planning commission, indian railways & world...

TRANSCRIPT

Planning Commission, Indian Railways & World Bank

Joint Workshop on

Generating & Implementing Visionary Railway Strategies

A Vision for Financing: PPPs in Railways

New Delhi, March 26, 2009

2

IFC Member of the World Bank Group

Multilateral Investment Guarantee Agency, 1988 Provides guarantees to foreign investors against non-commercial risk

IFC is owned by its 179 member countries

International Finance Corporation, 1956Invests and advises to promote sustainable private sector development

International Development Association, 1960 Provides concessional loans to Governments of the poorest developing countries

International Centre for Settlement of Investment Disputes, 1966

International Bank for Reconstruction and Development, 1945 Lends to Governments of middle-income developing countries

3

IFC Investment & Advisory Services

IFC also provides technical assistance and advice to Governments and businesses

Financing Advisory ServicesIFC is the world’s largest multilateral provider of financing for private enterprises with over US$26 billion in outstanding investment commitments

LoansEquity

Guarantees

Environment & Social Sustainability

Access to Finance

Business Environment

Public-Private Partnerships

Enterprise Assistance

4

IFC Infrastructure AdvisoryWhat is a PPP?

Possible PPP Models

Management Contracts

Service ContractsOutsourcing

AffermageEnhanced Affermage

Concession Contracts

BOT, BTO, BOO, DBO

Investor's Risk

State's Risk

Technical Assistance

Lease Contracts

Full Divestiture

5

Major Forms of PPPs for New Rail Projects

Finance & Build Rail Line

Operate & Maintain Rail Line

Finance & Maintain Trains

Operate Train Services

Train Availability Contract

Public Public PrivatePublic/Private

(Hire payments to private)

Train Operating Concession

Public Public PrivatePublic/Private

(Hire payments to private)

Infrastructure Build Concession

PrivatePublic/Private

(Lease Payments to private)

Public/Private Public/Private

Infrastructure “BOT” Concession

Private PrivatePublic/Private

(Access charges paid to private)

Public/Private

Integrated Concession

Private Private Private Private

The defined assets are transfered to public sector at end of concessionin each of the cases

Source: www.worldbank.org/transport

6

Typical Challenges for Governments to Revitalize/Maintain Railway Market Share

• Competition esp. from trucking sector

• Mobilizing funding for heavy investments

• Technical complexities

• Keeping level playing field

• Politically economy of sector

7

Indian Railways : Future Strategies

• Indian Railways turnaround story from 2001-2007 remarkable

• Limited utility of that growth model for long-term and sustained growth—need for investment in infrastructure expansion, rationalization of services & infusion of managerial efficiencies

• Narrowing fiscal space has vacated greater room for private-sector participation

• PPP experience in Railways offer many lessons & could play a role in Indian Railways growth strategy

• Globally Railways transforming due to competitive pressures from other modes of transport & declining revenues

• Segmentation of assets & services into ‘core’ and non-core’ important

• Pricing strategy—flexibility needed for both passenger and freight traffic

8

Indian Railways : Salience of PPPs to Maintain Growth Momentum

As per Eleventh FYP 2007-2012:

Salience of PPPs

Of the more than $50 billion funding requirement for expansion & modernization of the railway infrastructure $15 bn (30%) is expected to be raised from non-budgetary resources

Possible areas for PPP

• World Class Railway Stations (22 Stations in major cities)

• SPVs for Rolling stock Units (Fill supply gap in locomotives & coaches)

• Operation of Container Trains (14 contracts allowed already)

• Multi-modal Logistics Parks (12 locations identified)

• Agri-retail Chain • Commercial Utilization of Surplus Land• Dedicated Freight Corridor Projects (Approx. $5.2 bn reqd.)

• High-speed Rail Corridors• Hospitality, Tourism and Catering (BOT models)

9

PPP Trends in Developing Countries

Total PPP Projects by Sector 1990-2007

Energy44%

Water and sewerage

23%Transport

27%

Telecom6%

Total Projects: 1225

o/w Energy: 545

Telecom: 68

Transport: 330

Water & Sewage: 282

Total Investment ($ mn) by Sector 1990-2007

Water and Sewerage10%

Transport

26%

Energy

36%

Telecom

28%

Total Investment: $ mn 276,184

o/w Energy: $ mn 100,676

Telecom: $ mn 77,092

Transport: $ mn 71,191

Water & Sewerage: $ mn 27,225

Source: World Bank PPI Databse

10

PPP Trends in Developing Countries: Transport Sector

Global Transport PPP 1990-2007: Number of Projects

Railroads100(9%)

Airports128

(12%)

Seaports325

(30%)

Roads546

(49%)

Global Transport PPP 1990-2007: Investment Volume $ bn

Roads100

(47%)

Seaports42

(20%)Airports31

(15%)

Railroads39

(18%)

Source: World Bank PPI Databse

11

India PPP Trends : Infrastructure Sector 1990-2007

97

34

6

3

133

24

9

34

43

5

0.218

10

4

0.255

Energy

Telecom

Airports

Railroads

Roads

Seaports

Water & Sewerage

Number of Projects Investment Vol. $ billion

Source: World Bank PPI Databse

12

IFC Infrastructure Advisory: Kenya-Uganda Railways Joint Concession

•The Kenya-Uganda Railways Joint Concession, designed and implemented by the two governments with advice from IFC, became operational on November 1, 2006

•It was designed to avoid the shortcomings of previous concessions and to maximize the long-term benefits for all stakeholders

•The lessons of the previous concessions were taken into account, and other features added that have made the KR-UR concession an attractive and promising one.

13

Kenya-Uganda Railway Joint Concession: Full Privatization

Key IFC PPP lessons Pre-requisites for rail concessioning•Incentivize investment by concessionaire

•Minimize public funding of concession

•Allow rationalization – exit flexibility for investors

•Find innovative ways to maintain passenger services

•Minimize inability to remove concessionaire if not performing

•Make strong effort to recognize & optimize social objectives

•Build in safety and environmental regulation into the concession contract

•Help ensure increase in allocative efficiency

•Amendment of the Railways Act or legislation

•Safety and environment regulators

•Retrenchment of surplus staff

•Adequate funding of the pension Fund

•Liquidating past environmental liabilities

•Disposal of unwanted assets

•Containing track encroachments

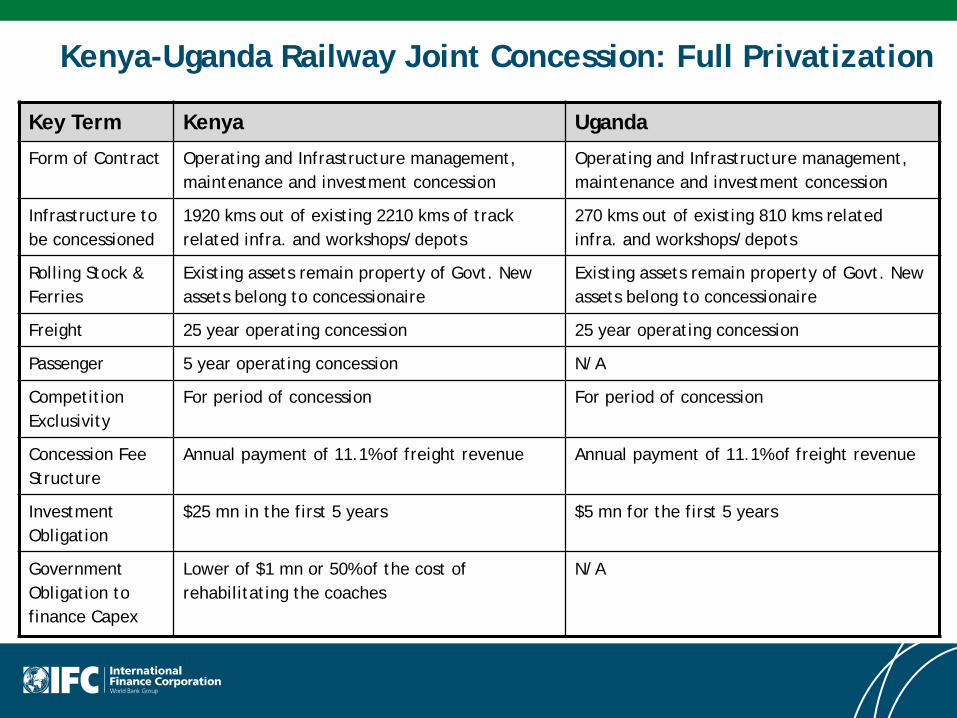

Kenya-Uganda Railway Joint Concession: Full Privatization

Key Term Kenya Uganda

Form of Contract Operating and Infrastructure management, maintenance and investment concession

Operating and Infrastructure management, maintenance and investment concession

Infrastructure to be concessioned

1920 kms out of existing 2210 kms of track related infra. and workshops/depots

270 kms out of existing 810 kms related infra. and workshops/depots

Rolling Stock & Ferries

Existing assets remain property of Govt. New assets belong to concessionaire

Existing assets remain property of Govt. New assets belong to concessionaire

Freight 25 year operating concession 25 year operating concession

Passenger 5 year operating concession N/A

Competition Exclusivity

For period of concession For period of concession

Concession Fee Structure

Annual payment of 11.1% of freight revenue Annual payment of 11.1% of freight revenue

Investment Obligation

$25 mn in the first 5 years $5 mn for the first 5 years

Government Obligation to finance Capex

Lower of $1 mn or 50% of the cost of rehabilitating the coaches

N/A

15

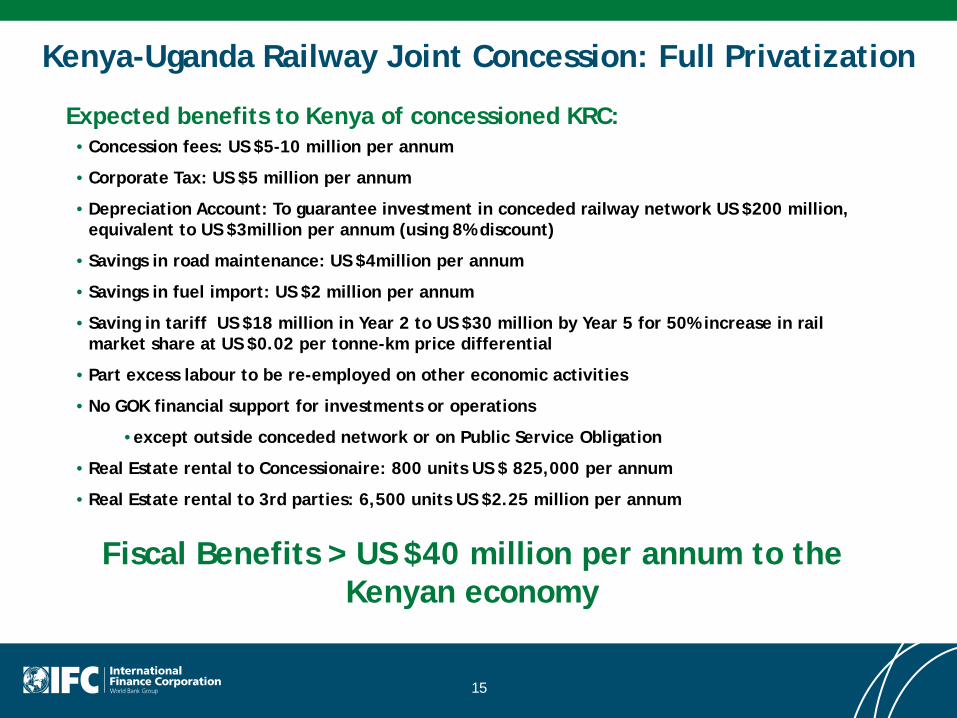

Kenya-Uganda Railway Joint Concession: Full Privatization

Expected benefits to Kenya of concessioned KRC: • Concession fees: US $5-10 million per annum

• Corporate Tax: US $5 million per annum

• Depreciation Account: To guarantee investment in conceded railway network US $200 million, equivalent to US $3million per annum (using 8% discount)

• Savings in road maintenance: US $4million per annum

• Savings in fuel import: US $2 million per annum

• Saving in tariff US $18 million in Year 2 to US $30 million by Year 5 for 50% increase in rail market share at US $0.02 per tonne-km price differential

• Part excess labour to be re-employed on other economic activities

• No GOK financial support for investments or operations

•except outside conceded network or on Public Service Obligation

• Real Estate rental to Concessionaire: 800 units US $ 825,000 per annum

• Real Estate rental to 3rd parties: 6,500 units US $2.25 million per annum

Fiscal Benefits > US $40 million per annum to the Kenyan economy

16

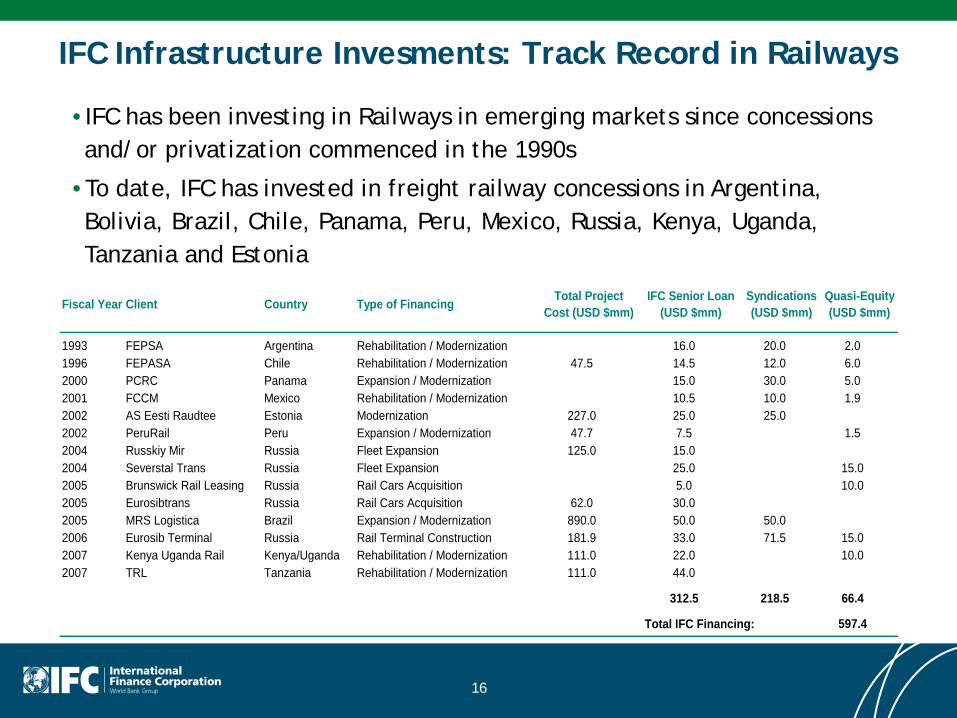

IFC Infrastructure Invesments: Track Record in Railways

•IFC has been investing in Railways in emerging markets since concessions and/or privatization commenced in the 1990s

•To date, IFC has invested in freight railway concessions in Argentina, Bolivia, Brazil, Chile, Panama, Peru, Mexico, Russia, Kenya, Uganda, Tanzania and Estonia

Fiscal Year Client Country Type of Financing Total Project Cost (USD $mm)

IFC Senior Loan (USD $mm)

Syndications (USD $mm)

Quasi-Equity (USD $mm)

1993 FEPSA Argentina Rehabilitation / Modernization 16.0 20.0 2.01996 FEPASA Chile Rehabilitation / Modernization 47.5 14.5 12.0 6.02000 PCRC Panama Expansion / Modernization 15.0 30.0 5.02001 FCCM Mexico Rehabilitation / Modernization 10.5 10.0 1.92002 AS Eesti Raudtee Estonia Modernization 227.0 25.0 25.0 2002 PeruRail Peru Expansion / Modernization 47.7 7.5 1.52004 Russkiy Mir Russia Fleet Expansion 125.0 15.0 2004 Severstal Trans Russia Fleet Expansion 25.0 15.02005 Brunswick Rail Leasing Russia Rail Cars Acquisition 5.0 10.02005 Eurosibtrans Russia Rail Cars Acquisition 62.0 30.0 2005 MRS Logistica Brazil Expansion / Modernization 890.0 50.0 50.0 2006 Eurosib Terminal Russia Rail Terminal Construction 181.9 33.0 71.5 15.02007 Kenya Uganda Rail Kenya/Uganda Rehabilitation / Modernization 111.0 22.0 10.02007 TRL Tanzania Rehabilitation / Modernization 111.0 44.0

312.5 218.5 66.4

Total IFC Financing: 597.4

17

IFC Infrastructure Investment: Tanzania Railway (2007)Description Sponsor Project Cost

• Rehabilitate, develop, and operate the approximately 2700km railway network under a 20 year concession

• RITES (51%)

• Government of Tanzania (49%)

• Project Cost = $111mm

• Equity = $34mm

• World Bank IDA Credit = $33mm

• IFC A Loan = $44mm

Development Impact: • Enhance safety, reliability, and efficiency

of the railway system• Improve transportation of goods and

people, particularly into the poorer and more central regions from the coast

• Provide a connection to neighboring six countries, some of which are landlocked

18

IFC Infrastructure Investment: MRS Logistica (Brazil - 2005)

Description Principal Sponsors Project Cost

• Increase company’s freight handling capacity by 60-80% through way expansion, track reconfigurations, signaling improvements, and rolling stock acquisitions/upgrades

• CSN (32%)

• MBR (32%)

• CVRD (10%)

• Usiminas (10%)

• Project Cost = $890mm

• IFC A Loan = $50mm

• IFC B Loan - $50mm

Development Impact: • Enhance safety, reliability, and efficiency

of the railway system• Increase freight cargo volumes and

support the growth of Brazil’s export market

• Reduce transport cost required to access domestic and international markets

19

IFC Infrastructure Invesment: Peru Rail (2002)

Description Principal Sponsors Project Cost

• Upgrade and rehabilitate the railway network

• Rehabilitate rolling stock

• Purchase communication equipment

• Orient-Express Hotels Ltd. (50%)

• Peruval Corp. S.A. (50%)

• Project Cost = $47.7mm

• IFC A Loan = $7.5mm

• IFC C Loan - $1.5mm

Development Impact: • Transport large amounts of minerals,

petroleum derivatives, and other bulk commodities that constitute a substantial part of total exports

• Help in the strategic regional development of the ports and in the attraction larger tourism inflows to the country

20

Thank You!

International Finance CorporationWorld Bank Group

South AsiaInfrastructure Advisory Services

50 M, ShantipathGate No. 3, Niti Marg, Chanakyapuri

New Delhi – 110021, INDIATel: (+91 11) 4111 1000

Fax: (+91 11) 4111 1001/2www.ifc.org