renew nsrp executive housing market · renew nsrp executive housing market september 2010 prepared...

TRANSCRIPT

RENEW NSRP Executive Housing Market September 2010 Prepared for Joanne Tyzzer, Darren Jones, Brian Davies North Staffordshire Regeneration Partnership Renew North Staffordshire Stoke City Council email: [email protected]

Arc4 contact David Cumberland / Ross Tolmie-Thomson Arc4 Ltd Beehive Mill Jersey Street Ancoats Manchester M4 6JG Tel +44 (0) 161 228 1689 email [email protected] [email protected]

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 2 of 80

arc4 Beehive Mill Jersey Street Ancoats Manchester M4 6JG T: 0161 228 1689 F: 0161 228 6514 Email: [email protected] Website: www.arc4.co.uk Contents

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 3 of 80

Section 1.0 Report Overview 4 Introduction 4 Section 2.0 Methodology 7 Current Executive Housing Market

Future Executive Housing Market Research Framework

8 9 9

Section 3.0 Executive Housing Market Definition 12 Section 4.0 Executive Housing Market Assessment 14 Current Executive Housing Market

Current high-end property market context Wider Housing Reference Area

14 17 22

Section 5.0 Strategic Policy context for housing delivery 25 Section 6.0 Demand for Executive Housing 31 Household income and ACORN profiles

Demographic and population projections Changes in employment and incomes

31 33 37

Section 7.0 Primary Fieldwork 38 Estate agent testimonies

Focus group attitudes and aspirations Developer perceptions

38 43 45

Section 8.0 Current supply of new build executive housing 48 Section 9.0 Developing an executive housing market 50 Section 10.0 Conclusions

Including recommendations 56 63

Appendices 65

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 4 of 80

Section 1 Report overview 1.1 Introduction 1.1.1 Arc4 Ltd. has been commissioned by RENEW and NSRP to undertake an assessment of the

Executive Housing Market (EHM) in the North Staffordshire regeneration Partnership (NSRP) area, including the local authorities of Stoke, Newcastle-under-Lyme and Staffordshire Moorlands. The assessment framework is split into two distinctive areas: a review of the current EHM in terms of housing supply and demand profiles, then secondly an assessment of the future EHM in terms of market demand and developer potential. Stakeholder and consumer consultation has been an important component of this research, which ensures a wide range of views and expertise is captured in the research.

1.1.2 Under the aegis of the NSRP Business Plan, there is a priority within the housing and

regeneration frameworks to diversify the stock profile. Limited supply of high value executive housing assets (properties in the higher Council Tax bands G and H) is weakening the housing offer. Testing the housing markets appetite for increasing the supply of properties in tax bands E to H will feature heavily in the assessment process.

1.1.3 In summary this research

• Provides a definition of an executive housing market and the attributes of an exclusive housing product

• Explores the size and profiles of the current executive housing market in North Staffordshire

• Provides material on future executive housing aspirations based on market testing of the demand group and housing agents

• Reviews the potential for future executive housing delivery across the district based on developer and local planning authority perspectives.

1.1.4 There is a requirement to produce an evidence-based, focussed review of opportunities and identify issues pertaining to the suitability of developing executive housing on land both owned and identified with potential for this supply type.

1.1.5 The adopted Newcastle-under-Lyme and Stoke-on-Trent Core Spatial Strategy outlines that

in order to achieve the strategic aims both regionally and sub-regionally, substantial restructuring of the employment and residential offer in North Staffordshire is required. Although the Regional Spatial Strategy has been abolished, Stoke City Council are still working to the same housing growth numbers as before, since they have been included within the Core Strategy and were arrived at through thorough research of the evidence base.

1.1.6 The latest available indicators suggest that the existing provision for the executive market is

limited in North Staffordshire, specifically so within the city of Stoke-on-Trent. As outlined by the RENEW North Staffordshire Regeneration Partnership Business Plan 2008 – 2011, the sub region has a constrained supply of high-end market housing and the imbalance of housing supply is closely allied to the socio-economic profile and under performance of the area in retaining and attracting economically independent households.

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 5 of 80

1.1.7 The latest Strategic Housing Market Assessment identified Stoke-on-Trent as a unique market in continuing to suffer population loss, in particular to neighbouring authorities Newcastle-under-Lyme and Staffordshire Moorlands (SHMA 2008). A contributory factor is the limited residential offer across the spectrum of the housing market, one of the main SHMA recommendations identifying the requirement for ‘more executive housing in the housing sectors shown to be disproportionately dominated by terraced dwellings’.

1.1.8 One of the principal objectives of the RENEW North Staffordshire Regeneration Partnership

Business Plan 2008 – 2011 in recognising the limited housing choice, is to provide a diversified residential offer. Providing the right type of dwellings, in the right location and environment will be key to addressing and reversing the trend of net population loss. An important factor for competitiveness in the knowledge economy is the extent to which places have a skilled, creative and entrepreneurial workforce. Employers will choose to locate partly on the basis of where this workforce is located and therefore the residential offer must be closely aligned with the aspirations of economically independent households.

1.1.9 We note that ‘top end of the market’ executive housing can also have a further significant

impact on the economy. The evidence suggests that residents of executive housing include a high proportion of entrepreneurs, with a consequent high level of business start-ups. This leads to establishment of new employment opportunities, often in locations convenient to the home of the entrepreneur.

1.1.10 One of the NSRP Business Plan priorities, in providing a portfolio of high quality/specification

detached houses or luxury apartments, seeks to meet the aspirations of existing and future residents on higher incomes, both in the interests of greater social inclusivity and to remove a barrier to the pursuit of economic prosperity. A broader housing choice is essential to accommodate the changing aspirations of the resident population and to retain graduates and attract new economically active households into the area.

1.1.11 Current housing supply throughout areas of Stoke-on-Trent, Newcastle-under-Lyme and

Staffordshire Moorlands, reflect an earlier pattern of economic structure and development that does not meet the current, nor future needs, for a balance of dwellings types and choice and the need to develop mixed communities.

1.1.12 Much of the offer within the constituent authorities competes for skilled workforce and

economically independent households with a limited residential offer. Issues of deprivation, worklessness and social exclusion are inextricably linked with poor quality housing and less desirable environments. Therefore, an improved residential offer and quality of place is essential to the creation of mixed and balanced communities and fundamental to improving the economic performance of the area (RENEW NSPR BP).

1.1.13 Creating sustainable, mixed communities coupled with high design quality and place making

is a key part of the Government’s approach to housing and planning policy going forward. Providing a quality residential offer is not about ‘gentrification’ alone, but about creating quality places through new development and interventions in existing neighbourhoods to provide a range of house types and tenures. It is the aim of RENEW and the NSRP that opportunities are identified to address the need for provision of a broader mix of housing supply across the intervention areas in the sub region.

1.1.14 This research provides an intelligence report examining the issues around the provision of

executive housing and developing a meaningful definition framed within a North Staffordshire context. The report provides an examination of both the local and regional housing market (in

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 6 of 80

terms of depth of the potential market) and the planning supply context for the provision of executive housing. The report focuses in particular at recent experience of developing executive housing framed in the context of the local potential market demand, competing sites, migration, travel to work patterns, sales performance and land/site supply.

1.1.15 Our perspective is holistic. We do not see development and the supply of housing in

isolation. As such, we have examined the objectives of recent spatial planning policy at both the (now abolished) Regional Spatial Strategy and emerging Local Development Framework levels. This research paper looks to test the potential demand and requirement for larger executive developments within North Staffordshire.

1.1.16 Much has changed in the national and regional arenas since this report was commissioned, including the election of the Coalition Government and its abolition of whole swathes of regional governance including the Regional Development Agencies, Regional Assemblies and planned regional Leaders’ Boards, together with Regional Spatial Strategies. Further clarity around the new Local Economic Partnerships and the extent of their remit is awaited.

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 7 of 80

Section 2 Methodology 2.1 Methodology 2.1.1 The research methodology has been mainly desk-based, with primary input from discussions

with the client on previous work and telephone interviews with local agents and relevant development stakeholders with specific delivery experience within this market. These include officers from the local authority planning departments, developers (both specialist and mainstream), estate and land agents. Linkages have also been drawn from feedback received from the focus group work undertaken as part of the wider contract brief.

2.1.2 Stage I – Strategic policy context for housing delivery in North Staffordshire.

Note that in this report, unless specifically stated otherwise, the description “North Staffordshire” is used to refer to the three Local Authorities that comprise the NSRP. Consolidation and review of literature outlining strategic planning policy for housing delivery in North Staffordshire, draws on the Local Development Frameworks, the (now abolished) Regional Economic, Housing and Spatial Strategies and findings of the Strategic Housing Market Assessment (SHMA). This is supplemented by a critique of the underlying vision for residential development in North Staffordshire. It is important that this analysis is provided in the context of the wider economic climate and the likely impact upon development of any kind going forward. A shift in market conditions and economic fundamentals has called into question the established development framework that operated previously, shown to be dependent upon the availability of credit for development and mortgage liquidity. Development across all market tenures now operates in a constrained marketplace, therefore it is important that the research draws clear links to the economic model update work for North Staffordshire being undertaken simultaneously by Experian. Consideration of the wider economic environment will provide an indication of potential quantum and viability for selected sites.

2.1.3 Stage II - Demand side trends

Market research of the local and sub-regional household profiles and secondary data analysis to establish a target market definition, the potential pool of demand and its share of the overall market. We have analysed population and household projections, migration and travel-to-work patterns, including identifying key local employers identified as sources of potential target market for this housing, demographic and household change and the findings of the latest Strategic Housing Market Assessment. This provides the context on the current and future demand profile for proposed executive housing development in North Staffordshire.

2.1.4 Stage III – Supply side trends and review of the experience and impact of executive housing

development elsewhere

In this stage we examine historic completion rates by type of property (including new build and conversions), outlining the relatively narrow supply within North Staffordshire in recent years compared to neighbouring locations. This analysis includes discussions with the

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 8 of 80

respective planning departments to identify sources of existing property stock with potential for delivering executive type housing.

We undertook an examination of future supply to ascertain competing areas and developments through the SHLAA process, National Land Use Database schedule, Five Year Land Supply and current outstanding permissions data.

Desk-based, case study review of experience and impact of executive housing development in comparable housing markets. We appreciate that a comparable market to North Staffordshire may not exist explicitly, however the key success factors can be identified from executive housing development case studies and an analysis provided of the factors to be in place to underpin development of this type in the North Staffordshire market.

This element primarily aims to consolidate understanding and provision of a workable definition of executive housing in the North Staffordshire context. We have undertaken previous analysis of executive housing case studies and are well aware that this does not necessarily include volume-built, higher-end detached market housing. As noted above, provided the right location and environment, executive housing may include;

• Mix of bespoke detached properties at low density ie, Wynard, Stockton-on-Tees • Individual architect designed properties ie, Tutti Frutti Urban Splash, Manchester • Self build developments ie, Ashley Vale, Bristol • Environmentally sustainable developments ie, Accordia, Cambridge; Upton,

Northampton; Great Bow Yard, Somerset • New build period townhouses ie, The Square, York

2.1.5 Stage IV – Site locations and agent interviews

Analysis of the strategic potential sites is supplemented with local agent interviews examining the aspirations of those purchasing executive housing and areas of search for such housing to understand the depth of the potential market.

2.2 Current Executive Housing Market 2.2.2 The first phase of the assessment investigates the extent of housing in the North

Staffordshire sub-region, which fits the broad definition of an Executive product. Several secondary data sources were used to identify the extent of high property values and high incomes. This has included:

• Council Tax banding information for 2008 (based on property valuations at 1991);

• Land registry property sale values;

• Household Income 2008 (Annual Survey of Hours and Earnings).

2.2.3 The following variables are identified; the proportions of properties in Band ‘E to H’, property

values ‘£350-500k, £500k-£750k, £750+’ and household incomes of ‘£900+pw and £1k+pw’. Where data is available, results have been analysed on a number of geographical scales:

• Address level

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 9 of 80

• Postcode sector • Lower SOAs • Wards

2.2.4 This information has been triangulated to produce a series of maps and tables identifying the

spatial extent of the current executive housing markets and the numbers in the market. 2.2.5 The second phase of the assessment has involved identifying households from the ASHE

data 2008 who command sufficient incomes and access to equity or savings, therefore form the primary target market for property deemed to be of executive housing standard. Detailed analysis of the selected market profile looks at the current property and household characteristics.

2.2.6 The third phase of the assessment was to define distinctive market typologies through a

process of qualitative and quantitative methods (see definition of executive housing below). This process brings together selective property and household characteristics to define executive housing products and demand behaviour.

2.2.7 A number of variables were used to develop market typologies. A series of profiles or short

case studies have been developed to illustrate these typologies with the context of North Staffordshire and its surrounding area. A number of case study examples from a range of national perspectives are provided in section 9.

2.3 Future Executive Housing Market 2.3.2 It is essential that the proposed market typologies are rigorously tested with housing

practitioners, who have a practical understanding of high value housing markets. A series of interviews, market area observations, and discussions with a range of stakeholders has taken place to test the emerging findings.

2.3.3 Aspirations for future development from the housing supplier and planning control

perspectives state the requirements necessary for future executive housing.

2.4 Research Framework 2.4.2 Our research approach is structured as follows and has been split into sections for ease of

access. Section Topic Background review

Stage 1 Strategic policy context for housing delivery in Stoke-on-Trent

Review of existing plans and strategies

• Examination of latest regional and local planning strategy;

• Examination of latest regional and local economic strategy;

• Adopted Stoke-on-Trent and Newcastle-under-Lyme Core Strategy; Staffordshire Moorlands Submission Core Strategy.

• RSS, The Regional Economic Strategy, NSRP Business Plan 2008-11; SHMA, Stoke-on-Trent AMR, Newcastle under Lyme AMR, Staffordshire Moorlands AMR,

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 10 of 80

RENEW AMR 2008/09.

What is the existing position? • Where are the high value dwellings

located? • Executive housing supply in the planning

pipeline ie, benefit of detailed consent? • How do the constituent local authorities

stand in valid comparison within NSHMA and to adjacent markets?

• Where do current high earners live? • Correlation between the two

• Land Registry house price indices;

• Council Tax Register; • Mapping correlation of

properties and earners at ward and / or output area geographies;

• Latest NSHMA; • ONS neighbourhoods; • Supply pipeline data; • Travel to work data

comparison of resident and workplace based incomes;

• Income data by Lower Super Output Area / ward;

• Focus group feedback; • Estate agent feedback; • Council planning

departments feedback. Local housing market overview

• Overview of local market trends and differentiation of local housing markets.

• Land Registry; • New build market data. • Local economic drivers.

Demand analysis • Forecasts for current and future population

and household change; • Drivers and dynamics of population and

household change; • Migration and travel to work trends; • Socio-economic profiling; • What type of households? Neighbourhood

statistics analysis of socio-economic composition;

• Demand for executive housing, fuelled by demographic changes;

• Where are the gaps between demand and supply?;

• Growth of working age population; • Key areas of economic growth now and

forecast; • Potential constraints unique to the local

market, lifestyle offer etc.

• Population and household projections;

• Migration statistics into and within the Stoke Housing Market area and the sub-region;

• GDP statistics; • Local economic drivers; • ACORN profiling; • Neighbourhood

Statistics and NOMIS; • 2001 Census, ONS; • Population estimates,

ONS; • Annual Survey of Hours

and Earnings; • GIS mapping analysis. • Focus group feedback

Supply analysis • What has been built? An overview of

historic supply in the local authority market in terms of size, number and spatial

• Latest development supply pipeline statistics;

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 11 of 80

location of executive housing; • What is being built? A review of planned

schemes and those under construction in respect of outstanding planning permissions, SHLAA and National Land Use Database;

• Locally determined growth strategy - supply targets;

• What reasonable quantum of executive housing should the local authorities be aiming for?

• What is the gap between existing demand and supply?

• Latest development capacity data;

• Developer feedback • Local authority planning

feedback.

Where do the three local authorities want to be?

• Current gap analysis between demand and supply profile;

• ‘Visions’ to be supplied by the respective local authorities

• Experian, ASHE; • SHMA • Council feedback and

emerging LDF documents

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 12 of 80

Section 3 Executive Housing Market Definition 3.1 Introduction 3.1.1 Housing referred to as ‘executive’ is a vague market product and has eluded definitive

classification due to the many forms, densities, locations and contexts within which property referred to as ‘executive’ can be found. Indeed the term is often used, somewhat erroneously, to uplift the image of developments that would otherwise be classified as volume built housing. The term ‘executive’ may be allocated to new build developments in one location due to relative exclusivity in the context of resident household incomes, that may not be regarded as distinct developments in more affluent locations. Furthermore the term can be used dependent upon consumer perception and aspiration, in reference to new build bespoke properties, gated communities or period properties.

3.1.2 The term ‘executive’ equates to the most desirable and commonly, most expensive property

in a particular location. Executive markets are locations that generally operate on a regional basis, across regional housing markets due to their exclusivity, the operation of such not confined to local authority boundaries. Purchasers of executive housing will often travel over large distances to employment locations, due to the nature of the desired character of residence.

3.1.3 In broad terms, executive housing is acknowledged as, ‘High quality accommodation in low

density, suited to the needs and aspirations of higher income households’. 1 3.1.4 The first aspect of this research is to establish a meaningful definition of executive housing in

the North Staffordshire market context. An executive housing market is dependent upon the components of supply and demand. In these terms, a housing supply profile based on property prices, property sizes, dwelling types, interior specifications, outside space and location. A housing demand profile based on household income, equity and savings, household type, household size, household needs, length of occupancy, access to occupancy and business ownership.

3.1.5 Characteristics of an executive housing market would also include a clear linkage to the

national / international market, beneficial or at least low taxation, in terms of the location choice of industry and employment opportunities most conducive to business leaders, excellent environmental conditions, a contiguous executive or prime property market and associated lifestyle offer (discussed in further detail below).

3.1.6 An executive housing market can be defined in a number of ways combining the property

value, but including a suite of elements such as price, density, design, location and specification, in order to establish a meaningful definition. In addition to a price level, this may include for example factors such as low density (eg, approximating five units per acre), with large floor space in excess of 2,000sqft, offering facilities such as 4+ bedrooms, double garages and ensuite bedrooms or luxury apartments in desirable locations. They can include bespoke design and self-build and are generally in owner occupation.

1 Tomaney, J. Bradley, D. (2006). The economic role of mobile professional and creative workers and their housing residential preferences: evidence from North East England. Nathanial Lichfield and Partners. Centre for Urban and Regional

Development Studies, University of Newcastle upon Tyne. Newcastle.

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 13 of 80

3.1.7 It is appreciated that in many markets and normal market conditions, property regarded as executive housing is likely to attract prices in excess £450,000. However a certain level of discount has been factored into our analysis for Stoke, in terms of both council tax banding and property pricing. This has been appropriate in order to capture the top end of the market for comparable properties with those in the adjacent local authorities of North Staffordshire. This approach has been informed by analysis of transaction levels across North Staffordshire and interviews with local agents active across the area, listed in appendix F. Our analysis therefore includes council tax banding E – H, rather than just G – H, to include the top end of the residential markets in each LA.

3.1.8 In addition our analysis of the depth of the top end market in North Staffordshire has

identified disparities in achieved property values. Analysis of the depth of this market represented by transaction activity identified a number of price bands.

3.1.9 As we outline in section four below there are a significantly higher number of transactions

recorded in Staffordshire Moorlands and Newcastle-under-Lyme for properties in excess of £400,000 compared to Stoke. The justification for adopting a £400,000 threshold for upper market housing is two-fold. Namely this property value reflects the council tax discount for Stoke encompassing a comparable upper-end market within bands E-H. Secondly the feedback from considerable focus group work with local agents and residents identified this level at which properties were considered to be upper market in Stoke.

3.1.10 Therefore the value ranges we have identified and will use in this assessment of current

high-end property transactions include;

• £400 - £500K range covers the ‘very high end’ property stock in Stoke and ‘high end’ property in Newcastle-under-Lyme and Staffordshire Moorlands;

• £500 - £750K range covers the ‘exceptional and exclusive’ properties in Stoke and the ‘very high end’ properties in Newcastle-under-Lyme and Staffordshire Moorlands;

• £750K+ covers the ‘exceptional and exclusive’ properties in Newcastle-under-Lyme and Staffordshire Moorlands.

3.1.11 Below we examine the current upper end housing offer demand in terms of both transaction

levels and housing type. This will inform the recommendations as to the housing typologies and characteristics comprising a conducive ‘Quality of Place’ and residential offer in our case study section. An explanation of the relationship between these aspects is discussed in section 9.

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 14 of 80

Section 4 Executive Housing Market Assessment Current Executive Housing Market 4.1.1 As Table 4.1 illustrates the buying activity of detached properties in the three local authorities

of North Staffordshire over the last three years highlights properties commanding prices in excess of £750,000 and £1M in Newcastle-under-Lyme and Staffordshire Moorlands. In comparison the top end of the Stoke market is represented by a market high of 0.9% during 2008 of between £500,000 - £600, 000 (Land Registry, Q2 2009).

4.1.2 The analysis has focussed upon detached property transactions due to nominal levels of

activity in the higher price categories for other property types such as flats, semi-detached and terraced properties. We appreciate that in certain markets the executive market has the potential to include properties of these types, such as prime location flats and townhouses. We identify the current demand levels for these alternative housing types in the higher price bands in section 4.2 below.

Table 4.1: Buying activity detached properties North Staffordshire 2007 – 2009 to date

Stoke 2007 2008 2009

Nos % Nos % Nos %

Under 100K 29 2.9% 26 4.8% 7 5.5%

100 -150K 215 21.7% 114 20.9% 55 43.0%

150 - 200 347 34.9% 200 36.6% 49 38.3%

200 - 300 283 28.5% 147 26.9% 13 10.2%

300 - 400 76 7.7% 40 7.3% 3 2.3%

400 - 500 38 3.8% 14 2.6% 1 0.8%

500-600 5 0.5% 5 0.9% 0 0.0%

Total 993 100.0% 546 100.0% 128 100.0%

Newcastle-under-Lyme 2007 2008 2009

Nos % Nos % Nos %

Under 100K 7 1.4% 4 1.2% 4 3.8%

100 -150K 63 12.8% 45 13.4% 18 17.0%

150 - 200 211 42.7% 117 34.9% 30 28.3%

200 - 300 132 26.7% 103 30.7% 39 36.8%

300 - 400 52 10.5% 48 14.3% 9 8.5%

400 - 500 21 4.3% 7 2.1% 4 3.8%

500-750 7 1.4% 10 3.0% 1 0.9%

750-1M 1 0.2% 0 0.0% 0 0.0%

1M+ 0 0 1 0.3% 1 0.9%

Total 494 100.0% 335 100.0% 106 100.0%

Staff Moors 2007 2008 2009

Nos % Nos % Nos %

Under 100K 9 1.2% 6 1.8% 4 3.5%

100 -150K 232 30.4% 40 11.9% 23 20.4%

150 - 200 174 22.8% 96 28.6% 27 23.9%

200 - 300 221 29.0% 128 38.1% 40 35.4%

300 - 400 81 10.6% 41 12.2% 12 10.6%

400 - 500 32 4.2% 19 5.7% 4 3.5%

500-750 12 1.6% 6 1.8% 3 2.7%

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 15 of 80

750-1M 1 0.1% 0 0.0% 0 0.0%

1M+ 1 0.1% 0 0.0% 0 0.0%

Total 763 100.0% 336 100.0% 113 100.0%

Source: Land Registry Q2 2009

4.1.3 As Table 4.1 illustrates, at the height of the property market, the top 4% of transactions in

Stoke were recorded above £400,000, characterising an exclusive executive housing market. Comparable levels of transactions in Newcastle-under-Lyme and Staffordshire Moorlands are recorded between the £500 - £750,000 price categories, with a greater representation of transactions recorded in these local authorities in the uppermost price bands.

Table 4.2: Percentage of properties recorded within respective council tax bands

Council tax bands

LA A B C D E F G H Total E-H F-H

Stoke-on-

Trent

62.0 19.5 12.5 3.9 1.5 0.4 0.1 0.0 100.0 2.0 0.6

Newcastle-

under-Lyme

44.8 18.0 19.8 7.8 4.8 3.1 1.7 0.1 100.0 9.6 4.8

Staffordshire

Moorlands

22.0 23.7 24.5 14.1 9.6 4.3 1.8 0.1 100.0 15.7 6.2

Total 49.4 20.0 16.8 7.0 4.0 1.9 0.8 0.1 100.0 6.8 2.8

Source: Council tax records RENEW

4.1.4 Table 4.2 illustrates the respective distribution of properties across North Staffordshire by

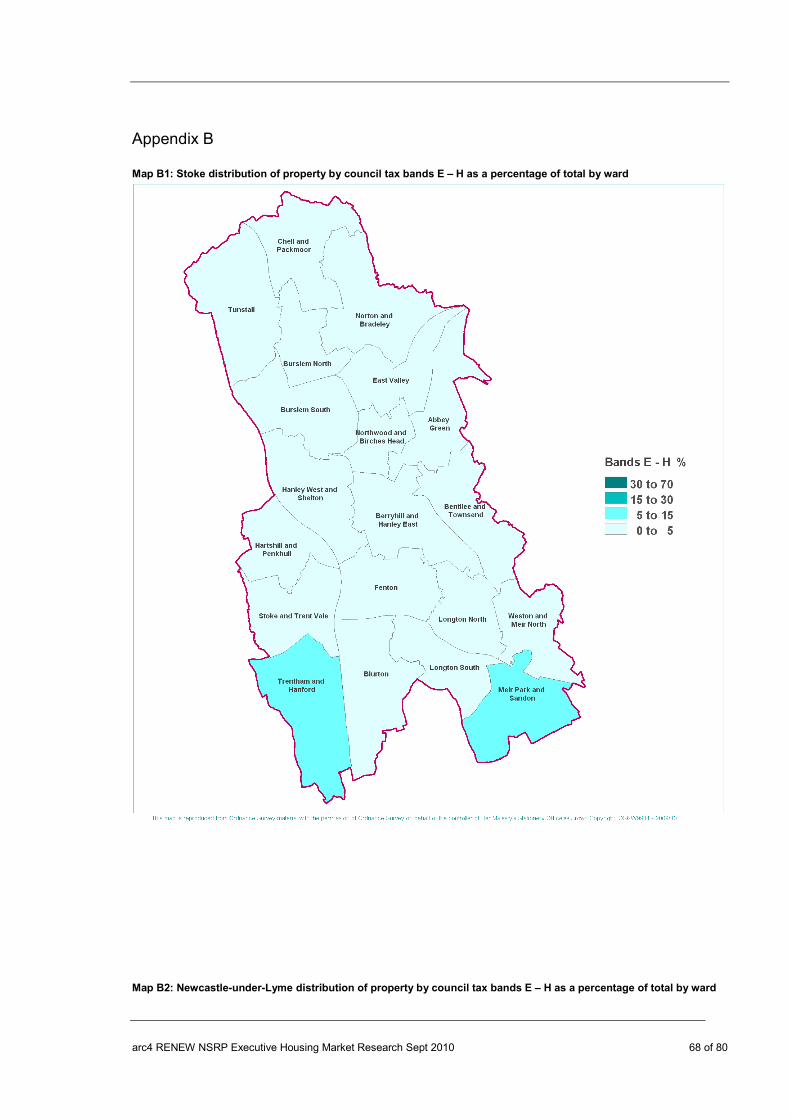

council tax banding. Reflecting the transaction activity in Table 4.1 both Newcastle-under-Lyme and Staffordshire Moorlands record higher levels of stock within the higher tax bands compared to Stoke. A full breakdown of properties by CT band and ward is provided in Appendix A and B. This data has been compared to respective household income data by ward to identify the most conducive locations for potential executive housing delivery in terms of a target market.

4.1.5 Council tax banding classifies properties from band A (properties with the lowest tax rating)

to band H (highest tax rating) in accordance with the properties value at the time of assessment. A summary of the distribution of council tax band classifications, across the North Staffordshire housing market, is shown in Table 4.2 and a full breakdown by ward in Appendix A. However in terms of the target bands of E – H, a total of 2,273 properties were identified within these bands in Stoke, compared to more than double at 5,107 properties within Newcastle-under-Lyme and a further 6,649 properties within Staffordshire Moorlands.

4.1.6 The disparities become even greater when considering the bands F – H, with 617 properties

in Stoke compared to a more substantial 2,573 in Newcastle-under-Lyme and 2,613 within Staffordshire Moorlands. Properties within council tax bands F – H account for just 0.6% of all properties within Stoke, compared to 4.8% of properties in Newcastle-under-Lyme and 6.2% in Staffordshire Moorlands. There is a justifiable requirement to factor in a ‘banding discount’ in terms of analysis in regards ‘top-end’ of the respective markets. The transaction and council tax data above indicates that high value housing offers an insignificant contribution to the Stoke housing market in particular.

4.1.7 In terms of ward distribution of higher value properties as illustrated in full in Appendix A and

B, Table 4.3 identifies the top ten Stoke wards with the highest representation of properties

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 16 of 80

in the uppermost council tax bands. The three wards of Trentham and Hanford (30%), Meir Park and Sandon (16.9%) and Abbey Green (11.2%) contain almost two-thirds of all Stoke properties within bands E – H, at 58.1%.

Table 4.3: Top ten Stoke wards recording highest valued properties council tax bands E - H Ward name E F G H E-H Total (%) F-H Total (%)

Abbey Green 3.4 1.1 0.1 0.0 4.7 1.3

Blurton 2.2 0.9 0.1 0.0 3.2 1.0

Chell and Packmoor 0.8 0.0 0.0 0.0 1.0 0.1

East Valley 1.8 0.9 0.1 0.0 2.8 1.0

Hartshill and Penkhull 1.5 0.4 0.1 0.2 2.1 0.7

Longton South 1.9 0.3 0.1 0.0 2.3 0.4

Meir Park and Sandon 4.8 2.1 0.2 0.0 7.1 2.3

Northwood and Birches Head 1.5 0.0 0.0 0.0 1.5 0.0

Norton and Bradeley 0.9 0.1 0.1 0.0 1.2 0.2

Trentham and Hanford 9.6 2.2 0.7 0.2 12.6 3.1

Source: RENEW

4.1.8 In terms of ward distribution of higher value properties as illustrated in full in Appendix A and

B, Table 4.4 identifies the top ten Newcastle-under-Lyme wards with the highest representation of properties in the uppermost council tax bands. The three wards of Loggerheads and Whitmore (25.2%), Westlands (16.6%) and Keele (15.7%) contain almost half of all Newcastle-under-Lyme properties within bands E – H, at 47.5%.

Table 4.4: Top ten Newcastle-under-Lyme wards recording highest valued properties council tax bands E – H

Ward name E F G H E-H F-H

Audley and Bignall End 4.3 1.3 0.3 0.0 5.9 1.6

Halmerend 12.1 8.8 3.0 0.4 24.2 12.1

Keele 18.2 12.3 5.1 1.9 37.6 19.4

Loggerheads and Whitmore 24.6 17.8 17.2 0.4 60.0 35.4

Madeley 9.3 7.5 1.7 0.2 18.7 9.3

May Bank 2.2 1.7 1.3 0.0 5.2 3.0

Newchapel 3.1 1.1 0.1 0.0 4.3 1.2

Seabridge 11.2 2.5 0.2 0.0 13.9 2.7

Thistleberry 8.1 4.1 0.7 0.0 13.0 4.9

Westlands 14.2 18.0 7.3 0.0 39.6 25.4

Source: RENEW 4.1.9 In terms of ward distribution of higher value properties as illustrated in full in Appendix A and

B, Table 4.5 identifies the top ten Staffordshire Moorlands wards with the highest representation of properties in the uppermost council tax bands. The three wards of Horton (12.1%), Dane (10.5%) and Bagnall and Stanley (9.0%) contain over one-third of all Staffordshire Moorlands properties within bands E – H, at 31.6%. As indicated in Appendix B map B3, the distribution of higher valued properties is more widespread across the authority in comparison to the pockets of higher value stock in Newcastle-under-Lyme and in far fewer proportions in Stoke.

Table 4.5: Top ten Staffordshire Moorlands wards recording highest valued properties council tax bands E – H Ward name E F G H E-H F-H

Alton 24.1 10.4 4.8 0.3 39.6 15.6

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 17 of 80

Bagnall and Stanley 22.1 19.4 9.1 0.0 50.6 28.5

Biddulph North 14.0 4.5 2.6 0.0 21.1 7.1

Caverswall 14.9 7.2 4.2 0.1 26.5 11.6

Cheddleton 13.2 6.6 1.7 0.2 21.7 8.5

Dane 26.2 22.7 9.2 0.9 59.0 32.8

Hamps Valley 22.2 8.9 4.1 0.3 35.6 13.3

Horton 21.5 27.0 19.5 0.4 68.4 46.9

Ipstones 19.1 7.8 2.6 0.1 29.6 10.5

Manifold 26.7 10.1 4.0 0.0 40.8 14.1

Source: RENEW

4.1.10 The distribution of properties in council tax bands E – H is shown in Appendix B1 – B3. It is

clear that higher value property makes a nominal contribution to the overall housing stock in Stoke as a local authority. In Newcastle-under-Lyme, there appears to be a clear distinction between the north and east of the local authority with a low representation of higher valued stock compared to the south in particular in Loggerheads and Whitmore, Keele and Westlands and west such as in Halmerend and Madeley.

4.1.11 Higher value property appears to represent a greater proportion and wider distribution of

property stock in Staffordshire Moorlands, particularly towards the east of the district in the National Park (Appendix Map B3).

4.2 Current ‘high-end’ property market context 4.2.1 Land Registry sales data was examined for the period Q1 2005 – Q2 2009. The dataset

comprises 31,702 individual residential sales records from open market transactions in the three local authorities of North Staffordshire, over the four-year period. By way of comparison the rate of private sector turnover is far greater in Stoke at 18,839 transactions over this period, compared to 7,139 in Newcastle-under-Lyme and 5,724 sales in Staffordshire Moorlands within this period.

4.2.2 In terms of analysing the depth of the high-end property market in North Staffordshire,

unsurprisingly a significantly higher number of transactions have been recorded in Staffordshire Moorlands and Newcastle-under-Lyme for properties in excess of £400,000 compared to Stoke. The justification for adopting a £400,000 threshold for upper market housing is two-fold. Namely this property value reflects the council tax discount for Stoke encompassing a comparable upper-end market within bands E-H. Secondly the feedback from considerable focus group work with local agents and residents identified this level at which properties were considered to be in the highest market.

4.2.3 The total number of recorded transactions above this threshold between Q1 2007 and Q2

2009 was 63 sales in Stoke. All sales were existing stock apart from two new build sales and all apart from three being detached properties. Table 4.6 identifies those ‘high-end’ non-detached property sales over this period, illustrating the constrained demand for upper market housing typologies from the traditional detached type. Each transaction was recorded as an existing semi-detached property within a suburban / rural location.

Table 4.6: Non-detached upper market property transactions - Stoke

Price Type New Build / Existing Post Code Ward Name Rural / Suburban / Urban

£370,000 Semi Existing ST3 5YD Longton North Suburban / Rural

£379,950 Semi Existing ST4 8XJ Trentham & Hanford Suburban / Rural

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 18 of 80

£395,000 Semi Existing ST2 9DD Berryhill & Hanley East Suburban / Rural

Source: RENEW, Land Registry

4.2.4 In Newcastle-under-Lyme the number of transactions above this threshold was 53. All sales

were existing stock apart from four new build sales and all sales except 17 being detached properties, 9 semi-detached and 8 terraced. Table 4.7 identifies those ‘high-end’ non-detached property sales over this period, illustrating the depth of upper market housing typologies from the traditional detached type. Each transaction was recorded as an existing property apart from two new builds, the majority within a rural / suburban location. Notably there is an equal representation of larger terraced / townhouse and semi-detached properties.

Table 4.7: Non-detached upper market property transactions – Newcastle-under-Lyme

Price Type New Build / Existing Post Code Ward Name Rural / Suburban / Urban

£750,000 T Existing ST5 0QW May Bank Suburban

£760,000 T Existing TF9 4HE

Loggerheads and

Whitmore Rural

£775,000 S Existing ST5 5HB

Loggerheads and

Whitmore Rural

£595,000 T Existing TF9 2PA

Loggerheads and

Whitmore Rural

£495,000 T Existing TF9 2PA

Loggerheads and

Whitmore Rural

£500,000 S Existing ST5 0QN May Bank Urban / Suburban

£520,000 T New Build TF9 4NA

Loggerheads and

Whitmore Rural

£350,000 T Existing TF9 4HJ

Loggerheads and

Whitmore Rural

£350,000 S Existing CW3 9QL Madeley Rural

£355,000 S Existing CW3 9AN Halmerend Rural / Suburban

£375,000 S Existing ST5 3LT Westlands Suburban / Urban

£377,500 S Existing ST5 1DP Town Urban / Suburban

£385,000 S Existing TF9 2QH

Loggerheads and

Whitmore Rural

£389,950 S Existing TF9 4NB

Loggerheads and

Whitmore Rural

£397,000 S New Build ST5 3JG Westlands Rural / Suburban

£429,000 T Existing ST5 2NF Thistleberry Suburban

£475,000 T Existing ST5 3GZ Knutton and Silverdale Rural / Suburban

Source: RENEW, Land Registry

4.2.5 In Staffordshire Moorlands 78 transactions were recorded above £400,000. All sales were

existing stock apart from seven new build sales and all sales except 39 being for detached properties. Table 4.8 identifies those ‘high-end’ non-detached property sales over this period, illustrating the depth of upper market housing typologies from the traditional detached type. Each transaction was recorded as an existing property apart from two new builds, the majority within a rural / suburban location. Notably there is an equal representation of larger terraced / townhouse and semi-detached properties, with only one recorded sale for a flat within this market.

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 19 of 80

Table 4.8: Non-detached upper market property transactions – Staffordshire Moorlands

Source: RENEW, Land Registry

4.2.6 As the tables above indicate there is a considerable paucity of new build executive property

supply on the current market throughout the three authorities of North Staffordshire. The total number of new build sales in this sector across the three authorities being 13 sales over this period. The main focus of transaction activity within the high end market recorded within existing properties within a rural and suburban location. This feature of the North Staffordshire executive market is highlighted within section 6 agent and developer interviews

Price Type New Build / Existing Post Code Ward Name Rural / Suburban / Urban

£370,000 T Existing ST13 5LR Leek East Rural / Suburban

£440,000 S Existing ST13 8JS Leek North Rural / Suburban

£365,000 S Existing ST13 8DL Leek West Suburban / Rural

£495,000 S Existing ST10 4JH Checkley Rural

£980,000 S Existing CW12 3QJ Horton Rural

£370,000 T Existing ST9 9PS Bagnall and Stanley Rural

£390,000 T Existing SK17 0NZ Manifold Rural

£360,000 S Existing ST9 9NJ Bagnall and Stanley Rural

£400,000 S Existing ST13 5PA Leek South Suburban

£370,000 S Existing ST13 7EA Cheddleton Rural

£400,000 S Existing ST11 9BG Forsbrook Rural

£450,000 T Existing ST9 9NS Bagnall and Stanley Rural

£385,000 T Existing ST13 6AB Leek North Urban

£481,000 S Existing ST10 4BN Alton Rural

£364,000 T Existing ST9 9LX Bagnall and Stanley Rural

£570,000 S Existing ST8 6QP Biddulph North Suburban

£670,000 F New Build DE6 2FR Hamps Valley Rural

£365,000 S Existing ST11 9HQ Forsbrook Suburban / Rural

£404,000 T Existing ST9 9QF Horton Rural

£950,000 S Existing SK11 0RF Dane Rural

£357,000 S Existing ST13 5SB Leek East Suburban / Rural

£480,000 S Existing ST13 8SB Leek North Rural

£430,000 S Existing ST13 5EZ Leek North Urban

£395,000 T Existing ST13 8SA Leek North Rural

£375,000 T Existing ST13 7AL Leek South Rural

£590,000 S Existing ST13 7QZ Hamps Valley Rural

£500,000 T Existing ST10 2BA Churnet Rural

£370,000 T Existing ST13 8RN Horton Rural

£600,000 T Existing ST13 5RD Leek South Rural

£410,000 S New Build ST10 3BQ Alton Rural

£440,000 T Existing ST9 0BA Cheddleton Rural

£425,000 T Existing ST8 7PS Biddulph South Rural

£430,000 T Existing ST8 7RS Biddulph North Rural

£660,000 S Existing ST10 4AP Alton Rural

£385,000 S Existing ST10 4BH Alton Rural

£595,000 S Existing ST13 8SH Dane Rural

£350,000 S Existing ST9 9DY

Brown Edge and

Endon Rural

£350,000 S Existing ST13 8PU Horton Rural

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 20 of 80

below. Illustrating a distinct absence of new build property currently on the market, the highest priced new build stock in North Staffordshire is £259,995, volume-built and not representative of an executive market according to the definitions provided.

4.2.7 The value ranges used in this assessment of current high-end property transactions include;

• £400 - £500K range covers the ‘very high end’ property stock in Stoke and ‘high end’ property in Newcastle-under-Lyme and Staffordshire Moorlands;

• £500 - £750K range covers the ‘exceptional and exclusive’ properties in Stoke and the ‘very high end’ properties in Newcastle-under-Lyme and Staffordshire Moorlands;

• £750K+ covers the ‘exceptional and exclusive’ properties in Newcastle-under-Lyme and Staffordshire Moorlands.

4.2.8 Identified property sales within the three high-end value ranges are broken down by ward

and local authority in Tables 4.9 – 4.11 below. Table 4.9: High end house price transactions by ward - Stoke

Ward name £400 -

£500K

£500 -

£750K

£750K+

Abbey Green 2

Bentilee and Townsend 1

Berryhill and Hanley East 1

Blurton 1

Burslem North 1

East Valley 4

Longton North 1

Meir Park and Sandon 1

Northwood and Birches Head 1

Stoke and Trent Vale 1

Trentham and Hanford 9 1

Source: Land Registry, RENEW

4.2.9 As illustrated in Table 4.9, only one property could be classified as ‘exclusive and

exceptional’ in terms of price, this property recorded in the Trentham and Hanford ward. As we have illustrated elsewhere, this ward comprises the highest proportion of private sector stock in the highest council tax bands and the highest average household income of Stoke wards.

4.2.10 Stoke has a highly constrained supply of high value housing. Indeed the fact that all but one

property has been sold for sub-£500,000 would indicate that compared to some higher value areas an executive housing product does not exist.

4.2.11 Table 4.10 illustrates the higher representation of high value properties within Newcastle-

under-Lyme. A total of 130 transactions are recorded within the ‘high-end’ range, 18 sales within the ‘very-high’ range and 6 within the ‘exceptional’ range. These transactions are recorded within the ward of Loggerheads and Whitmore and include a sale in excess of £1.1M. The wards of Westlands, Halmerend and May Bank also record representation within the ‘very high’ range.

Table 4.10: High end house price transactions by ward - Newcastle-under-Lyme

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 21 of 80

Ward name £400 -

£500K

£500 -

£750K

£750K+

Audley and Bignall End 2

Halmerend 9 3

Keele 1

Knutton and Silverdale 1

Loggerheads and Whitmore 42 7 6

Madeley 3 1

May Bank 5 2

Newchapel 3

Seabridge 3

Thistleberry 5 1

Town 3

Westlands 27 4

Wolstanton 1

Source: Land Registry, RENEW

4.2.12 Table 4.11 illustrates the higher representation of high value properties within Staffordshire

Moorlands. A total of 145 transactions are recorded within the ‘high-end’ range, 30 sales within the ‘very-high’ range and 8 within the ‘exceptional’ range. These transactions are recorded within six wards and include sales in excess of £1M.

Table 4.11: High end house price transactions by ward – Staffordshire Moorlands

Ward name £400 -

£500K

£500 -

£750K

£750K+

Alton 7 1

Bagnall and Stanley 10 1

Biddulph Moor 2

Biddulph North 8 2 1

Biddulph South 1

Brown Edge and Endon 5 1

Caverswall 2 1

Cheadle South East 1

Cheadle West 1

Checkley 5 1 1

Cheddleton 12

Churnet 5 4

Dane 6 2 1

Forsbrook 9 1

Halmerend 1

Hamps Valley 6 2 2

Horton 15 9 1

Ipstones 8

Leek East 8

Leek North 9 1

Leek South 7 1

Leek West 3

Manifold 10 3 2

Tutbury and Outwoods 1

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 22 of 80

Werrington 3

Source: Land Registry, RENEW

4.3 Wider Housing Reference Area 4.3.1 As the research identifies, the market for executive housing operates over a wide area,

larger than housing markets are normally defined. The market is often described as regional, but as North Staffordshire sits on the boundary of two regions it is appropriate to consider a cross-regional wider market area. Following consultation, we based it on the wider reference area for the North Staffordshire housing market and included the (pre-reorganisation) LA areas of Crewe and Nantwich, Congleton, Stafford and North Shropshire. .

4.3.2 Table 4.12 illustrates the buying activity of detached properties in this wider housing reference area over the last three years. The number of properties commanding prices in excess of £500,000 - £1M in North Shropshire represents 4.5% of the total market, higher than that in Newcastle-under-Lyme and Staffordshire Moorlands. The volume of transactions at £400K-£500K records almost 10% of the total market share of detached sales. In terms of sales volumes, North Shropshire is comparable with Newcastle-under-Lyme

4.3.3 In terms of transaction volumes, Stafford records a considerable number of sales within the

higher price bands, comparable with, though slightly higher in numerical terms with Staffordshire Moorlands over the three-year period. Comparable levels of transactions in the higher price categories are recorded, including individual exceptional priced sales in excess of £1M.

4.3.4 The analysis has focussed upon detached property transactions due to nominal levels of

activity in the higher price categories for other property types such as flats, semi-detached and terraced properties. In Stafford sales of these property types recorded over this three year period were 8 semi-detached between £400-£500K, no flats and 4townhouse / terraced properties. No transactions recorded for these types over £500,000.

Table 4.12: Buying activity wider Housing Reference Area 2007 – 2009 to date

North Shropshire 2007 2008 2009

Nos % Nos % Nos %

Under 100K 5 1.2% 3 1.2% 2 2.5%

100 -150K 20 4.8% 12 4.8% 9 11.3%

150 - 200 103 24.8% 55 21.9% 26 32.5%

200 - 300 159 38.3% 105 41.8% 25 31.3%

300 - 400 80 19.3% 42 16.7% 10 12.5%

400 - 500 30 7.2% 24 9.6% 7 8.8%

500-750 16 3.9% 8 3.2% 1 1.3%

750-1M 2 0.5% 2 0.8% 0 0.0%

Total 415 100.0% 251 100.0% 80 100.0%

Stafford 2007 2008 2009

Nos % Nos % Nos %

Under 100K 5 0.8% 2 0.6% 3 1.9%

100 -150K 27 4.1% 13 3.7% 23 14.6%

150 - 200 147 22.3% 75 21.1% 39 24.8%

200 - 300 301 45.7% 160 45.1% 59 37.6%

300 - 400 120 18.2% 60 16.9% 19 12.1%

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 23 of 80

400 - 500 38 5.8% 21 5.9% 9 5.7%

500-750 17 2.6% 20 5.6% 5 3.2%

750-1M 1 0.2% 3 0.8% 0 0.0%

1M+ 2 0.3% 1 0.3% 0 0.0%

Total 658 100.0% 355 100.0% 157 100.0%

Congleton 2007 2008 2009

Nos % Nos % Nos %

Under 100K 7 1.0% 3 1.0% 3 2.9%

100 -150K 16 2.4% 19 6.2% 17 16.2%

150 - 200 112 16.7% 51 16.7% 33 31.4%

200 - 300 339 50.7% 146 47.9% 36 34.3%

300 - 400 112 16.7% 52 17.0% 9 8.6%

400 - 500 49 7.3% 21 6.9% 4 3.8%

500-750 31 4.6% 12 3.9% 2 1.9%

750-1M 3 0.4% 0 0.0% 1 1.0%

1M+ 0 0.0% 1 0.3% 0 0.0%

Total 669 100.0% 305 100.0% 105 100.0%

Crewe and Nantwich 2007 2008 2009

Nos % Nos % Nos %

Under 100K 2 0.3% 4 1.3% 3 2.3%

100 -150K 52 8.3% 41 13.0% 22 17.2%

150 - 200 170 27.0% 86 27.3% 31 24.2%

200 - 300 224 35.6% 104 33.0% 37 28.9%

300 - 400 87 13.8% 46 14.6% 21 16.4%

400 - 500 70 11.1% 15 4.8% 12 9.4%

500-750 20 3.2% 15 4.8% 2 1.6%

750-1M 2 0.3% 4 1.3% 0 0.0%

1M+ 2 0.3% 0 0.0% 0 0.0%

Total 629 100.0% 315 100.0% 128 100.0%

Source: Land Registry Q2 2009

4.3.5 As Table 4.12 illustrates, the buying activity of detached properties in the wider South

Cheshire area incorporating Congleton and Crewe and Nantwich over the last three years has declined significantly in line with the wider market trends. In Congleton, in terms of absolute transaction levels and distribution of stock, similar trends are drawn with Staffordshire Moorlands. However in both Congleton and Crewe and Nantwich a higher concentration of sales are recorded in the mid-range executive properties namely £400K - £500K price band.

4.3.6 The analysis of the extent of the respective executive markets across the wider housing

market reference area identifies the comparative lack of housing being sold within this sector in Stoke-on-Trent in particular. The majority of transactions at this level are recorded for existing detached properties.

4.3.7 The overall position is shown in Table 4.13. To give a snapshot, it is probably reasonable to consider the annual level of transactions at prices of £500k and over, based on 2007 and 2008. This covers a year that had buoyant activity and one of declining activity. The figures for the first half of 2009 are much lower, and represent a depressed rather than a normal market. On this basis, there are

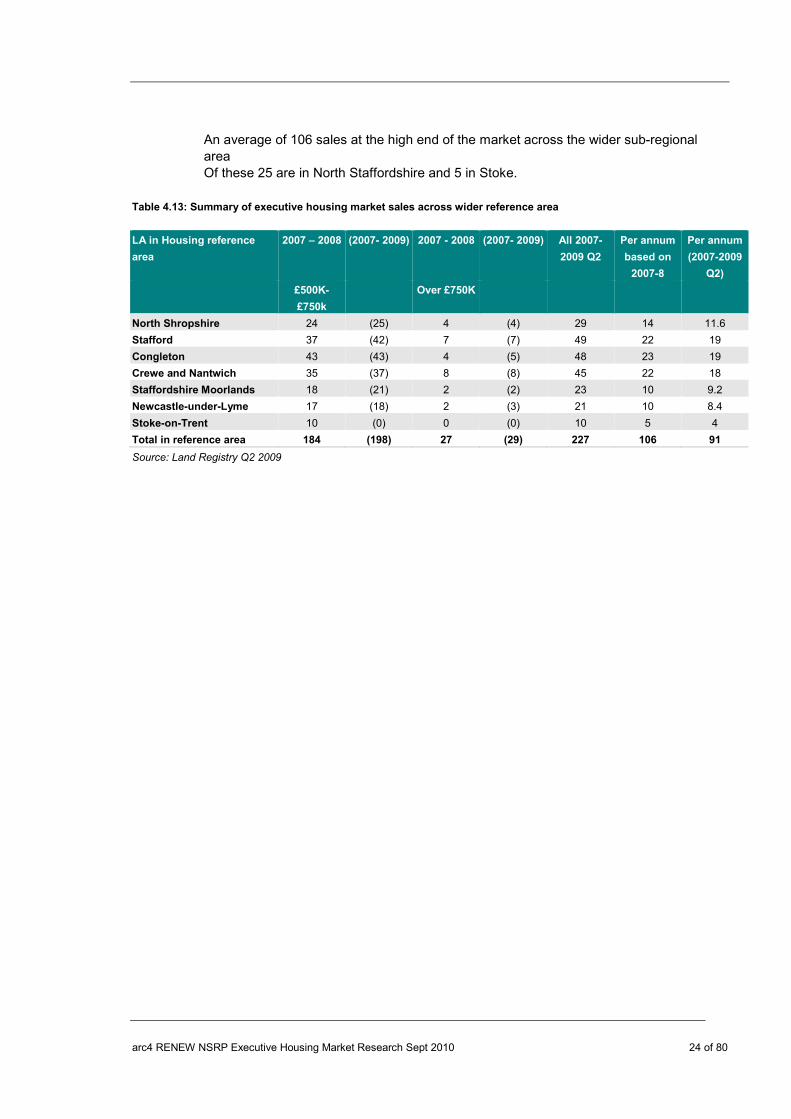

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 24 of 80

An average of 106 sales at the high end of the market across the wider sub-regional area Of these 25 are in North Staffordshire and 5 in Stoke.

Table 4.13: Summary of executive housing market sales across wider reference area

LA in Housing reference

area

2007 – 2008 (2007- 2009) 2007 - 2008 (2007- 2009) All 2007-

2009 Q2

Per annum

based on

2007-8

Per annum

(2007-2009

Q2)

£500K-

£750k

Over £750K

North Shropshire 24 (25) 4 (4) 29 14 11.6

Stafford 37 (42) 7 (7) 49 22 19

Congleton 43 (43) 4 (5) 48 23 19

Crewe and Nantwich 35 (37) 8 (8) 45 22 18

Staffordshire Moorlands 18 (21) 2 (2) 23 10 9.2

Newcastle-under-Lyme 17 (18) 2 (3) 21 10 8.4

Stoke-on-Trent 10 (0) 0 (0) 10 5 4

Total in reference area 184 (198) 27 (29) 227 106 91

Source: Land Registry Q2 2009

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 25 of 80

Section 5 Policy Context 5.1 National policy context 5.1.1 The one issue that dominates all others in the UK housing market at the current time is that

there is an underlying undersupply of the correct housing to meet demand. Demand has increased substantially over recent years through demographic and cultural shifts, smaller household sizes, increased life expectancy, immigration and rising wealth. Over the past decade house building has simply not kept pace, latest CLG figures reveal 133,710 completions during 2008 against a national target of 240,000.

5.1.2 One of the consequences of this imbalance has been to contribute to the extent that house

prices have risen dramatically over the last five years. In addition the cost differentials between tenures has risen to such a level that many households are trapped within the rented sector. For example, the ability for households in social rented accommodation to exercise any choice within the market is heavily restricted and first time buyer loans are currently at historically low levels.

5.1.3 The former Government’s policy solution to the perceived housing ‘crisis’ was contained

within the 2007 Housing Green Paper, which set ambitious targets for the volume of future house building in England. The Green paper proposed the delivery of three million homes by 2020. Meeting this 240,000 unit per annum target will be a significant challenge for both the development industry and the planning system and as such the then Government stated that policy would aim to move beyond supply and demand issues. The objective was to loosen the housing market and enable households to move between different tenures more easily at different life stages. The future direction of government policy on housing, beyond the very sketchy outlines in the Coalition Government agreement remains to be clarified.

How does lower density executive housing provision within North Staffordshire fit within the strategic planning framework for North Staffordshire and the wider sub-region?

5.1.4 Stoke, like other local authorities, is currently in a period of transition from the current

Structure Plan planning framework to the emerging Local Development Framework. Local Development Frameworks are designed to promote a proactive approach to managing and facilitating development. LDF’s differ considerably to previous spatial planning documents in that they are continuous and fluid and are designed to be driven by an overall vision for development.

5.1.5 The North Staffordshire Regeneration Partnership Business Plan establishes the aim to

promote and develop a quality housing range and offer, as part of an over-arching ambition to create sustainable communities and encourage economic growth. This mission statement on the sub-regional level reflects a series of national and regional policy drivers.

Planning Policy Statement 3: Housing

5.1.6 PPS3 sets out the Government’s national planning policy framework for delivering the

Government’s housing objectives. PPS3 has been developed in response to the Barker Review of Housing Supply in March 2004. The proposals draw on a range of research and consultation exercises. The underlying objective of PPS3 is to initiate the necessary step change in housing delivery to meet the emphasis on increasing supply. The Government

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 26 of 80

hoped to do this by creating and developing a more responsive approach to land supply at a local level. Planning guidance is currently being overhauled by the Coalition Government.

5.1.7 PPS3 set out a series of policy drivers pertinent to the development of new housing, they

include: 5.1.8 Achieving high quality housing - Reflecting policy in Planning Policy Statement 1: Delivering

Sustainable Development, good design should contribute positively to making places better for people. PPS3 indicated that design which is inappropriate for its context, or which fails to take the opportunities available for improving the character and quality of an area and the way it functions, will not be accepted.

5.1.9 PPS3 suggested that Local Planning Authorities should develop a shared vision with their

local communities of the type(s) of residential environments they wish to see and develop design policies that set out the quality of development that will be expected for the local area, aimed at:

• Creating places, streets and spaces which meet the needs of people, are visually

attractive, safe, accessible, functional, inclusive, have their own distinctive identity and maintain and improve local character;

• Promoting designs and layouts which make efficient and effective use of land, including encouraging innovative approaches to help deliver high quality outcomes.

5.1.10 In addition it is set out that Local Planning Authorities should encourage applicants to bring

forward sustainable and environmentally friendly new housing developments and in doing so should reflect the approach set out in the forthcoming PPS on climate change, including on the Code for Sustainable Homes.

5.1.11 Achieving a mix of housing – Drivers of policy on housing mix are dominated by the

requirement to provide for a mixed community. Key characteristics of a mixed community are indicated within PPS3 as being a variety of housing, particularly in terms of tenure and price. Pertinent to much development currently is the provision of housing for a mix of different households such as families with children, single person households and older people.

5.1.12 Regional Spatial Strategies, before their recent abolition, set out the region’s approach to

achieving a good mix of housing. Local Planning Authorities should plan for a mix of housing on the basis of the different types of households that are likely to require housing over the plan period, and with the accent now on “localism” will have responsibility for developing their plans on a purely local basis. This will include having particular regard to:

• Current and future demographic trends and profiles; • The accommodation requirements of specific groups, in particular, families with

children, older and disabled people; • The diverse range of requirements across the area.

5.1.13 Based upon the findings of a Strategic Housing Market Assessment and other local

evidence, Local Planning Authorities should set out in Local Development Documents:

• The likely overall proportions of households that require market or affordable housing, for example, x% market housing and y% affordable housing;

• The likely profile of household types requiring market housing eg multi-person, including families and children (x%), single persons (y%), couples (z%);

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 27 of 80

• The size and type of affordable housing required. 5.1.14 Achieving market housing mix – Local Planning Authorities should plan for the full range of

market housing. In particular one of the key findings of the North Staffordshire SHMA identifying the need to deliver ‘more executive housing in the housing sectors dominated by terraced stock’.

5.1.15 In summary, the local planning policy framework, informed by national drivers, indicates that

developers should bring forward proposals for market housing which reflect the demand and the profile of households requiring market housing in order to sustain mixed communities whilst proposals for affordable housing should reflect the size and type of affordable housing required.

5.1.16 In planning at site level, Local Planning Authorities should ensure that the proposed mix of

housing on large strategic sites reflects the proportions of households that require market or affordable housing and achieves a mix of households as well as a mix of tenure and price.

West Midlands Regional Housing Strategy

5.1.17 Responsibilities for housing planning and delivery significantly shifted to the regional level

following the Sustainable Communities Plan 2003 and the Planning and Compulsory Purchase Act 2004. Regional Housing Boards and Regional Planning Bodies were respectively required to produce a Regional Housing Strategy (RHS) and a Regional Spatial Strategy (RSS) for submission to the Regional Assemblies and Communities and Local Government (CLG). Much of this architecture has been swept away by the Coalition Government and the new arrangements have yet to be announced.

5.1.18 The purpose of the Regional Housing Strategy was to galvanise and apply the principles of

urban and rural renaissance throughout the region’s housing markets. The challenge for the Housing Strategy, in line with the counterpart document Regional Spatial Strategy and policies contained in the Regional Economic Strategy, were to:

• create mixed, balanced and inclusive communities; • assist in the delivery of WMRSS urban and rural renaissance; • influence the development of future housing provision to facilitate and enhance

the economic development of the region; • address the variety of housing needs across a range of specific sectors;

5.1.19 In summary the housing offer in the region should support future economic growth

throughout the region. The Regional Housing Strategy recognised the need to expand the residential offer in both, desirable locations where acute demand and supply imbalances have created affordability constraints through escalating prices, and areas of unpopular and obsolete housing, not meeting the aspirations of modern communities, through the Homes ad Communities Agency (HCA) sponsored HMR Pathfinder.

West Midlands Regional Spatial Strategy

5.1.20 The Planning White Paper, published in May 2007, proposed to streamline the planning

system, strengthen the strategic role of local authorities and importantly ensure that the planning system can cope with the future target to deliver 240,000 new homes per annum. Many of the White Paper’s proposals were included in the Housing and Regeneration Act

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 28 of 80

(2008) whilst others were incorporated in appropriate guidance. As indicated above, much of this will be replaced by a new policy and governance framework.

5.1.21 The West Midlands RSS was initially published in June 2004. Following the publication of the

Phase One Revision in light of the Black Country sub-region by CLG, a revised WMRSS was issued in January 2008 guiding development to 2026. It influenced and was influenced by the economy, housing, transport, the built and natural environment. The RSS helped to define the future role of places, how places work together and ultimately, about the effect places have on the quality of life that people living in, working in or visiting that area experience. As such it provided a broad and long-term development strategy for the Region.

5.1.22 The guiding principals of the RSS were to accomplish more sustainable patterns of

development throughout the region, recognising the key objective to stem the unsustainable out-migration of population, jobs and investment from the Major Urban Areas (MUAs). In order to stem the trend of residualisation within the MUAs, considerable expansion of the type, range and quality of the residential and employment offer is required. Urban Renaissance forms the principal forward strategy in the MUAs in order to meet their economic and social needs by attracting and retaining economically independent households.

5.1.23 The Regional Housing Board anticipated pressure on the existing residential stock from a

rapidly growing population across the region, through principal process of natural growth. The RSS outlined delivery of 365,600 new homes over the next 20 years, regional and sub-regional cities and towns being the principal focus for housing, employment, shopping, leisure, education, health and cultural facilities in the region.

5.1.24 The key spatial priority for the core regional cities will be to manage and spread the benefits

of growth, with targeted investment in housing, transport, social and environmental infrastructure. In a shift towards centralisation of development the major metropolitan areas will be the prime recipients of future growth. The polycentric framework of growth established in the RSS drew particular emphasis on the relationship between areas for residential and economic growth.

5.1.25 The four Major Urban Areas (MUAs) of North Staffordshire, Birmingham/ Solihull, the Black

Country and Coventry contain over half the population of the West Midlands and are therefore the main focus for urban renaissance. The overriding aim is to reverse the trend of outmigration, making the MUAs increasingly attractive places where people want to live, work and invest.

5.1.27 Implementation of urban renaissance throughout the MUAs will be facilitated, as outlined in

Policy UR1, by restructuring ‘land use and transport networks to create employment growth, new residential environments, improved environmental quality, integrated transport and joined up centres’.

5.1.28 The Regional Spatial Strategy indicated that Local Development Frameworks would need to

make provision for continuous delivery of housing to 2021 in line with PPS3. Table 3.1 presents the then housing allocations per annum across the region.

Table 5.1: Housing allocations per annum for the West Midlands planning areas

Planning area to 2007 2007-2011 2011-2021

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 29 of 80

Birmingham 2,300 3,000 3,000

Coventry 650 650 830

Dudley 600 700 975

Herefordshire 800 600 600

Sandwell 900 900 975

Shropshire 1,300 900 900

Solihull 400 400 470

Staffordshire 2,900 2,500 1,600

Stoke-on-Trent 600 600 600

Telford and Wrekin 1,330 1,300 700

Walsall 500 500 825

Warwickshire 2,000 1,500 1,350

Wolverhampton 500 500 825

Worcestershire 1,900 1,200 1,000

MUAs (approx) 6,450 7,250 8,500

Other areas 10,230 8,030 6,150

Total 16,680 15,280 14,650

Source: West Midlands Regional Spatial Strategy January 2008 Community Strategy 2004-2014 5.1.29 This document outlines the long term vision for the city to 2014, developed by the city council

and Local Strategic Partnership (LSP). The vision outlines a, ‘city that provides good quality housing, with good job prospects and wage levels. Where businesses are supported and new businesses are attracted to provide a diverse economy’.

• To create a culture of enterprise and innovation and make Stoke-on-Trent a

good place to do business; • To make Stoke-on-Trent an investment location by removing dereliction and unfit

housing; • To provide new quality jobs for our communities; • To develop the physical infrastructure to drive economic improvement.

5.1.30 The driver behind the setting of individual planning authority targets are the findings of

Strategic Housing Market Assessments as set out in PPS3. The North Staffordshire Strategic Housing Market Assessment was published in December 2008 the key findings and implications for the sub-regional area, comprising Stoke in particular include;

• The need to deliver more executive housing in the sectors dominated by

terraced stock, in terms of the quality and choice of residential environments; • A need for a more flexible planning approach to address the imbalance of

housing stock both current and in the pipeline; • Address the limited housing choice and mix in terms of type and tenure to

achieve sustainable communities, the current housing choice continues to act as a block on the area achieving its wider economic potential

• A continued process of residential ‘leapfrog’ to aspirational markets and neighbourhoods in adjacent markets such as Staffordshire Moorlands for the most economically independent households.

RENEW North Staffordshire Business Plan

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 30 of 80

5.1.31 These thematic findings are echoed in the RENEW NSRP Business Plan in order to create the conditions for sustainable growth. Businesses in the sub-region will, given strategic objectives, increasingly need to compete effectively in a globalised economy by ensuring they can innovate, attract and retain local and graduate skilled labour, have a choice of well located, well connected sites on which to grow.

• Retain and attract population; • Balance the demand and supply of housing; • Transform the urban form and local environment; • Facilitate housing choice and the provision of a quality housing stock; • Promote social cohesion and social mobility, to help achieve sustainable

communities.

5.1.32 The North Staffordshire Regeneration Business Partnership directs regeneration across the three local authorities, the 2008 – 11 Business Plan focussing on the four key areas including;

• Re-development of Stoke-on-Trent city centre, promoting strategic links and development in Newcastle town centre;

• Creating a better, skilled workforce within more knowledge-based companies; • Supporting communities through tackling issues such as worklessness,

improved housing offer and re-vitalised town centres; • Encouraging inward investment and improving the area’s image

‘Make-It’ Stoke-on-Trent / Newcastle-under-Lyme, Staffordshire brand 5.1.33 In line with the aims above, commissioned by the NSRP, the ‘Make-It’ brand aims to promote

the image of North Staffordshire, utilised as a cohesive brand logo by universities, local businesses, public and voluntary sector organisations, in order to reflect and promote local assets. It is hoped that the campaign will support the regeneration plans through attraction of inward investment, visitors and residents to the area. The brand aims to promote local assets such as world class heritage, attractive towns, creative skills, highly-rated higher education centres of learning, green space and a commitment to sustainability.

Newcastle-under-Lyme and Stoke-on-Trent Core Strategy 5.1.34 The joint Newcastle-under-Lyme and Stoke-on-Trent Adopted Core Strategy outlines the

Strategic Vision for the area to be, ‘a prosperous, vibrant, environmentally responsible and successful area of choice for businesses, visitors and residents in the period up to 2026. The outcomes of the strategic aims are envisaged to include reversal of population decline and therefore retention, rising income levels, strengthening housing markets, healthier people with a strong sense of well being and an enhanced reputation. The aims are focussed upon key themes of People, Prosperity, Place and Image.

• Gross total new dwellings to be built in Stoke-on-Trent is 13,500 and in

Newcastle-under-Lyme 6,257 by 2026. These translate as net RSS targets of 11,400 and 5,700 respectively;

• New housing will be focused in the inner urban core, including the city centre and neighbourhoods within the RENEW ‘areas of intervention’;

• Indicative net annual requirements total 570 in Stoke-on-Trent and 285 in Newcastle-under-Lyme over the Plan period. (The planning policy unit have highlighted that in the current climate it is highly unlikely that this level of delivery

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 31 of 80

will be achieved, instead a putative figure of 50% of 600 units is taken as the anticipated rate for 2008/09).

Staffordshire Moorlands Submission Core Strategy 5.1.35 The Staffordshire Moorlands Core Strategy has undergone a series of iterations following

consideration of responses through the consultation process. The latest Addendum to the Submission Version of the Core Strategy incorporated alterations to distribution of housing allocations across the main settlements of the district. It is anticipated that the Inspectorate examination will take place in June / July 2010 with full adoption in December 2010. The central theme of the Vision for Staffordshire Moorlands is predicated on the aspiration for the authority to become an exceptional place to live, work and visit. This translates into spatial and development objectives as part of a wider regenerated North Staffordshire to balance the need for sustainable growth and enhance the District’s natural and built assets.

• Latest population projections forecast the need to deliver 6,180 dwellings

between 2006 – 2026 in light of natural growth and projected employment growth of 15% equivalent to 5,192 jobs. This is considered in light of the RSS alternative growth options between a lower and higher range of 5,500 – 7,500 dwelling s between 2001 – 2026;

• As a preferred development option, new housing to be focused in the three main settlements of Leek, Biddulph and Cheadle, including the neighbourhoods within the RENEW ‘areas of intervention’;

• The spatial objectives for the individual settlements, underpinned by sustainable forms of development include the aims to, ‘create distinctive, sustainable, self-supporting settlements’; ‘meet the needs of the communities’; ‘encourage a strong, prosperous and diverse economy’; ‘maintain a quality environment and special places’.

arc4 RENEW NSRP Executive Housing Market Research Sept 2010 32 of 80

Section 6 Demand for Executive Housing Factors that will influence future demand - Household income and ACORN profiles 6.1.1 This section examines in detail the key drivers of demand pertinent to the market for

executive housing. An executive property is underpinned by the wealth of the housing purchaser. Household income is one measure of a household’s wealth and ability to access the executive housing market. In the most part potential purchasers of executive properties have considerable equity in the form of existing property to trade upwards, savings or windfalls. In terms of household income, there is a distinct correlation between those wards recording the highest property transaction levels and values, to the highest average household incomes. This pattern is reflected in map form in Appendix D.

6.1.2 Those wards recording the highest household income levels, in excess of £50,000, are

Trentham and Hanford, Meir Park and Sandon in Stoke. In Newcastle-under-Lyme they are Loggerheads and Whitmore, Halmerend and Westlands. In Staffordshire Moorlands Horton, Dane and Bagnall and Stanley are amongst a wider distribution of higher average household incomes in the authority.

6.1.3 In terms of relative affluence, Appendix C lists the proportion of total resident population by