review of director and executive remuneration in … - corporate... · review of director and...

TRANSCRIPT

Review of Director and Executive Remuneration in New Zealand -response

NZX Consultation Paper – Review of Corporate Governance Code

14th October 2016

Page 2

Overview and contents

Contents of this submission1. Summary of EY’s responses and suggestions:

2. TOR 1: NED remuneration

3. TOR 2: Executive remuneration

4. TOR 3: CEO remuneration

Appendix A: Example remuneration report

Appendix B: Example calculations

Appendix C: EY’s independence policy

Susan Doughty

Partner

People Advisory Services

Tel: 0275447237

Rohini Ram

Partner

People Advisory Services

Our submission may be relied upon by the NZX Limited pursuant to the scope of the submission request only, as outlined in the Consultation Paper, dated 31 August 2016. The submission represents our comments on director and executive remuneration only; it does not address any related legal issues. We disclaim all responsibility to any other party for any loss or liability that the other party may suffer or incur arising from or relating to or in any way connected with the contents of our submission, the provision of our submission to the other party or the reliance upon our submission by the other party.

Overview

Ernst & Young Limited (EY) are pleased to provide this submission to the NZX.

EY has reviewed the NZX’s Consultation Paper on the “Review of the NZX Corporate Governance Code” 31 August 2016.

This submission provides our responses to proposed amendments and recommendations related to Principle 5 – Remuneration including the questions related to this Principle. We have combined our responses to questions where we perceived there to be some overlap in the areas under discussion.

Our views and comments are based on our experience working with NZ, Australian and overseas company boards and management on a range of executive reward-related issues.

If there are any areas of this submission that you would like us to expand upon further, we would be pleased to discuss these with you.

Summary of EY’s response and suggestions

Page 4

Summary: EY’s response and suggestions

EY welcomes NZX’s review of non-executive director and executive remuneration reporting and hopes that the outcomes will support the needs of New Zealand business, the New Zealand corporate governance framework and shareholders.

The following provides a summary of EY’s response to Principle 5 – Remuneration and each Term of Reference (TOR).

Term of Reference 1: Non-Executive Remuneration (NED)► EY supports this recommendation. Non-executive Director remuneration should be clearly differentiated to that provided to executives. ► EY suggest that a NED remuneration reporting format be adopted (example provided).

Term of Reference 2: Executive remuneration► EY is in support of this recommendation as it provides a strong framework of understanding for shareholders and brings the NZ governance practice closer for executive

remuneration to that in other markets.► EY would not support, in its entirety, the highly prescriptive and detailed requirements applied in Australia and some other markets, however do support a simple and

consistent framework that can easily be interpreted by shareholders.► EY acknowledges that how remuneration is structured is highly dependent on the company’s business strategy and culture and should be determined by the company not

regulation.► EY support the adoption of the definition of “senior manager” as described by the Financial Markets Conduct Act 2013.► EY do not endorse the full disclosure of STI measures and targets► EY would support a clear and appropriate definition of the meaning intended on “performance hurdles”► EY support the use of “informed judgement (often referred to as “discretion”) and suggest that business parameters are applied in exercising judgement.► The NZX is silent on the definition of independence related remuneration consultants. EY, in principle, do not support the use of the world “independent” as this can be

open to interpretation and subject to confusion. NZ is also a small market with limited qualified remuneration specialists that can provide necessary advice. Therefore any additional restrictions could have a negative impact on what organisations seek to achieve.

► EY and the other “Big” Firms p

Page 5

Summary: EY’s response and suggestions

Term of Reference 3: CEO remuneration► EY supports the NZX’s recommendation that CEO potential and actual remuneration is clearly disclosed for both current and prior years.► EY encourage the NZX to ensure that the drafting of any new guidelines be cognisant of the range of equity vehicles and avoid references to single equity vehicles such as

Options.► EY ask that the NZX considers the guidelines for issuers specifically related to the accounting treatment of equity incentives (see Appendix B).► EY ask the NZX to consider adopting the Australian practice of reporting the “accounting cost”, but in conjunction with how the company itself ascribes values to each

remuneration element.

Principle 5: Remuneration

Page 7

Principle 5: Remuneration

EY has elected to respond to the recommendations put forward by NZX Limited related to Principle 5: Remuneration.

Term of reference:In responding to the Consultation document, we have classified our response in line with the following terms of reference (TOR) under Principle 5:

1. TOR 1: “Every issuer should have a formal and transparent method to recommend director remuneration packages to shareholders. Actual director remuneration should be should be clearly disclosed”;

2. TOR 2: “Issuers should publish a remuneration policy dealing with remuneration of directors and senior executives. The remuneration policy in relation to executive executive remuneration should outline the relative weightings of remuneration components and relevant performance criteria”;

3. TOR 3: “Issuers should disclose the remuneration arrangements in place for the CEO. This should include disclosure of the base salary, short term incentives and long term long term incentives and the performance criteria used to determine performance based payments”.

We have combined our responses to questions where we perceive there to be some overlap in the areas under discussion.

TOR 1: Non-executive Director remunerationTerm of reference: “Every issuer should have a formal and transparent method to recommend director remuneration packages to shareholders. Actual director remuneration should be clearly disclosed”

Page 9

TOR: 1 – Non-executive Director remuneration (NED)

NZX term of reference

“Every issuer should have a formal and transparent method to recommend director remuneration packages to shareholders. Actual director remuneration clearly disclosed”.

EY’s response

EY is in support of this recommendation. It is broadly understood that non-executive director (NED) remuneration should be clearly differentiated to that provided to ensure there is a clear line of demarcation between performance-based rewards and fees for services to the Board.

NED remuneration is significantly different, and rightly so, from executive remuneration. NEDs generally do not have any variable remuneration which is in contrast to where this is considered a primary component of the package. As a guideline, we refer to the ASX Corporate Governance Council Guidelines which specifically state that should “not normally participate in schemes designed for the remuneration of executives” and “should not receive options or bonus payments”. The typical profile of remuneration is illustrated below.

Element Definition Market practice insights

Base fee ► Annual fixed sum of money paid to a NED.

► Fee amount is determined by the Board.

► This is the typical structure for fees in the NZ market.

Committee fee ► Annual fixed sum of money paid to a NED who sits on a committee. ► There is the increasing use of member committee fees to recognise the added workload on Directors for some committees, i.e. Audit & Risk and Remuneration.

Committee Chair fee ► Annual fixed sum of money paid to a NED who is a committee chair. ► Fees are not generally paid to the Chairman of the Board to attend or chair committee fees, as base fees are typically set to recognise the additional workload of the chair.

Fixe

d re

mun

erat

ion

Key elements of NED remuneration

Page 10

Non-executive remuneration – contextual drivers

Driver Comments

1. Changing role of the NED The role of NED in NZ companies continues to evolve, with increased:

► oversight responsibility as governance guidelines evolve and public scrutiny increases.

► Scope and size of NZ companies (including expanded geographical operations).

► Accountability and liability for health and safety and other risks.

Organisations will face varying degrees of complexity depending on the maturity of the company, the markets they operate in and the growth strategy. Fees recognise these inherent challenges. As an example, we have seen an increase in Audit & Risk committee fees.

3. Comparator (peer) group The competition for attracting appropriately skilled NED talent is emerging as common factor when considering peer groups. Primarily Boards are concerned

► Ability to attract NED talent from a limited pool of professional directors (in NZ).

► Ability to recruit the necessary NED talent with the appropriate skills and capabilities required on the Board.

Where these factors are critical, fees may be set at a level to attract the required NED profile to the Board.

2. Market positioning policy Setting a rationale for a market positioning policy provides a clear understanding of the factors taken into account for the recommended fees. A median market NED fees is common practice in NZ however we note that a number of companies set their position above the median (often at the 75th percentile) against their This is acceptable when an appropriate comparator group has been established and rationale explained.

A clear understanding of the broad comparator group, e.g. companies within a size range.

Increases in NED remuneration has been primarily driven by the changing role of the NED, availability of talent and market positioning policies.

The following are key considerations in setting NED remuneration that could serve as high level guidelines.

Page 11

Suggested remuneration report format - NEDs

Topic Contents

Market policy► A clear statement regarding the market policy for where Directors’ fees will be positioned, e.g. around the 50th percentile of

the comparator group.

Market comparator group► A statement on how the comparator group is established.

Nature of remuneration

► A clear statement of the make up of Directors’ remuneration including committee fees and actual fees paid

► A statement that NEDs will not typically be subject to executive performance-based arrangements, such as incentives or options.

► Where a portion of fees is settled in equity

Fee pool► The total fee pool applied.

Disclosure of all remuneration

► Full disclosure of all remuneration received; ex gratia payments or other irregular payments.

Review cycle► The cycle on which Director fees’ will be reviewed, i.e. one year or 2 yearly.

In EY’s opinion the reporting structure of the Director remuneration policy should include the following key statements:

TOR 2: Executive remuneration

Term of reference: “The remuneration policy in relation to executive remuneration should outline the relative weightings of remuneration components and relevant relevant performance criteria”.

Page 13

TOR: 2 – Executive remuneration policy

Executive remuneration

NZ has lagged the major markets in its approach to remuneration disclosure requirements and standards of reporting.

Unlike NED remuneration, there is very little transparency in executive remuneration - which has become a key area of interest for investors and other stakeholders. and drivers of remuneration play a key part in supporting business strategy and company performance. Therefore more clarity is required to ensure investors can understanding of practice within the organisation.

EY’s response

EY is in support of TOR 2 as it provides a strong framework of understanding for shareholders and brings the NZ governance practice closer for executive remuneration to applied in other markets.

Although the NZX has stopped short of recommending disclosure of actual remuneration outcomes for executives (other than the CEO) due to the commercially sensitive this information, and the desire to avoid an additional compliance burden, EY believe that clear remuneration policy guidelines on the degree of information required to (fixed remuneration, STI and LTI) should be provided to issuers. This will enhance an investor’s understanding of remuneration practice and the key elements that drive policy development.

EY would not support, in their entirety, the highly prescriptive and detailed requirements applied in Australia and some other markets, however do support a simple and framework that can easily be interpreted by shareholders.

Page 14

TOR: 2 – policy development

Structure of executive remuneration

We note that the NZX has not recommended a prescribed definition for ‘senior executives’, although this may align with the ‘senior manager’ definition within the Financial Markets Conduct Act 2013.

The definition states: a “senior manager, in relation to a person (A), means a person who is not a director but occupies a position that allows that person to exercise significant influence over the management or administration of A (for example, a chief executive or a chief financial officer)”.

Structure of executive remuneration

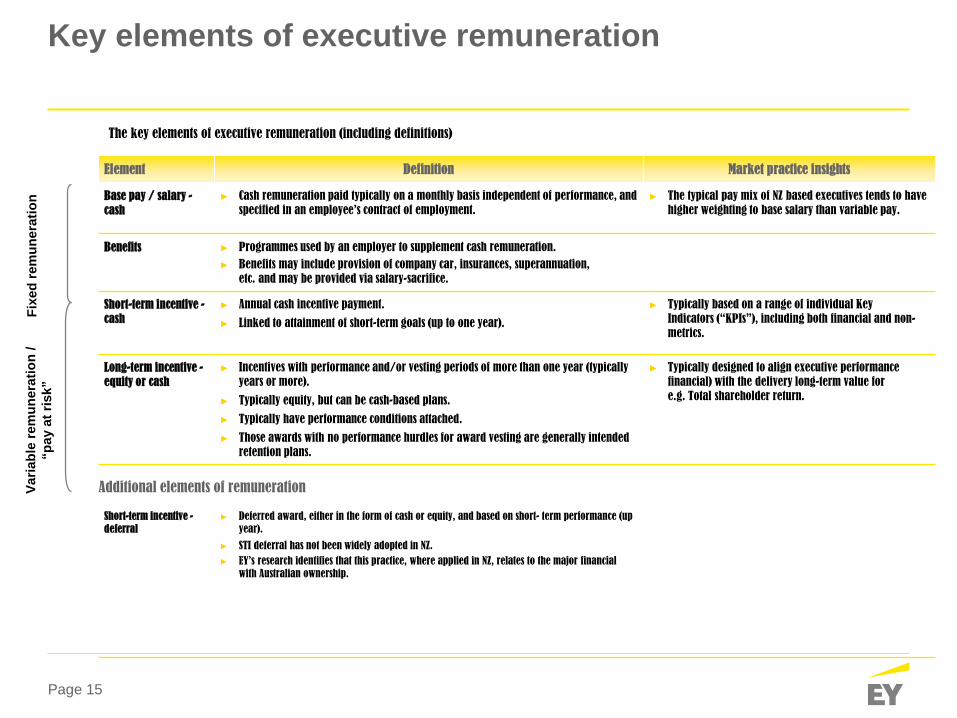

The key elements of executive remuneration are set out on the following page. As each of these components can be described differently by organisations, standard reporting of the elements of executive packages could help ensure consistency across reporting by issuers which will benefit shareholders and other stakeholders.

EY’s response

EY supports the use of the Financial Markets definition of “senior manager”.

EY acknowledges that how remuneration is structured is highly dependent on the company’s business strategy and culture and should be determined by the company not regulation.

Page 15

Key elements of executive remuneration

Element Definition Market practice insights

Base pay / salary -cash

► Cash remuneration paid typically on a monthly basis independent of performance, and specified in an employee’s contract of employment.

► The typical pay mix of NZ based executives tends to have higher weighting to base salary than variable pay.

Benefits ► Programmes used by an employer to supplement cash remuneration. ► Benefits may include provision of company car, insurances, superannuation,

etc. and may be provided via salary-sacrifice.

Short-term incentive -cash

► Annual cash incentive payment.

► Linked to attainment of short-term goals (up to one year).

► Typically based on a range of individual Key Indicators (“KPIs”), including both financial and non-metrics.

Long-term incentive -equity or cash

► Incentives with performance and/or vesting periods of more than one year (typically years or more).

► Typically equity, but can be cash-based plans.

► Typically have performance conditions attached.

► Those awards with no performance hurdles for award vesting are generally intended retention plans.

► Typically designed to align executive performance financial) with the delivery long-term value for e.g. Total shareholder return.

Fixe

d re

mun

erat

ion

Varia

ble

rem

uner

atio

n /

“pay

at r

isk”

► The key elements of executive remuneration (including definitions)

Short-term incentive -deferral

► Deferred award, either in the form of cash or equity, and based on short- term performance (up year).

► STI deferral has not been widely adopted in NZ. ► EY’s research identifies that this practice, where applied in NZ, relates to the major financial

with Australian ownership.

Additional elements of remuneration

Page 16

TOR 2: Performance hurdles and use of discretion

Performance Hurdles

The NZX has recommended the disclosure of performance hurdles for both short and long-term incentives plans, however have not defined the term “performance level of information required associated with this term.

In EY’s experience, “performance hurdles”, “performance measures” and “KPIs/objectives” can be used interchangeably by organisations. Therefore clarity is whether the definition relates to:

► A gating mechanism (hurdle) that must be achieved prior to any rewards being paid; and/or► Once the scheme is activated (past the gate) whether all performance measures are disclosed within short and long-term incentive plans; and► Whether the intent is to provide a description of the measure and/or the disclosure of the target.

Short-term incentive plans often incorporate a range of performance measures (hurdles), particularly if a balanced scorecard is applied (which is common practice organisations).

Commercially sensitive performance targets

Where LTI measures are company-specific and commercially sensitive, and therefore are not disclosed, retrospective disclosure of targets or parameters should be We recognise that in some limited circumstances these may still be commercially sensitive, and not appropriate for disclosure.

However, we believe that STI measures and targets should be treated differently. We note that business performance measures/targets for STIs are typically company-that public disclosure of the detail could be strategically disadvantageous for companies.

EY’s response

► EY would not endorse the full disclosure of STI measures and targets.

► EY would support a clear and appropriate definition of the meaning intended on “performance hurdles”.

Page 17

TOR 2: Performance hurdles and use of discretion

Discretion

EY support the use of “informed judgement” (often referred to as “discretion”) by the Board, and suggest that business parameters are applied in exercising

► We find that the use of discretion is an increasingly important consideration in both NZ and Australian organisations to ensure that structured (formulaic) outcomes are balanced by the Board against broader organisational factors. As shareholders increase their focus on pay for performance and alignment of pay business outcomes, the questions of whether and how to exercise judgement in variable pay programmes has become an increasing area of interest.

► There is a general expectation by shareholders that business judgment will be exercised to ensure pay-outs are appropriate and in line with the performance of business. This is inherently challenging as shareholders may hold views related to performance that differs to the Board, who often have more insight into given the Board’s involvement in the business.

► There is an expectation that the parameters under which informed judgement will be applied is broadly laid out within a company’s remuneration policy. As

► Major conduct risk issues► Major health & safety breaches► Major reputational risk impact.

Please note these are examples only and will vary across organisations depending on the range of major risk factors impacting each business.

Page 18

TOR 2: Independence of Remuneration Advisers

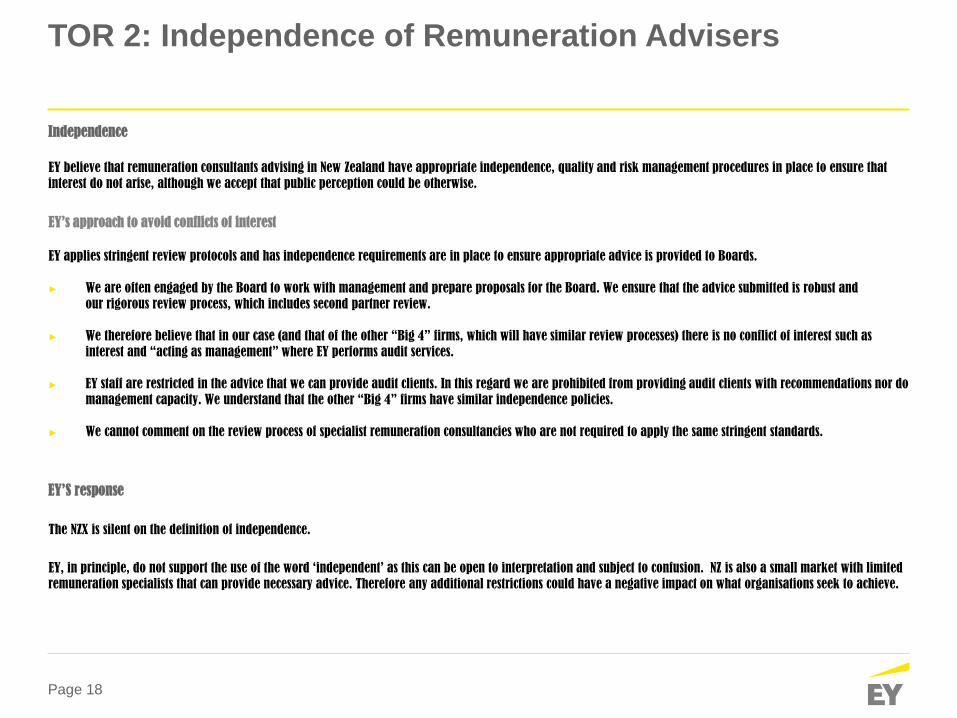

Independence

EY believe that remuneration consultants advising in New Zealand have appropriate independence, quality and risk management procedures in place to ensure that interest do not arise, although we accept that public perception could be otherwise.

EY’s approach to avoid conflicts of interest

EY applies stringent review protocols and has independence requirements are in place to ensure appropriate advice is provided to Boards.

► We are often engaged by the Board to work with management and prepare proposals for the Board. We ensure that the advice submitted is robust and our rigorous review process, which includes second partner review.

► We therefore believe that in our case (and that of the other “Big 4” firms, which will have similar review processes) there is no conflict of interest such as interest and “acting as management” where EY performs audit services.

► EY staff are restricted in the advice that we can provide audit clients. In this regard we are prohibited from providing audit clients with recommendations nor do management capacity. We understand that the other “Big 4” firms have similar independence policies.

► We cannot comment on the review process of specialist remuneration consultancies who are not required to apply the same stringent standards.

EY’S response

The NZX is silent on the definition of independence.

EY, in principle, do not support the use of the word ‘independent’ as this can be open to interpretation and subject to confusion. NZ is also a small market with limited remuneration specialists that can provide necessary advice. Therefore any additional restrictions could have a negative impact on what organisations seek to achieve.

TOR 3: CEO remuneration

Term of reference: “TOR 3: “Issuers should disclose the remuneration arrangements in place for the CEO. This should include disclosure of the base salary, short term incentives and long term incentives and the performance criteria used to determine performance based payments”.

Page 20

TOR 3: CEO remuneration

We believe that there is significant cross over between the proposed recommendations for executive remuneration and that of the CEO.

EY’s response

EY support the NZX’s recommendation that CEO potential and actual remuneration is clearly disclosed for both current and prior years.

In support of this recommendation we would ask that the NZX consider the guidelines for issuers specifically related to:

► The accounting treatment for any equity incentives► The challenges with attributing a value to equity grants► Common misperceptions and areas of confusion in relation to executive remuneration.

We have expanded on each of these in the following section.

Page 21

Different types of equity in executive incentive plans

Equity Vehicles

Equity can be delivered via a range of vehicles, including:

► Share options: Participants receive a right to acquire shares for a certain exercise price. Performance and service conditions for vesting usually apply (in New Zealand and Australia). The exercise price is typically equivalent to market value of the shares at date of award, but can also be at a discount or premium.

► Performance rights: Participants receive a right to acquire shares for nil consideration at a later date subject to satisfaction of certain vesting conditions, based on performance and service (in essence, a share option with a zero exercise price).

► Performance shares: Participants acquire shares immediately, with full legal ownership subject to satisfaction of certain vesting conditions, based on performance and service.

► Restricted shares: Participants acquire shares immediately, with full legal ownership subject to satisfaction of certain vesting conditions, based on their employment with the company.

► Loan share plans: Participants receive a loan (usually limited recourse) from the company to acquire shares. Performance and service conditions may apply.

EY’s response

EY encourage the NZX to ensure that the drafting of any new guidelines be cognisant of the range of equity vehicles (as outlined above) and avoid references to single vehicles such as Options, as the accounting treatment for vehicles is different (refer illustrations contained in Appendix A.)

Page 22

Overview of accounting treatment of equity incentives

Accounting treatment

The accounting treatment that applies to equity incentives (and to cash-based incentives where the value is linked to the equity price) is complex.

As the presentation of actual values can vary based on the valuation methodology applied, variable performance conditions used and expensing arrangements EY NZX to consider how equity values are to be reported.

We would note that the definition of “actual payments” is not provided. Reaching a meaningful conclusion on this definition remains a constant challenge for on the experiences we have observed in both Australia and the UK. We note in particular that, in Australia, the Productivity Commission and CAMAC ran significant this matter and have not yet provided a final recommendation that can be easily applied by organisations.

To illustrate the difficulties we have outlined worked examples in Appendix A of the different methodologies and interpretations that can be applied.

Potential remuneration

Actual remuneration should reflect the quantum available to the individual at the end of any relevant service period (which, in some cases, could be longer than the period). For example, an LTI could have a 3 year performance period, but a further one year service period. The quantum would be determined at the end of the

For simplicity, the NZX could consider adopting the Australian practice of reporting the “accounting cost”, but in conjunction with how the company itself ascribes remuneration element, e.g. STI target = X% of Fixed Remuneration and LTI grant = Y% of Fixed Remuneration with the method by which the dollar value of the LTI determined.

Example remuneration report

Appendix A

Page 24

The ‘ideal’ remuneration report

Remuneration Report – Key Features

► In our experience, companies recognise that the remuneration report is the primary method of communicating their remuneration approach to

► However as issuers have not been specifically directed to disclose detailed information, many companies choose to disclose the minimum levels of number of employees within each remuneration band range >$100,000. It is our opinion that this practice provides very little clarity to interested

► In addition, information relating to the overarching remuneration policy and structure of executive remuneration elements is either missing or highly

In EY’s opinion it is important that there is a consistent approach across listed companies in how remuneration elements are addressed within the remuneration

To assist the NZX in considering appropriate guidelines for the remuneration policy reporting, we have outlined a remuneration report structure for

Page 25

Remuneration report example

Topic Contents

Executives

Overview / summary

► Description of the company’s executive remuneration framework in terms of fixed remuneration and incentives, noting any key changes to framework in the current year.

► Key details of current year approach: incentive payments (and vesting) and rationale, termination payments and rationale, and any one-payments.

► Details of any expected reviews of, or changes to, remuneration structures in the coming year.

Remuneration strategy► Remuneration objectives, approach to quantum, approach to remuneration mix, key objectives of each remuneration element (e.g., fixed

remuneration, incentives, retention payments) and details of any significant changes.

Incentive plans

► Detailed plan descriptions, including overview of the performance measures in the plan, rationale for their selection, their weightings and schedules.

► An exception should be provided for targets that are commercially sensitive, which will typically apply only to plans with short-term targets, but may apply to other incentive plans that use company-specific commercially sensitive targets.

► Details of any outstanding equity grants (i.e., name of plan, grant date, award vehicle, number of instruments and vesting dates, but not accounting value of the awards).

Remuneration opportunity & contracts

Summary of each executive’s remuneration opportunity for the year:

► Fixed remuneration (as at the start of the year and any amendments made during the year).

► Cash incentive opportunities (target and maximum, to the extent the company has specified opportunities).

► Equity incentive opportunities (expressed as a dollar value or a percentage of fixed remuneration with an explanation regarding how this converted into a number of equity instruments).

Contractual information:

► Length of contract, notice periods, sign-on arrangements, termination entitlements and details of any guaranteed payments.

The following example refers only to executive and CEO remuneration and is not intended to cover Non-Executive Director remuneration. A sample report was provided in TOR 1: Non-executive remuneration.

Page 26

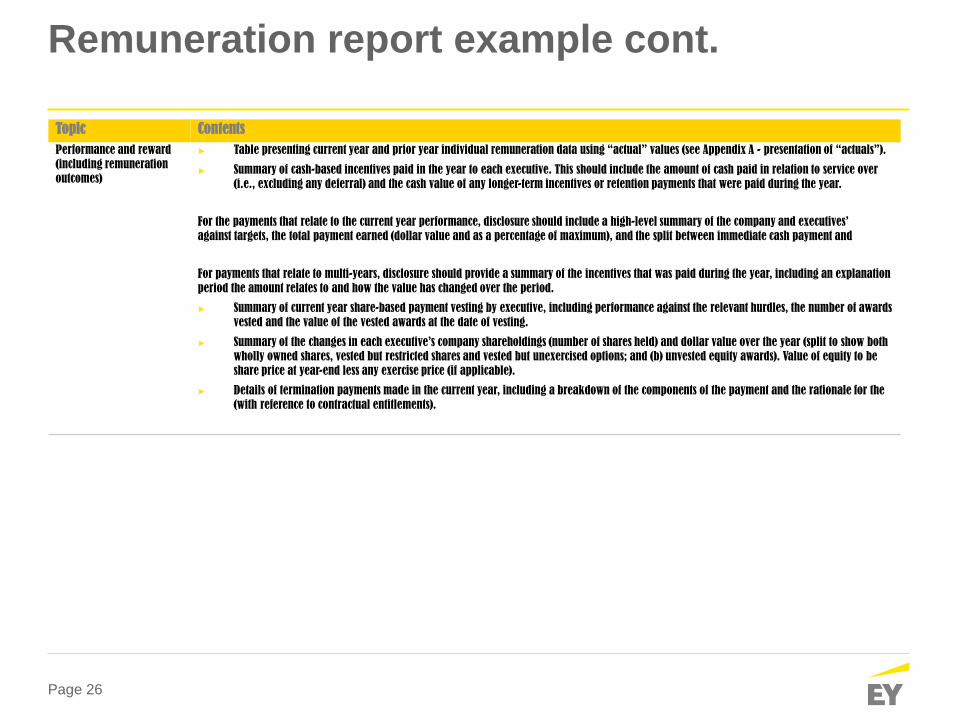

Remuneration report example cont.

Topic ContentsPerformance and reward (including remuneration outcomes)

► Table presenting current year and prior year individual remuneration data using “actual” values (see Appendix A - presentation of “actuals”).

► Summary of cash-based incentives paid in the year to each executive. This should include the amount of cash paid in relation to service over (i.e., excluding any deferral) and the cash value of any longer-term incentives or retention payments that were paid during the year.

For the payments that relate to the current year performance, disclosure should include a high-level summary of the company and executives’ against targets, the total payment earned (dollar value and as a percentage of maximum), and the split between immediate cash payment and

For payments that relate to multi-years, disclosure should provide a summary of the incentives that was paid during the year, including an explanation period the amount relates to and how the value has changed over the period.

► Summary of current year share-based payment vesting by executive, including performance against the relevant hurdles, the number of awards vested and the value of the vested awards at the date of vesting.

► Summary of the changes in each executive’s company shareholdings (number of shares held) and dollar value over the year (split to show both wholly owned shares, vested but restricted shares and vested but unexercised options; and (b) unvested equity awards). Value of equity to be share price at year-end less any exercise price (if applicable).

► Details of termination payments made in the current year, including a breakdown of the components of the payment and the rationale for the (with reference to contractual entitlements).

Approaches to attributing a value to equity incentivesAppendix B

Page 28

Appendix B: Approaches to attributing a value to equity incentives –overview

28

Difficulties associated with determining the appropriate value

Of particular importance in defining remuneration is the value attributed to equity incentives. There are various approaches to defining the value of equity incentives, and the choice of approach can have a significant impact on the value.

There is no one best approach to use for all scenarios – the most appropriate approach will depend on the context in which the definition is used.

Possible approaches

The possible approaches can be split broadly into those that reflect the cost to the company / shareholders vs. those that reflect the value to the individual.

There is no approach which accurately reflects the perceived value of the equity incentive to both the shareholders and the individual, which makes it difficult to make broad statements about the value of any one equity grant.

Additionally, we note that the different approaches reflect “values” at different times (e.g. the “accounting value at grant” is a prospective valuation at grant, whereas the “gain at vesting” is measured at vesting).

The approaches (described and illustrated on the following slides) and their corresponding values, based on the assumptions in our examples, are:

Approaches that reflect the cost to the company:

► Accounting value at grant

► Value disclosed

Approaches that reflect the gain to the individual:

► The projected value

► The gain at vesting

Page 29

Appendix B: Accounting treatment of equity incentives – worked examples

Example 1 Summary

Year 1 Year 2 Year 3 Total

Expense $20K $20k $20k $60k

Gain to executive from grant

$0 $0 $0 $0

Example 2 Summary

Year 1 Year 2 Year 3 Total

Expense $30k $30k ($60k) $0k

Gain to executive from grant

$0 $0 $0 $0

Element Example 1: Performance Rights with TSR performance hurdle Example 2: Performance Rights with EPS performance hurdle

Grant ► 10,000 performance rights granted at a share price of $10 (i.e.; the face value rights at grant is $100k)

► 10,000 performance rights granted at a share price of $10 (i.e.; the face value rights at grant is $100k)

Performance / vesting period ► 3 years ► 3 years

Illustrative “Fair value” pre performance adjustment

► $90k (takes into account that individual will not receive dividends during the 3-performance testing period)

► $90k

Illustrative “Fair value” post performance adjustment

► The “fair value” that incorporates the TSR hurdle (as TSR is a market based condition) is, say, $60k.

► The “fair value” that does not incorporate the EPS hurdle (as EPS is a non-based condition) is, say, $90k.

Expense ► The $60k will be expensed over the 3-year vesting period (i.e., $20k each ► The $90k will be expensed over the 3-year period (i.e., $30k each year).

Expense reversal? ► The performance condition is not met, and the expense cannot be reversed (as market-based condition).

► The performance condition is not met, but the expense can be reversed (as it is non-market based condition).

Expense to company vs.gain to individual

► The total expense to the company will be $60k, but the gain to the executive $0k.

► The total expense to the company will be $0k, which is aligned with the gain to executive, also $0k.

The following examples show how “actual” values can differ significantly based on the performance hurdles applied.

Page 30

Approaches to attributing a value to equity incentives - illustrative examples (assumptions)

Element Assumption

Grant ► 10,000 performance rights

Performance / vesting period► 3 years (also granted prior year if required for example – relevant to Remuneration Report value

example).

Share price at grant ► $10

Share price at vesting / Projected (i.e. best guess at time grant) share price at vesting

► $11 / $12

Accounting value

► Example 1 using TSR (i.e., incorporating the performance hurdle) is 60% of face value (i.e., 60% of share price multiplied by the number of rights).

► Example 2 using EPS (i.e., not incorporating the performance hurdle) is 90% of face value (i.e., the share price multiplied by the number of rights).

Vesting ► For simplicity, we assume that all the awards will vest.

Assumptions applied for illustrations

Page 31

Approaches to attributing a value to equity incentives – illustrative examples

31

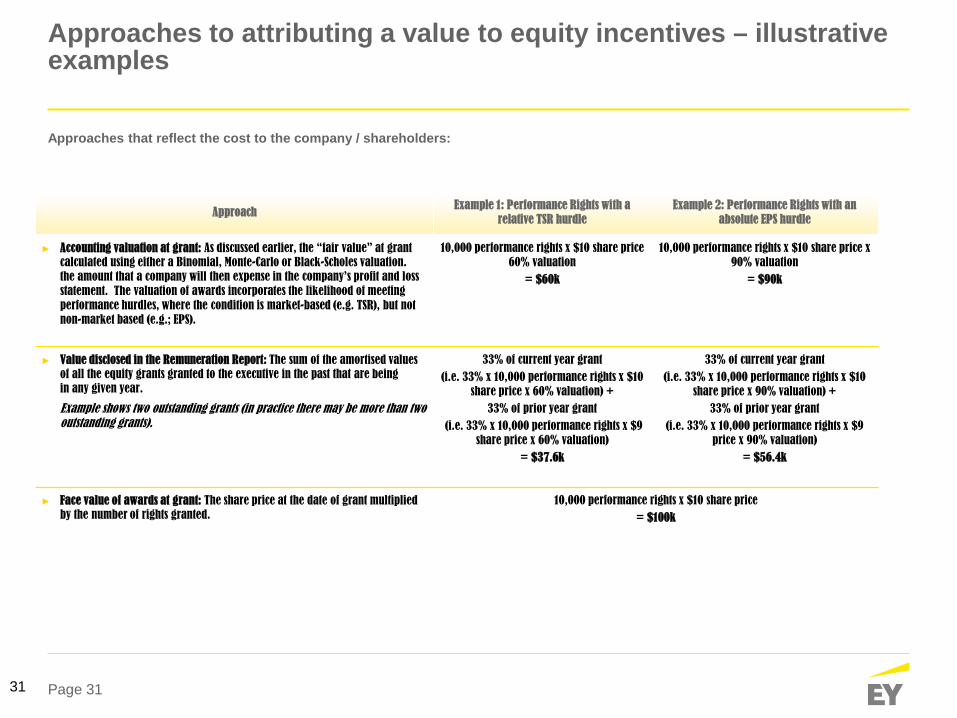

Approaches that reflect the cost to the company / shareholders:

ApproachExample 1: Performance Rights with a

relative TSR hurdleExample 2: Performance Rights with an

absolute EPS hurdle

► Accounting valuation at grant: As discussed earlier, the “fair value” at grant calculated using either a Binomial, Monte-Carlo or Black-Scholes valuation. the amount that a company will then expense in the company’s profit and loss statement. The valuation of awards incorporates the likelihood of meeting performance hurdles, where the condition is market-based (e.g. TSR), but not non-market based (e.g.; EPS).

10,000 performance rights x $10 share price 60% valuation

= $60k

10,000 performance rights x $10 share price x 90% valuation

= $90k

► Value disclosed in the Remuneration Report: The sum of the amortised values of all the equity grants granted to the executive in the past that are being in any given year.

Example shows two outstanding grants (in practice there may be more than two outstanding grants).

33% of current year grant (i.e. 33% x 10,000 performance rights x $10

share price x 60% valuation) + 33% of prior year grant

(i.e. 33% x 10,000 performance rights x $9 share price x 60% valuation)

= $37.6k

33% of current year grant (i.e. 33% x 10,000 performance rights x $10

share price x 90% valuation) + 33% of prior year grant

(i.e. 33% x 10,000 performance rights x $9 price x 90% valuation)

= $56.4k

► Face value of awards at grant: The share price at the date of grant multiplied by the number of rights granted.

10,000 performance rights x $10 share price= $100k

Page 32

Approaches to attributing a value to equity incentives –illustrative examples

Approaches that reflect the value to the individual

ApproachExample 1: Performance Rights with a relative TSR

hurdleExample 2: Performance Rights with an absolute EPS

hurdle

► The projected value: An estimate of the gain that may be delivered to the individual from current year grants based on price and performance assumptions.

10,000 performance rights x $12 share price= $120k

► The gain at vesting: The gain to the individual at the vesting date (i.e.; the difference between the potential sale price at and the cost to exercise).

10,000 performance rights x $11 share price= $110k

Page 33

Appendix C. EY’s independence policy

Ernst & Young are precluded from providing the following to Ernst & Young’s audit clients: ► Entering into a business relationship such as a joint venture or similar arrangement;► Personal appointments, such as serving as officer or director;► Acting as client management;► Providing certain staff secondment services;► Performing most bookkeeping and payroll services;► Performing certain valuation services;► Forecasts or projections;► Trustee appointments;► Administering share or pension plans;► Performing certain legal services; or► Performing liquidations and certain types of merger, disposal, and financing transaction services.

Specific applications for Ernst & Young’s team mean that, for audit clients, Ernst & Young are unable to:► Provide recommendations or any certification in regard to the Company’s remuneration arrangements and any advice in regard to the appropriateness or reasonableness

of an individual’s quantum or remuneration level;► Make any decisions regarding the remuneration strategy or structures at the Company, but rather, we can provide advice to the Board in its decision-making capacity;► Undertake any functions that are or should be undertaken by management; ► Provide legal or contractual reviews, legal drafting, provision of administration services in respect of remuneration matters, executive / staff search and selection,

secondment of EY staff to the client, or the provision of services relating to certain types of tax representation, handling of funds, or work that will impact the financial results of the Company or its internal control functions.

Note that we agree with the client the strict definition of our role and who we are reporting to within the company at engagement commencement

Page 34

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organisation, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about organization, please visit ey.com.

© 2016 Ernst & Young, New Zealand.All Rights Reserved.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other advice. Please refer to your advisors for specific advice.

ey.com/nz