payment fraud trends and preventionaz9194.vo.msecnd.net/pdfs/110401/232.pdf · payment fraud trends...

TRANSCRIPT

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Payment Fraud Trends and Prevention

Brad Larson Clairersquos Boutiques

Terry Crawford AMC Theatres

Jerl Rossi Northrop Grumman Corporation

Claudia Swendseid Federal Reserve Bank of Minneapolis

April 4 2011

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

bull Please turn off all cell phones or mobile devicesbull Thank you to todayrsquos sponsors

ndash This morningrsquos Continental Breakfast sponsored by

Javelin

ndash Breakfast Roundtables sponsored by SWACHA

ndash Thought Leadership Spotlight Session sponsored by

Fundtech

ndash Monday Night Celebration sponsored by Fiserv

bull Most of the education sessions at the conference can be counted towards your continuing AAP accreditation If you are interested in becoming an Accredited ACH Professional (AAP) please stop by the NACHA amp RPA booth

bull Please take a moment to complete session evaluations Each evening attendees will receive an email link to access session evaluations that are offered each day Attendees are automatically entered into a daily drawing for a chance to win a $50 gift card

bull Register now for PAYMENTS 2012 ndash Receive the PAYMENTS 2011 Early-Bird Rates ndash Only available onsite ndash Visit the Registration Desk for more details

Thanks to all of our

Track Sponsors

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Agenda

Who We Are

Payment Fraud Trends

Payment Fraud by Instrument

Fraud Prevention

Conclusions

3

Disclaimer The views expressed in this presentation are those of the speakers and do NOT necessarily reflect the views of the organizations for which they work

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

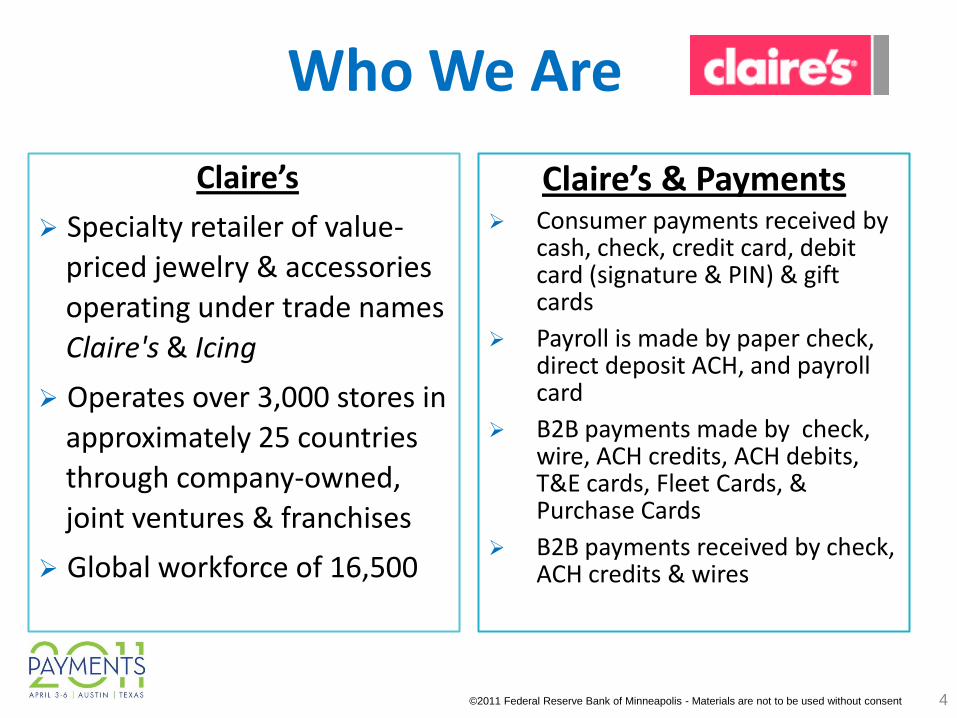

Who We Are

Clairersquos amp Payments Consumer payments received by

cash check credit card debit card (signature amp PIN) amp gift cards

Payroll is made by paper check direct deposit ACH and payroll card

B2B payments made by check wire ACH credits ACH debits TampE cards Fleet Cards amp Purchase Cards

B2B payments received by check ACH credits amp wires

4

Clairersquos

Specialty retailer of value-

priced jewelry amp accessories

operating under trade names

Claires amp Icing

Operates over 3000 stores in

approximately 25 countries

through company-owned

joint ventures amp franchises

Global workforce of 16500

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Who We Are

AMC amp Payments Consumer payments received by cash credit

cards debit cards (signature amp PIN) amp gift cards

Credit card volume (over 12 billion per year) is about 55 of total revenue PCI DSS ldquolevel 1rdquo merchant

Payroll is made by paper check direct deposit ACH amp payroll card

B2B payments made by check wire ACH credits ACH debits TampE cards Fleet Cards amp Purchase Cards B2B payments received by check ACH credits wires amp credit cards

5

AMC One of the worldrsquos most innovative amp

largest theatrical exhibition companies 2nd largest US exhibitor

Operates over 380 theatres with over 5325 screens in 30 states the District of Columbia amp 4 countries

Privately held amp headquartered in Kansas City Missouri since its founding in 1920 Employs about 16800 full amp part-time associates

Hundreds of millions of guests attend AMC theatres each year

(Annualized) transactions $(000rsquos)

Wires 300 191677

ACH 400000 1474190

Checks 1110000 927666

Credit Card (receipts)

72782500 1318326

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Who We Are

NOC amp Payments 95 payroll is via direct deposit 5 check

Customer Remittance

Vendor Payments

6

Northop Grumman (NOC) Leading global security company that has

achieved historic accomplishments from transporting Lindbergh across the Atlantic to carrying astronauts to the moon amp back

120000 employees provide systems products amp solutions in aerospace electronics information systems shipbuilding amp technical services to government amp commercial customers worldwide

Conducts business mostly with the US GovernmentDepartment of Defense Other customers include local state amp foreign governments amp domestic amp international commercial companies

In 2009 delivered 6 ships to the US Navy amp Coast Guard amp launched 2 space tracking amp surveillance system satellites

(Annualized) VolumeAmount

($ millions)

Wires 8000 $ 3000

ACH 64000 $ 28000

Checks 35000 $ 300

Credit Card 1258000 $ 22

(Annualized) VolumeAmount

($ millions)

Wires 10000 $ 10100

ACH 700000 $ 16885

Checks 500000 $ 4458

Credit Card 297787 $ 150

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Who We Are

Federal Reserve System Sets amp implements nationrsquos monetary

policy

Supervises amp regulates range of financial institutions amp activities to ensure safe amp sound banking practices

Provides payments services to financial institutions (FIs) amp the federal government

Mission in payments to foster the integrity efficiency amp accessibility of US dollar payments amp settlement systems issue a uniform currency amp act as the fiscal agent amp depository for the US government

Fed amp Payments The Fed clears amp settles a large

portion of US interbank payments

7

Service Average

Volume Daily

AverageValue Daily

Fedwire Funds 494 000 $24 trillion

Fedwire Securities

78000 $12 trillion

FedACH 399 million $654 billion

Check 29 million $414 billion

National Settlement

2100 $55 billion

commercial volume only data through 3rd quarter 2010

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Payment Fraud Defined

Payments focused on today

Check

ACH credits amp debits

Card

Impact of cyberspace on payment fraud

Payments Fraud Definition Fraud that occurs when someone gains

financial or material advantage by using a payment instrument or

information from a payment instrument to complete a transaction that

is not authorized by the legitimate account holder

8

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Accurate Data on Payment Fraud is Limited

No definitive data on total number of payment fraud attacks or amount of losses in US

Practices of FIs companies amp industries to monitor fraud vary

Fraud data collected is often not shared data that is shared is not comparable

Fraud ldquofactsrdquo reported are subject to hype

0

20

40

60

80

100Internally track loss

Internally track loss avoidedPeer benchmarking

Report to Natl Shared Databases

0

20

40

60

80

100

Internally track loss amp loss avoided

Peer benchmarking

of FIs Tracking amp Sharing ATMDebit Card Fraud Data

Chart Data Source ABA 2007 Deposit Account Fraud Survey

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Corporate Fraud Attacks amp Losses

10

Source 2010 AFP Payments Fraud amp Control Survey

Nearly frac34 of corporations

reported payments fraud

attacks in 2009 about 30

suffered losses

Large companies are more

often the target of fraud

small companies more often

suffer losses

Fraud attempts have been

steady since 2006 fraud

losses have declined since

2006

55

6872 71 71 73

17 19

58

37 37

30

0

10

20

30

40

50

60

70

80

90

100

2004 2005 2006 2007 2008 2009

Respondents

Fraud Losses

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Payment Types

Check ACH1 Corporate amp Commercial

Cards2

Consumer Cards

(DbCr)

Subject to Fraud 90

25 Debits 7 Credits

17 20

Financial Loss From Fraud 17 11

43 Own 16 Accepted

NA

Responsible for Greatest Financial Loss

645 Debits1 Credits

8 20

Primary Reason for Loss

Did not use positive pay

services

Did not use debit blocks

filters amp positive pay

Illicit use of own card data amp inadequate

internal controls

NA3

Corporate Fraud by Payment Type

Check fraud most attempted amp most subject to losses consistent trend since 2004

Card fraud losses growing

Main reasons for losses

Internal controls not enforced

Common prevention services not used

AFP 2010 Payments Fraud amp Control Survey

1Includes ACH debits amp credits except as noted2Includes payments made on organizationrsquos own cards amp B2B card payments accepted3NA ndash data not collected in 2010 survey

11

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

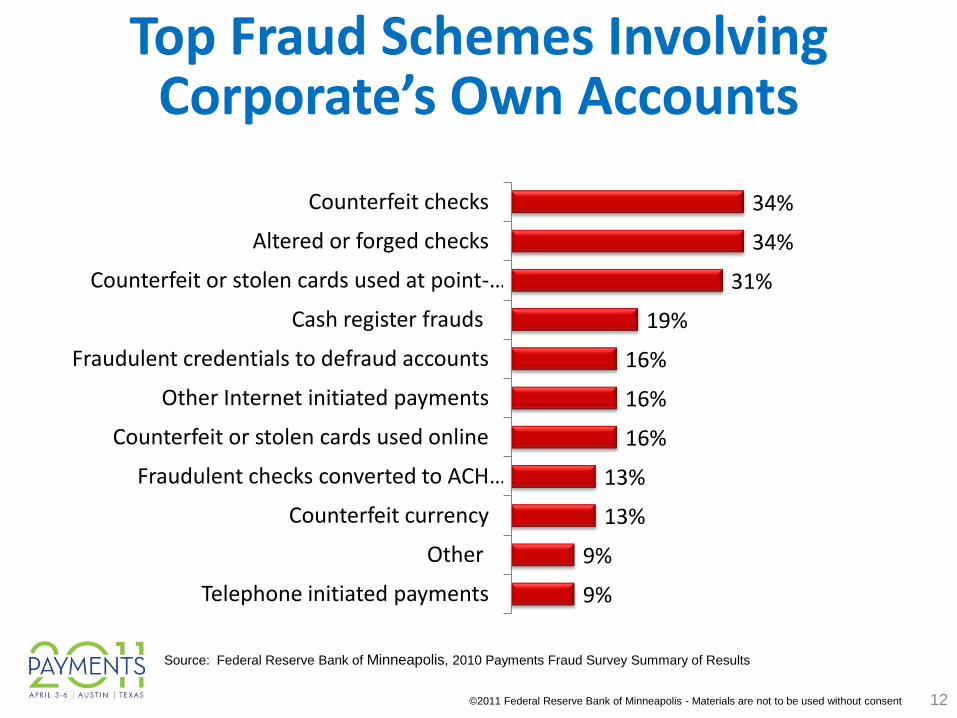

Top Fraud Schemes Involving Corporatersquos Own Accounts

12

9

9

13

13

16

16

16

19

31

34

34

Telephone initiated payments

Other

Counterfeit currency

Fraudulent checks converted to ACH hellip

Counterfeit or stolen cards used online

Other Internet initiated payments

Fraudulent credentials to defraud accounts

Cash register frauds

Counterfeit or stolen cards used at point-hellip

Altered or forged checks

Counterfeit checks

Source Federal Reserve Bank of Minneapolis 2010 Payments Fraud Survey Summary of Results

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Top Fraud Schemes Involving Payments Accepted

13

9

9

13

13

16

16

16

19

31

34

34

Telephone initiated payments

Other

Counterfeit currency

Fraudulent checks converted to ACH payments

Counterfeit or stolen cards used online

Other Internet initiated payments

Fraudulent credentials to defraud accounts

Cash register frauds

Counterfeit or stolen cards used at point-of-hellip

Altered or forged checks

Counterfeit checks

Source Federal Reserve Bank of Minneapolis 2010 Payments Fraud Survey Summary of Results

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

External Parties Responsible for Most Payments Fraud

Perpetrators of Payments Fraud that Resulted in Financial Loss in 2009

AllRespondents

Revenues gt$1 B

Revenues lt $1 B

Outside Individual (eg check forged stolen card)

87 87 88

Organized Crime Ring 15 15 12

Internal Party 11 12 8

External known party (eg vendor 3rd party service provider trading partner)

8 10 4

Criminal invasion(eg hacked system malware)

4 3 7

Other 4 2 6

Lost or stolen laptop or other devise 2 1 2

14

Source 2010 AFP Payments Fraud amp Control Study

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Comparative Cost of Payments Fraud

Payment Method

Comparative ValueRange

Total DollarValue

Estimated

Loss

Source of Information

Credit Card $07 - $14per$100 purchases

$21 trillion $147 - 294 billion(20072008)

Nilson Report 2008 Javelin 2009 ID Fraud Survey Report

Debit Card ndashPIN

$001 - $028 per$100 purchases

$03 trillion $327 million (2007) Pulse 2008 Debit Issuer Study

Debit Card ndashSignature

$024 - $096 per$100 purchases

$06 trillion $324 million(2007)

Pulse 2008 Debit Issuer Study

Debit Card ndashATM

$025 per $100 value or $025 per transaction

$0579 trillion(58 billion trans)

$145 million(2007)

Pulse 2008 Debit Issuer Study

ACH $023 per $100 value of transactions

$31 trillion $698 billion(20052006)

NACHA 2005 ABA 2006

Check $027 per $100 value of checks paid

$416 trillion $11 billion(2006)

ABA 2006 Nilson Report 2007 FRB Kansas City

Cash $008 per $100 value of cash in circulation

$079 trillion In circulation YE lsquo07

$61 million (2007)

US Secret Service press release March 2008

DATA IS NOT PRECISE INTENDED TO ENABLE GENERAL COMPARISON OF FRAUD ACROSS PAYMENT TYPES

Estimated values For cards aggregate losses were calculated by applying the 2007 average loss rate to the 2006 payment value For check amp ACH the loss range was calculated based on the aggregate loss estimate amp 2006 payment value

Total dollar values reflect 2006 estimates from the 2007 Federal Reserve Payments Study except currency in circulation

15

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Check Fraud

16

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Small Biz Accounts Targeted More by Check Fraud than Larger Biz

2218

5

1216

1 6

4

4

5

1

4

16 95

Community Mid-Sized Regional Money Center All

Target of Check Fraud By Size of Bank amp Account Type

Large Corporation

Middle Market

Small Business

Source 2009 ABA Deposit Account Fraud Survey

17

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

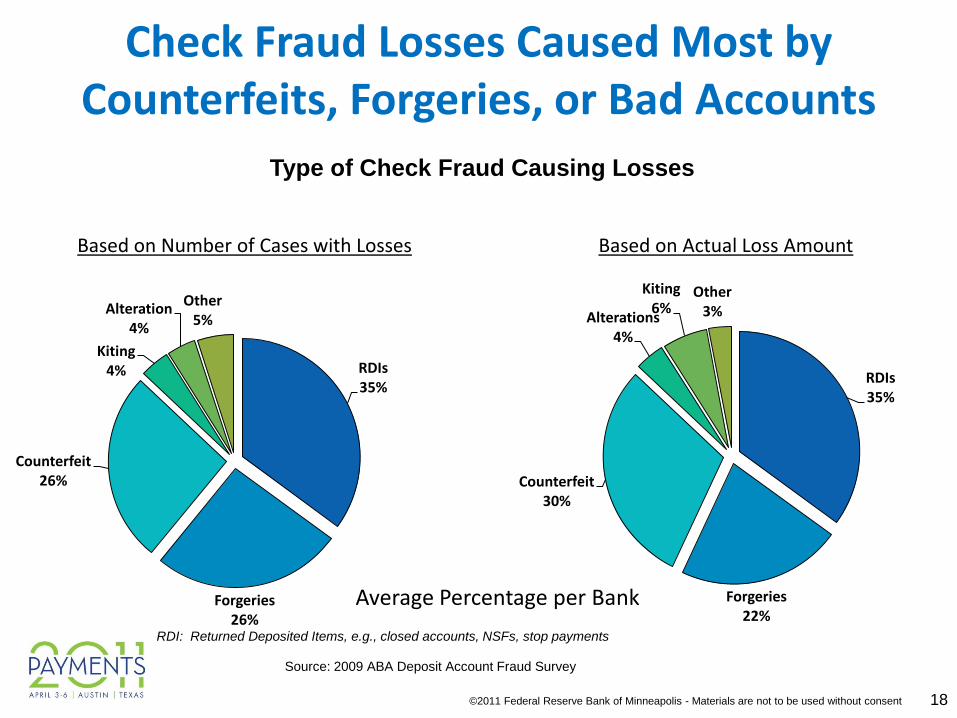

Check Fraud Losses Caused Most by Counterfeits Forgeries or Bad Accounts

RDIs35

Forgeries26

Counterfeit26

Kiting4

Alteration4

Other5

RDIs35

Forgeries22

Counterfeit30

Alterations4

Kiting6

Other3

Based on Number of Cases with Losses Based on Actual Loss Amount

Average Percentage per Bank

Source 2009 ABA Deposit Account Fraud Survey

18

RDI Returned Deposited Items eg closed accounts NSFs stop payments

Type of Check Fraud Causing Losses

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Why is Check Fraud Persistent amp Widespread

Low risk crime

Low barriers amp costs to entry

Account amp other information needed is accessible

Attributes of paper facilitate fraud

Remote deposit capture (RDC) may increase aspects of fraud risk Check alterations forged or missing endorsements amp counterfeits may be

harder to detect

Certain check security features may be lost through imaging process

Certain physical alterations such as check ldquowashingrdquo may be obscured by imaging process

Insider fraud potential may increase as customer employees are not subject to FI screeningmdasheg presenting checks more than once stealing personal information on checks

Use of RDC by foreign correspondent banks amp services may raise money laundering risks

19

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Best Ways to Mitigate Check Fraud Risk

Institute positive pay Require signature verification Reconcile accounts daily Consider using image-survivable check security

features egmodulus check serial numbersreference numbers encrypted check data (eg payee amount) printed on

check

Secure check stock amp implement dual control around key treasury functions

20

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

ACH Fraud

21

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

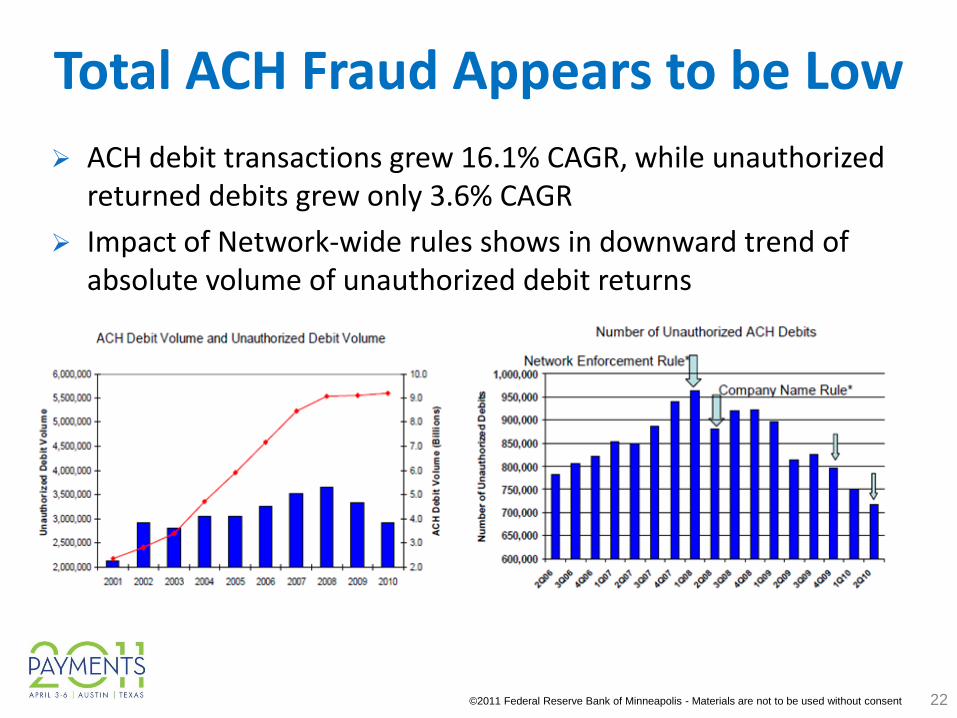

Total ACH Fraud Appears to be Low

22

ACH debit transactions grew 161 CAGR while unauthorized returned debits grew only 36 CAGR

Impact of Network-wide rules shows in downward trend of absolute volume of unauthorized debit returns

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

But ACH Fraud Remains a Concern of Corporates

On a scale of 1 ndash 5 with 5 = Very Important corporations have high degree of concern about ACH debit fraud

ACH fraud that affects corporations

Unauthorized debits to accounts

ACH kiting

Invalid debit originationCounterfeit ACH

Fraudulent claims of unauthorized debits

Insider origination fraud

Corporate account takeovers that issue fraudulent ACH payments

23

Source Phoenix Hecht 2010 Report to Treasury Management Monitor Respondents

Middle Market Large Corporate

Fraud Concern 2009 2010 2009 2010

ACH Debits 406 403 424 412

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

ACH Origination Fraud

24

Source 2010 AFP Payment Fraud amp Control Survey

68

108

3

12

61

8

13

5

13

75

11

0 0

14

0

10

20

30

40

50

60

70

80

1-5 6-10 11-15 16-20 gt 20

Number of Attempts

Corporate ACH Fraud

All Respondents (Median = 3)

Revenues gt $1 B (Median = 4)

Revenues lt $1 B (Median = 3)

ACH Fraud Resulting in

Financial Loss

All Respondents 11

Revenues gt $1 B 9

Revenues lt $1 B 18

33 of middle market

corporations amp 102 of

large corporations report

a major ACH fraud issue

in past two years

Source 2010 AFP Payment Fraud amp Control Survey

2011 Phoenix Hecht After the Financial Crisis

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

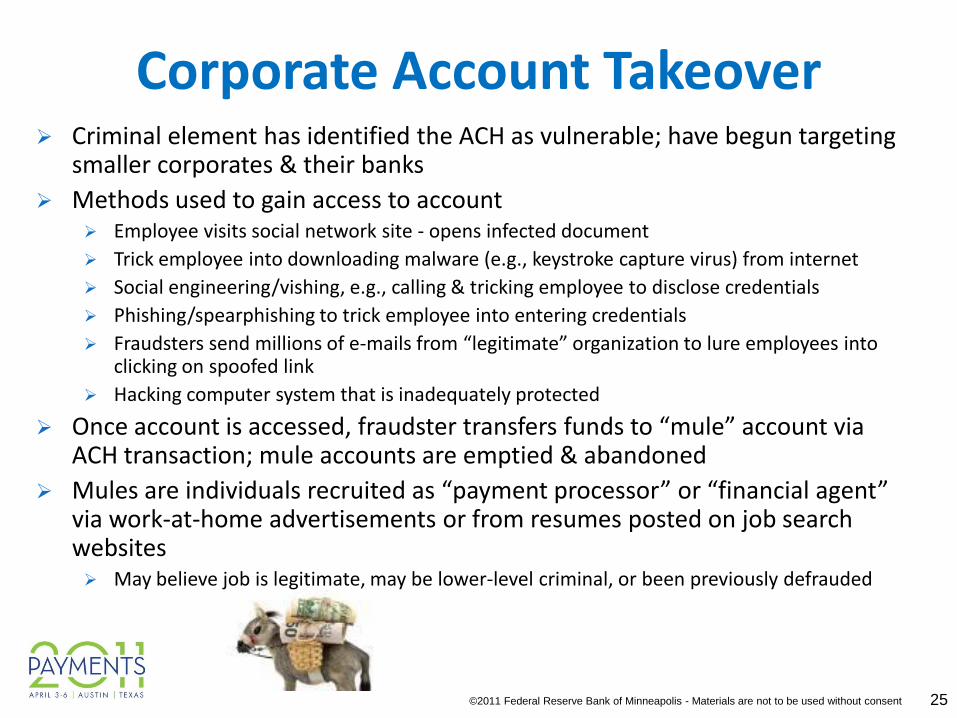

Corporate Account Takeover Criminal element has identified the ACH as vulnerable have begun targeting

smaller corporates amp their banks

Methods used to gain access to account Employee visits social network site - opens infected document

Trick employee into downloading malware (eg keystroke capture virus) from internet

Social engineeringvishing eg calling amp tricking employee to disclose credentials

Phishingspearphishing to trick employee into entering credentials

Fraudsters send millions of e-mails from ldquolegitimaterdquo organization to lure employees into clicking on spoofed link

Hacking computer system that is inadequately protected

Once account is accessed fraudster transfers funds to ldquomulerdquo account via ACH transaction mule accounts are emptied amp abandoned

Mules are individuals recruited as ldquopayment processorrdquo or ldquofinancial agentrdquo via work-at-home advertisements or from resumes posted on job search websites May believe job is legitimate may be lower-level criminal or been previously defrauded

25

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Best Ways to Mitigate ACH Fraud Risk

26

Implement best practices for online amp IT data security authenticating customers amp initiating payments

Use ACH Positive Pay debit blocks amp filters as appropriate

Implement proactive detection amp monitoring Develop amp use files of known fraudulent recipients

eg develop blacklists Reconcile accounts daily amp make timely returns Retain rights of refusal Require due diligence of 3rd party processors Educate customers amp employees on fraud amp how to

report

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Card Fraud

27

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Card Fraud Losses

28

2009 card fraud losses estimated at $689 billion a 7 increase from 2008 (Pulse) 20 respondents experienced consumer creditdebit card

fraud 17 experienced corporatecommercial purchasing card fraud

Signature debit card fraud increased 43 PIN debit fraud loss rose by 24 Credit card fraud affected 65 million victims Debit card fraud affected 35 million victims

Source 2010 AFP Payments Fraud amp Control Study Pulse 2010 Debit Issuer Study

Payment Type Costs ($B)

Losses by online retailer due to credit card fraud $36

Losses by brick-and-mortar retailer due to debit amp credit card fraud $20

Cost of compliance with debit amp credit card security eg PCI $20 ndash $55

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

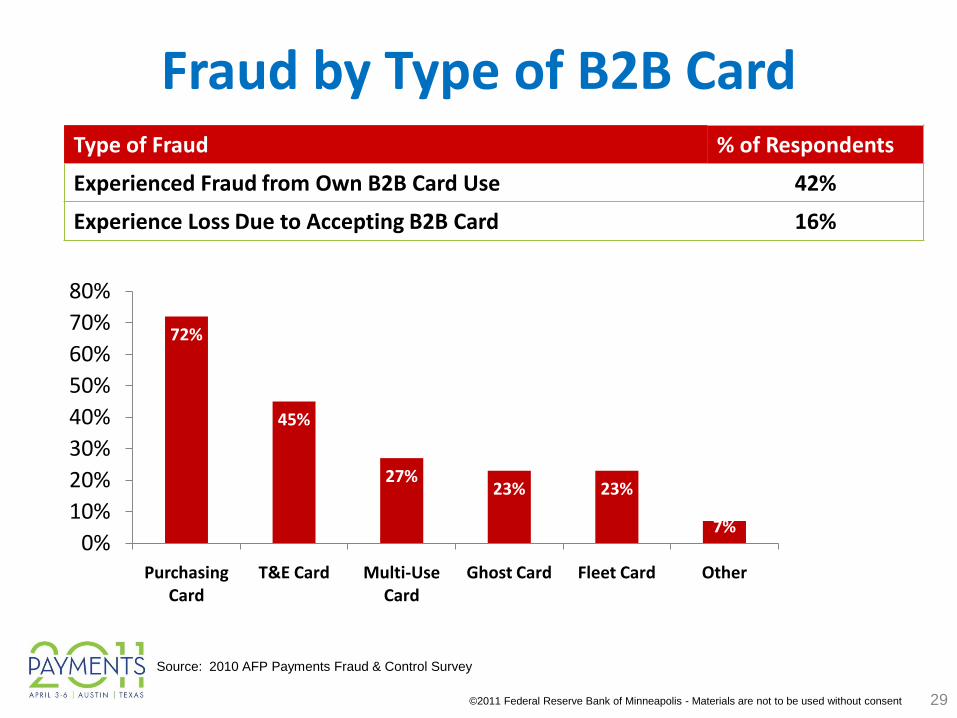

Fraud by Type of B2B Card

72

45

2723 23

70

10

20

30

40

50

60

70

80

Purchasing Card

TampE Card Multi-Use Card

Ghost Card Fleet Card Other

29

Source 2010 AFP Payments Fraud amp Control Survey

Type of Fraud of Respondents

Experienced Fraud from Own B2B Card Use 42

Experience Loss Due to Accepting B2B Card 16

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Stolen amp Counterfeit Cards Are Main Sources of Debit Fraud Losses

Signature Debit Fraud Losses

Account Takover

3

Stolen Card 21

Lost Card 9

Counterfeit 37

e-Commerce amp MOTO

25

Other 5

PIN Debit Fraud LossesAccount

Takeover 7

Stolen Card 45

Lost Card 7

Counterfeit 23

e-Commerce amp MOTO

6Other 12

30

Source ABA Deposit Account Fraud Survey Report - 2009

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Best Ways to Mitigate Card Fraud Risk

Use intelligent fraud prevention amp detection systems to identify high-risk transactions

Validate compliance with PCI standards Use real-time authorization amp address verification

systems Use check card verification codes amp secure payment

services for card-not-present acceptance Respond immediately to fraud amp chargeback issues Implement programs amp protective controls to prevent

misuse of corporate payment cards by employees Set transaction limits amp block unauthorized vendors Use payment tools that provide real-time spend visibility

amp detailed reporting

31

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Impact of Cyberspace on Payments Fraud

32

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Main Effects of Cyberspace on Payments Fraud

Another environment for direct payments fraudmdasheg fraudulent payment used to buy goodsservices online

Facilitates cyber crimes central to committing other types of payments fraud later

Stolen data used to make purchasesmdash40 in-person amp 37 online (Javelin 2009 Identity Fraud Survey Report)

Increases velocity of payments fraud

33

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Cyberspace Crime Lowers the Cost of Payments Fraud

Source RSA Security Survey September 2010

Estimated cost of buying information amp services online to perpetrate fraud

34

Cost on Black Market Estimate (2010)

Credit Card $150 - $300

SSN amp Date of Birth (DOB) $150 - $300

Full data setCredit card CVV2 code expiration date username amp password address SSN DOB

$5 - $20

Online Banking AccountDepends on account type amp balance

$50 - $1000

Denial of Service Attack $50 for 24 hours tosingle target

Zeus Trojan Virus Kit $3000 - $4000

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Phishing Activity Targets by Industry

35

APWG Phishing Activity Trends Report 2nd Q 2010

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Fraud Prevention

36

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Fraud Detection More Is Needed

76

4841

26 23

0

10

20

30

40

50

60

70

80

90

100

Customer Notifies Us At the Point of transaction

Third-Party Notification

At the Point of Origination

During Account AuditReconciliation

When is Fraud Usually Detected

37

Source Information Security Media Group 2010 Faces of Fraud Survey

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Education amp Technology Most Used to Detect amp Prevent Fraud

77

6758

45

28

0

10

20

30

40

50

60

70

80

90

Employee Education Customer Awareness Fraud Tools amp Technologies

Real-Time Decision Tools

Manual Account Monitoring

Most Effective Fraud Prevention Tools

38

Source Information Security Media Group 2010 Faces of Fraud Survey

Internal controls are central to fraud prevention

Top 3 internal controls considered effective

Authenticationauthorization for payment processes

Dual controls amp separation of duties

Audit amp management review to verify controls are applied

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Use amp Effectiveness of Risk Services by Corporations

Corporate Views on Risk Services Used amp Effectiveness

39

16 Use

22 Use

23 Use

28 Use

29 Use

36 Use

42 Use

49 Use

49 Use

51 Use

57 Use

71 Use

Account masking services

Post no check services

ACH payee positive pay

ACH positive pay

Card alert services for corp cards

Account alert services

Check payee positive pay

Multi-factor authentication to initiate payments

ACH debit filters

Check positive payreverse positive pay

ACH debit blocks

Online information services

Use amp very effective

Use amp somewhat effective

Use amp somewhat ineffective

Use amp very ineffective

Plan to use win 12 to 24 months

Source Federal Reserve Bank of Minneapolis 2010 Payments Fraud Survey Summary of Results

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Use amp Effectiveness of Internal Controls by Corporations

40

8 Use

8 Use

8 Use

11 Use

16 Use

18 Use

22 Use

32 Use

37 Use

44 Use

57 Use

65 Use

Magnetic stripe or card chip authentication

Biometrics authentication

Participate in fraudster databases amp alerts

Centralized fraud database for multiple pymt types

Centralized fraud database for one pymt type

Verify customer state ID card is authentic

Software wpattern matching or other indicators

Fraud detection pen for currency

Positive ID of purchaser or account for POS trx

Centralized risk management department

Customer authentication for online transactions

Human review of payment transactions

Use amp very effective

Use amp somewhat effective

Use amp somewhat ineffective

Use amp very ineffective

Plan to use win 12 to 24 months

Source Federal Reserve Bank of Minneapolis 2010 Payments Fraud Survey Summary of Results

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

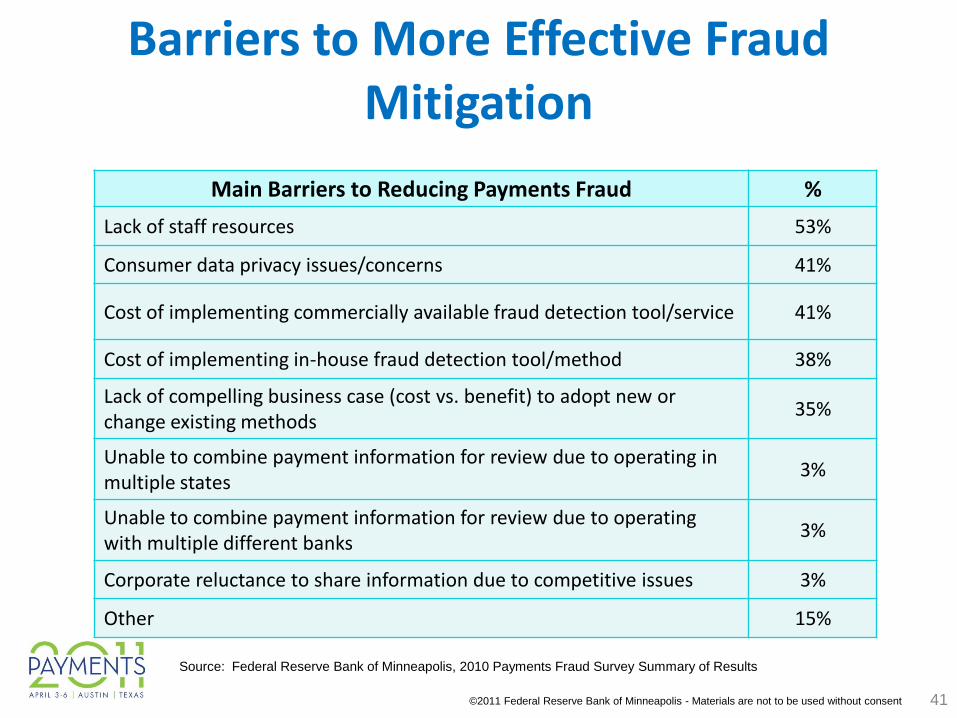

Barriers to More Effective Fraud Mitigation

Main Barriers to Reducing Payments Fraud

Lack of staff resources 53

Consumer data privacy issuesconcerns 41

Cost of implementing commercially available fraud detection toolservice 41

Cost of implementing in-house fraud detection toolmethod 38

Lack of compelling business case (cost vs benefit) to adopt new or change existing methods

35

Unable to combine payment information for review due to operating in multiple states

3

Unable to combine payment information for review due to operating with multiple different banks

3

Corporate reluctance to share information due to competitive issues 3

Other 15

41

Source Federal Reserve Bank of Minneapolis 2010 Payments Fraud Survey Summary of Results

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Conclusions

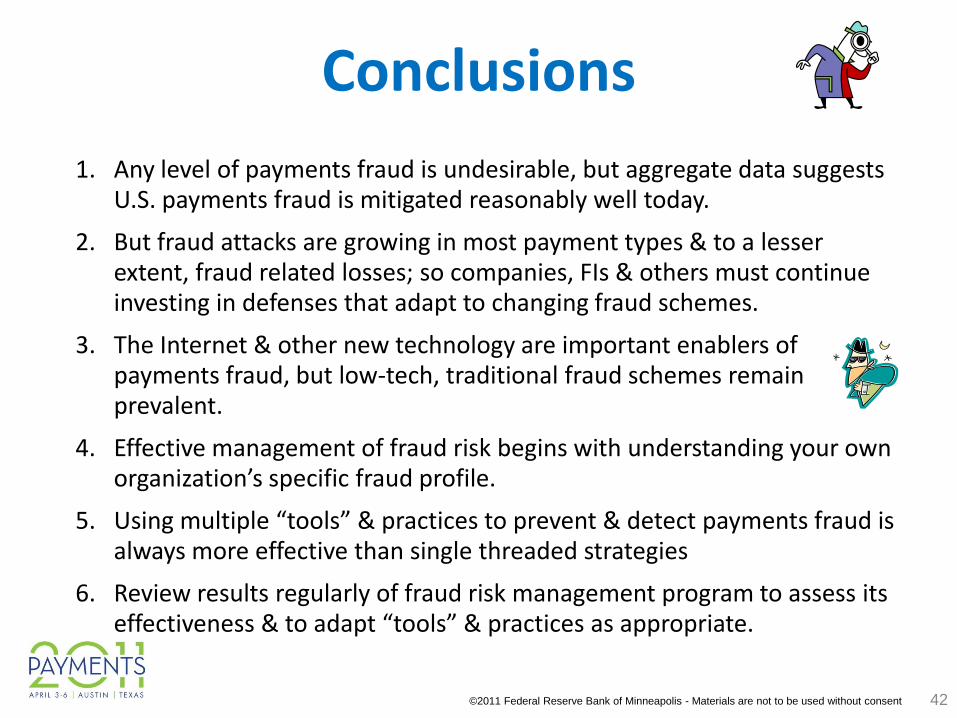

1 Any level of payments fraud is undesirable but aggregate data suggests US payments fraud is mitigated reasonably well today

2 But fraud attacks are growing in most payment types amp to a lesser extent fraud related losses so companies FIs amp others must continue investing in defenses that adapt to changing fraud schemes

3 The Internet amp other new technology are important enablers of payments fraud but low-tech traditional fraud schemes remain prevalent

4 Effective management of fraud risk begins with understanding your own organizationrsquos specific fraud profile

5 Using multiple ldquotoolsrdquo amp practices to prevent amp detect payments fraud is always more effective than single threaded strategies

6 Review results regularly of fraud risk management program to assess its effectiveness amp to adapt ldquotoolsrdquo amp practices as appropriate

42

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Questions

43

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Contact Information

44

Brad LarsonVice President Global TreasurerClaires Stores847-765-3144bradlarsonclairescom

Terry CrawfordSenior Vice President amp TreasurerAMC Entertainment Inc816-489-4690tcrawfordamctheatrescom

Jerl RossiCorporate Director Treasury OperationsNorthrop Grumman Corporation310-556-4523jerlrossingccom

Claudia Swendseid Senior Vice PresidentFederal Reserve Bank of Minneapolis612-204-5448claudiaswendseidmplsfrborgwwwfrbservicesorg

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Resources

Industry Linksbull American Bankers Association wwwabacombull Association for Financial Professionals wwwafponlineorgbull Bank Administration Institute wwwbaiorgbull BITS wwwbitsinfoorgbull Credit Union National Association wwwcunaorgbull Board of Governors of the Federal Reserve System wwwfederalreservegovbull Electronic Check Clearing House Organization (ECCHO) wwwecchocombull Federal Financial Institutions Examination Councils (FFIEC) wwwffiecgovbull Federal Reserve Financial Services wwwfrbservicesorgbull Independent Community Bankers of America wwwicbaorgbull National Automated Clearing House Association wwwnachaorgbull National Association of Federal Credit Unions wwwnafcunetorgbull X9 Financial Industry Standards wwwx9org

45

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Online Sales amp Revenue Lost to Fraud

15 17 21 19 26 28 31 37 4 33 27

417

531

724

1118

1444

1750

2214

2643

28572750

3000

0

50

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Total e-commerce Revenue Lost to Fraud

In $Billions

46

Source Cybersource 2011 Online Fraud Report

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Relative Losses Declining Among Online Retail Sites

36

32

29

1718

16

14 14 14

12

09

00

05

10

15

20

25

30

35

40

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Revenue Lost to Online Fraud$15

$17

$21

$19$26

$28$31 $40

$33

47

Source Cybersource 2011 Online Fraud Report

$37

$27

Revenue lost as a percentage of total online sales amp total online fraud losses ($ billions)

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent 48

Payment

Type

Subtype

(Fraud Type)Consumer Protection Legal Authority

Who is liable if cannot

recover against fraudster or

merchant

Legal Authority

ACH

Credit Items (PPD) $0

Consumer not liable if report

fraud within 60 days after

receiving statement

Reg E 12 CFR 2056(b)(3) Originating Depository Financial

Institution (ldquoODFIrdquo) is liable for

breach of warranty that item is

authorized

Credit Items can be returned at

any time

The ODFI warranty

is set forth in

NACHA OR 2211

Liability for breach

of warranty is set

forth in NACHA

223

Return deadline for

credit items is set

forth in NACHA OR

614

Debit Items

(ARC BOC IAT POP and

RCK have similar recredit

rights pursuant to

NACHA OR Sections 862

through 865)1

$0

Consumer not liable if report

fraud within 60 days after

receiving statement

Reg E 12 CFR 2056(b)(3) ODFI is liable for breach of

warranty that item is authorized

ODFI must accept the return of

unauthorized items that the RDFI2

returns within 60 days after the

settlement date

Separate warranty claims can be

brought after the 60-day period

outside of the ACH network

The ODFI warranty

is set forth in

NACHA OR 2211

NACHA OR3 Section 861

Consumer has right of immediate

recredit if notifies bank within 15

days after receiving statement

Liability for breach

of warranty is set

forth in NACHA

223

Return deadline for

debit items is set

forth in NACHA OG4

102 103

Appendix A Payments Fraud Liability Matrix Disclaimer This appendix is for informational purposes only The information dates to January 2010 amp may no longer be entirely current It does not constitute legal advice Consult an attorney about a particular case problem or question

1 ARC means lockbox items pursuant to NACHA OR 37 POP means Point of Purchase conversion items pursuant to NACHA OR 38 BOC

refers to Back Office Conversion items Re-presented check entries (RCK) which means items that are collected via ACH after the original

paper check has been dishonored are not covered by Reg E as it specifically excludes items that were first originated by a check 2 Receiving Depository Financial Institution 3 NACHA Operating Rules (2009) 4 NACHA Operating Guidelines (2009) The number

following OG refers to the page number

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent 49

Payment

Type

Subtype

(Fraud Type) Consumer Protection Legal Authority

Who is liable if cannot

recover against fraudster or

merchant

Legal Authority

Check5

Forged (counterfeit)

check

$0

Consumer not liable as the check

is not properly payable which

means that it was not authorized

or not in accordance with any

agreement

UCC 4-401 If check is not

properly payable the depository

bank must not charge or is

required to recredit the amount

of the fraudulent check

Paying bank is liable as there is no

breach of presentment warranty

Presentment

warranties are set

forth in UCC 3-417

and 4-208

Forged drawerrsquos

signature

$0

Consumer not liable as the check

is not properly payable which

means that it was not authorized

or not in accordance with any

agreement

UCC 4-401 If check is not

properly payable the depository

bank must not charge or is

required to recredit the amount

of the fraudulent check

Paying bank is liable as there is no

breach of presentment warranty

Presentment

warranties are set

forth in UCC 3-417

and 4-208

Possible exception if consumerrsquos

negligence substantially

contributed to the forged

signature or if consumerrsquos failure

to timely report forgery

UCC 3-406 drawerrsquos negligence

UCC 4-406 drawerrsquos failure to

report

Forged endorsement $0

Consumer not liable as check is

not properly payable which

means that it was not authorized

or not in accordance with any

agreement

UCC 4-401 If check is not

properly payable the depository

bank must not charge or is

required to recredit amount of

the fraudulent check

Depository bank is liable as there

is breach of transfer or

presentment warranties

Presentment

warranties are set

forth in UCC 3-417

and 4-208

Transfer warranties

are set forth in UCC

3-416 and 4-207

5These protections also apply to business checks

Appendix A Payments Fraud Liability Matrix Disclaimer This appendix is for informational purposes only The information dates to January 2010 amp may no longer be entirely current It does not constitute legal advice Consult an attorney about a particular case problem or question

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent 50

Payment

Type

Subtype

(Fraud Type) Consumer Protection Legal Authority

Who is liable if cannot

recover against fraudster

or merchant

Legal Authority

Check

Fraudulent Alteration $0

Consumer not liable as check is

not properly payable which

means that it was not authorized

or not in accordance with any

agreement

UCC 3-407 UCC 4-401 If check

is not properly payable the

depository bank must not charge

or is required to recredit amount

of fraudulent check

Depository bank is liable as there

is breach of transfer or

presentment warranties

Presentment

warranties are set

forth in UCC 3-417

and 4-208

Transfer

warranties are set

forth in UCC 3-416

and 4-207

Possible exception if consumerrsquos

negligence substantially

contributed to the forged

signature or if consumer failed to

timely report the forgery

UCC 3-406 drawerrsquos negligence

UCC 4-406 drawerrsquos failure to

report

Remotely Created

Checks

$0

Consumer not liable as check is

not properly payable which

means that it was not authorized

or not in accordance with any

agreement

UCC 4-401 If check is not

properly payable the depository

bank must not charge or is

required to recredit amount of

the fraudulent check

Depository bank is liable for all

kinds of fraud for remotely

created checks

Reg CC 12 CFR

22934 contains

transfer and

presentment

warranties for

remotely created

checks in which

depository bank

warrants that the

check is authorized

Appendix A Payments Fraud Liability Matrix Disclaimer This appendix is for informational purposes only The information dates to January 2010 amp may no longer be entirely current It does not constitute legal advice Consult an attorney about a particular case problem or question

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent 51

Payment

Type

Subtype

(Fraud Type)Consumer Protection Legal Authority

Who is liable if cannot

recover against fraudster or

merchant

Legal Authority

Credit Cards

Card Present

(signature or Pin

required)

$50

The consumerrsquos maximum liability

under federal law is $50 for

unauthorized use

Truth in Lending Act (ldquoTILArdquo) 15

USC 1643(a) and Reg Z 12 CFR

22612(b)

The Issuing Bank is generally

liable for fraudulent transactions

VISA and

MasterCard Rules6

$0

The consumer has no liability for

unauthorized use under VISA

MasterCard consumer policies

provided that the consumer has

taken reasonable measures to

protect the card and has not

acted negligently in failing to

report the loss timely

VISA MasterCard websites

Card not present

(telephone or web

initiated use)

$50

The consumerrsquos maximum liability

under federal law is $50 for

unauthorized use

Truth in Lending Act (ldquoTILArdquo) 15

USC 1643(a) and Reg Z 12 CFR

22612(b)

The Acquiring Bank is generally

liable for fraudulent transactions

if the Acquirer is not able to pass

the liability on to the merchant

pursuant to the merchant

agreement

VISA and

MasterCard Rules

$0

The consumer has no liability for

unauthorized use under VISA

MasterCard consumer policies

provided that the consumer has

taken reasonable measures to

protect the card and has not

acted negligently in failing to

report the loss timely

VISA MasterCard websites

Appendix A Payments Fraud Liability Matrix Disclaimer This appendix is for informational purposes only The information dates to January 2010 amp may no longer be entirely current It does not constitute legal advice Consult an attorney about a particular case problem or question

6The VISA and MasterCard network rules apply only between the Issuing Bank (the bank that issues cards to cardholders) and the Acquiring Bank (the bank that has the relationship with the merchant) These rules are not public and the legal authority is derived from statements made by VISA and MasterCard in litigation and from other secondary sources

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent 52

Payment

Type

Subtype

(Fraud Type) Consumer Protection Legal Authority

Who is liable if cannot

recover against fraudster or

merchant

Legal Authority

Debit Cards

Card Present (signature

or PIN required)

$0

The consumer has no liability for

unauthorized use under VISA

MasterCard consumer policies

provided that the consumer has

taken reasonable measures to

protect the card or has acted

negligently in failing to report the

loss timely

VISA MasterCard websites The Issuing Bank is generally liable

for fraudulent transactions if

merchant has obtained signature

or required use of PIN

VISA and

MasterCard Rules

Up to $50

If the consumer provides notice

within two business days after

learning of the loss of the debit

card

Reg E 12 CFR 2056(b)(1)

Up to $500

of unauthorized transfers incurred

after the close of the two business

day timeframe and until consumer

actually provides notice

Reg E 12 CFR 2056(b)(2)

Unlimited consumer liability for

transactions occurring in the

period starting 60 days after the

consumerrsquos receipt of the

statement and until notice is

provided

Reg E 12 CFR 2056(b)(3)

Appendix A Payments Fraud Liability Matrix Disclaimer This appendix is for informational purposes only The information dates to January 2010 amp may no longer be entirely current It does not constitute legal advice Consult an attorney about a particular case problem or question

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent 53

Payment

Type

Subtype

(Fraud Type)Consumer Protection Legal Authority

Who is liable if cannot

recover against fraudster or

merchant

Legal Authority

Debit Cards

Card not Present

(telephone or web

initiated use)

$0

The consumer has no liability for

unauthorized use under VISA

MasterCard consumer policies

provided that the consumer has

taken reasonable measures to

protect the card or has acted

negligently in failing to report the

loss timely

VISA MasterCard websites The Acquiring Bank is generally

liable for fraudulent transactions if

the Acquirer is not able to pass the

liability on to the merchant

pursuant to the merchant

agreement

Secondary Sources7

Reg E 12 CFR 2056(b)(1)

Up to $50

If the consumer provides notice

within two business days after

learning of the loss of the debit

card

Up to $500

of unauthorized transfers incurred

after the close of the two business

day timeframe and until consumer

actually provides notice

Reg E 12 CFR 2056(b)(2)

Unlimited consumer liability for

transactions occurring in the

period starting60 days after the

consumerrsquos receipt of the

statement and until notice is

provided

Reg E 12 CFR 2056(b)(3)

Appendix A Payments Fraud Liability Matrix Disclaimer This appendix is for informational purposes only The information dates to January 2010 amp may no longer be entirely current It does not constitute legal advice Consult an attorney about a particular case problem or question

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent 54

Payment

Type

Subtype

(Fraud Type)Consumer Protection Legal Authority

Who is liable if cannot

recover against fraudster or

merchant

Legal Authority

Debit Cards

Decoupled Debit Cards

(Cards issued by

Institution other than

Bank in which consumer

maintains an account

Settlement between

merchant and card issuer

is through branded

payment networks such

as VISAMasterCard

Settlement between Card

issuer and consumer is

via ACH debits to

consumerrsquos bank account)

$0

The consumer has no liability for

unauthorized use under VISA

MasterCard consumer policies

provided that the consumer has

taken reasonable measures to

protect the card or has acted

negligently in failing to report the

loss timely

VISA MasterCard websites Under NACHA Rules the ODFI

which is likely the Card Issuerrsquos

bank is liable for breach of

warranty as described above under

ACH Debits The ODFI is likely to

pass liability to card issuer by

agreement

Under Payment network rules it is

either the Card Issuer or the

Acquiring Bank that is liable

depending on whether it is a card-

present or card not present

situation See above for debit

cards

Up to $50

If the consumer provides notice

within four business days after

learning of the loss of the debit

card

Reg E 12 CFR 20514(b)(5)(V)

Up to $500

of unauthorized transfers incurred

after the close of the four business

day timeframe and until consumer

actually provides notice

Reg E 12 CFR 20146(b)(5)(v)

Unlimited consumer liability for

transactions occurring in the

period starting 90 days after the

consumerrsquos receipt of the

statement and until notice is

provided

Reg E 12 CFR 20514(b)(5)(V)

Consumer has right of immediate

recredit under NACHA Rules if

notifies its bank within 15 days

after receiving statement

NACHA OR Section 861

Appendix A Payments Fraud Liability Matrix Disclaimer This appendix is for informational purposes only The information dates to January 2010 amp may no longer be entirely current It does not constitute legal advice Consult an attorney about a particular case problem or question

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

bull Please turn off all cell phones or mobile devicesbull Thank you to todayrsquos sponsors

ndash This morningrsquos Continental Breakfast sponsored by

Javelin

ndash Breakfast Roundtables sponsored by SWACHA

ndash Thought Leadership Spotlight Session sponsored by

Fundtech

ndash Monday Night Celebration sponsored by Fiserv

bull Most of the education sessions at the conference can be counted towards your continuing AAP accreditation If you are interested in becoming an Accredited ACH Professional (AAP) please stop by the NACHA amp RPA booth

bull Please take a moment to complete session evaluations Each evening attendees will receive an email link to access session evaluations that are offered each day Attendees are automatically entered into a daily drawing for a chance to win a $50 gift card

bull Register now for PAYMENTS 2012 ndash Receive the PAYMENTS 2011 Early-Bird Rates ndash Only available onsite ndash Visit the Registration Desk for more details

Thanks to all of our

Track Sponsors

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Agenda

Who We Are

Payment Fraud Trends

Payment Fraud by Instrument

Fraud Prevention

Conclusions

3

Disclaimer The views expressed in this presentation are those of the speakers and do NOT necessarily reflect the views of the organizations for which they work

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Who We Are

Clairersquos amp Payments Consumer payments received by

cash check credit card debit card (signature amp PIN) amp gift cards

Payroll is made by paper check direct deposit ACH and payroll card

B2B payments made by check wire ACH credits ACH debits TampE cards Fleet Cards amp Purchase Cards

B2B payments received by check ACH credits amp wires

4

Clairersquos

Specialty retailer of value-

priced jewelry amp accessories

operating under trade names

Claires amp Icing

Operates over 3000 stores in

approximately 25 countries

through company-owned

joint ventures amp franchises

Global workforce of 16500

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Who We Are

AMC amp Payments Consumer payments received by cash credit

cards debit cards (signature amp PIN) amp gift cards

Credit card volume (over 12 billion per year) is about 55 of total revenue PCI DSS ldquolevel 1rdquo merchant

Payroll is made by paper check direct deposit ACH amp payroll card

B2B payments made by check wire ACH credits ACH debits TampE cards Fleet Cards amp Purchase Cards B2B payments received by check ACH credits wires amp credit cards

5

AMC One of the worldrsquos most innovative amp

largest theatrical exhibition companies 2nd largest US exhibitor

Operates over 380 theatres with over 5325 screens in 30 states the District of Columbia amp 4 countries

Privately held amp headquartered in Kansas City Missouri since its founding in 1920 Employs about 16800 full amp part-time associates

Hundreds of millions of guests attend AMC theatres each year

(Annualized) transactions $(000rsquos)

Wires 300 191677

ACH 400000 1474190

Checks 1110000 927666

Credit Card (receipts)

72782500 1318326

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Who We Are

NOC amp Payments 95 payroll is via direct deposit 5 check

Customer Remittance

Vendor Payments

6

Northop Grumman (NOC) Leading global security company that has

achieved historic accomplishments from transporting Lindbergh across the Atlantic to carrying astronauts to the moon amp back

120000 employees provide systems products amp solutions in aerospace electronics information systems shipbuilding amp technical services to government amp commercial customers worldwide

Conducts business mostly with the US GovernmentDepartment of Defense Other customers include local state amp foreign governments amp domestic amp international commercial companies

In 2009 delivered 6 ships to the US Navy amp Coast Guard amp launched 2 space tracking amp surveillance system satellites

(Annualized) VolumeAmount

($ millions)

Wires 8000 $ 3000

ACH 64000 $ 28000

Checks 35000 $ 300

Credit Card 1258000 $ 22

(Annualized) VolumeAmount

($ millions)

Wires 10000 $ 10100

ACH 700000 $ 16885

Checks 500000 $ 4458

Credit Card 297787 $ 150

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Who We Are

Federal Reserve System Sets amp implements nationrsquos monetary

policy

Supervises amp regulates range of financial institutions amp activities to ensure safe amp sound banking practices

Provides payments services to financial institutions (FIs) amp the federal government

Mission in payments to foster the integrity efficiency amp accessibility of US dollar payments amp settlement systems issue a uniform currency amp act as the fiscal agent amp depository for the US government

Fed amp Payments The Fed clears amp settles a large

portion of US interbank payments

7

Service Average

Volume Daily

AverageValue Daily

Fedwire Funds 494 000 $24 trillion

Fedwire Securities

78000 $12 trillion

FedACH 399 million $654 billion

Check 29 million $414 billion

National Settlement

2100 $55 billion

commercial volume only data through 3rd quarter 2010

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Payment Fraud Defined

Payments focused on today

Check

ACH credits amp debits

Card

Impact of cyberspace on payment fraud

Payments Fraud Definition Fraud that occurs when someone gains

financial or material advantage by using a payment instrument or

information from a payment instrument to complete a transaction that

is not authorized by the legitimate account holder

8

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Accurate Data on Payment Fraud is Limited

No definitive data on total number of payment fraud attacks or amount of losses in US

Practices of FIs companies amp industries to monitor fraud vary

Fraud data collected is often not shared data that is shared is not comparable

Fraud ldquofactsrdquo reported are subject to hype

0

20

40

60

80

100Internally track loss

Internally track loss avoidedPeer benchmarking

Report to Natl Shared Databases

0

20

40

60

80

100

Internally track loss amp loss avoided

Peer benchmarking

of FIs Tracking amp Sharing ATMDebit Card Fraud Data

Chart Data Source ABA 2007 Deposit Account Fraud Survey

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Corporate Fraud Attacks amp Losses

10

Source 2010 AFP Payments Fraud amp Control Survey

Nearly frac34 of corporations

reported payments fraud

attacks in 2009 about 30

suffered losses

Large companies are more

often the target of fraud

small companies more often

suffer losses

Fraud attempts have been

steady since 2006 fraud

losses have declined since

2006

55

6872 71 71 73

17 19

58

37 37

30

0

10

20

30

40

50

60

70

80

90

100

2004 2005 2006 2007 2008 2009

Respondents

Fraud Losses

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Payment Types

Check ACH1 Corporate amp Commercial

Cards2

Consumer Cards

(DbCr)

Subject to Fraud 90

25 Debits 7 Credits

17 20

Financial Loss From Fraud 17 11

43 Own 16 Accepted

NA

Responsible for Greatest Financial Loss

645 Debits1 Credits

8 20

Primary Reason for Loss

Did not use positive pay

services

Did not use debit blocks

filters amp positive pay

Illicit use of own card data amp inadequate

internal controls

NA3

Corporate Fraud by Payment Type

Check fraud most attempted amp most subject to losses consistent trend since 2004

Card fraud losses growing

Main reasons for losses

Internal controls not enforced

Common prevention services not used

AFP 2010 Payments Fraud amp Control Survey

1Includes ACH debits amp credits except as noted2Includes payments made on organizationrsquos own cards amp B2B card payments accepted3NA ndash data not collected in 2010 survey

11

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Top Fraud Schemes Involving Corporatersquos Own Accounts

12

9

9

13

13

16

16

16

19

31

34

34

Telephone initiated payments

Other

Counterfeit currency

Fraudulent checks converted to ACH hellip

Counterfeit or stolen cards used online

Other Internet initiated payments

Fraudulent credentials to defraud accounts

Cash register frauds

Counterfeit or stolen cards used at point-hellip

Altered or forged checks

Counterfeit checks

Source Federal Reserve Bank of Minneapolis 2010 Payments Fraud Survey Summary of Results

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Top Fraud Schemes Involving Payments Accepted

13

9

9

13

13

16

16

16

19

31

34

34

Telephone initiated payments

Other

Counterfeit currency

Fraudulent checks converted to ACH payments

Counterfeit or stolen cards used online

Other Internet initiated payments

Fraudulent credentials to defraud accounts

Cash register frauds

Counterfeit or stolen cards used at point-of-hellip

Altered or forged checks

Counterfeit checks

Source Federal Reserve Bank of Minneapolis 2010 Payments Fraud Survey Summary of Results

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

External Parties Responsible for Most Payments Fraud

Perpetrators of Payments Fraud that Resulted in Financial Loss in 2009

AllRespondents

Revenues gt$1 B

Revenues lt $1 B

Outside Individual (eg check forged stolen card)

87 87 88

Organized Crime Ring 15 15 12

Internal Party 11 12 8

External known party (eg vendor 3rd party service provider trading partner)

8 10 4

Criminal invasion(eg hacked system malware)

4 3 7

Other 4 2 6

Lost or stolen laptop or other devise 2 1 2

14

Source 2010 AFP Payments Fraud amp Control Study

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Comparative Cost of Payments Fraud

Payment Method

Comparative ValueRange

Total DollarValue

Estimated

Loss

Source of Information

Credit Card $07 - $14per$100 purchases

$21 trillion $147 - 294 billion(20072008)

Nilson Report 2008 Javelin 2009 ID Fraud Survey Report

Debit Card ndashPIN

$001 - $028 per$100 purchases

$03 trillion $327 million (2007) Pulse 2008 Debit Issuer Study

Debit Card ndashSignature

$024 - $096 per$100 purchases

$06 trillion $324 million(2007)

Pulse 2008 Debit Issuer Study

Debit Card ndashATM

$025 per $100 value or $025 per transaction

$0579 trillion(58 billion trans)

$145 million(2007)

Pulse 2008 Debit Issuer Study

ACH $023 per $100 value of transactions

$31 trillion $698 billion(20052006)

NACHA 2005 ABA 2006

Check $027 per $100 value of checks paid

$416 trillion $11 billion(2006)

ABA 2006 Nilson Report 2007 FRB Kansas City

Cash $008 per $100 value of cash in circulation

$079 trillion In circulation YE lsquo07

$61 million (2007)

US Secret Service press release March 2008

DATA IS NOT PRECISE INTENDED TO ENABLE GENERAL COMPARISON OF FRAUD ACROSS PAYMENT TYPES

Estimated values For cards aggregate losses were calculated by applying the 2007 average loss rate to the 2006 payment value For check amp ACH the loss range was calculated based on the aggregate loss estimate amp 2006 payment value

Total dollar values reflect 2006 estimates from the 2007 Federal Reserve Payments Study except currency in circulation

15

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Check Fraud

16

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Small Biz Accounts Targeted More by Check Fraud than Larger Biz

2218

5

1216

1 6

4

4

5

1

4

16 95

Community Mid-Sized Regional Money Center All

Target of Check Fraud By Size of Bank amp Account Type

Large Corporation

Middle Market

Small Business

Source 2009 ABA Deposit Account Fraud Survey

17

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Check Fraud Losses Caused Most by Counterfeits Forgeries or Bad Accounts

RDIs35

Forgeries26

Counterfeit26

Kiting4

Alteration4

Other5

RDIs35

Forgeries22

Counterfeit30

Alterations4

Kiting6

Other3

Based on Number of Cases with Losses Based on Actual Loss Amount

Average Percentage per Bank

Source 2009 ABA Deposit Account Fraud Survey

18

RDI Returned Deposited Items eg closed accounts NSFs stop payments

Type of Check Fraud Causing Losses

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Why is Check Fraud Persistent amp Widespread

Low risk crime

Low barriers amp costs to entry

Account amp other information needed is accessible

Attributes of paper facilitate fraud

Remote deposit capture (RDC) may increase aspects of fraud risk Check alterations forged or missing endorsements amp counterfeits may be

harder to detect

Certain check security features may be lost through imaging process

Certain physical alterations such as check ldquowashingrdquo may be obscured by imaging process

Insider fraud potential may increase as customer employees are not subject to FI screeningmdasheg presenting checks more than once stealing personal information on checks

Use of RDC by foreign correspondent banks amp services may raise money laundering risks

19

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Best Ways to Mitigate Check Fraud Risk

Institute positive pay Require signature verification Reconcile accounts daily Consider using image-survivable check security

features egmodulus check serial numbersreference numbers encrypted check data (eg payee amount) printed on

check

Secure check stock amp implement dual control around key treasury functions

20

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

ACH Fraud

21

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Total ACH Fraud Appears to be Low

22

ACH debit transactions grew 161 CAGR while unauthorized returned debits grew only 36 CAGR

Impact of Network-wide rules shows in downward trend of absolute volume of unauthorized debit returns

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

But ACH Fraud Remains a Concern of Corporates

On a scale of 1 ndash 5 with 5 = Very Important corporations have high degree of concern about ACH debit fraud

ACH fraud that affects corporations

Unauthorized debits to accounts

ACH kiting

Invalid debit originationCounterfeit ACH

Fraudulent claims of unauthorized debits

Insider origination fraud

Corporate account takeovers that issue fraudulent ACH payments

23

Source Phoenix Hecht 2010 Report to Treasury Management Monitor Respondents

Middle Market Large Corporate

Fraud Concern 2009 2010 2009 2010

ACH Debits 406 403 424 412

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

ACH Origination Fraud

24

Source 2010 AFP Payment Fraud amp Control Survey

68

108

3

12

61

8

13

5

13

75

11

0 0

14

0

10

20

30

40

50

60

70

80

1-5 6-10 11-15 16-20 gt 20

Number of Attempts

Corporate ACH Fraud

All Respondents (Median = 3)

Revenues gt $1 B (Median = 4)

Revenues lt $1 B (Median = 3)

ACH Fraud Resulting in

Financial Loss

All Respondents 11

Revenues gt $1 B 9

Revenues lt $1 B 18

33 of middle market

corporations amp 102 of

large corporations report

a major ACH fraud issue

in past two years

Source 2010 AFP Payment Fraud amp Control Survey

2011 Phoenix Hecht After the Financial Crisis

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Corporate Account Takeover Criminal element has identified the ACH as vulnerable have begun targeting

smaller corporates amp their banks

Methods used to gain access to account Employee visits social network site - opens infected document

Trick employee into downloading malware (eg keystroke capture virus) from internet

Social engineeringvishing eg calling amp tricking employee to disclose credentials

Phishingspearphishing to trick employee into entering credentials

Fraudsters send millions of e-mails from ldquolegitimaterdquo organization to lure employees into clicking on spoofed link

Hacking computer system that is inadequately protected

Once account is accessed fraudster transfers funds to ldquomulerdquo account via ACH transaction mule accounts are emptied amp abandoned

Mules are individuals recruited as ldquopayment processorrdquo or ldquofinancial agentrdquo via work-at-home advertisements or from resumes posted on job search websites May believe job is legitimate may be lower-level criminal or been previously defrauded

25

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Best Ways to Mitigate ACH Fraud Risk

26

Implement best practices for online amp IT data security authenticating customers amp initiating payments

Use ACH Positive Pay debit blocks amp filters as appropriate

Implement proactive detection amp monitoring Develop amp use files of known fraudulent recipients

eg develop blacklists Reconcile accounts daily amp make timely returns Retain rights of refusal Require due diligence of 3rd party processors Educate customers amp employees on fraud amp how to

report

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Card Fraud

27

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Card Fraud Losses

28

2009 card fraud losses estimated at $689 billion a 7 increase from 2008 (Pulse) 20 respondents experienced consumer creditdebit card

fraud 17 experienced corporatecommercial purchasing card fraud

Signature debit card fraud increased 43 PIN debit fraud loss rose by 24 Credit card fraud affected 65 million victims Debit card fraud affected 35 million victims

Source 2010 AFP Payments Fraud amp Control Study Pulse 2010 Debit Issuer Study

Payment Type Costs ($B)

Losses by online retailer due to credit card fraud $36

Losses by brick-and-mortar retailer due to debit amp credit card fraud $20

Cost of compliance with debit amp credit card security eg PCI $20 ndash $55

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Fraud by Type of B2B Card

72

45

2723 23

70

10

20

30

40

50

60

70

80

Purchasing Card

TampE Card Multi-Use Card

Ghost Card Fleet Card Other

29

Source 2010 AFP Payments Fraud amp Control Survey

Type of Fraud of Respondents

Experienced Fraud from Own B2B Card Use 42

Experience Loss Due to Accepting B2B Card 16

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Stolen amp Counterfeit Cards Are Main Sources of Debit Fraud Losses

Signature Debit Fraud Losses

Account Takover

3

Stolen Card 21

Lost Card 9

Counterfeit 37

e-Commerce amp MOTO

25

Other 5

PIN Debit Fraud LossesAccount

Takeover 7

Stolen Card 45

Lost Card 7

Counterfeit 23

e-Commerce amp MOTO

6Other 12

30

Source ABA Deposit Account Fraud Survey Report - 2009

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Best Ways to Mitigate Card Fraud Risk

Use intelligent fraud prevention amp detection systems to identify high-risk transactions

Validate compliance with PCI standards Use real-time authorization amp address verification

systems Use check card verification codes amp secure payment

services for card-not-present acceptance Respond immediately to fraud amp chargeback issues Implement programs amp protective controls to prevent

misuse of corporate payment cards by employees Set transaction limits amp block unauthorized vendors Use payment tools that provide real-time spend visibility

amp detailed reporting

31

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Impact of Cyberspace on Payments Fraud

32

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Main Effects of Cyberspace on Payments Fraud

Another environment for direct payments fraudmdasheg fraudulent payment used to buy goodsservices online

Facilitates cyber crimes central to committing other types of payments fraud later

Stolen data used to make purchasesmdash40 in-person amp 37 online (Javelin 2009 Identity Fraud Survey Report)

Increases velocity of payments fraud

33

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Cyberspace Crime Lowers the Cost of Payments Fraud

Source RSA Security Survey September 2010

Estimated cost of buying information amp services online to perpetrate fraud

34

Cost on Black Market Estimate (2010)

Credit Card $150 - $300

SSN amp Date of Birth (DOB) $150 - $300

Full data setCredit card CVV2 code expiration date username amp password address SSN DOB

$5 - $20

Online Banking AccountDepends on account type amp balance

$50 - $1000

Denial of Service Attack $50 for 24 hours tosingle target

Zeus Trojan Virus Kit $3000 - $4000

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Phishing Activity Targets by Industry

35

APWG Phishing Activity Trends Report 2nd Q 2010

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Fraud Prevention

36

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Fraud Detection More Is Needed

76

4841

26 23

0

10

20

30

40

50

60

70

80

90

100

Customer Notifies Us At the Point of transaction

Third-Party Notification

At the Point of Origination

During Account AuditReconciliation

When is Fraud Usually Detected

37

Source Information Security Media Group 2010 Faces of Fraud Survey

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Education amp Technology Most Used to Detect amp Prevent Fraud

77

6758

45

28

0

10

20

30

40

50

60

70

80

90

Employee Education Customer Awareness Fraud Tools amp Technologies

Real-Time Decision Tools

Manual Account Monitoring

Most Effective Fraud Prevention Tools

38

Source Information Security Media Group 2010 Faces of Fraud Survey

Internal controls are central to fraud prevention

Top 3 internal controls considered effective

Authenticationauthorization for payment processes

Dual controls amp separation of duties

Audit amp management review to verify controls are applied

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Use amp Effectiveness of Risk Services by Corporations

Corporate Views on Risk Services Used amp Effectiveness

39

16 Use

22 Use

23 Use

28 Use

29 Use

36 Use

42 Use

49 Use

49 Use

51 Use

57 Use

71 Use

Account masking services

Post no check services

ACH payee positive pay

ACH positive pay

Card alert services for corp cards

Account alert services

Check payee positive pay

Multi-factor authentication to initiate payments

ACH debit filters

Check positive payreverse positive pay

ACH debit blocks

Online information services

Use amp very effective

Use amp somewhat effective

Use amp somewhat ineffective

Use amp very ineffective

Plan to use win 12 to 24 months

Source Federal Reserve Bank of Minneapolis 2010 Payments Fraud Survey Summary of Results

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Use amp Effectiveness of Internal Controls by Corporations

40

8 Use

8 Use

8 Use

11 Use

16 Use

18 Use

22 Use

32 Use

37 Use

44 Use

57 Use

65 Use

Magnetic stripe or card chip authentication

Biometrics authentication

Participate in fraudster databases amp alerts

Centralized fraud database for multiple pymt types

Centralized fraud database for one pymt type

Verify customer state ID card is authentic

Software wpattern matching or other indicators

Fraud detection pen for currency

Positive ID of purchaser or account for POS trx

Centralized risk management department

Customer authentication for online transactions

Human review of payment transactions

Use amp very effective

Use amp somewhat effective

Use amp somewhat ineffective

Use amp very ineffective

Plan to use win 12 to 24 months

Source Federal Reserve Bank of Minneapolis 2010 Payments Fraud Survey Summary of Results

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Barriers to More Effective Fraud Mitigation

Main Barriers to Reducing Payments Fraud

Lack of staff resources 53

Consumer data privacy issuesconcerns 41

Cost of implementing commercially available fraud detection toolservice 41

Cost of implementing in-house fraud detection toolmethod 38

Lack of compelling business case (cost vs benefit) to adopt new or change existing methods

35

Unable to combine payment information for review due to operating in multiple states

3

Unable to combine payment information for review due to operating with multiple different banks

3

Corporate reluctance to share information due to competitive issues 3

Other 15

41

Source Federal Reserve Bank of Minneapolis 2010 Payments Fraud Survey Summary of Results

copy2011 Federal Reserve Bank of Minneapolis - Materials are not to be used without consent

Conclusions

1 Any level of payments fraud is undesirable but aggregate data suggests US payments fraud is mitigated reasonably well today

2 But fraud attacks are growing in most payment types amp to a lesser extent fraud related losses so companies FIs amp others must continue investing in defenses that adapt to changing fraud schemes

3 The Internet amp other new technology are important enablers of payments fraud but low-tech traditional fraud schemes remain prevalent