passerelles n°2 - regulation for innovation in microfinance

DESCRIPTION

By offering mobile accounts and by engaging in the intermediation of mobile money, mobile phone service providers often take over (at least part of) the roles and responsibilities of traditional financial service providers, including deposit taking. The key objective of regulation, however, is to protect peoples’ savings and to guarantee the stability of the financial system. So, the regulators must take into account these new actors and continuously adapt national and international regulatory frameworks in order to include rules and regulations for new types of providers and for innovative products and services.TRANSCRIPT

P asserelles

Regulation foR innovation in MicRofinance

en

October 2015ISSN 2354-5402N° 2

Bridging academic research with field practice

The EIB Group helps leading microfinance providers, investment fund managers and other stakeholders to increase sustainable and responsible access to finance for micro and small-sized enterprises. The Institute complements the actions of the EIB Group in the area of microfinance. We provide grants and sponsorships for conferences, higher education and research in order to enable the continuous development of microfinance in Europe and beyond in line with our goal of promoting EU objectives by supporting European initiatives for the common good.

The EIB Group, which consists of the European Investment Bank, the European Investment Fund and the EIB Institute, has a long track record in microfinance both within and outside the European Union (EU). Within the EU, the EIF is active in financing micro-enterprises through the new EU Programme for Employment and Social Innovation (EaSI). The EIB is active across the sub-Saharan African, Caribbean and Pacific regions as well as in the Mediterranean partner countries. Recently, the Bank has begun microfinance activities within the EU, notably in Spain.

To find out more visit our websites on www.eib.org, www.eif.org and institute.eib.org or follow us on Facebook, Twitter and You Tube @EIBtheEUbank and @EIBINSTITUTE

The EIB Institute: a question of priority

© Advans

© Advans

Annonce Juillet_Institute.indd 1 07/09/15 16:06

3

Regulation for Innovation in Microfinance

Foreword Olivier Massart 5

IntroductionSophie Wiesner 7

Summary

the impact of mobile banking on inclusive finance and regulatory systems: What is the outlook for the next 10 years?Laurent Lhériau 8

Interview with the Reserve Bank of FijiBarry Whiteside 15

client Protection and Innovation Hearing from the “Voice of the Client” in IndiaNatalie Giggy, Justina Wong 19

Interview with Fundesurco Gabriel Meza-Vasquez 27

Editor

ADA asbl39, rue GlesenerL-1631 LuxembourgTel.: +352 45 68 68 1Fax: +352 45 68 68 68www.ada-microfinance.orgRCS Luxembourg F 199CCPL IBAN LU64 1111 1189 2705 0000

Copyright: ADA, October 2015

© pictures : Ken Banks, Charles Cordier, Morgan Davis, Fondesurco, Martin Garcia, Good World Solutions, Björn Groß, Simone D. McCourtie, Kalyan Neelamraju, Tom Perry, Reserve Bank of Fiji, Felix Sorger, John Trif, World Bank.

© cover picture : Simone D. McCourtie, World Bank

Graphic work : Cropmark Print : Imprimerie Centrale

The EIB Group helps leading microfinance providers, investment fund managers and other stakeholders to increase sustainable and responsible access to finance for micro and small-sized enterprises. The Institute complements the actions of the EIB Group in the area of microfinance. We provide grants and sponsorships for conferences, higher education and research in order to enable the continuous development of microfinance in Europe and beyond in line with our goal of promoting EU objectives by supporting European initiatives for the common good.

The EIB Group, which consists of the European Investment Bank, the European Investment Fund and the EIB Institute, has a long track record in microfinance both within and outside the European Union (EU). Within the EU, the EIF is active in financing micro-enterprises through the new EU Programme for Employment and Social Innovation (EaSI). The EIB is active across the sub-Saharan African, Caribbean and Pacific regions as well as in the Mediterranean partner countries. Recently, the Bank has begun microfinance activities within the EU, notably in Spain.

To find out more visit our websites on www.eib.org, www.eif.org and institute.eib.org or follow us on Facebook, Twitter and You Tube @EIBtheEUbank and @EIBINSTITUTE

The EIB Institute: a question of priority

© Advans

© Advans

Annonce Juillet_Institute.indd 1 07/09/15 16:06

DISCLAIMeR: Views and opinions expressed in this publication are those of the author(s) and do not necessarily reflect those of ADA. Neither ADA nor any of its employees, agents, third-party content providers or affiliates may be held liable for the use which may be made of the information contained therein. The authors acknowledge that no third-party textual or artistic material has been included in the publication without prior consent of the copyright holder to further dissemination by third parties.

Under the High Auspices of HRH the Grand Duchess Maria Teresa of Luxembourg

ADA is able to pursue its mission thanks to the support provided by the Luxembourg Directorate for Development Cooperation and Humanitarian Affairs.

With the financial support of:

4

P asserelles – n° 2

5

Regulation for Innovation in Microfinance

The computerization of our economy and the use of mobile technologies for financial intermediation facilitate financial transactions, particularly for providers operating in remote rural areas and for clients being excluded from the traditional financial system. The moments when money can be deposited or withdrawn from a mobile account correspond better to the moments when the money actually flows in and out of micro-enterprises and low-income households. People are no longer obliged to seize the opportunity of going to the town or market to make their financial transactions, but they can now manage their money at the time and in the frequency that is most convenient for them.

In addition, innovations like mobile money also secure financial transactions, as they reduce the risks of cash-handling. People do no longer have to keep money in their houses where it is often stolen (and where it is also subject to many more demands); they no longer have to carry cash across long distances (e.g. from the market place to their home town); and their mobile accounts are protected, even if their mobile devices are stolen or destroyed.

By offering mobile accounts and by engaging in the intermediation of mobile money, mobile phone service providers often take over (at least part of) the roles and responsibilities of traditional financial service providers, including deposit taking. The key objective of regulation, however, is to protect peoples’ savings and to guarantee the stability of the financial system. So, the regulators must take into account these new actors and continuously adapt national and international regulatory frameworks in order to include rules and regulations for new types of providers and for innovative products and services.

Regulation for Innovation in Microfinance

Olivier Massart, Managing Director, ADA

Mobile devices also allow for the collection of all types of data, including data on financial transactions and financial behavior; and while this data can be used to adapt microfinance products and services in order to better meet peoples’ needs, it can also be used for other purposes and raises questions in terms of client protection. As client protection is another objective of regulation, however, also these new risks must be taken into account by policy makers and central bankers.

The present issue of Passerelles on the subject of regulation and innovation in inclusive finance offers the reader some selected perspectives on the topic and invites those interested in sharing their views to submit comments on ADA’s website.

Foreword

6

P asserelles – n° 2

7

Regulation for Innovation in Microfinance

Background At different stages in the course of its his-tory, the sector of inclusive finance expe-rienced different developments in terms of regulation. In its early days, microfinance was focused on microcredit (especially on group lending vs. individual lending) and was nearly unregulated. The extension of the financial services offered, including savings and insurance, however, brought about an adaptation of regulatory frame-works in later years.

An increased commercialization and com-petition with an ever larger number of fi-nancial service providers (of very different legal forms) led to an attempt to adapt the rules of traditional finance to the context of microfinance. In addition, microfinance crises in certain countries (e.g. in Bolivia, Bosnia Herzegovina, and Morocco) cre-ated a renewed awareness of the impor-tance of formal regulatory frameworks and of their contribution to building inclusive financial systems.

In some places, the evolution of regula-tion lags behind market developments, and informal regimes (e.g. codes of conduct for providers and funders) replace formal ones. In other places, however, public ef-forts reinforce private efforts, and regula-tion helps to build inclusive financial sys-tems.

The so-called “regulator’s dilemma” there-by consists in guaranteeing the stability of the financial system, in controlling and legitimizing providers, and in protecting clients, while at the same time allowing for enough flexibility to foster inclusion and en-courage innovation.

Today, innovations, particularly in terms of new technologies, provide further opportu-nities for inclusion (e.g. via mobile money solutions). However, they also confront the sector with new challenges concerning regulation. This is one of the reasons why the topic has been reinitiated as a priority in international agendas – in a year which marks the european Year of Development, the definition of the post-2015 sustainable development goals, and also international discussions on financing for development.

Content and Structure

This second issue of Passerelles deals with the topic “Regulation for Innovation? Building Inclusive Financial Systems” and consists of two articles and two interviews.

The two articles link recent research on regulation and innovation to experiences from the field; while the two interviews pro-vide further insights into concrete cases.

A first article, written by Laurent Lhériau, an independent specialist in financial regula-tion, deals with regulatory frameworks for inclusive finance from the perspective of providers.

The focus of the article is on mobile net-work operators (MNOs), the specific legal challenges and opportunities that they encounter, and the future role that mobile financial service providers will play vis-à-vis traditional financial service providers. The article describes the medium-term and long-term consequences of the presence of MNOs for financial inclusion, and it dis-cusses how regulation and supervision are supposed to adapt to the described deve-lopments.

The first article is followed by a first inter-view with Barry Whiteside, Governor of the Reserve Bank of Fiji. The interview pro-vides the perspective of a regulatory body on regulation and innovation for financial inclusion and describes the specific ex-perience of Fiji in terms of mobile money. The Reserve Bank of Fiji has established a National Financial Inclusion Task Force and has defined a National Financial Inclu-sion Strategy, thus achieving its objective to reach 150,000 unbanked Fijians with some form of financial services – including mobile financial services – ahead of time.

A second article, written by Justina Wong, Senior Manager of Global Operations at Good World Solutions, and Natalie Giggy, Data Insights Manager at Good World So-lutions, deals with regulation and innova-tion by focusing on microfinance clients.

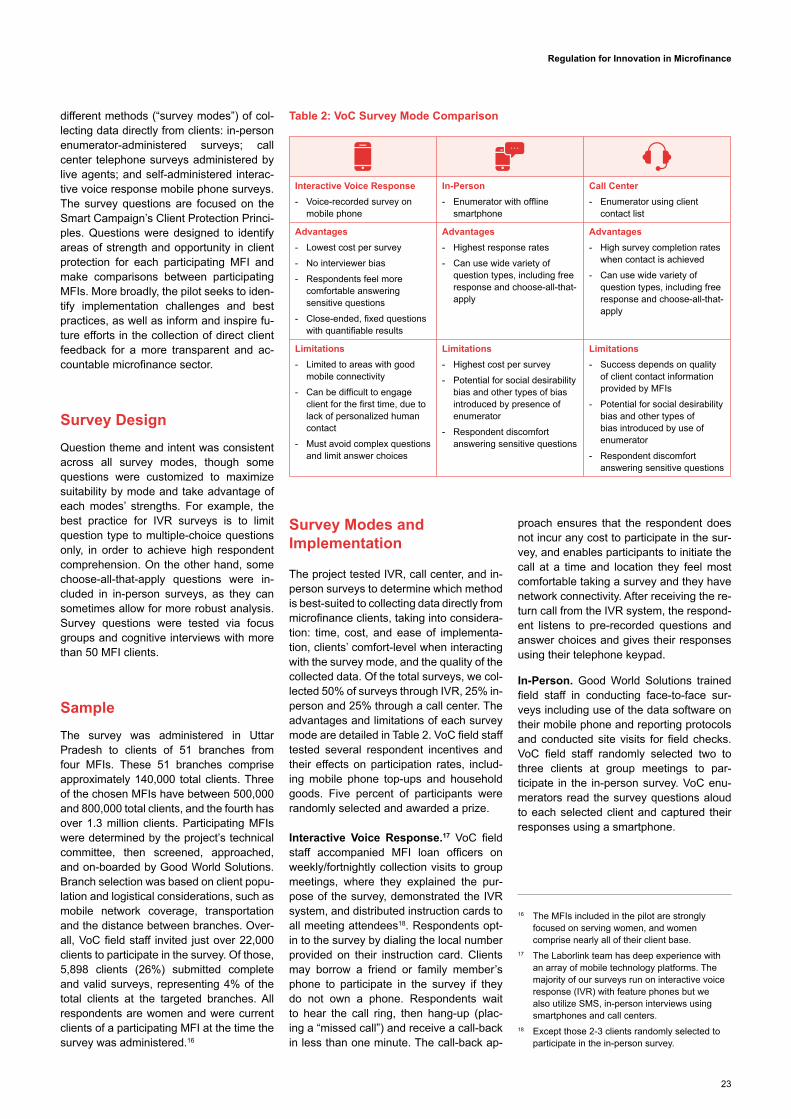

The article provides an overview of client protection principles and describes the technical details, as well as some first re-

sults of the so-called “Voice of the Client” project in India. This project uses new tools and techniques for the collection of data on client protection at the level of clients (not at the level of providers), with the informa-tion concerning, for example, loan collec-tion practices or complaint mechanisms.

The second article is followed by an inter-view with Gabriel Meza-Vasquez, General Manager of Fondesurco in Peru. In this interview, the topic of regulation and in-novation is discussed with a focus on mi-crofinance providers, highlighting the ex-perience of Fondesurco in terms of client protection and its participation in the “Voice of the Client” project in Peru. The interview underlines that the use of mobile phones and interactive voice response platforms has advantages for data collection, as it reduces time and costs; but the interview also identifies disadvantages of the use of new technologies, especially in rural areas.

Introduction Sophie Wiesner, Manager Research & Development, ADA

8

P asserelles – n° 2

The impact of mobile banking on inclusive finance and regulatory systems: What is the outlook for the next 10 years? Laurent Lhériau, specialist in financial regulation

Remote banking services have been growing over the last ten years and are currently domi-nated by mobile phone services

provided by mobile network operators (MNOs). These operators are increasingly switching from an additional financial ser-vices-based approach to one of alternative banking services for the underbanked in emerging or developing countries (eDCs).

The involvement of MNOs is a potential revolution for inclusive finance, an industry still not well-regarded either by the ‘conven-tional’ sector (MFIs and retail banks) or by regulators (even if the latter tend to develop “2.0” regulations for retail banking agents or payment institutions). Discussions are generally focused on real perspectives of expansion for financial inclusion rather than on the medium-term structural conse-quences (5-10 years) on the financial sec-tor, which could find itself overwhelmed in terms of players and standard operating methods. This may involve customers in developing countries shifting from a com-mercial relationship via ‘physical’ branches to more remote ones, with transactions be-ing carried out via mobile phones (as well as traditional bankcards).

To those who object that these solutions will take much longer (decades perhaps) before becoming standard use for consu-mers, one can respond with a few facts. In less than fifteen years, the mobile phone has conquered developing countries, even the least developed ones, just as it has in the rest of the world. The traditional cultural preference for hard cash is simply the re-sult of a lack of formal and affordable lo-cal financial services. «Trust», however, can change. Finally, the population of the eDCs is young, very young actually, and new technology is as natural them as it is to the young in developed countries. 60-year olds will have to radically alter their habits to switch to mobile banking solutions. A 15-year-old boy selling fish in a market, however, will see mobile banking as just an extension of the mobile phone in his pocket that he already uses to answer his regular customers setting aside what the morning tide brings him and to receive their pay-ment the next day.

This article is primarily intended to be forward-looking. Its purpose is to under-stand what MNOs need to fully deploy their mass banking services worldwide, and the legal restrictions they may encounter. It also looks to assess the potential impact this could have on the historical inclusive finance sector and what possible adapta-tion strategies the sector may resort to in view of the compliance standards to be met (and/or used for their benefit). Finally, the article aims to see how regulators and supervisors will engage in accompanying this transformation of the regulated finan-cial sector.

laurent lhériau

Laurent Lhériau holds a PhD in banking law and has been working on topics related to microfinance

and financial inclusion since 1998. He has contributed to developing

many financial laws and regulatory frameworks in french-speaking Africa; and he also supports a number of financial institutions in terms of compliance issues,

especially anti-money laundering/ combating the financing of terrorism

(aMl-cft), as well as their institutional development. Laurent lhériau has written many articles

and is the author of the Microfinance Regulation Handbook (3rd edition, published by AfD in October 2015). He teaches at various universities and at professional organisations.

9

Regulation for Innovation in Microfinance

1. Mobile banking and MNOs: challenges and opportunities

1.1. Legal and regulatory compliance: given their potential, what do MNOs need to operate today?

1.1.1. Prudential compliance: with reference to CAMeL(I)S.

There is a general, widespread belief that MNOs need a financial partner in order to run their banking operations. Although this is often technically true, it is strategically false: they do not need a partner. MNOs can decide to develop their operations with or without a financial partner and, in prac-tice, they increasingly opt to go it alone, i.e. by creating their own financial subsidiary in the form of a specialised entity (an elec-tronic money institution - eMI) or a univer-sal bank.

What are the conditions governing these activities? A rapid glance at prudential supervisory requirements based on the CAMeL(I)S1 rating standards not only shows that there are no obstacles, but also that MNOs often outperform competition standards.

capital

The first obstacle is not an actual one. MNOs are used to paying at least a hun-dred million euros, sometimes up to sev-eral billion euros, for operating rights such as 3G and 4G licences. This, however, only grants them the right to install their anten-nae! Investing several tens of millions of euros to create a bank is not an issue if the business model justifies it: the invested capital will bring a return one way or anoth-er. One time-saving alternative could also be to acquire a small local bank in need of recapitalisation, and then to eventually rebrand it as part of the MNO whose name is better known than that of the smaller bank). Similarly, adhering to a solvency ra-tio is not an issue. In France, Orange’s re-cently announced intention to create their own bank and compete with the banking sector shows that, in certain countries, it is now possible to create a fully function-ing bank rather than just an eMI like the three MNOs in the Democratic Republic of Congo (DRC).

asset quality

The current mobile banking business model developed by the MNOs is focused exclu-sively on straightforward savings products and payment services. Assets are thus deposited in banks even when this is not required due to the banking partnership. In terms of prudential standards, the assets are therefore of a better, superior quality compared with those of the average bank.

Nevertheless, a greater diversification of the credit portfolio, in particular with a view to developing customer credit, could result in a standardisation of asset activity.

Management

MNOs are often listed large-cap multina-tional companies and as such are credible and stable shareholders. The rest is just a matter of resources, which can be bought. The only delicate issue, on an operational level, lies in managing retail networks and securing a possible supply to networks in fiduciary currency.

Earnings: income & profitability

This aspect is without doubt unknown, since MNOs currently communicate very little on the profitability of their operations. Judging from the now systematic deploy-ment of mobile banking services by MNOs as soon as they obtain a mobile phone licence in a given country, we can safely assume that the profitability is significant. Further evidence can be found in the crea-tion of eMIs or specialist mobile banks insomuch as obtaining and retaining finan-cial authorisations assumes profitability.

Profitability is based on several pillars in-cluding payment services, but also returns on deposits, the sale of customer traf-fic data or the growth of credit portfolios (though still very limited).

Liquidity

The overall liquidity of the system simply requires a sufficient portion of convert-ible assets to be maintained. If, in princi-ple, this is not an issue, the geographical scattering of agencies demands a liquidity management rethink to ensure that cash withdrawal services provided to customers are not disrupted by working capital short-ages. This can be addressed in two ways: by granting lines of credit to retailers in the form of current account overdraft authori-sations, and/or by a sufficiently dense and well-supplied network. Unlike stock market regulators who can impose requirements on listed companies’ shares, regulators do not currently seem to be imposing liquidity requirements within the retail networks of MNOs or their financial subsidiaries.

1 CAMeLIS: Capital, Assets, Management, Financial equilibrium, Liquidity, Financial Information, Sensitivity to Market Risks. The CAMeLIS system is a direct spin-off of the CAMeLS bank rating system (Capital Adequacy, Asset Quality, Management, earnings, Liquidity & ALM, Sensitivity) by raising questions about the quality of information as an integral part of the analysis.

10

P asserelles – n° 2

financial information

Management Information Systems (MIS) in mobile banking systems have the specifi-city of recording everything in real time on a single central server, thereby providing real time liquidity positions on a global and an individual (retail) level, as well as spe-cific liquidity details on an agent by agent basis. In this way, the sophistication of the transactions recording system is compa-rable to that of any international bank and appears to support all additional modules (AML-FT2 filters, “report” modules, etc.).

Market risk sensitivity

This last point mainly refers to the way as-sets are used and where required, to net foreign exchange positions resulting from international money transfers not yet offset. This sensitivity is therefore very low.

1.1.2. Compliance of market practices

Behavioural compliance in the market-place mainly falls under financial consumer law, in partial alignment with the Smart Campaign principles as well as principles of competition and financial integrity law. There are six sub-themes for an approach to rating market practices. This is called TeRICe3.

Transparency of conditions

It is a constant challenge for retail banks to display prices and, more generally, con-tractual and pre-contractual information corresponding to a threefold approach that can be summarised as “the right to know, the right to understand and the banker’s advisory role”. Any failure to communicate this information and the opaque nature of a number of clauses, including tariffs, tend to deprive customers of prices being sub-jected to competition.

How can mobile banks position them-selves in this tangled mess? In principle, one might be tempted to reply, “no better or worse” to the extent that although there is more information available, pricing prac-tices observed in mobile phone MNOs are sometimes far from transparent.

fairness

Treating customers fairly firstly requires not selling them ill-adapted products, es-pecially ones causing them to be over-in-debted. This issue is currently of marginal concern to mobile banking systems. One potentially sensitive aspect lies in control-

ling independent retailer networks and their behaviour in relation to customers who, if they are not exemplary, could run a repu-tational risk.

Appeal procedures & dispute resolution

MNOs generally set up their own call centres which, when sufficiently staffed for prompt response time, gives them a modern, leading edge, should an identical system be introduced for mobile financial services.

financial integrity (aMl-cft)

Anti-money laundering and combating the financing of terrorism are fundamental to banking systems offering savings and elec-tronic remote payment services, as these are considered particularly useful in the con-text of organised crime. However, MNOs have solid advantages to put forward.

The primary quality feature of the MIS is not only that it records and accurately traces transactions over time but also that it applies a large range of filters and analy-ses based on multiple criteria (including geographical) fed into the system. In fact, MNOs can detect which antenna a mobile phone was connected to when the transac-tion was made.

The second feature is agent-related, as they alone are in direct contact with the customer. Are they reliable? Here again, simple systems can ensure good quality treatment. As such, registering new cus-tomers allows digital processing, some-thing even banks do not systematically do. Rather than using paper documents, the agent can use a simple smartphone to take a photocopy of the contract and the customer’s ID. They then send it to the processing centre, which checks the qua-lity of work undertaken and only opens an account after checking and validating that all items are consistent. It is even possible to incorporate facial recognition features using digital photos taken by the agent. Notwithstanding the additional risk linked to the use of outsourced agents, the cus-tomer recording system seems to be more secure than those of the banks and MFIs.

competition

economic control carries with it the tempta-tion to turn this advantage into a perpetual source of revenue, which involves block-ing competitors out and/or driving out the weakest. As far as fast money transfers are concerned, some global leaders have had the nasty habit of imposing exclusiv-

2 Anti-money laundering/Funding terrorism. 3 TeRICe: Transparency of Conditions, equality

(fair and respectful treatment of customers), Appeals & disputes, Financial integrity (AML-FT), Competition, Savings.

11

Regulation for Innovation in Microfinance

ity clauses on their distributors, banks and MFIs. In competition law terms, this can be construed as an abuse of dominant posi-tion or an agreement restricting competi-tion, and some regulators have intervened to call for the removal of such clauses. Hence the actions taken by the Ministry of Finance in Senegal and the Al-Maghrib Bank in Morocco4.

The mobile phone sector has largely fuelled the legal press in terms of agree-ments or straight price cartels. There is no reason why this should not apply to mobile banking, especially in blocking access to fi-nancial institutions who could compete with mobile banking services offered by MNOs using a mobile phone solution that they themselves own. A logical reaction of the MNOs would be to set out such unfavoura-ble conditions to access their networks that their competitors would not be competitive. Such a practice would be non-compliant.

Savings (protecting saving)

The inherent credibility conferred by the public onto a leading telecom operator is undeniably and substantially more si-gnificant than that naturally attributed to an MFI or a small bank. Although a de-posit guarantee system tends to level out investor confidence in the banking system (up to the limit of the amount covered by the deposit guarantee fund), the lack of a guarantee system favours the most solid MFIs, leading banks or even MNOs or the financial subsidiaries under their brand. In Kenya, public confidence in leading MNO Safaricom thus contributed greatly to the initial success of M-PeSA, despite a virtual absence of regulations.

As such, the main restrictions to domination by MNOs should stem from market prac-tice law, i.e. laws forbidding anticompetitive agreements or the abuse of dominant posi-tion, and from the laws governing databas-es and the use of personal data. Although the former enacts common principles for market economies, the latter is, under the heading of protection, mainly a product of the european Union, which is often at-tacked by digital economy global leaders (and leading American companies). This is not insignificant, as the purpose of these norms is to prevent the formation of cartels in the economy in general and in the spe-cific case of inclusive finance, to protect the consumer.

1.2. Possible impacts on the inclusive finance market

Although mobile banking systems are likely to be a great success, particularly in un-derbanked countries or where the market is not yet saturated and, as such, market share positions can still be seized, it is im-portant to anticipate the possible impact of mobile banks on the existing financial sec-tor by focusing on some key points.

1.2.1. Securing revenue from payment services

Mobile payment services have demonstrat-ed a commercial ability to satisfy custom-ers with their conviviality (by using a sim-ple mobile phone), their availability (open 24-hours), proximity to cash conversion solutions (the local shopkeeper) and their genuine swiftness (a few seconds maxi-mum compared with so-called ‘prompt’ inter-account transfer systems or Western Union that take one or two days).

Logic would have it that mass-payment sys-tems are increasingly dominated by mobile banking solutions for either local payments (shopkeepers equipped with smartphones rather than electronic payment terminals) or money transfers, including international migrant remittances.

The impact on the income of financial in-stitutions may be drastic. Revenue from payment methods where commissions can make up a significant proportion of overall income should collapse. Countries with an under-represented banking sector such as the DRC, where branches are virtually non-existent across the territory, civil serv-ant wages are already being handled by mobile banks.

To remain competitive and preserve other even larger stakes like securing savings, conventional banking systems might even drive down payment costs to such a de-gree that they only represent a tiny propor-tion of their income.

Here lies the first major prudential conse-quence for the financial sector - a change to their financial equilibrium. Both taxpay-ers and regulators should incorporate this likely future reality into their systems.

1.2.2. Securing liquidity linked to customer deposits

The second prudential risk lies in the li-abilities side of the balance sheet. If, as a customer, I feel that my money is safer, more easily accessible, with a withdrawal cost that is the same or less for a mobile banking solution, why would I waste time depositing my money in a bank branch or an MFI? Figures on the amount of savings collected by mobile banks, and not just by M-PeSA in Kenya, suggest that the gra-dual shift of savings has begun. Although it is impossible to know when this will have a significant impact on the deposits of conventional financial institutions, we can predict that this movement will happen and that little by little, there will be a drop in people’s savings with financial systems that do not offer mobile banking.

On the whole, the liquidity of the banking system will not change because of this. We can even conceive that this liqui dity may rise since more customers will be re-gistered with banks. Nevertheless, in all of this, there will be winners and losers and the latter will become increasingly depend-ent on refinancing from the former. This will force them to generate a return on mobile banking equity while managing an increased liquidity risk.

In the extreme case scenario, the balance sheet structure of conventional banks and MFIs could be radically altered by this, with deposits likely to be reduced to their small-est possible share and replaced with debts to the financial sector.

1.2.3. What methodology and technology for credit transactions?

The third prudential risk lies in the impact of mobile banking on the credit portfolio. Managing deposits and a payment system is a profession in itself while appraising and managing credit portfolios is another. Clearly, in a system analysing customer debt potential (the basis of credit scoring systems), it is useful to have the customer’s funds in an account together with their transaction history. However, apart from consumer credit for employees with bank-

4 See “Reducing the costs of migrant remittances to optimize their impact on development : Tools and financial products for the Maghreb and the CFA Franc Zone”, by N. Bourenane, S. Bourjij & L. Lhériau, December 2011 paras 144-153; available at http://www.afd.fr/webdav/shared/Conference/eSF_BAD_DGT_AFD_2011_Transferts_argent_migrants_rapport_fr.pdf

12

P asserelles – n° 2

domiciled salaries that can be managed by a software package, it is not enough to develop a sound credit business activity. Credit to formal companies requires the analysis of their financial position and knowledge about the business. In microfi-nance, credit requests must be appraised both physically and in situ due to a lack of reliable financial statements. This requires a suitable methodology and experienced credit agents.

It can therefore be expected that the growth of large-scale credit operations by mobile banks will be slower and more selective. While this may be manageable in the case of consumer credit for employees, it may be less so for real estate loans guaranteed by a mortgage, could be very complex for lending to formal and informal businesses and all non-wage-earning individuals. To secure accelerated growth (if desired), a mobile bank may probably have to ac-quire market share from the existing credit market with proven managers who can sharpen their analysis using information collected by the mobile banking network.

2. What will be left of the ‘conventional’ inclusive financial institutions and what strategic risks will they have to bear? Given the current revolution in mass bank-ing services, what will be left of the conven-tional players in retail banking and micro-finance? There are two possible strategic hypotheses.

2.1. Credit

The first hypothesis is that inclusive finan-cial institutions will specialise in specific credit products where the capabilities of their credit agents and their methodology maintains a certain competitive advantage, even if information on withdrawals and re-payments could be increasingly secured using payment services.5

However, the likely consequence of this type of specialisation will be that they even-tually join global financial groups. Indeed, their balance sheet structure will typically be that of specialised subsidiary compa-nies where the asset side is a relatively specialised credit portfolio and the liabili-ties side is capital and debts with the finan-cial sector, i.e. all the makings of becoming vulnerable to takeover and then becoming a subsidiary.

This affiliation could also happen to mo-bile banks. Themselves MNO subsidiaries, they subsequently seek to (i) find sources to profitably and reliably use the mass of deposits collected, (ii) complete their market by purchasing skills and market share where they are not dominant and, (iii) further strengthen their lead on the ‘conventional’ banking sector. This MNO-bank strategy might indeed target other segments of the credit market based on the level of economic development in the country. This includes real estate loans guaranteed by mortgages and consumer credit for employees, etc.

Although this appears to be an honourable solution for organisations highly influenced by a credit culture, it would be otherwise for mutualist banking networks that are almost genetically built around branch networks that dominate the collection of savings which they then recycle as credit.

On the one hand, these organisations are undoubtedly ones that cannot become specialist players in credit, as this would fundamentally challenge the stability of their balance sheets and the special rela-tionship with their member clients. On the other hand, they are in direct opposition to mobile banks in the savings market and money transfers. This remark generally ap-plies to all financial institutions targeting their strategy on a general offer and would see their balance sheet and profit sources strongly affected.

In the long-term, they have no other option than to find tailored responses to avoid be-ing whittled away, both commercially and financially.

2.2. The response!

Organising a commercial response in-volves restructuring business models around remote banking and, as such, de-veloping mobile banking services in addi-tion to ‘physical’ branches. Achieving this entails:

- establishing capital-intensive and com-mercial links between the banking and microfinance sectors,

- Crossing certain economic and regula-tory thresholds,

- Benefiting from competition law protec-tion.

2.2.1. establishing capital-intensive and commercial links between banking and microfinance sectors

Faced with the financial power of MNOs, the breakdown of the banking sector and further, the microfinance sector, is both a technical and a capital-based weakness. It is a technical weakness because it is important to consider payment services in their broader sense, to have technical standards able to interchange. It is a cap-ital-based weakness because investment is needed for the growth of mobile banking and an international presence. Obviously, this is lower than what is required to devel-op a dense network of physical branches, but it is still out of the reach of most MFIs.

For MFIs in the form of public limited com-panies, the logical solution would be to join a large banking group, as appropriate in a sub-regional (by currency and banking zone) or even a global (the holding compa-ny for an MFI network now being part of a multinational banking group) strategy. This would enable, in particular, dual-banking offers to remain attractive for migrants by supplementing traditional inter-account or cash transfer services with mobile banking services in key “remittance corridors”6.

2.2.2. Crossing economic and regulatory thresholds to have the means to fulfil one’s ambitions

For mutualist banking networks, the cap-ital-intensive equation is less clear. Al-though in developed countries they have a “consolidating” function which sometimes goes as far as buying up small and medium enterprise ( SMes7), merchant banks8, or even all-purpose banks9, most mutualist financial networks in developing countries fall under microfinance, according to regu-lations and above all in terms of financial potential.

5 See Lhériau L. Le droit et la technologie au service de la bancarisation : focus sur la banque à distance, Techniques Financières & Développement n° 100, September 2010.

6 e.g. the United-States / Latin America (Mexico, Cuba, Haiti, etc.), Japan / the Philippines, europe / the Maghreb, the Gulf / Maghreb, europe / Sub-Saharan Africa, and eventually the Maghreb / Sub-Saharan Africa?

7 Crédit Mutuel with Crédit Industriel et Commercial in France

8 BPCe with Natixis and Crédit Agricole with Indosuez (with became CALYON then Crédit Agricole CIB) in France.

9 Crédit Agricole with Crédit Lyonnais (which became LCL) in France. Groupe des Banques Populaires du Maroc with the Banque Atlantique en Afrique de l’Ouest (Western Africa).

13

Regulation for Innovation in Microfinance

Investing in mobile banking nationally and internationally entails setting up credit companies which itself requires mergers in order to reach critical mass, or even additional external investors10 in order to acquire capital holdings. Apart from this, alliances ‘between equals’ remain possible to introduce dual-banking11 services which will ultimately have to incorporate new forms of technology.

2.2.3. Benefiting from competition law protection

The last part of the response is to be able to access, and even to impose oneself (as appropriate) in MNO information transfer networks. Having mobile banking solutions is not enough. You must (i) access infor-mation transfer networks at a manageable cost12, and (ii) be able to download it using the required mobile banking application on a mobile phone.

This refers back to competition law. The modernisation of competition law and its governance by regulators (also conten-tious) is therefore a major challenge for traditional players in the financial sector to secure access to networks and the mobile phones of customers.

3. What should the attitude of regulators and supervisors be?

3.1. To have a clear ideological position

Three principles are recommended for re-gulators and supervisors to accompany this revolution in the financial sector.

- The first is to remain neutral about technology and distribution channels. Supervisors do not have to try to be strategists guiding the sector or to save established players whose operational methods are technologically obsolete14. They must restrict themselves to sup-porting financial innovation by smooth-ing the path of restructurings and liqui-dations when necessary.

- The second is to remain firm on pruden-tial supervision fundamentals. MNOs can create banks to manage their op-erations in compliance with the Basel Committee’s 29 principles for effective banking supervision. As for conven-tional players, particularly MFIs, they have the responsibility of making tech-nological, capital and financial related improvements and thus demonstrate their ability to “play with the big boys”. The supervisor must take care of secur-ing savings. Although mobile banks can handle this better than MFIs, there is no reason to be complacent to MFIs.

- The third is to enter the field of regu-lating marketplace practices that only

partially happens at present. Competi-tion law and deposit guarantee aspects are vital to supporting this change in the sector.

3.2. ... And to tackle the five processes that must go together with this revolution...

From country to country, there are five po-tential legislative and regulatory processes for regulators which would benefit from be-ing modernised, sometimes radically:

1. The first process concerns the “retailers /agents 2.0” law insomuch as a remote bank cannot operate without a network of retailers who are authorised repre-sentatives of the financial institutions. It is fundamental to enable networks of thousands, even tens of thousands of retailers to operate in a secure manner, legally and operationally. This should include the possible pyramidal function of these networks, sometimes taking up the distribution methods of units of time for requests from MNOs to wholesalers (“super-dealers”), retailers and occa-sionally between two semi-wholesalers (“dealers”). Payment between individu-als (“peer-to-peer”) must also be com-pletely legalised and mainstreamed without the need for an additional regis-tration or a trader’s licence15.

10 This is starting to happen, particularly in West Africa with BIMAO, a subsidiary bank of the Crédit Mutuel du Sénégal, or with plans to create the FINAO financial institution, a subsidiary of six of the largest mutualist financial networks in West Africa and their Confederation, the CIF. For the FINAO, see http://www.jeuneafrique.com/229307/economie/le-reseau-aux-35nmillions-de-clients/.

11 e.g. the dual-banking agreement between the BPCe Group (France) and the Banques Populaires du Maroc. See http://bpce.fr/Journaliste/Actus-et-Communiques-de-Presse/Groupe/Le-Groupe-BPCe-et-le-Groupe-Banque-Centrale-Populaire-au-Maroc-renforcent-leur-partenariat-commercial

12 Access costs must be without fail competitive (i.e. more than affordable!) insomuch as rates are in tenths per transaction and the profit margins in hundredths more or less

13 The question of the competent authority is not always easy. As such, if a bank of MFI is blocked by the elevated pricing conditions of a MTO that wants to protect is sector, who is the competent authority?

14 This involves, for example, eventually abandoning electronic money which is largely technologically obsolete, notwithstanding its use for trade

15 everyone becomes a potential source of liquidity (“human cash dispensers”).

14

P asserelles – n° 2

16 Considering that personal data is an attribute of our personalities and not just a simple piece of commercial data constitutes a serious affirmation of european law which tends to span the entire world with the european Union’s legislative influence

17 electronic signatures make it possible to make a valid engagement electronically. electronic evidence refers to law courts accepting (commercial, civil and criminal) pieces of evidence on electronic devices

18 By making behaviour that disrupts the modern economy an offence in criminal law in the same way as hacking networks and databases, falsification or data destruction, etc.

repayments but also bill payment habits through the financial sector, saving and spending habits, inflows of money, es-pecially from abroad for migrant families and any worthwhile information such as our health: taking certain medicines might label one as a risky borrower.

Mobile banking services gather a mass of useful information. They are also part of this process and there has to be a lot more than just professional banking se-crecy to protect the consumer16.

This is clearly a challenge beyond the scope of mobile banking, but financial regulators have to understand that mo-bile banking is not a simple supplemen-tary financial service. It is central to the network economy.

5. Finally, in general terms, it is important to include information technology in na-tional law at all levels, to make e-com-merce secure (with an electronic signa-ture and electronic evidence17) and to modernise criminal law (for databases and cybercrime18).

2. The second process concerns inclusive deposit protection for all. Deposit guar-antee funds are elements that ‘level up’ customer confidence. They therefore encourage a range of players and not just institutions that are “too big to (let) fail”. Introducing a single deposit guar-antee fund for the entire financial sector is an important part of this revolution.

3. The third process is competition law- and substantive law-related; agree-ments to restrict competition and abuse of a dominant position (in the case of information secured by an MNO and supplied to mobile banks and/or credit agencies) and procedures concerning regulatory authorities.

4. The fourth process concerns civil liber-ties, keeping in mind that “If the service is free, it is because you are the prod-uct”. This maxim feeds the new eco-nomy, it reflects the value of information on our consumer habits and supports “big data”. In financial terms, this is the same principle used by credit agen-cies to collect information on loans and

15

Regulation for Innovation in Microfinance

What were the most important milestones on the way to Fiji’s National Financial Inclusion Strategy and what are the main elements of this strategy?

2009 was a pivotal year for financial inclu-sion in Fiji as this was the year the Reserve Bank of Fiji (Reserve Bank) crystalised its commitment to take a strategic role in driv-ing financial inclusion in Fiji. This journey began with the establishment of a new group in April 2009 with dedicated resources and personnel within the Bank whose main focus was to drive financial inclusion and financial system development in Fiji.

This was soon followed by Fiji’s hosting of the second regional Pacific Microfinance Week held in July 2009. The conference provided an excellent opportunity for many stakeholders in Fiji to learn about microfi-nance and financial inclusion as it featured international, regional and local speakers, who enlightened stakeholders on ways in which they could contribute.

Following this, the Reserve Bank con-vened a National Microfinance Workshop in November 2009 to take stock, consult and strategise on a way forward for finan-cial inclusion in the country. This forum included representatives from public and private sector entities (including financial institutions), civil society groups, NGOs, microfinance institutions, donor agencies and development partners. This consulta-tive and collaborative approach, I believe, has been fundamental in contributing to the success of most of our financial inclusion efforts. Getting the buy-in from all stake-holders is the critical very first step in the process.

One of the key outcomes outcomes of the the National Workshop was the esta-blishment of a National Financial Inclusion Taskforce (NFIT) – an apex body responsi-ble for driving, coordinating, facilitating and monitoring financial inclusion initiatives in

Interview with the Reserve Bank of Fiji Questions answered by Barry Whiteside, Governor of the Reserve Bank of Fiji

«For smaller traditional service providers in Fiji […] to remain sustainable and competitive, they will need to adapt their services and leverage off the efficiencies of mobile technology. »

Fiji. The NFIT is supported by four working groups (Microfinance, Financial Literacy, Inclusive Insurance and Statistics) to drive the work and agenda of the Taskforce. To set some quantifiable measure, NFIT was assigned a mandate of reaching 150,000 unbanked Fijians with some form of finan-cial services by the year 2014. This target was achieved well before December 2014 and by the year end, 138% of our target was recorded.

The main elements of the strategy that was formulated at the Workshop were as fol-lows: 1) accessible and appropriate finan-cial education and consumer protection to empower consumers; (2) providing appro-priate and affordable financial products and services to the unbanked population; (3) a comprehensive data upgrade with relevant surveys; and (4) providing an enabling reg-ulatory environment.

In 2011, we took this national commitment further, and were one of the first of the seventeen countries that took a stand at the Alliance for Financial Inclusion (AFI) annual meeting in Cancun, to make a global commitment, known as the Maya Declaration.

We were pleasantly surprised when the Reserve Bank of Fiji was awarded the in-augural Maya Declaration Award by AFI during the 5th AFI Global Policy Forum held in Malaysia in September 2013. The Award was in recognition of “the institution that has set clear and measurable targets, and put in concerted efforts to measure progress”.

Barry Whiteside

Barry Whiteside, career central banker and Governor of the Reserve Bank of Fiji, is a champion of financial inclusion in Fiji. He took over the helm of the Reserve Bank of fiji in December 2010, successfully

completing Fiji’s first medium-term financial inclusion strategy (2009-

2014), which included reaching 150,000 unbanked or underserved Fijians. Fiji’s efforts were recognized with the 2014 alliance for financial inclusion’s Maya

Award. Governor Barry Whiteside chairs the national financial inclusion

taskforce, a private & public sector partnership that guides and monitors the development of greater financial

inclusion in Fiji.

16

P asserelles – n° 2

What role does the Reserve Bank of Fiji and its National Financial Inclusion Task Force play with respect to the conceptualization, implementation, as well as constant evaluation and adaptation of this strategy? What are the other most important partners and initiatives that play a role in this respect?

The conceptualization of Fiji’s financial in-clusion strategy materialized at the work-shop held in 2009. The Reserve Bank has the ability of “drawing power” to get the stakeholders to come together, and we have utilized this opportunity to help drive financial inclusion.

The role of the Reserve Bank and the Na-tional Financial Inclusion Task Force was to then appropriately document the stra-tegy and its implementation plan and moni-tor and evaluate its progress. An important part of our implementation is the collabora-tive and partnership model and structure of our National Financial Inclusion Taskforce, put in place to ensure success of the stra-tegy.

As mentioned earlier, the NFIT established and chaired by the Reserve Bank is the collaborative and consultative vehicle for fi-nancial inclusion initiatives in Fiji. Member-ship of the NFIT working groups includes representatives from all the other most im-portant private and public sector partners, civil society groups, development partners and NGOs, and the Reserve Bank provides the secretariat support. This collaborative approach has successfully seen the cost-sharing of most activities undertaken to raise awareness.

This model has worked well for us, and we are pleased to report that we have learnt and shared the lessons of the last few years with all of our neighbours in the Pacific, some of which have replicated this model.

An important part of our journey is coming under the greater network of the Alliance for Financial Inclusion (AFI). This interna-tional network has enabled us to share information and learn from our peers not only at a regional level but globally as well. The continuous engagement and learnings nationally and internationally has brought us this far in our financial inclusion journey and must continue.

What is the specific situation of Fiji in terms of financial inclusion today, and what are the most important opportunities and challenges for the future?

Some of our major achievements to date include:

- Achieving the initial target set in early 2010 of providing a financial service to 150,000 unbanked Fijians by 2014;

- Integration of financial education (FineD Program) into the school curriculum of all schools in Fiji from class one to six from 2013 (this impacted 907 scho-ols and approximately 197,000 school children);

- Implementation of a national financial literacy strategy;

- Deployment and decentralization of banking services outside of the main urban centers;

- extension of financial services through agent banking and mobile banking;

- Increase in the opening of new bank accounts and access to other types of financial services between 2010 and 2014; this also includes G2P payments (government-to-person payments, in-cluding social welfare) direct to recipient accounts. Prior to this, such recipients did not have bank accounts;

- Implementation of diagnostic surveys to provide baseline data on the financial competencies of low income house-holds and completion of a national de-mand side survey;

- Diagnostic studies completed to pro-vide a market-based assessment for challenges and opportunities for micro-finance, microinsurance and mobile money in Fiji; and

- Collation of data and development of financial inclusion indicators and geo-spatial mapping of financial access points across Fiji.

Whilst there have been some achieve-ments in the past few years, much more re-mains to be done to promote and facilitate financial inclusion in Fiji. Some challenges and opportunities for further improvement and focus are around access and use of financial products and services.

- The great geographical spread, with is-lands scattered over vast distances, has contributed to high exclusion from any form of financial services and providing access remains a challenge;

- Increased participation of women, youth and MSMes (micro, small and medium enterprises) in formal financial services are opportunities to be explored;

- Increased means of improving the effi-ciency and cost-effectiveness of remit-tance services are also opportunities to be worked on, considering that inward remittances are an important contributor to our economy;

17

Regulation for Innovation in Microfinance

- Developing inclusive insurance to ca-ter for the low-income segment is an ongoing challenge although we do see some light on this horizon; and

- Moving further in the area of digital fi-nancial services for wider outreach and reduced costs will be important in over-coming the geographical challenges we face.

Why does the National Strategy for Financial Inclusion in Fiji support mobile Money? What vision of mobile money for financial inclusion stands behind this? During the November 2009 National Mi-crofinance Workshop, the participants had noted that the provision of financial ser-vices to the poor and lower income earn-ers, to some extent, are provided by mi-crofinance institutions and other financial services providers in Fiji, but that this has mostly been done at a financial loss and with limited outreach. The Workshop par-ticipants agreed that new technologies and electronic banking products, particularly linked to telecommunications, offer an op-portunity to expand services in a more cost effective manner.

Mobile money is envisioned to provide a more accessible, cheaper and convenient first step into the formal financial system for the unbanked. With the provision of mobile wallets, unbanked customers, par-ticularly those in rural and maritime areas, can receive “micro transfers” from families much more conveniently. As usage in-creases and awareness and competencies for mobile money improve, mobile money can even become a means of micropay-ments for bill payments and other financial services such as savings payments into bank accounts, and other savings vehicles, insurance premiums, etc. In time, we envi-sage that it could be a means of payment for goods and services and also reduce the reliance on transporting physical cash to many remote islands and inaccessible parts of the interior of the main islands that make up Fiji.

How does mobile money work in Fiji as of today (structurally, technically; key players and roles; main products & services)?

In Fiji today, we have two mobile network operators (MNOs) – Vodafone and Digicel who both provide mobile money services to their customers through the MNO-led model. After successful pilot projects both MNOs had launched their respective ser-vices by June 2010.

Customers are now able to use these ser-vices to make deposits and withdrawals, make utility and other payments, send or receive money domestically as well as receive money from abroad. Total e-value in circulation at the end of Quarter 4, 2014 was 4.49 million USD and the total num-ber of registered customer accounts was 356,303. However, only 37,497 have been active in the last 90 day period.

Total inward remittances received through the mobile money channel for 2014 was 508,855 USD which was an increase of 37 percent from the preceding year. This compares to total remittances into Fiji of FJD 383.2 million.

The RBF continues to work very closely with both companies to increase the uptake and usage of mobile money and we have, with the assistance of the Fiji Intelligence Unit, developed a simplified customer iden-tification and verification process to meet CDO requirements under the Financial Transaction Reporting framework.

What are the most important elements of regulation, put in place for mobile money in Fiji? What are the most important challenges in that respect and how are they met?

The RBF Act specifies that one of the prin-ciple purposes of the Reserve Bank is to promote a sound financial structure. This provision permits the financial system regu-lator authority over all payment services including mobile money financial services. Under this mandate, the Reserve Bank has the power to designate and oversight payments systems through the Reserve Bank (Payment and Settlement Systems Oversight) Regulations 2004. The current framework allows for off-site monitoring and on-site examination. To date off-site

monitoring has been “light touch”, and we have just recently completed our first on-site examination. We intend to build our capacity in this area.

One of the main elements put in place in Fiji was the issue of conditions of approval to the MNOs in 2010, which, besides re-porting requirements on the coverage and location of services and the requirement for interoperability, included the requirements for the safety and protection of customers in particular the governance of customers’ deposits and safety of technology infra-structure. One key condition was the es-tablishment of a Trust Account in a licensed commercial bank, prior to the launch, which would provide for the backing of all e-money in circulation for mobile money customers. In July 2014, the Reserve Bank, in collabo-ration with the Pacific Financial Inclusion Program (PFIP), further strengthened the protection of the funds in the Trust Account and developed the Mobile Money Issuer Trust Deed that was signed by both the MNOs and the Reserve Bank on behalf of the their customers. This Deed would en-sure safety of customer deposits by estab-lishing the rules of governance kept in the Trust Account.

While the MNOs have easily met the regu-latory requirements set by the Reserve Bank, in particular for the Trust Account, one of the most important challenges is the interoperability with bank accounts. To date, for various reasons, banks have not been willing to link their bank accounts to the mobile wallets. The Reserve Bank con-tinues to encourage the link but will need to improve its capability to work through the technical issues that hinder this develop-ment.

What role in terms of financial inclusion do you see for mobile financial service providers and traditional financial service providers in the next 10 to 15 years and how does this change the sector? How will regulation have to develop in order to follow the respective developments that you foresee?

In the next 10-15 years, we expect that the mobile financial service providers will play a bigger role in providing financial services to remote and inaccessible areas. With

18

P asserelles – n° 2

greater acceptance and uptake, we ex-pect that more products and services will be offered by the mobile financial service providers and expect more people in these areas to be using these services. We also envisage that mobile financial service pro-viders will be the “stepping stone” towards services provided by traditional financial service providers.

Traditional service providers like commer-cial banks will have their mobile banking solutions in place where their customers can access their bank accounts through their mobile phones to enable them to undertake bank transactions. In addition, we expect that traditional bank accounts will be linked to mobile wallets to allow payments to and from bank accounts and mobile wallets, thus we see mobile wallets playing a role in introducing unbanked peo-ple into the formal financial system and ulti-mately to bank accounts and other banking services.

For smaller traditional service providers in Fiji like microfinance institutions, finance companies, credit unions, cooperatives, etc. to remain sustainable and competi-tive they will need to adapt their services and leverage off the efficiencies of mobile technology. We expect that when this is achieved, we will have a good mix of vari-ous types of financial service providers in the country and a general improvement in the efficiencies in the financial sector. We anticipate that these smaller players will complement the services of banks, credit institutions and other traditional service providers, like insurance underwriters and players in the capital markets.

A regulatory environment that is based on proportionality will be put in place to enable the adoption of mobile financial services by traditional providers. To ensure that these services are delivered in a secure, re-sponsible and sustainable manner we will continue to work with our stakeholders in developing an enabling regulatory environ-ment. Some of the work is already under-way to enact new laws to cover Secured Transactions (on moveable assets), Na-tional Payment System and Microfinance Act, as well as the development of regula-tions to govern mobile money and inclusive insurance products to name a few.

In what way does the regulatory framework in Fiji consider client protection with respect to financial services? Is there anything in particular with respect to mobile financial services? And what evolution do you see in that respect?

The framework for regulation and supervi-sion in Fiji provides sufficient protection for customers of financial services within the current legislative environment. Fiji has a Consumer Credit Act 1999 (+ Amendments 2006) that provides protection to consu-mers of credit and hire purchases. In addi-tion, the Reserve Bank of Fiji, as regulator of the financial system under the Banking Act, has implemented a Banking Supervi-sion Policy on Complaints Management No. 13 in 2009 and Banking Supervision

Policy on Disclosure of Fees and Charges No. 8A&B for licensed financial institutions which are banks and credit institutions.

The Policy on Disclosures requires disclo-sure in pre-contractual agreements through a standard prescribed ‘key facts sheet’ that was introduced in 2013 to all licensed credit institutions, requirement for the cost and key conditions of financial services to be disclosed in branches, requirements for disclosure of minimum information in ad-vertisements, requirements that contracts must be in writing and requirement that monthly statements must be provided. To complement this, the Policy on Complaints Management establishes Complaints Man-agement Processes within Financial Insti-tutions to resolve complaints by consumers effectively and efficiently.

In terms of mobile money, there are a num-ber of conditions of approval that were given to the MNOs, clearly specifying that customers’ interests are protected, and the need for disclosures to safeguard custo-mers deposits, confidentiality of data and personal details etc. The Trust Deed instru-ment that has been jointly developed by the Reserve Bank and the MNOs provides further assurance on the pool of custo mers’ deposits that are held in trust by the Reserve Bank of Fiji on behalf of the customers.

«The RBF continues to work very closely with both [mobile network operators] to increase the uptake and usage of mobile money. »

19

Regulation for Innovation in Microfinance

Client Protection and Innovation –Hearing from the “Voice of the Client” in IndiaArticle written by Natalie Giggy, Data Insights Manager, Good World Solutions and Justina Wong, Senior Manager, Good World Solutions

As concerns about excess com-mercialization and other serious crises in the microfinance sector have emerged, a consensus has

been building about the importance of cli-ent protection. Stakeholders – from microfi-nance institutions (MFIs), to their investors and donors, to associations and non-gov-ernmental organizations – agree that client protection is necessary to the social mis-sion of microfinance and that microfinance institutions should treat clients fairly and re-spectfully while avoiding harmful practices.

Much progress has been made through the establishment of standards, like the Smart Campaign’s Client Protection Principles (CPPs).1 The primary goal of such standards is to focus attention on important areas that put the microfinance sector’s mission at risk, as well as to create a common lan-guage that facilitates commitment and ac-tion among practitioners. Furthermore, a secondary benefit is that these standards are not only good for clients, but also for MFIs and investors, operating on the as-sumption that client protection is good for business, increasing customer loyalty and retention while reducing operational risk. Indeed, a european Microfinance Platform study has found a positive relationship between client protection principles and financial returns.2

As part of the movement towards stronger client protection in the microfinance indus-try, standards such as the CPPs are the right place to start; they can and should be upheld no matter the country, borrower pro-file, and provider type. The principles are universal and aspirational, and therefore, flexible about how each principle should be implemented and how success is de-fined and measured. The result, however, is that because MFIs lack client-level data, it has proven difficult to apply and measure success against the very principles estab-lished to protect them.

natalie giggy

Justina Wong

Justina Wong is a Senior Manager at Good World Solutions, where

she is responsible for leading and managing all aspects of global programs and operations. She

was previously a Senior Manager at chemonics international, where

she designed and implemented international economic development

programs including the USAID Financial Sector Knowledge Sharing Project. Justina holds a Bachelor’s degree in government from Harvard

College and a Master’s degree in international economics from Johns

Hopkins University’s School of Advanced International Studies.

Natalie Giggy is a Data Insights Manager at Good World Solutions, where she manages survey design

and data analysis on tools that use technology to capture direct feedback from workers, farmers, artisans and consumers at the

bottom of the pyramid. Natalie holds a Bachelor’s degree in economics from UC Berkeley and a Master’s

degree in international affairs from UC San Diego.

1 Many other principles and standards related to client protection have been developed. In the UN Principles for Investors in Inclusive Finance, investors pledge to “treat […] their investees fairly, with clear and balanced contracts, and dispute resolution procedures”. The microfinance industry created and agreed on the Consultative Group to Assist the Poor (“CGAP”) Guide to Regulation and Supervision of Microfinance which include client protection. TrueLift is a global initiative to push for accountability in pro-poor development. MFTransparency is an NGO that promotes transparent pricing in the microfinance world by collecting interest rate data and publishing educational information about how interest rates work.

2 The study “Does good client protection impact financial performance?” demonstrated that most of the CPPs show a positive relationship either with return on assets (RoA) or return on equity (Roe). Two relevant findings to highlight are: good practices in transparency, collection practices, ethical staff behavior, complaints resolution, and privacy all coincide with better financial returns; and ethical staff behavior and collection practices are linked to higher financial returns, which means that treating clients respectfully may be good for an institution’s profitability. Further information under http://www.e-mfp.eu/sites/default/files/resources/ 2014/05/Brief_No_4_2014_web.pdf.

3 From the Working Group’s report on “Protecting New and Vulnerable Clients as Financial Inclusion Proceeds” in September 2013. Further information under http://www.centerforfinancialinclusion.org/fi2020/roadmap-to-inclusion/client-protection.

The Financial Inclusion 2020 Client Protec-tion Working Group, gathered by Accion’s Center for Financial Inclusion, noted a number of barriers to client protection, in-cluding: providers often see client protec-tion as a regulatory responsibility thus only needing to follow a “do no harm” commit-ment or fulfilling the letter of the law; regu-lations in establishing protection standards and enforcement are inadequate; and cli-ents’ voices are missing because they are rarely organized or represented in a way to allow their collective voice to be heard.3

20

P asserelles – n° 2

At the provider level, microfinance institu-tions particularly struggle to find ways to collect opinions and feedback from clients to assess their progress against the CPPs as well as other social performance mana-gement standards in a meaningful, timely, and effective way.4

To fill this gap, Hivos, MIX and Good World Solutions, together with its partners and sponsors, launched the Voice of the Client (VoC) pilot for direct client monitoring, us-ing mobile technology in Uttar Pradesh in India.5 The objective of the pilot was testing mobile technology to proactively reach cli-ents, offering them a channel to share their opinions on client protection principles re-lated to MFI products, services, and cus-tomer service. The scalability and cost ef-fectiveness of mobile technology has been applied to a number of financial services in developing countries, including payments, remittances, and mobile banking. Yet, we saw an untapped potential for mobile technology to enhance transparency and accountability in microfinance in support of the client protection principles. The pi-

lot collected nearly 6,000 surveys using three survey modes – an interactive voice response (“IVR”) platform, a live agent via a call center (“call center”), and in-person surveys administered by enumerators using smartphones (“in-person”).

This article aims to share information with the microfinance sector and development practitioners on how to use innovation to enhance current outreach to clients. The first part briefly reviews the key factors and drivers behind our pilot activity, including regulatory challenges in client protection concerning over-indebtedness, transpa-rency, fair and respectful treatment of clients, and grievance mechanisms, as well as current practices, limitations, and opportunities in collecting and analyzing data at the client level. In the second part, we share key findings based on survey data collected during the pilot and opera-tional lessons learned that will be applied to future field research.

Client Protection and Regulation We focus on the regulation of client protec-tion themes concerning over-indebtedness, transparency, fair and respectful treatment of clients, and grievance mechanisms, and particularly highlight the current regulatory situation in India as it relates to our pilot and to collecting data at the client level. We chose to specifically look at the Smart Campaign’s CPPs since they are univer-sally accepted client protection principles.

The legal and regulatory landscape con-cerning client protection in developing countries is weak and underdeveloped;

according to a survey conducted by ernst & Young and the Platform for Inclusive Fi-nance, only half of the countries in its re-search scope are implementing some kind of microfinance law, and not all include pro-visions on client protection.6 Furthermore, where regulation does exist, enforcement remains a major challenge. Two general types of enforcement exist: government agency enforcement enacted through state and central legislation; or, industry self-regulation where institutions agree to a voluntary code of conduct (also referred to as a code of ethics or a code of practice), surveillance and monitoring, and enforce-ment of such code.

each approach has its advantages and dis-advantages, which have been widely de-bated.7 State enforcement has the tenden-cy to become cumbersome, for example, India’s regulation on consumer protection varies across the wide array of classifica-tion for providers (see Table 1). effective enforcement is oftentimes not possible be-cause of information gaps; currently, most available information on client protection is self-reported by MFIs who face various constraints in measuring their performance in these areas or are evaluated by third-party, external assessors who tend to have the time, access, or funds to collect direct client feedback.

Preventing over-indebtedness among mi-crofinance clients is critical, both as it re-lates to the pro-poor mission of the sector and the sustainability of individual MFIs; over-indebtedness can result in loan de-linquency, and have income effects that adversely impact health, nutrition and edu-cation. The Smart Campaign’s principle on the prevention of over-indebtedness states that, “[p]roviders will take adequate care in

4 We have found this to be the case in our work with MFI partners in India, Peru, and Colombia.

5 The partners and sponsors of the project include: The Smart Campaign, Michael & Susan Dell Foundation, Appui au Développement Autonome (ADA) (www.ada-microfinance.org), Triple Jump, and Deutsche Bank. Hivos (www.hivos.org) and MIX (www.themix.org) selected Good World Solutions (www.goodworldsolutions.org), a nonprofit social enterprise, as the technical partner responsible for client data collection with use of innovative ICT. Good World Solutions’ Laborlink is a mobile solution that translates worker voices into actionable analytics. This enables companies to make data-driven decisions that improve worker well-being within their supply chains. Since 2010, Laborlink has reached more than 300,000 workers in the supply chains of major apparel and electronics companies in 16 countries. Transparency, fair treatment, and access to grievance mechanisms are all principles we work to uphold, so it was a natural fit to extend our mobile technology tools beyond factory walls to assess whether these same principles are being upheld in microfinance.

6 ernst & Young’s 2015 report on “Client protection in microfinance: the current state of law and regulation” is accessible at http://www.inclusivefinanceplatform.nl/documents/2014%20report%20 microfinance%20client%20protection_final.pdf

7 Further information under http://www.microsave.net/files/pdf/Principles_and_Practice_ Myths_of_Regulation_and_Supervision.pdf. See also Porteous, David and Brigit Helms, CGAP Focus Note, No. 27, “Protecting Microfinance Borrowers.” May 2005.

Table 1: India’s Regulatory Landscape. Information collected from CGAP

Microfinance Provider Regulator

Commercial banks providing microfinance loans

Regulated by the Reserve Bank of India (RBI) and supervised by the National Bank for Agriculture and Rural Development (NABARD)

Regional rural banks (RRB) Regulated by the Reserve Bank of India (RBI) and supervised by the National Bank for Agriculture and Rural Development (NABARD)

Self-help groups (SHG) Regulated by the NABARD

Cooperative Societies Regulated by the state-appointed Registrar of Cooperative Societies (RCS) and state government (with NABARD conducting supervision and inspections)

Microfinance NGO (registered as societies, trusts or Section 25 companies)

Self-regulatory organizations including Sa-Dhan and the Micro Finance India Network (MFIN)