opportunities and challenges in the manganese alloy...

TRANSCRIPT

Opportunities and challenges in the manganese alloy industry

Kevin FowkesManaging Consultant

Metal Bulletin 14th Asian Ferroalloys Conference

Hong Kong, 27th March 2012

1. Brief overview of recent developments in Mn alloy markets

2. Focus on India

3. Focus on Mn metal

Structure

1. Brief overview of recent developments in Mn alloy markets

2. Focus on India

3. Focus on Mn metal

Structure

• Manganese is the world’s fourth most heavily consumed metal

• Global mine output of 16 million Mn units in 2012 – over 90% goes into steel

• All steels contain manganese

• Manganese is used to remove sulphur from liquid steel(sulphur causes steel to crack)

What is manganese?

(sulphur causes steel to crack)

• There is no viable substitute for manganese as a de-sulphuriser

• Manganese is also used to improve the strength of certain steels(structural steels, high strength flat steels)

• Non-steel consumption of manganese includes de-polarisation of dry-cell batteries, and as an additive in certain aluminium and copper alloys

10

12

14

16

18

Global consumption of Mn alloys(million tonnes, gross weight basis)

HC FeMn

MLC FeMn

11%

9%

25%

Global demand for Mn alloys rose in 2012, despite a generally poor year.Long-term trend has been towards SiMn, away from HC FeMn

Mn metal

17.4

9%

8%

0

2

4

6

8

10

SiMn

48%

58%

9%

41%

8.1

9%

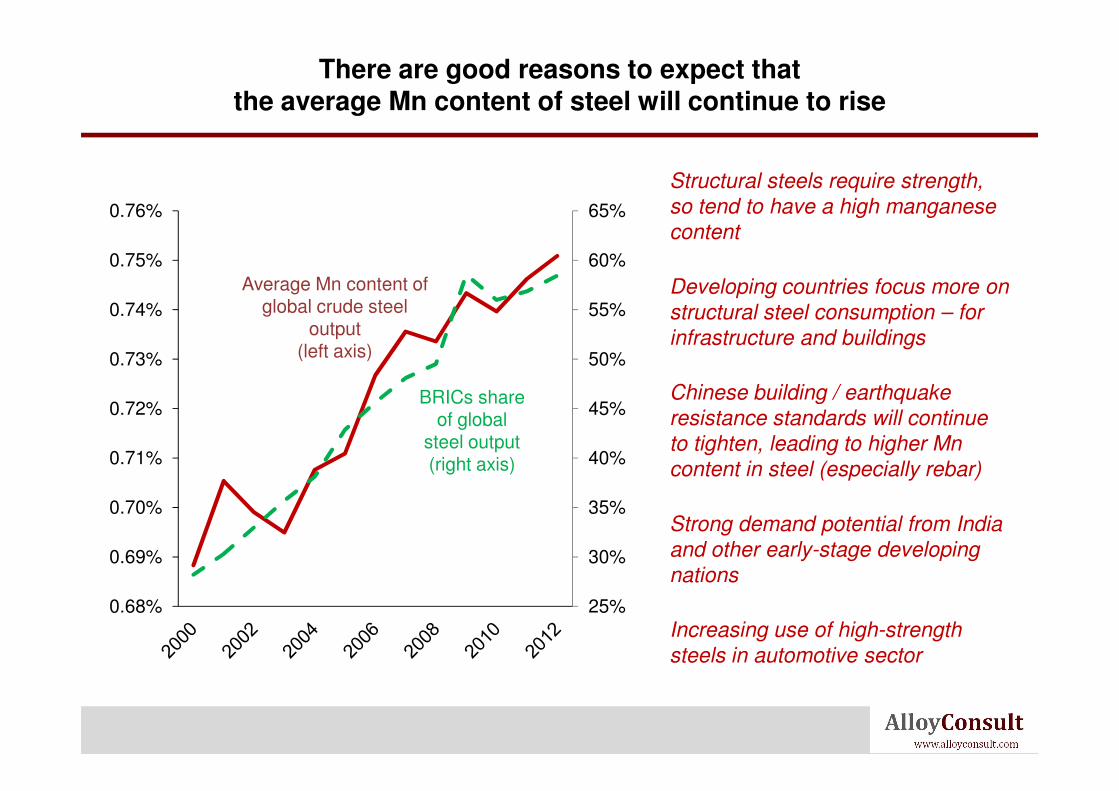

Average Mn content of global crude steel output

0.72%

0.73%

0.74%

0.75%

0.76%

Average Mn content per tonne of steel has increased by ~10% over the past decade, and is continuing to rise

+5.2%

+6.2%

5.5%

6.0%

6.5%

Global average annual growth rate, 2000-2012

0.68%

0.69%

0.70%

0.71%

0.72% +5.2%

4.0%

4.5%

5.0%

Crude steel production

Manganese demand*

* includes non-steel applications

10

12

14

16

18

Rest of world

Other Asia

11%

Mn alloy demand growth has been fuelled by China. In 2012 China accounted for 53% of global demand, Asia in total for 68%

Global consumption of Mn alloys(million tonnes, gross weight basis)

15%

17.4

0

2

4

6

8

10China

CIS

N.America

Europe

24%

13%

17%

21%

12%

7%

53%8.1

50%

55%

60%

65%

0.73%

0.74%

0.75%

0.76%

BRICs share

Average Mn content of global crude steel

output(left axis)

There are good reasons to expect that the average Mn content of steel will continue to rise

Structural steels require strength,

so tend to have a high manganese

content

Developing countries focus more on

structural steel consumption – for

infrastructure and buildings

Chinese building / earthquake

25%

30%

35%

40%

45%

0.68%

0.69%

0.70%

0.71%

0.72%BRICs share

of global steel output(right axis)

Chinese building / earthquake

resistance standards will continue

to tighten, leading to higher Mn

content in steel (especially rebar)

Strong demand potential from India

and other early-stage developing

nations

Increasing use of high-strength

steels in automotive sector

2000

2500

3000

3500

HC FeMnUS$ per tonne

Mn alloy prices have not shown any consistent improvementfrom the floor reached in Q4-2012

1500

2000

2500

3000

SiMnUS$ per tonne

0

500

1000

1500

EU US Japan China domestic

0

500

1000

1500

EU US Japan China domestic

12

14

16

18

20

2,500

3,000

3,500

Mn ore

Modest increases in Mn ore prices, if they are sustained, will most likely filter through to Mn alloy prices in the coming months

Mn ore and Mn alloy prices are

so well correlated because Mn

ore prices impact production

costs for non-integrated, higher

cost production

Filters directly into Chinese prices

– into Europe & elsewhere mostly

through Indian imports

EU SiMn spot price(US$ per tonne)

Mn ore bench spot price(US$ per dmtu)

0

2

4

6

8

10

500

1,000

1,500

2,000Mn ore

(right axis)

SiMn(left axis)

through Indian imports

Recent modest improvements

in Mn ore prices have not yet

been much reflected in Mn

alloy prices but if higher Mn

ore prices are sustained then

this is likely to changeR-squared correlation = 92.52%

1. Brief overview of recent developments in Mn alloy markets

2. Focus on India

3. Focus on Mn metal

Structure

1.5

2.0

2.5

MLCFeMn

HCFeMn

SiMn

India Mn alloy output by type(million tonnes, gross weight basis)

1.5

2.0

2.5

Exported

Consumed domestically

India Mn alloy output by consuming market(million tonnes, gross weight basis)

Indian Mn alloy output has risen fourfold over the past decade (~75% of output is SiMn). The growth has been driven by rising exports

0.0

0.5

1.0

1.5

0.0

0.5

1.0

12

600

700

800

900

1,000Other

MOIL

India Mn ore output by company(thousand tonnes, contained Mn basis)

1.2

1.4

1.6

1.8

2.0Imported

Domestic mines

India Mn ore supply by source(kt gross weight)

The growth of Indian Mn alloy output has been fuelled by imported ore. Indian Mn ore production has been quite stable for several years

0

100

200

300

400

500

600

0.0

0.2

0.4

0.6

0.8

1.0

1313

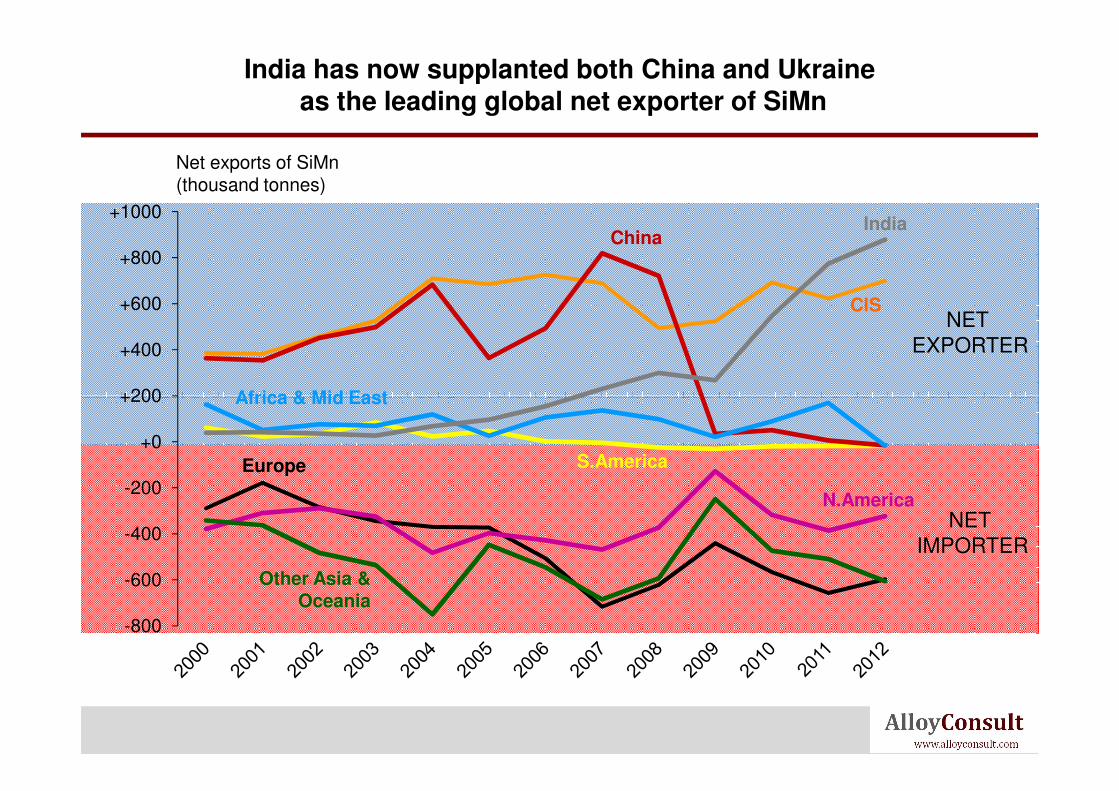

India has now supplanted both China and Ukraineas the leading global net exporter of SiMn

+200

+400

+600

+800

+1000India

CIS

China

Africa & Mid East

NET EXPORTER

Net exports of SiMn(thousand tonnes)

-800

-600

-400

-200

+0

+200

Europe

N.America

Other Asia & Oceania

Africa & Mid East

S.America

NET IMPORTER

200

300

India crude steel production(million tonnes)

2

3

India Mn alloy consumption(million tonnes, gross weight basis)

It is anticipated that Indian steel production will rise threefold by 2030, resulting in a similar increase in domestic demand for Mn alloys

SiMn

0

100

0

1

15Source: Hatch Consulting

HC FeMn

MLC FeMn

• India’s crude steel production is forecast to grow from 76 million tonnes in 2012 to ~270 million tonnes in 2030 (Source: Hatch, 2013)

• This will result in similar growth in Indian Mn alloy consumption:SiMn + 1.6 million tonnesHC FeMn +560,000 tonnesMLC FeMn +270,000 tonnes

In the longer term, India may be unable to sustain its exports ofMn alloys due to the strong growth of domestic demand

• The question is whether India will be able to maintain current Mn alloy export levels in the long-term(maybe will follow China’s path – exports end suddenly)

• Another parallel with China – India’s Mn alloy production is generally not low cost, despite rapid capacity expansion(increasing reliance on imported ore, captive power mostly based on coal & oil)

ShyamMICL

Hira

Nava Bharat

Maithan

India SiMn output by producer,2012

Indian Mn alloy production is increasingly showing parallels with China –a fragmented, non-integrated supply base with no clear leaders

Indian Mn alloy production is fragmented amongst a large number of producers with no clear market leader(increasingly similar to China)

No. of SiMn producers: approx 50

Market shares:SAIL

Sova

Srinivasa

Rohit

ChattisgarghJindal

SK Sarawagi

BalasoreKFA

Others

total ~1.6 million tonnes

Market shares:Top-15 producers ~40%Smaller producers ~60%

Major contrast to Indian Mn ore sector(MOIL market share ~45%)

1,500

Ind

ia a

vera

ge

SiMn cash cost curve, 2012 (US$/tonne FOB)

Ch

ina a

vera

ge

Indian suppliers are amongst the highest cost, yet are still in the most competitive half of the cost curve (due to the size of Chinese output)

00 2 4 6 8 10 12

Ind

ia a

vera

ge

Production, million tonnes ( gross weight basis)*

Ch

ina a

vera

ge

*includes SiMn remelted in the manufacture of MLC FeMn

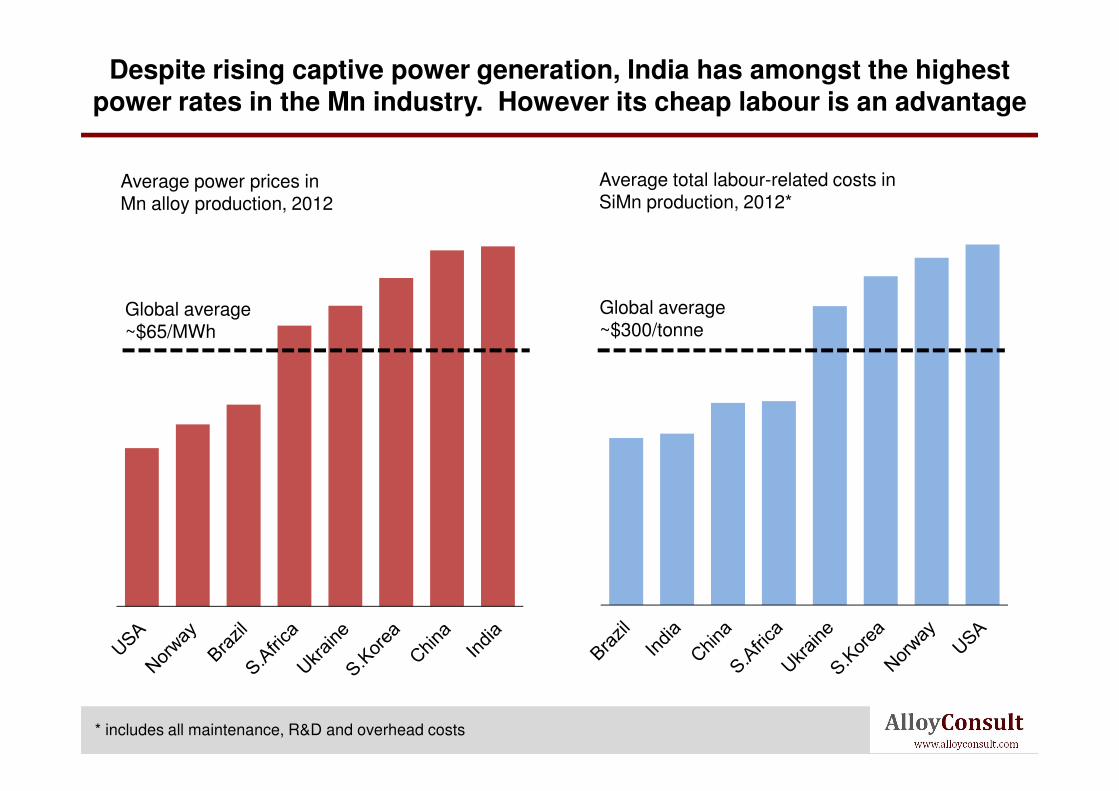

Average power prices in Mn alloy production, 2012

Despite rising captive power generation, India has amongst the highest power rates in the Mn industry. However its cheap labour is an advantage

Global average~$65/MWh

Global average~$300/tonne

Average total labour-related costs inSiMn production, 2012*

85% 67%

36%50%

85%

36%50%

* includes all maintenance, R&D and overhead costs

1. Brief overview of recent developments in Mn alloy markets

2. Focus on India

3. Focus on Mn metal

Structure

World Mn metal consumption, 2012

Mn metal is the only Mn alloy with a large non-steel demand segment (~30%). China accounts for ~70% of global demand

by region by end-use

Europe

N.AmericaRest of world

Al / Cu alloys

China

Oth. Asia

SS-200

SS-300/400

Carbon steel

MLC FeMnfeed

Al / Cu alloys& other

1.0

1.2

1.4

1.6

Other

China

11%

Mn metal production grew very strongly between 2000 and 2010, since when it has stabilised. China produces 97% of the world’s Mn metal

Global production of Mn metal by country(million tonnes)

0.0

0.2

0.4

0.6

0.8

13%

17%

21%

US$ per tonne

4,000

5,000

6,000

7,000

Mn metal*

MC FeMn

Mn metal usually trades at around double MC FeMn prices, but there are times when the two markets move differently

0

1,000

2,000

3,000

* Ryans’ Notes price for EMM flake

• Mn metal production can be considered extremely harmful to both the environment and worker health, due to use and disposal of toxic acids in the production process. This is a major reason why 97% of global output now takes place in China

• Rising environmental awareness and stricter legislation will make it increasingly difficult to build new Mn metal capacity in China – already production seems to have plateaued somewhat since 2010

Due to environmental and worker safety issues, it will become increasingly difficult to build new Mn metal capacity in China

have plateaued somewhat since 2010

• Chinese Mn metal output increasingly using imported carbonate ores due to deteriorating quality of domestic Mn ore

• Some new Mn metal projects springing up outside China (Gabon, N.America, Malaysia), based on less polluting technology

• Also expect growth in demand from high-end steels to increasingly be based on refined alloys (LC SiMn, LC FeMn, ULC FeMn) rather than Mn metal

40%

50%

60%

Scrap charge in Chinese stainless steel production

Anticipated trends in Chinese stainless scrap availability will make it easier to substitute refined alloys for Mn metal in the long term

Rising availability and use of stainless steel scrap in China will increase steelmakers’ flexibility to use other alloys in place of Mnmetal (LC SiMn, LC FeMn, ULC

10%

20%

30%

Source: Hatch Consulting

metal (LC SiMn, LC FeMn, ULC FeMn) because scrap contains fewer impurities (Si, C) than virgin raw materials

Opportunities and challenges in the manganese alloy industry

Thank you for your attentionThank you for your attention