retail: driver of innovation

TRANSCRIPT

Research Conferences Publishing Trade Shows

Retail: Driver of Innovation

Prof.Dr.Bernd Hallier

Bildbeispiel

Page 2

..

Page 3

Cornelisz Vroom was documentating the

return of the second VOC East India

Expedition.

The power of retail

Page 4

Rembrandt van Rijn

Page 5

Merchants (wholesalers/retailers) ruled

the world over five thousand years from

the Silk Road uptil Ahold!

Page 6

B. Hallier: Retail/Wholesale Innovation Cycles

1 Colonial Im- and Export; harbour dominance 1800

2 Prussian Custom Union - the focus changes to internal markets and the bigger

area stimulated efficiency like today’s EU

1825

3 Consumer Cooperatives to counter low income 1850

4 Department stores to cope with rich income 1875

5 Retailers Cooperatives to counter department stores 1900

6 Mail Order Houses to cope with the bad economic situation after World War I 1925

7 Supermarkets/Self-service from America after World War II 1950

8 Big Boxes and Shopping Centers as retail formats – EAN and scanning at the

backstage

1975

9 B2B and B2C by Internet – Total Supply Chain, DRR and ECR in-between retail and

consumer fast moving industry at the backstage

2000

10 M-Info, M-Shopping, C2C by Facebook, LinkedIn, YouTube and twitter – integration

of the agricultural suppliers into the Total Supply Chain

2025

Page 7

The Empowerment of Retail by

marketing-tools

branded goods +

great sales forces

below the

line (Vkf)

DPR/shelf

optimizing

scanning

build up

of marketing

national

distribution

split of

rabates

regional

distribution

local

distribution

merchandising

for the retail

efficient consumer

response ECR

computer integra-

ted trading CIT

category

management

category

captains partial

european

production for

private labels

partial

international

partial

global

coorgani-

sation

branded goods industry b retail branded goods industry

Source: Prof. Dr. B. Hallier/ EHI

Consumer impact

via YouTube,

Twitter,

FaceBook etc.

Page 8

Metro-Gruppe

59.960 16,6%

Rewe-Gruppe

54.772 15,2%

Edeka/AVA

47.665 13,2%

Aldi-Gruppe

37.500 10,4%

Tengelmann

26.889 746%

Metro-Gruppe

31.692 11,8%

Rewe AG

28.811 10,8%

Aldi Gruppe

23.100 8,7%

Tengelmann

17.555 6,6%

Asko-Gruppe

17.474 6,6%

Aldi Gruppe 23.100 8,7%

Metro Gruppe 9.835 6,67%

Rewe-Leibbrand 6.480 4,4% Tengelmann 6.385 4,3%

Schaper 4.180 2,8%

?

92.000

20,9%

?

86.000 19,5%

?

78.000 17,7%

?

60.000 13,6%

?

43.000 9,8%

1980

26,3%

1990

44,7%

2000

62,7%

2010 81,6%

Concentration in German Food Retailing Development 1980-2000/ Scenario 2010 Market Shares Top 5

Source:

M+M Eurodata

Page 9

1950

Local

Retailer

The “Expansion-Stairway” of European Retailing

1960 1970

Regional

Retailer

National

Retailer

Distribution

Power

Expansion Western-/Southern Europe

Expansion Eastern Europe

Global Expansion

1980 1990 2000

Page 10

The annual sales of WalMart is

equivalent to the GNP of the Switzerland

- but WalMart is growing faster!

Size of Retailers

Page 11

Important for the retailers are standards

for the international information and

logistics.

Page 12

What is the organizational backstage for

the global retail empires?

Page 13

Case Study 1

EAN/GS1

Page 14

All started with the European Article

Numbering System EAN – initiated by

Albert Heijn (Ahold)

EAN/GS1

Page 15

40 12345 12345 6

Prafix

bbn

bar code

OCR-B-

skript

Check digit

Individual

item number

from the

producer

Normal version of the 13-digit EAN

European Article Numbers(EAN)/

Barcode

Page 16

Scanner- Introduction in Germany

1 7 9 19 43 76 175729 719 966

15442252

3434

4849

7260

9773

12187

14901

17010

18000

1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996

Page 17

Consumer sale could be tracked

EAN/GS1

Page 18

Customer Cards / Data

**THANK YOU – COME AGAIN**

WE APPRECIATE YOUR LOYAY PATRONAGE

THANK YOU FOR SHOPPING

A&F MONTVALE, NEW JERSEY

Bacon PC 1,89 F

EGGS PC 1,29 F

TAX ,00 BAL 3,18 F

CASH 3,18 F

11/11/03 11:11 0015 02 0005 100

INQUIRE TODAY HOW OUR BOUNUS SAVING

CLUB CAN SAVE YOUUR MONEY

YOU COULD HAVE SAVED 1.00 TODAY

MY PLEASURE TO SERVE YOU DON

Page 19

FREQUENT SHOPPER PROFILE

Store Number: 000123

Card Number: 654321

JANE Q. SHOPALOT

67 ATLANTIC AVENUE

MANASQUAN NJ 08736

SSN: 999-99-9999

ISSUE DATE 09/10/90

ISSUE STATUS INITIAL

People in houshold = 4

People under age 18 = 2

Owner of any pets = dog

Marital Status = married

Age of person = 34

DATE FIRST SHOPPED : 09/11/90

DATE LAST SHOPPED : 04/11/91

Month: APR MAR FEB

Purchases

GROCERY 42.76 146.23 213.82

DAIRY 7.25 31.97 39.99

MEAT 17.35 81.60 88.79

PRODUCE 20.20 50.62 76.24

DELI 13.45 26.47 43.86

SEAFOOD 30.75 .00 .00

FROZEN 12.60 26.88 33.04

LIQUOR .00 .00 .00

FLORAL 12.50 .00 36.94

Total $ 156.86 363.77 532.68

TOTAL TRIPS 2 5 6

Transparent Customer

Page 20

Customer Segmentation

High purchasing value

High frequency

of purchase

Low frequency

of purchase

(1)

(2) (3)

(4)

„come more often“-Mailing „Thank you“-Mailing

„lost son“-Mailing „scottish“-Mailing

Low purchasing value

Page 21

The next step had been RFID (Radio

Frequency Identification) and WLAN

(Wireless Local Area Network)

New Technologies

Page 22

Parameters with an influence on RFID

Antenna range

Radio frequency field

shape (reflections, failures)

Number of smart

chips

Mix of products on the

pallet (cans, liquids …)

Positioning of smart chips

(alignment, handling,

hidden/covered)

Time available for reading,

speed of movement

Unintended reading

of the smart chip

close to the portal

Number of

bytes to be

read

Page 23

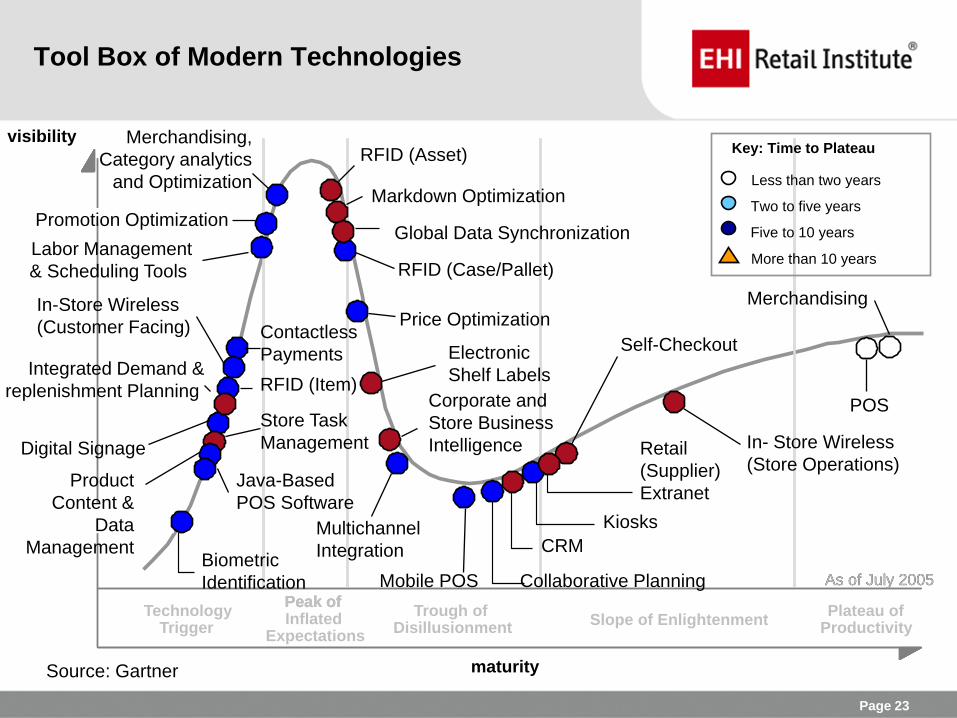

Tool Box of Modern Technologies

Technology Trigger

Peak of Inflated

Expectations

Trough of Disillusionment

Slope of Enlightenment Plateau of

Productivity

As of July 2005

Peak of Peak of

maturity

As of July 2005

visibility

POS

Self-Checkout

Retail

(Supplier)

Extranet

Kiosks

CRM

Mobile POS

Multichannel

Integration

Price Optimization

RFID (Case/Pallet)

RFID (Asset) Merchandising,

Category analytics

and Optimization

Labor Management

& Scheduling Tools

Contactless

Payments

RFID (Item)

Digital Signage

Store Task

Management

Java-Based

POS Software

Promotion Optimization

Integrated Demand &

replenishment Planning

Product

Content &

Data

Management Biometric

Identification

In-Store Wireless

(Customer Facing)

Electronic

Shelf Labels

Corporate and

Store Business

Intelligence

Markdown Optimization

Global Data Synchronization

Merchandising

In- Store Wireless

(Store Operations)

Collaborative Planning

Less than two years

Two to five years

Five to 10 years

More than 10 years

Key: Time to Plateau

Source: Gartner

Page 24

Link to central

merchandise

management system

Employee

PDAs Wireless

Bluetooth

peripherals Information

Terminal Self Check-out

Smart Trolley

Smart Scales

Access Points

Customer PDAs

Wireless

workplaces

Advertising

Displays

RFID

Multimedia

shelfs

METRO Group Future Store: Everything under a single roof!

Page 25

Personal Shopping Assistant

Page 26

The European EAN merged with other

organizations to become GS1 (Global Standard 1)

EAN/GS1

Page 27

Case Study 2

Page 28

In 1994 we had the BSE Scandal (British

Cow Disease)

EHI/Orgainvent

Page 29

Meat was an anonymous product – nobody

knew, if the beef came from the UK!

EHI/Orgainvent

Page 30

Meat sales dropped by 25 percent in

Germany

EHI/Orgainvent

Page 31

Bernd Hallier and six butchers in retail

discussed solutions in analogy to EAN!

EHI/Orgainvent

Page 32

They created the “EHI-Label” for tracing

and tracking of cows and beef

EHI/Orgainvent

Page 33

Name of Meat

Producer and number

of the factory of the

control-list of the

European Union

Logo of Meat Producer

Number within Orgainvent

Born/Breeding/Slaughtered

in the following country

Production-number

Category of Meat

Packed at:

Controlled by:

Sample for Tracement-Label

Name of Item

Page 34

Page 35

Page 36

Page 37

To transform a theoretical approach into

applied sciences – suppliers had to join

the system

Page 38

Cooperating suppliers had been

published as benchmarks

Page 39

Page 40

EHI supported the initiatives by

publications

Page 41

One tool was the monthly magazine

Dynamik im Handel

Page 42

Another tool had been “special editions”

about the topic

Page 43

Page 44

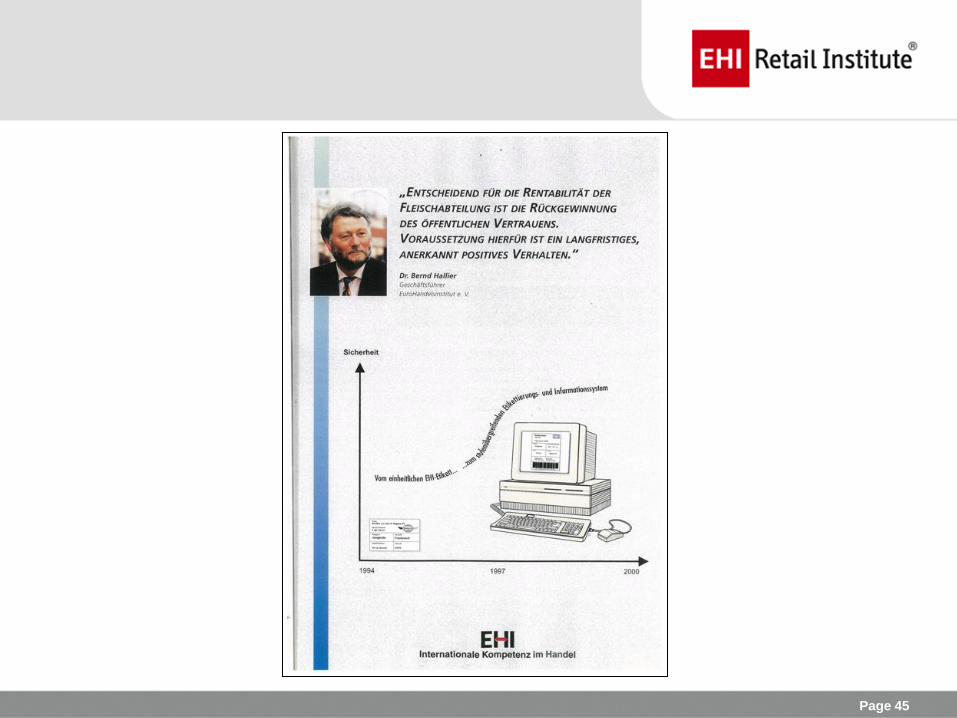

Also two advertisements had been

designed and had been placed 18 times

in EHI publications inbetween 1995 and

2001

Page 45

Page 46

Page 47

Last but not least each quarter the

progress of the EHI-Workshops had

been documented

Page 48

In the year 2000 the pyramid proved 22

steps of effort to regain the consumer

trust!

Page 49

Page 50

One of the brochures had been

distributed to all members of the German

Bundestag

Page 51

Page 52

The Federal Chancellor Gerhard

Schröder had been approached by a

letter of Prof.Dr.Hallier on April 7th 2000

to introduce the label compulsory.

Page 53

Page 54

On April 18th the Federal German

Minister of Agriculture informed his EU-

colleagues about the German decisions

Page 55

Page 56

Meanwhile – pushed by EHI – the Label

and the tracing-system became an EU

Regulation: 1825/2000 and VO (EG)

999/2001

EHI/Orgainvent

Page 57

While in the end of August the draft

version of the new book “From Crisis to

Competence” was finished the EU-

Commission wrote a draft to change from

ear-marks for cows to RFID in 2020!

EHI/Orgainvent

Page 58

If – within national boundaries – there will

not be enough knowledge

institutionalized – then those country’s

suppliers will fall out of the globalized

distribution/production!

EHI/Orgainvent

Page 59

Case Study 3

EHI/GlobalGAP

Page 60

Getting involved via Tracking/Tracing into

agriculture – EHI started EUREPGAP

(European Retailers Produce Good

Agricultural Practice) – now GlobalGAP

EHI/GlobalGAP

Page 61

Continuous Growth

More than 100.000 certified

producers in more than 100 countries

STATISTICS

© GLOBALG.A.P Secretariat |

Page 62

GLOBALG.A.P GOVERNANCE

PARTNERSHIP PRINCIPLE IN ALL DECISION MAKING PROCESSES

Stakeholder

Page 63

GLOBALG.A.P MEMBERS

RETAIL & FOOD SERVICE MEMBERS

Page 64

GLOBALG.A.P MEMBERS

PRODUCER AND SUPPLIER MEMBERS

© GLOBALG.A.P Secretariat | Page 64

Page 65

Se

cre

taria

t

WE OPEN UP OUR STAKEHOLDER ENGAGEMENT

NEW STAKEHOLDER COMMITTEE STRUCTURE

© GLOBALG.A.P Secretariat | Page 65

• Find a common interest and create

your own Stakeholder Committee

• Min 5 GLOBALG.A.P members (min

1 retailer / min 1supplier/ min 1

associate member)

• Follow consistent rules and

templates

• Get Board approval

Stakeholder

Committees

Technical Advisory

Committees

National Technical

Working Groups

Board

Page 66

globalg.a.p Simplified

Producer keeps records of his practice

Producer self-monitoring

Producer inspection

Granting of a reward

Inspection

Documentation

Checklist

Checklist

Certificate

Page 67

How can add-ons benefit from this structure?

© GLOBALG.A.P Secretariat | Page 67

Producer keeps records of his practice

Producer self-monitoring

Producer inspection

Granting of a reward

Inspection

Incl. Add-on

Documentation

Checklist

Checklist

Certificate

Documentation

Add-on Checklist

Add-on Checklist

e.g. Certificate

Page 68

Globalg.a.p database frontend

Page 69

STEP-WISE APPROACH TO GLOBALG.A.P CERTIFICATION

PFA

Foundation

Level

PFA

Intermediate

Level

GLOBALG.A.P

• GLOBALG.A.P Primary Farm

Assurance (PFA): the response for

emerging markets

• Implementation through the

GLOBALG.A.P System following

member demands

• Implementation currently in the USA,

India, Poland, China, Kenya, South

Africa

WAY TO GLOBALG.A.P

National

GAP

Systems

Page 70

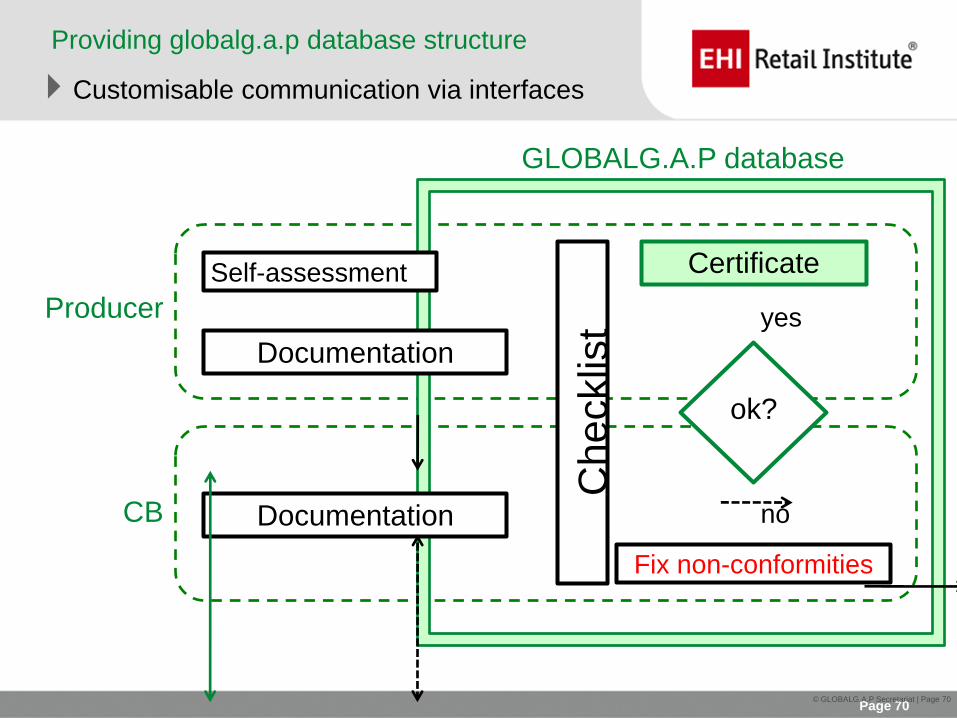

Providing globalg.a.p database structure

Customisable communication via interfaces

© GLOBALG.A.P Secretariat | Page 70

Producer

CB

GLOBALG.A.P database

Self-assessment

Documentation

Documentation

Ch

ecklis

t

ok?

Certificate

Fix non-conformities

yes

no

Page 71

THE FUTURE INTERNET

Actual developments

Farm Management Documentation

Documentation of all farm management actions

Linking from Farm Management Documentation to

certification

Spraying, soil cultivation, field management, ...

Includes potential information for different issues

(e.g. traceability, sustainability)

Checklists Documentation

Download, fill in and upload checklists to the

GLOBALG.A.P Database

Different checklists for IFA, Add-ons and PFA

Information is stored in the database and available

for registered users

Checklist results can be downloaded as pdf

© GLOBALG.A.P Secretariat | Page 71

Open XML Interfaces are available to various existing solutions

Page 72

THE GLOBALG.A.P CERTIFICATION SYSTEM

Independent 3rd Party Certification

• All certification bodies (CB) must be

ISO 65 accredited

• Restricting initial non-accredited

certification activities

• All certification bodies have had

external system and witness

assessments before entering large

scale certification activities

THE GLOBALG.A.P SYSTEM

Publication of All Approved CBs on the

Website

•Status and scope of accreditation

•Contact details

•Country offices

•Worldwide choice of CBs

© GLOBALG.A.P Secretariat | Page 72

Certification Body

Producer/

Producer Group

Accreditation Body Memorandum of

Understanding

Accreditation

ISO 65

Licence

Agreement

Sublicence

Agreement

GLOBALG.A.P

Secretariat

Page 73

DO YOU KNOW ALL RAW MATERIAL PRODUCERS?

EFFECTIVE MANAGEENT OF PRODUCER

INFORMATION

• Use our database to get a

structured overview of your

suppliers

© GLOBALG.A.P. Sekretariat | Seite 73

Page 74

GLOBALG.A.P FLOWERS AND ORNAMENTALS

•RECOGNIZED CERTIFICATION BODIES

• ABCERT AG Germany

• Agrar-Control GmbH Germany

• AgroManagement Denmark

• AGROQUALITA S.p.a Italy

• BCS Öko-Garantie GmbH Germany

• CERES - Certification of Environmental Standards

GmbH Germany

• Certiquality S.r.l. Italy

• Control Union Certifications B.V. Netherlands

• CSQA Certificazioni Srl Italy

• ECAS B.V. Netherlands

• Eco-LOGICA Costa Rica

• ICONTEC Colombi

• IMO - Institute for Marketecology Switzerland

• Institute of Quality & Control Israel

• IRAM-Instituto Argentino de Normalizacion y

Certificacion Argentina

• Lacon - Privatinstitut für Qualitätssicher. und

Zertifizierung Österreich

• LSQA (LATU Sistemas S.A.) Uruguay

• National Britannia Certification Ltd England

• NSF-CMi Certification England

• ProCert Safety AG Switzerland

• SATIVA Desenvolvimento Rural Lda Portugal

• SGS Australia PTY LTD Australia

• The Kenya Flower Council Kenya

Page 75

CERTIFIED PRODUCERS BENCHMARKED SCHEMES

• Belgium

• Switzerland

• Colombia

• Costa Rica

• Germany

• Denmark

• Ecuador

• Egypt

• Spain

• Ethiopia

• England

• Indonesia

• Israel

• Italy

• Kenya

• Sri Lanka

• Morocco

• Netherands

• Portugal

• Turkey

• Tanzania

• Uganda

• South Afrika

• Zambia

In total nearly 600 producers in

2 countries

GLOBALG.A.P FLOWERS AND ORNAMENTALS

© GLOBALG.A.P Secretariat | Page 75

• FLORVERDE – Colombia

• MPS-GAP – Netherlands

• SWISSGAP HORTIKULTUR – Switzerland

• KENYAGAP – Kenya

• KENYA FLOWER COUNCIL – Kenya

Page 76

GLOBALG.A.P NATIONAL TECHNICAL WORKING

GROUPS

MORE LOCAL INPUT IN GLOBALG.A.P STANDARD SETTING

© GLOBALG.A.P Secretariat | Page 76

Europe

Belgium

Bulgaria

Czech Republic

Denmark

France

Germany

Greece

Africa

Cote D‘Ivoire

Egypt

Ghana

Kenya

Senegal

South Africa

Tanzania

Uganda

Italy

Netherlands

Norway (Aqua)

Poland

Spain

Turkey

Ukraine New NTWGs in 2010

North/South America

Argentina

Brazil

Chile (Aqua/FV)

Colombia (Aqua/FV)

Costa Rica

Guatemala

Mexico

Peru

Uruguay

USA

Page 77

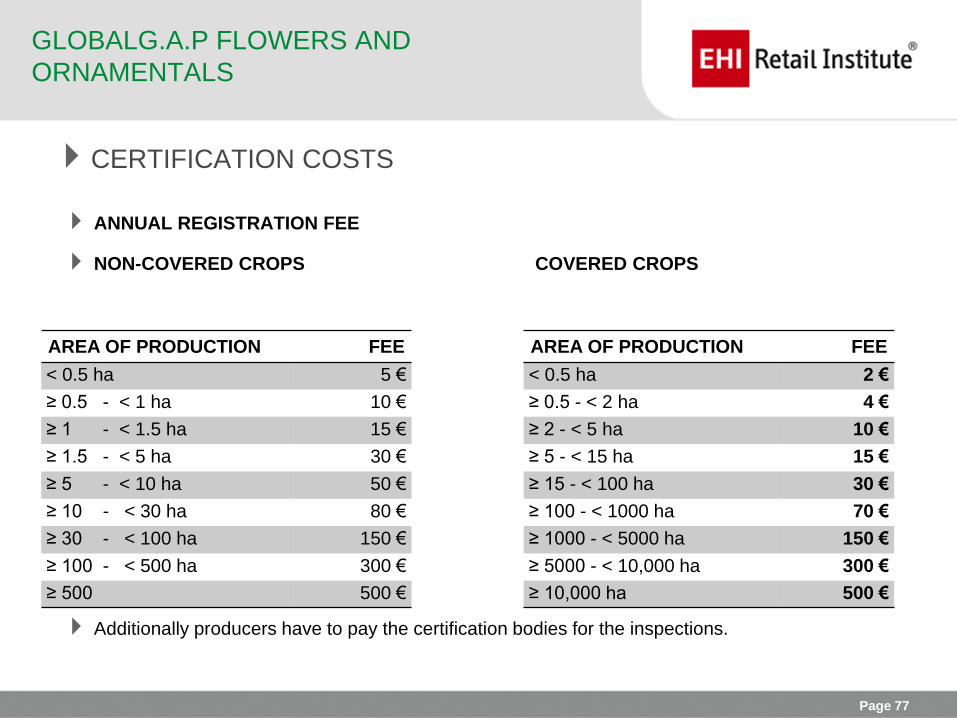

CERTIFICATION COSTS

ANNUAL REGISTRATION FEE

NON-COVERED CROPS COVERED CROPS

Additionally producers have to pay the certification bodies for the inspections.

GLOBALG.A.P FLOWERS AND

ORNAMENTALS

AREA OF PRODUCTION FEE

< 0.5 ha 5 €

≥ 0.5 - < 1 ha 10 €

≥ 1 - < 1.5 ha 15 €

≥ 1.5 - < 5 ha 30 €

≥ 5 - < 10 ha 50 €

≥ 10 - < 30 ha 80 €

≥ 30 - < 100 ha 150 €

≥ 100 - < 500 ha 300 €

≥ 500 500 €

AREA OF PRODUCTION FEE

< 0.5 ha 2 €

≥ 0.5 - < 2 ha 4 €

≥ 2 - < 5 ha 10 €

≥ 5 - < 15 ha 15 €

≥ 15 - < 100 ha 30 €

≥ 100 - < 1000 ha 70 €

≥ 1000 - < 5000 ha 150 €

≥ 5000 - < 10,000 ha 300 €

≥ 10,000 ha 500 €

Page 78

CONTENT OF THE STANDARD

SITE HISTORY AND SITE MANAGEMENT

RECORD KEEPING AND INTERNAL SELF-

ASSESSMENT/INTERNAL INSPECTION

WORKERS HEALTH, SAFETY AND WELFARE

SUBCONTRACTORS

WASTE AND POLLUTION MANAGEMENT,

RECYCLING AND RE-USE

ENVIRONMENT AND CONSERVATION

COMPLAINTS

RECALL/WITHDRAWAL PROCEDURE

GLOBALG.A.P STATUS

LOGO USE

© GLOBALG.A.P Secretariat | Page 78

GLOBALG.A.P FLOWERS AND ORNAMENTALS

Page 79

CONTENT OF THE STANDARD

TRACEABILITY

PROPAGATION MATERIAL

SITE HISTORY AND SITE MANAGEMENT

SOIL MANAGEMENT

FERTILIZER APPLICATION

IRRIGATION/FERTIGATION

INTEGRATED PEST MANAGEMENT

PLANT PROTECTION PRODUCTS

EQUIPMENT

PROPAGATION MATERIAL

SOIL AND SUBSTRATE MANAGEMENT

FERTILIZER USE

HARVESTING

POST-HARVEST TREATMENTS

PLANT PROTECTION PRODUCTS

© GLOBALG.A.P Secretariat | Page 79

GLOBALG.A.P FLOWERS AND ORNAMENTALS

Page 80

HOLISTIC APPROACH TO FARM ASSURANCE

GRASP to producers

Voluntary assessment – no impact on

the GLOBALG.A.P Certificate

Only applicable if a National

Interpretation Guideline is available

(local stakeholder consultation)

1 day individual training course for

GLOBALG.A.P auditors and inspectors

- one stop visit

National Interpretation Guidelines:

Austria, Brazil, Chile, Colombia, Costa

Rica, Kenya, Mexico, Morocco, South

Africa, Spain, Vietnam

GLOBALG.A.P RISK ASSESSMENT ON SOCIAL

PRACTICE (GRASP)

Principles:

• Raising Awareness on social issues

• Risk assessment – transparent results

via GLOBALG.A.P Database

• Providing implementation tools

Page 81

STEP-WISE APPROACH TO GLOBALG.A.P CERTIFICATION

© GLOBALG.A.P Secretariat | Page 81

PFA

Foundation

Level

PFA

Intermediate

Level

GLOBALG.A.P

• GLOBALG.A.P Primary Farm

Assurance (PFA): the response

for emerging markets

• Implementation through the

GLOBALG.A.P System following

member demands

• Implementation currently in the

USA, India, Poland, China,

Kenya, South Africa

GLOBALG.A.P AND SUSTAINABIILITY

Page 82

OUTLOOK

• We can display retailer specific

requirements in add-on

checklists (water usage,

sustainability requirements,

field passport)

• We cooperate with product

labeling initiatives which

• Engage in our Technical

Committees

© GLOBALG.A.P Secretariat | Page 82

GLOBALG.A.P FLOWERS AND

ORNAMENTALS

Page 83

Why are retailers so powerful?

Summary

Page 84

The basic difference between a supplier

and a wholesaler/retailer:

- the supplier depends on his

product

- the retailer can exchange

product A against product B

Summary

Page 85

Retailers have a profile via their

assortment – their product mix!

Summary

Page 86

Today’s retail is mass distribution: this is

only possible by international standards

Summary

Page 87

For the retailer the standard might be

even more important than the product

itself

Summary

Page 88

Standards as enablers for business have

to be created by TeamSpirit between all

stakeholders.

Summary

Page 89

Speaker:

Prof.Dr.Bernd Hallier

EHI Retail Institute

Spichernstraße 55

50672 Cologne

www.ehi.org

www.european-retail-academy.org

Thank you!