an insight into microfinance practice in indiaand filean insight into microfinance practice in india...

TRANSCRIPT

AN INSIGHT INTO MICROFINANCE PRACTICE IN INDIA A N DINDONESIA – LESSONS FOR UGANDA

David KalyangoFiona Musana (Eds.)

August 2002FSD Series No. 8

Financial Systems Development (FSD) Programme 2002

Responsible:

A. Hannig

Publisher:Bank of Uganda – German Technical Co-operationFinancial System Development (FSD) Programme

37/43 Kampala Road

P.O. Box 27650

Kampala, Uganda

Printer:

United Printers

143/5 6th Street Industrial Area

P.O.Box 1726

Kampala, Uganda

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

i

Microfinance Regulation and Supervision

Table of Contents

Table of Contents ............................................................................................................ i

Abbreviations ................................................................................................................. ii

Foreword ........................................................................................................................ 1

Background .................................................................................................................... 3Supervision of the Microfinance Industry from the Indian Perspective –An Analysis – Edward Katimbo-Mugwanya, Anthony Opio & David Kalyango,Bank of Uganda ............................................................................................................. 7The Indonesia Experience – Anthony Opio & David Kalyango,Bank of Uganda ........................................................................................................... 14Savings Issues – Guy Winship, FINCA Uganda........................................................ 20

Self Regulation Mechanisms for Unregulated MFIs – Dorothy Katantazi,MEDNET ........................................................................................................................ 22

Lending to the Rural Population, Successes and Challenges –Eva Mukasa, Uganda Women’s Finance Trust ......................................................... 24

Training in Microfinance (Capacity building): - Virginia Bara ................................. 28

Concluding Remarks - Lance Kashugyera, Medium and Small EnterprisesPolicy Unit , Ministry of Finance ................................................................................ 30Annex - Profile of Delegates ....................................................................................... 31

ii

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

AbbreviationsADB Asian Development BankBI Bank Indonesia (Central Bank of Indonesia)BIMAS Bimbingan Massal (subsidised government credit programme in Indonesia

in the 1970s and 1980s to promote the green revolution)BIS Bank for International SettlementBKD Badan Kredit Desa (village credit board)BKK Badan Kredit Kecamatan (sub-district credit board) in Central JavaBK3I Co-ordinating body for credit co-operatives at national level, IndonesiaBK3D Co-ordinating body for credit co-operatives at provincial level, IndonesiaBMT Baitul Maal Wat-Tamwil (Integrated Islamic Business Centre)BMZ Bundesministerium für Wirtschaftliche Zusammenarbeit und Entwicklung

(Federal Ministry for Economic Co-operation and Development)BoU Bank of UgandaBPD Bank Pembangunan Daerah (Regional Development Bank)BPR Bank Perkreditan Rakyat (People’s Credit Bank)BRAC Bangladesh Rural Advancement CommitteeBRI Bank Rakyat IndonesiaBU Bank Umum (Commercial bank)CERUDEB Centenary Rural Development BankCGAP Consultative Group to Assist the PoorestCI Credit InstitutionsDFI Development Finance InstitutionsDRI Differential Rate of InterestFI Financial InstitutionFSD Financial System Development Programme(Bank of Uganda – GTZ)GNP Gross National ProductGTZ Deutsche Gesellschaft für Technische Zusammenarbeit GmbH

(German Technical Co operation)IBRA Indonesian Bank Restructuring AgencyIMF International Monetary FundKosipa Koperasi Simpan Pinjam (saving and loan co-operative)KPM Kelompok Pengusaha Mikro (microentrepreneur group)KSM Kelompok Swadaya Masyarakat (self-help group)KSP Kelompok Simpan Pinjan (savings and credit group)KUD Koperasi Unit Desa (village unit co-operative)LDKP Lembaga Dana Kredit Pedesaan (rural fund and credit institution)LPD Lembaga Perkreditan Desa (village credit institution) in BaliMCC Microfinance Competence CentreMDI Micro Deposit-taking InstitutionMFI Microfinance InstitutionMIS Management Information Systemn.a. Not availableNABARD National Bank for Agriculture and Rural DevelopmentNBFC Non-Bank Financial CompaniesNGO Non Governmental OrganisationNPA Non-Performing AssetsNPL Non-Performing LoansNSE New Supervisory EntityPAKTO Paket Oktober 1988 (banking deregulation package)PHBK Pengembangan Hubungan Bank dengan KSM (Linking Banks and Self-Help Groups)PLPDK Pusat Lembaga Perkreditan Desa Kecamatan (LPD Centre)ProFI Pilot Project “Promotion of Small Financial Institutions” (GTZ/BI)PSDP Private Sector Development ProgrammeRBI Reserve Bank of India

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

iii

Microfinance Regulation and Supervision

ROA Return on AssetsROE Return on EquityROSCA Rotating Saving and Credit AssociationsRp (Indonesian) RupiahRRB Regional Rural BankRs (Indian) RupeesSACCO Savings and Credit Co-operativesSGSY Swarnajayanti Gram Swarozgar Yojana (Rural self-employment scheme

of the Ministry of Rural Development, India)SHG Self-Help GroupSHPI Self-Help Promoting InstitutionsSME Small and Medium EnterprisesSRO Self-Regulatory OrganisationsSSI Small-Scale IndustriesUSH Uganda ShillingUSP Usaha Simpan Pinjam (savings and loan business)UWFT Uganda Women’s Finance TrustYIS Yayasan Indonesia Sejahtera (one of the leading Indonesian NGOs)

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

1

Microfinance Regulation and Supervision

Foreword

Uganda, like many other countries, is going through a process of redefining the practical, supervisory andregulatory requirements of the microfinance industry. In order to contribute to a better understanding of thecomplexities of microfinance business and provide input into the effective implementation of the MicroDeposit-taking Institutions (MDI) 2002 Bill, Financial System Development Project1 organised a two-weekmission for a section of Ugandan microfinance practitioners, central bank supervisors, trainers and policy-makers to India and Indonesia. Similar to Uganda, the two countries are undergoing a process of strengtheningtheir microfinance practice, supervision and regulation. This visit which took place between July 9 – 23rd,2001, enabled the Ugandan mission to go a step further in defining the supervisory and regulatory framework.

Specifically, the Ugandan delegates were able to:

• Gain an insight into the supervision and regulatory support from the Reserve Bank of India and BankIndonesia;

• Confirm lessons from the existing regulatory framework for Microfinance institutions;

• Understand the methodology, challenges, successes and opportunities in lending to the rural population;

• Draw lessons on self-regulation by the operators and the extent of responsibility and authority delegatedby supervising body to self-regulating bodies;

• Gain an understanding of savings mobilisation practices that can be cost-effective and savings productsthat suits the lower income people. Specifically, focus on the rollout and different structures of thesavings products and risk management in savings mobilisation.

• Study policy issues affecting microfinance in India and Indonesia;

• Analyse the process of transition and key organisational changes in the process of transformation.

FSD Series No. 8 highlights the outcome of this mission and draws lessons for the microfinance industry inUganda. Basically, this experience confirmed the assertion that the diversities in approach make microfinancean interesting business. It might not be easy to come up with any generalisations between the countries andeven among institutions. The challenge of sustainability in the face of competition is moving the microfinanceindustry world-wide into innovative approaches, products and services that emphasise the need to be clientresponsive. The visit reaffirmed the commitment both countries have shown in exploring alternative mecha-nisms for improving access of the poor to financial services in a cost effective and sustainable manner2.

The publication is based on visits and discussions with Reserve Bank of India (RBI) and the National Bankfor Agriculture and Rural Development (NABARD) in Mumbai, with a number of practitioners in Mumbai andin Andhra Pradesh (including a number of rural banks such as Manjira Grameena Bank and two NGOs,namely BASIX and SHARE), and some MFI associations (such as the Network of India Credit and SavingsProgrammes or INDNET, Sa-Dhan/The Association of Community Development Finance Institutions, andthe South Asian Network for Microfinance Initiatives).

Discussions took place with a number of relevant institutions in Indonesia. The main contributions were fromBank Indonesia (the central bank), Bina Swadaya (a micro-finance NGO), and Bank Rayat Indonesia (BRI)in Java. Discussions with a private micro-finance bank (Bank Dagang Bali), a regional development bank(Bank Pembangunan Daerah) in Denpasar, and representatives from both peoples credit banks (BankPerkreditan Rakyat and others) and a rural financial institution (Lembaga Dana Kredit Pedesaan/LDKP) inrural Bali were also useful. Contributions from the GTZ financial services technical support projects in bothIndia and Indonesia (Financial Sector Support Project in India and ProFi project in Indonesia) were also veryuseful.

1 In June 2002, FSD expanded into a programme, following recommendations from the Ugandan partners and the mid-term reviewmission in September-October 2001.2 Both countries presented their cases at a high-level policy dialogue seminar organised by the Financial System DevelopmentProject in November 1999,

2

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

On behalf of the Uganda Delegation, we would like to extend our heartfelt gratitude to the India and Indonesiahosts for their gracious and heart-warming welcome and hospitality. For us, it was a positive indication ofdedication not only to the empowerment of their countries but also to enhancing the blossoming South-SouthDialogue.

Dr. Alfred Hannig Edward Katimbo-MugwanyaProgramme Director FSD Executive Director Supervision, Bank of Uganda

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

3

Microfinance Regulation and Supervision

1 Background

1.1 Introduction to IndiaIndia is the world’s second most populous country with nearly one billion people, many of whom live at orbelow the poverty line. The nature and type of financial services needed within low-income communities arenot dissimilar to that found in sub-Saharan Africa, and that the current financial institutions were not able (orwilling) to provide such services also has parallels.

Notwithstanding these similarities, a number of environmental differences should not be overlooked, notleast the high population density and numbers, the high degree of bank regulation and supervision, and therequirement for all regulated financial institutions to follow a directive lending policy, mean that the opportunitiesand challenges facing the sector are somewhat different to that found in East Africa.

1.1.1 The Banking Sector in India3

The rural financial sector in India is composed of over 139,000 retail outlets of formal banking systemsummarised below:

Table 1: Formal Financial Institutions in Rural India

1 An overview and introduction to the banking sector in India can easily be obtained by those with internet access (seefor example www.indianetgbr.org, http://finance.indiamart.com/investment_in_india/banks.html; http://www.nabard.org;Information on the Reserve Bank of India (RBI) - the central bank responsible both for monetary policy and regulationand supervision of the industry in India - as well as the structure and challenges facing the industry can be found fromthese sources.

Type of institution Number Rural/semi-urban Branches

Commercial banks 106 32,854 Regional rural banks 196 14,142 State co-operative banks 28 789 District co-operative banks

367 12,128

Primary co-operative credit societies

92,000

State land development banks

19 1,154

Primary land development banks

745 686

TOTAL 1,461 153,753

The momentum for provisions of rural finance started way back in 1969 through the nationalisation of majorcommercial banks and setting minimum standards to control sectoral lending as follows:

- Minimum priority sector lending (40%)

- Minimum agricultural lending (18%)

- Minimum weaker sector lending (10%)

- Regulated interest rates on deposits and loans, generally rural loans were cheaper

- Special poor-targeted programmes

While in 1975 Regional Rural Banks were established, Government involvement in directing credit remainsa key instrument in providing rural finance through commercial banks, regional rural banks and co-operatives.

1.2 Introduction to Indonesia:-Indonesia is the worlds largest archipelago with 17,000 islands (about 6,000 of which are inhabited), apopulation of around 220 million (making it the fourth most populous nation after China, India, and the USA)at a high density of 109 persons per square km.

Population (per retail outlet): 4,700 as of March 1999

4

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

1.2.1 The Economy

Formerly a totally agricultural society, Indonesia has now become a commodity producer and is adding asignificant high-growth manufacturing community. While the government continues to control prices, operatestate-owned firms, and impose comprehensive restrictions, Indonesia is largely a free-market economywith a strong private sector. There are barriers to continued economic development, however, including lackof investment capital, an inadequate and slowly developing infrastructure, rising foreign debt and inflation,an undereducated workforce, human rights problems, and rampant and endemic corruption.

From a positive perspective, the Indonesian economy stabilised again in 1999. This follows the Bankingcrisis two years earlier. Micro-finance is well entrenched in Indonesia, with over 21,000 registered providersof micro-finance (regulated, non-regulated, NGO and co-operatives). The economic and banking crisis thataffected much of south-east Asia in 1997-98 was most strongly felt in Indonesia, where the real GDP fell by14.2% for the year ending 31 March 1999 (ADB figures).

Many financial institutions, including almost all the commercial banks and many of the MFI’s and non-bankfinancial institutions have been affected by this crisis and remain vulnerable. Increased attempts to tackle awide range of structural issues over the past few years have gained some momentum following the crisis,but much work still needs to be done with regards to regulatory and policy issues governing the financial andbanking sector in the country. Progress in this regard has been limited by a volatile and fragile politicalenvironment, including relatively (excuse the pun!) high levels of nepotism and corruption. The demand formicro-finance services remains high, and as with India and Africa, demand strongly exceeds supply. Whilethe structural, and hence the policy, regulatory and supervisory issues may differ from India and sub-SaharanAfrica, the operational issues facing the institutions – especially with regard to risk and liquidity management,and to savings mobilisation and compliance issues - appear to be fairly similar.

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

5

Microfinance Regulation and Supervision

Table 2: Overview of the Supply-Side of Indonesia’s Financial System

Figures per June 1999. Figures marked with * are estimates

Formal Sector: Central Bank: Bank Indonesia Banks:

• 170 commercial banks (Bank Umum/BU) with 5,997 bank offices and 3,703 BRI Unit Desa

• 2,420 Peoples’ Credit Banks (Bank Perkreditan Rakyat, BPR)

• 5,345 Badan Kredit Desa (BKD)

Non-bank financial institutions:

• 2,272 Rural Fund and Credit Institutions (Lembaga Dana dan Kredit Desa, LDKP)

• 633 state pawn shops (pegadaian)

• Finance companies

• Insurance companies Co-operatives:

• 5,335 Village Unit Co-operatives with Saving and Credit (Koperasi Unit Desa dengan USP/KUD/USP)

• One Credit Union (Badan Kordinasi Koperasi Kredit (BK3I/BK3D)

• 1,160 savings and credit co-operatives (Koperasi Simpan Pinjam, Kosipa)

Contractual savings institutions:

• Insurance companies

• Pension funds

Markets:

• Jakarta stock exchange

• Surabaya stock exchange

Semiformal sector: 400* NGO microcredit programmes Numerous development projects by government agencies and international donors

Informal sector: 250,000* Rotating savings and credit associations (ROSCA) and variants (Arisan)

Self-help groups:

• 6,000 savings and credit groups (Kelompok Simpan Pinjam/KSP)

• 15,000 microentrepreneur groups (Kelompok Pengusaha Mikro/KPM)

• 30,000 KPK (P4K)

• 2,908 BMT

Individual moneylenders (commercial and non-commercial) Traders and shopkeepers

6

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

1.3 Examples of some of the Institutions1.3.1 Bank Dagang Bali (BDB)

This is a privately owned commercial bank with its headquarters in Denpasar, Bali. It was founded by thefamily of Mr. & Mrs. Oka in 1970 and is licensed as a savings and lending institution. It is the first such bankin Bali.

According to its annual report of Year 2000 BDB has 8 branches, 18 sub branches, 4 cash service offices inaddition to its headquarters office at Denpasar. This is a total 31 banking facilities operation with 630 staff.Total assets of BDB were approx. Rp 1,374 billion. The total savings deposits of approximately Rp1, 110billion was held by 423,687 savers. Total loan outstanding were Rp 513 billion under 10,417 loan accounts,70% of the total loans are to micro and small businesses.

The lottery system as an incentive to savers was started by Oka and copied by others. Only passbooksavings are included in the lottery draws.

Savings investments and services for lower income people are highly developed at BDB. BDB holds alottery drawing 4 times a year for all holders of passbook savings and checking accounts. Each monthevery saver receives free of charge one lottery number per month for each RP 10000 as minimum balance.Savings are collected from door to door at work places and homes and offices by mobile savings teams.Many customers make daily deposits, many several times a week, others save weekly, bi-weekly or monthly.

1.3.2 Bina Swadaya

This is an NGO (Foundation) based in Jakarta which, as a facilitator, promotes SHGs for linkage with therural banks for credit. Bina Swadaya has structured itself to become a self-financing NGO by creating 2types of institutions:

• Rural banks (4) so far, - to do micro financing activities.

• Co-operatives covering the whole country – only savings activities.

• The foundation’s main activities are:-

• Microfinance development through promotion of SHGs

• Micro-enterprise development (capacity building through groups)

• Training and education

• Community based development consultancy.

The rural banks, Agro-business, Magazine & book publication, printing house, and “alternative tourism”ventures then support these main activities. Through these supporting activities, the foundation self-financesits budget up to 90% (proposed budget for 2001: US$6.9m-)

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

7

Microfinance Regulation and Supervision

2 Supervision of the Microfinance Industry from the Indian Perspective – AnAnalysis – Edward Katimbo-Mugwanya, Anthony Opio & David Kalyango, Bankof Uganda

2.1 IntroductionExperience in microfinance worldwide has shown that the provision of financial services to the economicallyactive poor is an area that requires regulatory support. The success lies in creating a balance betweenensuring the safety of deposits by the poor while encouraging development of microfinance at the nationallevel.

In India, the regulatory and supervisory authority of financial institutions is the Reserve Bank of India (RBI).However due to the large size of the financial sector and the diversity of the financial institutions, a specificlegislation governing the business of Microfinance is not yet in place. The proposed Financial CompaniesRegulation Bill 2000 is under consideration by the Government of India (GOI). The main focus of the bill isto consolidate and amend the law for regulation of financial institutions, to protect the interest of the depositorsof the financial companies and to prohibit receipt of deposits by unincorporated bodies.

Institutions involved in microfinance business include Banks, Non-Bank Financial Companies, Self-HelpGroups, Co-operatives and NGOs.

2.1.1 Background

The National Bank for Agriculture and Rural Development (NABARD) was established through an act ofParliament in 1982, to promote rural development. It has a total capitalisation of rupees 5 billion and totalassets amounting to US $8.2billion (as at 3lst March 2001). The mission of NABARD is to “Promotesustainable and Equitable Agriculture and Rural Prosperity through effective credit support, related services,Institutional development and other innovative initiatives”. It has 28 regional offices, One sub office, 304District offices, 4 training establishments and total staff strength of 5400 out of which 2800 are professionals.

2.1.2 Role and Functions of NABARD

• Refinancing Banks

• Provision of Loans to State Governments

• Takes risk in Lending

• Supporting formulation of policies related to rural credit

• Monitoring and evaluation of projects and programmes

• Institutional building and strengthening

• Training and Capacity Building

• Experimentation with new models and practices

• Dissemination of Innovative products and ideas

• Supporting Research and Development

2.1.3 Supervisory role

• Inspection of Co-operative Banks and Regional Rural Banks

• Supplementary Interventions

• Issuance of Reports and Monitoring Compliance

• Offsite Surveillance

2.1.4 Research in Financing Rural Development

Studies were carried out in the mid 80’s and established that:

• Savings and credit products at the time did not suit the needs of the poor

8

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

• Procedures were complicated and cumbersome

• High transaction costs for the poor

• System did not provide for anything to fall back on

• Some of the special programmes did not recognise savings

• Resources handled were often larger than the capacity of the poor

• Others made all the decisions

Conclusions reached were that the poor need hassle-free facility with:

• A mechanism to keep safe thrift and tiny surpluses

• Credit to meet emergencies

• Credit for micro enterprises

2.1.5 What was to be done?

• Design appropriate savings and credit products and system

• Improve the access of the poor to financial services which?

• Reduce transaction costs to the poor

• Reduce transaction costs of the financing agencies

• Enhance participation by poor in decision making

• Build up handling capacities of the agencies who can provide these services

• Identify new partners

• Work out roles for different partners

• Integrate formal banking system to ensure sustainability

• Dominant strategy: Self-Help Groups – Bank linkage.

2.2 The Linkage Programme

2.2.1 What does the linkage method achieve?

• Increases outreach to poor

• Cost effective for both banks and the poor

• Reduces dependence on informal finance

• Doorstep hassle-free, self managed financial services

• Reasonable market based interest rates

• Access of formal banks to savings and credit to the poor

• Graduation from consumption to production loans

• Graduation to higher income level with non subsidy

• Initiates the process of empowerment

2.2.2 Evolution of SHG – Bank linkage Programme

NABARD’s involvement in promoting Micro-finance through the concept of SHGs started in 1987. A pilotproject in 1999 linked 500 SHG’s with banks. In February 1992 the project was made operational throughoutthe country using a set of well defined guidelines with special reference to the objective criteria for selectionof SHGs, size of the group, assessment of credit, rate of interest, repayment period, security etc.

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

9

Microfinance Regulation and Supervision

The basic philosophy of the SHG – Bank linkage model promoted by NABARD is to establish synergybetween the banks, which have the financial strength and the NGOs, which have the ability to mobilise thepoor and build up their capacity to avail loans from the banks.

SHGs are formed on voluntary basis, perceived as people institutions providing the poor with the space andsupport necessary to take effective steps toward greater control of their private lives and in society.Notwithstanding the similarity in principles and functions, These groups are distinct from co-operative societies.SHGs are characterised by small size usually limited to less than 20 members per group. Homogeneity interms of socio-economic conditions and levels of living standard form the basis for the group formation.

Public meetings held on a weekly or fortnightly basis, inculcating the habit of saving through, creatingcommon fund by contributing regular savings from members, on lending to its members, availing creditsupport from financial institutions with collateral substitutes etc. are some of the binding factors in the groupfunctioning.

The process of group formation takes six months to one year and the management of these groups isvested in representatives selected from amongst the group members.

2.2.3 Progress of the Programme

NABARD provides 100% refinancing facilities to banks at a concessional rate of interest of 6.5 per cent perannum. The bank also facilitates training of bank officials and field staff of NGOs, providing selective capacitybuilding support to NGOs, SHGs and their federations and other related institutions by way of financialassistance and other support.

The policy support for the efforts of NABARD was provided by the Reserve Bank of India (RBI) which urgedbanks to consider mainstream financing of SHGs as a business activity. Banks have been given freedom toprescribe their own lending norms keeping in mind the realities. Thus they devise appropriate loans andsavings products. Priority would be accorded to this sector in preparation of credit plans by banks. Bankshave also been advised that Micro credit should form an integral of their corporate plan and should bereviewed at the highest level every quarter. A revised reporting system for monitoring microcreditdisbursements on a half-yearly basis has been put in place. In view of its potential in alleviation of poverty,banks have to make all out efforts at provision of Micro-credit.

The importance and relevance of the SHG bank linkage programme in India is recognised not only locallybut also by the Government of India (GOI). The government has also accepted rural development, as anovel approach for reaching and empowering the un-reached and under served poor. The GOI have sincedeclared the programme as a national priority. The SHG – Bank linkage programme was further extendedto Regional Rural Banks (RRBs) and Co-operative Banks in 1993 and is now permitted by the ReservedBank of India as a component of priority sector lending.

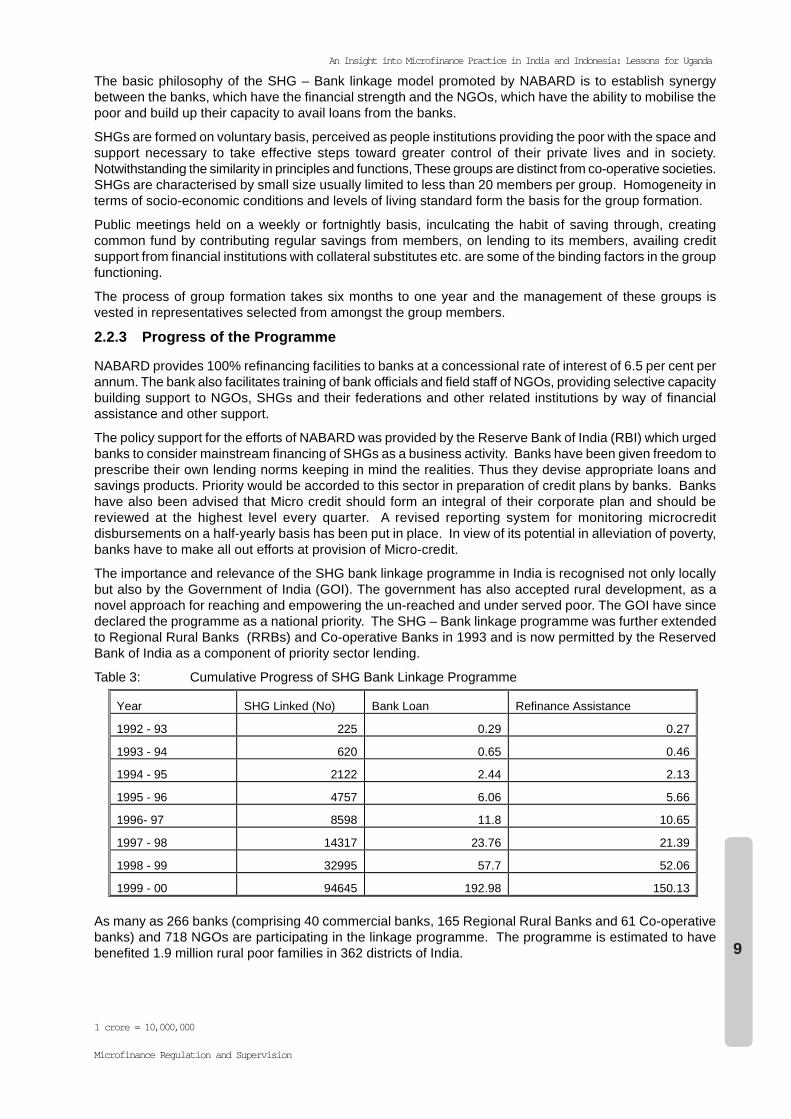

Table 3: Cumulative Progress of SHG Bank Linkage Programme

Year SHG Linked (No) Bank Loan Refinance Assistance

1992 - 93 225 0.29 0.27

1993 - 94 620 0.65 0.46

1994 - 95 2122 2.44 2.13

1995 - 96 4757 6.06 5.66

1996- 97 8598 11.8 10.65

1997 - 98 14317 23.76 21.39

1998 - 99 32995 57.7 52.06

1999 - 00 94645 192.98 150.13

1 crore = 10,000,000

As many as 266 banks (comprising 40 commercial banks, 165 Regional Rural Banks and 61 Co-operativebanks) and 718 NGOs are participating in the linkage programme. The programme is estimated to havebenefited 1.9 million rural poor families in 362 districts of India.

10

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

2.2.4 Participation of Banks

Among the Commercial Banks, State Bank of India leads with Credit-Linkage of the maximum number ofSHGs followed by Andhra Bank and State Bank of Hyderbad. Other banks having a significant share areCanara Bank, Indian Bank, Bank of Baroda, India Overseas Bank, Syndicate Bank, Bank of India and UnionBank India.

2.2.5 Impact of Microfinance on SHG members

• Better access to credit follows group formation

• Saving habit inculcated among members as part of lending is from members own savings

• Improvement in asset holding

• Impact on poverty alleviation

• Employment generation

The most important contribution to the success of the SHG is the homogeneity of the group. Homogeneityin terms of living together in the same village or having uniform standards of living and socio-economicconditions were the major factors influencing the cohesiveness of the groups. Homogeneity in the standardof living constitutes a major factor followed up by proximity of residences.

Regular meetings at fixed intervals in a common place is one of the core activities of the SHG during whichthey undertake financial transactions, both in terms of collections of savings and also disbursement ofloans.

In addition, this occasion is being used to discuss their common problems and other issues that need to besorted out through the intervention of the group or its members. The level of attendance and the frequencyof the meeting may judge the performance of the groups. Monthly meetings are a common phenomenafollowed by weekly meetings.

Savings form one of the main products in the SHG – Bank linkage programme. The members contributeperiodically e.g. at weekly intervals, a pre-determined amount as savings.

2.3 Framework for Microfinance in IndiaIn the mid 1990’s a Task force was constituted by NABARD under the chairmanship of Mr. Y. C. Nanda,Managing Director, NABARD and senior executives of banks and Non-bank financial institutions. The termsof reference of the Task force were to: -

• Work out a conceptual framework for a National Policy for Microfinance.

• Examine and suggest organisational and regulatory framework for bringing the operations of Microfinanceinstitutions to the mainstream having regard to the need of multiplicity of approaches and structures.

• Suggest a framework for inter-institutional co-ordination and the roles and responsibilities of self-regulatingorganisations.

• Examine and suggest for a need or otherwise of an independent legislation for microfinance.

• Assess the need for and suggest ways and means of an appropriate support mechanism for mergingmicrofinance institutions including financial resources.

The recommendations of the Task Force were as follows:

• Mainstreaming of MFIs and other MF structures through SHG – Bank linkage programme.

• As more and more MFIs enter the scenario, their need for loanable funds would increase and it wouldbecome difficult for MFIs and donors to continue meeting these needs.

• Banks shall develop and select appropriate loan products to suit the needs of both MFIs and theirborrowers.

Therefore, financing MFI’s by Commercial Banks for further credit retailing of Microcredit was imperative.The Reserve Bank of India, therefore, issued issuing guidelines to all banks to treat lending to MFI’s forfurther on lending as part of their regular credit operations under priority sector.

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

11

Microfinance Regulation and Supervision

2.4 Regulation of Microfinance Institutions in IndiaPresently only MFIs registered as Co-operatives and Non Bank Finance Companies are regulated. Theneed for regulation and supervision of NGO – MFIs arises from several considerations e.g. protecting theinterest of the small savers, ensuring proper terms of credit and financial discipline, institution of a properreporting system and also for their orderly development.

The task force recognised the mechanism of self-regulation of NGO-MFIs and need for encouraging promotionof Self-Regulatory Organisations (SRO). The Task force recommended that the major functions of SRO’swould be:

• Overseeing functioning of MFI as base level regulators

• Undertake registration of MFI

• Evolve proper systems for maintenance of accounts and reporting

• Setting performance standards

• Conducting inspections

• Undertaking training of MFI

• Representing MFIs in various fora

As the evolution of SRO may take sometime, it was recommended that GOI and RBI should start theprocess of regulating and supervision MFI’s immediately.

2.4.1 Why should MFIs be regulated?

• Microfinance by MFIs is already recognised as a legitimate financial activity by RBI

• This includes providing Savings services to clients by MFIs

• Savings of MFI poor are not protected

• Insurance is not available to protect-savings

When savings are used for on lending, or MFIs provide only loan service:

• Suitable lending norms are not in place

• No supervision of activities of MFIs

• No prudential norms

2.4.2 Steps taken by RBI/NABARD

MFI-Bank RBI has issued instructions to banks to finance MFI’s .NABARD has Issued Instructions to banks for refinance

MFI-NBFC’ RBI has exempted under section 25 of the Company’s Act, Institutions engaged in Microfinance and not taking public deposits from RBI registration and Regulation norms

2.4.3 Outreach by 2001

• 263,000 SHGs financed by banks comprising of 4.5 million poor households and 22.5 million poorpeople

• 90% SHGs are women groups

• Average size of loans $23. (US$ 46 Rupees)

• Member ontime repayment rate reach 100%

• 8,000 bank branches of over 314 banks involved

• One thousand thirty (1030) NGO’s involved

• Bank loan US $102M

• Refinance US $85m

12

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

2.4.4 Vision 2008

Microfinance outreach to extend to 20 million households or 100 million rural poor through 1 million SHGs.

Estimated demand for Microcredit – US$10.6 billion per year

2.4.5 What makes the SHG approach succeed?

At Group level

• Emphasis on Group formation and nurturing

• Group composition – affinity and homogeneity

• Members’ own stake in the group in the form of savings

• Members learn to maintain financial discipline

• Collective wisdom in credit decisions

• Peer support – minimise the risk of failures

• Savings and Credit is a continuing process

• Freedom of selecting loan purpose, with benefit of peer counseling.

At Bank Level

Emphasis on grading

• NGOs grade the SHGs before the linkage exercise begins

• Banks grade the SHGs for credit support

• Those with weakness have to improve their systems

• Cost effective, operationally simple and low risk strategy for expanding client base and business

• Externalizing some of the credit functions to SHG.

• Bank loans only after initial savings and internal lending

• Banking with disciplined clients and not beneficiaries

• More than 95% ontime payment.

2.5 Lessons learnt from IndiaThe National Bank for Agricultural and Rural Development is well capitalised. From the audited accountsfor the period ending 31st March 2000 NABARD made profits amounting to about US$30 million. Over 2500professional staff, including are working in the different branches of NABARD. As an institution NABARD isdedicated towards achieving its mission is to “promote sustainable and equitable agriculture and ruralprosperity through effective credit support, related services, institutional development and other innovativeinitiatives”.

The bank has been instrumental in facilitating the Self-Help Groups in its linkage-banking programme. Thisprogramme primarily aims to integrate informal savings and credit groups with mainstream banking systemby providing credit facility for enhancing their fund base. In the course of operation of SHGs best practiceshave been developed based on the following:

• Participation - groups of less than 20 are found to be effective

• Economic status - Members are mainly from poor families

• Office bearers – Management responsibilities are shared by members

• Meetings – Frequency of once a week has been found to be adequate

• Attendance – Average attendance may be over 90%

• Sanctions – Groups that impose sanctions effectively and regularly are strong

• Rules – Each group has its own rules of conduct, fund management and the like

• Common Fund – Includes savings , interest from loans, fines, penalties

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

13

Microfinance Regulation and Supervision

• Savings – Collective decision on quantum, timing

• Loans – Need based and short term with rigorous appraisal and investment plans

• Pattern of loans – small loans initially for consumption and investment, production etc.

• Interest on loans – Groups free to fix interest rate – ( market rate in the area)

• Records – procedures of meetings, overdue and other important issues are kept

• Ontime repayment – Ensure ontime payment

NABARD provides 100% refinance to Commercial Banks, Regional Rural Banks, Co-operative Banks andPrimary Agriculture Credit Societies to support loans disbursed to Self-Help Groups.

The Reserve Bank of India guidelines to banks for mainstreaming microcredit has improved the creditdelivery system through:

• Liberalising interest rates applicable to loans given by banks to MFIs, Self Help Groups/member basedinstitution beneficiaries

• Banks formulate their own models or choose any intermediary for extending microcredit

Microcredit is now seen as a priority sector and the criteria for selection of Microcredit organisations hasbeen left to the institutions financing them. Basic aspects like proper credentials, track record, systems ofmaintaining accounts and records in the regular audits in place and manpower for close supervision andfollow up

MFIs registered as ‘not for profit have been exempted from registration and prudential requirement.

2.6 Way Forward

Is the linkage banking lesson appropriate for Uganda? Having drafted the MDI Bill there is need to encourageand provide safeguards for linkage banking. Essentiality linkage banking increases the level of fundingto SHGs or MFI’s and increase capacity for the marginalised sector to access credit.

From the above it can be seen that there is a well-established institution (NABARD) behind the success ofSelf Help Groups. In Uganda, the Self-Help Groups are either in the form of Village financial institutions orNGOs, Co-operatives, Rotating Savings and Credit Associations (ROSCA’s). Funding is primarily from ownmember savings or from donations from external or internal sources. In India, resources are available fromGovernment of India through national budget allocation, Banks, and NABARD. The Government of Indiaprovides a rural infrastructure Development Fund through the Union budget. In the budget, funding is madeavailable to state governments and implemented at the village level by NGOs, SHGs and the like

Although India is making steps towards regulation, it still has to define its direction. There are a few lessons;NABARD could draw from the Ugandan experience. Uganda has gone through a consultative process withall the stakeholders, including microfinance practitioners, supervisors and regulators. There has also beeninput from the donor sides who have encouraged debate drawing experience from the international microfinancearena.

14

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

3 The Indonesia Experience – Anthony Opio & David Kalyango, Bank of Uganda

3.1 The legal framework for Microfinance in IndonesiaAs per Government Regulation 71 of 1992 Lembaga Dana Kredit Pedesaan (LDKP) including BKDs (BadanKredit Desa) and other similar institutions, which have obtained business licenses from the Minister ofFinance, are declared to be BPR (Bank Perkreditan Rakyat). If they had not converted to BPR they mustapply for a BPR licence (Rural Micro banks) i.e. convert within 5 years after the date of regulation (30th

October 1992). Hence all these MFIs should have converted to BPRs by 30th October 1997. It was notspelt out in the regulation what happens to MFIs that do not possess a BPR licence. To obtain a licence, theentities can chose one of the following legal forms; regional enterprise, co-operative or a limited liabilityCompany. The requirement for MFIs to convert to BPR (i.e. to assume the Microbank status) was largelyignored except in central Java where 35% of BKKs (Badan Kredit Kecamatan) converted to BPR. Less than10% of MFIs complied with the Act requiring them to convert to BPR by October 1997.

3.1.1 Reasons for the low conversion rate:

Where the village is the owner for example an. LPD, converting into a legal entity and BPR is complex. It isdifficult for villages to understand and comply with the legal requirements, relating to promotion and manage-ment of companies and co-operatives.

Once MFIs are incorporated (converted to BPR) they have to pay tax on profits and withholding tax must bededucted from interest paid to depositors.

Many non-bank MFIs such as LPD in Bali are reluctant to convert to BPR because of perceived BPR industryproblems. Some MFI are concerned about government interference if they transformed into co-operatives.

Lack of enforcement by the authorities for MFIs to convert, probably because non-bank MFIs are either nottaking deposits from the public or the level of deposit mobilization from the public is minimal

In view of the above, it was imperative that their operations be legitimised and they are subject to animproved regulatory and supervisory regime.

Therefore amendments have been made to the Banking Act and supervision of these institutions would beconducted by an independent supervisory entity within the financial services sector, which shall be establishedby an act. The New Supervisory Entity (NSE) was to be established not later than 31 December 2002. Untilsuch a supervisory entity has been established the tasks of supervision and regulations of banks shall beconducted by Bank Indonesia (BI). From January 2003:

• BI will be responsible for regulation

• NSE will be responsible for supervision. More recent developments indicate that the NSE may also beresponsible for regulation of non-banks

The NSE may therefore be responsible for all banks and non-bank financial institutions and any financialinstitution that accept or receive government funds (including LDKP and BKD). It is therefore likely thatNSE will also have primary responsibility for the regulation and supervision of non-bank, non co-operativeMFIs. Therefore until 31st December 2002 as an interim arrangement, supervision/regulation of MFs underthe new MFI Act will be the responsibility of the MOF acting on the advice of BI. However, the Ministry of Co-operatives neither has adequate resources nor a legal framework to supervise co-operatives properly.

Presently over 6000 non-bank, non-co-operative MFIs are not complying with the relevant laws. Additionally,the present legal framework is regarded as inappropriate. Not only is it being largely ignored by MFIs andnot enforced by the authorities, it is also constraining the development of MFIs.

New MFIs do not want to become BPR and in any case could not meet the Capital requirement of Rp 500mif a BPR is operating in a rural area. BPR capital requirement used to be RS 50million. It therefore appearsthat an alternative and facilitating framework for non-bank non-co-operative MFIs should be developed andthis is the purpose of the new MFI Act.

3.1.2 New Legal Framework

BPRs are under the Banking Act

Co-operatives are under Co-operatives Act

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

15

Microfinance Regulation and Supervision

The new act for Non Bank MFIs covers– The definition of Non Bank MFIs

– Provide the Legal Status of current MFIs

– Requirements for new MFIs

– Prudential Regulations

– Others

3.1.3 Proposal for Non Bank MFIs Regulation

• MFIs are institutions similar to LDKP and BKD

• The Operational range is limited under one district

• Limit the public fund that could be collected

• The regulation and supervision is decentralised to regional government or Regional Development Banks(BPD).

• Regulation for new MFIs

• Management separate from owners

• Prudential Regulation (Asset Quality etc.)

• Services, loans, savings and time deposits

• Operational license from regional governments

• Supervision by competent institution

• Owners are village, government or non-profit institution.

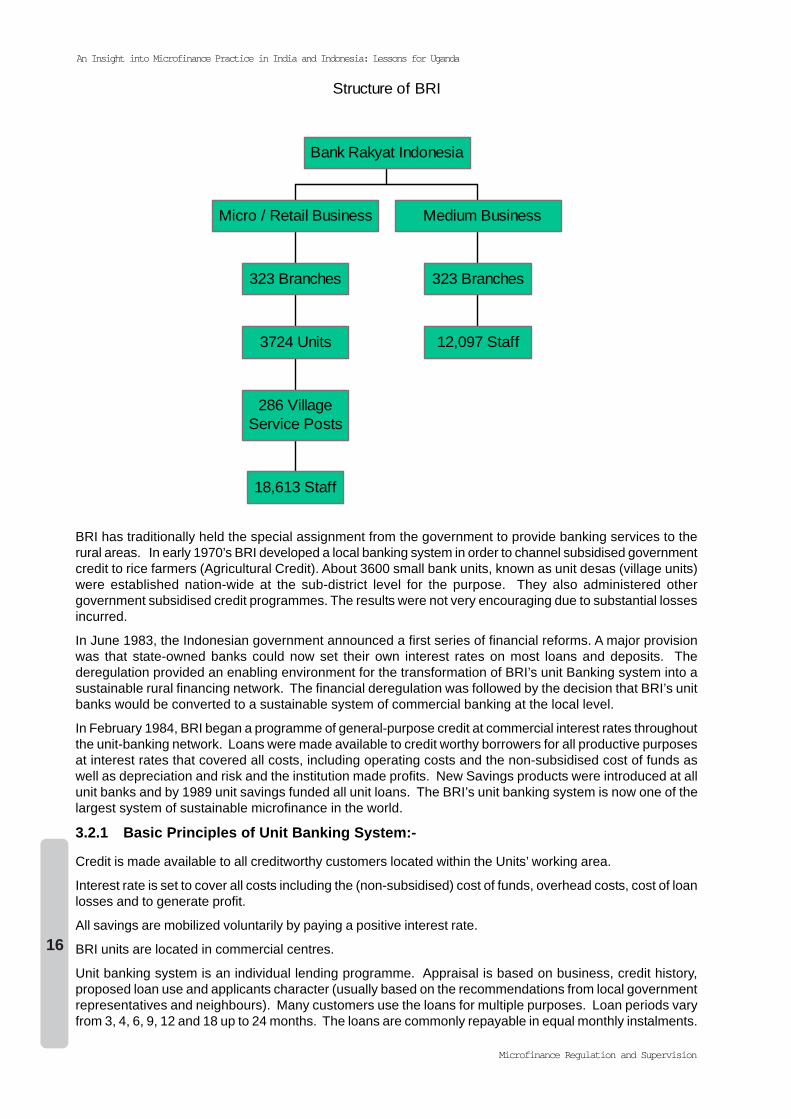

3.2 Bank Rakyat Indonesia, the Unit Banking system; successes and challengesBank Rakyat Indonesia (BRI) is a state owned commercial bank established in 1895. Its traditional missionwas to provide banking services to the rural areas of Indonesia with special emphasis on agricultural credit.At the end of 2000, BRI had more than Rp.77.3 trillion or US $8 billion in assets making it one of the largestbanks in Indonesia in terms of total assets. BRI offices extend throughout Indonesia in locations from largecities to rural areas. With 12 regional offices, 323 branches and staff at 30710, it has the most extensivenetwork in the country.

16

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

BRI has traditionally held the special assignment from the government to provide banking services to therural areas. In early 1970’s BRI developed a local banking system in order to channel subsidised governmentcredit to rice farmers (Agricultural Credit). About 3600 small bank units, known as unit desas (village units)were established nation-wide at the sub-district level for the purpose. They also administered othergovernment subsidised credit programmes. The results were not very encouraging due to substantial lossesincurred.

In June 1983, the Indonesian government announced a first series of financial reforms. A major provisionwas that state-owned banks could now set their own interest rates on most loans and deposits. Thederegulation provided an enabling environment for the transformation of BRI’s unit Banking system into asustainable rural financing network. The financial deregulation was followed by the decision that BRI’s unitbanks would be converted to a sustainable system of commercial banking at the local level.

In February 1984, BRI began a programme of general-purpose credit at commercial interest rates throughoutthe unit-banking network. Loans were made available to credit worthy borrowers for all productive purposesat interest rates that covered all costs, including operating costs and the non-subsidised cost of funds aswell as depreciation and risk and the institution made profits. New Savings products were introduced at allunit banks and by 1989 unit savings funded all unit loans. The BRI’s unit banking system is now one of thelargest system of sustainable microfinance in the world.

3.2.1 Basic Principles of Unit Banking System:-

Credit is made available to all creditworthy customers located within the Units’ working area.

Interest rate is set to cover all costs including the (non-subsidised) cost of funds, overhead costs, cost of loanlosses and to generate profit.

All savings are mobilized voluntarily by paying a positive interest rate.

BRI units are located in commercial centres.

Unit banking system is an individual lending programme. Appraisal is based on business, credit history,proposed loan use and applicants character (usually based on the recommendations from local governmentrepresentatives and neighbours). Many customers use the loans for multiple purposes. Loan periods varyfrom 3, 4, 6, 9, 12 and 18 up to 24 months. The loans are commonly repayable in equal monthly instalments.

Structure of BRI

18,613 Staff

286 VillageService Posts

3724 Units

323 Branches

Micro / Retail Business

12,097 Staff

323 Branches

Medium Business

Bank Rakyat Indonesia

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

17

Microfinance Regulation and Supervision

In 2000, the average loan size was $434 although small loans range between $200 to $2,500. Collateralsecurities are in form of property, vehicles, and other fixed or movable assets. However the collateralrequirement in Indonesia is not seen as a barrier to accessing of loans.

The organisation of individual BRI Units is kept very simple and transparent. This is done purposely, withthe basic unit staff consisting of four employees.

Organisation Chart of a Unit Desa (Village Unit)

Teller

Credit Officer Deskman

Unit Manager

The Unit manager heads the unit, approves the loans and is responsible for the unit’s performance. TheCredit officer analyses the loan applications, performs field inspections of the business of prospectiveborrowers, maintains regular contact with customers, and collects loans that have fallen in arrears.

The teller serves customers in carrying out cash transactions (mostly deposits, withdrawals and loanpayments)

The Deskman/Book keeper helps customers fill out bank forms and is responsible for keeping the books ofthe unit.

As business grows additional staff are added according to these standards:

• One credit officer for 400 loans (excluding fixed income loans)

• One teller for every 200 daily cash transactions

• One book keeper per 150 daily booking/transfer transactions

The maximum number of staff is eleven. If the unit’s business grows to where it needs more staff, the unit issplit into two or more units.

Village service posts are under the units. These service posts are manned by 2 people: a teller and abookkeeper and are open for one to five days per week. They receive loan applications, collect loanspayments and savings. Each of the branches supervises eleven units on average supervise units.

Above branch level are 12 regional offices each containing a Micro Business Department, which monitors thefinancial performance of the Units (largely on the basis of branch level reports) and takes corrective actionwhen appropriate. The Micro business department also co-ordinates unit policy and activities, setting ofinterest rates and internal fund transfer price, budget planning and purchases, personnel and recruitmentpolicy and training of unit staff.

As a separate business unit of BRI, the unit Banking system is directed by its own division at BRI headquar-ters in Jakarta and operates as a separate profit centre of the Bank. The core business of BRI units lies inextending small loans at commercially viable rates and collecting voluntary savings on which a positive realinterest rate is paid. In the past, many people were sceptical about the feasibility of successfully offeringcommercial banking services to small-scale customers particular those living in the rural areas. Peopleassumed that the bank would encounter problems with high over head costs, high risks and limited potentialfor both commercial loans as well as savings. Over a decade, BRI’s experience has proven these assump-tions wrong. The unit banking system has shown that providing financial services to the poor can be comple-mentary with institutional profitability.

3.3 Key Principles of Success of the Unit Banking System and Lesson LearnedDuring the past decade, BRI has learned many valuable lessons in moving away from a targeted, subsidisedrural finance programme into a full-service, fully commercial microfinance institution. Some of the mostimportant of these lessons are:

18

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

In order to minimise overhead costs; credit should be made available to all creditworthy microcredit customers.If a bank can serve only one particular segment, such as agriculture, staff and other overhead costs aretoo high. The bank should be able to lend for any productive enterprise.

Credit decisions should be based solely on a borrower’s willingness and ability to repay – and this decisionshould be left to the bank. The amount of the loan should be directly related to need and the assessedrepayment capacity of the enterprise and borrower. If agricultural extension workers or other governmentofficials make the decision, the creditworthiness criterion is diluted. The borrower should know that loandecisions are based solely on the bank officer’s judgement of creditworthiness, and that additional creditswill be available if earlier loans are repaid according to agreed terms.

Access to credit on a long-term basis is more important than cheap credit. Interest rates should be set tocover the costs of the bank so that the bank is financially viable, and can therefore provide credit over thelong term as needed. Consistency and sustainability are far more important to borrowers than cheapcredit programmes, which fade away when the government’s budget is tight or donor fashions change.

Almost all households want to, and are able to save, thus serving their need to save is just as important asserving their demand for credit. There is a large potential for savings among relatively low-income people.However, savings instruments must be designed to meet the needs of savers. People need a safe placeto keep their savings as well as liquid savings instruments for their routine enterprise and householdfinancial requirements. They need to have funds available to meet unforeseen emergencies as well as tomeet regular, relatively large expenses such as school fees.

Operating a large network of small banks requires a combination of simplicity and transparency,standardisation, and delegation of authority and responsibility. The cornerstone of the UnitBanking System’s transparency lies in the simplicity of the credit and savings instruments offeredand the Unit’ financial statements. Savings and loan terms, interest rates, reporting, training andprocedures are all standardised. With this simplicity and standardisation, it’s possible to createan efficient well-supervised system, which delegates authority to the local level. Thus, both theresponsibility and the authority for making good loans and earning a profit lie at the local level.Bank Dagang Bali (BDB)

This is a privately owned commercial bank with its headquarters in Denpasar, Bali. Privately founded bythe Oka family in 1970, it is licensed as a savings and lending institution. It is the first private bank in Bali.

According to its annual report of Year 2000 BDB has 8 branches, 18 sub branches, 4 cash service officesin addition to its headquarters office at Denpasar. This is a total 31 banking facilities operation with 630staff. Total assets of BDB were approx. Rp 1,374 billion. The total savings deposits of approximatelyRp1,110 423,687 savers held billion. Total loan

3.4 Lessons from IndonesiaThe attempt by government to regulate Rural Micro banks, as BPRs did not primarily succeed. This wasdue to the new legal status and complexity in governance and legal transformation that was too complexto the villages. Additional problems arose from the industry problems experienced in Indonesia and somewere concerned about government interference if they transformed into BPR’s. Furthermore some MFIswere not taking deposits from the public or the levels of deposits were minimal to warrant conversion.

It is therefore noteworthy that, in Indonesia the Government passed law to regulate institutions that couldnot be practically enforced. Government is reviewing the legislation under the new Microfinance InstitutionsAct. However the success of BRI is commendable. The programme succeeded because the unit banksloaned at market rates used income generated to finance their operations kept operating credit low anddevised appropriate savings instruments to attract depositors. By mobilising rural savings, the unit bankingsystem was provided with stable funds and also kept financing credit in rural areas thus helping developmentgrowth in the countryside. Other reasons for success included the simplicity of loan design, which cutcosts, effective management, close supervision and monitoring and appropriate staff training andperformance incentives.

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

19

Microfinance Regulation and Supervision

3.5 ConclusionThe state of regulation and supervision of microfinance in Indonesia, as in India are still at the foundationstage. The laws and regulations are either still under discussion or in progress and may take sometime tobe implemented. While linkage banking is a good programme, it is suitable for sustainable MFIs whichhave a proven track record and have shown some success i.e. profitability. Direct facilitation by Governmentof India will continue. BRI has proved that properly designed schemes can be successful in lending to therural poor. It results in profitability as BRI has shown. But the institution has also learnt from the problemsof earlier directed lending.

Uganda has made considerable progress in formulating the legal framework for regulating and supervisingmicrofinance institutions, which will access deposits from the public. As indicated in the Indian and Indonesiacases one cannot regulate all the institutions providing Microcredit/Microfinance. Some formal institutionsmay remain providing creditors only, while others will continue to provide credit informally.

However as funding sources dry up for credit, the need for savings mobilisation and commercialisationbecomes imperative options. Bank of Uganda will only license strong/sustainable institutions to mobilisesmall public savings and intermediate the same. Other institutions, which may not pass the barrier forlicensing requirements, will remain under tier 4 to enable the institutions to continue to provide meaningfulcontribution by provision of Microcredit to the population which do not have access to formal credit. It willalso enable the institutions grow into strong viable entities.

20

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

4 Savings Issues – Guy Winship, FINCA Uganda

4.1 Regulation and Supervision of Micro - Deposit-taking Institutions - Experiences relatingto Savings mobilisation

4.1.1 Introduction

The demand by low-income communities for savings services was as apparent in India as it is in southernand Eastern Africa. Also apparent was a belief that any financial institution taking savings from the public -whether intermediating these or not - needed to be regulated in order primarily to protect the resources of(especially smaller) savers. This would include some form of deposit insurance aimed especially at the lesswealthy, and the value of which is usually capped. Regulation to ensure prudent on lending and/or investmentof these savings was needed by an appropriate body. This would include the setting of objective prudentialnorms and standards, and the supervision that adherence to these was being met by an appropriate bodywith the authority, competence and willingness to do so.

A senior economist from RBI stressed that increased savings levels in a country invariably leads to loweringof foreign debt levels needed to cover domestic investment and consumption demand, and that mobilisingnew funds into the economy (from previously un - or under-banked sectors) would be of macro-economicbenefit.

A secondary objective seemed (in that it was less explicit) also to be a desire to use these resources to thebenefit of targeted sectors such as the rural and agricultural sectors, both through a directed lending policyimplemented through the supervisory authority, and by offering or withholding registration, for example inunder-serviced or over-serviced areas. Similar prudential norms to those used in East Africa were to befound, although the governance and political will to adhere to these established prudential standards seemedto be stronger.

Both the RBI and BI stressed to the delegation that an enabling macro-economic and politically stabileenvironment, along with an appropriate regulatory environment and adequate supervision to protect depositorswas important to have in place prior to registration of the institutions.

4.1.2 State Intervention

The nature and forms of state intervention, and regulation/supervision found in India seemed relativelyonerous, which was to be expected given the degree to which the banks are state-owned and managed (allcommercial banks in India were nationalised in 1969). The increasing commercialisation of the bankingsector and the recent opening of the sector to allow (albeit limited) foreign investment highlighted both theneed for additional structural support to promote financial services within low income communities and theimportance of regulation to protect these savings. This point was stressed by all agencies, although thenature and form of how such regulation and supervision should take place solicited less agreement.

Self-regulation was generally not considered an appropriate vehicle for setting, enforcing, or ensuring statutory(or, some senior managers at NABARD commented, even prudent) compliance with norms and standardsof micro-finance best (or better) practices. While it can be noted that regulation and supervision clearly donot have to be done by the same entity, it was still thought that self-regulation would not be appropriate forregulation or enforceable in terms of supervision. This was interesting as precisely this separation of the twofunctions takes place in much of the rural development finance sector in India, with the Reserve Bank ofIndia setting the standards, and NABARD supervising and monitoring them. Of course this is still not self-regulation.

As in many other countries the issue of ownership was considered central by both RBI and BI in ensuringadherence to prudential norms, and the lack of clarity of certain not-for-profit and NGO structures was anarea of concern. No clear solution other than ensuring adequate core capital in the form of equity, and thusrequiring registration with the Registrar of Companies as a (for-profit) company, was offered. It was stressedthat the institution needed to demonstrate ownership, effective governance and high level of managementcompetency. The institution should be (or have reasonable plans to attain such within a determinable period)financially sustainable, and has illustrated a low level of credit delinquency as well as sufficient capital.

Similar to Eastern and Southern Africa, RBI felt that the nature of the organisation, whether for-profit or not-for-profit, company or NGO, commercial bank or (regulated or non-regulated) non-bank financialinstitution, was not important. Instead, the issue was the taking of savings from the public and theintermediation of these savings. An interesting issue was that the RBI, and BI and senior staff of BRI inIndonesia, felt that regulation of micro-finance institutions only offering credit (viz. not taking or intermediating

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

21

Microfinance Regulation and Supervision

savings) was necessary, although at a much lower level of supervision (generally only getting annual auditedstatements and special reports).

4.2 The Need/Demand for Savings by the Poor - General Comments The need and demand for savings services by low income in both India and Indonesia reflected that in sub-Saharan Africa, in that savings by the poor was needed for expected occasions and eventualities, includingsocial and religious events such as weddings, pilgrimages and Easter etc; life-cycle occurrences – bothplanned and unexpected - such as birth and education of children, retirement or death of a family or communitymember; and business related events, such as building capital for investments, and for unexpected investmentopportunities especially business opportunities; and to provide assistance with volatile income and cashflow streams.

The nature of the demand for savings services by low-income savers in both India and Indonesia relates –in a manner that parallels the experience of micro-credit clients. It is an issue of accessibility, security,respect, and confidentiality. These also have the same importance as the interest rate receivable and feespayable on the savings accounts.

Accordingly, an MFI has to build trust so that depositors feel sufficiently safe to keep their money with theinstitution. The focus then should be on the development of appropriate products, with simple proceduresas well as efficient and prompt service.

4.3 The Case for Transformation & IntermediationA number of interesting issues arose as to why mobilise savings. This therefore leads to a question as towhy credit-only MFIs credit-only MFI’s (whether NGOs or other structures) transform? The main issue atboth the policy level and at the operational level should be to provide a wider range of financial services tolow-income people. This relates to the demand for such appropriate services by the poor as outlined above.

Other issues that were raised, which relate to the motivation for saving (and their intermediation) to theinitial micro-credit services included:

• increasing profitability of the institution as a result of taking savings (based on a bigger asset base, etc)

• providing related services so to attain improved scale economies and hopefully, reducing unit costs,lowering interest rates on related services (credit, payment, transfer, insurance and other services)

• Achieving economies of scale, there are clear synergies to be gained from increasing the range offinancial services from credit operations to include savings mobilisation

• Widening the range of services will broaden the client base, which may assist with improved riskmanagement and exposures

• Assisting the institution attain or improve financial sustainability, which is an important source of low-cost capital for growth

• Enabling access to savings lowers dependency on other funding sources, including commercialborrowings and donors

India and Indonesia’s experience demonstrate that the financial performance and outreach in credit-onlyinstitutions are invariably less successful than those that are mobilising and intermediating savings.

22

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

5 Self Regulation Mechanisms for Unregulated MFIs – Dorothy Katantazi, MEDNET

5.1 The Indian and Indonesian ContextAs far as self-regulation is concerned, the microfinance sector in both countries is more developed than inUganda. Nevertheless, there are still lessons that the Uganda team could share with their counterparts inAsia. The markets in Asia are more concentrated and bigger, as explained in chapter one.

The concern in this section is how individual countries address self-regulation for MFIs. Both countries arestill developing regulatory frameworks for microfinance. Currently, governments are directly involved inregulation and supervision through their Central Banks and in some cases through the state Banks i.e.NABARD in India. In Indonesia the regulation is carried out by BRI in Indonesia which is one of the statebanks. Both countries have not yet reached any position on MF laws. Some MFIs are supervised under theexisting Banking law while others, which are credit-only or based on their small size are still left unattended.

5.1.1 The Approaches to Self Regulation and Supervision

In the case of India, NABARD provides guidelines for self-regulation and supervision for non-Bank Creditonly institutions. (Criteria of selection of self-regulators and guidelines in supervision of non-Bank creditonly). The Reserve Bank of India has left credit institutions to grow before they can be regulated/supervised.This allows for free play and innovation.

In Indonesia, the Government /state -owned banks, BRI supervises its network of over 4000 BRI UnitDesas.

Nonetheless, a type of Self-Regulation Organisation (SRO) built on the German Model of Regional co-operatives is being studied. The proposal has characteristics and retains the basic principles. The SROconcept, once fully developed, would take up the supervisory role, while the Bank maintains regulatoryauthority. In relation to this, MF Associations would ensure minimal ethical standards while the Central Bankwould ensure compliance.

India plans to use their MF Network, Sa-Dhan, to regulate and supervise its members who do not fall underformal regulations/supervision. This approach, however, raises the following issues:

• Experience has shown that the idea of networks formally regulating their members has not workedanywhere else in the world.

• The sector was not ready for regulation e.g. while there are more than 1000 MFIs in India only 45 aremembers of their network, Sa-Dhan. Those are the more professional ones.

• Network lacks mandate and legitimacy in this area

• May give rise to conflict of interest in roles, since a network will be the promoter, the regulator and thesupervisor. There may be issues of compromise.

• Better for a network to focus on capacity building of members, win their members’ confidence encouragetransparency and have an independent regulator/supervision.

5.2 Recommendations:Formal self-regulation of members by Networks is not recommended. However, self-regulation can besuccessful if is done informally by networks through, setting standards and benchmarks for members towardsbest practices but not as policing the members. One option may be involvement of a Self-RegulatoryOrganisation (SRO) as is being researched in India. Uganda can also benefit from the German model thatIndia has drawn examples from.

Another option can be in exploring regulation and supervision through a private company (almost similar towhat the private MF Raters do) This company may be supported by the Central Bank in Capacity Buildingfor proper interpretation of the MF Bill and law. Then if the Central Bank is convinced regarding quality ofservices, they can delegate the supervision function to such a firm.

The third option may be explore the idea for parliament to set up a regulatory commission – however, onewould ask the following questions in this case: feasibility/administrative capacity/is Uganda ready for such.

The fourth option would be for Government not to interfere with the 4th Tier but have it as an allowablebusiness mentioned in the law, as long as these MFIs do not intermediate savings and just let their Networkssupport them to monitor their operations. This would allow for innovation and maturity of the Industry until

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

23

Microfinance Regulation and Supervision

such a time when regulation is warranted, coupled with the capacity to implement.

5.3 More LessonsUganda should have the MDI Bill and law ready but MFIs should not rush in for regulation, but rather,undertake careful assessment and reparation to avoid accidents for practitioners and for the industry e.g.Bolivia needed three years to prepare adequately.

Government should adopt a phased approach for transiting MDIs, to allow for learning, experience sharingand capacity building.

The Africa-wide Network of African Microfinance Associations could review the membership structure of itslocal networks - In India, the MF Network, Sa-Dhan has only a membership of 45 members while there aremore than 1000 practitioners in the industry.4 These include NGOs, co-operatives, for profit companies andgovernment owned institutions.

There is a need to explore the effectiveness of government intervention in as far as it can contributeto the development of banking and MFI sectors like has been demonstrated in India and Indonesia.In the case of Uganda, there might be need to ascertain the critical areas where this governmenteffort could be promptly directed. This in turn could lead to a more effective and efficient contributionto the development of this sector by the government.

4 Many of the members are Associate members who are represented by their Apex Organisations.

24

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

Microfinance Regulation and Supervision

6 Lending to the Rural Population, Successes and Challenges – Eva Mukasa,Uganda Women’s Finance Trust

6.1 Summary of ObservationsAs discussed in preceding sections, successes and challenges abound in provision of services and specificallycredit to the rural dwellers Experiences in India and Indonesia highlighted the following issues. In the caseof India, heavy involvement by the Government in forcing financial services especially credit, reach the ruralareas is manifested in various developmental support including:

• Capacity building of grassroots self help groups and institutions that serve the rural population.

• Mandatory minimum lending by commercial banks to the vulnerable groups (especially the poor andthe women).

• Setting up and promoting SHG – Bank Linkage programmes.

• Promotion of SHG – Bank linkage programme.

• Presence of Regional state Commercial Rural Banks in every state with mandate to do microfinanceence.

The combination of delivery mechanisms in India with the following structures:

(i) National Bank for Agricultural & rural Development (NABARD) which intervenes at all levelsincluding directly to SHG, serving as an apex body for financing other MFI’s and an apex forlinkage programmes between SHG and state banks, Co-operative Banks.

(ii) Regional Rural Banks for example the Manjira Grameen Bank Navajyothi

(iii) Mature NGOs that have transformed into MFI’s for example SHARE with subsidiaries thatdeliver different services.

(iv) Private Limited Companies such as BASIX.

There is no legal framework yet to regulate the sector but NABARD has been mandated by the ReserveBank to supervise all MFI’s and NGOs and Banks (Co-operative and Regional Rural Banks) in terms of themandatory lending to the vulnerable groups.

6.2 BackgroundGrowth with distributive justice and the alleviation of poverty has been the explicit objective of governmentpolicy in India for many decades. With the nationalisation of major commercial banks starting mid-1970’s,1975 another impetus to the expansion of the rural banking network was provided through: -

• The establishment of district-level regional rural banks (RRB’s) as subsidiaries of the major publicsector commercial banks.

• The expansion of the co-operative network through the establishment of village level Farmer’s

The RRB’s in particular were established to meet the credit requirements of the poor – small and marginalfarmers, landless workers, artisans and small entrepreneurs. The financial services to the poor in India areprovided mainly by more than 33000 rural and 14000 sub-urban branches of the major bank and RRB’s andby the 94000 co-operative outlets – either bank branches or village level societies. This implies that as faras availability of credit outlets serving the rural sector and the poor, there is one institutional outlet for every5600 persons. Current estimates show that there are 400 – 500 NGOs engaged in mobilising savings andproviding Microloan services to the poor.

Though many MFI’s were initially funded by donor support in the form of revolving funds and administrativegrants, in recent years, NABARD, SIDBI and Microfinance promotion organisations have also started providingbulk loans to MFI’s. Consequently, the MFI have now tended to become intermediaries between the largelypublic sector development finance institutions and retail borrowers. NABARD in particular has promotedthe SHG – bank linkage programme by refinancing commercial bank loans to SHGs.

6.3 Methodologies and ModelsMFI’s can be categorised as follows:

An Insight into Microfinance Practice in India and Indonesia: Lessons for Uganda

25

Microfinance Regulation and Supervision