plan. save. retire. - florida deferred compensation · pdf file · 2014-06-27plan....

TRANSCRIPT

1.

Plan. Save. Retire.with the State of Florida Deferred Compensation

200 EA

ST G

AIN

ES ST

RE

ET

TA

LLAH

ASSE

E, FLO

RID

A 32399-0323

RETIREMENT IS A LOT OF FUN—IF YOU PLAN AND SAVE

Golfing on a weekday. Snorkeling during the morning commute. Beachside lounging for hours upon hours. Winingand dining into the sunset. And at the end of the day, work has not once crossed your mind. Your vacation never ends if you plan and save today.Planning your future can help you enjoy all the pleasures of retirement. It’s easy: Just follow the tips below and you’ll be on your way to a stress-free destination.

Do your work today and haveyour fun tomorrowParticipating in the Deferred Compensation Plan can help you add to your retirement nest egg with savings that supplement your state retirement income and Social Security benefits. In addition to flexible contribution limits and tax-saving features, you can take advantage of a variety of investment options to give your money the opportunity to grow. The Plan provides investment choices that are monitored by the State of Florida and are required to meet performance standards. Introduced in 1982, the state of Florida Deferred Compensation Plan services more than 82,000 participant accounts. Currently, about 48% of your fellow employees have an account with the plan.

To find out more about the Plan, read on. Once you’ve taken a look at a few of the Plan’s benefits, we hope you’ll request enrollment materials and join the Plan. Enrollment is quick and easy, and the Plan is one of the smartest ways to help you reach an enjoyable retirement.

*The State administers the Plan in accordance with Internal Revenue Code 457 (IRC 457) and Florida Administrative Code Section 69C-6 (FAC 69C-6).

Five tips to enjoying your destinationLearn how to save wisely and enjoy the destination you’ve been dreaming about.

Expect to spend 20 to 30 years or longer in retirement.

Don’t count on your State pension or Social Security to provide 100% of your financial needs.

Take more responsibility for your future financial security. It may be up to you to provide the bulk of your retirement income.

Set aside additional funds for health care costs and other necessary expenses in retirement. Remember, group insurance rates will no longer be available to you after you retire.

Keep your investment expectations realistic and diversify your holdings within your account.

With these tips in mind, take a look at how the Plan can help ensure a smooth ride.

4.

Reaching retirement: Get an early startIf you want to reach your retirement income goals in time, the sooner you start saving, the better. That’s because you’ll give your money a chance to make money, which is to say it can “compound” in value. And the longer you invest, the more you can earn through compounding. To see how time and compounding can work, consider the following examples:

Two investors, John and Linda, each invest through their employer’s deferred compensation program. Linda starts saving at age 35. John, who is the same age, does not start until he is 45. Both save $200 monthly and receive a 7% annual rate of return. The graph above left shows how much each of them will have accumulated when they reach age 65. The graphs above right show how much Linda and John will have at age 65 by saving $25 a month and $600 a month.*

*The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan. Your results will vary.

3.

2.

5.

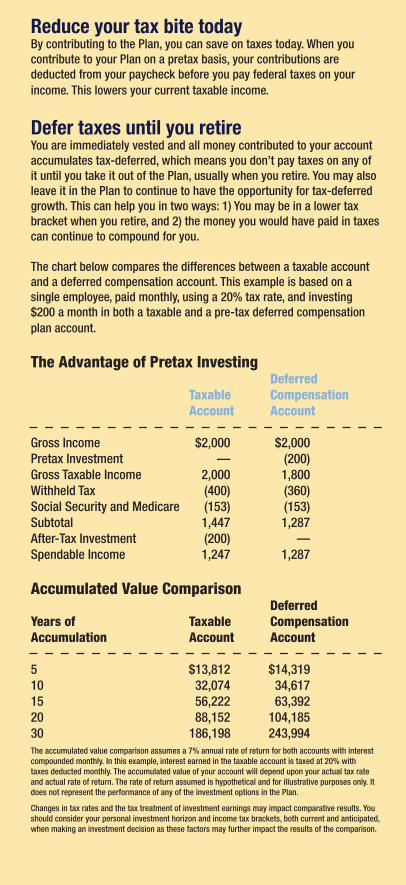

Reduce your tax bite todayBy contributing to the Plan, you can save on taxes today. When youcontribute to your Plan on a pretax basis, your contributions are deducted from your paycheck before you pay federal taxes on your income. This lowers your current taxable income.

Defer taxes until you retireYou are immediately vested and all money contributed to your account accumulates tax-deferred, which means you don’t pay taxes on any of it until you take it out of the Plan, usually when you retire. You may also leave it in the Plan to continue to have the opportunity for tax-deferred growth. This can help you in two ways: 1) You may be in a lower tax bracket when you retire, and 2) the money you would have paid in taxes can continue to compound for you.

The chart below compares the differences between a taxable account and a deferred compensation account. This example is based on a single employee, paid monthly, using a 20% tax rate, and investing $200 a month in both a taxable and a pre-tax deferred compensation plan account.

The Advantage of Pretax Investing Deferred Taxable Compensation Account Account

Gross Income $2,000 $2,000Pretax Investment — (200)Gross Taxable Income 2,000 1,800Withheld Tax (400) (360)Social Security and Medicare (153) (153)Subtotal 1,447 1,287After-Tax Investment (200) —Spendable Income 1,247 1,287

Accumulated Value Comparison DeferredYears of Taxable Compensation Accumulation Account Account

5 $13,812 $14,31910 32,074 34,61715 56,222 63,39220 88,152 104,18530 186,198 243,994The accumulated value comparison assumes a 7% annual rate of return for both accounts with interest compounded monthly. In this example, interest earned in the taxable account is taxed at 20% with taxes deducted monthly. The accumulated value of your account will depend upon your actual tax rate and actual rate of return. The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan.

Changes in tax rates and the tax treatment of investment earnings may impact comparative results. You should consider your personal investment horizon and income tax brackets, both current and anticipated, when making an investment decision as these factors may further impact the results of the comparison.

Destination: funNow that you’ve read a little about the State of Florida Deferred Compensation Plan, it’s time to work toward making your dreams come true. The fun awaits you, so take advantage and plan and save today!

• Receive additional income during retirement.• Avoid paying substantial amounts of federal income taxes.• Put your money to work for you, so you can have fun later.

The time to enroll is todayTo begin saving and investing for your future, request enrollmentmaterials by calling one or more of the companies listed below. You can get started with $20 a month. Each company offers a wide varietyof investment options at a low cost. Your investment company will assist you in completing all the necessary documents. The Plan also provides a selection of products that offer guaranteed returns and safety of principle.

Investment Provider Companies

VALIC 888-568-2542 www.valic.com/floridadcp

Great-West Retirement Services 800-444-9412 www.florida457.com

ING 800-282-6295 www.ingretirementplans.com/custom/fl457

Nationwide Retirement Solutions 800-949-4457 www.nrsflorida.com

T. Rowe Price Group 888-457-5770 rps.troweprice.com/florida

Self-Directed Brokerage Window

Charles Schwab* 888-393-7272 www.schwab.com *Enrollment available through Nationwide.

State of Florida Deferred Compensation Plan is administered by:State Chief Financial OfficerDepartment of Financial ServicesBureau of Deferred Compensation200 East Gaines StreetTallahassee, Florida 32399-0346

Phone: 850-413-3162Toll-free: 877-299-8002Office hours: M-F, 8-5 EST

www.MyFloridaDeferredComp.com

I am interested in receiving the Deferred Compensation Plan information package, which contains the following: • Performance Report, a comparison of the various products, fees and investment items.

• Commonly Asked Questions With Answers about the Deferred Compensation Plan

Tell me more

Check this box if you w

ould like to be added to the Performance Report m

ailing list.

Name

Address

City

State

Zip

Telephone (home)

Telephone (work)

Department/Agency

Department/Agency Address

City

State

Zip

State o

f Flo

rida m

oney w

as not used

to p

rod

uce or m

ail these materials.

$25/Month, 7% Annual Return Compunded Monthly

$600/Month, 7% Annual Return Compunded Monthly

Financial Future Broch.indd 17/21/2011 9:50:15 AM

1.

Plan. Save. Retire.with the State of Florida Deferred Compensation

200

EA

ST G

AIN

ES

STR

EE

TT

ALL

AH

ASS

EE

, FLO

RID

A 3

2399

-032

3

RETIREMENT IS A LOT OF FUN—IF YOU PLAN AND SAVE

Golfing on a weekday. Snorkeling during the morning commute. Beachside lounging for hours upon hours. Winingand dining into the sunset. And at the end of the day, work has not once crossed your mind. Your vacation never ends if you plan and save today.Planning your future can help you enjoy all the pleasures of retirement. It’s easy: Just follow the tips below and you’ll be on your way to a stress-free destination.

Do your work today and haveyour fun tomorrowParticipating in the Deferred Compensation Plan can help you add to your retirement nest egg with savings that supplement your state retirement income and Social Security benefits. In addition to flexible contribution limits and tax-saving features, you can take advantage of a variety of investment options to give your money the opportunity to grow. The Plan provides investment choices that are monitored by the State of Florida and are required to meet performance standards. Introduced in 1982, the state of Florida Deferred Compensation Plan services more than 82,000 participant accounts. Currently, about 48% of your fellow employees have an account with the plan.

To find out more about the Plan, read on. Once you’ve taken a look at a few of the Plan’s benefits, we hope you’ll request enrollment materials and join the Plan. Enrollment is quick and easy, and the Plan is one of the smartest ways to help you reach an enjoyable retirement.

*The State administers the Plan in accordance with Internal Revenue Code 457 (IRC 457) and Florida Administrative Code Section 69C-6 (FAC 69C-6).

Five tips to enjoying your destinationLearn how to save wisely and enjoy the destination you’ve been dreaming about.

Expect to spend 20 to 30 years or longer in retirement.

Don’t count on your State pension or Social Security to provide 100% of your financial needs.

Take more responsibility for your future financial security. It may be up to you to provide the bulk of your retirement income.

Set aside additional funds for health care costs and other necessary expenses in retirement. Remember, group insurance rates will no longer be available to you after you retire.

Keep your investment expectations realistic and diversify your holdings within your account.

With these tips in mind, take a look at how the Plan can help ensure a smooth ride.

4.

Reaching retirement: Get an early startIf you want to reach your retirement income goals in time, the sooner you start saving, the better. That’s because you’ll give your money a chance to make money, which is to say it can “compound” in value. And the longer you invest, the more you can earn through compounding. To see how time and compounding can work, consider the following examples:

Two investors, John and Linda, each invest through their employer’s deferred compensation program. Linda starts saving at age 35. John, who is the same age, does not start until he is 45. Both save $200 monthly and receive a 7% annual rate of return. The graph above left shows how much each of them will have accumulated when they reach age 65. The graphs above right show how much Linda and John will have at age 65 by saving $25 a month and $600 a month.*

*The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan. Your results will vary.

3.

2.

5.

Reduce your tax bite todayBy contributing to the Plan, you can save on taxes today. When youcontribute to your Plan on a pretax basis, your contributions are deducted from your paycheck before you pay federal taxes on your income. This lowers your current taxable income.

Defer taxes until you retireYou are immediately vested and all money contributed to your account accumulates tax-deferred, which means you don’t pay taxes on any of it until you take it out of the Plan, usually when you retire. You may also leave it in the Plan to continue to have the opportunity for tax-deferred growth. This can help you in two ways: 1) You may be in a lower tax bracket when you retire, and 2) the money you would have paid in taxes can continue to compound for you.

The chart below compares the differences between a taxable account and a deferred compensation account. This example is based on a single employee, paid monthly, using a 20% tax rate, and investing $200 a month in both a taxable and a pre-tax deferred compensation plan account.

The Advantage of Pretax Investing Deferred Taxable Compensation Account Account

Gross Income $2,000 $2,000Pretax Investment — (200)Gross Taxable Income 2,000 1,800Withheld Tax (400) (360)Social Security and Medicare (153) (153)Subtotal 1,447 1,287After-Tax Investment (200) —Spendable Income 1,247 1,287

Accumulated Value Comparison DeferredYears of Taxable Compensation Accumulation Account Account

5 $13,812 $14,31910 32,074 34,61715 56,222 63,39220 88,152 104,18530 186,198 243,994The accumulated value comparison assumes a 7% annual rate of return for both accounts with interest compounded monthly. In this example, interest earned in the taxable account is taxed at 20% with taxes deducted monthly. The accumulated value of your account will depend upon your actual tax rate and actual rate of return. The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan.

Changes in tax rates and the tax treatment of investment earnings may impact comparative results. You should consider your personal investment horizon and income tax brackets, both current and anticipated, when making an investment decision as these factors may further impact the results of the comparison.

Destination: funNow that you’ve read a little about the State of Florida Deferred Compensation Plan, it’s time to work toward making your dreams come true. The fun awaits you, so take advantage and plan and save today!

• Receive additional income during retirement.• Avoid paying substantial amounts of federal income taxes.• Put your money to work for you, so you can have fun later.

The time to enroll is todayTo begin saving and investing for your future, request enrollmentmaterials by calling one or more of the companies listed below. You can get started with $20 a month. Each company offers a wide varietyof investment options at a low cost. Your investment company will assist you in completing all the necessary documents. The Plan also provides a selection of products that offer guaranteed returns and safety of principle.

Investment Provider Companies

VALIC 888-568-2542 www.valic.com/floridadcp

Great-West Retirement Services 800-444-9412 www.florida457.com

ING 800-282-6295 www.ingretirementplans.com/custom/fl457

Nationwide Retirement Solutions 800-949-4457 www.nrsflorida.com

T. Rowe Price Group 888-457-5770 rps.troweprice.com/florida

Self-Directed Brokerage Window

Charles Schwab* 888-393-7272 www.schwab.com *Enrollment available through Nationwide.

State of Florida Deferred Compensation Plan is administered by:State Chief Financial OfficerDepartment of Financial ServicesBureau of Deferred Compensation200 East Gaines StreetTallahassee, Florida 32399-0346

Phone: 850-413-3162Toll-free: 877-299-8002Office hours: M-F, 8-5 EST

www.MyFloridaDeferredComp.com

I am interested in receiving the Deferred Compensation Plan information package, which contains the following: • Performance Report, a comparison of the various products, fees and investment items.

• Commonly Asked Questions With Answers about the Deferred Compensation Plan

Tell me more

Ch

eck

this

box

if y

ou w

ould

like

to b

e ad

ded

to th

e Pe

rfor

man

ce R

epor

t mai

ling

list.

Nam

e

Addr

ess

City

Stat

e

Zip

Tele

phon

e (h

ome)

Tele

phon

e (w

ork)

Depa

rtm

ent/A

genc

y

Depa

rtm

ent/A

genc

y Ad

dres

s

City

Stat

e

Zip

Sta

te o

f F

lori

da

mo

ney

was

no

t us

ed t

o p

rod

uce

or

mai

l the

se m

ater

ials

.

$25/Month, 7% Annual Return Compunded Monthly

$600/Month, 7% Annual Return Compunded Monthly

Financial Future Broch.indd 1 7/21/2011 9:50:15 AM

1.

Plan. Save. Retire.with the State of Florida Deferred Compensation

200

EA

ST G

AIN

ES

STR

EE

TT

ALL

AH

ASS

EE

, FLO

RID

A 3

2399

-032

3

RETIREMENT IS A LOT OF FUN—IF YOU PLAN AND SAVE

Golfing on a weekday. Snorkeling during the morning commute. Beachside lounging for hours upon hours. Winingand dining into the sunset. And at the end of the day, work has not once crossed your mind. Your vacation never ends if you plan and save today.Planning your future can help you enjoy all the pleasures of retirement. It’s easy: Just follow the tips below and you’ll be on your way to a stress-free destination.

Do your work today and haveyour fun tomorrowParticipating in the Deferred Compensation Plan can help you add to your retirement nest egg with savings that supplement your state retirement income and Social Security benefits. In addition to flexible contribution limits and tax-saving features, you can take advantage of a variety of investment options to give your money the opportunity to grow. The Plan provides investment choices that are monitored by the State of Florida and are required to meet performance standards. Introduced in 1982, the state of Florida Deferred Compensation Plan services more than 82,000 participant accounts. Currently, about 48% of your fellow employees have an account with the plan.

To find out more about the Plan, read on. Once you’ve taken a look at a few of the Plan’s benefits, we hope you’ll request enrollment materials and join the Plan. Enrollment is quick and easy, and the Plan is one of the smartest ways to help you reach an enjoyable retirement.

*The State administers the Plan in accordance with Internal Revenue Code 457 (IRC 457) and Florida Administrative Code Section 69C-6 (FAC 69C-6).

Five tips to enjoying your destinationLearn how to save wisely and enjoy the destination you’ve been dreaming about.

Expect to spend 20 to 30 years or longer in retirement.

Don’t count on your State pension or Social Security to provide 100% of your financial needs.

Take more responsibility for your future financial security. It may be up to you to provide the bulk of your retirement income.

Set aside additional funds for health care costs and other necessary expenses in retirement. Remember, group insurance rates will no longer be available to you after you retire.

Keep your investment expectations realistic and diversify your holdings within your account.

With these tips in mind, take a look at how the Plan can help ensure a smooth ride.

4.

Reaching retirement: Get an early startIf you want to reach your retirement income goals in time, the sooner you start saving, the better. That’s because you’ll give your money a chance to make money, which is to say it can “compound” in value. And the longer you invest, the more you can earn through compounding. To see how time and compounding can work, consider the following examples:

Two investors, John and Linda, each invest through their employer’s deferred compensation program. Linda starts saving at age 35. John, who is the same age, does not start until he is 45. Both save $200 monthly and receive a 7% annual rate of return. The graph above left shows how much each of them will have accumulated when they reach age 65. The graphs above right show how much Linda and John will have at age 65 by saving $25 a month and $600 a month.*

*The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan. Your results will vary.

3.

2.

5.

Reduce your tax bite todayBy contributing to the Plan, you can save on taxes today. When youcontribute to your Plan on a pretax basis, your contributions are deducted from your paycheck before you pay federal taxes on your income. This lowers your current taxable income.

Defer taxes until you retireYou are immediately vested and all money contributed to your account accumulates tax-deferred, which means you don’t pay taxes on any of it until you take it out of the Plan, usually when you retire. You may also leave it in the Plan to continue to have the opportunity for tax-deferred growth. This can help you in two ways: 1) You may be in a lower tax bracket when you retire, and 2) the money you would have paid in taxes can continue to compound for you.

The chart below compares the differences between a taxable account and a deferred compensation account. This example is based on a single employee, paid monthly, using a 20% tax rate, and investing $200 a month in both a taxable and a pre-tax deferred compensation plan account.

The Advantage of Pretax Investing Deferred Taxable Compensation Account Account

Gross Income $2,000 $2,000Pretax Investment — (200)Gross Taxable Income 2,000 1,800Withheld Tax (400) (360)Social Security and Medicare (153) (153)Subtotal 1,447 1,287After-Tax Investment (200) —Spendable Income 1,247 1,287

Accumulated Value Comparison DeferredYears of Taxable Compensation Accumulation Account Account

5 $13,812 $14,31910 32,074 34,61715 56,222 63,39220 88,152 104,18530 186,198 243,994The accumulated value comparison assumes a 7% annual rate of return for both accounts with interest compounded monthly. In this example, interest earned in the taxable account is taxed at 20% with taxes deducted monthly. The accumulated value of your account will depend upon your actual tax rate and actual rate of return. The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan.

Changes in tax rates and the tax treatment of investment earnings may impact comparative results. You should consider your personal investment horizon and income tax brackets, both current and anticipated, when making an investment decision as these factors may further impact the results of the comparison.

Destination: funNow that you’ve read a little about the State of Florida Deferred Compensation Plan, it’s time to work toward making your dreams come true. The fun awaits you, so take advantage and plan and save today!

• Receive additional income during retirement.• Avoid paying substantial amounts of federal income taxes.• Put your money to work for you, so you can have fun later.

The time to enroll is todayTo begin saving and investing for your future, request enrollmentmaterials by calling one or more of the companies listed below. You can get started with $20 a month. Each company offers a wide varietyof investment options at a low cost. Your investment company will assist you in completing all the necessary documents. The Plan also provides a selection of products that offer guaranteed returns and safety of principle.

Investment Provider Companies

VALIC 888-568-2542 www.valic.com/floridadcp

Great-West Retirement Services 800-444-9412 www.florida457.com

ING 800-282-6295 www.ingretirementplans.com/custom/fl457

Nationwide Retirement Solutions 800-949-4457 www.nrsflorida.com

T. Rowe Price Group 888-457-5770 rps.troweprice.com/florida

Self-Directed Brokerage Window

Charles Schwab* 888-393-7272 www.schwab.com *Enrollment available through Nationwide.

State of Florida Deferred Compensation Plan is administered by:State Chief Financial OfficerDepartment of Financial ServicesBureau of Deferred Compensation200 East Gaines StreetTallahassee, Florida 32399-0346

Phone: 850-413-3162Toll-free: 877-299-8002Office hours: M-F, 8-5 EST

www.MyFloridaDeferredComp.com

I am interested in receiving the Deferred Compensation Plan information package, which contains the following: • Performance Report, a comparison of the various products, fees and investment items.

• Commonly Asked Questions With Answers about the Deferred Compensation Plan

Tell me more

Ch

eck

this

box

if y

ou w

ould

like

to b

e ad

ded

to th

e Pe

rfor

man

ce R

epor

t mai

ling

list.

Nam

e

Addr

ess

City

Stat

e

Zip

Tele

phon

e (h

ome)

Tele

phon

e (w

ork)

Depa

rtm

ent/A

genc

y

Depa

rtm

ent/A

genc

y Ad

dres

s

City

Stat

e

Zip

Sta

te o

f F

lori

da

mo

ney

was

no

t us

ed t

o p

rod

uce

or

mai

l the

se m

ater

ials

.

$25/Month, 7% Annual Return Compunded Monthly

$600/Month, 7% Annual Return Compunded Monthly

Financial Future Broch.indd 1 7/21/2011 9:50:15 AM

1.

Plan. Save. Retire.with the State of Florida Deferred Compensation

200

EA

ST G

AIN

ES

STR

EE

TT

ALL

AH

ASS

EE

, FLO

RID

A 3

2399

-032

3

RETIREMENT IS A LOT OF FUN—IF YOU PLAN AND SAVE

Golfing on a weekday. Snorkeling during the morning commute. Beachside lounging for hours upon hours. Winingand dining into the sunset. And at the end of the day, work has not once crossed your mind. Your vacation never ends if you plan and save today.Planning your future can help you enjoy all the pleasures of retirement. It’s easy: Just follow the tips below and you’ll be on your way to a stress-free destination.

Do your work today and haveyour fun tomorrowParticipating in the Deferred Compensation Plan can help you add to your retirement nest egg with savings that supplement your state retirement income and Social Security benefits. In addition to flexible contribution limits and tax-saving features, you can take advantage of a variety of investment options to give your money the opportunity to grow. The Plan provides investment choices that are monitored by the State of Florida and are required to meet performance standards. Introduced in 1982, the state of Florida Deferred Compensation Plan services more than 82,000 participant accounts. Currently, about 48% of your fellow employees have an account with the plan.

To find out more about the Plan, read on. Once you’ve taken a look at a few of the Plan’s benefits, we hope you’ll request enrollment materials and join the Plan. Enrollment is quick and easy, and the Plan is one of the smartest ways to help you reach an enjoyable retirement.

*The State administers the Plan in accordance with Internal Revenue Code 457 (IRC 457) and Florida Administrative Code Section 69C-6 (FAC 69C-6).

Five tips to enjoying your destinationLearn how to save wisely and enjoy the destination you’ve been dreaming about.

Expect to spend 20 to 30 years or longer in retirement.

Don’t count on your State pension or Social Security to provide 100% of your financial needs.

Take more responsibility for your future financial security. It may be up to you to provide the bulk of your retirement income.

Set aside additional funds for health care costs and other necessary expenses in retirement. Remember, group insurance rates will no longer be available to you after you retire.

Keep your investment expectations realistic and diversify your holdings within your account.

With these tips in mind, take a look at how the Plan can help ensure a smooth ride.

4.

Reaching retirement: Get an early startIf you want to reach your retirement income goals in time, the sooner you start saving, the better. That’s because you’ll give your money a chance to make money, which is to say it can “compound” in value. And the longer you invest, the more you can earn through compounding. To see how time and compounding can work, consider the following examples:

Two investors, John and Linda, each invest through their employer’s deferred compensation program. Linda starts saving at age 35. John, who is the same age, does not start until he is 45. Both save $200 monthly and receive a 7% annual rate of return. The graph above left shows how much each of them will have accumulated when they reach age 65. The graphs above right show how much Linda and John will have at age 65 by saving $25 a month and $600 a month.*

*The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan. Your results will vary.

3.

2.

5.

Reduce your tax bite todayBy contributing to the Plan, you can save on taxes today. When youcontribute to your Plan on a pretax basis, your contributions are deducted from your paycheck before you pay federal taxes on your income. This lowers your current taxable income.

Defer taxes until you retireYou are immediately vested and all money contributed to your account accumulates tax-deferred, which means you don’t pay taxes on any of it until you take it out of the Plan, usually when you retire. You may also leave it in the Plan to continue to have the opportunity for tax-deferred growth. This can help you in two ways: 1) You may be in a lower tax bracket when you retire, and 2) the money you would have paid in taxes can continue to compound for you.

The chart below compares the differences between a taxable account and a deferred compensation account. This example is based on a single employee, paid monthly, using a 20% tax rate, and investing $200 a month in both a taxable and a pre-tax deferred compensation plan account.

The Advantage of Pretax Investing Deferred Taxable Compensation Account Account

Gross Income $2,000 $2,000Pretax Investment — (200)Gross Taxable Income 2,000 1,800Withheld Tax (400) (360)Social Security and Medicare (153) (153)Subtotal 1,447 1,287After-Tax Investment (200) —Spendable Income 1,247 1,287

Accumulated Value Comparison DeferredYears of Taxable Compensation Accumulation Account Account

5 $13,812 $14,31910 32,074 34,61715 56,222 63,39220 88,152 104,18530 186,198 243,994The accumulated value comparison assumes a 7% annual rate of return for both accounts with interest compounded monthly. In this example, interest earned in the taxable account is taxed at 20% with taxes deducted monthly. The accumulated value of your account will depend upon your actual tax rate and actual rate of return. The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan.

Changes in tax rates and the tax treatment of investment earnings may impact comparative results. You should consider your personal investment horizon and income tax brackets, both current and anticipated, when making an investment decision as these factors may further impact the results of the comparison.

Destination: funNow that you’ve read a little about the State of Florida Deferred Compensation Plan, it’s time to work toward making your dreams come true. The fun awaits you, so take advantage and plan and save today!

• Receive additional income during retirement.• Avoid paying substantial amounts of federal income taxes.• Put your money to work for you, so you can have fun later.

The time to enroll is todayTo begin saving and investing for your future, request enrollmentmaterials by calling one or more of the companies listed below. You can get started with $20 a month. Each company offers a wide varietyof investment options at a low cost. Your investment company will assist you in completing all the necessary documents. The Plan also provides a selection of products that offer guaranteed returns and safety of principle.

Investment Provider Companies

VALIC 888-568-2542 www.valic.com/floridadcp

Great-West Retirement Services 800-444-9412 www.florida457.com

ING 800-282-6295 www.ingretirementplans.com/custom/fl457

Nationwide Retirement Solutions 800-949-4457 www.nrsflorida.com

T. Rowe Price Group 888-457-5770 rps.troweprice.com/florida

Self-Directed Brokerage Window

Charles Schwab* 888-393-7272 www.schwab.com *Enrollment available through Nationwide.

State of Florida Deferred Compensation Plan is administered by:State Chief Financial OfficerDepartment of Financial ServicesBureau of Deferred Compensation200 East Gaines StreetTallahassee, Florida 32399-0346

Phone: 850-413-3162Toll-free: 877-299-8002Office hours: M-F, 8-5 EST

www.MyFloridaDeferredComp.com

I am interested in receiving the Deferred Compensation Plan information package, which contains the following: • Performance Report, a comparison of the various products, fees and investment items.

• Commonly Asked Questions With Answers about the Deferred Compensation Plan

Tell me more

Ch

eck

this

box

if y

ou w

ould

like

to b

e ad

ded

to th

e Pe

rfor

man

ce R

epor

t mai

ling

list.

Nam

e

Addr

ess

City

Stat

e

Zip

Tele

phon

e (h

ome)

Tele

phon

e (w

ork)

Depa

rtm

ent/A

genc

y

Depa

rtm

ent/A

genc

y Ad

dres

s

City

Stat

e

Zip

Sta

te o

f F

lori

da

mo

ney

was

no

t us

ed t

o p

rod

uce

or

mai

l the

se m

ater

ials

.

$25/Month, 7% Annual Return Compunded Monthly

$600/Month, 7% Annual Return Compunded Monthly

Financial Future Broch.indd 1 7/21/2011 9:50:15 AM

1.

Plan. Save. Retire.with the State of Florida Deferred Compensation

200

EA

ST G

AIN

ES

STR

EE

TT

ALL

AH

ASS

EE

, FLO

RID

A 3

2399

-032

3

RETIREMENT IS A LOT OF FUN—IF YOU PLAN AND SAVE

Golfing on a weekday. Snorkeling during the morning commute. Beachside lounging for hours upon hours. Winingand dining into the sunset. And at the end of the day, work has not once crossed your mind. Your vacation never ends if you plan and save today.Planning your future can help you enjoy all the pleasures of retirement. It’s easy: Just follow the tips below and you’ll be on your way to a stress-free destination.

Do your work today and haveyour fun tomorrowParticipating in the Deferred Compensation Plan can help you add to your retirement nest egg with savings that supplement your state retirement income and Social Security benefits. In addition to flexible contribution limits and tax-saving features, you can take advantage of a variety of investment options to give your money the opportunity to grow. The Plan provides investment choices that are monitored by the State of Florida and are required to meet performance standards. Introduced in 1982, the state of Florida Deferred Compensation Plan services more than 82,000 participant accounts. Currently, about 48% of your fellow employees have an account with the plan.

To find out more about the Plan, read on. Once you’ve taken a look at a few of the Plan’s benefits, we hope you’ll request enrollment materials and join the Plan. Enrollment is quick and easy, and the Plan is one of the smartest ways to help you reach an enjoyable retirement.

*The State administers the Plan in accordance with Internal Revenue Code 457 (IRC 457) and Florida Administrative Code Section 69C-6 (FAC 69C-6).

Five tips to enjoying your destinationLearn how to save wisely and enjoy the destination you’ve been dreaming about.

Expect to spend 20 to 30 years or longer in retirement.

Don’t count on your State pension or Social Security to provide 100% of your financial needs.

Take more responsibility for your future financial security. It may be up to you to provide the bulk of your retirement income.

Set aside additional funds for health care costs and other necessary expenses in retirement. Remember, group insurance rates will no longer be available to you after you retire.

Keep your investment expectations realistic and diversify your holdings within your account.

With these tips in mind, take a look at how the Plan can help ensure a smooth ride.

4.

Reaching retirement: Get an early startIf you want to reach your retirement income goals in time, the sooner you start saving, the better. That’s because you’ll give your money a chance to make money, which is to say it can “compound” in value. And the longer you invest, the more you can earn through compounding. To see how time and compounding can work, consider the following examples:

Two investors, John and Linda, each invest through their employer’s deferred compensation program. Linda starts saving at age 35. John, who is the same age, does not start until he is 45. Both save $200 monthly and receive a 7% annual rate of return. The graph above left shows how much each of them will have accumulated when they reach age 65. The graphs above right show how much Linda and John will have at age 65 by saving $25 a month and $600 a month.*

*The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan. Your results will vary.

3.

2.

5.

Reduce your tax bite todayBy contributing to the Plan, you can save on taxes today. When youcontribute to your Plan on a pretax basis, your contributions are deducted from your paycheck before you pay federal taxes on your income. This lowers your current taxable income.

Defer taxes until you retireYou are immediately vested and all money contributed to your account accumulates tax-deferred, which means you don’t pay taxes on any of it until you take it out of the Plan, usually when you retire. You may also leave it in the Plan to continue to have the opportunity for tax-deferred growth. This can help you in two ways: 1) You may be in a lower tax bracket when you retire, and 2) the money you would have paid in taxes can continue to compound for you.

The chart below compares the differences between a taxable account and a deferred compensation account. This example is based on a single employee, paid monthly, using a 20% tax rate, and investing $200 a month in both a taxable and a pre-tax deferred compensation plan account.

The Advantage of Pretax Investing Deferred Taxable Compensation Account Account

Gross Income $2,000 $2,000Pretax Investment — (200)Gross Taxable Income 2,000 1,800Withheld Tax (400) (360)Social Security and Medicare (153) (153)Subtotal 1,447 1,287After-Tax Investment (200) —Spendable Income 1,247 1,287

Accumulated Value Comparison DeferredYears of Taxable Compensation Accumulation Account Account

5 $13,812 $14,31910 32,074 34,61715 56,222 63,39220 88,152 104,18530 186,198 243,994The accumulated value comparison assumes a 7% annual rate of return for both accounts with interest compounded monthly. In this example, interest earned in the taxable account is taxed at 20% with taxes deducted monthly. The accumulated value of your account will depend upon your actual tax rate and actual rate of return. The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan.

Changes in tax rates and the tax treatment of investment earnings may impact comparative results. You should consider your personal investment horizon and income tax brackets, both current and anticipated, when making an investment decision as these factors may further impact the results of the comparison.

Destination: funNow that you’ve read a little about the State of Florida Deferred Compensation Plan, it’s time to work toward making your dreams come true. The fun awaits you, so take advantage and plan and save today!

• Receive additional income during retirement.• Avoid paying substantial amounts of federal income taxes.• Put your money to work for you, so you can have fun later.

The time to enroll is todayTo begin saving and investing for your future, request enrollmentmaterials by calling one or more of the companies listed below. You can get started with $20 a month. Each company offers a wide varietyof investment options at a low cost. Your investment company will assist you in completing all the necessary documents. The Plan also provides a selection of products that offer guaranteed returns and safety of principle.

Investment Provider Companies

VALIC 888-568-2542 www.valic.com/floridadcp

Great-West Retirement Services 800-444-9412 www.florida457.com

ING 800-282-6295 www.ingretirementplans.com/custom/fl457

Nationwide Retirement Solutions 800-949-4457 www.nrsflorida.com

T. Rowe Price Group 888-457-5770 rps.troweprice.com/florida

Self-Directed Brokerage Window

Charles Schwab* 888-393-7272 www.schwab.com *Enrollment available through Nationwide.

State of Florida Deferred Compensation Plan is administered by:State Chief Financial OfficerDepartment of Financial ServicesBureau of Deferred Compensation200 East Gaines StreetTallahassee, Florida 32399-0346

Phone: 850-413-3162Toll-free: 877-299-8002Office hours: M-F, 8-5 EST

www.MyFloridaDeferredComp.com

I am interested in receiving the Deferred Compensation Plan information package, which contains the following: • Performance Report, a comparison of the various products, fees and investment items.

• Commonly Asked Questions With Answers about the Deferred Compensation Plan

Tell me more

Ch

eck

this

box

if y

ou w

ould

like

to b

e ad

ded

to th

e Pe

rfor

man

ce R

epor

t mai

ling

list.

Nam

e

Addr

ess

City

Stat

e

Zip

Tele

phon

e (h

ome)

Tele

phon

e (w

ork)

Depa

rtm

ent/A

genc

y

Depa

rtm

ent/A

genc

y Ad

dres

s

City

Stat

e

Zip

Sta

te o

f F

lori

da

mo

ney

was

no

t us

ed t

o p

rod

uce

or

mai

l the

se m

ater

ials

.

$25/Month, 7% Annual Return Compunded Monthly

$600/Month, 7% Annual Return Compunded Monthly

Financial Future Broch.indd 1 7/21/2011 9:50:15 AM

1.

Plan. Save. Retire.with the State of Florida Deferred Compensation

200 EA

ST G

AIN

ES ST

RE

ET

TA

LLAH

ASSE

E, FLO

RID

A 32399-0323

RETIREMENT IS A LOT OF FUN—IF YOU PLAN AND SAVE

Golfing on a weekday. Snorkeling during the morning commute. Beachside lounging for hours upon hours. Winingand dining into the sunset. And at the end of the day, work has not once crossed your mind. Your vacation never ends if you plan and save today.Planning your future can help you enjoy all the pleasures of retirement. It’s easy: Just follow the tips below and you’ll be on your way to a stress-free destination.

Do your work today and haveyour fun tomorrowParticipating in the Deferred Compensation Plan can help you add to your retirement nest egg with savings that supplement your state retirement income and Social Security benefits. In addition to flexible contribution limits and tax-saving features, you can take advantage of a variety of investment options to give your money the opportunity to grow. The Plan provides investment choices that are monitored by the State of Florida and are required to meet performance standards. Introduced in 1982, the state of Florida Deferred Compensation Plan services more than 82,000 participant accounts. Currently, about 48% of your fellow employees have an account with the plan.

To find out more about the Plan, read on. Once you’ve taken a look at a few of the Plan’s benefits, we hope you’ll request enrollment materials and join the Plan. Enrollment is quick and easy, and the Plan is one of the smartest ways to help you reach an enjoyable retirement.

*The State administers the Plan in accordance with Internal Revenue Code 457 (IRC 457) and Florida Administrative Code Section 69C-6 (FAC 69C-6).

Five tips to enjoying your destinationLearn how to save wisely and enjoy the destination you’ve been dreaming about.

Expect to spend 20 to 30 years or longer in retirement.

Don’t count on your State pension or Social Security to provide 100% of your financial needs.

Take more responsibility for your future financial security. It may be up to you to provide the bulk of your retirement income.

Set aside additional funds for health care costs and other necessary expenses in retirement. Remember, group insurance rates will no longer be available to you after you retire.

Keep your investment expectations realistic and diversify your holdings within your account.

With these tips in mind, take a look at how the Plan can help ensure a smooth ride.

4.

Reaching retirement: Get an early startIf you want to reach your retirement income goals in time, the sooner you start saving, the better. That’s because you’ll give your money a chance to make money, which is to say it can “compound” in value. And the longer you invest, the more you can earn through compounding. To see how time and compounding can work, consider the following examples:

Two investors, John and Linda, each invest through their employer’s deferred compensation program. Linda starts saving at age 35. John, who is the same age, does not start until he is 45. Both save $200 monthly and receive a 7% annual rate of return. The graph above left shows how much each of them will have accumulated when they reach age 65. The graphs above right show how much Linda and John will have at age 65 by saving $25 a month and $600 a month.*

*The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan. Your results will vary.

3.

2.

5.

Reduce your tax bite todayBy contributing to the Plan, you can save on taxes today. When youcontribute to your Plan on a pretax basis, your contributions are deducted from your paycheck before you pay federal taxes on your income. This lowers your current taxable income.

Defer taxes until you retireYou are immediately vested and all money contributed to your account accumulates tax-deferred, which means you don’t pay taxes on any of it until you take it out of the Plan, usually when you retire. You may also leave it in the Plan to continue to have the opportunity for tax-deferred growth. This can help you in two ways: 1) You may be in a lower tax bracket when you retire, and 2) the money you would have paid in taxes can continue to compound for you.

The chart below compares the differences between a taxable account and a deferred compensation account. This example is based on a single employee, paid monthly, using a 20% tax rate, and investing $200 a month in both a taxable and a pre-tax deferred compensation plan account.

The Advantage of Pretax Investing Deferred Taxable Compensation Account Account

Gross Income $2,000 $2,000Pretax Investment — (200)Gross Taxable Income 2,000 1,800Withheld Tax (400) (360)Social Security and Medicare (153) (153)Subtotal 1,447 1,287After-Tax Investment (200) —Spendable Income 1,247 1,287

Accumulated Value Comparison DeferredYears of Taxable Compensation Accumulation Account Account

5 $13,812 $14,31910 32,074 34,61715 56,222 63,39220 88,152 104,18530 186,198 243,994The accumulated value comparison assumes a 7% annual rate of return for both accounts with interest compounded monthly. In this example, interest earned in the taxable account is taxed at 20% with taxes deducted monthly. The accumulated value of your account will depend upon your actual tax rate and actual rate of return. The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan.

Changes in tax rates and the tax treatment of investment earnings may impact comparative results. You should consider your personal investment horizon and income tax brackets, both current and anticipated, when making an investment decision as these factors may further impact the results of the comparison.

Destination: funNow that you’ve read a little about the State of Florida Deferred Compensation Plan, it’s time to work toward making your dreams come true. The fun awaits you, so take advantage and plan and save today!

• Receive additional income during retirement.• Avoid paying substantial amounts of federal income taxes.• Put your money to work for you, so you can have fun later.

The time to enroll is todayTo begin saving and investing for your future, request enrollmentmaterials by calling one or more of the companies listed below. You can get started with $20 a month. Each company offers a wide varietyof investment options at a low cost. Your investment company will assist you in completing all the necessary documents. The Plan also provides a selection of products that offer guaranteed returns and safety of principle.

Investment Provider Companies

VALIC 888-568-2542 www.valic.com/floridadcp

Great-West Retirement Services 800-444-9412 www.florida457.com

ING 800-282-6295 www.ingretirementplans.com/custom/fl457

Nationwide Retirement Solutions 800-949-4457 www.nrsflorida.com

T. Rowe Price Group 888-457-5770 rps.troweprice.com/florida

Self-Directed Brokerage Window

Charles Schwab* 888-393-7272 www.schwab.com *Enrollment available through Nationwide.

State of Florida Deferred Compensation Plan is administered by:State Chief Financial OfficerDepartment of Financial ServicesBureau of Deferred Compensation200 East Gaines StreetTallahassee, Florida 32399-0346

Phone: 850-413-3162Toll-free: 877-299-8002Office hours: M-F, 8-5 EST

www.MyFloridaDeferredComp.com

I am interested in receiving the Deferred Compensation Plan information package, which contains the following: • Performance Report, a comparison of the various products, fees and investment items.

• Commonly Asked Questions With Answers about the Deferred Compensation Plan

Tell me more

Check this box if you w

ould like to be added to the Performance Report m

ailing list.

Name

Address

City

State

Zip

Telephone (home)

Telephone (work)

Department/Agency

Department/Agency Address

City

State

Zip

State o

f Flo

rida m

oney w

as not used

to p

rod

uce or m

ail these materials.

$25/Month, 7% Annual Return Compunded Monthly

$600/Month, 7% Annual Return Compunded Monthly

Financial Future Broch.indd 17/21/2011 9:50:15 AM

1.

Plan. Save. Retire.with the State of Florida Deferred Compensation

200 EA

ST G

AIN

ES ST

RE

ET

TA

LLAH

ASSE

E, FLO

RID

A 32399-0323

RETIREMENT IS A LOT OF FUN—IF YOU PLAN AND SAVE

Golfing on a weekday. Snorkeling during the morning commute. Beachside lounging for hours upon hours. Winingand dining into the sunset. And at the end of the day, work has not once crossed your mind. Your vacation never ends if you plan and save today.Planning your future can help you enjoy all the pleasures of retirement. It’s easy: Just follow the tips below and you’ll be on your way to a stress-free destination.

Do your work today and haveyour fun tomorrowParticipating in the Deferred Compensation Plan can help you add to your retirement nest egg with savings that supplement your state retirement income and Social Security benefits. In addition to flexible contribution limits and tax-saving features, you can take advantage of a variety of investment options to give your money the opportunity to grow. The Plan provides investment choices that are monitored by the State of Florida and are required to meet performance standards. Introduced in 1982, the state of Florida Deferred Compensation Plan services more than 82,000 participant accounts. Currently, about 48% of your fellow employees have an account with the plan.

To find out more about the Plan, read on. Once you’ve taken a look at a few of the Plan’s benefits, we hope you’ll request enrollment materials and join the Plan. Enrollment is quick and easy, and the Plan is one of the smartest ways to help you reach an enjoyable retirement.

*The State administers the Plan in accordance with Internal Revenue Code 457 (IRC 457) and Florida Administrative Code Section 69C-6 (FAC 69C-6).

Five tips to enjoying your destinationLearn how to save wisely and enjoy the destination you’ve been dreaming about.

Expect to spend 20 to 30 years or longer in retirement.

Don’t count on your State pension or Social Security to provide 100% of your financial needs.

Take more responsibility for your future financial security. It may be up to you to provide the bulk of your retirement income.

Set aside additional funds for health care costs and other necessary expenses in retirement. Remember, group insurance rates will no longer be available to you after you retire.

Keep your investment expectations realistic and diversify your holdings within your account.

With these tips in mind, take a look at how the Plan can help ensure a smooth ride.

4.

Reaching retirement: Get an early startIf you want to reach your retirement income goals in time, the sooner you start saving, the better. That’s because you’ll give your money a chance to make money, which is to say it can “compound” in value. And the longer you invest, the more you can earn through compounding. To see how time and compounding can work, consider the following examples:

Two investors, John and Linda, each invest through their employer’s deferred compensation program. Linda starts saving at age 35. John, who is the same age, does not start until he is 45. Both save $200 monthly and receive a 7% annual rate of return. The graph above left shows how much each of them will have accumulated when they reach age 65. The graphs above right show how much Linda and John will have at age 65 by saving $25 a month and $600 a month.*

*The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan. Your results will vary.

3.

2.

5.

Reduce your tax bite todayBy contributing to the Plan, you can save on taxes today. When youcontribute to your Plan on a pretax basis, your contributions are deducted from your paycheck before you pay federal taxes on your income. This lowers your current taxable income.

Defer taxes until you retireYou are immediately vested and all money contributed to your account accumulates tax-deferred, which means you don’t pay taxes on any of it until you take it out of the Plan, usually when you retire. You may also leave it in the Plan to continue to have the opportunity for tax-deferred growth. This can help you in two ways: 1) You may be in a lower tax bracket when you retire, and 2) the money you would have paid in taxes can continue to compound for you.

The chart below compares the differences between a taxable account and a deferred compensation account. This example is based on a single employee, paid monthly, using a 20% tax rate, and investing $200 a month in both a taxable and a pre-tax deferred compensation plan account.

The Advantage of Pretax Investing Deferred Taxable Compensation Account Account

Gross Income $2,000 $2,000Pretax Investment — (200)Gross Taxable Income 2,000 1,800Withheld Tax (400) (360)Social Security and Medicare (153) (153)Subtotal 1,447 1,287After-Tax Investment (200) —Spendable Income 1,247 1,287

Accumulated Value Comparison DeferredYears of Taxable Compensation Accumulation Account Account

5 $13,812 $14,31910 32,074 34,61715 56,222 63,39220 88,152 104,18530 186,198 243,994The accumulated value comparison assumes a 7% annual rate of return for both accounts with interest compounded monthly. In this example, interest earned in the taxable account is taxed at 20% with taxes deducted monthly. The accumulated value of your account will depend upon your actual tax rate and actual rate of return. The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan.

Changes in tax rates and the tax treatment of investment earnings may impact comparative results. You should consider your personal investment horizon and income tax brackets, both current and anticipated, when making an investment decision as these factors may further impact the results of the comparison.

Destination: funNow that you’ve read a little about the State of Florida Deferred Compensation Plan, it’s time to work toward making your dreams come true. The fun awaits you, so take advantage and plan and save today!

• Receive additional income during retirement.• Avoid paying substantial amounts of federal income taxes.• Put your money to work for you, so you can have fun later.

The time to enroll is todayTo begin saving and investing for your future, request enrollmentmaterials by calling one or more of the companies listed below. You can get started with $20 a month. Each company offers a wide varietyof investment options at a low cost. Your investment company will assist you in completing all the necessary documents. The Plan also provides a selection of products that offer guaranteed returns and safety of principle.

Investment Provider Companies

VALIC 888-568-2542 www.valic.com/floridadcp

Great-West Retirement Services 800-444-9412 www.florida457.com

ING 800-282-6295 www.ingretirementplans.com/custom/fl457

Nationwide Retirement Solutions 800-949-4457 www.nrsflorida.com

T. Rowe Price Group 888-457-5770 rps.troweprice.com/florida

Self-Directed Brokerage Window

Charles Schwab* 888-393-7272 www.schwab.com *Enrollment available through Nationwide.

State of Florida Deferred Compensation Plan is administered by:State Chief Financial OfficerDepartment of Financial ServicesBureau of Deferred Compensation200 East Gaines StreetTallahassee, Florida 32399-0346

Phone: 850-413-3162Toll-free: 877-299-8002Office hours: M-F, 8-5 EST

www.MyFloridaDeferredComp.com

I am interested in receiving the Deferred Compensation Plan information package, which contains the following: • Performance Report, a comparison of the various products, fees and investment items.

• Commonly Asked Questions With Answers about the Deferred Compensation Plan

Tell me more

Check this box if you would like to be added to the Perform

ance Report mailing list.

Name

Address

City

State

Zip

Telephone (home)

Telephone (work)

Department/Agency

Department/Agency Address

City

State

Zip

State o

f Flo

rida m

oney w

as not used

to p

rod

uce or m

ail these materials.

$25/Month, 7% Annual Return Compunded Monthly

$600/Month, 7% Annual Return Compunded Monthly

Financial Future Broch.indd 17/21/2011 9:50:15 AM

1.

Plan. Save. Retire.with the State of Florida Deferred Compensation

200 EA

ST G

AIN

ES ST

RE

ET

TA

LLAH

ASSE

E, FLO

RID

A 32399-0323

RETIREMENT IS A LOT OF FUN—IF YOU PLAN AND SAVE

Golfing on a weekday. Snorkeling during the morning commute. Beachside lounging for hours upon hours. Winingand dining into the sunset. And at the end of the day, work has not once crossed your mind. Your vacation never ends if you plan and save today.Planning your future can help you enjoy all the pleasures of retirement. It’s easy: Just follow the tips below and you’ll be on your way to a stress-free destination.

Do your work today and haveyour fun tomorrowParticipating in the Deferred Compensation Plan can help you add to your retirement nest egg with savings that supplement your state retirement income and Social Security benefits. In addition to flexible contribution limits and tax-saving features, you can take advantage of a variety of investment options to give your money the opportunity to grow. The Plan provides investment choices that are monitored by the State of Florida and are required to meet performance standards. Introduced in 1982, the state of Florida Deferred Compensation Plan services more than 82,000 participant accounts. Currently, about 48% of your fellow employees have an account with the plan.

To find out more about the Plan, read on. Once you’ve taken a look at a few of the Plan’s benefits, we hope you’ll request enrollment materials and join the Plan. Enrollment is quick and easy, and the Plan is one of the smartest ways to help you reach an enjoyable retirement.

*The State administers the Plan in accordance with Internal Revenue Code 457 (IRC 457) and Florida Administrative Code Section 69C-6 (FAC 69C-6).

Five tips to enjoying your destinationLearn how to save wisely and enjoy the destination you’ve been dreaming about.

Expect to spend 20 to 30 years or longer in retirement.

Don’t count on your State pension or Social Security to provide 100% of your financial needs.

Take more responsibility for your future financial security. It may be up to you to provide the bulk of your retirement income.

Set aside additional funds for health care costs and other necessary expenses in retirement. Remember, group insurance rates will no longer be available to you after you retire.

Keep your investment expectations realistic and diversify your holdings within your account.

With these tips in mind, take a look at how the Plan can help ensure a smooth ride.

4.

Reaching retirement: Get an early startIf you want to reach your retirement income goals in time, the sooner you start saving, the better. That’s because you’ll give your money a chance to make money, which is to say it can “compound” in value. And the longer you invest, the more you can earn through compounding. To see how time and compounding can work, consider the following examples:

Two investors, John and Linda, each invest through their employer’s deferred compensation program. Linda starts saving at age 35. John, who is the same age, does not start until he is 45. Both save $200 monthly and receive a 7% annual rate of return. The graph above left shows how much each of them will have accumulated when they reach age 65. The graphs above right show how much Linda and John will have at age 65 by saving $25 a month and $600 a month.*

*The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan. Your results will vary.

3.

2.

5.

Reduce your tax bite todayBy contributing to the Plan, you can save on taxes today. When youcontribute to your Plan on a pretax basis, your contributions are deducted from your paycheck before you pay federal taxes on your income. This lowers your current taxable income.

Defer taxes until you retireYou are immediately vested and all money contributed to your account accumulates tax-deferred, which means you don’t pay taxes on any of it until you take it out of the Plan, usually when you retire. You may also leave it in the Plan to continue to have the opportunity for tax-deferred growth. This can help you in two ways: 1) You may be in a lower tax bracket when you retire, and 2) the money you would have paid in taxes can continue to compound for you.

The chart below compares the differences between a taxable account and a deferred compensation account. This example is based on a single employee, paid monthly, using a 20% tax rate, and investing $200 a month in both a taxable and a pre-tax deferred compensation plan account.

The Advantage of Pretax Investing Deferred Taxable Compensation Account Account

Gross Income $2,000 $2,000Pretax Investment — (200)Gross Taxable Income 2,000 1,800Withheld Tax (400) (360)Social Security and Medicare (153) (153)Subtotal 1,447 1,287After-Tax Investment (200) —Spendable Income 1,247 1,287

Accumulated Value Comparison DeferredYears of Taxable Compensation Accumulation Account Account

5 $13,812 $14,31910 32,074 34,61715 56,222 63,39220 88,152 104,18530 186,198 243,994The accumulated value comparison assumes a 7% annual rate of return for both accounts with interest compounded monthly. In this example, interest earned in the taxable account is taxed at 20% with taxes deducted monthly. The accumulated value of your account will depend upon your actual tax rate and actual rate of return. The rate of return assumed is hypothetical and for illustrative purposes only. It does not represent the performance of any of the investment options in the Plan.

Changes in tax rates and the tax treatment of investment earnings may impact comparative results. You should consider your personal investment horizon and income tax brackets, both current and anticipated, when making an investment decision as these factors may further impact the results of the comparison.

Destination: funNow that you’ve read a little about the State of Florida Deferred Compensation Plan, it’s time to work toward making your dreams come true. The fun awaits you, so take advantage and plan and save today!

• Receive additional income during retirement.• Avoid paying substantial amounts of federal income taxes.• Put your money to work for you, so you can have fun later.

The time to enroll is todayTo begin saving and investing for your future, request enrollmentmaterials by calling one or more of the companies listed below. You can get started with $20 a month. Each company offers a wide varietyof investment options at a low cost. Your investment company will assist you in completing all the necessary documents. The Plan also provides a selection of products that offer guaranteed returns and safety of principle.

Investment Provider Companies

VALIC 888-568-2542 www.valic.com/floridadcp

Great-West Retirement Services 800-444-9412 www.florida457.com

ING 800-282-6295 www.ingretirementplans.com/custom/fl457

Nationwide Retirement Solutions 800-949-4457 www.nrsflorida.com

T. Rowe Price Group 888-457-5770 rps.troweprice.com/florida

Self-Directed Brokerage Window

Charles Schwab* 888-393-7272 www.schwab.com *Enrollment available through Nationwide.

State of Florida Deferred Compensation Plan is administered by:State Chief Financial OfficerDepartment of Financial ServicesBureau of Deferred Compensation200 East Gaines StreetTallahassee, Florida 32399-0346

Phone: 850-413-3162Toll-free: 877-299-8002Office hours: M-F, 8-5 EST

www.MyFloridaDeferredComp.com

I am interested in receiving the Deferred Compensation Plan information package, which contains the following: • Performance Report, a comparison of the various products, fees and investment items.

• Commonly Asked Questions With Answers about the Deferred Compensation Plan

Tell me more

Check this box if you w

ould like to be added to the Performance Report m

ailing list.

Name

Address

City

State

Zip

Telephone (home)

Telephone (work)

Department/Agency

Department/Agency Address

City

State

Zip

State o

f Flo

rida m

oney w

as not used

to p

rod

uce or m

ail these materials.

$25/Month, 7% Annual Return Compunded Monthly

$600/Month, 7% Annual Return Compunded Monthly

Financial Future Broch.indd 17/21/2011 9:50:15 AM

200 EA

ST G

AIN

ES ST

RE

ET

TA

LLAH

ASSE

E, FLO

RID

A 32399-0323