policy and regulation for sustainable microfinance: country experiences in asia

TRANSCRIPT

POLICY AND REGULATION FORSUSTAINABLE MICROFINANCE:COUNTRY EXPERIENCES IN ASIA

PAUL B. MCGUIRE*

The Foundation for Development Cooperation, Brisbane, Australia

Abstract: This article considers the policy and regulatory environment for micro®nance

in Asia. It identi®es eleven criteria for `good practice' in policy and regulation, covering

the policies of governments and donor agencies to support micro®nance; the regulation

of non-bank micro®nance institutions; and the regulation of banks. It then grades the

performance of nine countries in Asia. It concludes that there is scope for improvement

in all nine countries. Overall, Philippines and Bangladesh have the policy and regulatory

environments that are most conducive to sustainable micro®nance, while Pakistan has

the one that is least conducive. However, di�erent countries have strengths in di�erent

areas, and no country is strong in all areas. Copyright # 1999 John Wiley & Sons, Ltd.

1 INTRODUCTION

It is now generally accepted that micro®nance has an important role in povertyreduction. By providing ®nancial services to poor households that do not have accessto formal ®nancial institutions, it can assist them to establish or expand viablemicroenterprises in the informal sector of the economy. However, the outreach ofmicro®nance remains very small compared with the potential demand. The Bank Poor'96 Regional Workshop on Micro®nance for the Poor in Asia-Paci®c found that:

Essentially, the task of outreach remains to be done. Of the target poorhouseholds in Asia-Paci®c, less than 5 per cent have access to ®nancial services.If we exclude BangladeshÐ the only country where truly large numbers havebeen reachedÐ the number to whom micro®nance services have been extendedfalls to less than 1 per cent of the target group (Getubig et al., 1997, p. 10).

If micro®nance is to make an important contribution to poverty reduction in theregion, the micro®nance sector will need to develop to the stage where it canreach large numbers of poor people on a sustainable basis. This requires increased

CCC 0954±1748/99/050717±13$17.50Copyright # 1999 John Wiley & Sons, Ltd.

Journal of International DevelopmentJ. Int. Dev. 11, 717±729 (1999)

* Correspondence to: Paul McGuire, PO Box 10445 Adelaide Street, Brisbane, QLD 4000, Australia.

attention to all aspects of micro®nance. There has been considerable research onhow individual micro®nance institutions1 (MFIs) can increase their outreach andsustainability, but until recently there has been very little research on the policy andregulatory environment in which they operate. This is changing, with a number ofstudies focusing on the regulatory framework having been published since 1997 (seeBerenbach and Churchill, 1997; Jansson and Wenner, 1997; Rock and Otero, 1997;and McGuire et al., 1998).

This article considers the policy and regulatory environment for micro®nancefrom a broad perspective, and with a particular focus on Asia. It is based oninterviews with around 250 micro®nance practitioners, bankers, regulators andpolicymakers in the region, as well as an extensive review of relevant documents andprevious studies. It identi®es eleven criteria for `good practice' in policy andregulation in terms of contributing to sustainable micro®nance, and grades theperformance of nine countries, namely Bangladesh, India, Indonesia, Malaysia,Nepal, Pakistan, Philippines, Sri Lanka and Thailand, on each of these criteria.

The eleven criteria fall into three categories. Section 2 looks at four criteria relatingto the policies of governments and donor agencies to provide direct support tomicro®nance. Five criteria relating to the regulatory environment for non-bank MFIsare considered in Section 3. Section 4 considers two criteria relating to the regulationof banks insofar as it a�ects the scope for banks to engage in micro®nance, whileSection 5 o�ers some concluding comments.

Grades are awarded as follows:

. The country which best meets the particular criterion is awarded an `A'. Othercountries that are judged to be broadly comparable in terms of that criterion arealso awarded an `A'.

. The country or countries that are judged to have the least conducive environment interms of the particular criterion are each awarded a `C'.

. Other countries with middle positions are given a rating of `B'.

The only exception to this relates to one criterion where no country is judged to have aclear regulatory environment and no country receives an `A'. This case is discussedbelow.

None of the criteria can readily be quanti®ed, and the grades are based onqualitative judgements. Other commentators may well come to di�erent conclusionsabout both the criteria for determining a good policy and regulatory environment,and the grades awarded to individual countries. The grades should not be regarded asde®nitive, but are designed to identify areas in each country where there may be scopefor policy reform and to encourage debate.2

1 MFIs are generally considered to be specialist institutions which provide ®nancial services, predomi-nantly credit and savings facilities, targeted to poor households. Most are non-government organizations(NGOs), although some may be registered as co-operatives or banks, or may adopt other organizationalforms. Other institutions, including more `traditional' co-operatives and banks, may also providemicro®nance services to poor households in addition to their other activities.2 Much more detailed discussion of the policy and regulatory environment in each country is contained inthe country annexes in McGuire et al. (1998). However, that study does not attempt to grade the countries,and the grades re¯ect the views solely of this author.

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

718 P. B. McGuire

2 ARRANGEMENTS FOR DIRECT SUPPORT OF MICROFINANCE

Active support from government and/or donor agencies, including direct ®nancialsupport, is a necessary catalyst to the establishment of a viable micro®nancesector. While MFIs should strive for self-su�ciency, attaining it takes a considerableperiod of time. To set up their programmes and for a number of years there-after, MFIs need to be subsidized. Expanding to achieve economies of scale alsorequires a considerable input of resources for capacity building and institutionaldevelopment.

On the other hand, it should be stressed that much support has been wasted orhas even been counter-productive. To be e�ective, support should focus explicitly onmaximizing the outreach and sustainability of the micro®nance sector. Moreover, therole of government should generally be to make policy and create an enablingenvironment. Direct provision of micro®nance services by government has rarely beensuccessful, and is likely to damage the longer term sustainability of the micro®nancesector.

Criterion 1: Support for Individual MFIs

Specialist non-government MFIs in all countries have received support from thegovernment and/or donor agencies. In the past, most of this has been in the form of®nancial assistance direct to individual MFIs. This support has been critical inenabling them to establish, and to increase their outreach and self-su�ciency.Without this support, it is unlikely that there would be a micro®nance sector at all, inthe sense of specialist MFIs providing ®nancial services to the poor in an innovativeand commercially viable manner.

Bangladesh has by far the largest micro®nance sector of the nine countries.The Grameen Bank has received support from the central bank from as early as 1979,and by end 1995 had received donor grants of some US$84 million. Some 250 MFIsare currently receiving donor support. While ®rm data are not available it is apparentthat MFIs have received more support in Bangladesh than in any other country,and Bangladesh scores an `A' on this criterion. India, Malaysia, Nepal, Philippinesand Sri Lanka all have signi®cant MFIs that have been underpinned by governmentand/or donor assistance, and they each receive `B' on this criterion. By contrast,in Indonesia, Pakistan and Thailand there has been relatively little support forspecialist MFIs, and such institutions have achieved limited outreach. They are eachgraded `C'.

Nevertheless, it should be noted that development of micro®nance and thesuccess of leading MFIs owes more to the vision of their founders and management,than to the criteria used by government and donor agencies for supporting them. Inall countries support has been largely ad hoc in nature, and has generally not beenexplicitly designed to maximise the twin objectives of outreach and sustainability inthe most cost-e�ective manner. The Guiding Principles for Selecting and SupportingIntermediaries agreed by major donor agencies in October 1995 (Committee ofDonor Agencies, 1995) provide a number of suggestions as to how support by donorsand government can best be directed to maximizing outreach and sustainability.

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

Policy and Regulation for Sustainable Micro®nance 719

Criterion 2: Support Through Apex Institutions

Most countries included in the study have some form of o�cial `apex' or `second tier'micro®nance institution which channels funds from the government and/or donoragencies to individual MFIs. Where they operate well, apex micro®nance institutionscan be an e�ective means for supporting MFIs. It is much more e�cient for oneinstitution to analyse and monitor the performance of individual MFIs than fordi�erent government and donor agencies to do their own appraisals and evaluations.Moreover, if all the support for a particular MFI can be channelled through oneagency, it is much easier to ensure that such support is complementary and directed tothe same objectives.

At the same time, experience points to a number of issues that need to be addressedto ensure that apex institutions operate on a sound basis. They are unlikely to bee�ective unless there is already a strong group of retail MFIs in the country concerned.Moreover, apex institutions should establish and enforce appropriate performanceand reporting standards for the MFIs that they fund. They should avoid unrealisticdisbursement targets which may cause them to lower their standards. They shouldavoid restrictive interest rate policies. They should develop appropriate criteria forfunding scaling-up, institutional development and equity, as well as providingloanable funds. And it is critical that apex institutions operate as independent entitiesand are not politicized. The role of apex institutions is discussed in more detail inMcGuire (1998).

The largest and most successful apex institution is the Palli Karma SahayakFoundation (PKSF) in Bangladesh, and Bangladesh is given an `A' on this criterion.Apex institutions are also an important part of the micro®nance sector in India, thePhilippines, Sri Lanka and Thailand, but none has yet achieved the performance ofPKSF. In some cases this re¯ects de®ciencies in their operations and procedures. InIndia, for instance, the major apex institutions infringe certain `good practice' criteria,such as imposing ceilings on the interest rates that their partner MFIs can chargeborrowers, at levels which make it di�cult if not impossible for the MFIs to achieveself-su�ciency. Some commentators suggested that the performance of the NationalDevelopment Trust Fund (NDTF) in Sri Lanka had been a�ected by politicization.These four countries each receive a `B'. The remaining four countries do not yet haveapex micro®nance institutions of any signi®cance, and they each score a `C'. Never-theless, it should be stressed that these ratings are subjective, and it may be better not tohave an apex institution at all, than to have one that does not meet certain key criteriaof good practice.

Criterion 3: Absence of Distortionary Support Programmes

Most if not all countries have various policies or programmes designed to extend®nancial services to the poor which are not successful and which may `crowd out'more successful MFIs, or otherwise infringe norms of good practice. These pro-grammes also generally provide one time ®nancial services with high transaction costsfor both the lender and borrower, rather than continued access to ®nancial services onan ongoing basis.

Seven of the nine countries included in the study impose directed credit require-ments, whereby banks are required to lend a certain proportion of their loan portfolio

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

720 P. B. McGuire

to particular sectors. Direction is an ine�cient means of reaching the poor, andimposes economic costs.

In some countries, the government operates speci®c micro®nance programmes inwhich funds are channelled through the banks. The largest of these programmes is theIntegrated Rural Development Programme (IRDP) in India, but a number of othercountries also have them. Such programmes have generally not been successful andmay crowd out or undercut specialist MFIs, although there are some exceptions suchas certain programmes channelled through Bank Rakyat Indonesia and the ruralbanks in Indonesia.

Another category of micro®nance programmes is those operated directly bygovernment agencies. The largest and possibly the most successful such programme isthe RD-12 programme of the Bangladesh Rural Development Board (BRDB), buteven its performance is not as good as that of leading MFIs in Bangladesh. Very fewother direct government programmes are successful.

In a number of countries, governments have `forgiven' certain categories of smallloans under their own programmes or those of state commercial banks. Theseepisodes have created major problems for MFIs.

All countries have some distortionary programmes of at least one of the typesdiscussed above. India, Indonesia, Pakistan, Sri Lanka and Thailand all haveunsustainable and/or unsuccessful mass programmes, operated either through banksor by government agencies. In India, Pakistan and Thailand the programmes o�ersubsidized interest rates, su�er from poor repayment performance and are unsustain-able. In Indonesia and Sri Lanka the programmes are more recent, but are notdesigned to be sustainable. These countries each receive a `C' on this criterion.Malaysia, Nepal and Philippines generally show greater reliance on market forces, butthere are still a number of distortions in their micro®nance programmes. Thesecountries are rated `B'. Bangladesh is one of only two countries to have abolished alldirected credit schemes, and does not have any signi®cant programmes channelledthrough banks. As discussed above the major government programme operates betterand is less distortionary than comparable programmes in other countries. Bangladeshis awarded an `A' on this criterion.

Criterion 4: Environment for Bank/NGO Linkages

One important way in which commercial banks can become involved in micro®nanceis through linkages with NGOs and self-help groups (SHGs). This approachcombines the strength of commercial banks in ®nancial management with the abilityof NGOs to reach the poor.

The only country included in the study with speci®c regulatory impediments to suchlinkages is Pakistan, and it receives a `C' on this criterion. However, other than in Indiaand Indonesia, there is little positive support for linkages from policy makers. Even inIndia the programme is not sustainable because the mark-ups that banks and NGOscan charge do not provide a su�cient margin for NGOs to recover the costs of formingand motivating SHGs. However, because they are well ahead of all other countriesstudied, India and Indonesia are given `A' for this criterion. The remaining sixcountries each score `B'.

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

Policy and Regulation for Sustainable Micro®nance 721

3 REGULATION OF NON-BANK MICROFINANCE INSTITUTIONS

The regulatory environment for MFIs is very important if the micro®nance sectoris to achieve signi®cant outreach on a sustainable basis. On the one hand, if MFIs areto ¯ourish they should be able to operate relatively freely without unnecessaryrestrictions, and charge interest rates and fees that are su�cient to cover their costs.On the other hand, it is appropriate to have some kind of framework to encourageMFIs to meet certain minimum performance and reporting standards, and toimprove their performance gradually over time.

Criterion 5: Broad Regulatory Framework for MFIs

In most countries, MFIs are able to obtain registration under the general provisionsapplying to NGOs and co-operatives. The broad requirements, such as having amemorandum of association or some similar document and preparing an annualreport and ®nancial statements, are quite simple and should pose no problem to anywell-managed MFI. The only exceptions to this appear to be Malaysia and Thailand,where the usual registration procedures for NGOs may not permit an institution toengage in micro®nance. These countries are graded `C' for this criterion.

In some cases MFIs are subject to unnecessary and burdensome rules and regula-tions after registration, and the rules are not transparent. Often, regulatory agencieshave considerable discretionary power. In India, Indonesia, Nepal, Pakistan and SriLanka, co-operative societies are heavily regulated. In India, NGOs are subject todetailed registration and reporting requirements where they receive foreign donations.In Indonesia, Nepal, Pakistan and Sri Lanka relations between the government andthe NGO movement have at times been strained, and in some cases have ¯uctuatedwith changes in the political landscape. These countries each rate a `B'.

Bangladesh and Philippines are each awarded an `A' on this criterion. While thereare still some unnecessary restrictions (such as some of those imposed by the NGOA�airs Bureau in Bangladesh), the political climate is generally more favourable toNGOs than in the other countries. This may re¯ect in part the role of the NGOmovement and NGO leaders in the war of independence in Bangladesh, and theoverthrow of the Marcos regime in the Philippines.

It should also be noted that in many countries, the requirements for registration arenot enforced rigorously. In some countries, this may have enabled some unscrupulousoperators to set up and take advantage of clients. It would seem appropriate forNGOs engaged in micro®nance to be required to be registered, and for regulatoryagencies to undertake simple monitoring of their activities to reduce the scope forfraud.

Criterion 6: Absence of Interest Rate Restrictions

Generally, interest rate ceilings and other restrictions on interest rates impede thedevelopment of micro®nance on a sustainable basis. Only two countries, Nepal andThailand, impose general ceilings on the interest rates that MFIs can chargeborrowers. In both of these countries, the ceilings are generally too low for MFIs to

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

722 P. B. McGuire

cover their costs. In fact, in Thailand this is implicitly recognized by regulatoryagencies, in that they do not enforce the ceilings. These two countries are each given a`C' on this criterion.

In other countries, there is no general ceiling applying to MFIs. However, this doesnot always mean that MFIs are free to determine their own interest rates. In Indiathere are ceilings on interest rates that can be charged by MFIs participating invarious government micro®nance programmes. In Pakistan and to a lesser extentMalaysia, MFIs have been constrained by an overall social and political climate thatmakes it di�cult for them to charge interest rates su�cient to cover their costs. Thesecountries each score a `B' on this criterion. By contrast, in Bangladesh, Indonesia,Philippines and Sri Lanka the climate o�ers greater encouragement to MFIs to setinterest rates on the basis of sustainability, and these countries receive an `A'.

Criterion 7: Progress on Performance Standards

It is generally agreed that where MFIs do not accept deposits from the public, it isunnecessary to subject them to formal prudential regulation and supervision by agovernment agency.3 In most countries, there would also be signi®cant practicaldi�culties in subjecting MFIs to prudential regulation and supervision. MFIs whichdo not accept deposits from the general public are not subject to prudential regulationor supervision by a government agency in any of the nine countries included in thestudy. There are also no compulsory reporting requirements designed speci®cally withthe needs of MFIs in mind.

Nevertheless, it is clear that at present most MFIs do not have adequate standards.For instance, in an analysis of MFIs in Bangladesh, the World Bank (1996) noted thatthe accounting, management information systems and external audit policies andstandards followed by the large MFIs are good and comprehensive. However, for themost part, the standards adopted by the small and medium MFIs need to besubstantially upgraded. Similarly in the Philippines, Llanto et al. (1996) found that anumber of major MFIs have inadequate ®nancial reporting and monitoring, makingit di�cult to determine past due loans and the extent of arrears. More generally, thesurvey of MFIs conducted by Sustainable Banking with the Poor (1996) found that agreater emphasis on ®nancial monitoring and reporting using standardized account-ing is needed. The challenge is to ®nd cost-e�ective ways of improving the standards,in terms of both performance and reporting, of the large numbers of MFIs that arenot currently operating on a sound basis.

In those countries with apex micro®nance institutions, these institutions can playa very important role in developing standards for the micro®nance sector. This role®ts in well with their other activities. Moreover, such institutions have an e�ectivemechanism for enforcing any standards that they develop, as any MFIs which borrowfrom them, or intend to borrow from them in the future, will need to meet the requiredstandards. However, apex institutions are not the only means for establishingperformance and reporting standards. Other possibilities include credit rating agenciesand self-regulation (discussed below). These options are not mutually exclusive.

3 See, for instance, CGAP (1996), Berenbach and Churchill (1997) and McGuire et al. (1998)

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

Policy and Regulation for Sustainable Micro®nance 723

While no country has yet developed a comprehensive framework of performanceand reporting standards, Palli Karma Sahayak Foundation (PKSF) in Bangladesh isa leader in this area, and Bangladesh is graded `A' on this criterion. So is the Philip-pines, where the Philippine Coalition for Micro®nance Standards, which includesMFIs, the People's Credit and Finance Corporation (PCFCÐan apex institution),the central bank, government and donor agencies, among others, has developed andis promoting standards for MFIs.

In Sri Lanka and Thailand, apex institutions are making some progress inestablishing standards for the MFIs that they fund, and these countries each rate a`B'. In India there are three `o�cial' apex institutions but none has focused to anygreat extent on standards for MFIs, and there is little co-ordination between them.Indonesia, Malaysia, Nepal and Pakistan do not currently have signi®cant apexinstitutions, and other initiatives to establish standards for MFIs, where they exist atall, are at a very early stage. These ®ve countries are each given a `C'.

Criterion 8: Progress on Self-regulation and Establishing Networks of MFIs

Another approach to establishing performance and reporting standards for MFIs isthrough self-regulation. Self-regulation may take a wide variety of forms, rangingfrom a voluntary code of conduct to which MFIs agree to adhere, to a rigorouslicensing system administered by an apex body and backed by the force of law.The feasibility of various forms of self-regulation depends on a range of factors,including the extent to which there is a network that can represent MFIs as a whole,the quantum of resources available for monitoring and supervision, and theavailability of incentives and/or sanctions to enforce compliance. Networks alsohave the potential to undertake a range of other activities, including informationexchange, training, research, and policy dialogue with government and donoragencies.

The Philippine Coalition for Micro®nance Standards, discussed above, is the mostimportant initiative for self-regulation in the region, and the Philippines is awarded an`A' on this criterion. Bangladesh is the only other country with a well establishednetwork for MFIs, and it receives a `B'. The other seven countries each score a `C'. Itshould be noted, however, that there have been recent moves to establish networks ofMFIs in a number of countries, including India, Pakistan and Sri Lanka. Thesemoves should be encouraged.

Criterion 9: Clarity for Savings Mobilization

In general, MFIs are not permitted to accept deposits from the general public unlessthey establish regulated banks, although there are several exceptions to this in thecountries included in the study. Prohibiting non-bank MFIs from accepting depositsfrom the public is generally appropriate, as accepting deposits from the public places avery heavy responsibility on any institution.

While the question of mobilizing savings from members is a di�cult onefor regulators, there is considerable evidence that there is a strong demand bypoor households for reliable savings facilities. Moreover, requiring borrowers to

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

724 P. B. McGuire

demonstrate an ability to save before they obtain a loan is a useful screening deviceand helps to instil borrower discipline. In many cases, MFIs require loan-linkeddeposits or compulsory savings deposits as a condition to receiving a loan. Suchcompulsory savings requirements are an integral part of many if not most micro-®nance programmes. MFIs should therefore be permitted to impose compulsorysavings requirements. Most commentators argue that MFIs should be able to usecompulsory savings in their lending programmes, although it should be noted that atany point in time, not all members are net borrowers.

Some MFIs also o�er voluntary savings facilities to their members. It wouldgenerally not seem appropriate to permit MFIs to use voluntary savings in theirlending programmes unless e�ective protections are in place. One option is to permitMFIs to mobilize voluntary savings from members if they establish an earmarkedaccount for voluntary savings with a regulated ®nancial institution.

In practice, no government in the region has really come to terms with these issuesand established a clear legal framework. Generally, regulatory authorities tend not tointervene so long as MFIs mobilize savings from members only. In such cases,however, NGOs do not have a clear legal basis for accepting deposits, and there isalways the possibility of sanctions. Only one country in the region has clari®ed thesituation. In Nepal, the central bank has established `limited banking' arrangementsfor authorizing NGOs to accept deposits, and 380 NGOs have been authorized tomobilize savings from members under these arrangements. Even here, however, someambiguities remain. With regard to this criterion, we are unable to follow thepractice, followed elsewhere in this article, of awarding an `A' to the best performingcountry. Nepal is given a `B' on this criterion, whilst the other eight countries areeach rated `C'.

4 REGULATION OF BANKS

Most institutions engaged in micro®nance are specialist micro®nance institutions(MFIs) registered as societies, non-pro®t companies or similar bodies. However,there is also considerable scope for regulated banks to become involved inmicro®nance. Some specialist MFIs may wish to establish regulated banks, so thatthey can raise deposits from the general public, and more generally increasetheir credibility with investors and depositors. And some traditional banks maywish to become involved in micro®nance. However, the extent to which regulatedbanks become involved in micro®nance depends critically on the policy environ-ment.4

Criterion 10: Licensing and Minimum Capital Requirements

One critical factor a�ecting the extent to which regulated banks become involved inmicro®nance is the scope for the establishment of small banks. Micro®nanceprogrammes in large banks rarely have a secure position within the bank, although

4 These issues are discussed in detail in Baydas et al. (1997).

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

Policy and Regulation for Sustainable Micro®nance 725

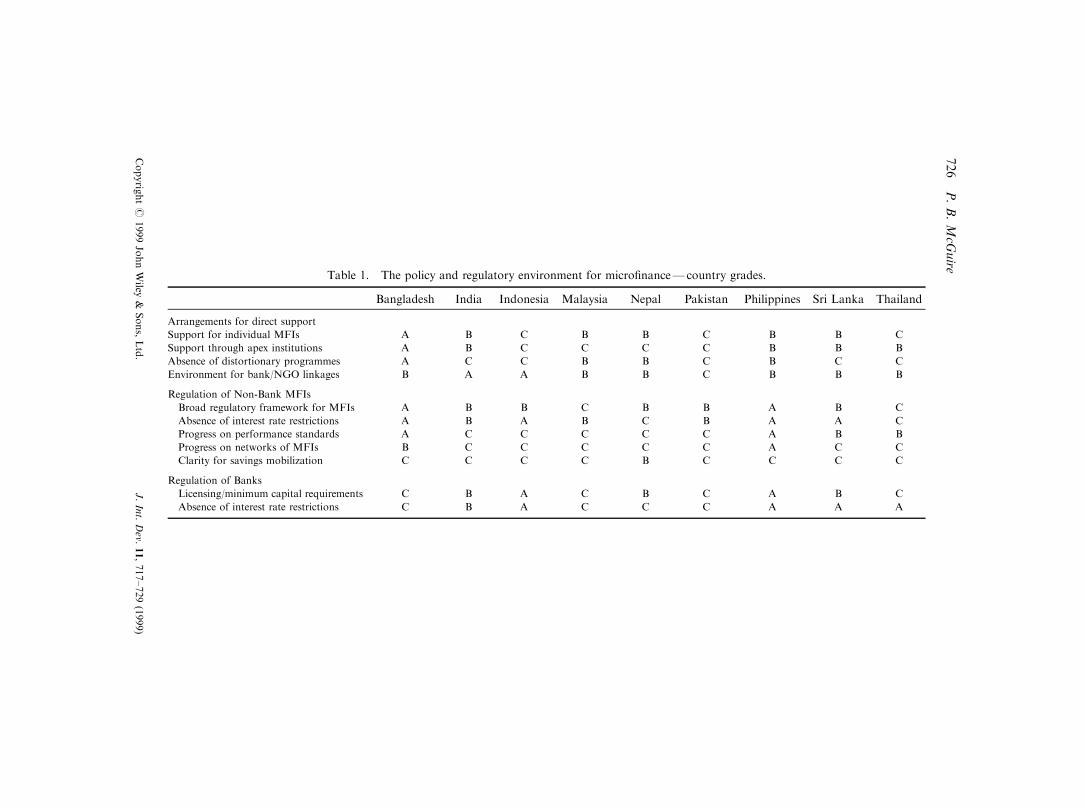

Table 1. The policy and regulatory environment for micro®nanceÐcountry grades.

Bangladesh India Indonesia Malaysia Nepal Pakistan Philippines Sri Lanka Thailand

Arrangements for direct support

Support for individual MFIs A B C B B C B B C

Support through apex institutions A B C C C C B B B

Absence of distortionary programmes A C C B B C B C C

Environment for bank/NGO linkages B A A B B C B B B

Regulation of Non-Bank MFIs

Broad regulatory framework for MFIs A B B C B B A B C

Absence of interest rate restrictions A B A B C B A A C

Progress on performance standards A C C C C C A B B

Progress on networks of MFIs B C C C C C A C C

Clarity for savings mobilization C C C C B C C C C

Regulation of Banks

Licensing/minimum capital requirements C B A C B C A B C

Absence of interest rate restrictions C B A C C C A A A

Copyrig

ht#

1999JohnWiley

&Sons,Ltd.

J.Int.Dev.

11,717±729(1999)

726

P.B.McG

uire

the unit desa system of Bank Rakyat Indonesia is a major exception to this. Smallerbanks, by contrast, operate in more localized areas and are more likely to be involvedin micro®nance. If regulated banks are to play an active role in micro®nance, it isimportant that there be some mechanism to enable small banks to be licensed. Thismeans ensuring that the minimum capital requirements for establishing a bank arerealistic for small banks operating at the local level, and that there are no otherunnecessary restrictions a�ecting the establishment of small banks.

Of the nine countries included in the study, only Indonesia and the Philippines havea permissive policy environment for the establishment of small banks. In these twocountries, there is considerable micro®nance activity by small banks operating at thelocal level, and they are each awarded an `A'.

In the other seven countries, there is much less scope to establish small banks. InIndia and Sri Lanka there is a network of regional rural development banks which areinvolved in micro®nance to some extent, but they are essentially controlled by thegovernment and in most cases their performance has been poor. In Nepal thegovernment has recently established regional rural development banks with a speci®cmicro®nance mandate, but they are subject to increasing political pressure. Thesethree countries each score a `B'. In Bangladesh, Malaysia, Pakistan and Thailandthere is no network of small regulated banks, nor are the regulations supportive oftheir establishment. These countries are each rated `C'.

Criterion 11: Absence of Interest Rate Restrictions

Interest rate ceilings on small loans by banks may prevent banks from lending directlyto the poor. Micro®nance is an inherently costly activity, and if it is to be sustainable,interest rates on microloans must be higher than on other loans. Interest rate ceilingson small loans should be removed, or at the very least set at levels that are su�cient toenable banks to operate micro®nance programmes sustainably.

Four of the countries included in the study, Bangladesh, India, Malaysia andNepal, impose interest rate ceilings on small loans by banks. All of these requirementse�ectively preclude regulated banks from lending direct to poor borrowers on asustainable basis. This is also true in Pakistan, where there is no formal ceiling butbanks generally charge small borrowers at the minimum rate because of perceivedsocial pressures to do so. India receives a `B' on this criterion because the ceilingsapply only to commercial banks, and not to regional rural banks and co-operativebanks. The other four countries listed above are each graded `C'. The remaining fourcountries, Indonesia, Philippines, Sri Lanka and Thailand, have no interest rateceilings, with banks free to determine their own interest rates in line with costs andmarket conditions. These four countries each rate an `A'.

5 CONCLUDING COMMENTS

If micro®nance is to make an important contribution to poverty reduction, themicro®nance sector will need to develop to the stage where it can reach large numbersof poor people on a sustainable basis. While there has been considerable research onhow individual MFIs can increase their outreach and sustainability, until recently

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

Policy and Regulation for Sustainable Micro®nance 727

there has been very little research on the policy and regulatory environment formicro®nance.

This article considers the policy and regulatory environment for micro®nance froma broad perspective, and with a particular focus on Asia. It grades nine countries inAsia on a total of eleven criteria for the policy and regulatory environment, focusingon the policies of governments and donor agencies to provide direct support tomicro®nance, the regulatory environment applying to non-bank MFIs which do notaccept deposits from the general public, and the regulation of banks insofar as ita�ects the scope for banks to engage in micro®nance. The grades are subjective, andthere is considerable scope for debate on both the criteria for determining whatconstitutes a `good' policy and regulatory environment, and the grades awarded toindividual countries.

Nevertheless, it is clear that there is room for improvement in the policy andregulatory environment for micro®nance in all countries. Overall, Philippines andBangladesh appear to have the most conducive policy and regulatory environ-ments for micro®nance, while Pakistan appears to have the least conducive. However,di�erent countries have strengths in di�erent areas, and no country is strong inall areas. For instance, while the policy and regulatory environment in Bangladeshhas been very conducive for specialist MFIs, it works against regulated banksengaging in micro®nance. In many countries, weaknesses in the policy and regulatoryenvironment appear to be unintended consequences of policies directed to otherobjectives.

Governments and donor agencies have provided much more support to micro-®nance in some countries than in others, and this partly explains why some countrieshave much more developed micro®nance sectors than others. Even so, some countrieshave tended to channel most of their support through the banking system or throughdirect government programmes, most of which have not been successful. Countriesthat have channelled support through specialist non-government MFIs, or in somecases through apex institutions which lend to specialist MFIs, have generally donebetter. Most countries have provided little positive support for linkages betweenregulated banks and NGOs.

The regulatory framework for non-bank MFIs is also important. In somecountries the overall political and social climate for NGOs is not conducive to theiroperating micro®nance programmes in a relatively unrestricted manner. Somecountries still maintain interest rate restrictions which make it hard for MFIs tooperate in a sustainable manner. It is also appropriate to consider how the regulatoryenvironment can contribute to high standards in the sector. In some countriesthere are interesting developments in establishing performance and reportingstandards for MFIs, whether through the policies of apex institutions or throughself-regulation. On the other hand, no country has really come to terms with thequestion of savings mobilization by MFIs and established a clear legal framework inthis area.

The regulatory framework for banks a�ects the extent to which they are involved inmicro®nance. While this has a number of elements, two stand out. First, mostcountries do not have provisions for the establishment of small banks, which are morelikely to engage in micro®nance than larger banks. Second, some countries stillmaintain interest rate ceilings on small loans by banks which preclude banks fromoperating sustainable micro®nance programmes.

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

728 P. B. McGuire

ACKNOWLEDGEMENTS

The article is based on research undertaken in 1997 as part of a study of the policy andregulatory environment for micro®nance in Asia (McGuire et al., 1998). The studywas conducted by the Foundation for Development Cooperation for the Bankingwith the Poor (BWTP) Network, a network of some 35 institutions involved inmicro®nance, including specialist MFIs, commercial banks and national policyinstitutions, from nine countries in Asia. The author would like to thank John D.Conroy and G. B. Thapa who co-authored the main study and contributed signi®-cantly to the ideas in this article, as well as the participants at the Fourth Asia-Paci®cWorkshop on Banking with the Poor held in Bangkok in November 1997 and twoanonymous referees. The usual disclaimers apply.

REFERENCES

Baydas, M. G., Douglas, H. and Valenzuela, L. (1997). Commercial Banks in Micro®nance:

New Actors in the Micro®nance World. Rural Finance Program, Ohio State University.

Berenbach, S. and Churchill, C. (1997). Regulation and Supervision of Micro®nance

InstitutionsÐExperience from Latin America, Asia and Africa. The Micro Finance Network

Occasional Paper no. 1. Washington DC: MFN.

CGAP (1996). Regulation and Supervision of Micro®nance Institutions: Stabilising a New

Financial Market. Focus Note no. 4.

Committee of Donor Agencies for Small Enterprise Development and Donors' Working

Group on Financial Sector Development (1995). Micro and Small Enterprise Finance:

Guiding Principles for Selecting and Supporting Intermediaries.

Getubig, I., Remenyi, J. and Quinones, B. (eds) (1997). Creating the Vision: Micro®nancing the

Poor in Asia-Paci®c. Kuala Lumpur: Asian and Paci®c Development Centre.

Jansson, T. and Wenner, M. D. (1997). Financial Regulation and its Signi®cance for

Micro®nance in Latin America and the Caribbean. Washington, DC: Microenterprise Unit,

Sustainable Development Department, Inter-American Development Bank.

Llanto, G. M., Garcia, E. and Callanta, R. (1996). An assessment of the capacity and ®nancial

performance of micro®nance institutions: the Philippine case. Philippine Institute for

Development Studies, Discussion Paper no. 96±12.

McGuire, P. B. (1998). `Second tier micro®nance institutions in Asia', Small Enterprise

Development, 9(2), 17±28.

McGuire, P. B., Conroy, J. D. and Thapa, G. B. (1998). Getting the Framework Right: Policy

and Regulation for Micro®nance in Asia. Brisbane: Foundation for Development

Cooperation.

Rock, R. and Otero, M. (eds) (1997). From Margin to Mainstream: The Regulation and

Supervision of Micro®nance. ACCION International (Monograph Series no. 11).

Sustainable Banking with the Poor (1996). AWorldwide Inventory of Micro®nance Institutions.

Washington, DC: World Bank.

World Bank (1996). Sta� Appraisal ReportÐBangladesh Poverty Alleviation Micro®nance

Project. Report no. 15431-BD.

Copyright # 1999 John Wiley & Sons, Ltd. J. Int. Dev. 11, 717±729 (1999)

Policy and Regulation for Sustainable Micro®nance 729