review of market practice in executive remuneration · pdf filereview of market practice in...

TRANSCRIPT

H E A L T H W E A L T H C A R E E R

R E V I E W O F M A R K E TP R A C T I C E I NE X E C U T I V ER E M U N E R AT I O N

19 January 2017

Sophie Black

© MERCER 2016 2© MERCER 2017 2

R E V I E W O F D E V E L O P M E N TSIN CORPORATEG O V E R N A NC E

© MERCER 2017 3

This presentation covers:

1. ISS updates to UK Proxy Voting Guidelines and pay-for-performance analysis

2. Hermes and LGIM remuneration guidelines

3. The Investment Association’s updated Principles of Remuneration

4. The UK Prime Minister’s statements on executive remuneration and the BEIS consultation

5. GC100’s updated reporting guidance

6. Executive Remuneration Working Group’s simplification project

U P D A T E O N R E C E N T D E V E L O P M E N T S I N C O R P O R A T EG O V E R N A N C E O V E R T H E L A S T F E W M O N T H S

© MERCER 2017 4

R E C E N T C O R P O R A T E G O V E R N A N C E D E V E L O P M E N T SF O C U S O N P A Y - F O R - P E R F O R M A N C E A N D B U I L D I N GS H A R E H O L D E R T R U S T

Key themes:

● Increasing trust between companies and their employees and shareholders through increased transparency

● Continued focus on pay-for-performance – companies should explain how the pay outcomes reflect company performance

● Simplified pay structures tailored to the strategy and business needs of the company

● Long-term alignment of executives with shareholders through higher holding requirements that should be maintained post-exit

Recent development HighlightsISS updates to UK Proxy VotingGuidelines(November 2016)ISS will be publishing theirupdated guidelines soon

● Updates include:− Acknowledgement of the ERWG’s conclusions; ISS expects that structures with greater certainty of reward should provide

lower levels of award− ISS will potentially recommend a vote against the RemCo Chair in the event of serious breaches of good practice− ISS expects appropriate pro-rating of outstanding share awards in termination scenarios

ISS pay-for-performancemethodology(November 16)

● Extending its pay-for-performance analysis to an additional c.500 European-based companies. Will include the largest 455UK-listed companies (cf. top 200 currently)

● Relative pay-for-performance analysis will now include assessments based on ROE, ROA, ROIC, revenue growth, EBITDAgrowth, and cash flow, as well as TSR

Hermes updatedRemuneration Guidelines(November 2016)

● Hermes has asked companies to consider:− A shareholder-approved ex-ante total cap on overall pay as well as for individual components− Fixed share awards plus a single incentive scheme reflecting primarily strategic goals, together with operational and

personal objectives (e.g. performance-granting)− Capturing TSR as an underpin− Increased emphasis on long-term executive share ownership− Disclosure of a CEO-to-employee pay ratio− Annual letter from the RemCo Chair to employees to explain the CEO pay award

© MERCER 2017 5

R E C E N T C O R P O R A T E G O V E R N A N C E D E V E L O P M E N T SF O C U S O N P A Y - F O R - P E R F O R M A N C E A N D B U I L D I N GS H A R E H O L D E R T R U S T

Recent development HighlightsInvestment Associationupdated Principles ofRemuneration(October 2016)

● Updated to reflect the Executive Remuneration Working Group’s recommendations, in particular:− Acknowledges need for increased flexibility of remuneration structures to reflect strategy and business needs− Encourages two-way shareholder engagement− Encourages companies to provide clear rationale for maximum incentive opportunities and actual outcomes (in light of

company performance)− Expects companies to consider and disclose specific internal and external reference points for judging the

appropriateness of quantum, e.g. pay ratios between the CEO and the executive team and median employee● Highlights as key areas for consideration:

− Post-employment shareholdings− Executive pension contributions should be consistent with the broader workforce− Appropriate bonus disclosure and use of Committee discretion

LGIM’s revised Pay Principles(September 2016)

● Encourages sizable executive shareholdings (≥2x salary); new recruits should be encouraged to buy shares● Supports post-retirement shareholding guidelines (e.g. half the holding for at least 2 years)● Companies should explain why the single figure for the CEO is considered appropriate each year relative to company

performance, employee pay, and shareholder experience● Expects companies to disclose the pay ratio between the CEO’s total single figure and median employee pay● Pensions should be aligned over time with general workforce● Discourages buy-out other than in exceptional circumstances (if awarded, should be predominantly in shares)

UK Prime Minister’sstatements… (July 2016)

● Theresa May has pledged to ensure:− Executive remuneration is subject to [annual] binding shareholder votes;− Employee and consumer representation on company Boards; and− Companies publish the executive-to-worker pay gap

● The Department for BEIS subsequently launched a consultation on corporate governance

… and resulting BEISconsultation (November 2016)

GC100’s updated reportingguidance (August 2016)

● Minor updates to existing guidance, including around target disclosure, application of Committee discretion, and cappingsalary in Policy

© MERCER 2017 6

I S S H A S R E C E N T L Y P U B L I S H E D T H E I R P R O P O S E DU P D A T E S T O I T S P R O X Y V O T I N G G U I D E L I N E S F O RR E M U N E R A T I O N F O R F T S E - L I S T E D C O M P A N I E S I N 2 0 1 7

● ISS has published updates to its 2017 guidelines to reflect developments in market practice and shareholderexpectations on remuneration . The updates include the following:

− ISS acknowledges the ERWG’s recommendation to consider pay models which are not fully aligned with thetypical UK structure. ISS expects companies to justify their overall Remuneration Policy in terms of the company’sspecific circumstances and strategic objectives, and states that any increase in certainty of reward should beaccompanied by a material reduction in incentive opportunities

− ISS will potentially recommend voting against the Remuneration Committee Chair in the event of a serious breachof good practice and where issues have been raised over several years

− ISS’ voting recommendation on implementation will consider the results of their pay-for-performance methodologyas well as its qualitative review of the company’s remuneration practices

− Clarification that in termination scenarios, appropriate pro-rating of outstanding share awards should be applied

● ISS has also amended policy wording on overboarding to provide clarity on the precise number of Board seats whichmay be held by Executive Directors and NEDs. A negative vote recommendation will be applied to the individual’sadditional seats, and not be at the company where the individual is the CEO or Chairman

© MERCER 2017 7

I S S I N T R O D U C E D A N E W P A Y - F O R - P E R F O R M A N C EA N A L Y S I S T H I S Y E A R F O R A L L S T O X X 6 0 0 C O M P A N I E S

In 2016, ISS introduced quantitative pay for performance analysis for the largest European companies. Analysis coversthree measures of pay and performance alignment, two relative to peers and one absolute:

1. Relative Alignment

– Percentile rank of CEO pay (3-year average) vs. percentile rank of 3-year TSR performance, against a peer groupselected based on size (revenue, assets, market cap), sector, and country of similar pay level

– Relative Alignment score is generated by subtracting the pay percentile rank from performance percentile rank,with a positive score indicating favourable to shareholders, and a negative score indicating favourable toexecutives

2. Multiple of Median

– Calculated by dividing CEO pay by the median pay for the peer group

– This is essentially the ‘compa ratio’ which is a number frequently found in benchmarking reports. This will be highlysensitive to the choice of peer group

3. Absolute Alignment

– Measures ‘directional alignment’ by calculating the difference between ‘the slopes of weighted linear regressionsfor pay and for shareholder returns’

– Difference indicates the degree to which CEO pay has changed more or less rapidly than TSR over the period

– This analysis is very similar to the performance graph and table required by UK reporting regulations. Thecalculated ‘alignment’ will be very sensitive to the performance periods rewarded in incentives (and to changes inCEO)

© MERCER 2017 8

I S S A N N O U N C E D C H A N G E S T O T H E M E T H O D O L O G YU N D E R L Y I N G I T S P A Y - F O R - P E R F O R M A N C E M O D E L F O RE U R O P E A N C O M P A N I E S M I D - N O V E M B E R

General updates (for European companies) Peer selection

● In 2016, ISS introduced quantitative pay-for-performance analysis for thelargest European companies. Analysis covers three tests of pay andperformance alignment, two relative to peers (Relative Alignment andMultiple of Median) and one absolute (Absolute Alignment)

● Effective from 1 February 2017, the analysis is extended to cover anycompany that is a constituent of either the STOXX Europe 600 Index or themain index for each covered country

● ISS has confirmed to Mercer their analysis will now include the largest 455UK-listed companies excluding investment trusts (cf. top 200 currently)

● With more than 1,100 companies now included, the quantitative tests will beapplied on a more consistent basis, aligning the European coverage of pay-for-performance assessments with that for US and Canadian companies

● We expect more performance measures, in addition to TSR, to beintroduced to the tests in 2017-18

● Following shareholder and corporate feedback, companies andshareholders are now able to suggest peer groups to ISS

● For companies that already disclose their benchmarking peers in the DRR,ISS will use this list as the default peer group unless the company contactsISS to suggest otherwise. Company- and shareholder-suggested peers,alongside formulaically selected ISS peers, will inform the final peer groupconstruction process

● ISS’ methodology will continue to focus on identifying peer companies thatare similar in terms of industry and company size. Note that ISS definescompany ‘size’ in terms of revenue, with the exception of companies in theOil & Gas sector (for which size is based on market cap) and banks(assets). Only companies domiciled in Europe may be included in the peerconstruction process

● ISS aim for 12-18 peers but the maximum number is 30. Peers will be set inmid-January and this group will be fixed until the next review date

● Only companies that subscribe to ISS Corporate Services are able to seetheir peer group ahead of the AGM (and challenge their peer group)

● The new approach to peer selection will be effective from 1 February 2017.Companies with AGMs between 1 February 2017 and 31 January 2018 willbe able to suggest a peer group for the 2017 AGM season. The submissionwindow is 28 November to 9 December 2016

© MERCER 2017 9

H E R M E S I N V E S T M E N T M A N A G E M E N T R E C E N T L YS H A R E D T H E I R U P D A T E D R E M U N E R A T I O NG U I D E L I N E S

● Hermes believes their new guidelines will improve the current pay system which they consider (i) provides for excessivequantum, (ii) is misaligned with long-term value, (iii) is too complex, (iv) exhibits weak accountability, and (v) has created lowlevels of trust between Remuneration Committees and investors

● Hermes’ starting point is a general principle that fixed pay be increased and variable pay be based on a simplified unifiedincentive (i.e. annual bonus and LTIP combined), for which:

1. Granting of awards is based on a performance scorecard looking back over at least 12 months;

2. Scorecard to be dominated by strategic goals and NOT to include TSR;

3. Awards to be delivered in shares with only a modest (25%) cash element;

4. Share awards to be held for at least 5 years or until a minimum shareholding has been achieved; and

5. Share awards also to be subject to an underpin based on absolute and relative TSR over the vesting period

● Other principles include:

1. A cap on the total pay opportunity to be published by the Company;

2. Executive Director shareholding requirements of 500% of salary for FTSE100, 300% for FTSE250 and 200% for others,with a post-departure extension over 3 years;

3. The RemCo Chair to write annually to employees to explain the rationale for the CEO’s pay, and to meet with employeesto obtain their views on senior executive pay; and

4. The CEO/median employee pay ratio to be published

● Some of these guidelines are controversial; we recommend monitoring the market response to these over the coming months.For example, we note that the performance-granting aspect of these proposals does not have the support of LGIM

© MERCER 2017 10

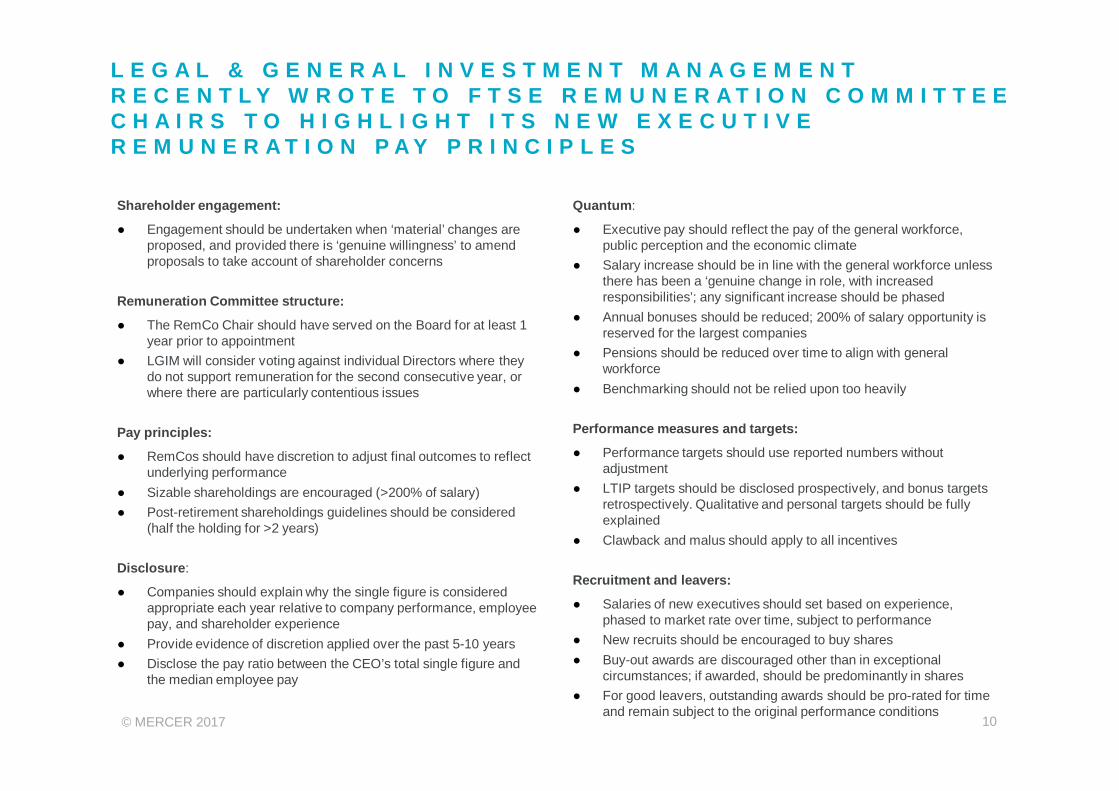

L E G A L & G E N E R A L I N V E S T M E N T M A N A G E M E N TR E C E N T L Y W R O T E T O F T S E R E M U N E R A T I O N C O M M I T T E EC H A I R S T O H I G H L I G H T I T S N E W E X E C U T I V ER E M U N E R A T I O N P A Y P R I N C I P L E S

Shareholder engagement:

● Engagement should be undertaken when ‘material’ changes areproposed, and provided there is ‘genuine willingness’ to amendproposals to take account of shareholder concerns

Remuneration Committee structure:

● The RemCo Chair should have served on the Board for at least 1year prior to appointment

● LGIM will consider voting against individual Directors where theydo not support remuneration for the second consecutive year, orwhere there are particularly contentious issues

Pay principles:

● RemCos should have discretion to adjust final outcomes to reflectunderlying performance

● Sizable shareholdings are encouraged (>200% of salary)● Post-retirement shareholdings guidelines should be considered

(half the holding for >2 years)

Disclosure:

● Companies should explain why the single figure is consideredappropriate each year relative to company performance, employeepay, and shareholder experience

● Provide evidence of discretion applied over the past 5-10 years● Disclose the pay ratio between the CEO’s total single figure and

the median employee pay

Quantum:

● Executive pay should reflect the pay of the general workforce,public perception and the economic climate

● Salary increase should be in line with the general workforce unlessthere has been a ‘genuine change in role, with increasedresponsibilities’; any significant increase should be phased

● Annual bonuses should be reduced; 200% of salary opportunity isreserved for the largest companies

● Pensions should be reduced over time to align with generalworkforce

● Benchmarking should not be relied upon too heavily

Performance measures and targets:

● Performance targets should use reported numbers withoutadjustment

● LTIP targets should be disclosed prospectively, and bonus targetsretrospectively. Qualitative and personal targets should be fullyexplained

● Clawback and malus should apply to all incentives

Recruitment and leavers:

● Salaries of new executives should set based on experience,phased to market rate over time, subject to performance

● New recruits should be encouraged to buy shares● Buy-out awards are discouraged other than in exceptional

circumstances; if awarded, should be predominantly in shares● For good leavers, outstanding awards should be pro-rated for time

and remain subject to the original performance conditions

© MERCER 2017 11

T H E I A ’ S P R I N C I P L E S O F R E M U N E R A T I O N H A V E B E E NS L I M M E D D O W N , W I T H A C L E A R E R F O C U S O N H I G H -L E V E L I S S U E S R E L A T I N G T O R E M U N E R A T I O NP O L I C I E S , Q U A N T U M A N D S T R U C T U R E

Key changes to IA Principles:

● Encourages use of remuneration structures appropriate to company strategy and business needs, in line with the ERWG’srecommendations. No particular approach is prescribed, but the selected structure should be justified and not be undulycomplex

● Overall remuneration levels (both maximum potential and actual pay outcomes) should be justified in the context of companyperformance and shareholder experience. Increases to salary and variable pay opportunities should be accompanied by a clearrationale, including consideration of the impact on all stakeholders

● Pay ratios should be included, comparing CEO total pay vs. executive team and median of the broader employee population.The IA is also interested to see change in ratio over time and explanation of why the ratio is appropriate for the company

● Committees are encouraged to consider requiring executives to retain a proportion of their shareholding for a period afterleaving. However, the Principles remain silent on details such as time period and proportion to be retained

Other ‘hot topics’ flagged by IA members:

● Bonus target disclosure: financial targets should be disclosed retrospectively in full. A ‘Red Top’ will be issued to any companywhich does not fully disclose bonus targets or commit to fully disclose targets in a future year (no later than 2 years afterpayment). Personal and strategic targets should be accompanied by an explanation of why payouts are merited

● Policy renewal: members expect disclosure of Policy maxima for all elements of variable remuneration. Flexibility to usediscretion is encouraged to ensure that remuneration outcomes fairly reflect company performance and shareholder experience.Companies should be clear where such discretion has been exercised and provide rationale

● Pension: executive pension arrangements should be in line with those provided for the wider workforce; any differences inpension contribution rates for executives and the general workforce should be disclosed and justified

● Shareholder consultation: reflecting another ERWG recommendation, companies and investors are encouraged to work togetherand treat the consultation process as a two-way dialogue to obtain investor feedback and, where appropriate, to enhanceproposals, rather than use it merely as a validation exercise. Committees are encouraged to understand shareholders’ viewsand keep abreast of their largest shareholders’ voting policies

© MERCER 2017 12

F O L L O W I N G H E R A P P O I N T M E N T A S P R I M E M I N I S T E R ,T H E R E S A M A Y H A S M A D E A N U M B E R O F S T A T E M E N T SO F I N T E N T R E G A R D I N G E X E C U T I V E R E M U N E R A T I O N ,A K E Y O N E B E I N G T H E C E O - T O - E M P L O Y E E P A Y R A T I O

● In July, Theresa May pledged to ensure:

− Executive remuneration is subject to [annual] binding shareholder votes;

− Employee and consumer representation on company Boards; and

− Companies publish the executive-to-worker pay gap

● These requirements would be more stringent than regulations in many European countries. It is unlikely thatthese will be enforced for 2017, and speaking to the CBI's annual conference in November, the Prime Ministersaid firms would not be required to adopt employee or consumer representation on the Board. No guidancehas been published by the Government on how the pay ratio could be calculated

● Mirroring comments by May, Chris Philp (Tory MP) has called for reforms to corporate structures to increasetransparency in executive pay in his paper ‘Restoring Responsible Ownership’

● Philp additionally calls for establishing a ‘shareholder committee’ comprising the five largest shareholders, andfor the committee to recommend the appointment and removal of Board Directors, and ratify proposed paypackages

● The Presidents Group of the Confederation of British Industry met in early September to discuss May’sproposals. The CBI has acknowledged the need to review this area, and consultation with key stakeholders iscurrently underway

© MERCER 2017 13

A N U M B E R O F S H A R E H O L D E R S H A V E E X P R E S S E DS U P P O R T F O R T H E D I S C L O S U R E O F T H EC E O - T O - E M P L O Y E E P A Y R A T I O

● A number of shareholders and shareholding bodies (the Investment Association, LGIM, Hermes) have also voiced their supportfor the disclosure of a CEO-to-employee pay ratio

● The definition of the CEO-to-employee pay ratio is not yet well socialised by the UK Government, shareholders or companies. Akey question is whether to compare CEO pay vs. the median or mean remuneration across all employees. The InvestmentAssociation, LGIM and Hermes refer to the median, whereas the High Pay Centre uses the mean

● There has been no clear indication of when the UK Government or shareholders will expect companies to start publishing theratio. Whilst it is unlikely that public disclosure will be legally enforced for 2017, there will likely be increasing shareholder focuson this topic over the next year

● Remuneration Committees that Mercer advises are getting ready by reviewing what the ratio (based on average employee pay)looks like for them and sector peers. It is still early days for a firm decision on whether to early adopt, though some Committeesare keen to be seen as ‘in tune’ with the public mood. We suggest monitoring emerging market practice in this area

1. Based on CEO single figure and average employee pay (defined as aggregate employee costs (excluding social security) divided by thenumber of employees). Analysis includes only full-year CEOs

2. Excludes quartiles where there are insufficient data points for analysis

© MERCER 2017 14

T H E D E P A R T M E N T F O R B U S I N E S S , E N E R G Y &I N D U S T R I A L S T R A T E G Y L A U N C H E D A C O N S U L T A T I O NO N C O R P O R A T E G O V E R N A N C E R E F O R M

● BEIS’ green paper seeks to stimulate a debate on a range of options for strengthening the UK’s corporate governanceframework. BEIS does not make any firm proposals at this stage, but has invited responses to 14 questions covering executivepay, strengthening the employee, customer and wider stakeholder voice, corporate governance in large,privately-held businesses, and the broader corporate governance framework

● With regards to executive pay, BEIS poses the following questions:

1. Do shareholders need stronger powers to improve their ability to hold companies to account on executive pay andperformance?

2. Does more need to be done to encourage shareholders to make full use of their existing and any new voting powers onpay?

3. Do steps need to be taken to improve the effectiveness of Remuneration Committees, and their advisers, in particular toencourage them to engage more effectively with shareholder and employee views before developing pay policies?

4. Should a new pay ratio reporting requirement be introduced? How can misleading interpretations and inappropriatecomparisons (for example, between companies in different sectors) be avoided?

5. Should the existing requirements to disclose annual bonus targets be strengthened? How could this be done withoutcompromising commercial confidentiality?

6. How could long-term incentive plans be better aligned with the long-term interests of companies and shareholders? Shouldholding periods be increased from a minimum of three to a minimum of five years?

● The deadline for responses on the consultation is 17 February 2017. Mercer will be preparing a detailed response

© MERCER 2017 15

G C 1 0 0 & I N V E S T O R G R O U P U P D A T E D T H E I RG U I D A N C E O N R E M U N E R A T I O N R E P O R T I N G I NA U G U S T 2 0 1 6

● The GC100 and Investor Group first published its guidance on remuneration reporting in 2013, to assist companiesand their shareholders in interpreting the new disclosure regulations that came into force that year

● In December 2014, the Group reviewed its 2013 guidance in light of experience over the 2014 AGM season andrecent developments, and issued a statement to clarify and emphasise certain aspects of the original guidance

● The Group updated its guidance again in August 2016. The majority of guidance remained relevant, though anumber of changes and additions were made. We summarise the changes below:

− Remuneration Committees are encouraged to consider whether non-disclosure of performance targets due to‘commercial sensitivity’ is truly justified. For long-term incentives where companies do not wish to disclosetargets prospectively, consider interim qualitative commentary relating to intra-cycle performance

− Remuneration Committees are expected to apply downwards discretion where qualitative performanceoutcomes do not reflect overall company financial performance

− Companies are reminded of the requirement to disclose maximum salary in the Remuneration Policy; thisdoes not have to be a £-amount, e.g. could instead be expressed as percentage increase p.a.

− The comparison group for the percentage change in CEO disclosure should be meaningful andrepresentative, i.e. not a narrow group of senior managers

© MERCER 2017 16

T H E E X E C U T I V E R E M U N E R A T I O N W O R K I N G G R O U P H A SR E C E N T L Y C O N C L U D E D T H E I R P R O J E C T O N‘ S I M P L I F I C A T I O N ’ ; O U T C O M E S A R E L I K E L Y T O H A V EI M P L I C A T I O N S F O R F U T U R E R E M U N E R A T I O N D E S I G N

● The ERWG believes that the current approach to executive pay is not fit for purpose, and has resulted in pooralignment of interests between executives, shareholders and the company

● The aim of the ‘simplification project’ is to explore alternative approaches through widespread consultation with keystakeholders, including shareholders, companies and other industry bodies

● The ERWG published initial proposals in April 2016, emphasising that a range of approaches (e.g. bonus deferral,restricted shares) should be considered by Remuneration Committees, alongside the traditional LTIP design

● The ERWG published its final report in July 2016, setting out ten recommendations, including:

− Remuneration Committees should have greater flexibility to choose a remuneration structure that is tailored toeach Company’s strategy, culture and business needs

− Committees are encouraged to assume greater accountability for its remuneration decisions, and Committeesand shareholders are asked to work together to improve the engagement process

● The majority of FTSE companies sought shareholder approval for their first Remuneration Policy in 2014, and willbe seeking approval for a new Policy in 2017

● It remains to be seen the extent to which companies will be influenced by the ERWG’s conclusions in theirremuneration design. Further testing with shareholders, and in particular ISS, is also required before the alternativemodels such as restricted shares become an accepted LTIP vehicle

© MERCER 2017 17© MERCER 2017 17

R E V I E W O F M AR K E TP R AC T I C E I N E X E C U T I V ER E M U N E R AT I O N

© MERCER 2017 18

S U M M A R Y

● Overall, executive remuneration practice at the FTSE50-150 has not changed significantly over the past year

● Quantum is increasingly constrained by the external environment; a number of shareholders have now expressed preferred caps (aspercentage of salary) on incentive opportunities

Salary:● Salary inflation during 2016 remains low.

● Median Executive Director salary increase at the FTSE50-150 was 2.4% (including freezes)

● For 2017, moderate salary inflation is likely to prevail due tocontinued shareholder pressure to limit executive salaryincreases to general inflation or the average employeeincrease

Pension:● There is a continued move away from Defined Benefit

pensions towards

● Defined Contribution and cash supplements. The typicalprovision is 20-25% of uncapped salary

Annual bonus:● The most common bonus measures remain profit and

personal/strategic measures

● Companies are continuing to use a basket of measuresrather than relying on any single measure

● Bonus deferral is common. The deferral requirement istypically 25-50% of salary for 3 years

Long-term incentives:● Most companies continue to use performance shares as the

single LTI vehicle. Options and matching plans are rare

● The most common LTI measures remain relative TSR andEPS. Returns (e.g. ROCE) is also common, particularly forcapital-intensive businesses

● The most common performance period remains 3 years, butthere continues to be a trend towards a longervesting/holding period due to shareholder pressure

● We expect the proportion of companies with an overall LTItime horizon of >3 years to increase in 2017, as companiesseek shareholder approval for a new Remuneration Policy

© MERCER 2017 19

A N N U A L B O N U S O P P O R T U N I T I E S R E L A T I V E T O M A R K E T

Opportunities(maximum as % of salary)

CEO CFO

Upper quartile 200% 175%

Median 150% 150%

Lower quartile 130% 125%

0% 20% 40% 60% 80% 100%

EPS/profit

Personal/strategic

Revenue

Cash flow

Returns

HSE/CSR

Customer

Other²

Measures(% of FTSE50-150 companies)

FTSE50-150 annual bonus trends

● Annual bonus opportunities have remained relatively stable in recent years

● Across the FTSE50-150, the typical aggregate weighting on non-financial measures in the bonus remainsaround 20-30%.

● The majority of companies reward the achievement of personal objectives in this element of the bonus

● The number of bonus measures is increasing; around 70% now use 3 or more bonus measures

1. Based on 2016 BSA of 185%/175% of salary to CEO/CFO2. Other includes: TSR, debt, dividends, EVA, property returns, new business, operating efficiency, risk, staff satisfaction

and working capital

© MERCER 2017 20

B O N U S D E F E R R A L I S P R E V A L E N T A C R O S S T H EF T S E 5 0 - 1 5 0 . C O M P A N I E S M O S T C O M M O N L Y R E Q U I R E2 5 - 5 0 % O F T H E B O N U S E A R N E D T O B E D E F E R R E D F O R3 Y E A R S

Prevalence of deferred bonus plans(% of FTSE50-150 companies)

Deferral period(% of FTSE50-150 companies1)

0%20%40%60%80%

100%

0%

20%

40%

60%

80%

100%

1 year 2 years 3 years 4 years 5+years

● Annual bonus deferral (into shares) is used to (i) lengthen the incentive time horizon, (ii) improve shareholderalignment, (iii) support retention, and (iv) facilitate malus. Around 80% of FTSE50-150 companies operate someform of bonus deferral

● The typical deferral requirement is 25-50% of the earned bonus, most commonly deferred for 3 years

● It is much more common to operate deferral as part of the annual bonus rather than a stand-alone share plan(particularly as the cash bonus and BSA performance measures are largely the same)

Note: the BSA vests in equal tranches 1, 2 and 3 years aftergrant

1. Based on companies that operate deferral on their annual bonus

© MERCER 2017 21

P E R F O R M A N C E S H A R E P L A N S R E M A I N T H E M O S TC O M M O N F O R M O F L O N G - T E R M I N C E N T I V E A TF T S E C O M P A N I E S

CEO CFO

Upper quartile 250% 250%

Median 200% 200%Lower quartile 190% 150%

FTSE50-150 aggregate1

long-term opportunities2

(face value, as % of salary)

Prevalence of long-term incentive vehicles(% of FTSE50-150 companies that operate LTIs)

Note: 2 FTSE50-150 companies do not operate long-term incentives:Aberdeen Asset Management and Fresnillo

Options

Co-investment/bonusshare matching plans

Performanceshares

(including ValueSharing Plans)

–

1%88%

1%

2%

8%

–

1. Assumes an option is valued at 33% of a performance share; forbonus matching and co-investment, assumes achievement of targetbonus and full take-up of voluntary investment

2. The chart captures the policy award levels, which are the same asthe normal maximum for most companies

3. Based on 2016 awards; the normal maximum is 200% of salary

© MERCER 2017 22

W H I L E R E L A T I V E T S R A N D E P S R E M A I N T H EM O S T P R E V A L E N T L O N G - T E R M I N C E N T I V EM E A S U R E S , ‘ S T R A T E G Y - R E I N F O R C I N G ’M E A S U R E S S U C H A S R O C E A R E A L S O C O M M O N

Prevalence of long-term incentive measures(% of FTSE50-150 companies1)

0% 20% 40% 60% 80% 100%

Revenue

Cash flow

Other (non-financial)³

Other (financial)²

Returns

EPS/profit

TSR● Over 90% of FTSE50-150 long-term

incentives now use 2 or more performancemeasures, and there is a trend towards theuse of more measures e.g. a scorecardapproach

● Most companies provide for RemunerationCommittee discretion in the RemunerationPolicy to adjust vesting of long-termincentives (typically downwards only) in lightof the underlying financial performance

1. Based on companies which operate a long-term incentive2. Other non-financial includes: customer service, strategic measures, and staff satisfaction3. Other financial includes: asset under management, debt reduction, dividends and property returns

© MERCER 2017 23

0%

20%

40%

60%

80%

100%

1 year 2 years 3 years 4 years 5+ years0%

20%

40%

60%

80%

100%

1 year 2 years 3 years 4 years 5+ years

LTI performance periods(% of FTSE50-150 LTIs)

LTI vesting/holding periods(% of FTSE50-150 LTIs)

Note: 1- and 2-year periods generally relate to plans whereperformance is measured over multiple periods (e.g. 1, 2 and 3years)

Some of the year-on-year movement is due to changes inconstituent companies within the FTSE50-150

W E E X P E C T T H E P R O P O R T I O N O F C O M P A N I E S W I T HA N O V E R A L L L T I T I M E H O R I Z O N O F > 3 Y E A R S T OI N C R E A S E I N 2 0 1 7

20152016

● The Investment Association now expects long-term incentive horizons to be at least 5 years. Many shareholders (e.g.Fidelity UK, Standard Life, Aviva and L&G) are also looking for time horizons of greater than 3 years with Fidelitybeing the most dogmatic

● Note, a 5-year horizon could comprise a 3-year performance period plus a 2-year holding requirement, and would notnecessarily require the shares to be subject to risk of forfeiture during the holding period. The majority of companiesdo not apply forfeiture over the holding period

● Over half of the FTSE50-150 apply a total LTI time horizon of more than 3 years and we expect this proportion toincrease in 2017 as many companies seek shareholder approval for a new Remuneration Policy

© MERCER 2017 24

M O S T F T S E 5 0 - 1 5 0 C O M P A N I E S H A V E A D O P T E DM A L U S A N D / O R C L A W B A C K P R O V I S I O N S , A N DT H E V A S T M A J O R I T Y O P E R A T E S H A R E H O L D I N GG U I D E L I N E S

Shareholding guidelines at the FTSE50-150(% of salary)

CEO CFOUpper quartile 265% 200%

Median 200% 200%Lower quartile 200% 150%

Malus/clawback:

● The FRC UK Corporate Governance Code requires – on a ‘complyor explain’ basis – the inclusion of malus and clawback provisionson Executive Director incentives granted in financial yearsbeginning on or after 1 October 2014

● Over 90% of the FTSE50-150 operate malus or clawbackprovisions on at least one incentive.

Shareholding guidelines:

● Around 97% of FTSE50-150 companies operate shareholdingguidelines. These are typically expressed as a multiple of salary,commonly at a level broadly equivalent to the LTI grant size

● The PLSA and ISS are applying pressure on companies to increaseguidelines to a minimum of 200% of salary. Hermes recommendsshareholding guidelines of 500% salary for the FTSE100 and 300%for the FTSE250

● Many companies require the guideline to be reached within a settime period (e.g. 5 years). Other companies simply require theretention (typically 50%) of vested long-term incentives until theguideline is met

● Post-employment holding requirements are starting to gain tractionamongst shareholders, with the IA, LGIM and Hermes allencouraging this practice in the latest update to their remunerationprinciples

Trend

© MERCER 2016 25