pvr ltd

TRANSCRIPT

Experience the difference”

Group Members

Arpit Jain - 80

Zil Shah - 81

Khyati Patel - 82

Nikita Bhasin - 83

Deeviash Sharma - 84

Kalpesh Kerai - 85

Table of Content Vision of the company

Introduction

History of the company

Segmentation & Revenue

Competitive Analysis

Acquisitions and mergers

Financial Status

Ratio analysis

Conclusion

Vision of the Company

• The Company's long-term vision is to excel in the retail entertainment domain to maintain its leadership position in the cinema exhibition business

Introduction

• Most premium film entertainment Company in India.• Listed as the “Most Trusted Brand” in the Category of

Entertainment by the “Brand Trust Report, 2013”.

• Incorporated on April 26, 1995 under the Companies Act as "Priya Village Roadshow Limited“.

• Certificate of commencement of business on December 4, 1995.

• On June 28, 2002 "Priya Village Roadshow Limited“ changed to "PVR Limited" consequent to the exit of Village Roadshow Limited from PVR.

History of the company

1994

• Joint venture agreement executed between Village Roadshow Limited

1996

• 1,199,300 Equity Shares of pvr issued to Ajay Bijli Motor Finance Limited

1997

• Computerized box office operations

2004

• Opened India's largest Multiplex Cinema

2005

• PVR Ltd, a multiplex cinema operator, has fixed its IPO price at Rs 225

2009

• Merged with Sunrise Infotainment Pvt. Ltd • PVR acquires DLF's DT Cinemas for Rs 60 cr

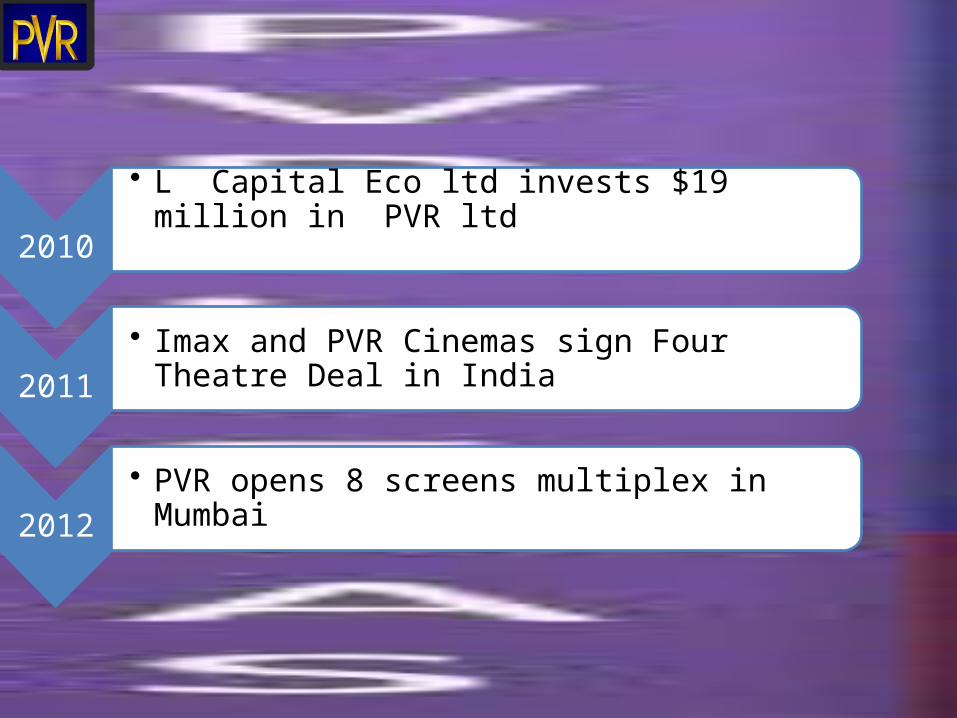

2010

• L Capital Eco ltd invests $19 million in PVR ltd

2011

• Imax and PVR Cinemas sign Four Theatre Deal in India

2012

• PVR opens 8 screens multiplex in Mumbai

Segmentation

Revenue

Competitive Analysis

28%

20%

16%

5%

5%

3%

23%

Market share (%)

PVRInoxBig Cinemas CinepolisFun CinemasSRS cinemasOthers

Mergers , Acquisitions & Expansion

• L Capital Eco ltd invests $19 million in PVR ltd

• Acquisition of Cinemax – a master stroke

• Only player with aggressive Expansion plans

Financial Status

2010 2011 2012 2013 20140

200

400

600

800

1000

1200

1400

309401

482

678

1285

TOTAL REVENUE

2010 2011 2012 2013 20140

200

400

600

800

1000

1200

1400

305391

468

670

1271

INCOME FROM SALES

2010 2011 2012 2013 20140

2

4

6

8

10

12

14

16

4

10

14

8

14

OTHER INCOME

2010 2011 2012 2013 20140

10

20

30

40

50

60

70

0.26

17

28

5558

PAT

2010 2011 2012 2013 20140

200

400

600

800

1000

1200

276339

398

565

1071

EXPENDITURE

2010 2011 2012 2013 20140

200

400

600

800

1000

1200

384449 442

975894

TOTAL ASSETS

Ratio Analysis• CURRENT RATIO = CURRENT ASSETS • CURRENT LIABILITIES

2010 2011 2012 2013 20140

0.5

1

1.5

2

2.5

3

1.4

2.4

1.591.31

0.99

CURRENT RATIO

DEBT – EQUITY RATIO = DEBT (BORROWED FUNDS) EQUITY (OWNERS FUNDS)

2010 2011 2012 2013 20140

0.2

0.4

0.6

0.8

1

1.2

1.4

0.550.56 0.62

0.52

1.28

DEBT-EQUITY RATIO

DEBTORS VELOCITY RATIO = ___365 DAYS__ DEBTORS TURNOVER RATIO

DEBTORS TUNROVER RATIO = ___CREDIT SALES___ AVG. DEBTORS + AVG. BILLS RECEIVABLES

2010 2011 2012 2013 20140

5

10

15

20

25

30

35

40

25

29

25

30

37

DEBTORS VELOCITY RATIO (DAYS)

TOTAL ASSETS TURNOVER RATIO = SALES TOTAL ASSETSTOTAL ASSETS = FIXED ASSETS + LONG TERM INVESTMENTS + CURRENT ASSETS

2010 2011 2012 2013 20140

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

0.80.88

1.11

0.69

1.69

TOTAL ASSETS TURNOVER RATIO

EARNING PER SHARE = NPAT – PREFERENCE DIVIDEND NUMBER OF EQUITY SHARES

2010 2011 2012 2013 20140

2

4

6

8

10

12

14

16

0.1

6.02

10.85

13.8514.08

EARNING PER SHARE (RS)

THANKYOU