ratemaking asops

DESCRIPTION

Ratemaking ASOPS. By the CAS Committee on Professionalism Education. WHY ASOPs?. As a CAS Member You Are Bound By: Actuarial Standards of Practice (ASOPs) Code of Professional Conduct Statement of Principles Qualification Standards Continuing Education Requirements - PowerPoint PPT PresentationTRANSCRIPT

Ratemaking Ratemaking ASOPSASOPS

By the CAS Committee on By the CAS Committee on Professionalism EducationProfessionalism Education

WHY ASOPs?WHY ASOPs?

As a CAS Member You Are Bound By:As a CAS Member You Are Bound By:Actuarial Standards of Practice (ASOPs)Actuarial Standards of Practice (ASOPs)Code of Professional ConductCode of Professional ConductStatement of PrinciplesStatement of PrinciplesQualification StandardsQualification StandardsContinuing Education RequirementsContinuing Education Requirements

As an Actuarial Candidate You Are As an Actuarial Candidate You Are Bound By:Bound By:Code of Professional Ethics for CandidatesCode of Professional Ethics for Candidates

How were ASOPs How were ASOPs created?created?

IS AFFILIATEDWITH

CASUALTYACTUARIAL

SOCIETY

CASUALTYACTUARIAL

SOCIETY

STATEMENTSOF

PRINCIPLES

STATEMENTSOF

PRINCIPLES

STANDARDSOF

PRACTICE

STANDARDSOF

PRACTICE

ACTUARIALSTANDARDS

BOARD

ACTUARIALSTANDARDS

BOARD

AMERICANACADEMY OFACTUARIES

AMERICANACADEMY OFACTUARIES

PROMULGATES

ARE USED BY

HAS FORMED

PROMULGATES

How to Read an How to Read an ASOPASOP

ASOPs have a consistent format:ASOPs have a consistent format: Table of ContentsTable of Contents Cover LetterCover Letter Section 1: Purpose, Scope, and Effective DateSection 1: Purpose, Scope, and Effective Date Section 2: DefinitionsSection 2: Definitions Section 3: Analysis of Issues and Section 3: Analysis of Issues and

Recommended PracticesRecommended Practices Section 4: Communications and DisclosuresSection 4: Communications and Disclosures Appendix 1: Background and Current Appendix 1: Background and Current

PracticesPractices Appendix 2: Comments/Responses on DraftsAppendix 2: Comments/Responses on Drafts

Applicability Guidelines for Applicability Guidelines for Actuarial Standards of Practice – Actuarial Standards of Practice –

As of Dec 2009As of Dec 2009

Question #1Question #1

True or False: Are the applicability True or False: Are the applicability guidelines clear, concise, and guidelines clear, concise, and complete?complete?

TRUETRUE

FALSEFALSE

Answer #1Answer #1

True is an Incorrect AnswerTrue is an Incorrect Answer

Press to retake Question #1

Answer #1Answer #1

The correct answer is False:The correct answer is False: These applicability guidelines should These applicability guidelines should

not be considered complete. They are not be considered complete. They are general recommendations and not the general recommendations and not the final word. Every actuary is bound by final word. Every actuary is bound by every ASOP regardless if it’s on the list every ASOP regardless if it’s on the list for your practice area in the for your practice area in the applicability guidelines.applicability guidelines.

RATEMAKING ACTUARIAL RATEMAKING ACTUARIAL

STANDARDS OF PRACTICESTANDARDS OF PRACTICEASOP # 12 Risk Classification (for All Practice ASOP # 12 Risk Classification (for All Practice Areas) Areas)

ASOP # 13 Trending Procedures in ASOP # 13 Trending Procedures in Property/Casualty InsuranceProperty/Casualty Insurance

ASOP # 25 Credibility Procedures Applicable to ASOP # 25 Credibility Procedures Applicable to Accident and Health, Group Term Life, and Accident and Health, Group Term Life, and Property/Casualty Coverages Property/Casualty Coverages

ASOP # 29 Expense Provisions in Property/Casualty ASOP # 29 Expense Provisions in Property/Casualty Insurance RatemakingInsurance Ratemaking

ASOP # 30 Treatment of Profit and Contingency ASOP # 30 Treatment of Profit and Contingency Provisions and the Cost of Capital in Provisions and the Cost of Capital in Property/Casualty Insurance Ratemaking Property/Casualty Insurance Ratemaking

ASOP # 38 – Using Models Outside the Actuary’s ASOP # 38 – Using Models Outside the Actuary’s Area of Expertise Area of Expertise

ASOP # 39 Treatment of Catastrophe Losses in ASOP # 39 Treatment of Catastrophe Losses in Property/Casualty Insurance Ratemaking Property/Casualty Insurance Ratemaking

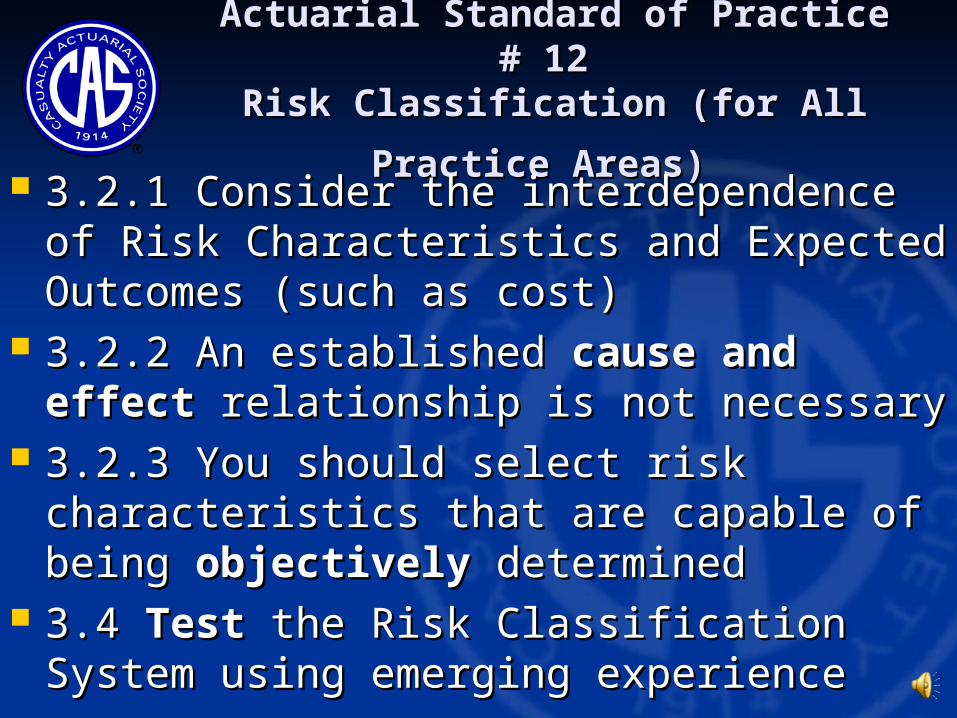

Actuarial Standard of Practice # Actuarial Standard of Practice # 12 12

Risk Classification (for All Risk Classification (for All

Practice Areas)Practice Areas) 3.2.1 Consider the interdependence of 3.2.1 Consider the interdependence of Risk Characteristics and Expected Risk Characteristics and Expected Outcomes (such as cost) Outcomes (such as cost)

3.2.2 An established 3.2.2 An established cause and effectcause and effect relationship is not necessary relationship is not necessary

3.2.3 You should select risk 3.2.3 You should select risk characteristics that are capable of being characteristics that are capable of being objectivelyobjectively determined determined

3.4 3.4 Test Test the Risk Classification System the Risk Classification System using emerging experienceusing emerging experience

Question #2Question #2

True or False: An established cause True or False: An established cause and effect relationship is necessary and effect relationship is necessary for ASOP #12 Risk Classification for for ASOP #12 Risk Classification for All Practice AreasAll Practice Areas TRUETRUE

FALSEFALSE

Answer #2Answer #2

True is an Incorrect AnswerTrue is an Incorrect Answer

Press to retake Question #2

Answer #2Answer #2

The correct answer is False:The correct answer is False: An established cause and effect An established cause and effect

relationship is not necessary since the relationship is not necessary since the task force recognized that there can be task force recognized that there can be significant relationships between risk significant relationships between risk characteristics and expected outcomes characteristics and expected outcomes where a cause-and-effect relationship where a cause-and-effect relationship cannot be demonstrated.cannot be demonstrated.

Actuarial Standard of Practice # Actuarial Standard of Practice # 13 13

Trending Procedures in Trending Procedures in Property/Casualty InsuranceProperty/Casualty Insurance

3.1 You should identify the intended 3.1 You should identify the intended purpose or usepurpose or use of the trending of the trending procedure: ratemaking, reserving, procedure: ratemaking, reserving, valuations, underwriting, and/or valuations, underwriting, and/or marketing. marketing.

3.2 The data can consist of historical 3.2 The data can consist of historical insurance or non-insurance insurance or non-insurance information.information.

3.3 Consider economic and social 3.3 Consider economic and social influencesinfluences

Actuarial Standard of Practice # Actuarial Standard of Practice # 25 25

Credibility Procedures Applicable to Credibility Procedures Applicable to Accident and Health, Group Term Accident and Health, Group Term

Life, and Property/Casualty CoveragesLife, and Property/Casualty Coverages 3.2 Consider 3.2 Consider various methodsvarious methods of of

determining credibility.determining credibility. 3.3 Carefully select 3.3 Carefully select related experiencerelated experience to to

be blended with the subject experience; it be blended with the subject experience; it should have frequency, severity, or other should have frequency, severity, or other determinable similar characteristics determinable similar characteristics

3.4 3.4 Informed Actuarial JudgmentInformed Actuarial Judgment — The — The use of credibility procedures is not always use of credibility procedures is not always a precise mathematical process.a precise mathematical process.

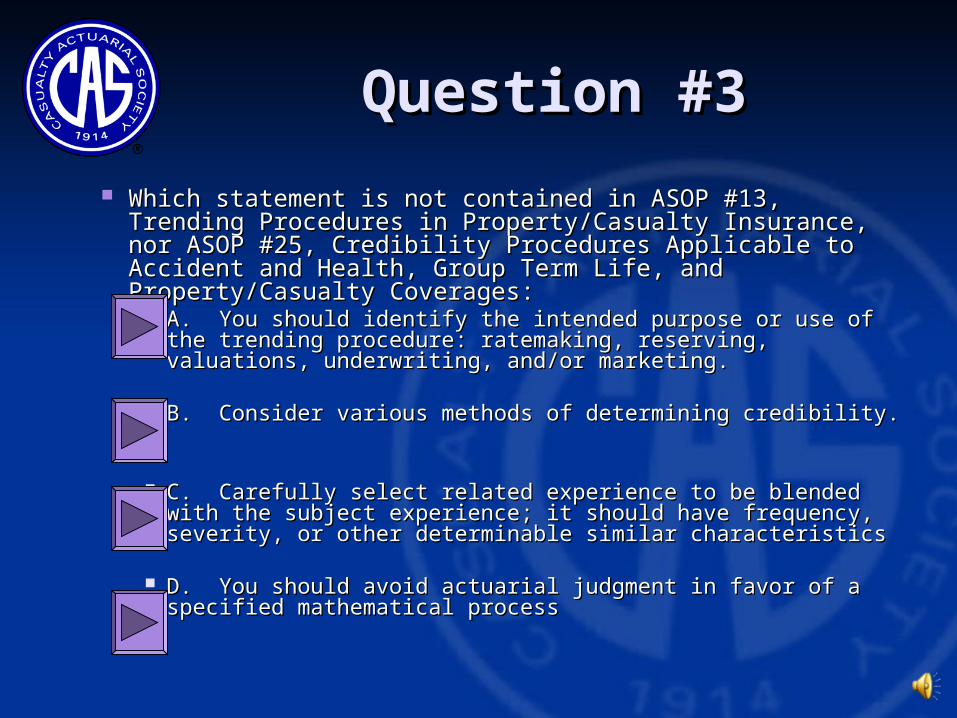

Question #3Question #3

Which statement is not contained in ASOP #13, Trending Which statement is not contained in ASOP #13, Trending Procedures in Property/Casualty Insurance, nor ASOP Procedures in Property/Casualty Insurance, nor ASOP #25, Credibility Procedures Applicable to Accident and #25, Credibility Procedures Applicable to Accident and Health, Group Term Life, and Property/Casualty Health, Group Term Life, and Property/Casualty Coverages:Coverages:

A. You should identify the intended purpose or use of the A. You should identify the intended purpose or use of the trending procedure: ratemaking, reserving, valuations, trending procedure: ratemaking, reserving, valuations, underwriting, and/or marketing. underwriting, and/or marketing.

B. Consider various methods of determining credibility.B. Consider various methods of determining credibility.

C. Carefully select related experience to be blended with C. Carefully select related experience to be blended with the subject experience; it should have frequency, severity, or the subject experience; it should have frequency, severity, or other determinable similar characteristics other determinable similar characteristics

D. You should avoid actuarial judgment in favor of a D. You should avoid actuarial judgment in favor of a specified mathematical processspecified mathematical process

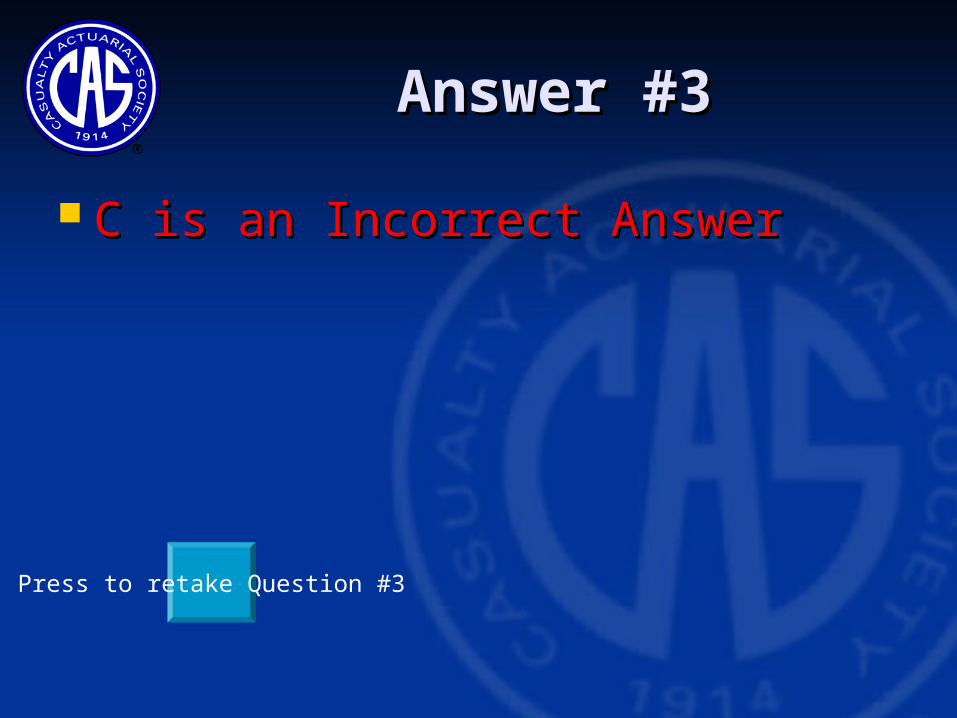

Answer #3Answer #3

A is an Incorrect AnswerA is an Incorrect Answer

Press to retake Question #3

Answer #3Answer #3

B is an Incorrect AnswerB is an Incorrect Answer

Press to retake Question #3

Answer #3Answer #3

C is an Incorrect AnswerC is an Incorrect Answer

Press to retake Question #3

Answer #3Answer #3

The correct answer is D:The correct answer is D: Informed actuarial judgment is Informed actuarial judgment is

requested because the use of credibility requested because the use of credibility procedures is not always a precise procedures is not always a precise mathematical process.mathematical process.

Actuarial Standard of Practice # Actuarial Standard of Practice # 29 29

Expense Provisions inExpense Provisions inProperty/Casualty Insurance Property/Casualty Insurance

RatemakingRatemaking 3.2 + 3.6 You 3.2 + 3.6 You shouldshould determine provisions for determine provisions for

projected: projected: loss adjustment expenses (3.2) loss adjustment expenses (3.2) commission and brokerage fees (3.2) commission and brokerage fees (3.2) other acquisition expenses (3.2) other acquisition expenses (3.2) general administrative expenses (3.2) general administrative expenses (3.2) taxes, licenses, and fees (3.2) taxes, licenses, and fees (3.2) provision for residual market and statutory provision for residual market and statutory

assessments (3.6)assessments (3.6) 3.3 + 3.5 + 3.7 You 3.3 + 3.5 + 3.7 You may may also:also:

amortize start-up costs amortize start-up costs add provision for policyholder dividendsadd provision for policyholder dividends include the cost of Reinsurance include the cost of Reinsurance

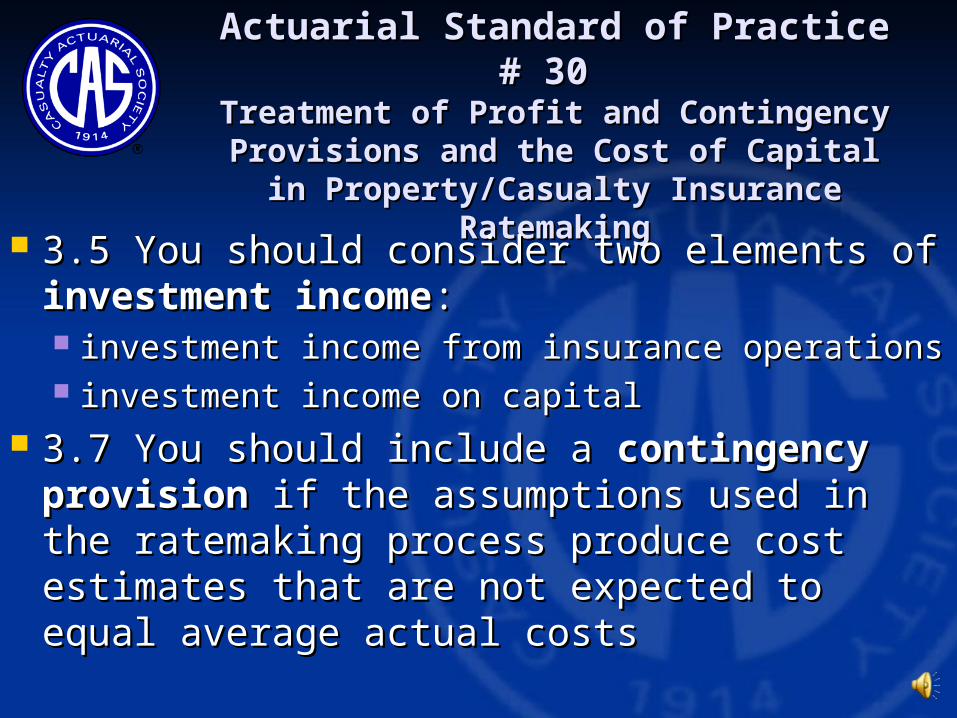

Actuarial Standard of Practice # Actuarial Standard of Practice # 30 30

Treatment of Profit and Contingency Treatment of Profit and Contingency Provisions and the Cost of Capital in Provisions and the Cost of Capital in

Property/Casualty Insurance Property/Casualty Insurance RatemakingRatemaking

3.5 You should consider two elements of 3.5 You should consider two elements of investment incomeinvestment income: : investment income from insurance operations investment income from insurance operations investment income on capitalinvestment income on capital

3.7 You should include a 3.7 You should include a contingency contingency provisionprovision if the assumptions used in the if the assumptions used in the ratemaking process produce cost ratemaking process produce cost estimates that are not expected to equal estimates that are not expected to equal average actual costsaverage actual costs

Actuarial Standard of Practice # Actuarial Standard of Practice # 3838

Using Models Outside the Using Models Outside the Actuary’s Area of ExpertiseActuary’s Area of Expertise

3.1 You 3.1 You shouldshould do all of the following when do all of the following when using models that incorporate specialized using models that incorporate specialized knowledge outside of your own area of knowledge outside of your own area of expertise: expertise: a. determine appropriate reliance on experts; a. determine appropriate reliance on experts; b. have a basic understanding of the model; b. have a basic understanding of the model; c. evaluate whether the model is appropriate for the c. evaluate whether the model is appropriate for the

intended application; intended application; d. determine that appropriate validation has d. determine that appropriate validation has

occurred; and occurred; and e. determine the appropriate use of the model. e. determine the appropriate use of the model.

Question #4Question #4

Which of the following do you NOT need to do Which of the following do you NOT need to do when using models that incorporate specialized when using models that incorporate specialized knowledge outside of your own area of expertise : knowledge outside of your own area of expertise : A. determine appropriate reliance on expertsA. determine appropriate reliance on experts

B. have a thorough understanding of the modelB. have a thorough understanding of the model

C. evaluate whether the model is appropriate for the C. evaluate whether the model is appropriate for the intended applicationintended application

D. determine that appropriate validation has occurredD. determine that appropriate validation has occurred

E. determine the appropriate use of the modelE. determine the appropriate use of the model

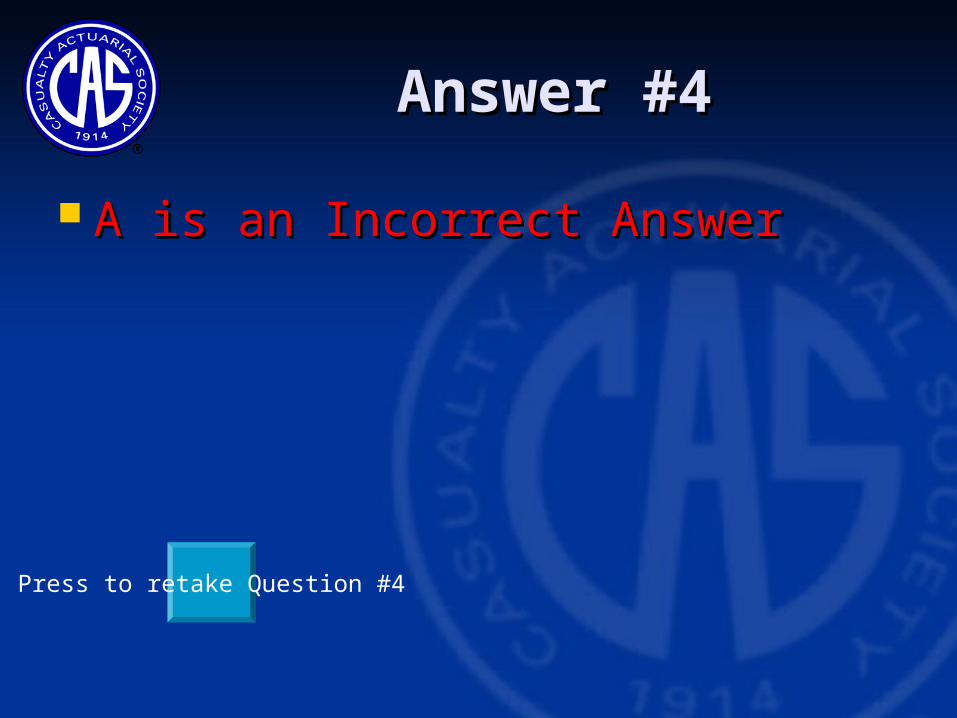

Answer #4Answer #4

A is an Incorrect AnswerA is an Incorrect Answer

Press to retake Question #4

Answer #4Answer #4

C is an Incorrect AnswerC is an Incorrect Answer

Press to retake Question #4

Answer #4Answer #4

D is an Incorrect AnswerD is an Incorrect Answer

Press to retake Question #4

Answer #4Answer #4

E is an Incorrect AnswerE is an Incorrect Answer

Press to retake Question #4

Answer #4Answer #4

The correct answer is B:The correct answer is B: You do not necessarily have to have a You do not necessarily have to have a

thorough understanding of the model; thorough understanding of the model; you must have a basic understanding you must have a basic understanding thoughthough

Actuarial Standard of Practice # Actuarial Standard of Practice # 3939

Treatment of Catastrophe Losses Treatment of Catastrophe Losses in in

Property/Casualty Insurance Property/Casualty Insurance Ratemaking Ratemaking 3.3.1 When using 3.3.1 When using historical insurance historical insurance

datadata you should: you should: Consider data applicabilityConsider data applicability Adjust to reflect future conditions Adjust to reflect future conditions Modify it to stabilize outcomes and reduce Modify it to stabilize outcomes and reduce

sensitivitysensitivity Vary trends where necessaryVary trends where necessary

3.3.2 You should consider using catastrophe 3.3.2 You should consider using catastrophe modelsmodels if if the available historical data the available historical data doesn’t represent the exposure doesn’t represent the exposure

RATEMAKING ACTUARIAL RATEMAKING ACTUARIAL

STANDARDS OF PRACTICESTANDARDS OF PRACTICEASOP # 12 Risk Classification (for All Practice ASOP # 12 Risk Classification (for All Practice Areas) Areas)

ASOP # 13 Trending Procedures in ASOP # 13 Trending Procedures in Property/Casualty InsuranceProperty/Casualty Insurance

ASOP # 25 Credibility Procedures Applicable to ASOP # 25 Credibility Procedures Applicable to Accident and Health, Group Term Life, and Accident and Health, Group Term Life, and Property/Casualty Coverages Property/Casualty Coverages

ASOP # 29 Expense Provisions in ASOP # 29 Expense Provisions in Property/Casualty Insurance RatemakingProperty/Casualty Insurance Ratemaking

ASOP # 30 Treatment of Profit and Contingency ASOP # 30 Treatment of Profit and Contingency Provisions and the Cost of Capital in Provisions and the Cost of Capital in Property/Casualty Insurance Ratemaking Property/Casualty Insurance Ratemaking

ASOP # 38 – Using Models Outside the Actuary’s ASOP # 38 – Using Models Outside the Actuary’s Area of Expertise Area of Expertise

ASOP # 39 Treatment of Catastrophe Losses in ASOP # 39 Treatment of Catastrophe Losses in Property/Casualty Insurance Ratemaking Property/Casualty Insurance Ratemaking

CONGRATULATIOCONGRATULATIONSNS

You have successfully completed You have successfully completed this session on the Ratemaking this session on the Ratemaking

ASOPsASOPs