putting all the pieces of loan compliance together rebecca ketter, ccbco 6/19/09

Post on 20-Dec-2015

213 views

TRANSCRIPT

Putting all the pieces of loan compliance togetherRebecca Ketter, CCBCO 6/19/09

A Big Year for ChangesUnparalleled crisis brings

unparalleled reaction…

–HOEPA/HMDA

–TILA

–RESPA

–HVCC

–SAFE

An alphabet soup of changes!!!

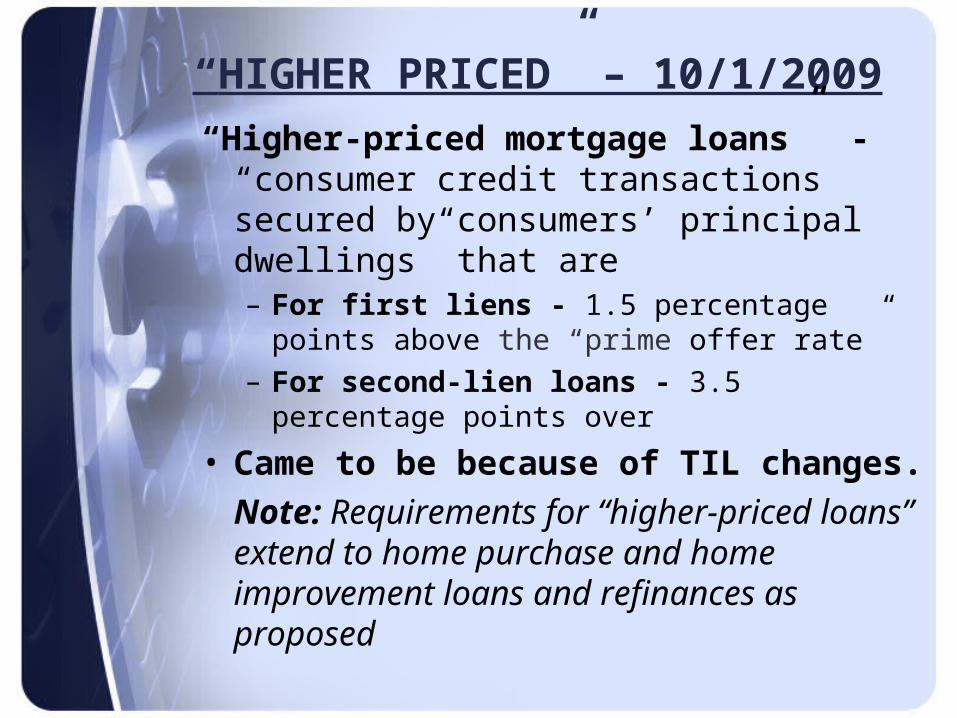

“HIGHER PRICED” – 10/1/2009

“Higher-priced mortgage loans” - “consumer credit transactions secured by consumers’ principal dwellings” that are– For first liens - 1.5 percentage points above

the “prime offer rate” – For second-lien loans - 3.5 percentage

points over

• Came to be because of TIL changes.

Note: Requirements for “higher-priced loans” extend to home purchase and home improvement loans and refinances as proposed

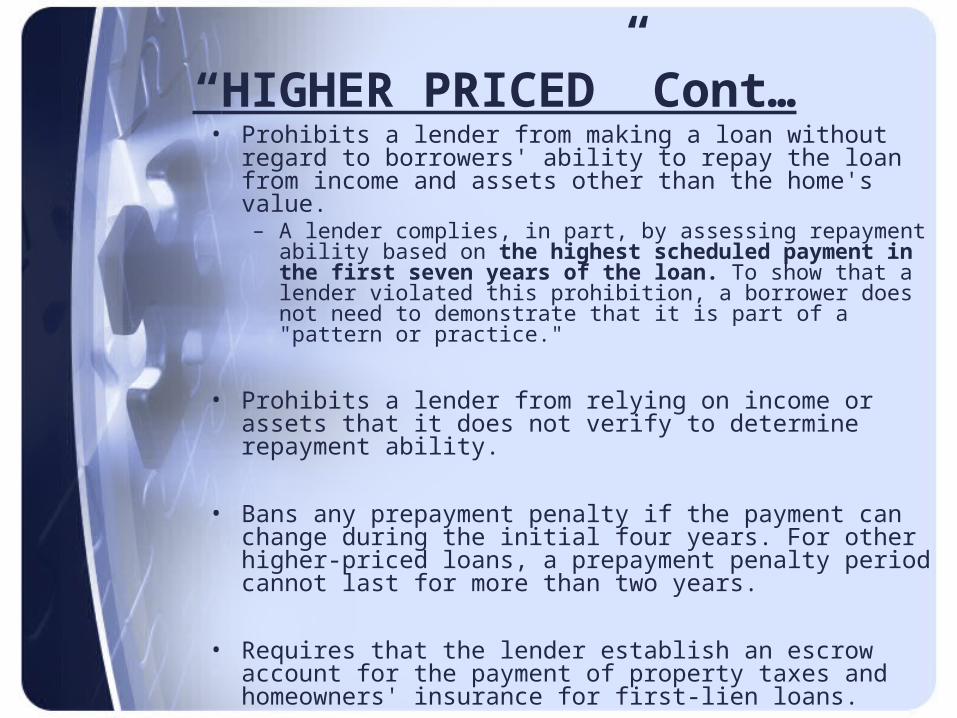

“HIGHER PRICED” Cont…• Prohibits a lender from making a loan without regard to

borrowers' ability to repay the loan from income and assets other than the home's value. – A lender complies, in part, by assessing repayment ability

based on the highest scheduled payment in the first seven years of the loan. To show that a lender violated this prohibition, a borrower does not need to demonstrate that it is part of a "pattern or practice."

• Prohibits a lender from relying on income or assets that it does not verify to determine repayment ability.

• Bans any prepayment penalty if the payment can change during the initial four years. For other higher-priced loans, a prepayment penalty period cannot last for more than two years.

• Requires that the lender establish an escrow account for the payment of property taxes and homeowners' insurance for first-lien loans.

HMDA - effective 10/1/09Compliance is mandatory for loan applications taken on

or after October 1, 2009 and for all loans that close on or after January 1, 2010 (regardless of the application date).

Currently a HMDA rate spread is reported if the yield between the APR and Treasury Securities is 3% on first liens and 5% on subordinate liens.

This will be replaced with the “Average Prime Offer Rate” and will now be a rate of 1.5% for first liens and 3.5% for subordinate liens.

HMDA reporting for 2009 shall have January to September 30 applications reported as the 3 to 5 rate spread, and applications taken after October 1 reported using the new 1.5 to 3.5 rate spreads.

Truth In Lending changes• Apply to dwelling-secured consumer loans for

which a creditor receives an application on or after July 30, 2009.

• Early Disclosures are no longer just for purchases; Truth in Lending now includes:– Refinances– Home Equity (closed-end)

• Dwelling secured = no longer just the primary dwelling– 2nd home, for example– Business purpose is still exempt

Early disclosure timing• Deliver or mail no later than three (3)

business days after we receive the application.

– Applies to purchase.

– Applies to Non-purchase.

– Applies for primary dwelling.

– Applies for a dwelling other than the primary dwelling.

Cannot Charge Fees!!!

We cannot charge the customer any fees, other than a credit report feeUntil early disclosures are

received by the customer.

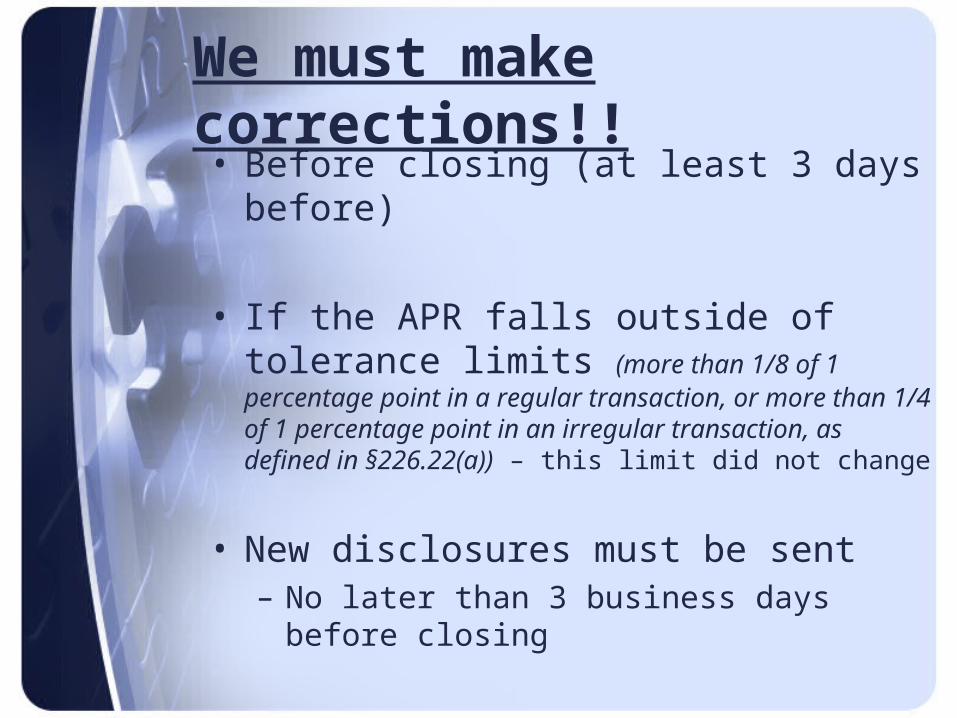

We must make corrections!!• Before closing (at least 3 days before)

• If the APR falls outside of tolerance limits (more than 1/8 of 1 percentage point in a regular transaction, or more than 1/4 of 1 percentage point in an irregular transaction, as defined in §226.22(a)) – this limit did not change

• New disclosures must be sent– No later than 3 business days before closing

We must wait!

Seven (7) business day waiting period– Creditors must wait

seven business days after they provide the early disclosures before closing the loan

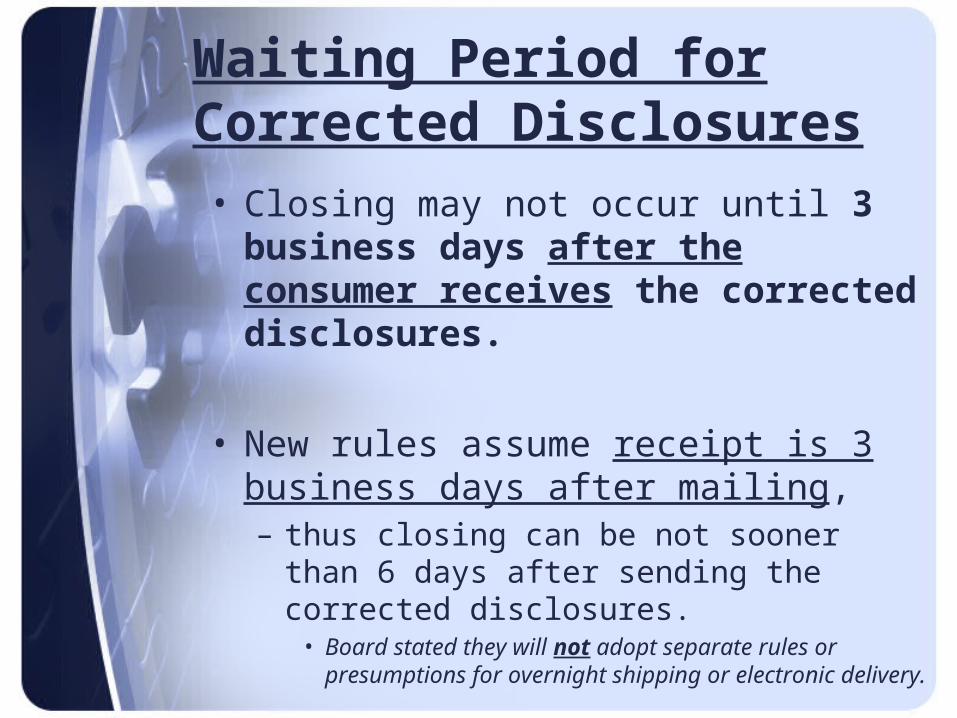

Waiting Period for Corrected Disclosures• Closing may not occur until 3 business

days after the consumer receives the corrected disclosures.

• New rules assume receipt is 3 business days after mailing, – thus closing can be not sooner than 6 days

after sending the corrected disclosures.• Board stated they will not adopt separate rules or

presumptions for overnight shipping or electronic delivery.

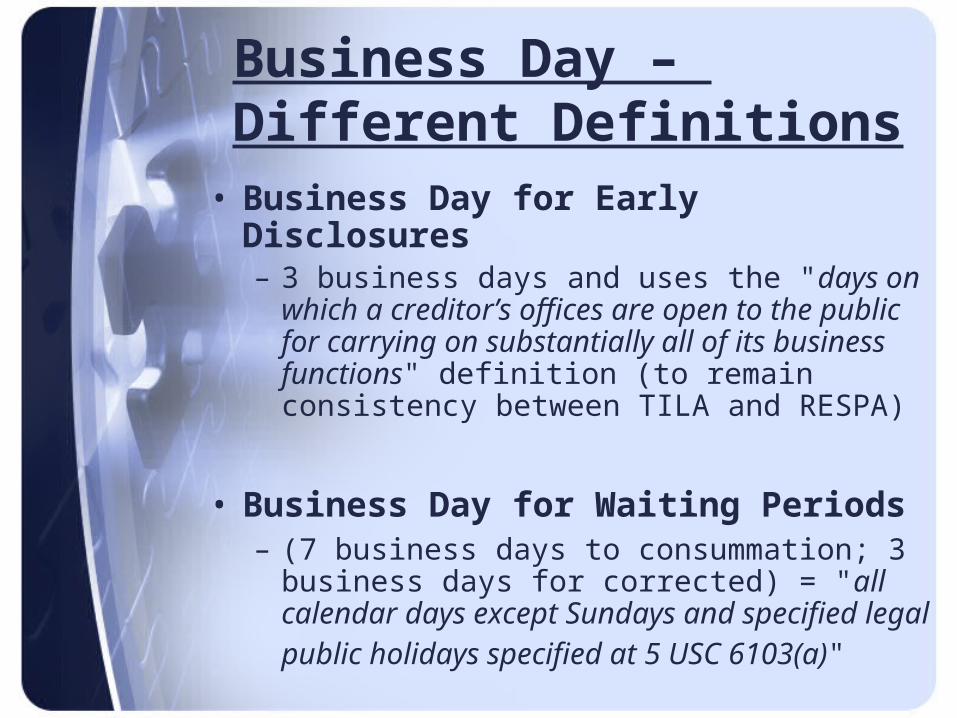

Business Day – Different Definitions

• Business Day for Early Disclosures – 3 business days and uses the "days on which

a creditor’s offices are open to the public for carrying on substantially all of its business functions" definition (to remain consistency between TILA and RESPA)

• Business Day for Waiting Periods – (7 business days to consummation; 3

business days for corrected) = "all calendar days except Sundays and specified legal public holidays specified at 5 USC 6103(a)"

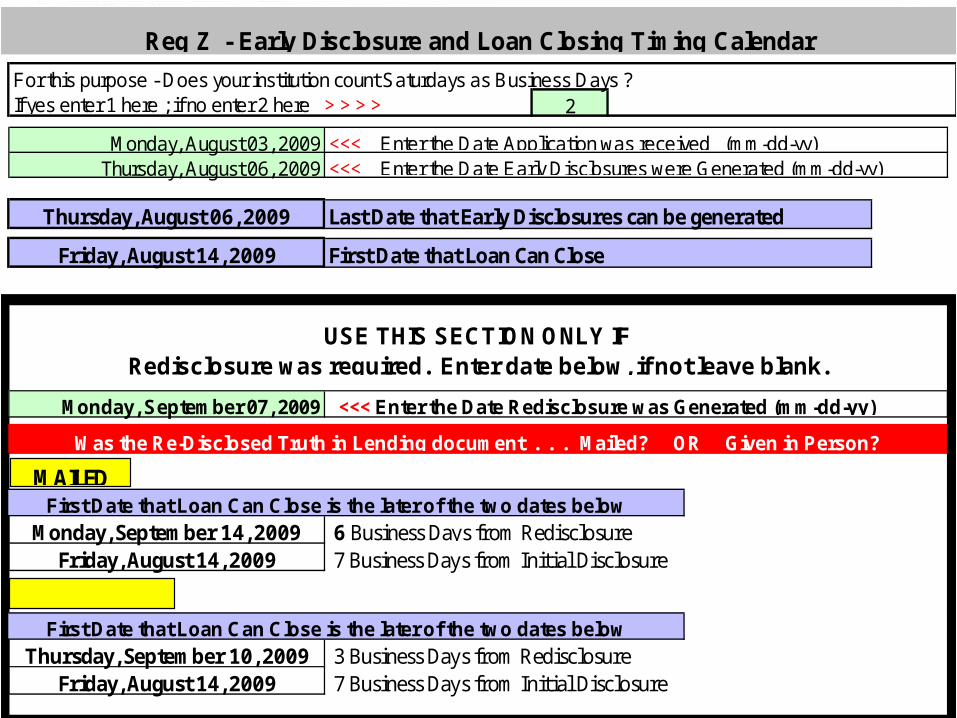

For this purpose - Does your institution count Saturdays as Business Days ?If yes enter 1 here ; if no enter 2 here > > > > 2

Monday, August 03, 2009 <<< Enter the Date Application was received (mm-dd-yy)Thursday, August 06, 2009 <<< Enter the Date Early Disclosures were Generated (mm-dd-yy)

Thursday, August 06, 2009 Last Date that Early Disclosures can be generated

Friday, August 14, 2009 First Date that Loan Can Close

Monday, September 07, 2009 <<< Enter the Date Redisclosure was Generated (mm-dd-yy)

First Date that Loan Can Close is the later of the two dates below

Monday, September 14, 2009 6 Business Days from RedisclosureFriday, August 14, 2009 7 Business Days from Initial Disclosure

First Date that Loan Can Close is the later of the two dates below

Thursday, September 10, 2009 3 Business Days from RedisclosureFriday, August 14, 2009 7 Business Days from Initial Disclosure

Reg Z - Early Disclosure and Loan Closing Timing Calendar

USE THIS SECTION ONLY IFRedisclosure was required. Enter date below, if not leave blank.

Was the Re-Disclosed Truth in Lending document . . . Mailed? OR Given in Person?

MAILED

Given In Person

Clear as mud?

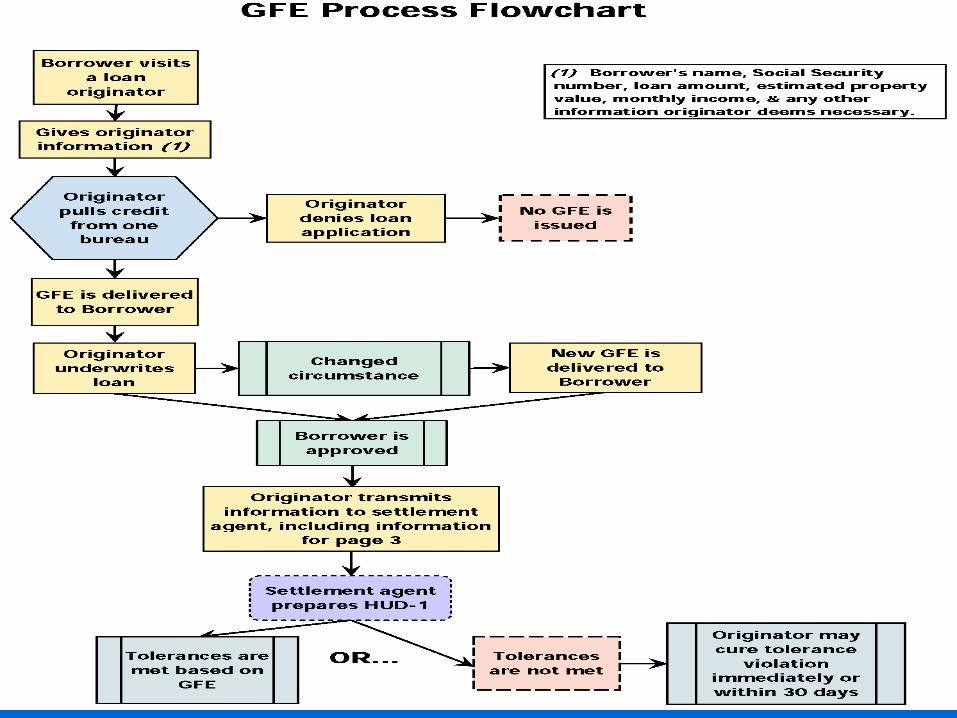

January 1, 2010 - RESPA• New Application Definition

• New Good Faith Estimate (now 3 pages long)

• New HUD-1 (also now 3 pages in length) – New HUD-1a

• Servicing disclosure – was effective January 16, 2009

Principles of RESPA Reform

• Help consumers shop for the best loan

• Shopping leads to greater competition & lower prices

• Key final terms of the loan disclosed to the borrower at closing

• Preserve a competitive market for all settlement

service providers

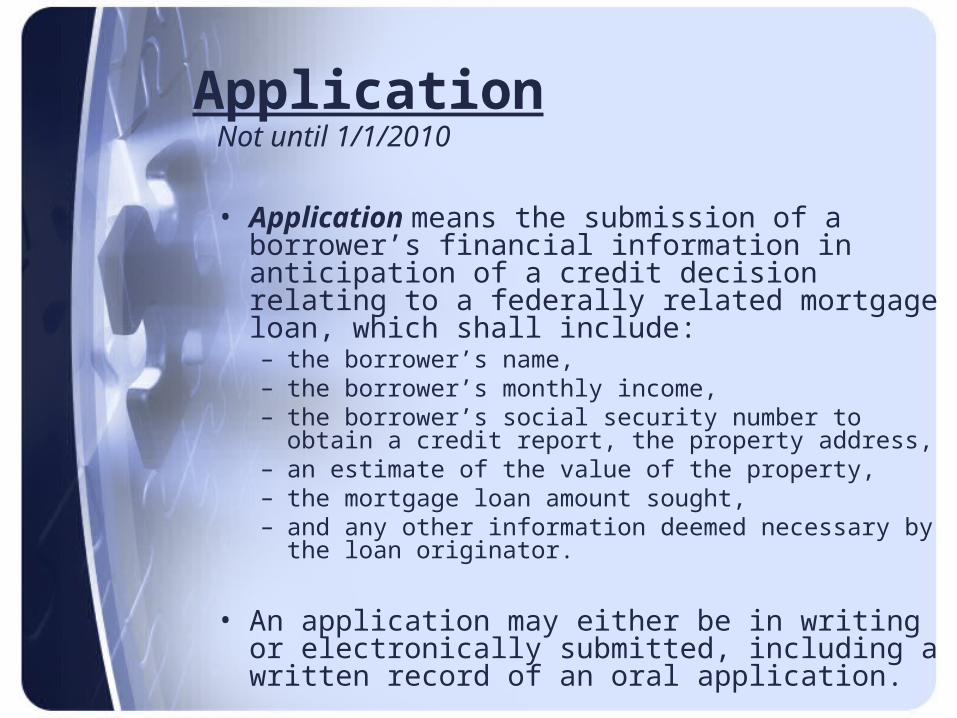

ApplicationNot until 1/1/2010

• Application means the submission of a borrower’s financial information in anticipation of a credit decision relating to a federally related mortgage loan, which shall include: – the borrower’s name, – the borrower’s monthly income, – the borrower’s social security number to obtain a

credit report, the property address, – an estimate of the value of the property, – the mortgage loan amount sought, – and any other information deemed necessary by the

loan originator.

• An application may either be in writing or electronically submitted, including a written record of an oral application.

Good Faith Estimate Changes

Some closing costs will have tolerance levels; we will have 30 days from the date of closing to correct errors, and repay consumers any overcharges, to avoid violations.

• Zero (0%) for:– (i) The origination charge;– (ii) While the borrower’s interest rate is locked, the credit or

charge for the interest rate chosen;– (iii) While the borrower’s interest rate is locked, the adjusted

origination charge; and– (iv) Transfer taxes.

• 10 % for:– Lender required settlement services– Lender-required services, title services and required title

insurance, and owner’s title insurance…– Government recording charges.

Lets take a look.

Binding GFE – effective 1/1/2010

The loan originator is bound, within the tolerances, to the settlement charges and terms listed on the GFE provided to the borrower, unless a new GFE is provided prior to settlement.

GFE Page 1

• Important dates

• Summary of loan terms

• Escrow account information

• Summary of settlement charges

GFE

Page 1

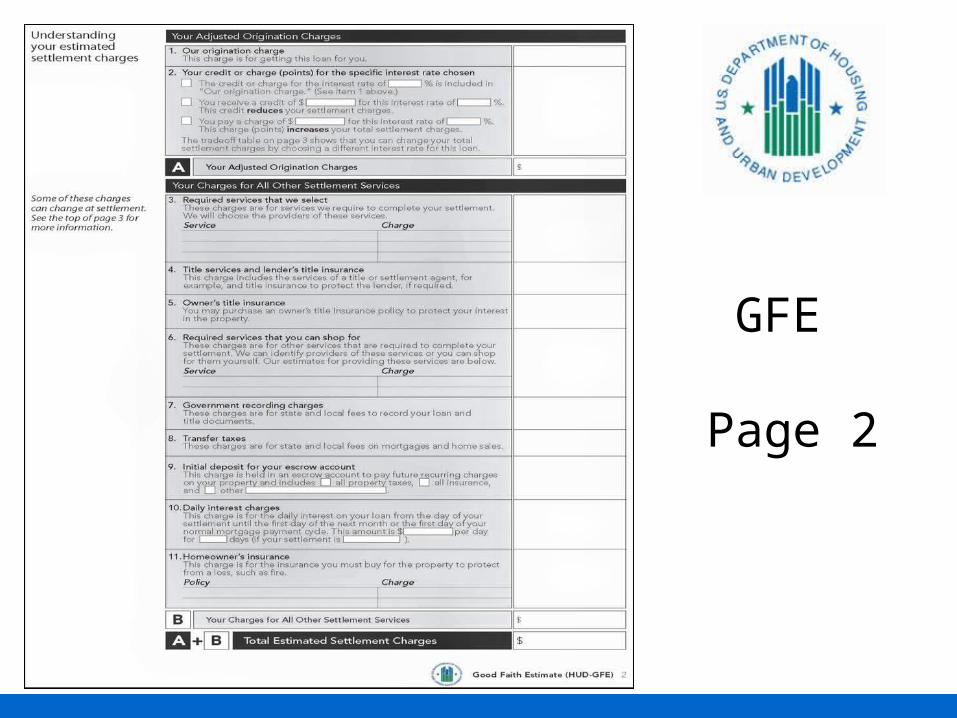

GFE Page 2

• contains all costs associated with the loan

• two categories: •Adjusted Origination Charges•All Other Settlement Services

GFE

Page 2

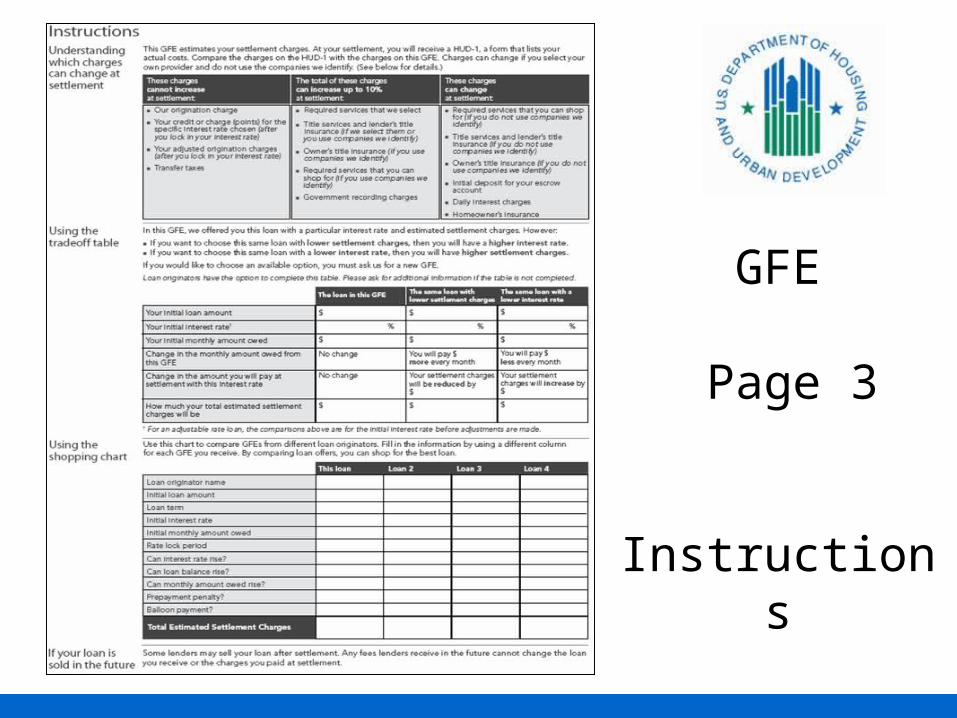

GFE Page 3

•Primarily an instruction page

•List of which charges can change

•Table of other loan options

•Shopping chart

GFE

Page 3

Instructions

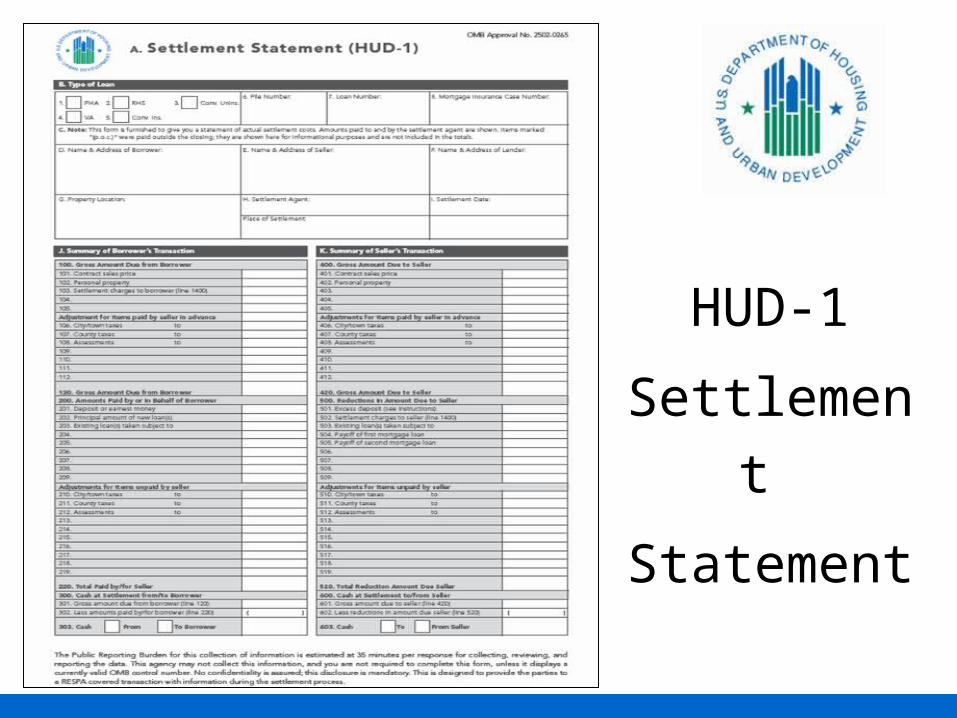

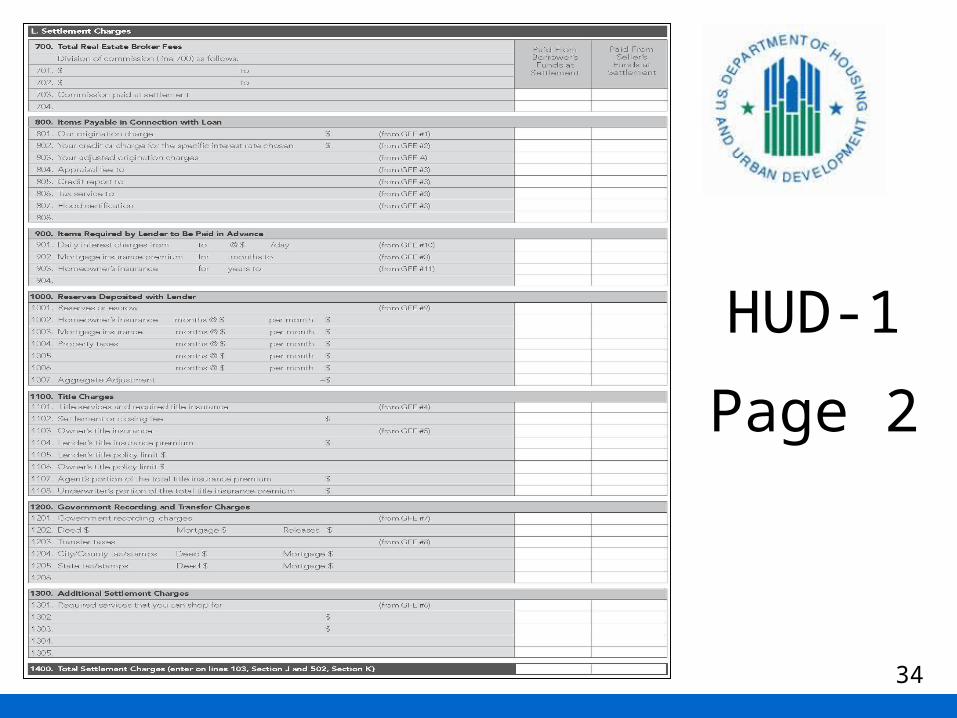

Moving on to the HUD (settlement statement)

HUD-1

Settlement

Statement

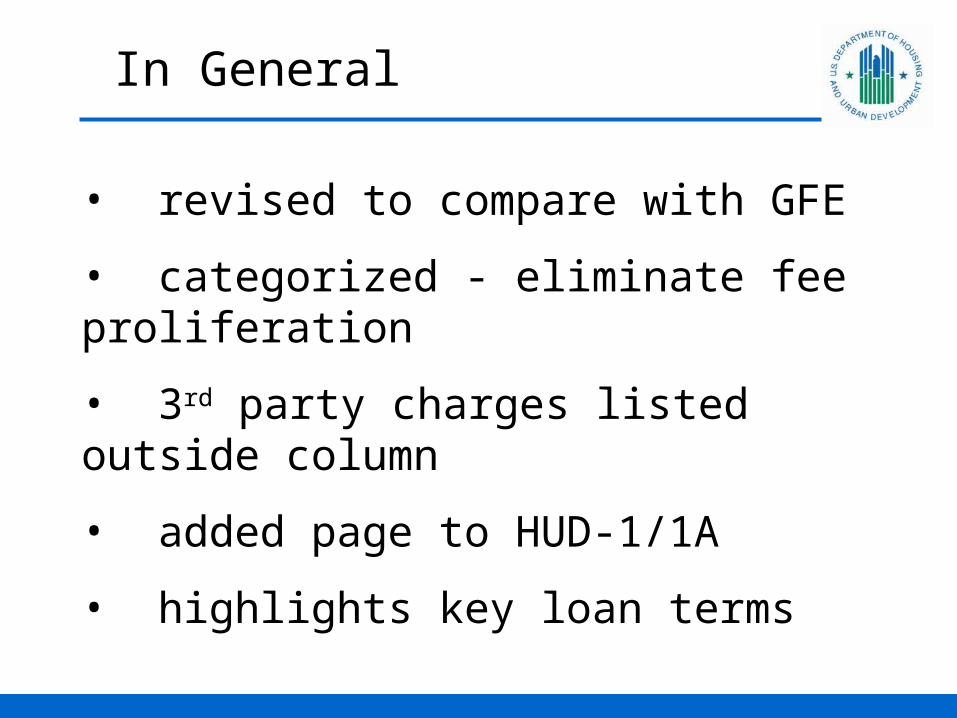

In General

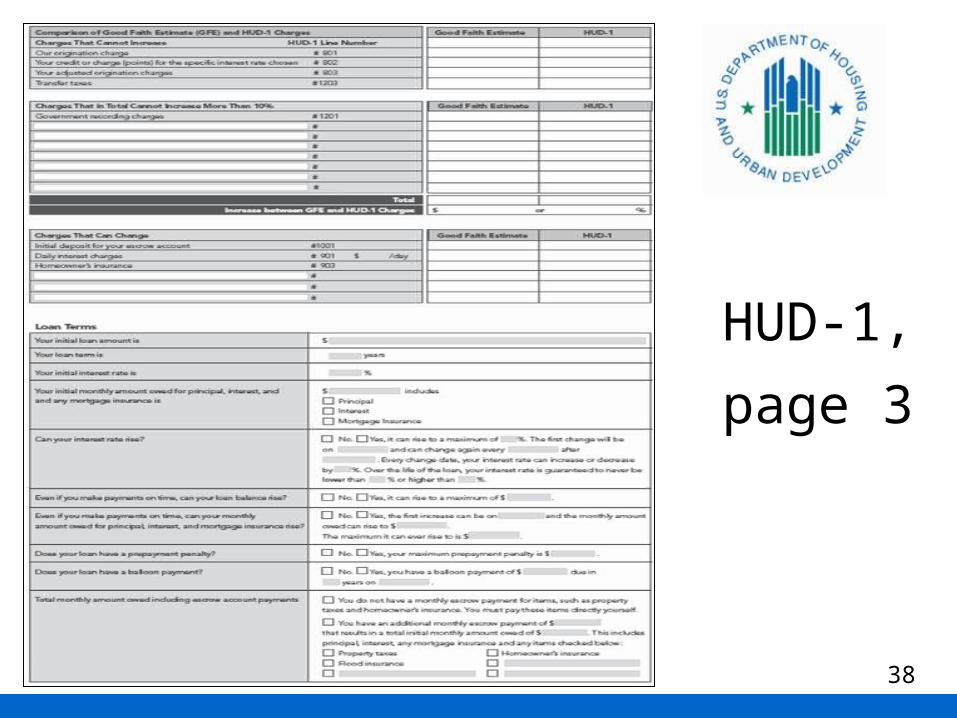

• revised to compare with GFE

• categorized - eliminate fee proliferation

• 3rd party charges listed outside column

• added page to HUD-1/1A

• highlights key loan terms

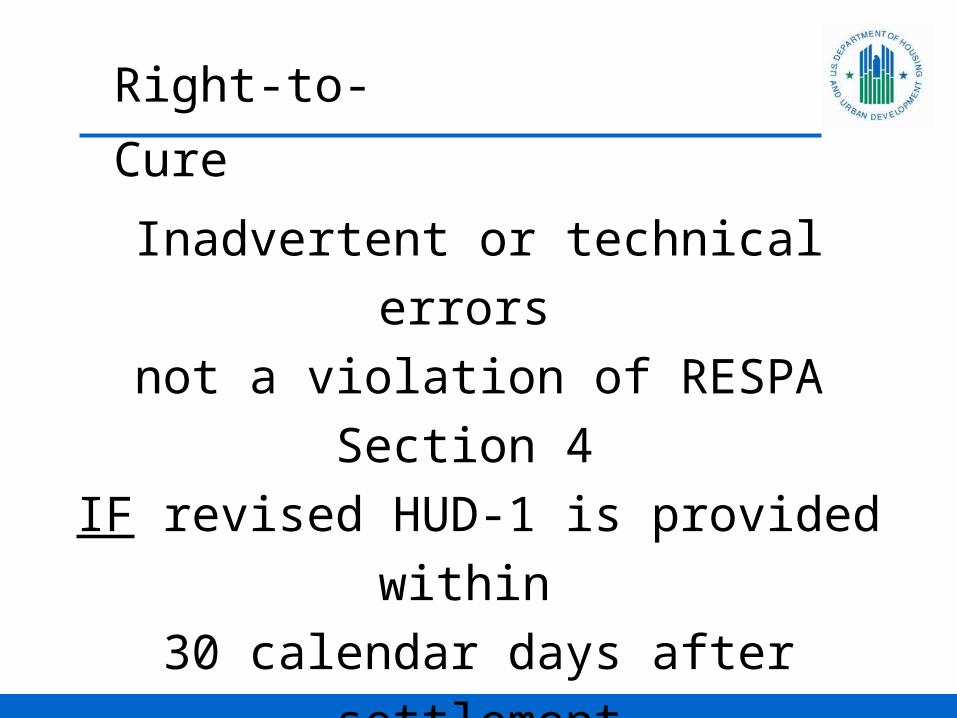

Right-to-Cure

Inadvertent or technical errors

not a violation of RESPA Section 4

IF revised HUD-1 is provided within

30 calendar days after settlement

HUD-1

Page 2

34

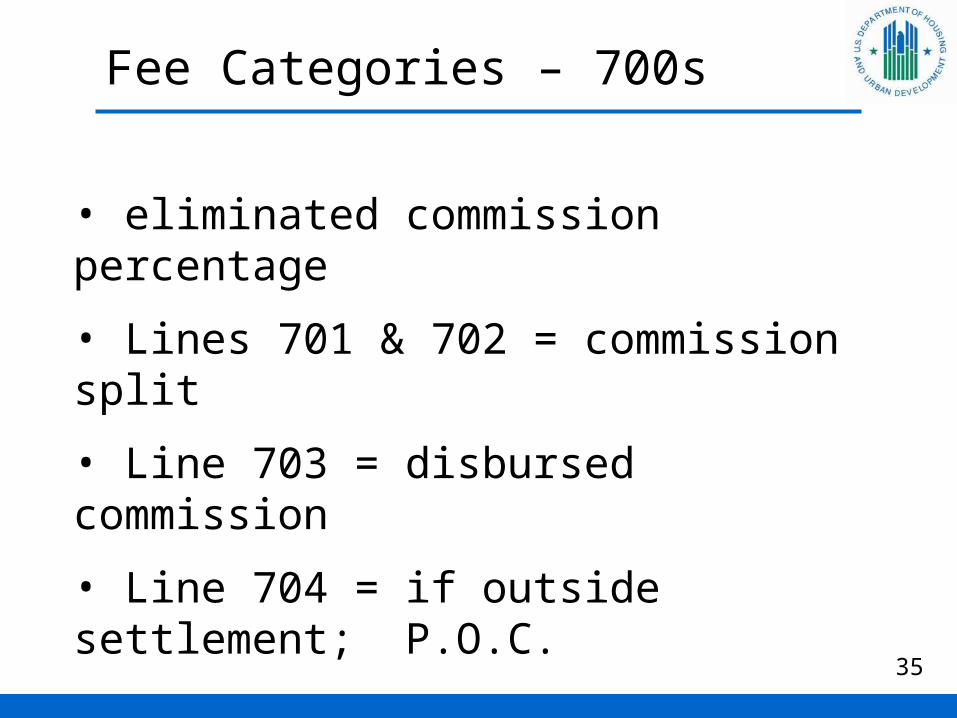

Fee Categories – 700s

35

• eliminated commission percentage

• Lines 701 & 702 = commission split

• Line 703 = disbursed commission

• Line 704 = if outside settlement; P.O.C.

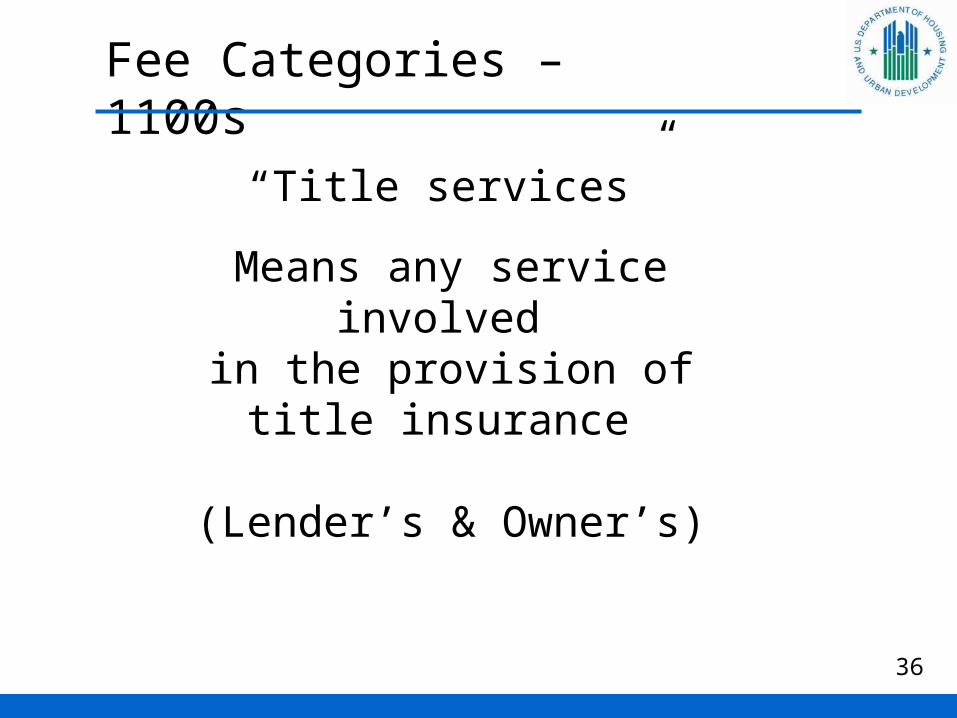

Fee Categories – 1100s

“Title services”

Means any service involved in the provision of title insurance

(Lender’s & Owner’s)

36

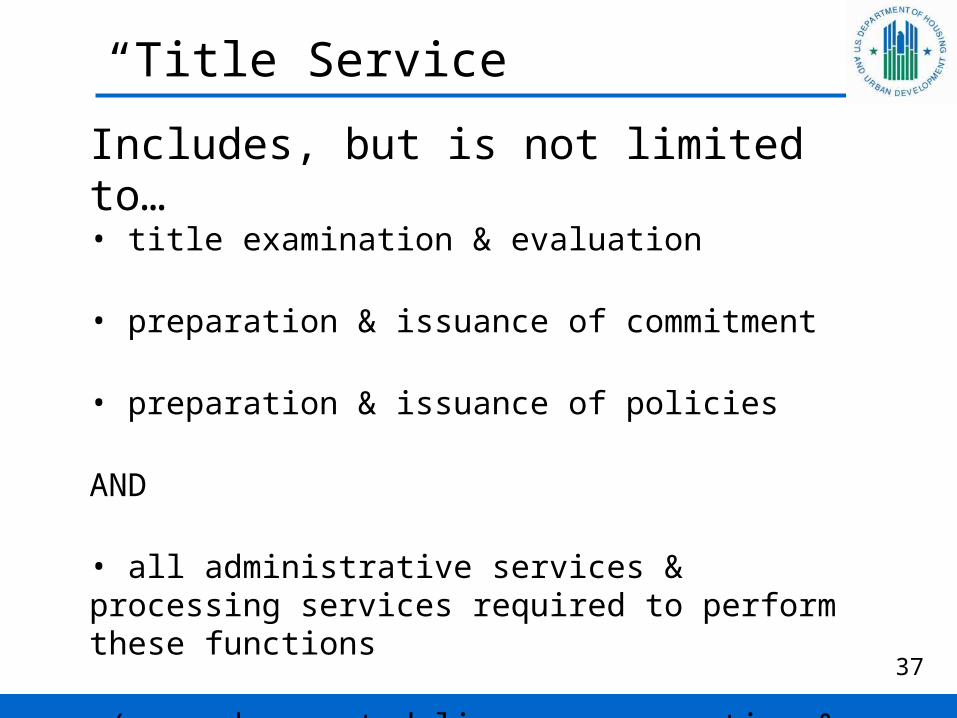

“Title Service”

Includes, but is not limited to…• title examination & evaluation

• preparation & issuance of commitment

• preparation & issuance of policies

AND

• all administrative services & processing services required to perform these functions

•(e.g. document delivery, preparation & copying, wiring, endorsements, & notary)

37

HUD-1,

page 3

38

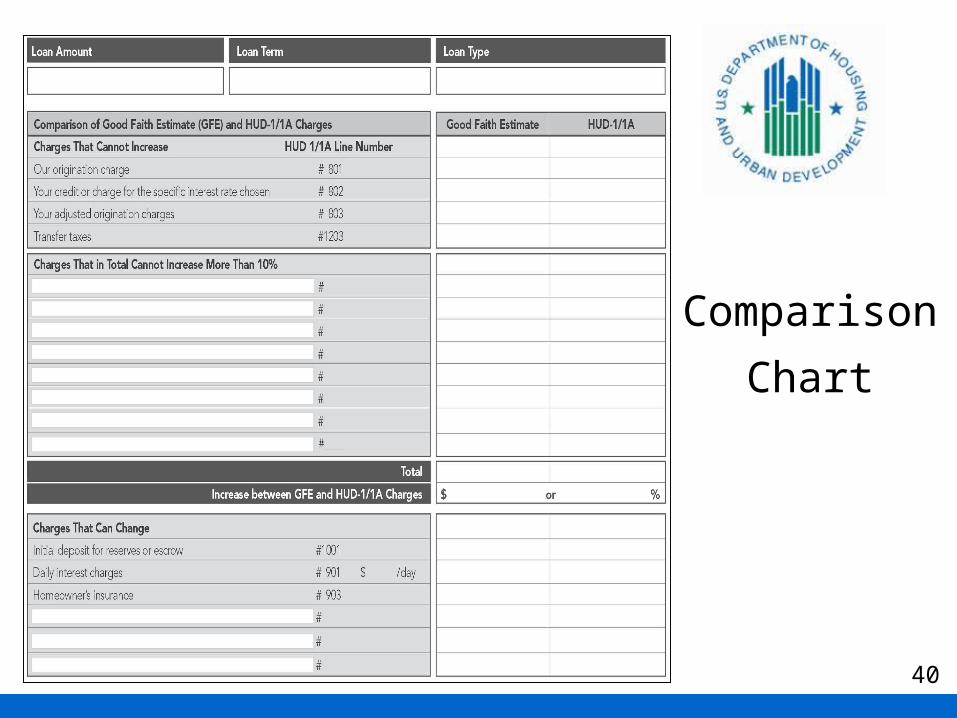

Comparison Chart

• compares charges listed on GFE & actual charges listed on the HUD-1/1A

• identifies tolerance compliance or violation

• 3 categories: charges that cannot increase, sum of charges that cannot increase more than 10% and charge that can increase

39

Comparison

Chart

40

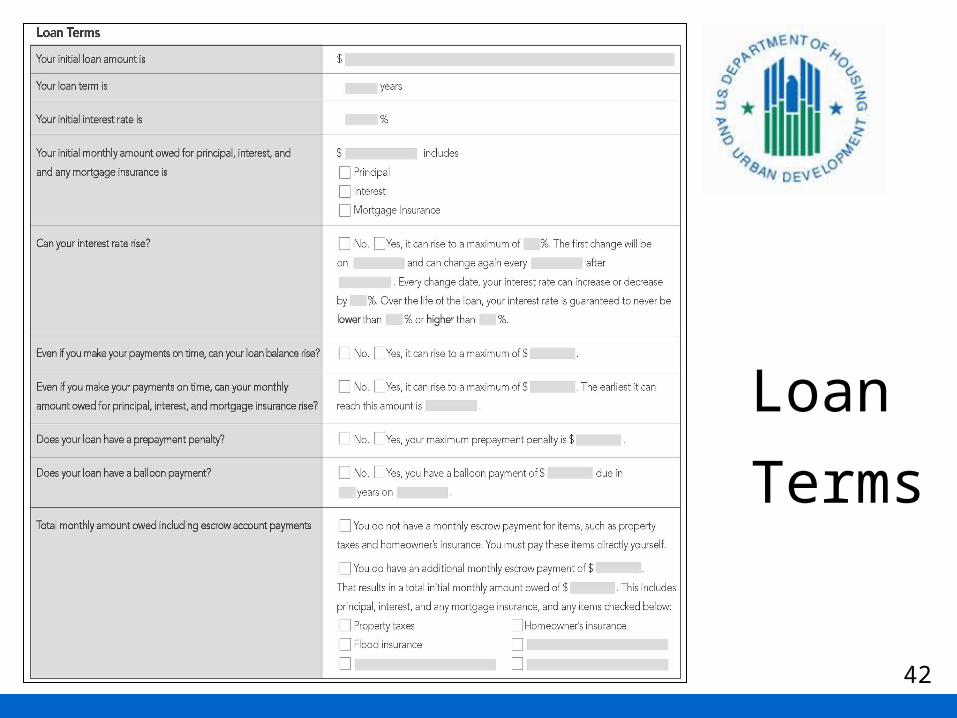

Loan Terms

• ensures borrowers that they received loan applied they applied for

• highlights key loan terms

41

Loan

Terms

42

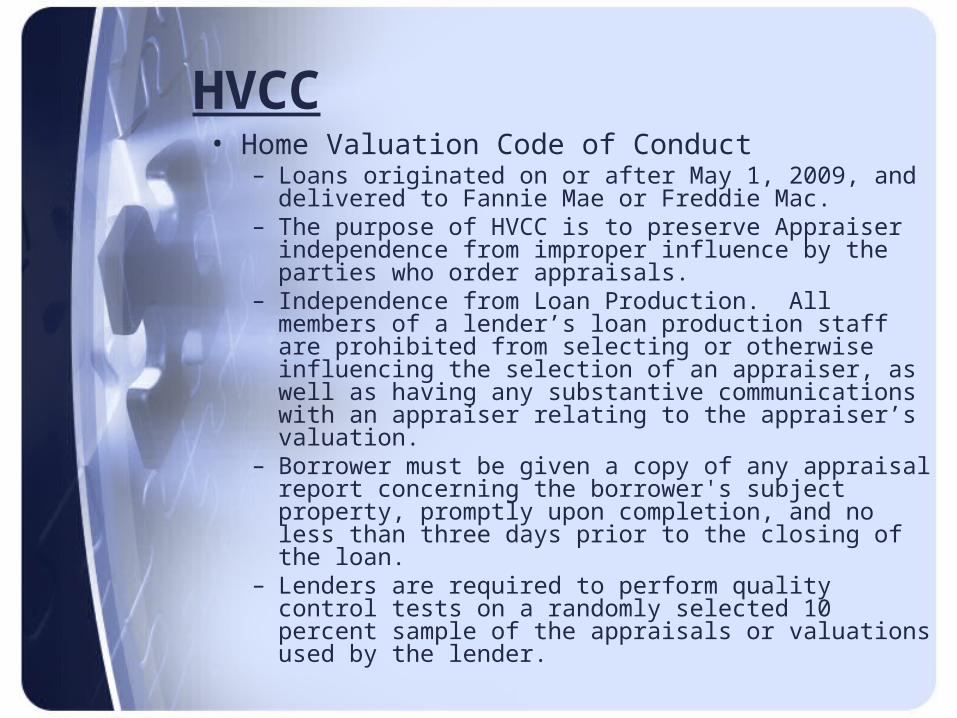

HVCC• Home Valuation Code of Conduct

– Loans originated on or after May 1, 2009, and delivered to Fannie Mae or Freddie Mac.

– The purpose of HVCC is to preserve Appraiser independence from improper influence by the parties who order appraisals.

– Independence from Loan Production. All members of a lender’s loan production staff are prohibited from selecting or otherwise influencing the selection of an appraiser, as well as having any substantive communications with an appraiser relating to the appraiser’s valuation.

– Borrower must be given a copy of any appraisal report concerning the borrower's subject property, promptly upon completion, and no less than three days prior to the closing of the loan.

– Lenders are required to perform quality control tests on a randomly selected 10 percent sample of the appraisals or valuations used by the lender.

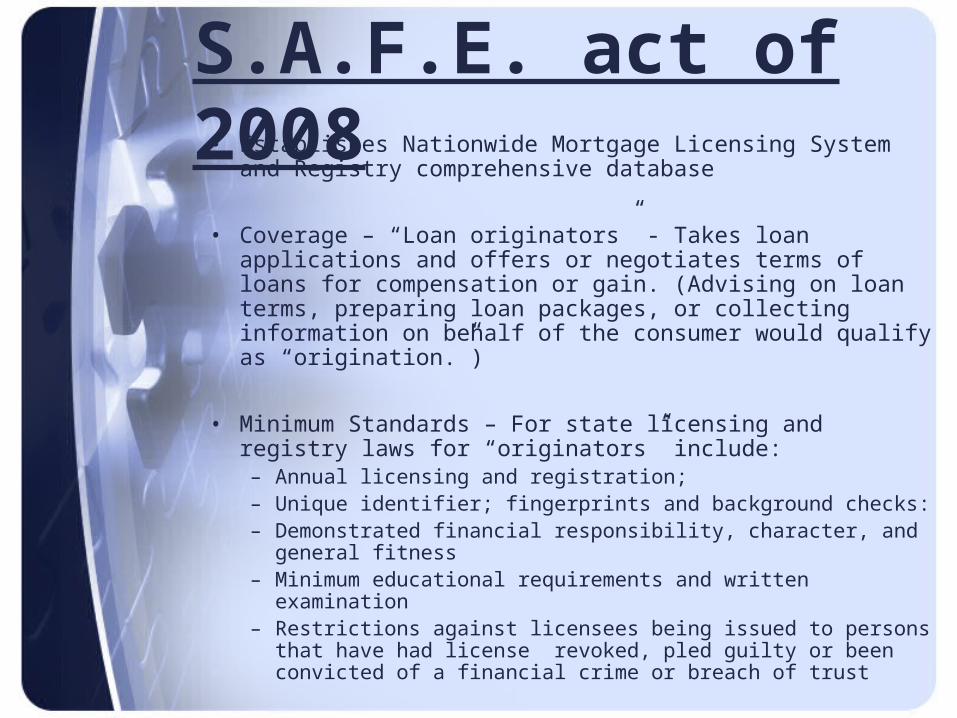

S.A.F.E. act of 2008• Establishes Nationwide Mortgage Licensing System and

Registry comprehensive database

• Coverage – “Loan originators” - Takes loan applications and offers or negotiates terms of loans for compensation or gain. (Advising on loan terms, preparing loan packages, or collecting information on behalf of the consumer would qualify as “origination.”)

• Minimum Standards – For state licensing and registry laws for “originators” include:– Annual licensing and registration;– Unique identifier; fingerprints and background checks: – Demonstrated financial responsibility, character, and general

fitness– Minimum educational requirements and written examination– Restrictions against licensees being issued to persons that

have had license revoked, pled guilty or been convicted of a financial crime or breach of trust

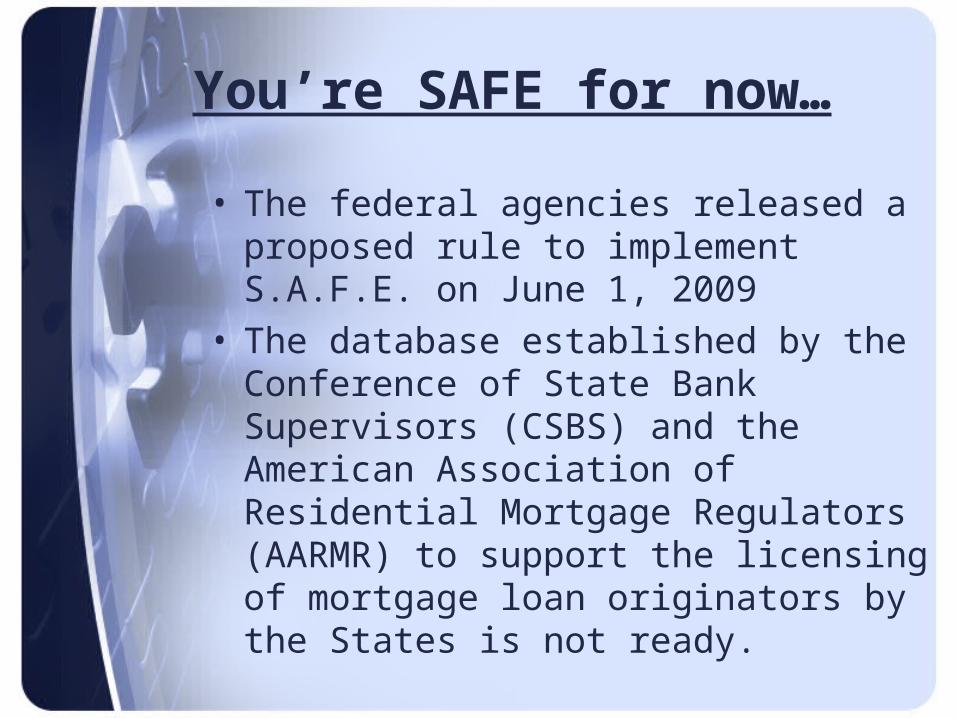

You’re SAFE for now…

• The federal agencies released a proposed rule to implement S.A.F.E. on June 1, 2009

• The database established by the Conference of State Bank Supervisors (CSBS) and the American Association of Residential Mortgage Regulators (AARMR) to support the licensing of mortgage loan originators by the States is not ready.