prospects, challenges and trends in the global ammonia market · • key market developments:...

TRANSCRIPT

Prospects, challenges and trends in the global ammonia market

Georgy Eliseev Fertecon | Agribusiness intelligence

Transformation: A New Era for the Agri-nutrients Industry

Fertecon is now part of IHS Markit Fertecon | Agribusiness intelligence

“The Informa Agribusiness Intelligence portfolio is a clear extension of our Chemical and Downstream businesses and builds our existing

data, pricing, insights, forecasting and news services within our Resources segment. Agriculture is the largest end chemical market in the

world and this transaction expands our capabilities into fertilizers and chemical crop protection, while substantively expanding our capabilities

in biofuels.”

Lance Uggla, CEO of IHS Markit

As of 1 July 2019, Agribusiness Intelligence joined IHS Markit in its Energy & Natural Resources division

UpstreamOil Markets,

Midstream &

DownstreamGas, Power

& Energy

FuturesChemical

and gas

feedstocks

Agribusiness

Intelligence

Agribusiness Intelligence offers

breadth and depth across the

agribusiness value chain:

• Fertilizers

• Crop Protection

• Policy

• Food Commodities

• Animal Health 2

Agenda

Fertecon | Agribusiness intelligence

• Key market developments: 2018-2019

• Key drivers for ammonia demand

• Ammonia cost curve and competitiveness

• Global ammonia trade and trade flows

• Capacity growth in 2014 – 2019 and Outlook to 2025

• New capacity changes trade flows:

• USA

• Russia

• Indonesia

• Overview of industrial demand segment

• Overview of phosphate segment

• Risks and outlook for ammonia trade

3

Transformation: A New Era for the Agri-nutrients Industry

Key market developments: 2018-2019Fertecon | Agribusiness intelligence

Source: Fertecon

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

300

320

340

360

380

Anmmonia FOB MiddleEast (Left Axis)

Urea FOB Middle East(Left Axis)

Oil Brent $/bbl (RightAxis)

Corn CBOT $/t (RightAxis)

Aug. 18 - Aug. 19$ $

-33%

-4%

-18%

+16%

• Ammonia prices have recently fallen below

the prices of other commodities

• Ammonia prices continuously decrease from

Sep. 2018

• Unlike urea prices, ammonia prices did not

recover in spring 2019

2018 – 2019 Prices for Selected Commodities

4

Transformation: A New Era for the Agri-nutrients Industry

Urea breaks away from ammonia

-100

-50

0

50

100

150

200

250

300

350

400

Urea Production Margin Ammonia FOB Middle East Urea FOB Middle East

Fertecon | Agribusiness intelligence

Source: Fertecon

$

Note: Urea production (upgrade) margin is calculated at 0.58 t of ammonia per 1 t of urea and after deduction

of processing costs per t of urea. Source: Fertecon cost model.

The highest level of

margins since 2012

• Ammonia - urea price

difference reaches record

high

• The urea production margin

(how much producer earns

more if convert ammonia in 1

t of urea) has been positive

since the end of 2017 (no

market self-regulation)

• The urea production margin

has reached the highest level

since 2012

• Why integrated producers do

not swing to urea?

Market self-regulation

Ammonia and Urea Prices, Urea Production Margin, 2016 - 2019

5

Transformation: A New Era for the Agri-nutrients Industry

Key drivers of ammonia demand

for fert urea45%

for non-fert urea9%

for fert AN8%

for non-fert AN4%

for CAN3%

for industrial7%

for DAP/MAP

6%

for NPK/NP8%

for AS4%

for D.A.3%

for other ferts3%

Ammonia demand by end use, 2018 Ammonia export by end use, 2018

Fertecon | Agribusiness intelligence

Source: Fertecon

• Global ammonia demand is

dominated by urea production

– 54%

• Not all integrated

ammonia/urea producers are

flexible to swing from

merchant ammonia to urea or

vice versa

• Some older technology

integrated plant always

produce merchant ammonia

along with urea (CO2

balance)

• Ammonia merchant market is

dominated by industrial

applications and

Phosphates/NPK.

for industrial40%

for MAP/DAP/NPK

39%

for AN/CAN

11%

for D.A.6%

Other/Unknown4%

Caprolactam

Acrylonitrile

MDI/TDI

Aniline

MMA

Adipic acid

Nitrobenzene

Ethanolamine

etc.

AN,

including

non-fert

100% = 179 million tonnes 100% = 19.0 million tonnes

Note: D.A. = direct application

6

Transformation: A New Era for the Agri-nutrients Industry

0

2

4

6

8

10

12

14

16

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

2016 2017 2018 2019

Energy Prices Gazprom Average Sales Price (Europeand other markets, including LNG)

Spot TTF Netherlands

Henry Hub, USA

Oil Brent (in mmbtu equivalent)

Feedstock pricesFertecon | Agribusiness intelligence

Sources: Fertecon, Gazprom, IHS Markit, EIA

• Natural gas prices are still at low

levels

• Recently, soft winter and LNG

inflow have pushed the European

spot gas prices down

• Contract gas prices in Europe (LT

contracts from Russia and other

sources) are following the track of

spot prices

$/mmbtu

7

Transformation: A New Era for the Agri-nutrients Industry

Global costs curve becomes lowerFertecon | Agribusiness intelligence

Ammonia exporters cost curve, 2018 respect to 2014

Source: Fertecon

2014 Cost Curve

• Lower gas prices round

the world since 2014

have reduced ammonia

costs

• The global cost curve

became lower and flatter

• This change has not

affected low-cost

producers (Middle East,

North Africa, Russia,

North America)

• However, high-cost

producers have become

more competitive

• High-cost (marginal)

producers can afford

producing at lower

ammonia prices

Source: Fertecon

8

Transformation: A New Era for the Agri-nutrients Industry

Costs: cfr EuropeFertecon | Agribusiness intelligence

147 147

251

300329 342 348 359

472506

537569

0

100

200

300

400

500

600

700

Lybia Algeria Egypt USA Belarus Trinidad Russia EU spotgas

Ukraine EUcontract

gas

Turkey Serbia

2014

Gas Costs Other Plant Costs Domestic Transportation Freight Duty Delivery Cost NW Europe cfr

183 183

225 230248 255 257

273

329 337

376 390

0

100

200

300

400

500

600

700

Algeria Lybia USA Trinidad Belarus EU spotgas

Russia Egypt Ukraine EUcontract

gas

Turkey Serbia

2019

Source: Fertecon

cfr NW Europe Year Average $592

cfr NW Europe 8m Average $338

9

Transformation: A New Era for the Agri-nutrients Industry

Trade flowsFertecon | Agribusiness intelligence

Source: Fertecon

Canada to US (1.0)

LA to US (2.1)

US to LA (0.5)

LA to Asia (0.4)

LA to Africa (0.4)

LA to Europe (0.4)

Eurasia to Europe (2.1)

Eurasia to Africa (1.1)

Africa to Europe (1.4)

ME to Europe (0.1)

Eurasia to Asia (0.4)ME to Asia (3.2)

Latin America Intra-Regional

LA to Asia (0.4)

Eurasia Intra-Regional

Europe Intra-Regional

Asia/Oceania Intra-Regional

Baltic

Yuzhny

1.6

0.9

2.3

0.6

West from Suez East from Suez

~1.2 mt

Africa to Asia (0.4)

• Global Ammonia Trade ~ 19

million tonnes, Sea Trade –

16.6 million tonnes

• Market “West of Suez”

accounts for almost 2/3 of

global market

• Market “East of Suez” is fast

growing

• West has traditional surplus

and East has traditional

shortage, West – East net

transfer is ~1.2 million tonnes

• Trade flows are stable with

special infrastructure in place

and long-term contracts

10

Transformation: A New Era for the Agri-nutrients Industry

Ammonia Demand: East and WestFertecon | Agribusiness intelligence

Source: Fertecon

11

Transformation: A New Era for the Agri-nutrients Industry

Capacity additions peak in 2016-2019

-

100

200

300

400

500

600

0

2

4

6

8

10

12

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020F 2021F 2022F 2023F 2024F

Capacity Additions, million t

Total Total (excl. China) Merchant Ammonia FOB Middle East (annual average)

Fertecon | Agribusiness intelligence

Source: Fertecon

• Prices at >$500 in 2011-2014

• Wave of investments in 2011-

2015

• Commissioning peak in 2015-

2018

• Capacity ramping up in 2017-

2019

• Most of new capacity additions

in 2016-2019 – outside China

• Over 7 million tons of merchant

ammonia new capacity in 2016-

2019

• Not many new projects in 2020

– 2024 (but long list of “possible’

projects

• Only one merchant ammonia

unit expected in 2020 – 2021 in

Oman.

12

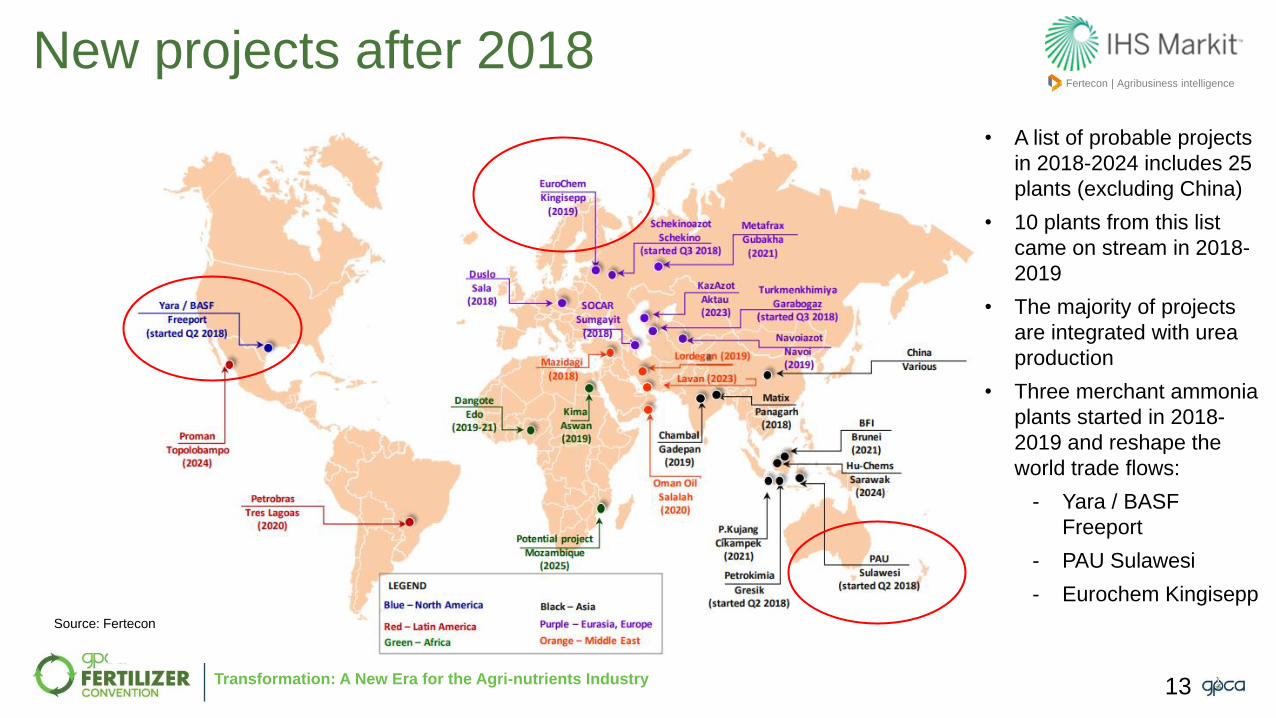

Transformation: A New Era for the Agri-nutrients Industry

New projects after 2018Fertecon | Agribusiness intelligence

Source: Fertecon

• A list of probable projects

in 2018-2024 includes 25

plants (excluding China)

• 10 plants from this list

came on stream in 2018-

2019

• The majority of projects

are integrated with urea

production

• Three merchant ammonia

plants started in 2018-

2019 and reshape the

world trade flows:

- Yara / BASF

Freeport

- PAU Sulawesi

- Eurochem Kingisepp

13

Transformation: A New Era for the Agri-nutrients Industry

Fertecon | Agribusiness intelligence

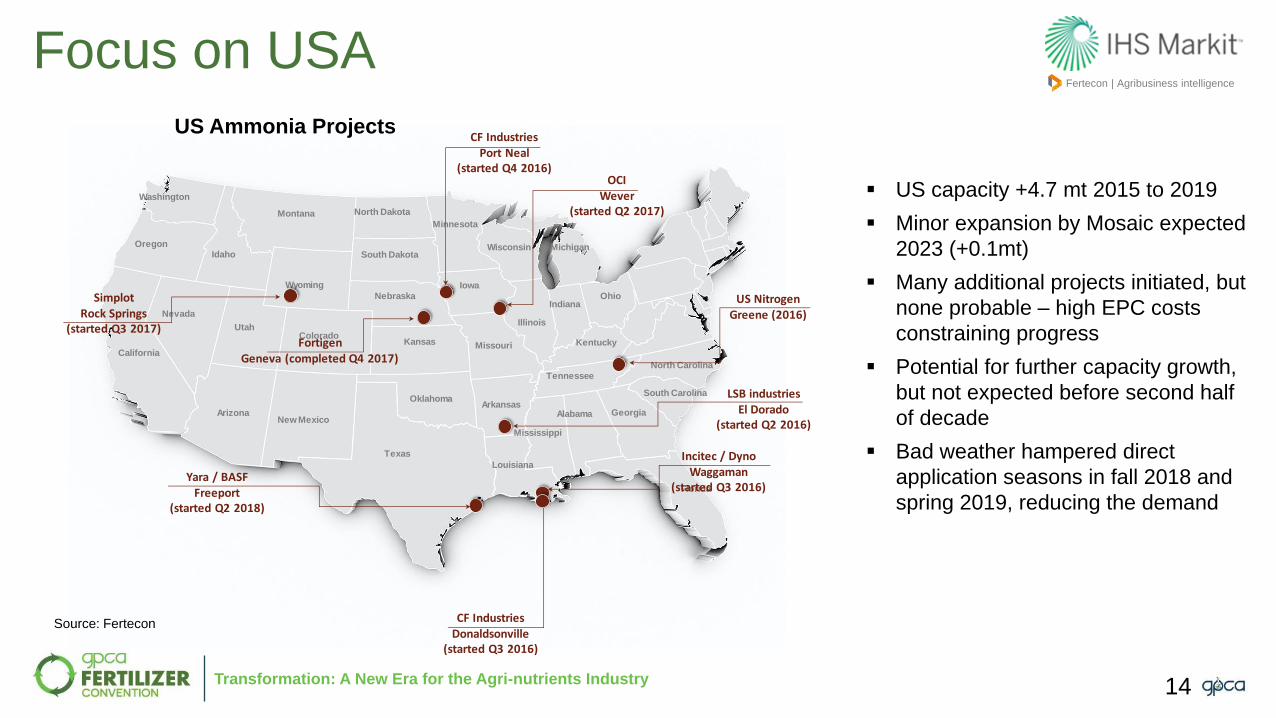

Focus on USA

New Mexico

Texas

Oklahoma

Louisiana

ArkansasGeorgia

Florida

Tennessee

South Carolina

Mississippi

Alabama

North Carolina

Washington

Oregon

California

Idaho

Montana

Nevada

Arizona

Colorado

Wyoming

North Dakota

South Dakota

Nebraska

Kansas Missouri

Minnesota

Wisconsin

Indiana

Kentucky

Ohio

Utah

Michigan

Illinois

Iowa

CF IndustriesDonaldsonville

(started Q3 2016)

Incitec / DynoWaggaman

(started Q3 2016)

OCIWever

(started Q2 2017)

CF IndustriesPort Neal

(started Q4 2016)

SimplotRock Springs

(started Q3 2017)

US NitrogenGreene (2016)

LSB industriesEl Dorado

(started Q2 2016)

Yara / BASFFreeport

(started Q2 2018)

FortigenGeneva (completed Q4 2017)

US capacity +4.7 mt 2015 to 2019

Minor expansion by Mosaic expected

2023 (+0.1mt)

Many additional projects initiated, but

none probable – high EPC costs

constraining progress

Potential for further capacity growth,

but not expected before second half

of decade

Bad weather hampered direct

application seasons in fall 2018 and

spring 2019, reducing the demand

US Ammonia Projects

Source: Fertecon

14

Transformation: A New Era for the Agri-nutrients Industry

USA: import substitutionFertecon | Agribusiness intelligence

3,772 3,890

3,160

2,446

1,947

891

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2014 2015 2016 2017 2018 2019 7m

US Offshore Ammonia Imports

Texas Florida Louisiana Pacific Total

-50%

DAP/NPK

LA

Tampa, FLTX

973

323

492

Incitec / Dyno, Waggaman,

LA 0.726 mt (Q3 2016)

LSB Industries / El Dorado,

AK 0.340 mt (Q2 2016)

CF Industries, Donaldsonville, LA

1.1 mt, 0.166 merchant (Q3 2016)

CF – Mosaic agreement to supply

0.725 mt since 2017

MS

Yara/BASF, Freeport, TX 0.726 mt (Q2 2018)

Chemicals

Fertilizers,

Chemicals

Imports in 2018

Source: IHS Markit, Fertecon

new projects

Import flows

000’t

000’t

Note: in metric tonnes

15

Transformation: A New Era for the Agri-nutrients Industry

6,742 6,8116,295 6,032

5,046 5,2504,668

3,7633,079

1,241

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 H1

USA Ammonia Import

Trinidad Canada Latin America Ukraine and Russia Middle East Others Total

Fertecon | Agribusiness intelligence

USA: from import to export

44 32 38

241 135 113

222

744

358

168

-

500

1,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 H1

USA Ammonia Export CF-Mosaic

Line starts

Source: IHS Markit

Source: IHS Markit

16.4 16.0

18.7 3.1

0.4

Capacity Production Import Export ApparentConsumption

USA Ammonia Production, Export, Import and Apparent Consumption,

2018, million t

10.910.1

6.7 16.8

2018

2010

Source: IHS Markit, Fertecon

000’t

000’t

16

Transformation: A New Era for the Agri-nutrients Industry

Fertecon | Agribusiness intelligence

Trinidad looks for new markets

5.355

4.644 4.6584.321 4.333 4.267 4.507 4.472

4.104

1.132

0

1

2

3

4

5

6

2010 2011 2012 2013 2014 2015 2016 2017 2018 Q1 2019

Trinidad & Tobago Ammonia Export, million t

USA Latin America Europe Asia & Australia Africa

83% 81% 81%80% 78% 77%

69% 56%48%

39%

X% Share of USA in Trinidad’s Export

Source: IHS Markit

Trinidad & Tobago

New Markets for Trinidad

ammonia

• Trinidad & Tobago (T&T) ammonia

faces competition with new capacity

in the US

• The share of USA in T&T export

shrinks from >80% to <50%

• Competition with US supply in LA

markets: Mexico and Chile

• Growing Morocco import absorbs a

part of T&T export

• T&T expand to Europe (contract in

Belgium, eventual sales to Finland,

Turkey) and Asia

• Gas curtailment in Trinidad seem

already overcome

Million t

Source: IHS Markit, Fertecon

17

Transformation: A New Era for the Agri-nutrients Industry

Focus on Russia: KingiseppFertecon | Agribusiness intelligence

Russian Export to NW

Europe (LT contracts Acron

and Uralchem) 2018: 800 kt

Russian Railway Export to

Lithuania (to Eurochem Liphosa

Phosphate plant) 2018: 160 kt

Russian Railway Supply of

Eurochem Phosphorite

Kingisepp Plant 2018: ~130 kt

Russian Export to Belgium

through Yuzhny, 2018: 383 kt

Eurochem becomes 3rd

Russian contract supplier

to NW Europe

• Successful start up of a new plant in March 2019

• ~60,000 t per month of maritime exports, 8,000 t

railway export to Lithuania (May 2019)

• Eurochem new plant mainly supplies ammonia to

Eurochem’s fertilizer plants in Russia, Belgium

and Lithuania, but replaces purchased merchant

ammonia

• New contract supplier of ammonia to NW Europe

Eurochem Kingisepp

NH3 capacity 0.89 mt

115 kt in H1 2019

Eurochem Lifosa (NH3

requirement ~0.2 mt)

Eurochem Antwerp (NH3

requirement 0.2-0.3 mt)

300-500 kt in 2016-2018 0

20

40

60

80

100

120

140

Jan

Feb

Mar

Ap

rM

ay

Jun

Jul

Au

gS

ep

Oct

Nov

Dec

Jan

Feb

Mar

Ap

rM

ay

June

July

Au

gS

ep

Oct

Nov

Dec

Jan

Feb

Mar

Ap

rM

ay

Jun

Jul

Au

gS

ep

Oct

Nov

Dec

Jan

Feb

Mar

Ap

rM

ay

Jun

Jul

Au

g

2016 2017 2018 2019

Export of Ammonia from Baltic Ports

2016: 758 kt

2017: 855 kt 2018: 840 kt2019 8m: 867 kt

Source: Fertecon

18

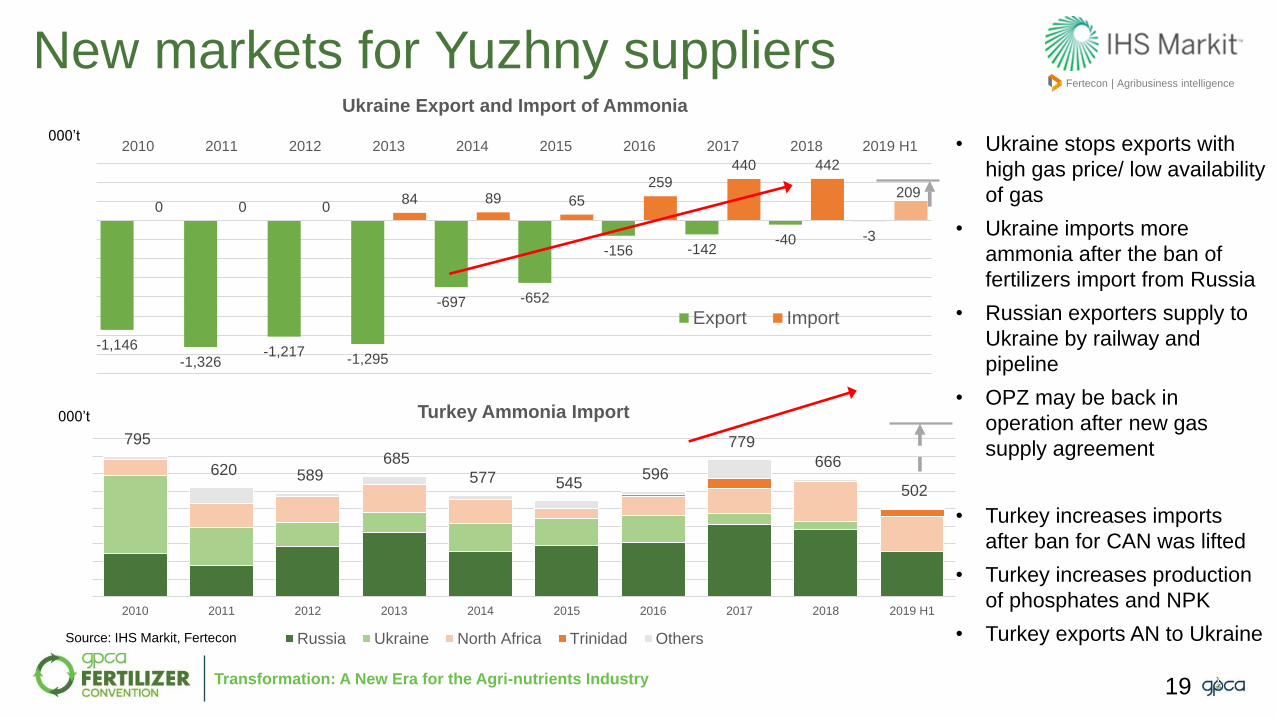

Transformation: A New Era for the Agri-nutrients Industry

New markets for Yuzhny suppliersFertecon | Agribusiness intelligence

795

620 589 685

577 545 596

779

666

502

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 H1

Turkey Ammonia Import

Russia Ukraine North Africa Trinidad Others Total

-1,146

-1,326-1,217

-1,295

-697 -652

-156 -142-40 -3

0 0 084 89 65

259

440 442

209

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 H1

Ukraine Export and Import of Ammonia

Export Import

• Ukraine stops exports with

high gas price/ low availability

of gas

• Ukraine imports more

ammonia after the ban of

fertilizers import from Russia

• Russian exporters supply to

Ukraine by railway and

pipeline

• OPZ may be back in

operation after new gas

supply agreement

• Turkey increases imports

after ban for CAN was lifted

• Turkey increases production

of phosphates and NPK

• Turkey exports AN to Ukraine

000’t

000’t

Source: IHS Markit, Fertecon

19

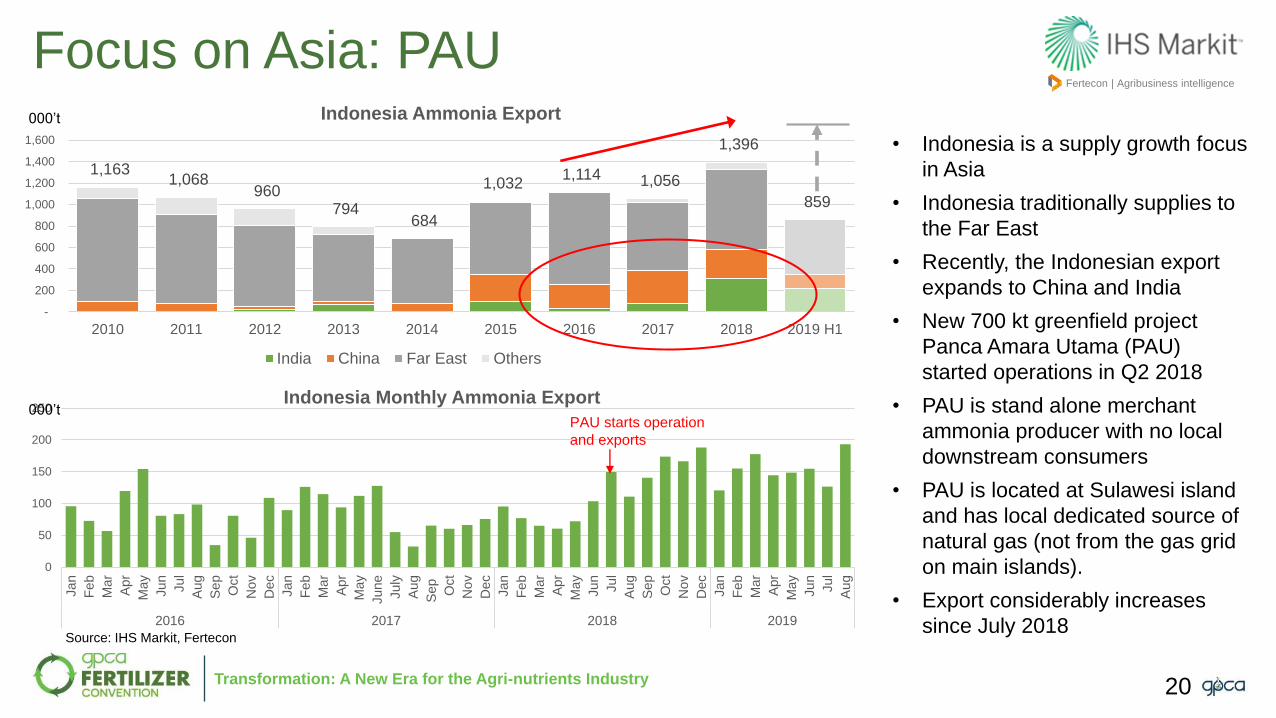

Transformation: A New Era for the Agri-nutrients Industry

Focus on Asia: PAUFertecon | Agribusiness intelligence

1,163 1,068

960 794

684

1,032 1,114 1,056

1,396

859

-

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 H1

Indonesia Ammonia Export

India China Far East Others Series5

0

50

100

150

200

250

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oct

No

v

De

c

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

ne

Ju

ly

Au

g

Se

p

Oct

No

v

De

c

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oct

No

v

De

c

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

2016 2017 2018 2019

Indonesia Monthly Ammonia Export

• Indonesia is a supply growth focus

in Asia

• Indonesia traditionally supplies to

the Far East

• Recently, the Indonesian export

expands to China and India

• New 700 kt greenfield project

Panca Amara Utama (PAU)

started operations in Q2 2018

• PAU is stand alone merchant

ammonia producer with no local

downstream consumers

• PAU is located at Sulawesi island

and has local dedicated source of

natural gas (not from the gas grid

on main islands).

• Export considerably increases

since July 2018

000’t

000’tPAU starts operation

and exports

Source: IHS Markit, Fertecon

20

Transformation: A New Era for the Agri-nutrients Industry

Far East Markets: Industrial Segment Fertecon | Agribusiness intelligence

• Far East merchant ammonia

markets are dominated by

industrial ammonia

applications

• Main markets: caprolactam

and acrylonitrile, are affected

by China – US trade dispute

and general industrial

slowdown in China

• Industrial applications of urea

(resins) and AN (mining) have

also slowed down

• Demand is supported by

environmental segment

(ammonia and urea for

deNOx)

$/t

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

Caprolactam and Acrylonitrile Prices, 2018-2019

Acrylonitrile Asia/Far East imports Caprolactam Asia Spot

Source: IHS Markit

21

Transformation: A New Era for the Agri-nutrients Industry

China increases importFertecon | Agribusiness intelligence

291 288 340 293

203

396 465

719

933

630

-

200

400

600

800

1,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 7m

China Ammonia imports

Indonesia Middle Eeast Trinidad Others Total

NanjingCaojing

Zhanjiang

Dafeng

306

161

425

Chinese Ammonia Terminals

2018 import (port

line-up), 000’t

SK Chemicals (new terminal,

first delivery in Sep. 2019)

BASF

Bayer

Huntsman

Sinopec

Lucite

Shanghai Secco

Akzo-Nobel

Fibrant

BASF-YPC

Zhanhua Phosphates

BASF

000’t

• China reduces ammonia capacity in line with restructuring of the industry

(closure of smaller and older plants), adjusting to slow demand growth (“0

growth” policy of fertilizer consumption).

• Import of ammonia has grown up in 2016-2018 with 3 main import terminals.

• Main consumers of import ammonia are the local JVs of international

chemical companies.

• In 2019 import slows down with more merchant ammonia available in the

country (due to weak domestic fertilizer markets).

• More than 50% of import comes from Middle East.

• Risks of US-China trade conflict.

Source: IHS Markit, Fertecon22

Transformation: A New Era for the Agri-nutrients Industry

Far East slows down Fertecon | Agribusiness intelligence

2,162 2,067 2,123 2,123 2,0331,838

2,0412,231

2,378

1,136

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 H1

Far East Import of Ammonia

South Korea Taiwan Japan Series4

2,162 2,067 2,123 2,123 2,0331,838

2,0412,231

2,378

1,136

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 H1

Far East Sources of Imported Ammonia

Middle East Indonesia and Malaysia Australia Trinidad Others

• South Korea, Taiwan and Japan have

increased import in 2016-2018 by 7-

10% pa.

• Like in China, main consumers of

imported ammonia are in chemical

industry.

• The industrial slowdown in 2019 affects

the ammonia import in far East: no

growth expected in 2019.

• About half of imports come from Middle

East, followed by Indonesia and

Malaysia.

• Competition with ammonia from other

regions (Trinidad, Indonesia, Yuzhny,

USA) is strengthening.

000’t

000’t

Source: IHS Markit, Fertecon

23

Transformation: A New Era for the Agri-nutrients Industry

Weakness in phosphate segmentFertecon | Agribusiness intelligence

547 716

547 647

808 824

1,041

1,447 1,445

659

-

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 5m

Morocco Ammonia Import

Russia and Ukraine Trinidad North Africa Others Total

100

150

200

250

300

350

400

450

Ammonia and DAP Prices

Ammonia FOB Middle East

DAP FOB Saudi Arabia

• Phosphate fertilizer industry has

had smooth growth in 2016 – 2018

despite growing overcapacity.

• Top producers managed to limit the

excess supply by lower operating

rates and closures of less efficient

operations.

• However, in 2019 the oversupply

finally affected MAP/DAP/NPK

markets.

• The announced reduction of

Chinese output could not yet stop

the decrease of prices.

• Morocco is the fast growing

importer of ammonia for the

expanding phosphate granulation

capacity

• In 2019 Morocco slows down

because of depressed

MAP/DAP/NPK markets.

000’t

$/t

Source: IHS Markit, Fertecon

24

Transformation: A New Era for the Agri-nutrients Industry

Focus on India

1,661

2,171 2,036

1,935 2,005 2,150

2,304 2,341

2,592

1,407

-

500

1,000

1,500

2,000

2,500

3,000

2010 2011 2012 2013 2014 2015 2016 2017 20182019 H1

India Ammonia Imports, 000’t Other Middle East &North Africa

Iran

Indonesia & Malaysia

Russia & Ukraine

Turkey

Others

Total

Fertecon | Agribusiness intelligence

Kandla

SikkaDahej

Mumbai

Goa

Mangalore

Paradeep

Ennore

Cochin

Tuticorin

Kakinada

Vizag

Haldia259

176

111

234

72

69

187133

44

324

188

664

65

Ammonia import to

India, 2018

• India uses imported ammonia for DAP/NP/NPK production.

• Ammonia import grows since 2013.

• Indian P nutrient requirements are covered by import of DAP/NP/NPK, or

by producing phosphates from the imported Phosphatic acid, or from the

imported Phosphorite Rock. Decision is made upon the prices for

DAP/NP/NPK, PhosAcid, Ammonia, Potash, and Subsidy/Minimum Retail

Price.

• Import is dominated by Iran and other Middle East exporters. However,

Iran’s share decreases in 2019 due to sanctions. 2018 import (port

line-up), 000’t

000’t

000’t

Source: IHS Markit, Fertecon

25

Transformation: A New Era for the Agri-nutrients Industry

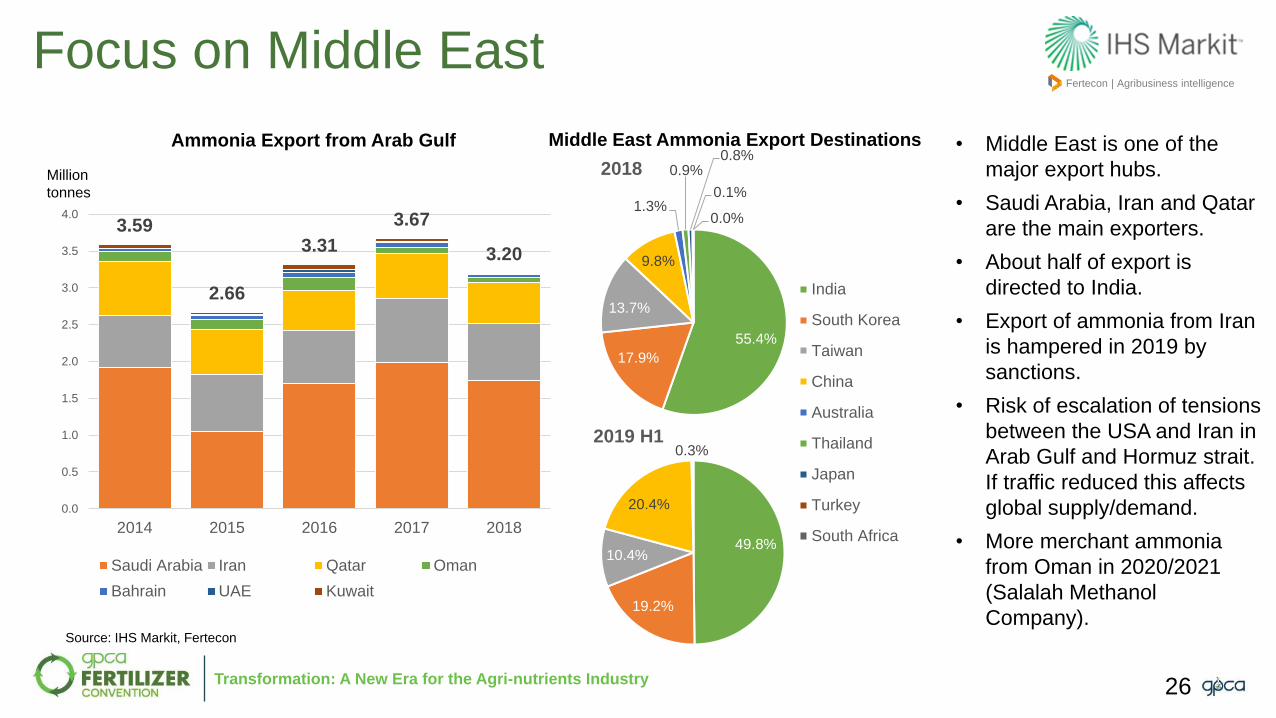

Focus on Middle EastFertecon | Agribusiness intelligence

3.59

2.66

3.31

3.67

3.20

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2014 2015 2016 2017 2018

Ammonia Export from Arab Gulf

Saudi Arabia Iran Qatar Oman

Bahrain UAE Kuwait Arab Gulf

55.4%

17.9%

13.7%

9.8%

1.3%

0.9%0.8%

0.1%

0.0%

2018

India

South Korea

Taiwan

China

Australia

Thailand

Japan

Turkey

South Africa49.8%

19.2%

10.4%

20.4%

0.3%2019 H1

Middle East Ammonia Export Destinations • Middle East is one of the

major export hubs.

• Saudi Arabia, Iran and Qatar

are the main exporters.

• About half of export is

directed to India.

• Export of ammonia from Iran

is hampered in 2019 by

sanctions.

• Risk of escalation of tensions

between the USA and Iran in

Arab Gulf and Hormuz strait.

If traffic reduced this affects

global supply/demand.

• More merchant ammonia

from Oman in 2020/2021

(Salalah Methanol

Company).

Million

tonnes

Source: IHS Markit, Fertecon

26

Transformation: A New Era for the Agri-nutrients Industry

Fertecon | Agribusiness intelligence

27

Kandla

Mumbai

Goa

Mangalore

Paradeep

Ennore

CochinTuticorin

Kakinada

Vizag

HaldiaSikka

Mesaieed

Ammonia Fleet in ME and India

Dahej

Al Jubail

Sur

BIK

AssaluehRAK

Al JabirahOM SUR – KR USN

ETA 09-20

24 kt

WaregemSA RAZ – JO AQJ

ETA 09-27

25 kt

StandorfIran – CN ZHA

ETA 09-21

22 kt

Galle

Fujairah

Clipper MarsUA YUZ – IN PRT

ETA OCT

36 kt

Gas LineIran – TW TXG

ETA 09-24

22 kt

Trammo CornellQA MES – IN KAK

ETA 09-23

25 kt

AlmaronaQA MES - IN NML

ETA 09-23

17 kt

Marianna GoldenIN ENR - ID BXT VIS

ETA 09-24

17 kt

WepionSA RAZ – KR USN

ETA 09-23

24 kt

The MoonIran – IN PRT

ETA 09-30

19 kt

Al BarrahTW TXG – SA JUB

ETA 09-25

24 kt

Aqaba

SCF TobolskCN CJG – SA RAZ

ETA 09-21

23 kt

KentIN PRT –

ETA 09-27

23 kt

Trammo DietlinIN IXY -

ETA 09-27

25 kt

Sitrah

Abu Qir Suez

Ar Ruwais

SeashineQA MES – IN ENR

ETA 09-26

25 kt

In Far East

In Indonesia

In Black Sea

Loaded to India

35%

Unloaded from India0%

Loaded to Far East36%

Unloaded from

Far East19%

Loaded to ME10%

Unloaded from ME0%

Middle East Mkt Tonnage

Loaded from ME

46%

Unloaded to Indonesia9%

Loaded from West from Suez

19%

Unloaded to West of

Suez26%

India Mkt Tonnage

Snapshot 23 Sep 2019

Source: IHS Markit, Fertecon

Ammonia terminals

Loaded ammonia vessels

Unloaded ammonia vessels

Transformation: A New Era for the Agri-nutrients Industry

OutlookFertecon | Agribusiness intelligence

Source: Fertecon

• Regional ammonia net trade

analysis shows a major shift in

the Americas region and tighter

market balance in Asia (east of

Suez)

• Export from Eurasia will

continue to grow

• Net export from the Americas

will stay at 2.7 million tonnes

• Net import will remain stable in

Europe and Africa, and east of

Suez.

28

Thank youwww.gpca.org.ae