presented to: association of credit union internal auditors 22 nd annual conference presented by:...

TRANSCRIPT

FRAUD AND INTERNAL

AUDIT’S ROLEPresented to:

ASSOCIATION OF CREDIT UNION INTERNAL AUDITORS

22nd ANNUAL CONFERENCE

Presented By:

Tiffany R. Couch, CPA/CFF, CFE

Principal, Acuity Group PLLC

OBJECTIVES

IntroductionFraud and Today’s Business

Climate Understanding Fraud BasicsFinancial Services - StatisticsInternal Audit’s Role

FRAUD AND TODAY’S BUSINESS CLIMATE

High Profile Headlines

Banking Crisis

Housing Crisis

MF Global – Client Trust Money

Missing?

Solyndra

• Layoffs

• Foreclosures

• Personal Debt at all time high

• Fuel and costs of goods & services

READ THE HEADLINES - EMPLOYEES

Layoffs

Frozen Credit

Health Care “Reform”

Increased Costs Fuel Goods Freight

READ THE HEADLINES - EMPLOYERS

FRAUD AND TODAY’S BUSINESS CLIMATE

PRESSURE

UNDERSTANDING FRAUD BASICS

OPPORTUNITY

PRESSURE RATIONALIZATION

OCCUPATIONAL FRAUD –Using one’s occupation for unauthorized personal gain through deliberate misuse of the employing entity’s resources or assets.

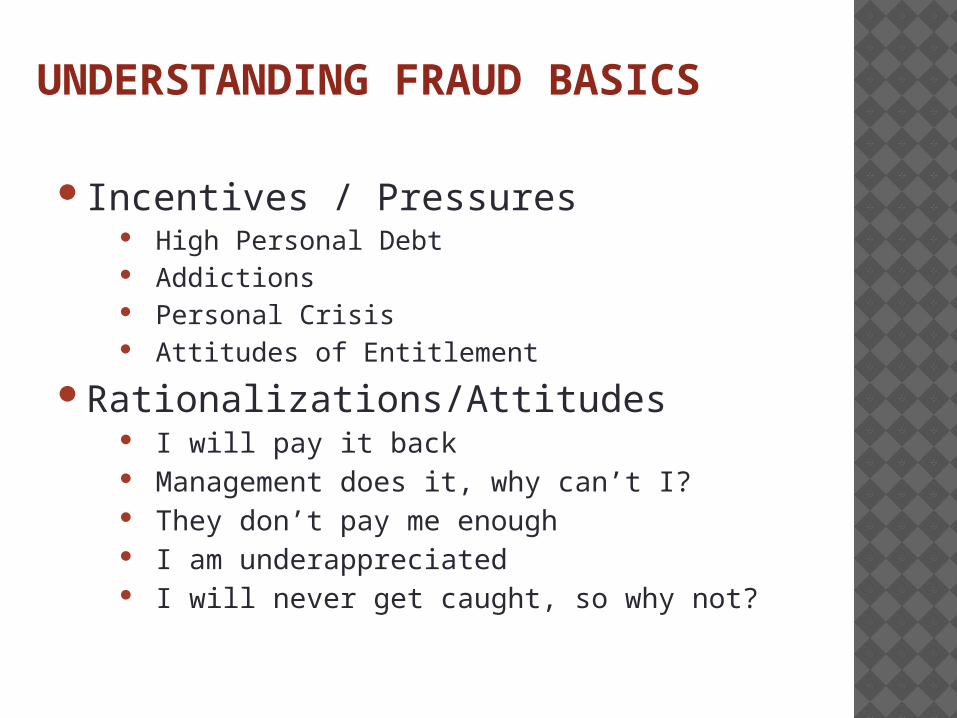

UNDERSTANDING FRAUD BASICS

Incentives / Pressures High Personal Debt Addictions Personal Crisis Attitudes of Entitlement

Rationalizations/Attitudes I will pay it back Management does it, why can’t I? They don’t pay me enough I am underappreciated I will never get caught, so why not?

Opportunity

FRAUD SCHEMES DEFINED

Asset Misappropriation Skimming /Larceny Billing Schemes Check forgery Expense Reimbursement Schemes Payroll Schemes

Corruption Kickbacks Self-Dealing

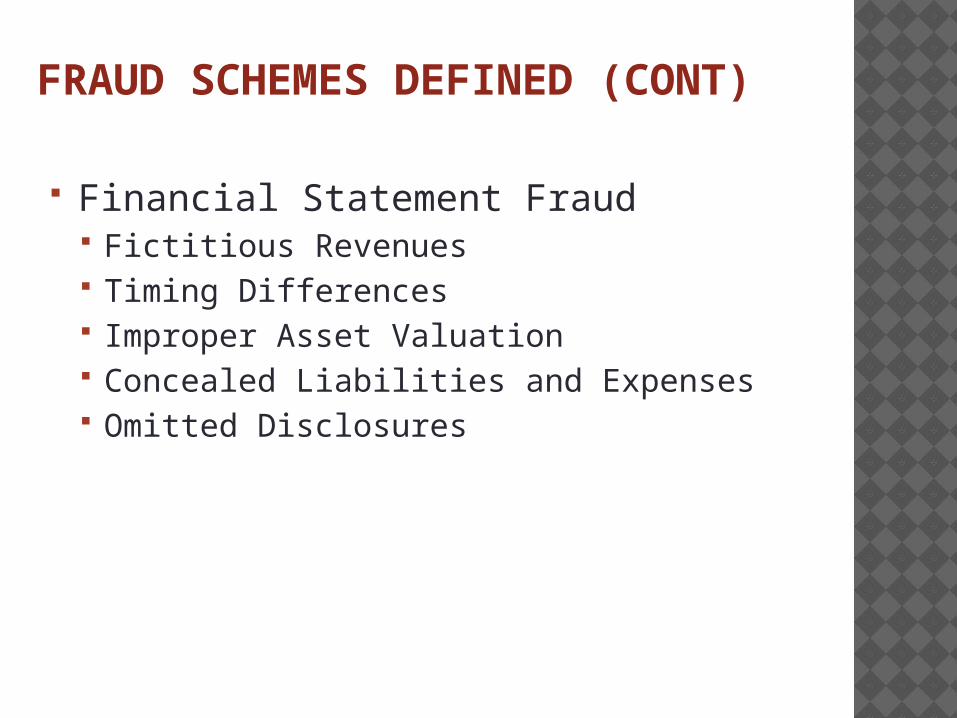

FRAUD SCHEMES DEFINED (CONT)

Financial Statement Fraud Fictitious Revenues Timing Differences Improper Asset Valuation Concealed Liabilities and Expenses Omitted Disclosures

METHODS OF FRAUD

7.6%

33.4%

86.7%

% of All Cases

Fraudulent Financial Statements ($1,000,000)

Asset Misappropriation ($120,000)

Corruption ($250,000)

Note: The sum of percentages on this chart exceeds 100% because a number of cases involved multiple schemes that fell into more than one category.Courtesy of ACFE - 2012 Global Fraud Study

Financial Services

Construction

Religious, Charitiable, Social Services

Services (Professional)

Insurance

Retail

Education

Health Care

Manufacturing

Government and Public Administration

Banking and Financial Services

0.0% 5.0% 10.0% 15.0% 20.0%

3.4%

3.5%

4.0%

5.7%

6.1%

6.4%

6.7%

10.1%

10.3%

16.7%

4.3%

4.9%

2.8%

5.1%

6.6%

5.0%

5.9%

10.7%

9.8%

16.6%

20102012

STATISTICS – BY INDUSTRY

Courtesy of ACFE 2012 Report to the Nations

STATISTICS - FINANCIAL SERVICES229 CASES

Courtesy of ACFE 2012 Report to the Nations

SCHEMENUMBE

R OF CASES

PERCENT OF

CASES

Corruption 83 36.2%

Cash on Hand 48 21.0%

Cash Larceny 29 12.7%

Billing 29 12.7%

Non-Cash 24 10.5%

Financial Statement Fraud

22 9.6%

Skimming 21 9.2%

Check Tampering 21 9.2%

Expense Reimbursements

13 5.7%

Register Disbursements 9 3.9%

Perpetrators

PERPETRATORS

Courtesy of Association of Certified Fraud Examiners (2012 Report to the Nations)

Less than 1 Year

1 to 5 Years 6 to 10 Years More than 10 Years

$-

$50,000

$100,000

$150,000

$200,000

$250,000

Tenure of Perpetrator – Median Loss

Tenure of Perpetrator

Med

ian

Loss

KEY RED FLAGS - EMPLOYEES

Behavioral Red Flags Living Beyond Means

Financial Difficulties

Unusually Close Association with Vendor or Customer

Control Issues, Unwillingness to Share Duties

Wheeler-Dealer Attitude

Irritability, Suspiciousness or Defensiveness

Addiction Problems

Refusal to Take Vacations

Detection

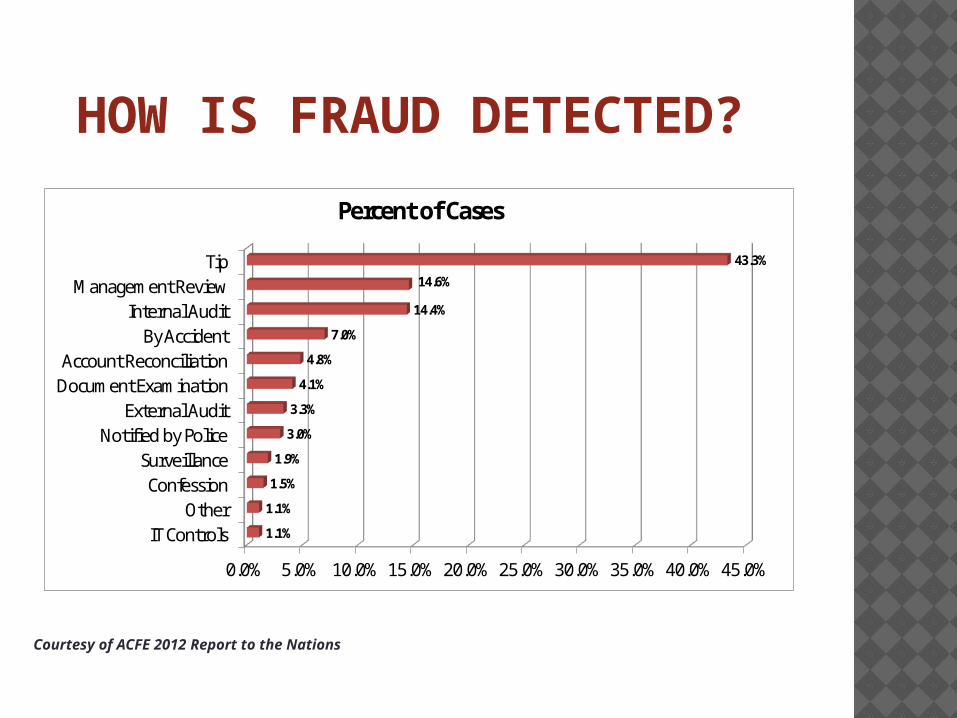

HOW IS FRAUD DETECTED?

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0%

IT ControlsOther

ConfessionSurveillance

Notified by PoliceExternal Audit

Document ExaminationAccount Reconciliation

By AccidentInternal Audit

Management ReviewTip

1.1%

1.1%

1.5%

1.9%

3.0%

3.3%

4.1%

4.8%

7.0%

14.4%

14.6%

43.3%

Percent of Cases

Recession, Recipe for Fraud?

Courtesy of ACFE 2012 Report to the Nations

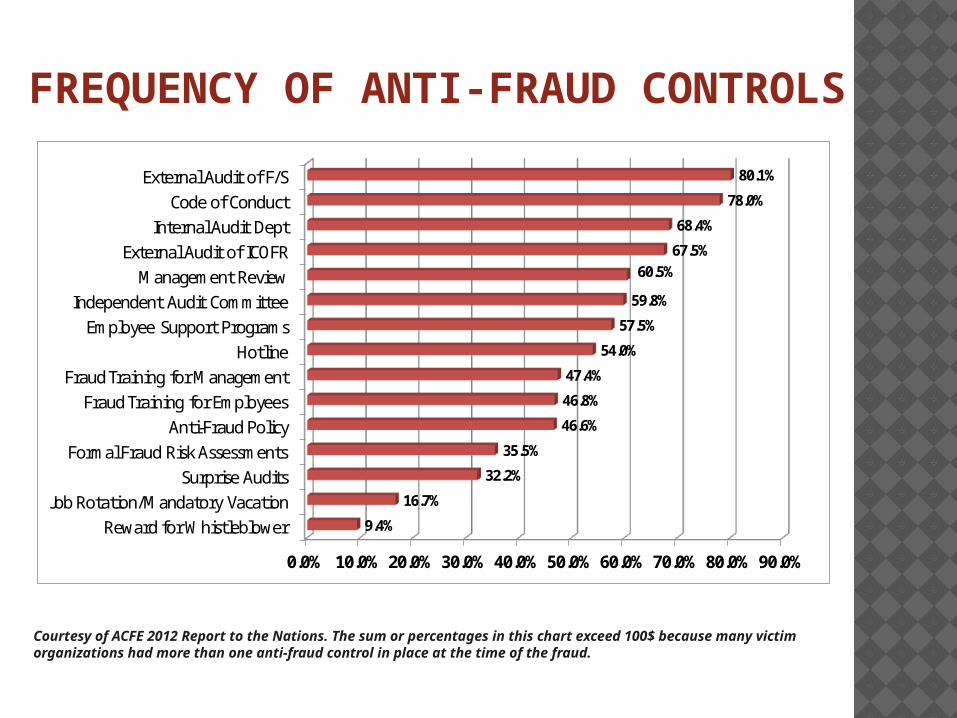

FREQUENCY OF ANTI-FRAUD CONTROLS

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0%

Reward for WhistleblowerJob Rotation/Mandatory Vacation

Surprise AuditsFormal Fraud Risk Assessments

Anti-Fraud PolicyFraud Training for Employees

Fraud Training for ManagementHotline

Employee Support ProgramsIndependent Audit Committee

Management ReviewExternal Audit of ICOFR

Internal Audit DeptCode of Conduct

External Audit of F/S

9.4%

16.7%

32.2%

35.5%

46.6%

46.8%

47.4%

54.0%

57.5%

59.8%

60.5%67.5%

68.4%

78.0%

80.1%

Recession, Recipe for Fraud?

Courtesy of ACFE 2012 Report to the Nations. The sum or percentages in this chart exceed 100$ because many victim organizations had more than one anti-fraud control in place at the time of the fraud.

INTERNAL AUDIT

Change your Mindset

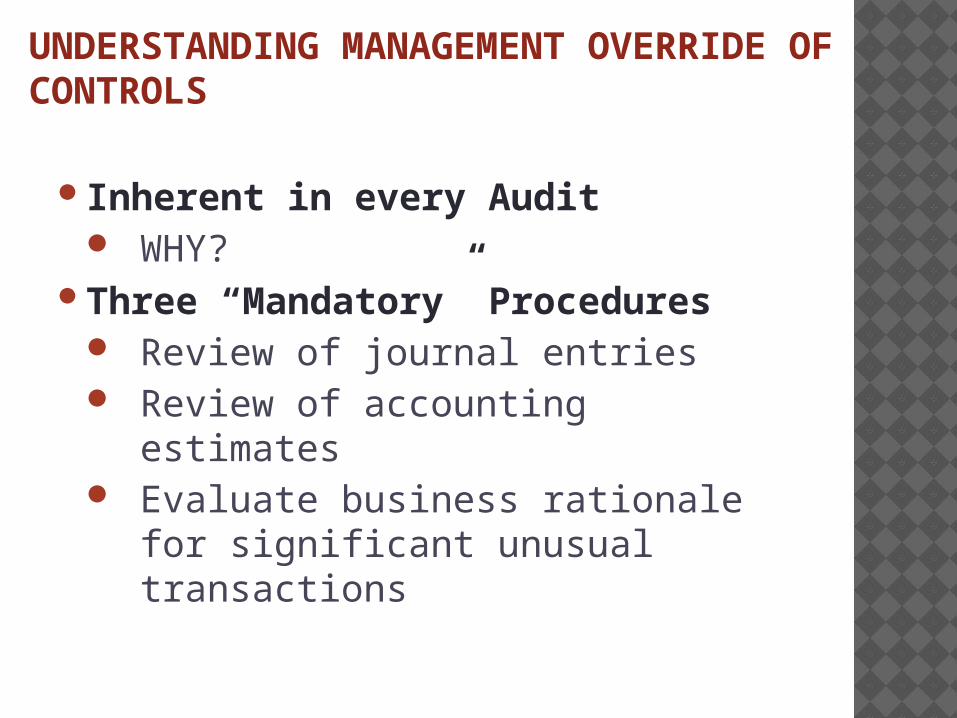

UNDERSTANDING MANAGEMENT OVERRIDE OF CONTROLS

Inherent in every Audit WHY?

Three “Mandatory” Procedures Review of journal entries Review of accounting estimates Evaluate business rationale for

significant unusual transactions

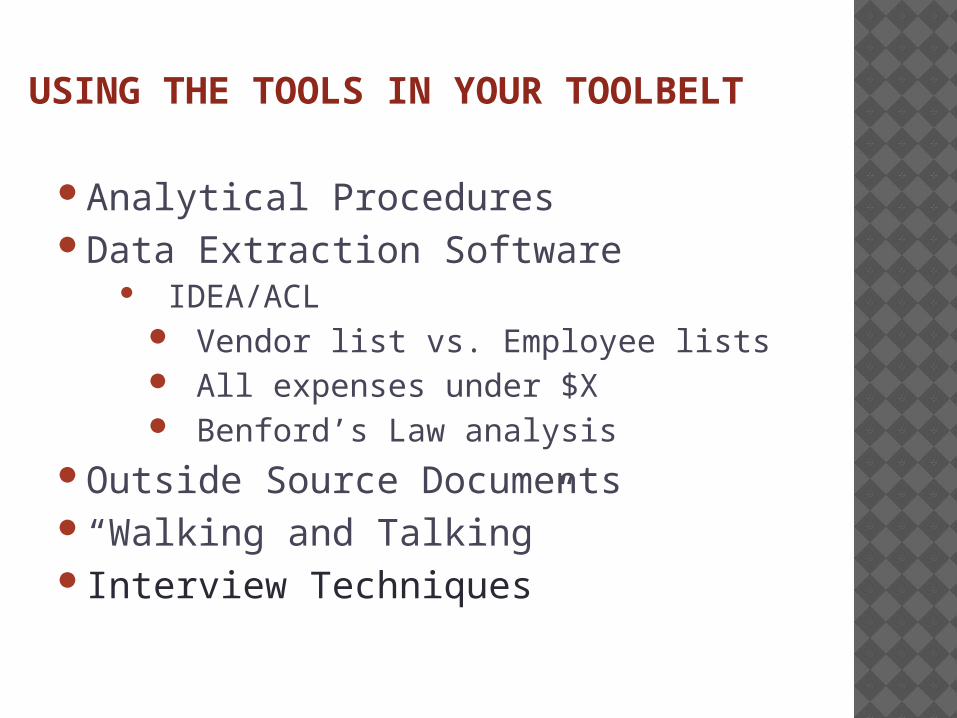

USING THE TOOLS IN YOUR TOOLBELT

Analytical ProceduresData Extraction Software

IDEA/ACL Vendor list vs. Employee lists All expenses under $X Benford’s Law analysis

Outside Source Documents“Walking and Talking” Interview Techniques

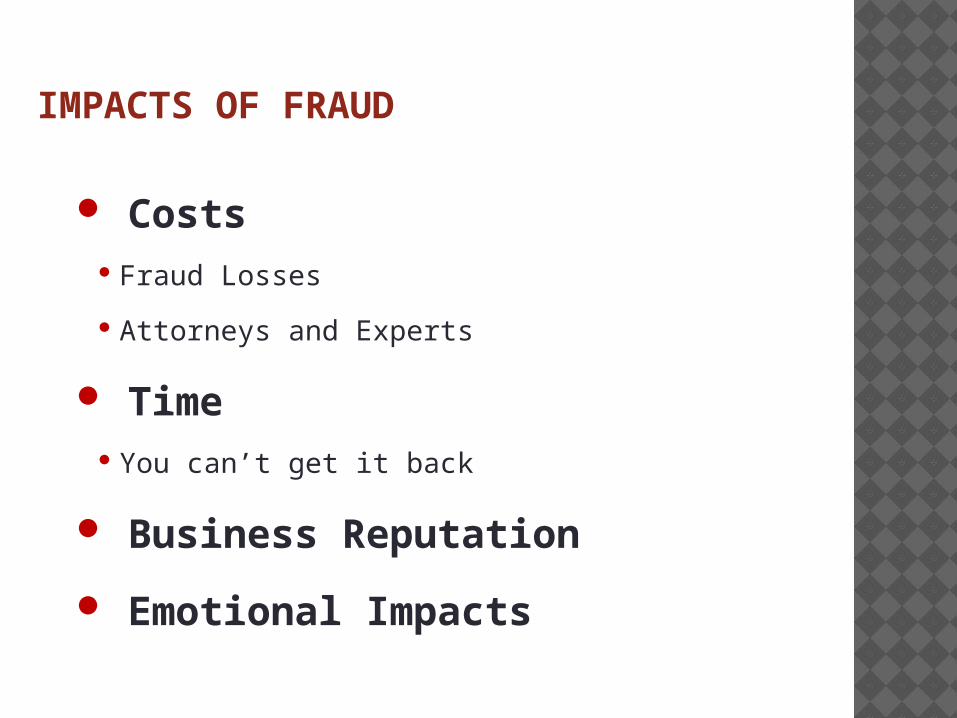

IMPACTS OF FRAUD

Costs Fraud Losses

Attorneys and Experts

Time You can’t get it back

Business Reputation

Emotional Impacts

REMEMBER – TRUST IS NOT AN INTERNAL CONTROL!

THANK YOU AND Q&A

“It’s only when the tide goes out that you learn who’s been swimming naked”

- Warren Buffet

CONTACT INFORMATIONTiffany R. Couch, CPA/CFF, CFE

Acuity Group PLLC360-573-5158