restructuring road management - trend or necessity?lnweb90.worldbank.org/.../$file/rrmton02.pdf ·...

TRANSCRIPT

INTERNATIONAL SEMINAR

BRA / NRA Seminar onRestructuring Road Management – Trend or Necessity?

Experiences of Institutional and Managerial Reformsin Baltic and Nordic Road Administrations

26. - 27. September 2002, in Pärnu, Estonia

TECHNICAL REPORT

Organizers

Baltic Road AssociationNordic Road Association

Estonian National Road Administration

PÄRNU 2002

Seminar on Restructuring Road Management – Trend or Necessity?

2

CONTENTSROAD TRANSPORT, ROAD MANAGEMENT AND RESTRUCTURING OF ROADMANAGEMENT IN ESTONIA ......................................................................................................... 5

Märt Järvik, Head of the Road Traffic Department,Ministry of Transportation and Communications, Estonia

ROAD POLICY (FINANCING, ORGANIZATION) Latvia Case..................................................... 9Talis Straume, Director of the Road Traffic Department,Ministry of Transportation, Latvia

REFORM OF STRUCTURES. OWNERSHIP POLICY AND CORPORTE GOVERNANCE.RE-STRUCTURING OF FINNISH ROAD ADMINISTRATION .................................................. 11

Samuli Haapasalo, Director General of the Ownership Policy and Privatisation Department, Ministry of Transport and Communications, Finland

ROAD MANAGEMENT REFORM IN ESTONIA.......................................................................... 17Riho Sõrmus, Director General, Estonian Road Administration

ROAD ADMINISTRATION REFORMS......................................................................................... 20Olafs Kronlaks, Director General, Latvian Road Administration

LITHUANIAN ROADS .................................................................................................................... 25Virgaudas Puodžiukas, Director General, Lithuanian Road Administration

ROAD ADMINISTRATION REFORMS IN DENMARK............................................................... 36Henning Cristiansen, Director General, Danish Road Administration

ROAD ORGANISATIONS’ REFORM IN FINLAND .................................................................... 43Eero Karjaluoto, Director General, Finnish Road Administration

RESTRUCTURING OF THE NORWEGIAN PUBLIC ROADS ADMINISTRATION................. 53Olav Soefteland, Director General, Norwegian Public Roads Administration

ROAD ADMINISTRATION REFORMS IN SWEDEN .................................................................. 58Ingemar Skogö, Director-General, Swedish National Road Administration

TARTU REGIONAL ROAD OFFICE, HOW IT FUNCTIONS...................................................... 65Kuno Männik, Regional Road Director, Estonian Road Administration

ROAD MANAGEMENT REFORM IN LATVIA, ITS RESULTS, RECOMMENDATIONSAND PERSPECTIVES WITHIN THE CONTEXT OF ROAD MAINTENANCE......................... 70

Vilnis Urbanovics, President of State Joint Stock Company (Central Region Roads),Latvia

SURPASSING THE SWEDISH MODEL OF ROAD MANAGEMENTLIBERALISATION?......................................................................................................................... 74

Martin de Jong, Delft University

PRIVATISATION OF ROAD MAINTENANCE IN ESTONIA ..................................................... 92Ants Kikas, Chairman of the Board, TP Consulting, Ltd., EstoniaKostel Gerndorf, Tallinn Technical University, Estonia

Seminar on Restructuring Road Management – Trend or Necessity?

3

DANISH USER SURVEY .............................................................................................................. 107Jarl Ahlers Mortensen, Head of Secretariat, Operation and Maintenance, Denmark

LEADERSHIP AND VALUES IN ROAD ADMINISTRATIONS ............................................... 120Elisabeth Schjølberg, Regional Director, Norwegian Public Roads Administration

MANAGEMENT OF THE STATE ROAD FUND ........................................................................ 122Vilnis Millers, Head of State Road Fund Department, Latvian Road Administration

NEW MODELS FOR FUNDING TRANSPORT INFRASTRUCTURE SERVICES................... 129Lasse Weckström, Development Director, Finnish Road Administration

PROCUREMENT STRATEGY, NEW INNOVATIVE PROJECT DELIVERY METHODS,PARTNERING & CLIENT PERSPECTIVES................................................................................ 130

Pekka Pakkala, Procurement Development Manager, Finnish Road Administration

PERFORMANCE BASED PROCUREMENT, NORWEGIAN PPP ROAD PROGRAM............ 139Kjersti Billehaug, Chief Engineer, Norwegian Public Roads Administration

Seminar on Restructuring Road Management – Trend or Necessity?

4

Prefatorily

Dear user!

Hereby you have the collection of the presentations to Pärnu Seminar in the order ofthe official time-schedule for Sept. 26th and 27th.

The presentations have been included in their authentic shape i.e. as they weresubmitted by the authors. In some cases you find only text, in other cases only slidesor both text and slides. The compilers of the collection have not revised the texts andtitles either on their substance or grammar.

Both CD and paper versions are legally equal.

We wish you succesfully pass the next steps of your reforms.

Organizers

Seminar on Restructuring Road Management – Trend or Necessity?

5

ROAD TRANSPORT, ROAD MANAGEMENT ANDRESTRUCTURING OF ROAD MANAGEMENT IN ESTONIA

Märt JärvikHead of the Road Traffic Department

Ministry of Transportation and Communications, Estonia

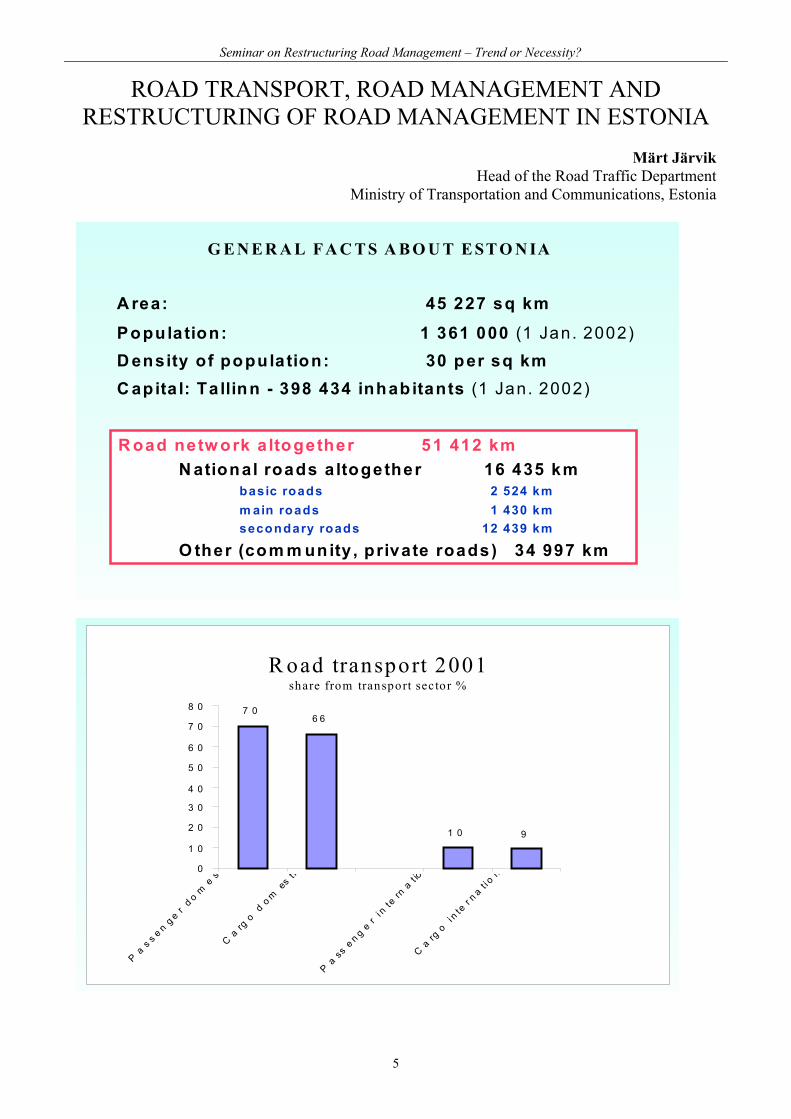

A rea: 45 227 sq km

G E N E R A L F A C T S A B O U T E ST O N IA

Population: 1 361 000 (1 Jan. 2002)D ensity of population: 30 per sq kmC apita l: Ta llinn - 398 434 inhabitants (1 Jan. 2002)

R oad netw ork a ltogether 51 412 kmN ational roads a ltogether 16 435 km

basic roads 2 524 kmm ain roads 1 430 kmsecondary roads 12 439 km

O ther (com m unity , private roads) 34 997 km

7 06 6

1 0 9

0

1 0

2 0

3 0

4 0

5 0

6 0

7 0

8 0

Pa

s s e ng e

r d o

me

s

Ca

rgo

do m

est ic

Pa

sse n g

er

i nte

rna

t io

Ca

rgo i n

ter n a

t i on

R oad transport 2001share from transport sector %

Seminar on Restructuring Road Management – Trend or Necessity?

6

Road Offices Jan. 01, 2002

Regional Road Offices Jan. 01, 2003

Seminar on Restructuring Road Management – Trend or Necessity?

7

GENERAL FACTS ABOUT ESTONIA

Motor vehicles (1Jan 2002) 493 349including passsenger cars 407 272lorries 80 535buses 5 542motorcycles 6 837

Road traffic accidents (2001) 1 889Killed 199Injured 2 444

Automobiles per 1000 inhabitants 372 (1 Jan 2002)Passenger cars per 1000 inhabitants 312Killed per 100 000 inhabitants 14,6Killed per 10 000 automobiles 4,0

DEATH RATE IN SEVERAL COUNTRIES

0

5

10

15

20

25

30

0 100 200 300 400 500 600 700 800 90 0

A ut om ob ile s p e r 10 00 inh ab itan ts

Fat

alit

ies

per

100

000

inh

abita

n

L V

R U SL T G R

PLC YS L OE ST O N IA

E

C ZB

F L

A

H

B G

S K

IR O

IR LD K D

F IN

C HIL ISN L NS

U K

M T

P

U S A

M KT R

Seminar on Restructuring Road Management – Trend or Necessity?

8

Fatalities per 100 000 inhabitantsin Nordic countries and in Estonia

Liiklusõnnetuste läbi hukkunute arv Eestis ja Põhjamaades 100 000 elaniku kohta

0

5

10

15

20

25

30

35

1975 1980 1985 1990 1995 2000 Eesti Norra Soome Rootsi Taani

EST DK

N S FIN

Vision 100

321

364

250

227

213

202

189

175

159

130

118

108

103

100

199204232

213

279284

332

287

491

436

343

142

0

100

200

300

400

500

600

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Hukk

unute

arv a

astas

LÕ hukkunud Visioon100

LÕ hukkunud (trend)

Seminar on Restructuring Road Management – Trend or Necessity?

9

ROAD POLICY(FINANCING, ORGANIZATION)

Latvia CaseTalis Straume

Director of the Road Traffic DepartmentMinistry of Transportation, Latvia

FINANCING

Basic Strategic Concept

ROAD USER IS A ONE WHO PAYS FOR ROAD INFRASTRUCTURE USAGE

Development Scenario

1991 – 1994 road infrastructure financed from the state budget by means of appropriation of thefunds

1994 - establishment of the State Road Fund- introduction of the annual vehicle tax and earmarking it as a direct State Road

Fund revenue

1996 introduction of the excise duty on oil prodects providing that 50% of the amountlevied is assigned to the State Road Fund

2000 60% of the excise duty on oil products assigned to the State Road Fund

2002 decision of the Parliament (Saeima) to assign to the State Road Fund 85% of theexcise duty on oil products setting out for the Government the task to draft all thenecessary legislative amendments for implementation of the decision alongside withthe preparation of the Budget of 2003(according to the statistics available a transport share constitutes 85% of the totalamount of the excise duty levied)

SHORT TERM TASKS:

- to provide legal basis for implementation of the parliamentary decision to assign to the StateRoad Fund 85% of the levied amount of the excise duty;

- to assess the feasibility of replacing the existing system when the assigned excise duty share isexpressed in percentage of the total by that fixing certain amount per separate unit

The option to be explored: to fix that from each fuel liter sold X santims are assigned to the RoadFund.

Seminar on Restructuring Road Management – Trend or Necessity?

10

ORGANIZATION

Basic Strategic Concept

ROAD INFRASTRUCTURE SHOULD BE MANAGED AS A BUSINESS STRUCTURE

Development Scenario

1991 – 1994 privatization of the so called “heavy road industry”, state owned only the companiesdealing with daily road maintenance

1997 – 1998 - separating of the functions of CUSTOMER-CONSULTANT-ENTREPRENEUR

- establishment of the State Stock Company “Latvian Road Administration”;administration of the road network performed on the basis of the Agreementwith the Ministry of Transport

- commercializing of daily road maintenance works establishment of four regionalstate stock comapanies dealing with daily road maintenance

- concluding of the first five year period daily road maintenance prerformancecontracts

2002 first public tender for performance of daily road maintenance works within the next5-year period

SHORT TERM TASKS:

- setting out of governmentally approved road condition standards

OPTIONS TO BE EXPLORED:

- establishing of a separate Road Fund Agency chaired by the Road Council which representsboth the interests of the owner (the Ministry) and the road users;

- determination of optimal amounts of road maintenence lots to be put under tendering;

- evaluation of the expedience of privatization of road maintenance state stock companies

Seminar on Restructuring Road Management – Trend or Necessity?

11

REFORM OF STRUCTURES.OWNERSHIP POLICY AND CORPORTE GOVERNANCE.

RE-STRUCTURING OF FINNISH ROAD ADMINISTRATIONSamuli Haapasalo

Director General of the Ownership Policy and Privatisation DepartmentMinistry of Transport and Communications, Finland

I. THE MINISTRY OF TRANSPORT AND COMMUNICATIONSFINLAND

REFORM OF STRUCTURES 1990-2002

1989:Purview of the Ministry of Transport and Communications consisted mostly of agencies:

• 3 AGENCIES- Road Administration- Motor Vehicles Registration Centre- Telecommunications Administration Centre

• 3 ENTERPRISES OPERATING AS AGENCIES- Finnish state railways- Post and Telecommunications of Finland- Finnish Civil Aviation Administration

• 1 RESEARCH INSTITUTE- Finnish Meteorological Institute

• 2 STATE-OWNED LIMITED COMPANIES- Finnair Plc- Finnish Broadcasting Company

2002:• 8 LIMITED COMPANIES

- Finnair Plc (share issue 1995)- Finnish Broadcasting Company Ltd- Finland Post Plc 1- Sonera Plc (Telecom Finland)

Sonera has been partly privatized in 1998, 1999 and 2000;Rights issue 2001; Merger agreement 2002

- VR Group Ltd (1990 - 30.6.1995 state owned enterprise)- Finnish Motor Vehicle Inspection Ltd (1993 - 1995 state owned enterprise)- Raskone Ltd (1994 - 1998 state owned enterprise)- Dedicated Networks Of Finland Ltd

• 2 STATE-OWNED ENTERPRISES- Finnish Civil Aviation Administration (1991 -)- Finnish Road Enterprise (2001 -)

1 1990 - 1993 Post and Telecoms was a state owned enterprise, 1994 - 30.6.1998 PT Finland Ltd, 1.7.1998 PT Finland

Ltd was demerged into two companies(All underlined have a new organisational model)

Seminar on Restructuring Road Management – Trend or Necessity?

12

• 2 AGENCIES- Road Administration- Maritime Administration (net budgeted agency)

(ongoing restructuring: Maritime Administration, 3 state enterprises?)

• 3 SMALL ADMINISTRATIVE AND REGULATIVE AGENCIES- Finnish Communications Regulatory Authority (including postcommunications)- Vehicle Administration Centre- Rail Administration

• 2 RESEARCH INSTITUTES- Meteorological Institute- Marine Research Institute

REFORM OF STRUCTURES ON THE PURVIEW OF MINISTRY OF TRANSPORT ANDCOMMUNICATIONS FINLAND1990 - 2002(State owned unincorporated enterprises and limited companies)

THE MAIN CHANGES:

• POST AND TELECOMMUNICATIONS OF FINLAND, STATE OWNED ENTERPRISE1990 1993

• FINNISH STATE RAILWAYS, STATE OWNED ENTERPRISE 1990 - 30.6.1995

• FINNISH CIVIL AVIATION ADMINISTRATION, STATE OWNED ENTERPRISE 1991

• MOTOR VEHICLES REGISTRATION CENTRE, STATE OWNED ENTERPRISE 1993 1995

• RASKONE (State Repair Shop), STATE OWNED ENTERPRISE 1.7.1994 - 1998

• PT FINLAND LTD. (Finnish Post Ltd.; Telecom Finland Ltd.), LIMITED COMPANY 1994

• VR GROUP LTD. (Finnish State Railways), LIMITED COMPANY 1.7.1995

• FINNISH MOTOR VEHICLE INSPECTION LTD., LIMITED COMPANY 1996

• NEW STRUCTURE FOR MARITIME ADMINISTRATION (into a net budgeted agency)

• DEMERGER OF PT FINLAND: SONERA-GROUP PLC, FINLAND POST LTD, 1.7.1998

• SONERA’S PARTIAL PRIVATISATION 11/1998 (IPO), 10/1999, 03/2000, RIGHTS ISSUE2001, MERGER AGREEMENT 2002

• RASKONE, LIMITED COMPANY 1999

• ROAD ADMINISTRATION 2001 1) AGENCY, 2) FINNISH ROAD ENTERPRISE

• MARITIME ADMINISTRATION (restructuring in process)

II. OWNERSHIP POLICY AND CORPORATE GOVERNANCE

REORGANISATION AND BUSINESS PRINCIPLES – CONCEPT AND STRUCTURE

• Application of business principles is the only way to promote services

• Through incorporation the owner can acquire and realise financial value

Seminar on Restructuring Road Management – Trend or Necessity?

13

Sonera: EUR 6.6 billion, relatively the greatest financial value acquired from any company inany European country (although the state still owns 52,8% of the company)

• Clear separation of regulation from ownership monitoring

Legislation Ownership monitoringEU regulation Ownership policyLicences PrivatisationControl Corporate Governance

• Opening competition in each incorporation case

Model of unincorporated state enterprises also used in non-competitive markets

CURRENT BUSINESS STATUS IN THE FIELD OF TRANSPORT ANDCOMMUNICATIONS

LISTED COMPANIES: Ownership % (Authorisation)• SONERA CORPORATION (PLC) 52,8 (0)• FINNAIR GROUP (PLC) 58 (50)

STATE OWNED COMPANIES:• FINLAND POST CORPORATION (PLC) 100• VR GROUP 100• FINNISH MOTOR VEHICLE INSPECTION 100 (0)• RASKONE LTD (state repair shop) 86 (67)• DEDICATED NETWORKS OF FINLAND LTD 100• FINNISH BROADCASTINGCOMPANY, YLE 100

(monitoring by Parliament)

UNINCORPORATED STATE ENTERPRISES:• Finnish Civil Aviation Administration 1991 • Finnish Road Enterprise 2001

REGULATORY DEPARTMENTS• Communications Department• Transport Policy Department

ORGANISATIONS THAT BUY SERVICES• Finnish Communications Regulatory Authority (Ficora)• Finnish Road Administration• Finnish Rail Administration• Finnish Vehicle Administration

PRINCIPLES OF OWNERSHIP MONITORING• Shareholder value• Market-orientation• Corporate Governance

- Board of directors- All board members independent business experts etc. outside of the company- Owners at the AGM (annual general meeting)- Principle: no interference at operational level (Company Act, Stock Market Act, Prospectus)

Seminar on Restructuring Road Management – Trend or Necessity?

14

THE MAIN PRINCIPLES OF GOVERNMENT’S OWNERSHIP POLICY ESPECIALLYIN TELECOM, MOBILE AND SERVICE SECTOR:• The state is fully market oriented owner, as any professional institutional investor• Fully commercial• Pragmatic• Strong value orientation• The state does not interfere at operational level• Room and flexibility for the company to grow and develop based on the Finnish knowhow and

technological expertise as a part of the whole cluster• Pragmatic approach in privatisation; the government to remain as liberal regulator, not as an

owner

MODEL OF UNINCORPORATED STATE ENTERPRISES• Act on unincorporated state enterprises = ”Companies Act”• Separate acts on unincorporated state enterprises

- Finnish Civil Aviation Administration Act- Finnish Road Enterprise ActThese acts and government’s decisions establish unincorporated state enterprises, decide ontheir property as shown in balance sheet and provide for the special features of each enterprise.

• Permanent model(Finnish Civil Aviation Administration)

• Interim stage before a company is established(Sonera Corporation, Finland Post Corporation, VR Group, Finnish Motor Vehicle Inspection,Raskone; Finnish Road Enterprise?)

• A flexible, effective model to combine business and service production• Business operations the same as in a limited company

- independent decision making- internal financing (not in the state budget)- decisions on investments- decisions on resources- loaning- own board of directors and CEO

• Yet a part of government organisation- Moderate monitoring by Parliament- Moderate framework monitoring by the Government and the Ministry of Transport and

Communications• Also possible in monopolistic sectors

III. THE RE-STRUCTURING OF FINNISH ROAD ADMINISTRATION

”A well functioning infrastructure is perhaps the most crucial basis for all development in themodern society”

- all the transport modes, telecommunications

Traditionally Ministry of Transport and Communications together with several agencies hasbeen responsible for the infrastructure issues. The agencies are usually organised according todifferent modes of transport, Road, Rail and Maritime etc.

(agencies)

Seminar on Restructuring Road Management – Trend or Necessity?

15

In Finland we used to have all the roles of road policy and production in the same agency –Finnish National Road Administration• budgeting• building, maintenance• purchasing/ordering and competitive tendering/bidding• traffic safety• regional issues

The first implementation step in Finland in 1997 governmental decision in the CabinetCommittee on Economic Policy:• Clear separation of roles

1. Ordering, competitive tendering, administrative affairs, ownership2. All production

• The separation of the roles all through the organisation in the headquarters and in all regionalorganisations

2001CLEAR ORGANISATIONAL RESTRUCTURING

THREE MAIN POINTS:• Road Administration

- Client, invitations for tenders, bidder, authority, developer• Road Enterprise

- separate business organisation almost like a plc (out of the state budget, own income, owninvestment, CEO and board etc.), but some overall framework and monitoring fromParliament, Government and Ministry

- field: building, maintenance, planning• Full competition

- but some steps protecting the existing private sector (max 4 years)

WHAT WAS THE GOAL OF THE MTC?• Cost-efficiency

more and better quality for the same money• Clear structures and separate roles• Development of the whole industry (incl. private sector infrastructure maintenance, planning

and constructing companies)• Opening of competition• Technological development

new structures as a catalyst• Restructuring of the whole industry

- consolidation- networks and alliances- mergers and acquisitionsBetter infrastructure, ideal cost-efficiency

PRECONDITIONS TO BE FOLLOWED• Smooth principles concerning the personnel• No conflicts or turbulence in the existing market• Balanced time period in restructuring

- Competition opened gradually during 4 years in all areas• The very best of the whole industry

Normal market and competition

Seminar on Restructuring Road Management – Trend or Necessity?

16

WHICH KIND OF GOALS HAVE WE REACHED UNTIL NOW?• The new structure

- transparency- competition- basis for the development- more and better quality with the same money

~ re-allocation of the money• Better instruments for the MTC in transport and road policy

- the goals set for RA- ownership policy and corporate governance concerning RE- clarity and development of the private sector and the whole industry

• The development of Road Administration and clearance of its role• RE’s fine results in the first year 2001

- 16 MEUR extra result and dividend (!) from the Road Enterprise• Cost-efficiency

Seminar on Restructuring Road Management – Trend or Necessity?

17

ROAD MANAGEMENT REFORM IN ESTONIARiho Sõrmus

Director GeneralEstonian Road Administration

The present report should give you a brief overview of the restructuring/reorganization of the roadmanagement organization in Estonia. The reports of my colleagues will surely supplement andspecify the topic.

The structure and administration of the road management organizations has lately been a topicalissue in many countries. So it is here, in Pärnu, on our present Workshop.

The reason is simple. There is no standard road management structure which would satisfy allcountries. As countries have different names, they have also different economic policies anddifferent level of development. What is possible and acceptable in one country, needn’t be so inanother. But in nearly all countries, the main aim of restructuring has been, and is, decreasing therole of the state and increasing the role of private sector in road management. I mean both statejoint-stock companies and private enterprises. All efforts to reorganize the road managementorganization by optimal strenghening etc. of the role of the state have ended and will end in futurewith the realization that only enterprising spirit will help us more ahead. The state, however, hasalways retained the role of drafting, ordering and checking, although a certain videspread stableforesees privatizing this function as well.

We cannot forget two opposite concepts – monopoly and competition. In my opinion, in manycountries there is imaginary competition which under closer scruting turns out to be a certainapproved monopoly. But that’s enough of speculations, let’s get to the point – Estonia.

Estonia has been a traditional country where road management has been carried out via theMinistry of Transport and Communications in the Road Administration and via the RoadAdministration in the county road offices. Until 1999 our organization had a classical and simplestructure – in every county there was a road office administered by the Road Administration andfinanced from the state budget. We have 15 counties. This was a good and simple system. At thebeginning of 90-ies the road offices did everything – maintenance, repairs, road construction oncounty roads, produced materials, asphaltconcrete and did all that on their own orders or the ordersof the Road Administration. They had necessary equipment and production factories/bases. Theychecked their own work as well. Only the construction of the most important main roads wasordered from private enterpreneurs at the beginning of the 90-ies. Road offices also participated inthe procurement process going on out of state roads, which network was of course wrong. Togetherwith the decreasing finances and the development of economic policy it became clear in mid nintiesthat it was harmful and dangerous to continue in the same way and it would be better toreorganizing oneself rather than reorganized from above.

Due to decreased finances, the production factories and most of the equipment was not used tothis full capacity.

The development of economic policy caused the separation of the roles of the orderer and theperformer of the work. The experiences of many countries in reorganizing their structure wereexamined. As no model used in other countries seemed to be suitable for overtaking, which wasalso proved later, the need for consultants arose.

Thus, the reorganization plan of the road management organization was elaborated and adoptedby the Ministry in 1997. The main emphasis in the plan was laid on the county road office. On thatlevel the plan set forth privatisation of all the production facilities – asphalt concrete plants, theequipments – that is all the production property. Maintenance work was left in the hands of thestate. In addition, the legal basis required development, general and financial management neededimprovement.

As there was great debate concerning maintenance, it was first decided to privatize maintenancein one county and thouroughly analyse the results. The sale of production factories/bases was

Seminar on Restructuring Road Management – Trend or Necessity?

18

started, but soon on this basis of experiences doubts arose, that in those counties where maintenancecould be privatised, it was not necessary to sell the production bases before starting the process ofprivatising. On the one hand, the sale of the production bases was not a simple or rapid process, onthe other hand, there was political pressure that maintenance should be privatised also in some othercounties.

In the year 2000 a private enterprise started work in Põlva county. It partly bought and partlyrented the assets of the road office and employed an agreed part of the employees – both workersand office staff. The road office itself continued the work with 16 clerks as the drafter, orderer andchecker of the work. The length of the contract is 5 years. In other 14 countries where maintenancewas privatised, the road office was planned to remain the orderer of repairs and construction workand carry out maintenance itself or order if from other enterpreneurs.

There was much discussion about the form of enterprise – whether if should be a state joint-stockcompany or private enterprise. The former would have been a transitional entity on the way ofprivatisation. Later the shares of the state joint-stock company should have been sold anyway. Thiswould have made the process of privatisation longer, more complicated and more expensive.

As I mentioned before, due to great political pressure, it was decided in 2000 (before malingeconomic analysis which would give correct data only in 3-4 years) to proceed with privatisingmaintenance work, first in two counties and after a few month in two more counties – alltogether in4 counties.

At the same time, it was decided to transform one road office intoa state joint-stock company andas soon as possible sell its shares. The formed state joint-stock company had to participate on equalbasis together with other private enterprises in the bidding in order to get the maintenance contract.The result was that the state joint-stock company won the bidding and got the contract for 5 years.

Legal problems made the planned privatising of maintenance work in 4 counties morecomplicated, in 2001 maintenance was privatised in one more county. By the end of 2001maintenance work was performed on private basis in 3 counties in 2 there was a private limitedcompany and in one a state joint-stock company. As you can see, we have been very careful withprivatising maintenance work.

Political pressure continued and we saw that the conditions of the roads had not deteriorated, ifwe leave aside problems of financing maintenance, which occurred all over the country. Financesfrom maintenance from the state budget decreased this year, but the contracts in 3 counties providedfor an increase of maintenance costs by a few per cent. Thus, there was only one possibility ofsolving the problem and that was at the expense of those counties where maintenance work wascarried out by the state or the state road office.

That in turn increased the wish to speed up privatising process in maintenance work. Thatdecision presumes changes in the structure, functioning and organisation of work in the roadmanagement organization.

For establishing a profesional and administratively capable road management organization wherebudgetary resources which mainly cover administrative costs are rationally used, it is practical toform an ordering organization whose management structure is based on regional centres in the formof regional offices.

Research carried out in that line showed that it is practical to form 6 regional road offices inEstonia, whereas they maintain the right to carry out maintenance work themselves in thosecountries where the regional centre is situated. The main reason for that decision was the wish toavoid possible monopolies in the market of maintenance work and to control prices.

In December 2001, the relevant decision was made by the minister – to form 6 regions andprivatise maintenance work only in 9 counties, not in 15.

Concidering the functions of the former road offices and the experiences other countries, it isnecessary that in the mentioned 9 counties where maintenance work will be privatised, thesubordinate unit (subdivision) in the capacity of an ordering body will continue its existance, butnot as the former county road office. The laster will continue as departments of regional road

Seminar on Restructuring Road Management – Trend or Necessity?

19

offices, continuing to offer public service and ordering and checking of maintenance work in thecounty.

In the opposite case in 9 counties 15-18 people in the road offices as an ordering body wouldcontinue their work, whereas they would have lots of specific duties and the functions of the state asan orderer and drafter of work would not substantially decrease.

However, it is possible to centralise those functions to a great extent by joining 2-3 counties.That would favour specialization of employees and decrease administrative costs.

Thus, we can hope that by the end of the year the performers of maintenance work in 9 countiesin Estonia will be enterpreneurs in the form of 8 private enterprises and 1 State joint-stockcompany. At present 5 of them are already working in 4 counties, the tendering process has startedin order to establish the winner of the contract. Improvements are also being made in contracts andeconomic analysis in being carried out, but it is possible target a sufficient overview of the relationsof the state and private enterprise only in 3-4 years.

At present one more new regional road office (formed on 1.st July) is working. The next twoshould be established on 1.st November and the last 3 by the end of the year.

What would be the advantages of this reform in Estonia. Competition creates preconditions forfaster development of road management, the quality of the offered public service should improve asthe roles of the orderer and performer of the work are separated, the appearance and the passabilityof the roads should improve and become more uninform because there will be less subjectivity inapplying the requirements concerning the condition of the road, it is possible tpo use availableresources in a more optimal way.

What would be the disadvantages of the reform? On the basis of 1,5 year experiences, we cansay that road management is not so flexible and promptly managable where maintenance is carriedout by the private sector. That means we have to organise not planned additional tasks through thestate procurement system which takes 2-3 month. Due to scanty budgetary resources, there ismoney only only for maintenance work for a certain level of passability or roads, and we lackmoney for smaller repair work.

We cannot forget that the primary aim of enterpreneurs is to make profit. The state system, onthe other hand, tends to manage with excessive expenses although the system in certain cases ismore flexible. Enterpreneurs will first take a look at their contract and if certain work is notprovided for by the contract, they will ask that they will get for that.

In order to make the best decision whether to privatise all maintenance work in Estonia, weshould make the decision in 2005 or 2006, despite political pressures.

By way on conclusion I can say that the reorganisation process carried out in Estonia now is notfinal, ideal or 100% suitable for some other country which has not started with the reorganization ofroad management.

Seminar on Restructuring Road Management – Trend or Necessity?

20

ROAD ADMINISTRATION REFORMSOlafs KronlaksDirector General

Latvian Road Administration

Five years have passed since the reorganisation in 1997, which was the most significant in thewhole lifetime of the Latvian Road Administration. At present it has sustained verification by timeand it has been widely recognised.

Before the first of June 1, 1997, the Latvian Road Administration (LRA) was a state civil serviceinstitution subordinate to the Ministry of Transport (MoT). The Latvian Road Administration had26 directly subordinate routine maintenance companies with approximately 2500 employees intotal. The Latvian Road Administration was directly responsible for road routine maintenancetherefore it directly purchased maintenance machines and materials. State contracts for periodicmaintenance, reconstruction and construction were awarded by the LRA to private contractors.LRA and subordinate road maintenance companies were greatly influenced by differentorganisational and financial regulations and due to this fact the salaries were low, and theemployees had little motivation to work permanently at the road administration.

The reorganisation was implemented in June, 1997, after the government had initiated thedelegating of certain state functions to state owned business companies. In the result the LRA wastransformed into a non-profit state owned company which was owned by the Ministry of Transportbut which could work according to free market principles and decide about its own developmentand structure independently. The LRA became a consultant to the Ministry of Transport and nowhas made an agreement with the MoT about performing some of the functions of the MoT. 26routine maintenance companies became independent from the LRA and were transformed into 4independent state joint stock companies for road routine maintenance, which now execute roadroutine maintenance works on the basis of 5-year contracts with the Latvian Road Administration.

LRA’s activities after the reorganisation are greatly based on business company principles in amarket economy. LRA awards state contracts to private contractors through bidding and tenders,and now LRA is becoming more and more independent in deciding about the use of its ownresources. LRA has become competitive and attractive employer in the road engineering market andbecause of this it acquired a stabile number of employed road engineers.

The present Status of the Latvian Road Administration is a Non-profit organisation state jointstock company “Latvian Road Administration”, The company is registered in the Latvian Registerof Enterprises; its actual owner is the state and its supervisor is the Ministry of Transport. Mainlegal documents regulating the activities of the LRA are the Statutes of the Latvian RoadAdministration, and the 5-year contract with the Ministry of Transport, with additional annualcontract with the Ministry of Transport.

4 state joint stock companies for road routine maintenance execute road routine maintenanceworks on the basis of 5-year contracts with the Latvian Road Administration each in its own region.

The present structure of the Latvian Road Administration includes four large divisions eachimplementing a part of the main functions of the Latvian Road Administration. Technical Divisionis responsible for preparing and following and the general strategy for the whole road sector,Production Division deals with road construction and periodic maintenance, in particular withtenders for road works and awarding of contracts to private companies. Road Maintenance Divisionis responsible for planning and supervising routine maintenance works, and Traffic OrganisationDivision is responsible for supervising road traffic safety both on state main roads and in cities.

The supervision of the Ministry of Transport over the LRA is implemented through the RoadTransport Department of the Ministry.

Seminar on Restructuring Road Management – Trend or Necessity?

21

Two state proxies who represent the stock holder’s meeting of the LRA are appointed by theMinistry and they check whether the LRA performs the duties defined in the agreement with theMinistry.

There is a number of benefits gained both by the LRA and its employees after theReorganisation. The LRA’s status allows to implement free market oriented principles and applypractices of private companies, for example be flexible in determining competitive salaries for itsemployees. The LRA now is maintaining a stabile personnel of engineers who are not so eager tochange careers. The stability of the staff ensures the improvement of quality of those works, whichthe LRA performs as the consultant to the ministry of Transport. The LRA finances thedevelopment of its own management systems and Information Technologies, which allow it tobecome more competitive. For example, at present the LRA is willing to certify its QualityManagement System according to ISO 9001.

Benefits to the employees are the following:• Additional payments and allowances, such as:

o additional motivation payments (bonuses for work results),o vacation allowance,o maternity and retirement allowances, etc.

• Education and training benefits, such as:o fully paid professional road engineering educationo full or partial payment of study fees which are not connected with civil engineering,

and,• Health and life insurance.

In conclusion some of the Future perspectives of the LRA have to be mentioned. The current tasksof the LRA still are the improvement of contract relations with the MoT, work with the politiciansin order to promote road sector needs and solution of problems and further development of theLRA’s personnel and competitiveness to be ready for future road sector market.

Important milestone will be the elections of the new Parliament, which will be held on October 5,2002. The new Parliament and the new government may initiate a number of new ideas andpolitical decisions, which may lead even to further reorganisations and changes in the road sectoraffecting also the Latvian Road Administration. At present it is unfortunately too early to make anysubstantial forecasts concerning such new political initiatives.

Status of the Latvian Road Administration (LRA) before June 1, 1997

• LRA – state civil service institution under the Ministry of Transport (MoT);• LRA has 26 directly subordinate routine maintenance companies• LRA directly purchases maintenance machines and materials;• LRA awards state contracts and supervises projects for periodic maintenance, reconstruction

and construction;• LRA is greatly influenced by financial regulations;• Salaries are low, personnel lacks motivation

Reorganisation

• Governmental initiative of delegating the state functions to business companies;• LRA is transformed into a non-profit state owned company;• LRA works basing on the agreement with the MoT and performs the functions of the MoT;

Seminar on Restructuring Road Management – Trend or Necessity?

22

• 26 routine maintenance companies are transformed into 4 independent state joint stockcompanies for road routine maintenance;

• State joint stock companies perform road routine maintenance works on the basis of 5-yearcontracts.

LRA’s Activities after Reorganisation

• LRA’s activities are based on business company principles in a market economy.• LRA awards state contracts to private contractors through bidding and tenders• LRA becomes more independent in deciding about the use of its own resources;• LRA becomes competitive in the road engineering market;• Personnel in the LRA becomes stabile.

LRA’s Status

• Full name – Non-profit organisation state joint stock company “Latvian Road Administration”;• Status – company registered in the Latvian Register of Enterprises; owner – the state;

supervisor – the Ministry of Transport• Main legal documents:

- Statutes of the Latvian Road Administration,- 5-year contract with the Ministry of Transport,- additional annual contract with the Ministry of Transport.

Four Road Routine Maintenance Regions

Kurzeme Roads

Vidzeme Roads

Latgale Roads

Central Region Roads

Seminar on Restructuring Road Management – Trend or Necessity?

23

LRA’s Structure

Road Maintenance Division

Maintenance Planning Department

Maintenance Supervision Department

26 District Units

Traffic Organisation DivisionTraffic Organisation Planning

DepartmentTraffic Organisation

Supervision Department

Production Division

Tender and Contract Department

Work Supervision DepartmentProject Implementation Unit

Technical DivisionStrategy Department

Road Network DepartmentPavement Preservation

Management DepartmentBridge Department

Director General

Administrative Department

Public Relations andMarketingDepartment

Communications and Computers Department

AccountingState Road Fund Department

Personnel DepartmentLegal Department

Office of Director General

Quality Manager

Road Museum

LRA’s Tasks and Responsibilities

• Administration of the State Road Fund;• Management of the state road network;• Organisation of public procurement;• Management of state road reconstruction and construction programmes / projects;• Supervision of road maintenance, repairs and construction in the state road network.

S u p e rv is io n o f th e M in is t ry o f T ra n s p o r t o v e r th e L R A

S ta te p ro x ie s ( s to c kh o ld e r ’s m e e t in g ) 5 -y e a r c o n t ra c t

M in is t ry o f T ra n s p o r t

L a tv ia n R o a d A d m in is t ra t io n

R o a d T ra n s p o r t D e p a r tm e n t

Seminar on Restructuring Road Management – Trend or Necessity?

24

Benefits Gained after the Reorganisation in 1997

• LRA’s status allows to implement free market oriented principles and apply practices of privatecompanies;

• Salaries are competitive;• Stabile personnel of engineers;• LRA decides on issues of staff motivation, purchases and development;• Stability of the staff ensures the improvement of quality;• LRA finances the development of its own management systems and IT;• LRA pursues the certification of its Quality Management System according to ISO 9001

Benefits to the employees

• Additional payments and allowances:- additional motivation payments,- vacation allowance,- maternity and retirement allowances, etc.

• Education and training:- paid professional education- full or partial payment of study fees

• Health:- health insurance,- life insurance.

Conclusion: Future Perspectives

• Current tasks:- improvement of contract with the MoT,- work with the politicians,- development of the personnel.

• New Parliament elections on October 5, 2002:- new political decisions concerning the LRA?- new changes in the status and function of the LRA?

Seminar on Restructuring Road Management – Trend or Necessity?

25

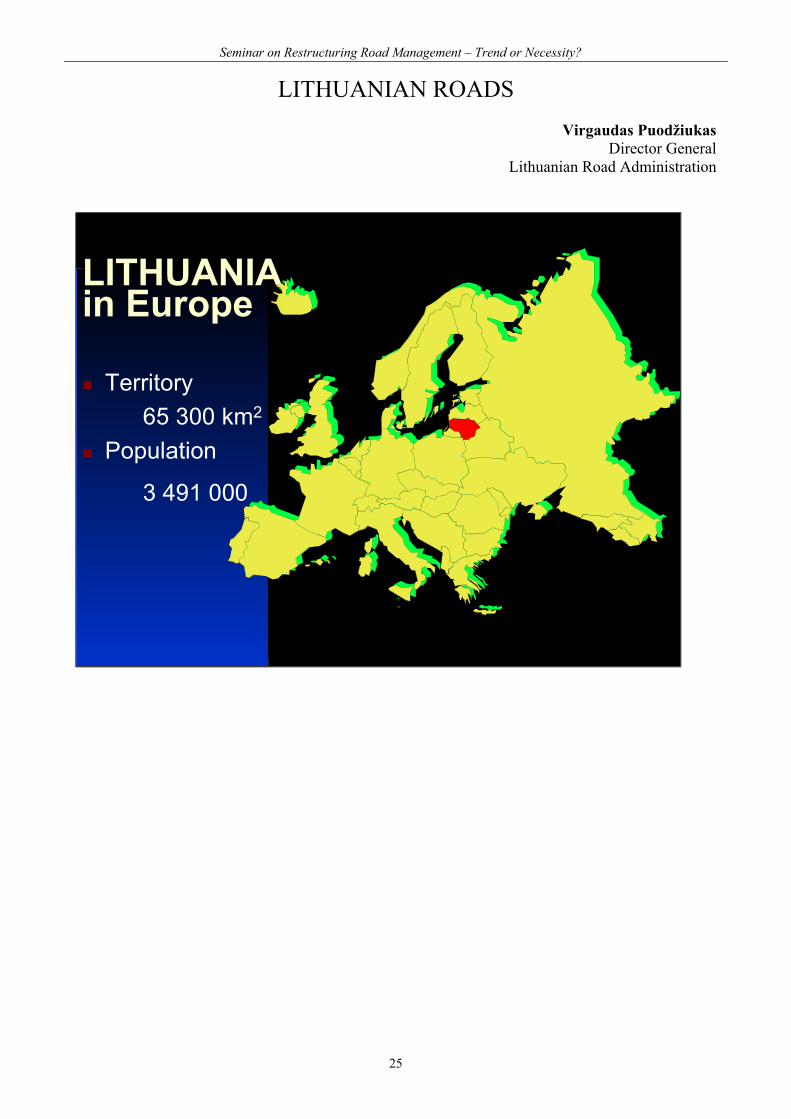

LITHUANIAN ROADSVirgaudas Puodžiukas

Director GeneralLithuanian Road Administration

LITHUANIAin Europe

Territory65 300 km2

Population

3 491 000

Seminar on Restructuring Road Management – Trend or Necessity?

26

General road network information

Main roads1724,3 kmNational roads4864,0 kmRegional roads14724,3 km

State roads

Total state roadslength 21312,6 km

Road Network Density: 6,1 km per 1000 inhabitants 328 km per 1000 km2

TEN corridorsLithuania is crossed by

two Trans EuropeanNetwork (TEN)corridors:

In the North-Southdirection, Corridor I(highway VIABALTICA and railline RAIL BALTICA),linking Tallinn - Riga- Kaunas - Warsaw,and its branchCorridor I A (Tallinn- Riga - Siauliai -Kaliningrad)

In the East-Westdirection, CorridorIX, branches IX B(linking Kiev - Minsk- Vilnius - Klaipeda)and IX D (Kaunas -Kaliningrad)

Seminar on Restructuring Road Management – Trend or Necessity?

27

E-category roadsE67 VIA BALTICAHelsinki - Tallin –Riga – Kaunas –Varsaw – Praha;E28 Berlin – Gdansk- Kaliningrad -Vilnius – Minsk;E77 Pskov - Riga -Siauliai - Kaliningrad- Varsaw –Budapest;E85 Klaipeda -Kaunas - Vilnius -Lyda - Bukarest –Aleksandropoli;E262 Kaunas -Daugavpils -Rezekne - Ostrav;E272 Vilnius -Panevezys - Siauliai- Palanga - Klaipeda.

Total length of E-category roads is 1490 km

56,6 % of state roads are paved.Of which: Asphalt – concrete 24 % Light asphalt 75 % Cement – concrete 1 %43,3 of regional roads has gravel pavementThe prevailing width of asphalt pavements is 6-7metresAll main and national roads are cement or asphaltpaved20 % of asphalt pavements are wider than 7 metres521 km of roads have four lanes

Seminar on Restructuring Road Management – Trend or Necessity?

28

The number of vehicles per 1000 inhabitants in 1990-2001

217 227 235 246 257236 240

277

312326

348 397

0

50

100

150

200

250

300

350

400

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Dynamic of Traffic Volumes in 1990-2001, %

100

119

8881

104 106121 130 139 139 134 140

0

20

40

60

80

100

120

140

%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Seminar on Restructuring Road Management – Trend or Necessity?

29

Dynamic in financing of Lithuanian roads, in 1996 – 2002, million LTL

294

445

428

600

451

100

24

423

149

0

334

127

3

404

42

66

495

88

0

100

200

300

400

500

600

1996 1997 1998 1999 2000 2001 2002

Local budget Loans Grants

Seminar on Restructuring Road Management – Trend or Necessity?

30

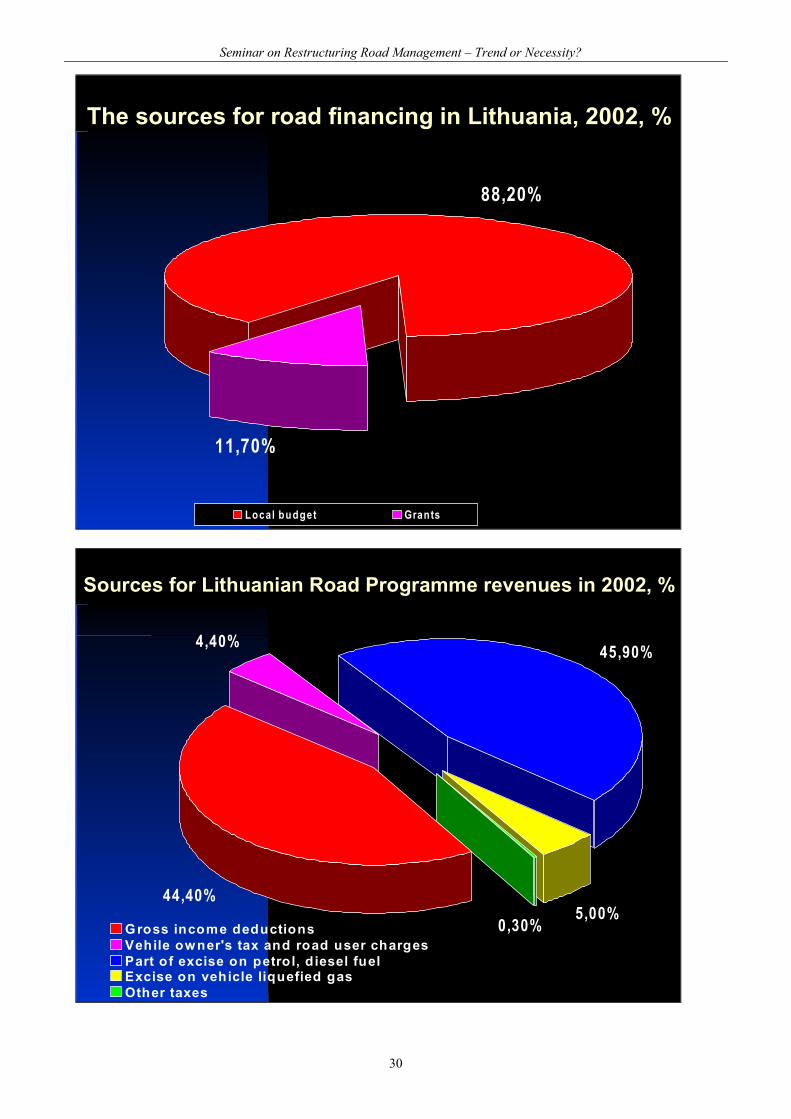

The sources for road financing in Lithuania, 2002, %

88,20%

11,70%

Local budget Grants

Sources for Lithuanian Road Programme revenues in 2002, %

44,40%

4,40% 45,90%

5,00%0,30%Gross income deductions

Vehile owner's tax and road user chargesPart of excise on petrol, diesel fuelExcise on vehicle liquefied gas Other taxes

Seminar on Restructuring Road Management – Trend or Necessity?

31

The structure of Road expenditure , %

28%

43%

25%

4%

Road maintenanceRoad con stru ctio n, reco nstructio n, rep air, bridg e repairLo cal ro adsOther exp end itures

STRUCTURE OF THE ROAD MAINTENANCE EXPENDITURES

22%

42%

3%

12%

7%

4%4% 5% 1% S umm er routine

ma inte na nce

W inte r routinema inte na nce

Bridge ma intenance

P avem ent m aintenance

Repairing grave l roads

Repairing roadbed

Roa d ma rking

S igns, cra sh ba rrie rs

Repairing roadside ,buildings

Seminar on Restructuring Road Management – Trend or Necessity?

32

Structure of Road Sector

The Ministry of Transport (MoT)

Lithuanian Road Administration (LRA)

10 Regional State Enterprises1 Motorway State Enterprise

Central Quality Control Laboratory

Transport and Road Research Institute

Operating Management of the Roads

Lithuanian Road Administration (LRA)

Transport and RoadResearch InstituteCentral Quality

Control LaboratoryPrivate Companies

11 State Enterprises Private Companies

Private Companies

Research anddesign

Roadmaintenance

Road constructionand repair

70 % 30 %TOTAL

100 %50 % 50 % 20 %80 %

Private Companies

State Enterprises

Seminar on Restructuring Road Management – Trend or Necessity?

33

Structure of road assetmanagementMOT:

Asset’s owner;-Management – general.LRA:

No asset ownership;-Management:

General planning;Contracting;Financing;Control.

State enterprises:Delegated asset ownership.

-Management:Detail planning, Road inventory;Asset accounting.

-Execution of maintenance works

Structure of Financing RoadMaintenance in 2002

Routine main tenanc e in

s ummer 22%

Main tenanc e o f the embankment

and c u lv e r ts 4%

Main tenanc e o f b r idges and

p ipe lines 2%

Main tenanc e o f as pha lt

pav ements12%

Res tora tion o f g rav e l pav ement

w ear7%

Res tora tion o f road s igns and

barr ie rs , e tc .4%

Res tora tion o f road marking

4%

Routine main tenanc e in

w in te r42%

Daily ins pec tion and repa ir o f

minor damages3%

Unit price contracts (according to bill of quantities)

33%

Lump sum contracts (According to standard)

67%

Seminar on Restructuring Road Management – Trend or Necessity?

34

Management of Fund Allocated onRoad Maintenance

Data baseTraffic volumes

LoadsAccident rates

Road lengthVolumes of construction work

Road condition

Optimal levels (standards) of road maintenance(Minimum combined costs)

Realistic funding

Realistic levels (standards) of road maintenance

Contract awardAssignment of tasks, funds and level of maintenance

Contract implementationSupervision of works Supervision of the road maintenance

level (standard) implementation

Optimal scope of funding Governmental policyWillingness of society to pay

The System of DocumentsRegulating the Road Maintenance

Classification of worksA list of compulsory works

Standard (level) ofmaintenance

Maintenance technologies

Economic rates

Guidelines of technicalsupervision and take over

Methodology ofmaintenance level

assessment

Package of rates on thenumber of working hours,equipment, and materials

Planning

Production

SupervisionAcceptance

3

1

1

2

2 5

2

3

2

5

4

6

4

5

6

7

6

7

Seminar on Restructuring Road Management – Trend or Necessity?

35

ConclusionsAdvantages: limited number of capable enterprises reduced amount of state employees contracting out of works lump sum contracts (achieved level of maintenance) independent supervision of works

Shortcomings: incomplet separation of Client and Contractor function lack of legislation regulating lump sum contracts insufficiently developed data bank

Today’s priorities and perspectivesEnsurance of proper routine maintenance level and traffic

safety.Modernisation of European Corridors

VIA BALTICA ( Marijampolė bypass)Implementation year 2000 – 2005.Project cost – 16,5 million EUR,of which 6,5 million EUR by EU PHARE,10,0 million EUR – Lithuanian funds.

Lithuanian Highway ProjectImplementation year 2001 – 2004.Project cost – 115,55 million EUR.Financed by EU ISPA program – 65,55 million EURand Lithuanian funds – 50 million EUR.

Preservation and modernisation of the existing road network

Seminar on Restructuring Road Management – Trend or Necessity?

36

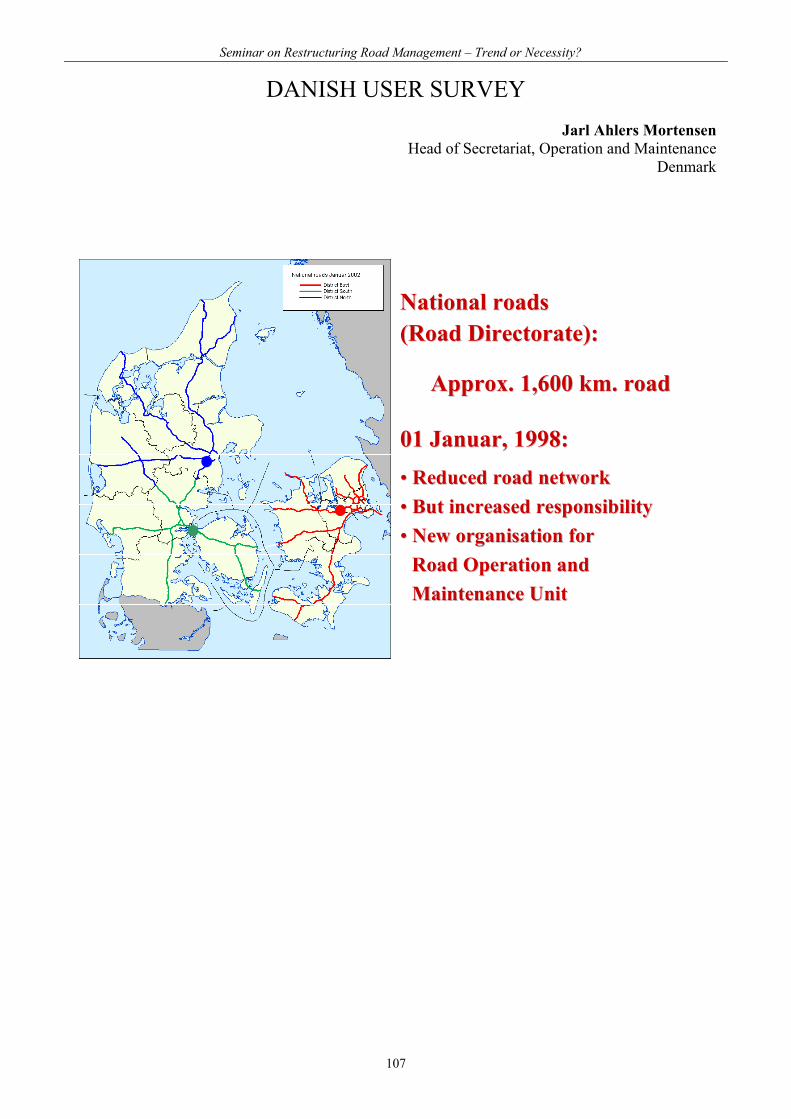

ROAD ADMINISTRATION REFORMS IN DENMARKHenning Cristiansen

Director GeneralDanish Road Administration

1. IntroductionAs you know, I am General Director of the Danish Road Directorate and chairman of Nordic RoadAssociation in the term from the middle of 2000 to the middle of 2004.

First of all, I want to thank you for having taken the initiative to this seminar entitled”Restructuring Road Management – Trends or Necessity?”. I imagine this initiative was taken byBRA as a result of the fact that the Baltic road administrations are moving into a process of changeon the organizational level – in particular at the present time. But so are a great number of theNordic road administrations too – as you will experience during this seminar.

The programme of the seminar has been prepared by NRA's Technical Committee 13, RoadSector Organization and Management, and its BRA counterparts in the Administration Committee.

2. State-of-the-ArtAt first, I want to outline the present situation as to road management and performance in Denmark.As you can see from this slide, the Danish road network had a total length of 71,900 kilometres atthe beginning of 2002. According to the Road Act of 1971, the administrative and economicresponsibility for the road network is shared by three levels of road authorities.

At the first level of the organization of the Danish road sector we find the Dansih Parliament (theFolketing) and the Minister of Transport taking the political decisions for the national road network.At the next level we have 14 county councils which are responsible for the regional roads, andfinally we have 275 local councils and municipalities having the responsibility for the local roads.

The administration of each road network is carried out by its own administrative body; therefore,the Danish Road Directorate administrates the national roads, the 14 technical departments in thecounties administrate their respective road networks etc. Consequently, each one of these has theeconomic and technical responsibility for its own road network.

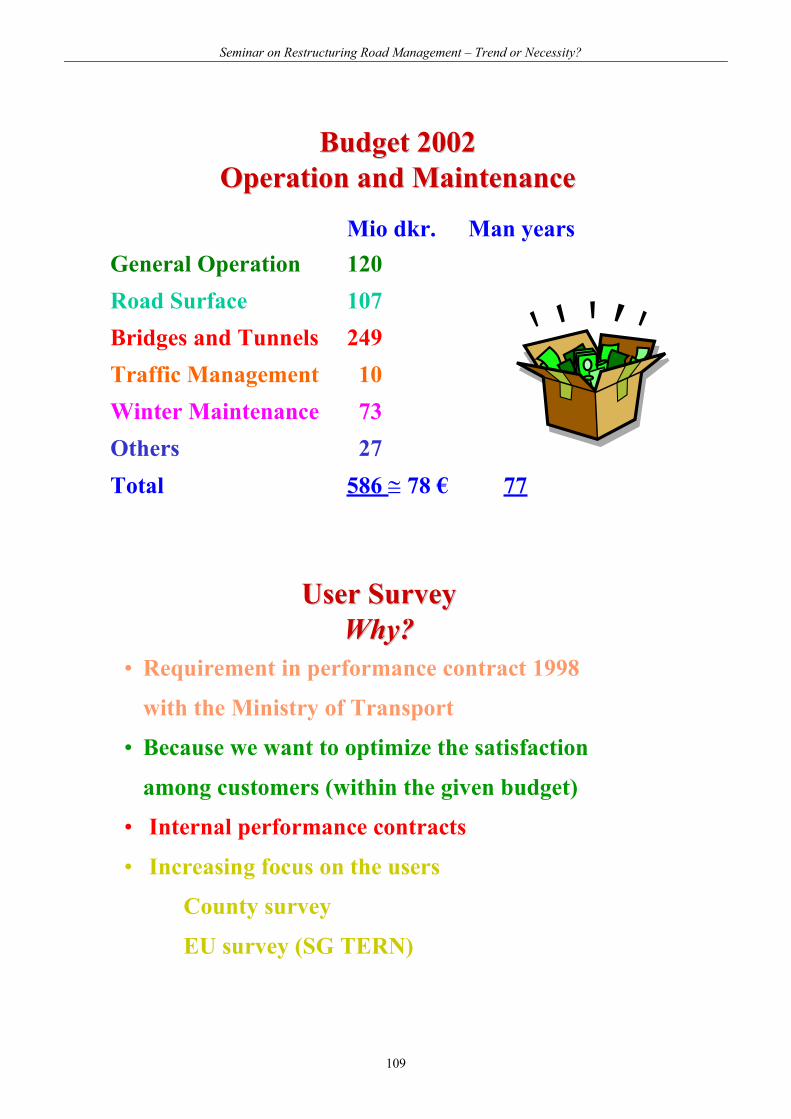

1,660 kilometres of the Dansih roads are national roads for which the Road Directorate isresponsible (excepted from this are the Great Belt and Øresund bridge and tunnel constructions forwhich the Sund and Belt Limited is responsible). 980 km of these roads are motorways – and thisfigure will surpass 1,000 kilometres before the end of 2002 as we are opening two more motorwaysections this autumn. Although the national roads represent only 2 per cent of the total length ofroads in Denmark, we have 27 per cent of the road traffic use on these national roads. In 2002, thebudget for the national roads is 2.1 billion Danish crones, equivalent to 280 million Euro, andcorresponding to one fifth of the total budget.

The 10,000 kilometres of regional roads are administrated by the 14 county councils. The shareof traffic on the regional roads amounts to 32 per cent of the total traffic.

On this slide you see the 71,900 kilometres of public roads all together. The local roads, i.e. [thatis] minor roads and streets, covering 60,240 kilometres, are administrated by the 275 municipalitiesand town councils.

The Danish Ministry of Transport consists of two departments. In addition to this, the Ministryhas an administration department dealing with finance, budgets, accounts, personnel, etc., and aplanning department which is responsible for general transport policies, transverse planning issues,research and development issues, physical planning, statistics and forecasts for the transport sectorand issues pertaining to environment, energy etc.

The Ministry's first department deals mainly with road transport, including legislationconcerning roads, road traffic, road safety and road environmental issues. This department is alsoresponsible for harbours, coast protection and territorial waters. Furthermore, its tasks include

Seminar on Restructuring Road Management – Trend or Necessity?

37

matters regarding aviation and airports, as well as the operation of the meteorological services. Inaddition to this, the department is responsible for matters pertaining the large bridge and tunnelconstructions across the Great Belt and Øresund (The Sound) and matters concerning questions oninternational infrastructure (especially as regards the relations to the EU).

The Ministry of Transport also contains a number of public directorates, agencies, companiesetc. These directorates, agencies and companies work within defined areas and are the operationalunits within their respective fields.

As already mentioned, the Danish Road Directorate has the administrative and economicresponsibility for the national roads. In this matter, it functions exclusively as an orderer since allactivities are put up for tender. Therefore, the Road Directorate has no activities in the field, and allactual activities are performed by private companies (consultants, contractors and suppliers). TheRoad Directorate has never had a field organization for construction, operations and maintenanceworks.

From 1972 to 1998, an agreement existed between the state and the counties as well as withsome major municipalities. Under this agreement, the counties – in addition to their own roads –were responsible for the routine operation and maintenance of the national road network consistingin these years of about 4,600 kilometres of national roads. However, the Road Directorate still hadthe responsibility for the major bridges and tunnels. As for operation and maintenance during theseyears, the Road Directorate was responsible for the general technical and economic management.

This arrangement ceased on 1 January 1998 when a new Road Act, passed by the DanishParliament (the Folketing), came into force.

According to this, the total length of the national roads (or State roads) was reduced toapproximately 1,625 kilometres. These national roads are carrying the major part of the heavytraffic and they consist of almost 1,000 kilometres of motorways.

In its capacity as a road manager, the Danish Road Directorate has always to a large extend hadthe function of an ordering organization. Unlike the other Nordic countries, Denmark has never hada national road service carrying out practical activities in the field. Instead, we have had acomparatively small construction and entrepreneur organization ordering and controlling thevarious tasks, which have been carried out under private management.

Today, the Danish Road Directorate has a status as what you may call a '90/10 establishment',meaning that just under 10% of the total budget of the Road Directorate is spent on wages andmanagement, whereas the remaining 90% of the resources are spent on advisers, contractors andsuppliers.

Throughout the years, the Road Directorate has always been a comparatively smallestablishment. The maximum number of employees has amounted to a little more than 700 personsin 1995. But following 1998, when about 3,000 kilometres of roads passed to countyadministration, we also had to reduce the number of employees to about 540 persons. With theRoad Act of 1998 the Road Directorate also had to take upon more raod sector tasks.

This year, the Road Directorate has gone through a process of organizational adaptation and, as aresult of this, the number of employees will be reduced from 540 persons at the beginning of 2001to about 440 persons by the end of 2002 - a reduction of almost 20 per cent. This reduction in theproductive capacity of the Road Directorate has been effected through natural wastage, voluntaryredundancy and dismissals. We only continue a small proportion of the tasks we have performed upto now, and we do this through invitation to submit tenders.

A trend in the public sector is that the Government wants to change the employees from beingcold hands to warm hands: that means that the number of employees in jobs like roadadministration and management, etc. has to be reduced and jobs and employees in the social sector,health services, elderly care, etc are given higher priority. We experience this trend in the WesternEuropean countries especially.

The question was then: how to tackle this severe reduction in employees? First we had to decidewhat our core activities or tasks should be in the future and what could be excluded from the taskswe had up till now.

Seminar on Restructuring Road Management – Trend or Necessity?

38

This process which was carried out within only half a year, resulted in the three core activities ofthe Road Directorate. They are as follows:

(1) First of all the responsibility for traffic handling on the 1,625 kilometres of national roads,including the responsibility for maintaining the good condition of the road network with emphasison road safety, road passability, and preservation of the road capital.

(2) The next of the core activities concerns extension as well as improvement of the nationalroad network in accordance with political demands as they appear in investment programmes andlaws concerning planning and construction.

In fact, the vast majority of the tasks managed by the Road Directorate – and consequently thecorresponding economic resources – are placed in these two core activities, and they stay thestarting point of the Road Directorate activities as a whole as well as they precondition and form thebasis of our other tasks aiming at the entire Danish road network whether those relate to the roadtechnical departments in municipalities and counties or to the Ministry of Transport.

(3) The third core activity consists in solving a vast number of tasks for the entire road sector inorder to keep on ensuring an overall coherence in the development of the Danish infrastructure.

The handling of this task is mainly based on data – about roads, about traffic, about accidents,about environment and so on – on regulations and standards of roads, on knowledge of trafficeconomy as well as of material technology. By gathering this knowledge concerning the roadsector, it is possible to apply it on the overall planning and development of traffic in Denmark.

In parallel to the establishment of a digital administration – which has been given first priority bythe former as well as the present government in Denmark – factors like the orientation of the RoadDirectorate towards the internet and the participation in web portals with other actors within theroad and transport sectors get still more important.

On the basis of the strategy for the core activities, the Road Directorate has chosen the followingorganization:

The Road Construction Unit ensures a continued improvement and extension of the nationalroad network. The tasks of this unit begin with the actual planning and end with the opening of thecompleted construction. In this way they include designing, acquisition of area and tasks concerningsurveying as well call for tenders, management of contracting and supervision.

The Road Operations and Maintenance Unit has the overall responsibility for the safe andeffective handling of traffic on the 1,625 kilometres of national roads. This unit has to ensure arational operation of the national road network, among other things by means of call for tenders andmanagement of contracts concerning maintenance, winter services, renovation of road surfaces,bridges and tunnels, equipment and so on. Furthermore, this unit manages services for road users,controlling of traffic, traffic technique and road safety, so that the management of road operationand the handling of traffic are co-ordinated under a joint management responsibility.

The Road and Road Traffic Unit will be charged with the task of supporting the Constructionand Maintenance Unit by means of strategies for road planning as well as a continuous developmentof relevant road regulations. The tasks of this unit will also be aimed at the Ministry of Transportand the Danish Parliament (the Folketing) bearing the responsibility for the overall strategicplanning of the national road network as well as the overall planning activities concerning the entireroad sector with a view to implementing the objectives of transport policies. Furthermore, this unitmust take care of the contact potential as to co-operation with the road committees in municipalitiesand counties, with a view to ensuring the necessary overview of the road network transversely tothe administrative levels.

The Informatics Unit: As the Road and Road Traffic Unit, the Informatics Unit will also haveto contribute to the preservation and the further development of a joint basis for the roadcommittees transversely to administrative levels. This unit has a function as a knowledge and datacentre to all road committees providing information about roads, bridges and traffic. Furthermore,this unit will go on giving technical and system related support to the rest of the Road Directorate asregards information technology.

Seminar on Restructuring Road Management – Trend or Necessity?

39

The Danish Road Institute is the road engineering knowledge centre of the Road Directorateand the road committees as a whole.

The Market Unit: The competences of the former Commercial Unit and the Export Unit areunited in a Market Unit which will be responsible for the action plan and the business volume of thecommercial activities as a whole.

3. The future – the new challengesThis is what our organization looks like in September 2002. The question is what the future has instore?

Many people would probably like to know the exact answer to that question, but that is not howreality works: Neither to smaller or larger private enterprises having thousands of employees, nor tostate agencies as our own having four to five hundred employees.

Being subject to this reality changing faster than ever, it is – from my point of view – above allour ability to constantly intercepting changes in signals and adapting to alterations in demandswhich will determine the future of the Road Directorate as an establishment – rather than the abilityand the will to depict some future state about which the most positive thing you can say is that it isprobably never going to be precisely as pictured. Simply because the preconditions of thisconception of the future keep changing.

I shall give you a specific example: The strategic decision of the Road Directorate concerningthe motorway section from Riis to Ølholm to try out the procedure of a turnkey contract [totalentre-prise] which had been in demand from various quarters as an alternative to our traditional call fortenders. A number of preconditions – among other things a wish from the contractor sector to behave the possibility to tender – turned out not to be real. Two of the large contracting firms, forinstance, have recently backed out. Decisions made outside the Road Directorate, maybe evenabroad, have an impact on our strategies for tender and on our possibility to carry through theassignments for which we are responsible.

As a consequence of these factors, the ability to change and a rather flexible organizationalstructure are of far greater importance than being able to depict a future which is after all impossibleto picture. We must be able to change quickly and constantly according to new demands andexpectation from our clients, e.g. [that is] the Ministry of Transport as well as the road users, thecitizens and our business clients. This calls for internal co-operation, preferably supported by a highdegree of project organization. But above all it demands a certain attitude among employees as wellas leaders. In order to emphasize this point, I shall put it in rather direct terms: According to ourmarket experience, both demand and business volume may change considerably in only a shorttime.

Once upon a time an organizational change was comparatively long-life and would maybe lastfor five to ten years. This is no longer the case. Nowadays, we have a fast-moving development –and projects concerning a new organization between municipalities, counties and the state compelthe Danish Road Directorate to be ready to accomplish as well a smaller as a larger number of tasksin the future.

The present structure in the public sector has existed since 1970. At that time, the number ofcounties and municipalities was reduced substantially. And ever since there has been an ongoingdiscussion about this structure, but there has been no agreement as to do something about it. Themain task of the counties is the operation of the hospital services. For many years, the counties havebeen criticized for failing to fulfil this task satisfactorily – among other things there have been longwaiting lists for various kinds of treatment.

In the light of this state of affairs, the Danish Parliament (the Folketing) decided to conduct aninquiry into the public service given by the state, the 14 counties and the 275 municipalities in orderto find out if this service could be more effective if the tasks were divided among the publicadministrations in a different way – or by changing the size and the number of counties andmunicipalities. The result of this inquiry is expected within a couple of years, in order that amodified structure can take effect as from the next county and municipal elections due in 2005.

Seminar on Restructuring Road Management – Trend or Necessity?

40

Of course, it is impossible to know exactly how this new structure will be. However, it seemsprobable that the counties will be abolished and three regional hospital services will be establishedinstead. The remainder county tasks will be transferred to the state and the roughly 100municipalities, which will probably be left.

Above, I have pointed out the changes we have seen in the organization and mode of operationwithin the Road Directorate. But there have also been drastic changes in several other agencies anddirectorates within the Ministry of Transport.

The predominant tendency has been a conversion into companies and/or a privatization of theseformer agencies. Furthermore, several of these have been split up into a number of companies orsmaller units operating independently.

For the time being, the Ministry of Transport is sole proprietor of these companies, but some ofthe split-up companies have been sold by the Ministry. Subsequently, these newly foundedcompanies function and act as private companies. Along with this split-up into smaller units, areduction on the economic level as well as in the number of employees is carried out.

As an example, I shall now mention the Danish State Railways, which formerly included allfields from construction, operation and maintenance of the railways and purchase of trains to theactual traffic on the rails. Furthermore, the Danish State Railways managed a number of bus andferry services. As a result of a split-up, the former Danish State Railways was divided into [1] a newDanish State Railways managing the traffic on the rails, [2] the Danish National Railways Agencyresponsible for the operation and maintenance of the railways, [3] Scandlines managing the ferryservices, and [4] Combus managing the bus services. The new Danish State Railways in itself wasfurther divided into a number of partly independent units: Passenger traffic on the national level,Urban railway traffic in Copenhagen and the suburbs, and Goods Traffic. The Goods Traffic unithas later been sold off and is therefore no longer a part of the Danish State Railways. Scandlinesmerged into a German shipping company and Combus was sold to a private bus company. At a laterstage, a part of the Danish National Railways Agency - the consultant department - was sold to aprivate international consultancy company.

In addition to this, the State has started to put up the railway traffic for tender, in order that otherrailway companies than the Danish State Railways may tender. Following this, 15% of the railwaytraffic was put up for tender last year, and the private English company, Arriva, won the contract.

I could mention other agencies and directorates having been converted into limited companies:among others Post Denmark and Copenhagen Airports. For the moment, the state is the soleshareholder, but the possibility of selling half the shares to private persons is considered.

Another example of this conversion into a state company, is the building of the large bridge andtunnel constructions, Great Belt and Øresund.

Here we saw the establishment of a state limited company – as for Øresund together with theSwedish state – functioning as building owner while the construction was going on. Only a rathersmall organization was established inasmuch as it was solely in charge of the overall managementof the projects, while tasks like planning, construction, supervision and control were put up fortender, i.e. bought outside the organization. At present, the Sund & Belt Limited is responsible forthe traffic management of the two bridge and tunnel constructions, whereas the operation andmaintenance as such has been put up for tender.

Within the Ministry of Transport, only the Danish Meteorological Institute and Denmark's RoadSafety and Transport Agency have the same structure and functions as earlier.

These years show us new ways of co-operation between public establishments and privatecompanies. We see this in the changing of public agencies and directorates into companies as I havejust explained. In these cases, public establishments are increasingly operating and functioning asprivate enterprises having among other things the possibility to tender on equal terms. They havebecome companies being able to and having to compete with other companies. They must make aprofit if they want to survive.

We also see a higher degree of Public-Private-Partnership in connection with public tasks, andthese may appear in various forms. This also concerns other ways of financing new road

Seminar on Restructuring Road Management – Trend or Necessity?

41

constructions and models like BOT, PPP and the like gain ground. This involves a new division oftasks between public authorities, agencies and private enterprises.

I would like to draw your attention to the PIARC Report ”Restructuring of the Road Sector” -published in 2000. This report gives a very good overview of the present situation as regards roadadministrations in the World and the trends we experience. These trends of development seems tobe very much alike between the different countries - dependent of course from which stage ofdevelopment they have start. I've listed some of the tendencies stated in the report:• Private financing of infrastructure where we experience a greater involvement of the private

sector• Problems of maintenance and how to finance it• Importance of road transport in Europe is growing - road transport's position in relation to the

other modes of transport is still growing• Increasing interest in transport system quality (congestion, environmental impact)• A stronger regional and local influence on decisions concerning the development and use of

transport systems• An increasing and direct dialogue with the road users, with the neighbouring roads and with

other transport modes• A stronger focus on results, i.e. [that is] value for money for taxpayers• New technologies, such as ITS, creating new possibilities for efficient use of the transport

system• An increased internationalization of standards for roads, equipment, vehicles, etc.

We also see a tendency towards a diminishing of the role of pure and simple sector ministries andsector authorities – and in any case their role has somewhat altered compared to previously. TheMinistry of Agriculture for instance has changed into the Ministry of Food, Agriculture andFisheries. The Road Directorate will have to relate to these new roles and structures.

If an organization is to be ready for change, this demands a readiness to change from theemployees. In the light of this, the Road Directorate is aiming specifically at developing thecompetences of the employees – and in this connection project work and sharing of knowledge arethe keywords.

This means that all university-trained employees working in projects are offered a projectmanaging course – in order that the employees use identical 'tools' in their work. Furthermore, wehave worked out a manual for project managers as a guiding principle for project work in generalwithin the Road Directorate.

We experience that co-operation across the country borders is becoming still more significant. Inthis world of specialization it is getting still more difficult to find other persons within theindividual countries sharing your specific problems. More and more often, you find your colleagueswithin the road sector or the road authorities in another country. For us Danish this appliesparticularly to the other Nordic countries, but also to the Baltic countries as well as the othercountries in Europe and the rest of the world. Sharing of knowledge is really becoming aninternational affair. To Danish road and traffic people, this is primarily realized through NordicRoad Association, Baltic Road Association and finally World Road Association (PIARC). It iswithin these organizations we shall find our colleagues in future.