programme business case addendum business transformation · programme business case addendum ....

TRANSCRIPT

tio Inland Revenue Te Tan i Taake

Programme Business Case Addendum

Business Transformation

Delivering New Zealand's future revenue system

October 2014

COMMERCIAL IN CONFIDENCE

Programme Business Case Addendum Business Transformation

This document has been released by Inland Revenue under section 81(1B) of the Tax Administration Act 1994 (TAA). Some sections of the document have been withheld: • As they must be kept secret in accordance with section 81 of the TAA; • as the programme business case contains advice still being considered by Ministers; • as some information was received subject to an obligation of confidence; • to protect the privacy of certain individuals; or • to enable commercial activities or negotiations to be carried out, without prejudice or disadvantage. The release of this document also supports the purposes of the Official Information Act 1982 by increasing progressively the availability of official information to the people of New Zealand.

2 COMMERCIAL IN CONFIDENCE / September 2014

Programme Business Case Addendum Business Transformation

Table of Contents 1 Executive Summary 4

2 Introduction 8

3 The strategic case 9

Overview 9

Brief summary 9

Material changes since last programme business case update 10

4 The economic case 12

The preferred way forward 12

Programme costs and benefits 12

5 The financial case 14

6 The management case 15

Learning from the experiences of others 15

Programme delivery 16

Programme governance and management arrangements 18

Programme methodologies and approaches 19

Programme controls 19

Organisational change management 21

Benefits management 23

Programme assurance 24

Working with the corporate centre 24

Assurance plan 24

Risk management 27

7 The commercial case 29

Commercial model for design 29

Appendix A - Programme benefits profile 31

Appendix B - EY benefits assessment 32

Appendix C - Governance roles and responsibilities 35

Appendix D - Biographies of programme leadership team 40

Appendix E - Transformation methodology 43

Appendix F - Risk and issue management 46

3 COMMERCIAL IN CONFIDENCE / September 2014

2

4

Enable Streamline Streamline Complete secure income and social policy delivery of digital business tax delivery the future services processes revenue

system

eveloped for the programme, setting out the starting point

New Zealand's future revenue system is to be delivered in four stages

The case for change remains sound and has not been updated

An initial view of success metrics and targets for the programme's investment

objectives has been developed

The preferred way forward, option 3B, remains unchanged

The overall programme cost and benefit assumptions remain unchanged

Programme roadmap remains unchanged

The programme business case financial case remains unchanged

Delivery approach for Stage 1 has been developed

Programme governance and management has been strengthened

Programme methodologies and frameworks have been adopted

Programme assurance arrangements have been updated and independent reviews

undertaken

Programme risks have been updated

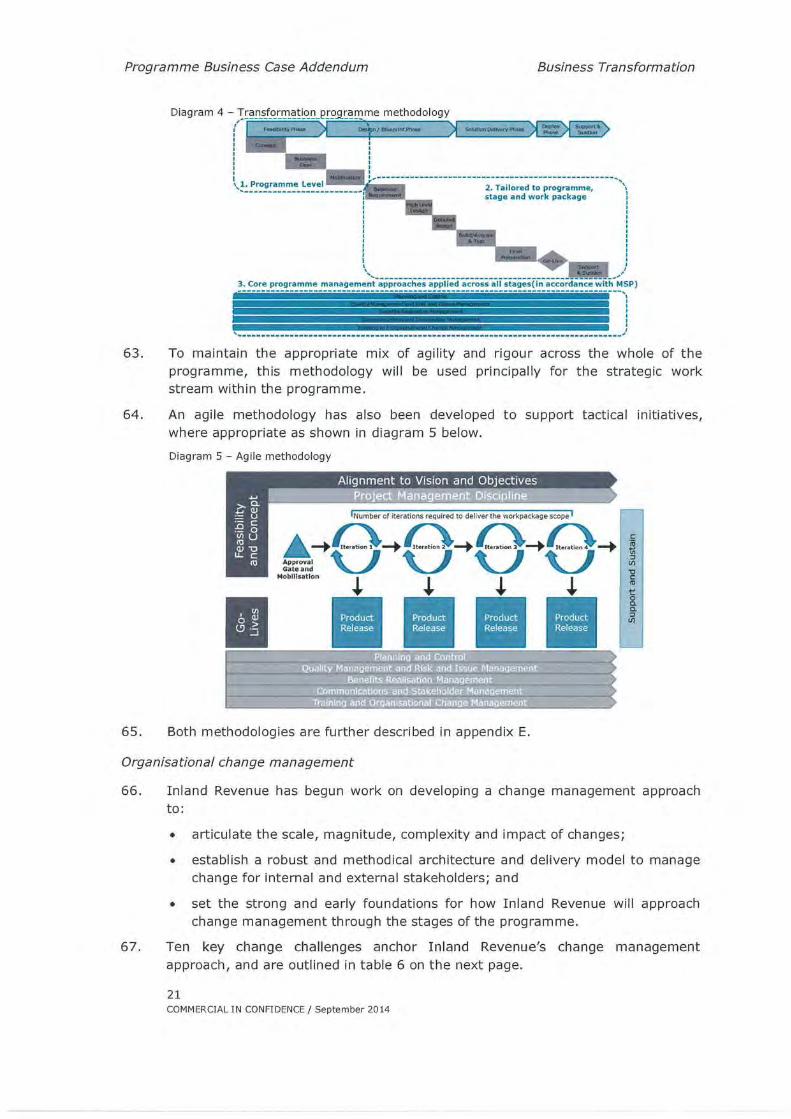

Commercial model has been updated from prime to service aggregation

The products and services that the programme requires have been updated

The Strategic Case

The Economic Case

The Financial Case

The Management Case

The Commercial Case.

Programme Business Case Addendum Business Transformation

1 Executive Summary

Purpose

1. The purpose of this addendum is to provide a summary of the material updates to the programme business case since it was last updated in October 2013.

Background

2. Business Transformation is a business-led, technology-enabled change programme to implement the infrastructure and capability that will enable Inland Revenue to deliver a modern revenue system, as represented by IR for the Future.

3. The programme business case indicates that between $1,300 million and $1,900 million (excluding depreciation and capital charges) in real terms over 10 years will be required to deliver the preferred option; and indicates financial benefits of $1,400 million to $2,700 million and economic benefits to New Zealand of $1,200 million to $2,500 million over 10 years.

4. A roadmap has been d and proposed stages. The roadmap is Inland Revenue's current view of how the programme will be phased and this view will be tested during the design phase.

Material changes to the programme business case

5. Table 1 below shows the current status of each of the cases in the programme business case together with any material updates.

Table 1 - Programme business case status updates Case

Status

4 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

6. The most significant updates are to the programme's planning, governance and management arrangements and commercial model to prepare for the next phase. By and large, these updates are a result of Inland Revenue building its delivery capability and knowledge.

7. In recent months, Inland Revenue has engaged extensively with a wide range of organisations including: those that have undertaken large change programmes; potential design service providers; and providers of commercial-off-the-shelf (COTS) core tax and social policy technology platforms.

8. As a result of the insights gained, Inland Revenue believes it is possible to shorten the programme timeline by approximately two years, and to bring costs in at the lower end of the indicated range.

9. A single stage business case has been developed to support an investment decision to progress to the next phase, which comprises of:

• the design of the future revenue system ; and

. initiatives to provide some early improvements to Inland Revenue's digital services for customers.

10. The design of the future revenue system will include:

• high level design of the future revenue system;

• selection of the COTS solution application suite of software, including the core, to best meet the requirements identified;

. detailed design and planning for the first stage;

• identification of future policy and legislation opportunities to frame and support the modernisation of the revenue system;

• extensive engagement with customers, third parties and other government agencies;

. development of a detailed understanding of the change impacts across the wider revenue system; and

• commencement of foundational work that will include planning for migration from the old to the new platform.

11. The requirement for Inland Revenue to interface with RealMe and the New Zealand Business Number (NZBN) will be included within scope of the design phase of the programme.

12. Three simple initiatives are proposed to improve the accessibility of Inland Revenue's digital services:

• improving myIR, Inland Revenue's existing secure online service, to encourage customers to resolve queries or perform simple tasks digitally and not revert to more traditional channels.

5 COMMERCIAL IN CONFIDENCE / September 2014

Programme Business Case Addendum Business Transformation

• making some improvements to Inland Revenue's websitel so customers find it easier to locate the information they need, and deliver mobile/tablet compatible content for high-use information.

• extending the mobile application (app) to make it available on Android devices, in addition to Apple devices.

Programme assurance

13. Since programme business case was last updated:

• Inland Revenue has worked closely with the Corporate Centre to agree the approach and plan for on-going engagement and collaboration throughout the life of the programme that is documented in a memorandum of understanding (MoU);

• an assurance plan is in place for the programme, developed in consultation with Inland Revenue's Corporate Risk and Assurance group and the Corporate Centre; and

• a number of independent assurance reviews have taken place.

14. Since the programme business case was last updated the following assurance reviews have occurred:

• KPMG, in their capacity as the programme's Independent Quality Assurance (IQA) provider, have completed a programme baseline IQA review;

• a Gateway review (Gate 0) was undertaken on the programme in September 2014; and

• Deloitte undertook a review, in September 2014, to assess the current programme governance and management arrangements against the lessons learnt from other programmes (including Novopay and the Child Support Reform project).

15. In general, the reviews were positive and indicated that the programme is on firm footing and is being is well managed and governed. Inland Revenue is currently addressing the material recommendations from these reviews. There were no recommendations that impacted this addendum or the Single Stage Business Case for the next phase.

16. The key risks to the next phase of the programme are considered to be:

• the scope of the programme changes through the design phase due to changes in priorities: this will be mitigated by strong programme management and programme planning;

• the programme is unable to attract and retain the right people with the right skills for the design phase: this will be mitigated by the use of external expertise with proven capability and the development of a retention strategy for critical resources across the transformation journey;

The structure and design of Inland Revenue's website was completed nearly 10 years ago: since then both website design and technology has advanced significantly.

6 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

• some stakeholders may feel that they have not had an opportunity to participate in the design phase: this will be mitigated by ensuring that engagement is representative of stakeholders; and

• the COTS solution selected at the end of high-level design may not fully meet Inland Revenue's detailed design requirements: this will be mitigated by ensuring all potential solutions are fully explored and evaluated.

7 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

2 Introduction

17. The purpose of this addendum is to provide a summary of the material updates to the programme business case since it was last updated in October 2013. This addendum should be read in conjunction with the Programme Business Case dated 22 October 2013, and with the single stage business case for design and improving digital services dated September 2014.

Structure of this document

18. This document has been developed with reference to Treasury's guidelines for Better Business Case single stage business case development published in February 2014. A scoping document was prepared and agreed between Inland Revenue and the corporate centre.

19. Table 2 below shows the current status of each of the cases in the programme business case together with any material updates.

Table 2 - Programme Business Case status updates

Programme

Status

Business Case

Chapter

The case for change remains sound and has not been updated The Strategic Case An initial view of success metrics and targets for the programme's

investment objectives has been developed

The preferred way forward, option 3B, remains unchanged The Economic Case The overall programme cost and benefit assumptions remain unchanged

Programme roadmap remains unchanged

The Financial Case The programme business case financial case remains unchanged

Delivery approach for Stage 1 has been developed

Programme governance and management has been strengthened

The Management Case Programme methodologies and frameworks have been adopted

Programme assurance arrangements have been updated and independent

reviews undertaken

Programme risks have been updated

Commercial model has been updated from prime to service aggregation The Commercial Case. The products and services that the programme requires have been

updated

8 COMMERCIAL IN CONFIDENCE / September 2014

Our story

Our challeog,

14. norallw

Our transformat.", goals

lornset oar biAlnee

• =rzrz...,.-

• •

Programme Business Case Addendum Business Transformation

3 The strategic case

Overview

20. The case for change remains sound and has not been updated; a brief summary follows. Investment objective metrics and targets have been developed and are included in this section.

Brief summary

Business Transformation is a business-led, technology-enabled change programme to implement the infrastructure and capabilities that will enable Inland Revenue to deliver a modern revenue system, as represented by IR for the Future.

21. An effective tax and social policy system is founded on having both good policy and good administration. The tax and social policy framework is considered to be fundamentally sound. However, the administration and some related legislative settings need modernisation as it has been over 20 years since the last major transformation of Inland Revenue's business processes and systems.

22. IR for the Future describes the vision of being an organisation recognised for service and excellence. This vision will enable Inland Revenue to be agile, effective and efficient, enable customers to self-manage with speed and certainty, enable government to make timely policy changes, and work with other agencies to optimise interaction across government. To fully achieve this Revenue will need to transform the way it does business, simplify benefit customers, and provide a stable technology platform to transformation.

23. The overall investment objective of the programme is to implement the capabilities required, as described within the Target Operating Model (TOM), to deliver IR for the Future, by:

• Improving agility so that policy changes can be made in a timely and cost effective manner.

• Delivering more effective services to improve customer compliance and help support the outcomes of social policies.

• Improving productivity and reducing the cost of providing our services.

• Improving the customer experience by making it easier and simpler for our taxation and social policy customers.

9 COMMERCIAL IN CONFIDENCE! September 2014

vision, Inland processes to support this

RNA Assessment

Obtain information (mm cristsi and Irditanilkx1 v.iiirttrog,—"'"dx.tkarititef

IR=land Crilindivicluals tax informatiordquestions

Custornors' Vknv

• Access to account

• Status Of transaction

• Risk analysis

Where required individual* do something 0 chock contron'proodoinkmalon)

• Customer profile

• Provide slonnalion

peco noopae•

Assessment - calculation of liability

csso My,

t • CurINS

(9•116., try •00.

A conceptual view of individuals' future income tax

Programme Business Case Addendum Business Transformation

• Increasing the secure sharing of intelligence and information across government to improve delivery of services to New Zealanders and improve public sector performance.

• Minimising the risk of protracted system outages and intermittent systems failure.

24. Business Transformation is an outcome driven programme. While the intended outcomes will remain constant over the life of the programme; Inland Revenue's view of how they will be achieved is likely to evolve.

A key outcome of the programme is to make it easier for New Zealanders to pay tax and meet their social policy obligations. In this regard, a key objective is that Inland Revenue's processes and systems will be 'simple at the front, smart at the back'.

25. This will enable New Zealanders to have greater certainty through:

• easy, digital access to their account information and the status of their transactions;

• more immediate and accurate information about their obligations and entitlements;

• for businesses, leveraging their everyday business processes to meet their tax obligations; and

• simplified and tailored interactions with Inland Revenue.

26. The information Inland Revenue receives, and shares through interoperable government systems, will be accurate and free of errors. This will enable a reduction in processing effort and provide more focus on customers and compliance. Also, Inland Revenue will be to share more information with other agencies because has confidence in its integrity.

Material changes since last programme business case update

27. Metrics and targets that measure the success of achieving each investment objective have been developed and are shown in table 3 on the next page. These were endorsed by Inland Revenue's Investment Board on 19 December 2013 and noted by the Minister of Finance and the Minister of Revenue. The indicative 2017/18 target is intended to be achieved at the conclusion of the first stage of the programme.

10 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

Table 3 - Investment objective: success metrics and targets Measure Baseline Indicative

2017 18 tar et Aspirational

10- ear tar et Ministers' satisfaction2 in achieving the six investment objectives

To be determined in discussion with the Ministers of Finance and Revenue

>= 6 (out of 10)

>= 8 (out of 10)

Weighted time to implement policy (a quantitative measure is being developed and will be tested and agreed with central agencies) Percentage of correct customer obligations received on time

Percentage of social policy customers receiving accurate and timely payments Cost to serve'

Customer perception of dealing with Inland Revenue - Makes it easy to get it right Reduction in customer tax compliance burden (expressed in hours) Outcomes achieved from information sharing and security of information General perception - You can easily access IR Customer-facing system availability4

Case studies

74%

>= 75% >= 90%

(41 % of EMS's received electronically)

(Stage 1 delivers a (90% to 100% digital

50% increase in EMS's uptake and all

received electronically products are validated and EMS's are upfront) validated upfront)

>= 75% >= 95%

<= $0.73 per $100 <= $0.54 per $100

(index = 75-81)

(index = 47-57)

>= 80% agree >= 90% agree

20 hours less >= 25 hours less

(>= 25%

(>= 30%

improvement)

improvement)

64%

$0.86 per $100 (index = 100)

78% agree

81 hours p.a.

Case studies

>= 70% agree >= 80% agree

<10 days >100 days

68% agree

<7 days

28. The targets will be updated as decisions are made and as detailed business cases are developed. The measures and targets will help guide investment decisions in individual business cases. Any future changes will be incorporated into future updates of the Programme Business Case.

2 This will be measured through a survey of the Ministers of Finance and Revenue, and other relevant Ministers depending on the policy being implemented. The survey criteria will be agreed with Ministers.

3 Inland Revenue's baseline/gross tax revenue plus payments processed through Inland Revenue. 4 Mean time between failure.

11 COMMERCIAL IN CONFIDENCE! September 2014

Reduction in customer compliance costs associated with meeting tax and social policy obligations.

Reduction in development and implementation effort associated with implementing policy changes within Inland Revenue.

Reduction or removal of the risk that a technology or process failure will occur, limiting the ability of Inland Revenue to collect obligations or disburse entitlements.

Providing certainty to customers, significantly simplifying customer requirements to meet their obligations, and improving customers' experience with Inland Revenue and government.

Reducing fraud, associated with filing incorrect tax information, not filing required obligations, or obtaining social entitlements fraudulently.

Easier for customers

Improving revenue system integrity

Economic benefits to New Zealand

Reduced time to implement new policy initiatives

Reduced risk of operational failure

$1,200m - $2,500m

Not currently quantified

Increasing Crown revenue through improving the Financial benefits to accuracy of customer tax assessments and reducing the Crown

the number of customers in debt, and productivity savings for Inland Revenue.

$1,400m - $2,700m

Benefit Area Description Over life of programme

Programme Business Case Addendum Business Transformation

4 The economic case

29. There have been no material changes to the economic case since the programme business case was last updated:

• the preferred way forward, option 3B, remains unchanged;

• the overall programme cost and benefit assumptions remain unchanged but have been tested as described below; and

• The programme roadmap remains Inland Revenue's current view of the sequencing of delivery.

The preferred way forward

30. Option 3B delivers an organisation that is agile, effective and efficient, enables customers to self-manage with speed and certainty, enables government to make timely policy changes and works with other agencies to optimise interaction across government.

Programme costs and benefits

31. The programme business case indicates that between $1,300 million and $1,900 million (excluding depreciation and capital charges) in real terms over 10 years will be required to deliver the preferred option; and indicates financial benefits of $1,400 million to $2,700 million and economic benefits of $1,200 million to $2,500 million over 10 years. The main benefits that the programme will deliver are shown in table 4 below.

Table 4 — Programme benefits for the preferred option

12 COMMERCIAL IN CONFIDENCE! September 2014

New Zealand's future revenue system is to be delivered in four stages

Enable secure digital services

2 Streamline

' income and business tax processes

Streamline social policy delivery

4 Complete delivery of the future revenue system

Programme Business Case Addendum Business Transformation

32. The profile of financial and economic benefits over the life of the programme is shown in appendix A.

33. Further work is now being undertaken to refine the benefit measures and quantify all benefit areas.

34. An independent assessment of benefits has been undertaken by Ernst & Young. This assessment concluded that the current benefit figures and the quantification process are reasonable and appropriate for this stage of the programme. The executive summary from Ernst & Young's assessment can be found in appendix B.

Programme roadmap

35. The roadmap is Inland Revenue's current view of how the programme will be sequenced and this view will be tested during the next phase.

36. Based on the current roadmap, the programme will be delivered in four customer-focused stages over a period of approximately eight to ten years:

• Stage 1: Enabling secure digital services will allow the majority of customers to self-manage and reduce businesses' compliance burden in fulfilling their PAYE and GST obligations;

• Stage 2: Streamline income and business tax processes will leverage the foundations delivered in the previous stage and further reduce businesses' compliance burden to fulfil their tax obligations;

• Stage 3: Streamline social policy delivery will improve the delivery of the social policies that Inland Revenue administers; and

• Stage 4: Complete delivery of the future revenue system will include transitioning any remaining taxes and social policies to a new platform and de-commissioning technology platforms that are no longer required.

13 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

5 The financial case

Withheld under section 81 of the Tax Administration Act 1994

14 COMMERCIAL IN CONFIDENCE / September 2014

Business changes were minimal and technology was modified to support existing business processes, which led to delays in benefit realisation and an under estimation of the change management effort required.

Policy was not fully used as lever, resulting in re-work and the old world being taken into the new.

Integration is complex, so legacy platforms have remained in place for extended periods.

A large focus on intelligence and advanced analytics led to increased revenue, case management and reduced debt.

Inland Revenue is engaging design service provider(s) and selecting the COTS solution early to ensure the processes are reengineered to fully leverage the new technology. A dedicated work-stream in the programme is focused on change management. Inland Revenue has included policy as a lever in the programme.

Inland Revenue has established the foundational sub-programme to focus on platform integration and data migration in parallel with the design phase.

None. Confirms elements of the Inland Revenue's Target Operating Model which emphasises the development of an advanced intelligence capability. Confirms Inland Revenue's preference to select a single, fully integrated solution covering all required functions.

Insight

Response

Programme Business Case Addendum Business Transformation

6 The management case

42. Since the programme business case was last updated, Inland Revenue has:

• undertaken research to learn from others in delivering large scale, technology enabled transformational change;

• developed a delivery approach for Stage 1;

• updated programme governance and management arrangements and built capability;

• adopted programme methodologies and frameworks;

• updated assurance arrangements; and

• updated risks for the next phase.

Learning from the experiences of others

43. In recent months, Inland Revenue' has engaged extensively with a range of organisations including: those that have undertaken large change programmes; potential design service providers; and providers of COTS core tax and social policy technology platforms.

44. As a result of the insights gained, Inland Revenue believes it is possible to bring the programme timeline back by approximately two years, and to bring costs in at the lower end of the indicated range. The key insights from these engagements, together with the programme's response are shown in table 6 below.

Table 6 — Insights from other change programmes

7 These engagements involved the programme leadership team and a number of Deputy Commissioners

15 COMMERCIAL IN CONFIDENCE! September 2014

The focus on delivering early benefits distracted management attention from delivering longer term change.

There was common trend towards service aggregation commercial delivery models.

There are COTS application suites of software currently available or under development that appear to be suitable for Inland Revenue's requirements.

The approach to design, the resources required, and the timeframes and costs will vary, potentially significantly, depending on the application suite of software selected.

Inland Revenue has established the tactical sub programme with a defined scope and dedicated resources to identify and implement initiatives that will deliver early benefits to New Zealanders.

Inland Revenue has reconsidered its commercial model for the design phase and has moved to service aggregation.

None. Confirms Inland Revenue's proposed approach to use COTS.

Inland Revenue has reconsidered its approach to design and is proposing to select the COTS application suite of software earlier in the design phase.

Insight

Response

Programme Business Case Addendum Business Transformation

Programme delivery

Replacing the FIRST platform

45. Fundamental to the transformation journey is the replacement of the FIRST technology platform. To ensure that New Zealand has twenty-first century tax administration, replacing FIRST is not optional, but a necessity. New technology will provide the catalyst to modernise New Zealand's revenue system, made up of two generic components —core functions unique to tax administration and industry-standard functions.

46. The next phase of the programme is design. Design will focus on Inland Revenue's portfolio of tax and social policy products, including core processing systems to support assessment, collection, and disbursement of obligations and entitlements, and risk assessment.

47. However, the transition to a new technology platform and business processes is complex and will take time. Therefore delivering some visible, early improvements that provide confidence in the modernisation of the revenue system is important. Three simple initiatives have been evaluated to improve Inland Revenue's digital services.

48. A single stage business case has been developed to support Cabinet's consideration of:

• commencement of the design phase of the business transformation programme; and

• initiatives to provide some early improvements to Inland Revenue's digital services for customers.

The design phase— scheduled to start in January 2015 and end in early 2016

49. During the design phase Inland Revenue will:

• delivered an overall design of the future revenue system that will enable:

16 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

o far greater certainty of programme costs, benefits and sequencing;

o detailed design of Stage 1 Enabling Secure Digital Services, completed in enough detail to commence implementation, subject to Government's approval to proceed.

• selected the COTS solution application suite of software, and identified common all-of-government capabilities that will be adopted;

• determined how best to interface with RealMe, the government's secure online identity verification service, and the New Zealand Business Number (NZBN);

. recommended future policy and legislative opportunities to frame and support the modernisation of the revenue system;

• engaged with and understood the change impacts on customers, third parties, other agencies, and the department itself.

50. The requirement for Inland Revenue to interface with RealMe and the New Zealand Business Number (NZBN) will be included within scope of the design phase of the programme.

51. At the end of the design phase, Inland Revenue will prepare for Ministers to consider:

• an updated programme business case, including a validated or revised programme roadmap, costs, benefits and timeframes; and

• a detailed business case for the first stage of the programme, including options for technology replacement and the level of capability required.

52. The recommended sequence for design is:

• high-level design for all stages of the programme and the selection of the COTS application suite of software; and

. detailed design for the first stage of the programme, based on the selected COTS application suite of software.

Improving digital services— scheduled to be delivered in 2015

53. Three initiatives are proposed to improve the accessibility of Inland Revenue's digital services:

• improving myIR, Inland Revenue's existing secure online service, to encourage customers to resolve queries or perform simple tasks digitally and not revert to more traditional channels. For example, Inland Revenue receives approximately 230,000 calls annually from myIR customers which could potentially be avoided if the services within myIR were improved.

• making some improvements to Inland Revenue's website8 so customers find it easier to locate the information they need, and deliver mobile/tablet compatible content for high-use information. The current customer experience is unwieldy and unhelpful.

8 The structure and design of Inland Revenue's website was completed nearly 10 years ago: since then both website design and technology has advanced significantly.

17 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

• extending the mobile application (app) to make it available on Android devices, in addition to Apple devices.

Programme governance and management arrangements

54. Inland Revenue has begun to prepare for transformation by lifting its capability, recruiting highly experienced transformation and change management practitioners, and strengthening its management and governance arrangements.

55. The programme governance structure is illustrated by diagram 2 below. The changes made since October 2013 are:

• the addition of the portfolio governance authority, replacing the programme steering committee, as part of Inland Revenue's governance structure;

• the replacement of the programme sponsor group with the programme executive working committee;

• the establishment of executive working committees and detailed working committees for the tactical and foundational sub-programmes;

• the establishment of four design councils - technical architecture, business process, organisational design and policy; and

• the establishment of a design integration forum, a programme planning forum and business owners' forums.

Diagram 2 - Current governance structure9

External Commissioner Independent Reference for Inland Quality

Groups Revenue Assurance

Includes External Members

Investment Board

Portfolio Governance

Authority

Deputy Commissioner Gateway Change (SRO)

Design Councils Programme Executive Executive - Technical Executive Working Working

HUSIOICSS Process Organisational Design Working Committee - Committee -

- Policy Committee Tactical Foundational

Detailed Detailed Business Owners Programme Working Working

Forums Director Committee - Committee - Tactical Foundational

Design Integration

Forum Work streams

Integrated Programme

Planning Forum

External advice & assurance

Inland Revenue management and

functions Governance

bodies

56. It is expected that this governance structure will remain in place during the design phase; however some fine tuning may occur. For more information on governance

9 External reference groups include the Transformation Reference Group, the Tax Simplification Panel and the ICT Advisory Group.

18 COMMERCIAL IN CONFIDENCE / September 2014

Programme Business Case Addendum Business Transformation

roles and responsibilities, and membership of governance bodies, please refer to appendix C.

57. In July 2014, Inland Revenue reviewed its portfolio office to ensure that the required disciplines were established for managing its investment portfolio, and to strengthen administration of the portfolio. The objective of the changes made is to ensure clarity, integration, and alignment across the governance and delivery of all Inland Revenue's projects and programmes, and to minimise discretionary change so that the organisation can focus on transformation.

58. The current high-level organisational structure for the programme is shown in diagram 3 below.

Diagram 3 - Current programme organisation structure

Programme Director

Communications & Stakeholder Management

Programme Manager

Programme Management

Office

Shared Services Senior Business Transformation

Lead

Commercial Director - Portfolio

Commercial Director - Tactical

Business Integration &

Design

Technical & Architecture

Tactical sub- programme

Foundational sub-programme Business Cases

Business Intelligence & Information Management

Organisational Change & Training

Withheld under section 81 of the Tax Administration Act 1994

Programme methodologies and approaches

60. The following methodologies and approaches have been adopted to ensure that the programme is successfully delivered:

• programme controls;

• business transformation methodologies;

• organisational change management; and

• benefit management.

Programme controls

61. The programme operates in an environment where there is a clear understanding of objectives, scope, timescales, costs, dependencies and risks. A ten keys programme management framework has been adopted which focuses on

19 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

providing proactive and transparent planning, base-lining and status reporting as follows:

• Confirm stakeholders are committed - aimed at identifying, evaluating, informing, influencing and maintaining support by individuals and groups affected by or influencing the programme.

• Ensure programme scope is realistic and managed - aimed at agreeing, managing and modifying as required the scope of work to be delivered to accomplish the programme's objectives.

• Plan so work and schedule are predictable - focused on controlling the production and acceptance of programme services/deliverables and ensuring their delivery is compliant with acceptance criteria and delegated authorities. A high emphasis will be placed on the project plan and ensuring that this is realistic and documents the major milestones and deliverables for all phases.

• Ensure cost is managed and on track - aimed at maintaining an up to date forecast for the programme, and measuring, managing and reporting actual costs in relation to the approved budget.

• Mobilising and directing high performance teams - aimed at identifying, recruiting, mobilising, structuring, leading and motivating the people necessary for successful completion.

• Mitigate risks - focused on identifying risks, evaluating them and developing avoidance, mitigation and other activities to effectively manage these and minimise impacts on the programme.

• Mitigate issues - focused on identifying issues, evaluating them and developing avoidance, mitigation and other activities to effectively manage these and minimise impacts on the programme.

• Support mutually beneficial partnerships - aimed at establishing and managing meaningful and effective relationships with key delivery partners, based on sound contracts and contract management processes.

• Realise business benefits - focused on estimating, measuring, monitoring and realising benefits to the enterprise to be derived from the programme.

• Coordinate dependent projects - aimed at identifying, planning, coordinating and controlling all projects which have a high level of dependence with the programme.

Business Transformation Methodology (B TM)

62. Inland Revenue has developed a methodology that will be applied during the life of the programme. The methodology will be combined with the experience and methods of selected design providers where appropriate. The methodology is aligned with the Managing Successful Programmesth (MSPTm) and Better Business Case guidance. Diagram 4 below provides a summary view of the methodology.

10 MSP is a recognised programme management methodology developed by the Office of Government Commerce, which is part of the UK Cabinet Office. The methodology is now a recognised standard for public sector programme management internationally.

20 COMMERCIAL IN CONFIDENCE! September 2014

Alignment to Vision and Objectives

'Number of iterations required to deliver the workpackage scope I

Iteration I Iteration 2 Iteration 3 Iteration 4

kai

1, 1 Approval Gate and

Mobilisation

Product Release

Product Release

Product Release

Product Release

Programme Business Case Addendum Business Transformation

Diagram 4 — Transformation pro_gramme methodology

2. Tailored to programme, stage and work package

1. Programme Level

3. Core programme management approaches applied across all stages(in accordance with MSP)

63. To maintain the appropriate mix of agility and rigour across the whole of the programme, this methodology will be used principally for the strategic work stream within the programme.

64. An agile methodology has also been developed to support tactical initiatives, where appropriate as shown in diagram 5 below.

Diagram 5 — Agile methodology

65. Both methodologies are further described in appendix E.

Organisational change management

66. Inland Revenue has begun work on developing a change management approach to:

• articulate the scale, magnitude, complexity and impact of changes;

• establish a robust and methodical architecture and delivery model to manage change for internal and external stakeholders; and

• set the strong and early foundations for how Inland Revenue will approach change management through the stages of the programme.

67. Ten key change challenges anchor Inland Revenue's change management approach, and are outlined in table 6 on the next page.

21 COMMERCIAL IN CONFIDENCE! September 2014

Change challenges Description

Ensuring that performance and service expectations are achieved while the business is changed. Change becomes the new normal for Inland Revenue's people and customers. Ensuring that Inland Revenue's people and customers understand their options and opportunities, and make informed choices. Ensuring that effective transition change approaches are tailored to business and customer groups. Focusing on robust and thorough processes to ensure that no area is untouched.

The changes that are implemented 'stick'.

Ensuring that credibility and customer compliance remains high.

Ensuring that positive and shared change is delivered to both Inland Revenue, as well as affected government agencies. Focusing on ensuring that Inland Revenue leaders communicate, engage and lead change.

Ensuring that potential external impacts are anticipated and managed.

Business disruption

Absorbing change

Creating a positive experience

Getting the change strategies right

Coverage of all impacted areas

Change take up

Customer, intermediaries and third party take up and community change

Government agency take up and support

Consistent and sustainable leadership

External environment impacts are identified and managed

Programme Business Case Addendum

Business Transformation

Table 6 -Ten key change challenges

68. Robust and sustainable change architecture will ensure Inland Revenue continues to deliver its commitments while managing significant change over an extended period of time. Inland Revenue's change architecture focuses on four key areas as outlined in diagram 6 below.

Diagram 6 -Change architecture

1

2

Enterprise Change - People & Culture/Business Led Culture & Leadership

• Building leadership change agity • Getting Change Fit, Tiers 1.4 and (rontine

leaders • Leadership as a he contdbutor to achieving

change and desired culture • Strategy to support the culture change

required by BT

Workforce and Capability

• Current state • Future state • Capability gap assessment • Capability roadm ap

Learning & Development

• • Idtify en and develop future skill sets

• Infrastructure to support future fure learning requirements

Employment Relations

• Staff communications • Unions • Consultation • Transition planning

Strategic Change - Transformation/Business Led Org Impact Assessments • Stages 1-4 impact

assessments • 3,,, parties & intemledia ries • Central and Cross agendes • Change release management

Change Challenges • People, customer, third

parties, business, central and cross agency change challenges

• Solution, strategies and plans to respond and manage the change challenges and risks

Strategic Customer Change

customer behaviour to influence channel shift and digital take-up

• Understanding Design

Communications and Stakeholder

• Journey management- telling the BT story, change narrative and momentum

• By stages, business outcomes &impacted area

Interim & Target Organisation

States . Interim state

hypothesis .Business Blueprint

(Structure, size, skills, capability and facilities)

----71

3

Managing Change - Business Led/Transformation Business Integration and

Readiness • Business readiness • Managing business impacts • Leading change • Making it real/Model office

Customer Readiness • Detailed impacts • Digital readiness • Promotion and education - take up • Communications

Third Parties/ Intermediaries

• Ensuring 3rd parties eg, NZICA understand, prepare and be ready for change.

• Co-Design

Central and Cross Agency Readiness

• Readiness for changes to data/information sharing formats, security and systems

4

Enabling Change - Transformation Led (transactional work)

Project Delivery Change • Detailed impacts, training needs,

user support, procedures and project life cycle

lob Analysis • Detailed job expectation changes • People transition activities

User Adoption and Embedding • Change warranty • Take up metrics • Embedding the change • Training and user requirements

22 COMMERCIAL IN CONFIDENCE / September 2014

6 Review

au Irvcniu, the frevelits Fe

Report& Review 0

utuu 0

dy A Define °Plan

Detailed design

Buda acquire &

test Hir4vel n

Flour propurution

Support & sustain

SePPOrt& sustain

Business Ca. Mobirisstion Business

retainements

Benefits reahsation management

1 Ideri cry

2 ASSeSS

3 Qnflne

4 Plan

5 Report

Usts the Indicative benefits that the programme / project will achieve, In accordance with the Better Business Case guidance.

The benefits assessment will examine benefit quantification, baseline data & realisation timeframes. It will also map capabilities and their projected maturity to benefit realisation.

Benefits will be developed In more detail and will be updated In the benefit model and dependency map.

The benefits plan will detail the monitoring approach for all benefits and will finalise the quantification & realisation tirneframe for the all benefits.

The programme and project level benefits reports will provide Information on the progress and success of benefits.

The benefits review process will ensure that maximum value Is realised for all stakeholders and that benefits management is transitioned into business as usual.

Programme Business Case Addendum Business Transformation

69. An organisational impact assessment for Stage 1 only has been completed to ensure Inland Revenue understands the impacts by stakeholder group. Almost all areas of Inland Revenue will be impacted over time.

Benefits management

70. A benefits management framework Programme Steering Committee11 on 9 April 2014.

71. The process of managing benefits has been acknowledged as a core part of the

for the programme was approved by the

programme management approach, and will be in place across all phases of the programme.

72. During the design phase, benefits management will be focussed on:

• using the benefits framework, establish a benefits management strategy, benefits management plan and benefits realisation plan for each phase of the programme;

• base-lining and agreeing measures for key performance indicators for each of the work packages in the programme roadmap;

• ensuring that work packages will deliver the identified benefits;

• undertaking the cost benefit analysis required to support the development of required business cases; and

• ensuring that programme delivery is aligned to the realisation of benefits through focused management.

73. During the solution delivery phase, benefits management will be focussed on:

• developing organisational structures and role descriptions to support the effective implementation of solutions or realisation of benefits;

• completing testing to confirm that anticipated benefits will be realised and to identify any issues, risks or potential dis-benefits; and

• completing business readiness assessments and transition plans to support effective progression into the next phase.

11 From 1 July 2014 Inland Revenue's governance arrangements changed, and the Programme Steering Committee was replaced by the Portfolio Governance Authority.

23 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

74. The sustain and support phase will be focussed on ensuring that the benefits identified during preceding phases will be sustained over the medium to long term. The key elements of this phase will include the following:

• building targets into budgeting;

• building targets into the performance framework for individuals with responsibility for the achievement of benefits; and

• tracking benefit realisation.

75. The realisation of benefits will be tracked via formal audit and review of the leading indicators for each benefit area.

Programme assurance

76. Since programme business case was last updated:

• Inland Revenue has worked closely with the Corporate Centre to agree the approach and plan for on-going engagement and collaboration throughout the life of the programme that is documented in a memorandum of understanding (MoU);

• an assurance plan is in place for the programme, developed in consultation with Inland Revenue's Corporate Risk and Assurance group and the Corporate Centre; and

• a number of independent assurance reviews have taken place.

Working with the corporate centre

77. The Corporate Centre comprises the Government Chief Information Officer (GCIO), the Treasury, the Department of Prime Minister and Cabinet (DPMC), the State Services Commission (SSC) and the government procurement group in the Ministry of Business, Innovation and Employment (MBIE).

78. Throughout the life of the programme, the corporate centre and Inland Revenue will work to ensure:

• assurance practices are in place, including agreement to an assurance plan;

• delivery of shared capabilities is properly considered; and

• on-going assessment of delivery impacts to timeframes and within cost and benefit thresholds, through to benefits realisation.

79. A number of principles have been agreed that are intended to guide all aspects of the relationship between Inland Revenue and the Corporate Centre:

• clear points of contact and co-operation at various levels;

• openness and transparency, with free and frank exchanges of opinions, sharing of relevant information, and appropriate and timely consideration of requests and comments;

• support of governance and independent quality assurance (IQA) arrangements, and clear understanding of responsibilities;

• commitment to agreed courses of action; and

24 COMMERCIAL IN CONFIDENCE / September 2014

Programme Business Case Addendum Business Transformation

• mutual resolution, wherever possible, of differences of opinion.

Assurance plan

80. An assurance plan is in place for the programme. The plan, developed in consultation with Inland Revenue's Corporate Risk and Assurance group and the Corporate Centre, ensures that:

• there is an overall plan for assurance activities, with a strong independent and external component;

• on-going IQA reviews are undertaken;

• Gateway reviews are undertaken at both programme and initiative level, and;

• progress is continuously monitored by the corporate centre.

81. The assurance plan includes a variety of internal and external assurance services, as shown in table 7 below.

Table 7 - Required assurance services

Service Detail

Internal assurance

Internal Assurance & Internal reviews to provide adequate assurance to the Commissioner and Advice

management on the status and adherence to and effectiveness of policies, processes and procedures within Inland Revenue.

Project Quality A 'Health Check' which is intended to provide an assessment of the Assurance current position of all work-streams as well as to provide assurance to the

Senior Responsible Owner (SRO) and Executive Working Committee that the programme is well positioned to deliver expected outcomes within time and budget, and to the expected level of quality.

External assurance Formal Assurance Assurance reviews conducted at key decision points determined by the (IQA) progress of the programme or as requested by the Commissioner, SRO

and/or Executive Working Committee, including the following; - time/quality/cost reviews across the programme, and/or - reviews of programme deliverables and key documentation.

Technical Assurance Assurance reviews on technical components of the programme including; (TQA) - the quality of the technical requirements content, and/or

- the process and methodology used in the development of the technical requirements.

- the adequacy of testing and implementation readiness. Probity To assist the programme to ensure all procurement activities are fair and

transparent, and achieve value for money and that all probity risks are managed. This will include the application of a Probity Plan, a Conflict of Interest Framework and managing probity risks and issues as they arise. This will also include on-going probity assurance advice provided by an external legal firm.

Gateway A multi-gate project and programme assurance regime designed to provide confidential, independent, high-level, action-oriented recommendations to project sponsors at key project milestones, focusing on the issues that are important to the continuing success of the project.

82. Different types of technical and strategic capability may be required to provide assurance at varying times of the programme and for specific deliverables and/or activities.

Independent assurance reviews

25 COMMERCIAL IN CONFIDENCE! September 2014

10 Keys to Success: ST:

Ermine Programme scope is reetntic and nianeged

[Winn stakelmaders ere corrienkted

Nen ma work and seiShols WI peetictible

Ensot cost s manned and on Deck

Mobising and demi largA performing teams

Margate reit

Mitsiete sows

Support rautuady benefiziel partnerships

Ragan business tonefas

Coortimate Dependent Projects

Programme Control Strengths

10 Law 11 woo maaa.••••

•••••••

C••••••••••

P., sew., .•••••••••• ••••••••

law • ••••••••

••••••••••

uuoilinu

—2•440.11

nDesig Effectiveness

Not yet assessed

00

?rack

Key:

Urgent attention Actions required required now not critical

MSP Assessment

riusity and mauranne7111

Programme Business Case Addendum Business Transformation

83. Since the programme business case was last updated the following assurance reviews have occurred:

• KPMG, in their capacity as the programme's Independent Quality Assurance (IQA) provider, have completed a programme baseline IQA review;

• a Gateway review (Gate 0) was undertaken on the programme in September 2014; and

• Deloitte undertook a review, in September 2014, to assess the current programme governance and management arrangements against the lessons learnt from other programmes (including Novopay and the Child Support Reform project).

84. KPMG's key findings were 'that Inland Revenue has established a sound programme governance structure and effective programme management processes, and has implemented practices that align with New Zealand Public Sector Guidelines for Managing and Monitoring Major Projects'.

85. In addition, KPMG noted that 'The programme is being well managed, using a methodology which has been tailored specifically to the transformational needs of the programme. Strong sponsorship and appropriate governance are also evident given the current stage of programme establishment.'

86. The baseline review assessed the programme against the MSP governance themes, with the results shown in diagram 7 on the next page. The business case theme was not reported on because independent business case reviews were undertaken by KPMG in March 2013 and August 2013.

Diagram 7 -Programme baseline review

87. The Gateway 0 review conducted in the week commencing 1 September 2014 rated the overall status of the programme as Amber meaning that successful

26 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

delivery appears feasible but significant issues exist requiring management attention. The review team noted that:

'At this juncture, the management challenges identified as part of this Review do not constitute significant issues as per the AMBER definition but nonetheless do need to be addressed promptly. Given the risk, size and timeline of the programme, this is not unusual. The programme is on a firm footing and there is every prospect that it could proceed towards improved delivery confidence status as uncertainty is driven our.

88. Inland Revenue is in the process of addressing all of the review's recommendations. There were no recommendations that impacted this addendum or the Single Stage Business Case for the next phase.

89. Deloitte conducted a review of the programme's governance and management arrangements which was completed in September 2014. The review concluded that:

'There is sufficient evidence to conclude that the programme has significantly developed capability across the programme. The governance structures put in place are new, but are comprehensive. The governance bodies have invested time to understand the context and nature of the programmes and projects they are governing. We are satisfied that the disciplines and rigour in BT's programme management frameworks are appropriate for managing programmes of such scale'.

90. The report made recommendations across nine areas. There were no recommendations that impacted this addendum or the Single Stage Business Case for the next phase.

Risk management

91. Inland Revenue's risk management approach recognises that major programme transformations are high-risk undertakings; and that a focused effort is required to ensure effective and successful delivery of the programme and associated business benefits. Risk will be mitigated by adopting preventive strategies that will reduce the impact or likelihood of risk occurring. The effectiveness of mitigation strategies will be regularly reviewed and updated with treatment owners.

92. The programme's risk management framework is fully aligned to corporate standards. The programme has fully adopted and applied the enterprise risk management policy and framework. For more information on how the programme will manage risks, refer to appendix F.

93. The key risks to the next phase of the programme are considered to be:

• the scope of the programme changes through the design phase due to changes in priorities: this will be mitigated by strong programme management and programme planning;

• the programme is unable to attract and retain the right people with the right skills for the design phase: this will be mitigated by the use of external expertise with proven capability;

27 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

• some stakeholders may feel that they have not had an opportunity to participate in the design phase: this will be mitigated by ensuring that engagement is representative of stakeholders; and

• the COTS solution selected at the end of high-level design may not fully meet Inland Revenue's detailed design requirements: this will be mitigated by ensuring all potential solutions are fully explored and evaluated.

28 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

7 The commercial case

94. Since the programme business case was last updated, Inland Revenue has:

• updated the programme's commercial model for design; and

. updated the products and services that the programme requires.

Commercial model for design

95. A prime model was identified as Inland Revenue's preferred model for design and implementation services in the programme business case. The market's ability to support a prime vendor model was tested through the procurement process. A further three approaches were identified as possible — consortium, service aggregation and selective sourcing12.

96. An extensive evaluation of the most appropriate commercial model for the programme has been undertaken over the past 12 months. This evaluation has included the following:

4, visits to reference sites, including other tax administrations, and discussions with short-listed vendors during the procurement process;

• uplifting of Inland Revenue's commercial management capability with the appointments of individuals with experience in management of complex commercial arrangements, for example the appointment of two Commercial Directors and an experienced Programme Director; and

• the delivery approach for Stage 1 - strategic, foundational and tactical work-streams — has created the need to consider the management of multiple vendors.

97. As a result of the detailed evaluation of other similar programmes as outlined above, in April 2014, the Programme Steering Committee (PSC)13 agreed to change the delivery model from prime to service aggregation for the design phase because:

• Inland Revenue now has more certainty around the scale and scope of the programme;

• Inland Revenue now has the skills and expertise to manage more complex commercial models;

. a service aggregation model offers greater flexibility and will allow Inland Revenue to select vendor(s) which best suit its needs; and

. it is the most common model adopted for large, technology-enabled change programmes.

12 Programme Business Case„ 22 October 2013, page 69 13 From 1 July 2014 Inland Revenue's governance arrangements changed, and the Programme Steering

Committee was replaced by the Portfolio Governance Authority.

29 COMMERCIAL IN CONFIDENCE / September 2014

Programme Business Case Addendum Business Transformation

Products and services required

98. A range of services and products have been and will be required to be sourced over the life of the programme. The services and products required for the design phase of the strategic work-stream and for the tactical work-stream are discussed within the single stage business case design and improving digital services.

99. The programme continues to offer opportunities to New Zealand suppliers. Recent and upcoming opportunities for the local market include the:

a) supply of a range of data management services;

b) supply of a business process mapping (BPM) tool;

c) supply of programme management services and tools; and

d) planned establishment of an open panel for the services and capabilities needed to support the transformation programme on an on-going basis.

100. The services required for the design phase are:

• design services provider for the duration of the design phase; and

• COTS provider(s) to participate in detailed design with the design partner.

101. The procurement process for selecting the design provider has been underway since October 2013 and is nearing completion. Inland Revenue has identified a preferred vendor to lead high-level design.

102. Inland Revenue will be engaging with the market for a COTS solution based on core tax and social policy functionality.

103. The Ministry of Business, Innovation and Employment (MBIE) has been consulted regarding the procurement process for selecting both the design provider and the COTS core application suite of software. The GCIO has been consulted regarding the selection of the COTS core application suite of software and has been invited to participate in this process.

30 COMMERCIAL IN CONFIDENCE / September 2014

Programme Business Case Addendum Business Transformation

Withheld under section 81 of the Tax Administration Act 1994

31 COMMERCIAL IN CONFIDENCE! September 2014

Programme Business Case Addendum Business Transformation

Withheld under section 81 of the Tax Administration Act 1994

Programme Business Case Addendum Business Transformation

Withheld under section 81 of the Tax Administration Act 1994

Programme Business Case Addendum Business Transformation

Withheld under section 81 of the Tax Administration Act 1994

Commissioner (CIR)

Naomi Ferguson

Investment Board (TB)

Membership:

• Commissioner (Chair) - Naomi Ferguson • Deputy Commissioner Change (Convenor) - Greg James • Chief Financial Officer - Giles Southwell • Chief People Officer - Jeanie TrueII • Chief Technology Officer - Myles Ward • Deputy Commissioner Corporate Integrity and Assurance

- Mary Craig • Deputy Commissioner Information, Intelligence and

Communications - Mike Cunnington • Deputy Commissioner Policy and Strategy - Struan Little • npniitv Crimmiccinnpr Sprvirp Dplivprv - Arlprip Whitp

Withheld under section 81 of the Tax Administration Act 1994

Senior Responsible Owner (SRO)/Programme Sponsor

Deputy Commissioner Change - Greg James

Programme Governance Authority (PGA)

The CIR has independent, statutory powers in relation to administration of the Tax Acts and protecting the integrity of the tax system. The CIR cannot be guided or governed by the Minister in applying tax laws; the CIR has both responsibility and accountability.

To ensure that Inland Revenue's investment portfolio is aligned to its strategic direction and delivers the benefits and capability required to support running, improving and changing the organisation.

Responsible for ensuring that the assigned programme or project meets its objectives and delivers the benefit enablers. The SRO ensures that the programme / project is prepared and reviewed at appropriate stages. The SRO also takes ownership of the business case. This role cannot be delegated. The role of the PGA is to govern the existing portfolio of programmes and

The CIR has accountabilities under the State Sector and Public Finance Acts, employment law, health and safety and other legislation. As well as well-understood splits between operational matters and governance responsibilities for Ministers.

The IB is responsible for: • making all investment decisions with regard to Inland

Revenue's single investment portfolio, in line with agreed investment objectives, the Government's and departmental priorities. It will maintain a multi-year investment focus, looking out over a four year horizon in line with Inland Revenue's Four Year Plan;

• governing prioritisation and investment decisions within the single investment portfolio according to four investment categories: Run, Improve, Change and External Imperatives; and

• ensuring appropriate enterprise-wide investment decisions are made, including balancing trade-offs between competing internal and external priorities, in order to maintain an optimised investment profile with regard to risk, cost, verifiable benefits and resourcing to deliver on agreed priorities.

Ensuring Inland Revenue allocates the necessary executive and financial commitment to the Programme. The SRO will undertake this role with the appropriate organisational accountability and power to maintain programme momentum in a dynamic business environment.

The PGA is responsible for: • governing projects and programmes within Inland

Programme Business Case Addendum Business Transformation

Appendix C — Governance roles and responsibilities

Overall governance of the programme will be provided by Inland Revenue, via the following governance structures.

Body

Role

Responsibilities

35 COMMERCIAL IN CONFIDENCE / September 2014

Programme Business Case Addendum Business Transformation

Membership:

• DC Change (Chair) - Greg James • Chief Financial Officer - Giles Southwell • Chief Technology Officer - Myles Ward • Deputy Commissioner Information, Intelligence and

Communications - Mike Cunnington • Deputy Commissioner Service Delivery - Arlene White

Withheld under section 81 of the Tax Administration Act 1994

Executive Working Committee (EWC)

Membership: • Deputy Commissioner Change (Chair) - Greg James • Chief Technology Officer - Myles Ward • Chief Financial Officer - Giles Southwell • Deputy Commissioner Service Delivery - Arlene White • Deputy Commissioner Information Intelligence 8c

Communications - Mike Cunnington • Programme Director (non-voting member) - Les Greeff

Programme Director

Les Greeff

projects to ensure good management control, accountability and benefits delivery out of the investments.

The EWC will own the programme and has overall responsibility for the delivery of the associated business outcomes. The EWC will have the responsibility for ensuring that the business devotes the necessary executive and financial commitment to the programme and has the organisational accountability and power to maintain programme momentum in a dynamic business environment.

The Programme Director is the appointed representative of Inland Revenue and ensures that the day-to-day business decisions are made for the programme. The primary responsibilities of this role include approving programme deliverables on behalf of Inland Revenue, taking overall responsibility for the timely delivery of Inland Revenue's obligations, allocating internal and contractor resources to the programme, monitoring significant risks in conjunction with the Programme Manager(s), disposing of business issues escalated for resolution

Revenue's single investment portfolio; • ensuring projects and programmes are managed well and

remain healthy from cost / benefit, timeline, quality and risk / issue perspective;

• raising project execution issues by reporting to the IB when projects fall out of specification; and

• ensuring that relevant quality assurance processes are adhered to.

The EWC is responsible for: • providing visible business support and endorsement for the

programme, thereby adding emphasis and support to all associated organisational change and benefits realisation issues;

• reviewing and approve deliverables, and make decisions required by the programme, within agreed Delegated Authorities;

• assisting the programme with any business engagement and senior stakeholder management issues;

• assisting with securing and appointing key senior business resources required by the programme, including key governance forums; and

• assisting the sub programmes and work-streams to resolve issues and risks, including removing organisational road blocks.

The Programme Director is responsible for: • overall governance and day to day management of

programme, including internal communications, and status updates to EWC, PGA, and executive leadership team (ELT) members;

• business case development and expediting for approval of the business case;

• all procurement and sourcing of all products and services required;

• contract management of all service provider(s) contracted for the required products and services;

• programme and project management - focus on deadlines, deliverables, costs, and quality of solution;

• driving the pace and schedule of the programme; • developing and enforcing programme methods and

standards;

36 COMMERCIAL IN CONFIDENCE! September 2014

Bod Role

Res . onsibilities

Programme Business Case Addendum Business Transformation

Bod Role Res . onsibilities

Design Councils

Four Design Councils will be in place:

• Business Process Design Council (BDC) - which will focus on decisions associated with future state business processes and the TOM

• Organisational Design Design Council (ODDC) - which will focus on decisions associated with future state organisational design

• Technical Architecture Design Council (TADC) - which will focus on decisions associated with future state technical and solution architecture

• Policy Design Council (PDC) - which will focus on decisions associated with the future state policy design.

Business Owners Forums (B0F5)

The BOF will be executed via five forums:

• Delivery Process Business Owner Forum (PBOF) - to represent the service delivery business functions

• Data Business Owner Forum (DBOF) - to represent the data business functions

• Analytics, Insights and Metrics Business Owner Forum (ABOF) - to represent the analytics, insights and metrics business functions

• Information and Knowledge Management Business Owner Forum (KBOF) - to represent the information

or escalating these issues for resolution to the EWC or PGA, approving and/or escalating programme change requests (PCRs), managing the overall programme budget including internal costs, and reporting programme progress to the PGA.

The Design Councils for the programme will provide executive authority for governing and controlling all design components associated with the programme. The Design Councils will have the authority to ratify any decisions relating to the designs developed by the programme, i.e., within the authorities delegated via the approved business case.

The BOFs will own the business processes across IR that will be incorporated into the BT solutions, and will ratify, refine and recommend changes to the existing business processes. The BOF's will ensure that the Future State business processes represent the optimum future state in terms of best practice relative to benchmarking research, and are fit for purpose to deliver the IR Target Operating Model and the IR for the

• business process definition; • stakeholder management and communications • organisational impact assessment; • organisational design and organisational change

management; • assistance with strategic integration of major change

initiatives; • learning and development (transactional change

management and capability build); • design of business transformation interventions; • aligning the programme to business strategy; • benefits tracking and realisation, including organisational

effectiveness; and • coordination and control of communications and

stakeholder management associated with the programme. The Design councils are responsible for: • providing strategic design authority oversight across the

programme, and to ensure that all associated designs are compatible with, and align to, approved strategies, standards, policies, and roadmaps;

• providing assurance to the IB that the programme is delivering anticipated outcomes and designs that are aligned with key design principles and approved design strategies

• reviewing design options presented and make appropriate design decisions; and

• ensuring the effectiveness of data quality management, and data governance, systems within the organisation.

The BOFs are responsible for: • representing a wide range of business functions, act as

advocates of the Inland Revenue culture and will be the channel in and out of the business;

• representing and recommend sign-off the 'to-be' processes whilst ensuring buy-in from relevant parties;

• working closely with programme management to ensure acceptance of programme changes (process, organisation and technology);

• ensuring that future business process design is aligned to the Benefits Realisation Strategy and Plan as defined in the programme business case and the detailed business cases

37 COMMERCIAL IN CONFIDENCE! September 2014

and knowledge management business functions

Future. submitted to Treasury and Cabinet; and • Information System Business Owner Forum (BOF) - to • reviewing all key deliverables within their areas of

represent the information systems and technology responsibility and will ensure that all business process business functions. content is fit-for purpose and appropriate and relevant to

deliver the IR TOM and IR for the Future. Foundation Executive Working Committee (FEWC)

The FEWC is responsible for providing

The FEWC is responsible for:

management and sponsorship • providing oversight across the foundation sub programme; oversight for the foundation sub • providing assurance to the PGA that the foundation sub programme and making programme is delivering anticipated outcomes and benefits implementation decisions related to

to the agreed scope, timescale and budget;

the execution of the initiatives included • ensuring alignment to the outcomes defined in the within this sub programme, as defined

Programme Charter, and in the foundation Initiative Briefs;

in the Foundation Sub Programme • monitoring the sub programme's risk profile and to work Charter, within the constraints defined

with the PGA and programme leadership team (PLT) to

by the PGA, and as approved in the effectively manage risks; Initiative Briefs approved at the TB on • providing oversight of quality assurance activities being 04 March, 2014. undertaken across the foundation sub programme; and

• providing formal approval of planned deliverables, or to provide appropriate Delegated Authority to other governance bodies or individuals as required.

Tactical Executive Working Committee (TEWC)

The TEWC is responsible for providing