25

20

15 07 08 09 10 11 12 13 14

‘Expanded’ unemployment rate A further 2.2m have given up trying

Source: MacroSolutions

RESEARCH UPDATE EDITION 9

15

…ESPECIALLY YOUTH UNEMPLOYMENT BETTER MATRIC PASS RATES HAVE DONE ZERO FOR THE YOUTH UNEMPLOYMENT RATE

40

50

60

70

30

80

40

50

60

70

30

80

90 92 94 96 98 00 02 04 06 08 10 12 14

Matric pass rate

Unemployment rate for 15 – 24 year-olds

Source: MacroSolutions

RESEARCH UPDATE EDITION 9

OUR JOB SEEKERS FACE HUGE OBSTACLES…

16

SA’s

troublesome

labour

environment

is a huge

obstacle to

job seekers

Labour relations are keeping the

unemployed outsiders out

IMF:

“SA does not

exhibit the

characteristics of

fast job-creating

countries”

Higher quantitative

pass rates, YES

Better qualitative

supply of skills, NO Few get tertiary

education admission (lots then drop out too)

For the rest finding meaningful employment is very, very hard

RESEARCH UPDATE EDITION 9

…AS INCREASING MECHANISATION CLEARLY DEMONSTRATES…

17

100

120

140

160

100

180

120

140

160

180

70 75 80 85 90 95 00 05 10 15

Source: Macquarie Securities

Capital : labour ratio Units of capital per unit of labour used

in all production processes

RESEARCH UPDATE EDITION 9

PRIVATE SECTOR EMPLOYMENT IS INDEED WEAK

18

Source: SA Reserve Bank

RESEARCH UPDATE EDITION 9

SA is a constitutional democracy, politically stable, entrenched property

rights, contract enforcement is high, independent judiciary & high tax compliance

Macro-economic institutions

have credibility & macro

policy generally conservative

Huge mineral wealth,

huge tourism potential & proximity

to Africa are key strengths

Young population with a rapidly growing

middle class & well-developed social security system

are sources of growth & stability

Strong financial sector with sound

regulatory oversight & deep

capital markets

Many world class companies, a solid culture of

entrepreneurship

SA economy generally flexible

(‘survived’ many, many crises)

SA’S MANY STRENGTHS SUGGEST A HIGH GROWTH POTENTIAL

19

RESEARCH UPDATE EDITION 9

THEN WHAT IS THE TROUBLE…?

20

The

economy

is in need

of a

‘growth

driver’

No global boom (driving exports or

commodity prices)

No sector boom (a la mining in the

1950/60’s), stimulating other forms of

activity

No infrastructure boom (big numbers yes, but little net growth)

No consumer credit boom

No big pool of skilled, productive &

competitive labour to attract

production facilities

No Monetary or Fiscal room for

support for the economy

RESEARCH UPDATE EDITION 9

WHAT NEEDS TO BE DONE…?

21

Address cyclical problems:

Current account & fiscal

deficits & inflation pressures

Address the deep distrust

between Govt, Labour and

Business

Create greater policy

certainty, both on a macro

and sectoral level

Address SA’s highly

problematic labour relations

(may include elements of

labour law)

Speed up social &

economic infrastructure

spend (still many

bottlenecks)

Aggressively address

underperforming areas in

the public service (incl

education)

Ensure the more competitive

ZAR is not undermined by

higher inflation

Targeted support for key

industries

RESEARCH UPDATE EDITION 9

CAN, AND WILL, IT BE DONE…?

22

Confidence remains

generally very depressed

and expectations low

• Rating Agencies & analysts

skeptical over Govt’s

willingness to effect the right

reforms

• So, fears of little more than lip-

service to the NDP, despite

Govt’s contrary comments

• India: optimism surges as a

strong, reform-minded

government is elected

Still, an opportunity exists

• Govt bombarded with calls for

growth-enhancing reforms

(sense of crisis is building)

• A good plan is on the table

and Govt has committed to it

• Politics will give 5 years

breathing space (but political

will is still required)

• The Rand is more competitive

• The SARB has shown it will

protect the ZAR’s new-found

competitiveness

• The world economy is looking

better Failure to reform & grow faster risks social,

fiscal & financial instability

RESEARCH UPDATE EDITION 9

Only 2 things

drive savings

1. Ability to save

i.e. need sufficient

income

2. Willingness to save

income available,

choose to save

or not

SA situation • Many simply do not have

ability to save: will rely on

Govt/ family aid

• Many do have ability to

save, but choose not to or

simply fail to realise that

they need to save more

SA HOUSEHOLDS AND SAVINGS

23

RESEARCH UPDATE EDITION 9

SA households save way too little (& make poor investment decisions)

Many, many will discover 3 years into retirement they

could not really afford the luxuries of the previous 25+ yrs

For future

liabilities: kids’

education,

depreciation of residence, etc

For retirement

(most discover this

with a shock, far too late)

DC members:

Largely oblivious as to whether

their retirement

provision is sufficient

I suspect many are badly under-

provided

Discretionary savings often go into low

yielding

investments or ones that lose people all of their capital

DB Members:

Largely oblivious as to whether their

retirement provision is

sufficient

Do not fully consider the possibility of below-

inflation pension increases (requiring

additional provision)

FOR THOSE WHO CAN SAVE…

24

RESEARCH UPDATE EDITION 9

AVERAGE TOTAL RETURNS (% P.A.) 1960 – MAY 2014

25

Sector

10

years

60-69

(%)

10

years

70-79

(%)

10

years

80-89

(%)

10

years

90-99

(%)

15

years

00-14*

(%)

55

years

60-14*

(%)

What we

expect*

(%)

Shares 15.8 21.3 26.7 16.6 18.1 19.6 11.0

LT Gilts 4.5 6.8 11.8 19.5 13.7 11.5 7.5

Cash 4.4 8.2 14.8 16.2 8.6 10.3 6.5

Inflation 2.5 10.3 14.7 9.4 6.2 8.4 5.5

* Our estimates over the longer term

Balanced Fund of 60:30:10

Over 53 years: 16.2% vs 8.4% inflation = 7.8% real

Going forward: 9.6% vs 5½% inflation = 4.1% real

RESEARCH UPDATE EDITION 9

3 5 y e a r s w o r k e d

% saved Inv. Return % of

pension taken

Pension as

% of last salary

13 9.0 6.5 32

30 9.0 6.5 75

13 13.5 6.5 75

13 9.0 15.0 75

17.5 12.0 6.5 75

All examples above assume 9% p.a. salary gain & 6% p.a. inflation

Realistic overall Investment Returns going forward ± 8% - 10% p.a.

(vs 17½% previous 14 years)

Message? Can’t rely on high investment returns to build your capital,

people will have to save far more

HOW MUCH MUST YOU SAVE? – A GUIDE

26

RESEARCH UPDATE EDITION 9

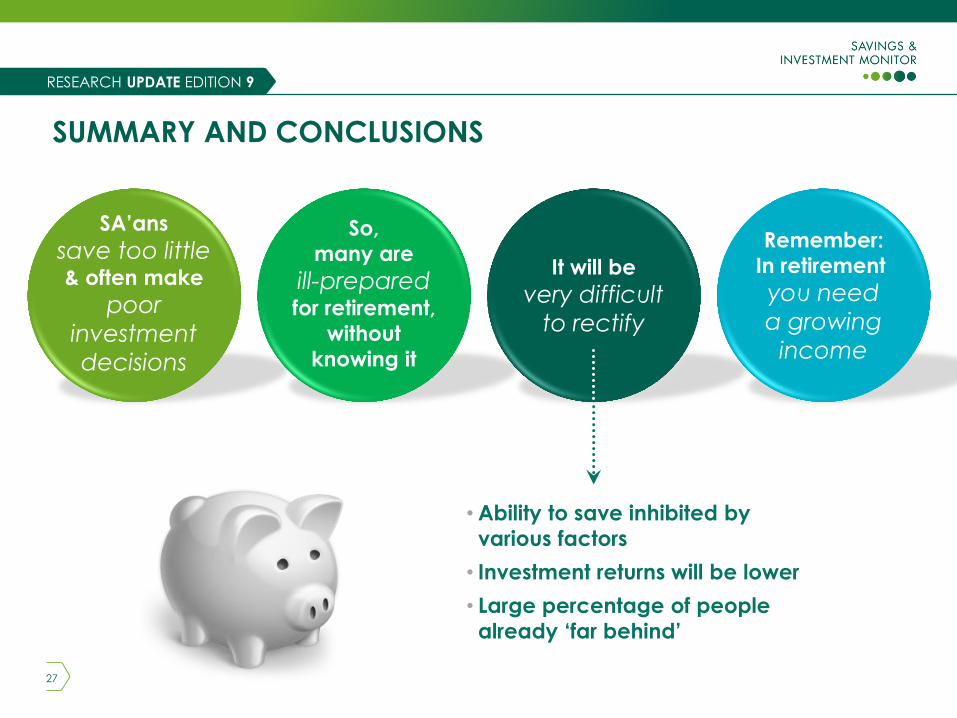

SA’ans

save too little & often make

poor

investment

decisions

So,

many are

ill-prepared for retirement,

without

knowing it

It will be

very difficult

to rectify

Remember:

In retirement

you need

a growing

income

•Ability to save inhibited by

various factors

• Investment returns will be lower

• Large percentage of people

already ‘far behind’

SUMMARY AND CONCLUSIONS

27

RESEARCH UPDATE EDITION 9

The biggest present you

can give your children

is to never become

dependent on them

(retirement provision)

The biggest present you

can give yourself is to

make your children

independent of you

(education)

SOME WISE WORDS SOMEONE ONCE TOLD ME…

28

RESEARCH UPDATE EDITION 9

FULLY understand

your retirement

provisioning

FULLY understand your future liabilities

FULLY consider ALL the risks you

face

Get a consultant to advise you as to

how much you must

save

Stick with renowned institutions

when entrust- ing your

savings for investment

• retirement

• ‘big asset’

replacements

• health

• children’s studies

• caring for parents

and/or children

• inflation

• etc

REMEMBER: Time is your best friend when it comes to capital building

WHAT SHOULD PEOPLE DO NOW? A FEW THINGS...

29

RESEARCH UPDATE EDITION 9

REGULATORY INFORMATION

30

Old Mutual Investment Group (Pty) Limited

Physical Address: Mutualpark, Jan Smuts Drive, Pinelands, 7405

Telephone number: +27 21 509 5022

Old Mutual Investment Group (Pty) Limited (Reg No 1993/003023/07) is a licensed financial services provider, FSP 604, approved by the Registrar of Financial Services Providers (www.fsb.co.za) to provide intermediary services and advice in terms of the Financial Advisory and Intermediary Services Act 37 of 2002. Market fluctuations and changes in rates of exchange or taxation may have an effect on the value, price or income of investments. Since the performance of financial markets fluctuates, an investor may not get back the full amount invested. Past performance is not necessarily a guide to future investment performance. The investment portfolios may be market-linked or policy based. Investors’ rights and obligations are set out in the relevant contracts. In respect of pooled, life wrapped products, the underlying assets are owned by Old Mutual Life Assurance Company (South Africa) Limited who may elect to exercise any votes on these underlying assets independently of Old Mutual Investment Group. In respect of these products, no fees or charges will be deducted if the policy is terminated within the first 30 days. Returns on these products depend on the performance of the underlying assets. Disclosures: Personal trading by staff is restricted to ensure that there is no conflict of interest. All directors and those staff who are likely to have access to price sensitive and unpublished information in relation to the Old Mutual Group are further restricted in their dealings in Old Mutual shares. All employees of the Old Mutual Investment Group are remunerated with salaries and standard incentives. Unless disclosed to the client, no commission or incentives are paid by the Old Mutual Investment Group to any persons other than its representatives. All inter-group transactions are done on an arms length basis. We outsource investment administration of our local funds to Curo Fund Services (Pty) Ltd, 50% of which is owned by the Old Mutual Investment Group. Disclaimer: The contents of this document and, to the extent applicable, the comments by presenters do not constitute advice as defined in FAIS. Although due care has been taken in compiling this document, Old Mutual Investment Group does not warrant the accuracy of the information contained herein and therefore does not accept any liability in respect of any loss you may suffer as a result of your reliance thereon. The processes, policies and business practices described may change from time to time and Old Mutual Investment Group specifically excludes any obligation to communicate such changes to the recipient of this document. Old Mutual Investment Group has comprehensive crime and professional indemnity insurance. For more detail, as well as for information on how to contact us and on how to access information please visit www.oldmutualinvest.com.

THANK YOU

Old Mutual is a Licensed Financial Services Provider

THANK YOU