north northamptonshire strategic housing market ... 08 07 nn shma update technical...north...

TRANSCRIPT

North Northamptonshire Strategic Housing Market Assessment Update

Final Technical Report

August 2012

www.housingvision.co.uk

North Northamptonshire Strategic Housing Market Assessment Update Final Technical Report Housing Vision (HV)

Project Director: Dr Richard Turkington

Director The Housing Vision Consultancy 59 Stocks Lane Newland Malvern Worcs. WR13 5AZ 01886 833118 (phone) 01886 830102 (phone/fax) 07714 106386 (mobile) [email protected] www.housingvision.co.uk

Date: 7th August 2012

Contents Page 1.0 Introduction 4 2.0 What key influences and drivers are at work in

the housing market? 10

3.0 What choices do consumers have in the

housing market? 83

4.0 What is the current pattern of need and demand

for affordable housing? 123

5.0 What is the projected requirement for housing? 135

APPENDICES A Gross household incomes by ward in East

Northants, mean and lower quartile 151

1. Introduction 1.1 Context and approach 1.1 The final National Planning Policy Framework issued in March 2012,

establishes at paragraph 159 that Local Planning Authorities should have a clear understanding of housing requirements in their area and should prepare a Strategic Housing Market Assessment to identify the scale and mix of housing and the range of tenures that the local population is likely to require over the plan period which:

• meets household and population projections, taking into account migration and demographic change;

• addresses the need for all types of housing, including affordable housing and the needs of different groups in the community;

• and caters for all types of housing demand. 1.3 The context for this Update is the review by the North Northamptonshire

Joint Planning Unit (JPU) North of the Northamptonshire Joint Core Strategy (JCS) which covers the North Northamptonshire Housing Market area (the administrative areas of Corby Borough Council, Kettering Borough Council, East Northamptonshire Council and Wellingborough Borough Council).

1.4 A minimum housing requirement will be established in the JCS against

which 5 year housing land supply requirements will be assessed. It is important to ensure that this approach is based on a robust evidence base identifying housing need and demand within the HMA area.

1.5 The required evidence base is provided by this Update to the North

Northamptonshire Strategic Housing Market Assessment completed in 2007 for the period 2011 -2031. More specifically, it provides a brief refresh of the SHMA to ensure that it is up-to-date and satisfies the Paragraph 159 requirements of the draft Planning Policy Framework.

1.6 In accordance with government guidance on Housing Market Assessment,

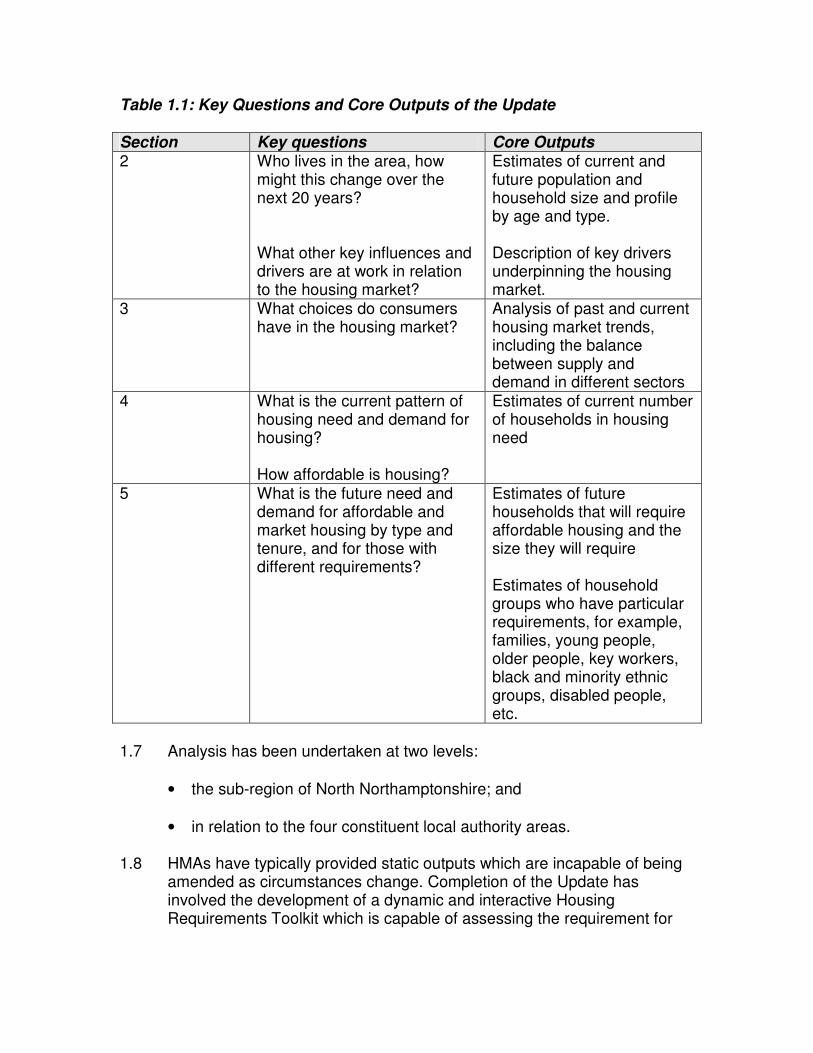

the approach adopted makes maximum use of existing and available demographic, social and housing data to identify the dynamics of the local housing market; the ‘choices’ available to local people; the imbalances between need, demand and supply which constrain those choices and the projected future requirement for housing. The following table summarises the Core Outputs required and associated Key Questions which guide the structure of the report.

Table 1.1: Key Questions and Core Outputs of the Update Section Key questions Core Outputs 2 Who lives in the area, how

might this change over the next 20 years? What other key influences and drivers are at work in relation to the housing market?

Estimates of current and future population and household size and profile by age and type. Description of key drivers underpinning the housing market.

3 What choices do consumers have in the housing market?

Analysis of past and current housing market trends, including the balance between supply and demand in different sectors

4 What is the current pattern of housing need and demand for housing? How affordable is housing?

Estimates of current number of households in housing need

5 What is the future need and demand for affordable and market housing by type and tenure, and for those with different requirements?

Estimates of future households that will require affordable housing and the size they will require Estimates of household groups who have particular requirements, for example, families, young people, older people, key workers, black and minority ethnic groups, disabled people, etc.

1.7 Analysis has been undertaken at two levels:

• the sub-region of North Northamptonshire; and

• in relation to the four constituent local authority areas. 1.8 HMAs have typically provided static outputs which are incapable of being

amended as circumstances change. Completion of the Update has involved the development of a dynamic and interactive Housing Requirements Toolkit which is capable of assessing the requirement for

housing arising from household growth, including from older households. The application of the Toolkit is fully described in Section 5.

1.2 Data sources 1.9 The approach to the Update places primary reliance on secondary data

sources which are capable of continual updating, enabling monitoring of housing markets by housing and planning officers. The many data sources used are listed below accompanied by appropriate weblinks as follows:

• 2001 Census data, available through the NOMIS website at: https://www.nomisweb.co.uk/Default.asp

• ONS mid-year population estimates 2010 including components of population change, available through the ONS website at:

http://www.ons.gov.uk/ons/publications/re-reference-

tables.html?edition=tcm%3A77-231847

• ONS 2010-based subnational population projections, available through the ONS website at:

http://www.ons.gov.uk/ons/publications/re-reference-

tables.html?edition=tcm%3A77-246448

• Annual Population Survey for 2008 (commuting) and 2011 (occupational groups), available through the NOMIS website at:

https://www.nomisweb.co.uk/articles/554.aspx

• English Indices of Multiple Deprivation 2010, available through the CLG website at:

http://www.communities.gov.uk/publications/corporate/statistics/indices

2010

• Annual Survey of Hours and Earnings (ASHE) providing mean and median incomes form full and part-time work by local authority area, available through the NOMIS website at:

https://www.nomisweb.co.uk/Default.asp

• CACI PayCheck Profile data for gross household incomes by district and postcode. This is commissioned commercial data available by direct approach to CACI at:

http://www.caci.co.uk/

• Patient Register Data Service (PRDS), the National Health Service Central Register (NHSCR) and Higher Education Statistics Agency (HESA), available through the ONS website at:

http://www.ons.gov.uk/ons/publications/re-reference-tables.html?edition=tcm%3A77-218545

• Labour Force Survey (LFS) 2001, available through the Business Information and Skills (BIS) website at:

http://www.education.gov.uk/rsgateway/DB/VOL/v000303/index.shtml

• Land Registry property price post-coded data, available through the Land registry website at:

http://epsiplatform.eu/content/uk-land-registry-releases-data-free-

charge

• Valuation Office Agency (VOA) data on private rents, available through the VOA website at:

http://www.voa.gov.uk/corporate/statisticalReleases/120126_PrivateRe

ntalMarket.html

• Private rental data provided through the websites rightmove.co.uk and findaproperty.com, available at:

http://www.findaproperty.com/search-tools/ and http://www.yourrightmove.co.uk/

• Housing Strategy Statistical Appendix (HSSA) data for 2010-11 on affordable lettings, sales and completions, available through the CLG website at:

http://www.communities.gov.uk/publications/corporate/statistics/lahousi

ng201011

• COntinuous REcording of lettings and sales of social housing in England (CORE) data on affordable lettings and sales; available through the CORE website at:

https://core.communities.gov.uk/

• Affordable housing stock, applications and lettings data.

• Housing and planning data provided by constituent local authorities. 1.10 Please note that where percentages have been rounded this is indicated

in the text, and where applied, cumulative totals may slightly exceed or fall below 100%.

1.3 A note on boundaries 1.11 Data is collected and collated according to a range of boundaries which

seldom conform with each other. The requirement is to achieve the best fit possible and the boundaries used in this Study are summarised in the table below.

Table 1.2: boundaries used in the SHMA Update

Boundary Data Source Population profile, internal migration, travel to work and housing stock profile data

ONS

Household profile, deprivation and affordable lettings, sales and completions data

CLG

Incomes data CACI Property price data Land Registry Private rental data VOA, rightmove and

findaproperty.com

District Council areas

Affordable housing stock, applications and lettings data

Constituent local authorities

Incomes data

CACI

Constituent postcodes

Property price data Land Registry

1.12 Map 1.1 below identifies the constituent local authority areas.

9

10

2. What key influences and drivers are at work in the housing market?

2.1 Introduction 2.1 This section reviews the key drivers underpinning the housing market

which were identified by the 2007 SHMA, and progresses from an overview of key social indicators to a review demographic and especially household projections and the factors underpinning them including international, and especially internal migration; and commuting patterns.

2.2 Who lives in the area now? Population 2.2 The following table provides mid-year population estimates by age

bands provided, further detail of projected trends is provided in Table 2.6.

Table 2.1: mid-year population estimates by age bands, 2010, 000s

0 to 4 years

5 to 14 years

15 to 44 years

45 to 64 years

65 plus years All Ages Area

No. % No. % No. % No. % No. % No. %

Corby 4.3 7.7 6.8 12.2 21.6 38.7 14.7 26.3 8.5 15.2 55.8 100.0

East Northants. 5.2 6.1 10.9 12.8 31.3 36.7 23.8 27.9 14.1 16.5 85.3 100.0

Kettering 6.2 6.8 11 12.1 34.7 38.3 24.1 26.6 14.7 16.2 90.6 100.0

Wellingborough 4.9 6.5 9.1 12.0 28.8 38.0 20.5 27.1 12.5 16.5 75.7 100.0

North Northants. 20.6 6.7 37.8 12.3 116.4 37.9 83.1 27.0 49.8 16.2 307.4 100.0

East Midlands - 5.9 - 11.1 - 39.5 - 26.3 - 17.1 - 100.0

England and Wales - 6.2 - 11.3 - 40.5 - 25.4 - 16.6 - 100.0

(Source: ONS Mid-year Population Estimates, 2010, Table 9 Local Authority Quinary, ONS website) Key findings:

• The distribution of population by age band is remarkably similar for all local authorities although with a slight emphasis towards a younger population in Corby.

Ethnicity 2.3 The following table uses experimental data to estimate population by

ethnicity.

11

Table 2.2: ethnic origin, 2009

White Mixed

Asian or Asian British

Black or Black British

Chinese or

Other All

Groups Area No % No % No % No % No % No %

Corby 52.2 94.6 0.7 1.3 1.2 2.2 0.6 1.1 0.7 1.3 55.2 100.0

East Northants. 79.8 93.9 1.2 1.4 2.0 2.4 1.1 1.3 0.8 0.9 85.0 100.0

Kettering 84.4 93.7 1.2 1.3 2.7 3.0 1.0 1.1 0.8 0.9 90.1 100.0

Wellingborough 66.3 87.6 1.6 2.1 4.0 5.3 2.4 3.2 1.2 1.6 75.7 100.0

North Northants. 282.7 92.4 4.7 1.5 9.9 3.2 5.1 1.7 3.5 1.1 306.0 100.0

East Midlands 4,010.8 90.1 71.6 1.6 238.3 5.4 71.2 1.6 59.1 1.3 4,451.2 100.0

England and Wales - 87.9 - 1.8 - 5.9 - 2.8 - 1.6 - 100.0

(Source: ONS Experimental Population Estimates Mid-2009, ONS Website)

Key findings:

• The area is estimated to have a non-White population of less than 8%, ranging from over 12% in Wellingborough – which has the largest Asian/Asian British and Black/Black British populations, to just over 5% in Corby.

2.4 The following table reviews Occupation Groups and is drawn from the

June 2011 Annual Population Survey.

12

Employment Table 2.3: Occupation Groups for 16 to 74 year olds, June 2011

Corby East Northants Kettering Wellingborough North Northants East

Midlands

England and

Wales

Occupation groups No % No % No % No % No % % %

Managers and Senior Officials 1,400* 5.0 8,100 18.4 6,800 14.6 6,000 15.1 22,300 14.1 15.0 15.9

Professional Occupations 2,800* 9.7 4,700 10.6 6,300 13.6 1,900* 4.7 15,700 9.9 12.2 14.1

Associate Professional and Technical Operations 2,500* 8.7 6,800 15.5 6,000 13.0 3,600 9.0 18,900 11.9 13.4 14.9

Administrative and Secretarial Occupations 2,400* 8.4 3,900 9.0 1,500* 3.2 2,500* 6.3 10,300 6.5 10.0 10.7

Skilled Trades Occupations 2,300* 7.9 4,800 11.0 4,700 10.1 6,600 16.6 18,400 11.6 11.2 10.1

Personal Service Occupations 3,000* 10.4 3,800 8.7 2,400* 5.2 6,600 16.7 15,800 10.0 9.0 8.8

Sales and Customer Services Occupations 1,100* 3.8 2,400* 5.4 3500* 7.6 2,300* 5.8 9,300 5.9 7.3 7.3

Process, Plant and Machines Operatives 5,,300 18.7 4,800 10.8 4,800 10.4 5,200 13.1 20,100 12.7 8.4 6.5

Elementary Occupations 7,,800 27.3 4,300 9.8 10,300 22.3 5,000 12.7 27,400 17.3 13.2 11.3

Total 28,600 100 44,000 100 46,300 100 39,600 100 158,200 100 100 100

(Source: Annual Population Survey, NOMIS website)

Note: * Small sample sizes

Key findings:

• Compared with North Northants as a whole:

o Corby has a smaller proportion of managers and senior officials and higher proportions of process, plant and machine operatives and elementary occupations;

o Wellingborough has a smaller proportion of professional occupations and higher proportions of skilled trades and personal service occupations; and

o Kettering has a smaller proportion of personal service occupations.

13

Income 2.5 The following table profiles the proportion of households receiving

gross incomes by income bands. Incomes are for all household ad from all sources including social security benefits. This data has been applied in the Housing Requirements Toolkit.

Table 2.4: gross household income patterns, percentages, June 2012 Income band Corby East

Northants. Kettering W/borough

£0 - £5k 3.06 2.23 2.52 2.91

£5 - 10k 12.65 10.1 11.01 12.01

£10 - 15k 12.54 10.9 11.45 12.08

£15 – 20k 10.38 9.52 9.85 10.1

£20 – 25k 8.4 8.08 8.28 8.35

£25 - 30k 7.46 7.35 7.46 7.41

£30 – 35k 6.69 6.8 6.83 6.71

£35 - 40k 6.44 6.72 6.69 6.53

£40 - 45k 5.69 6.02 5.93 5.73

£45 - 50k 4.58 4.95 4.83 4.61

£50 - 55k 4.15 4.68 4.52 4.32

£55 – 60k 3.33 3.81 3.64 3.46

£60 - 65k 2.78 3.2 3.02 2.86

£65 - 70k 2.09 2.48 2.31 2.16

£70 - 75k 1.9 2.35 2.17 2.03

£75 - 80k 1.45 1.88 1.71 1.6

£80 - 85k 1.12 1.48 1.34 1.26

£85 - 90k 0.82 1.07 0.95 0.88

£90 - 95k 0.77 1.01 0.88 0.82

£95 - £100k 0.64 0.83 0.73 0.68

£100-120k 1.64 2.25 1.96 1.8

£120-140k 0.76 1.15 0.99 0.9

£140-160k 0.41 0.62 0.51 0.46

£160-180k 0.16 0.32 0.25 0.22

£180-200k 0.08 0.16 0.12 0.1

£200k + 0.02 0.06 0.04 0.03

Mean income £34,136 £38,564 £36,732 £35,338

Median income £26,998 £31,341 £29,617 £28,071

Lower quartile £13,706 £15,931 £15,010 £14,173

(Source: CACI commissioned data)

The following key findings and trends are identifiable:

• East Northants has the highest mean, median and lower quartile incomes and Corby the lowest. However, there are wide variations by ward in East Northants (see Appendix A).

• Income levels and income distributions by proportion of households are most clearly seen in the following chart, especially the peaks at £10-15k at the lower end of the income distribution and at £100-120k at the upper end.

14

Chart 2.1: percentage of households by gross income band, May 2012

0

5

10

15

20

25

30

35

40

45

50

£0 -

£5k

£5 -

10k

£10

- 15k

£15

– 20k

£20

– 25k

£25

- 30k

£30

– 35k

£35

- 40k

£40

- 45k

£45

- 50k

£50

- 55k

£55

– 60k

£60

- 65k

£65

- 70k

£70

- 75k

£75

- 80k

£80

- 85k

£85

- 90k

£90

- 95k

£95

- £10

0k£1

00-1

20k

£120

-140

k£1

40-1

60k

£160

-180

k£1

80-2

00k

£200

k +

Corby East Northants. Kettering W/borough

(Source: CACI commissioned data)

15

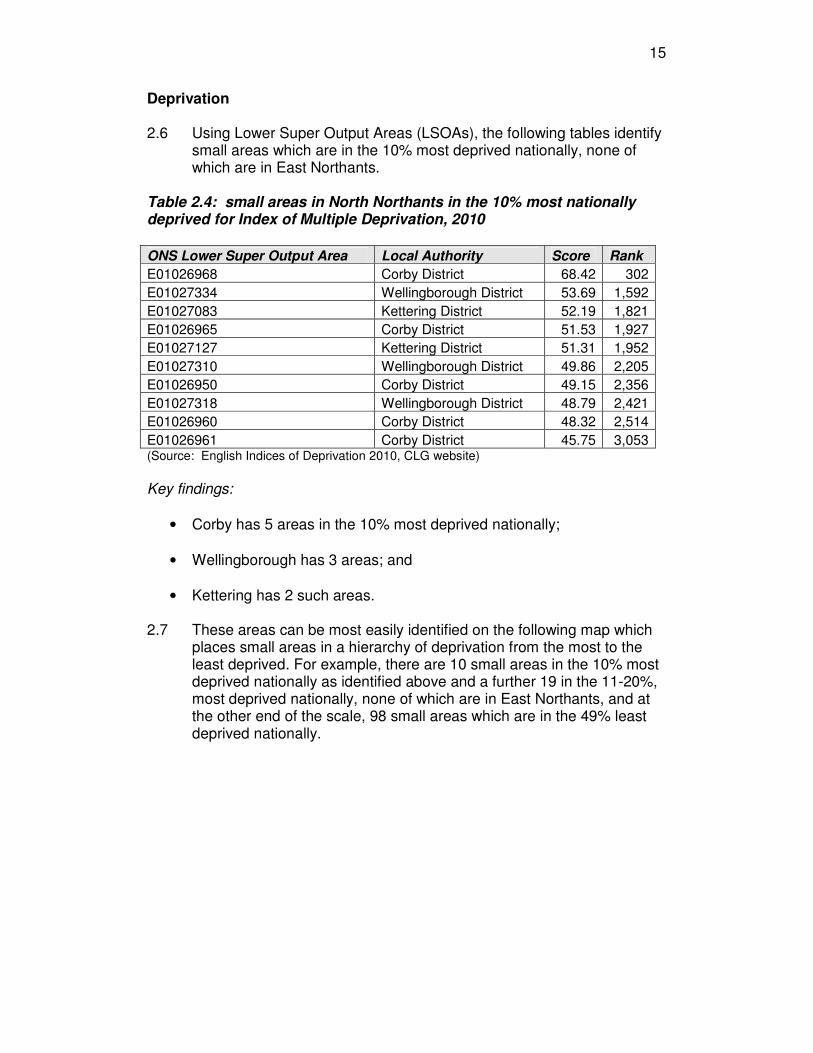

Deprivation 2.6 Using Lower Super Output Areas (LSOAs), the following tables identify

small areas which are in the 10% most deprived nationally, none of which are in East Northants.

Table 2.4: small areas in North Northants in the 10% most nationally deprived for Index of Multiple Deprivation, 2010

ONS Lower Super Output Area Local Authority Score Rank

E01026968 Corby District 68.42 302

E01027334 Wellingborough District 53.69 1,592

E01027083 Kettering District 52.19 1,821

E01026965 Corby District 51.53 1,927

E01027127 Kettering District 51.31 1,952

E01027310 Wellingborough District 49.86 2,205

E01026950 Corby District 49.15 2,356

E01027318 Wellingborough District 48.79 2,421

E01026960 Corby District 48.32 2,514

E01026961 Corby District 45.75 3,053 (Source: English Indices of Deprivation 2010, CLG website) Key findings:

• Corby has 5 areas in the 10% most deprived nationally;

• Wellingborough has 3 areas; and

• Kettering has 2 such areas. 2.7 These areas can be most easily identified on the following map which

places small areas in a hierarchy of deprivation from the most to the least deprived. For example, there are 10 small areas in the 10% most deprived nationally as identified above and a further 19 in the 11-20%, most deprived nationally, none of which are in East Northants, and at the other end of the scale, 98 small areas which are in the 49% least deprived nationally.

16

17

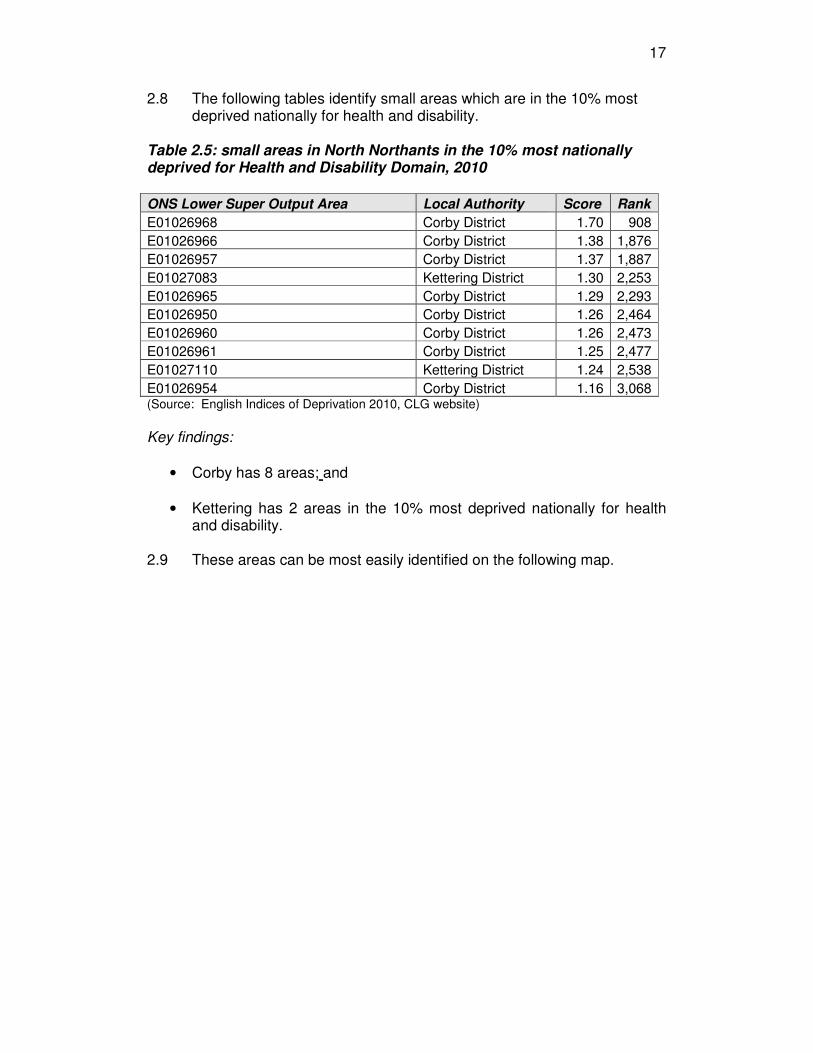

2.8 The following tables identify small areas which are in the 10% most deprived nationally for health and disability.

Table 2.5: small areas in North Northants in the 10% most nationally deprived for Health and Disability Domain, 2010

ONS Lower Super Output Area Local Authority Score Rank

E01026968 Corby District 1.70 908

E01026966 Corby District 1.38 1,876

E01026957 Corby District 1.37 1,887

E01027083 Kettering District 1.30 2,253

E01026965 Corby District 1.29 2,293

E01026950 Corby District 1.26 2,464

E01026960 Corby District 1.26 2,473

E01026961 Corby District 1.25 2,477

E01027110 Kettering District 1.24 2,538

E01026954 Corby District 1.16 3,068 (Source: English Indices of Deprivation 2010, CLG website) Key findings:

• Corby has 8 areas; and

• Kettering has 2 areas in the 10% most deprived nationally for health and disability.

2.9 These areas can be most easily identified on the following map.

18

19

2.3 Population and household change 2.10 This section considers how the area’s population might change over

the 20 years from 2011-2031, and uses demographic data provided by Edge Analytics to estimate the future number of households, broken down by age and type. Edge Analytics are specialists in demographic modelling and population forecasting. Two scenarios have been modelled, ‘Natural Change’ and ‘Migration-led Recalibrated’. ‘Natural Change’ is underpinned by the relationship between births and deaths whereas Migration-led Recalibrated’ uses revised population constraints to derive assumptions about future fertility, mortality and migration. These revised population constraints are based on alternative estimates of immigration for 2001-2009, for each area. Future migration assumptions are based on the latest five years of historical evidence 2004/5 – 2008/9 which includes the peak of the market plus the first year of the economic recession. Data has been provided for different household types and which have been applied in toolkit modelling. However, to aid understanding, these have been reduced to 7 types conforming with different housing requirements as follows:

• One person

• Couple/+1 or more adults no children

• Couple/+ 1 or more adults 1-2 children

• Couple/+ 1 or more adults 3+ children

• Lone parent/+ 1 or more adults 1-2 children

• Lone parent/+ 1 or more adults 3+ children

• Other households 2.11 Household projections are underpinned by projected changes in

population, and the following table and chart use the most recent 2010-based ONS data to project changes in the area’s population by age, and which clearly identify the real and proportionate increases in the youngest and oldest age groups.

Table 2.6: projected change in the population of North Northamptonshire by age band, 2011-2031

Age band 2011 2016 2021 2026 2031 2011-2031

0-14 59.2 64.7 69.7 71.3 70.9 +19.76%

15-24 36.0 33.9 33.8 37.0 41.0 +13.88%

25-34 35.9 41.3 43.5 41.7 41.2 +14.77%

35-44 46.2 42.6 44.5 50.0 52.2 +12.98%

45-54 45.4 50.4 48.6 45.4 47.5 +4.63%

55-64 39.6 40.0 45.6 50.3 48.8 +23.23%

65-74 28.5 35.1 36.7 37.3 43.1 +51.22%

75-84 16.3 18.3 22.8 28.3 29.7 +82.2%

85+ 6.8 7.8 9.0 11.2 14.8 +117.65%

20

Totals 313.9 334.1 354.2 372.5 389.2 +23.99%

(Source: ONS Subnational Population Projections 2010, ONS website)

Key findings:

• There is projected growth of almost 24% in the area’s population between 2011 and 2031;

• Growth is below average for all age groups under 65 but substantially in excess of the average for those aged 65-74 (+51%); 75-84 (+82%) and 85+ (+118%).

• Overall, those aged 65+ are projected to increase from 51,600 in 2011 to 87,600 in 2031, a growth of almost 70% (69.77%).

• Such an increase will have a profound effect on housing requirements creating both need and demand for such specialised provision as designated, sheltered and extra-care housing, and the potential for large scale downsizing from under-occupied homes.

21

Chart 2.2: projected change in the population of North Northamptonshire by age band, 2011-2031

0.0 50.0 100.0 150.0 200.0 250.0 300.0 350.0 400.0 450.0

2011

2016

2021

2026

2031

0-14 15-24 25-34 35-44 45-54 55-64 65-74 75-84 85+

(Source: ONS Subnational Population Projections 2010, ONS website)

22

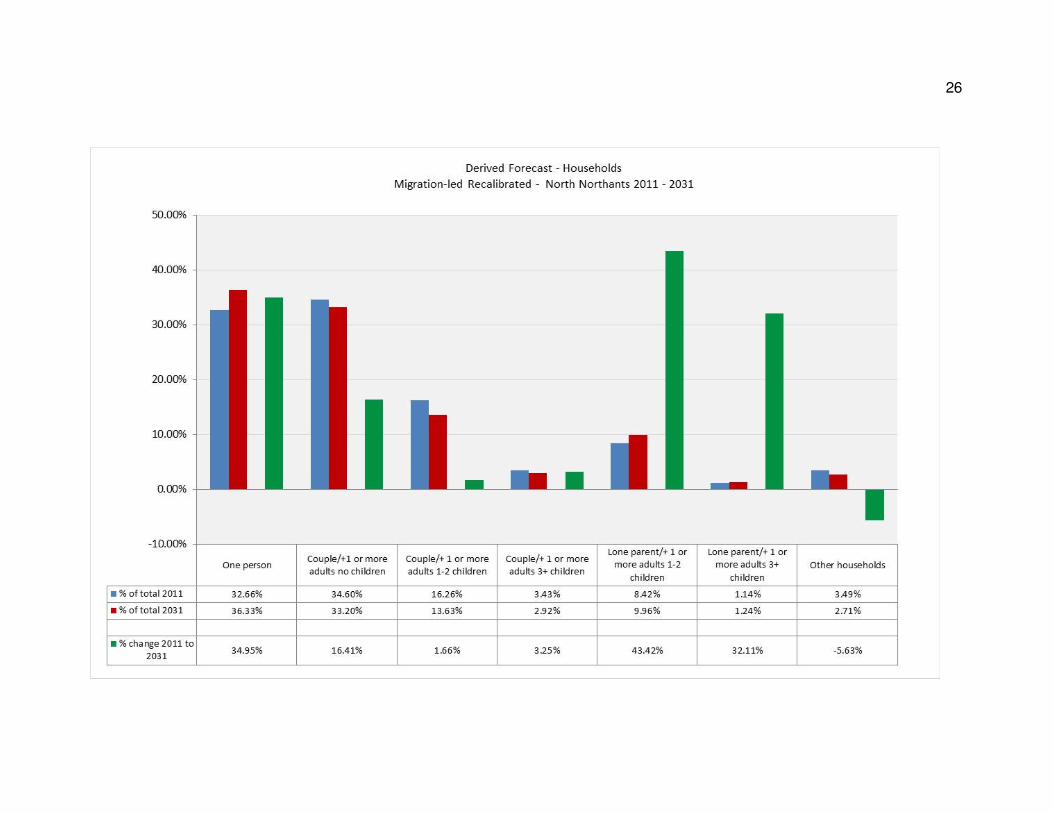

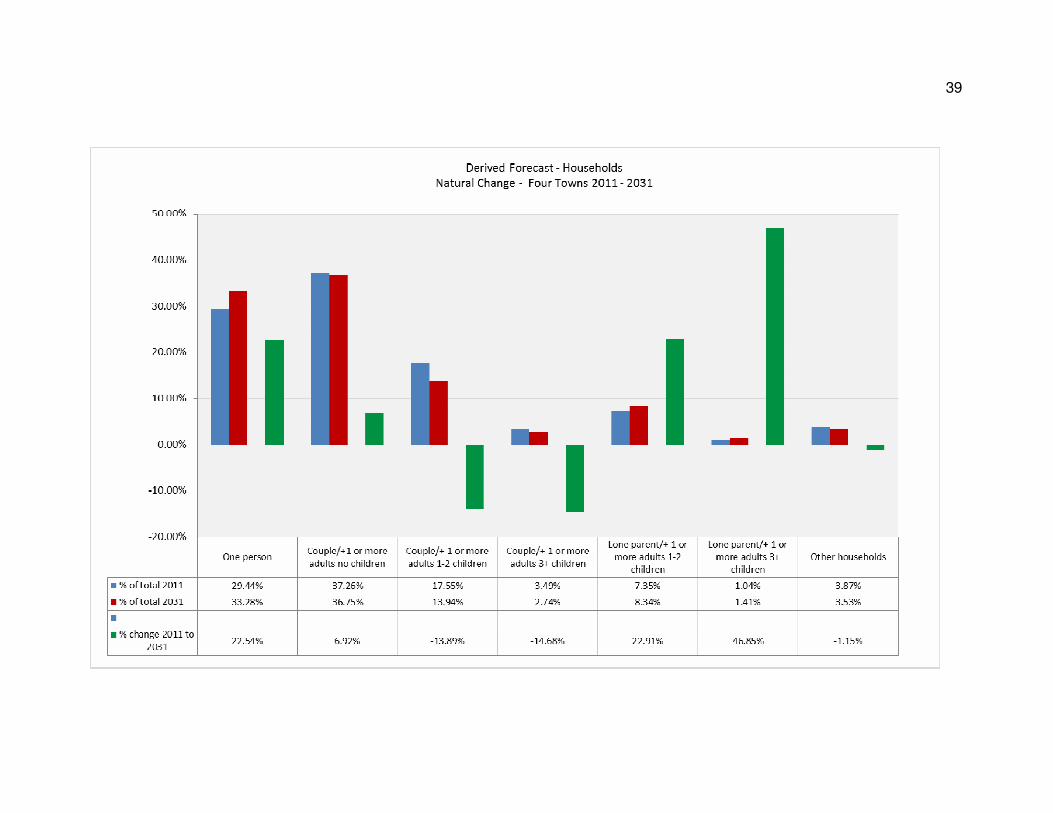

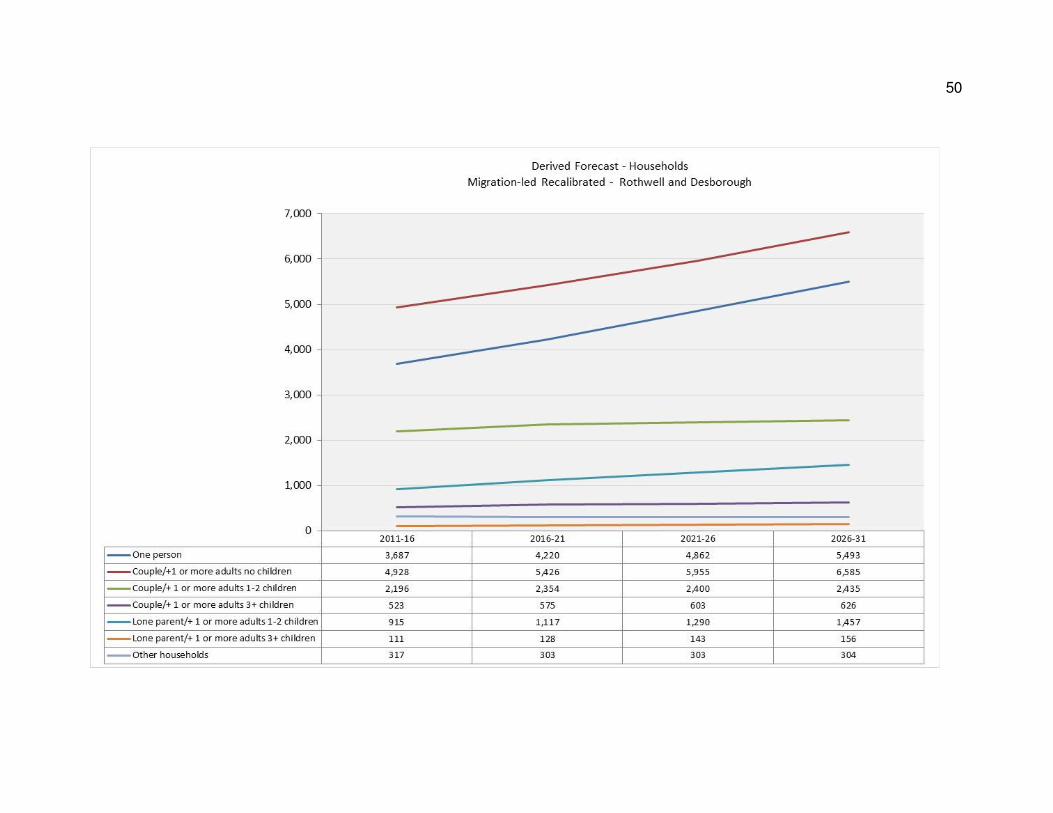

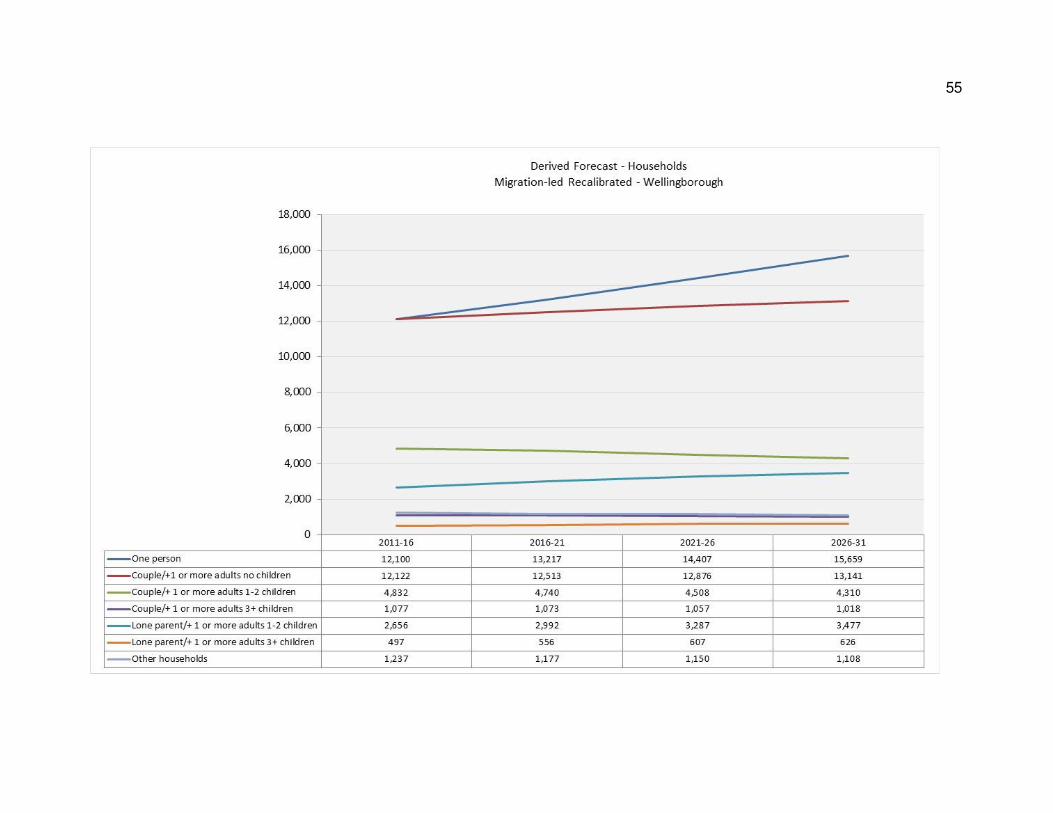

2.12 Household projections data has been expressed for both the Natural Change then the Migration-led Recalibrated scenarios for the North Northants area as a whole and then for each local authority area. For each scenario, a graph and table are provided identifying the numeric impact of projected changes over 20 years from 2011 then a bar chart and table identifying the proportionate change in the number of households of different types. Comments are provided identifying the impact of Natural Change then for the Migration-led Recalibrated scenario with comparisons identified as appropriate.

23

24

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

% of tota l 2011 32.97% 35.34% 15.66% 3.30% 8.11% 1.06% 3.57%

% of tota l 2031 37.51% 34.08% 12.30% 2.64% 9.37% 1.21% 2.89%

% change 2011 to 2031 23.63% 4.79% -14.64% -12.85% 25.61% 24.10% -11.82%

One personCoupl e/+1 or more

adults no chi ldren

Couple/+ 1 or more

adul ts 1-2 chi ldren

Couple/+ 1 or more

a dults 3+ chi ldren

Lone parent/+ 1 or

more a dul ts 1-2

chi ldren

Lone parent/+ 1 or

more adults 3+

chi ldren

Other househol ds

Derived Forecast - Households

Natural Change - North Northants 2011 - 2031

25

26

27

Key findings for the period 2011-2031 Natural Change

• One person households: growth of almost 25%

• Couple/+1 or more adults no children households: 5% growth

• Couple/+ 1 or more adults 1-2 children households: 15% decline

• Couple/+ 1 or more adults 3+ children households: 13% decline

• Lone parent/+ 1 or more adults 1-2 children households: over 25% growth

• Lone parent/+ 1 or more adults 3+ children households: almost 25% growth

• Other households: 12% decline Migration-led Recalibrated

• One person households: growth of almost 35% (10% increase on Natural Change)

• Couple/+1 or more adults no children households: over 16% growth (11% increase)

• Couple/+ 1 or more adults 1-2 children households: almost 2% growth (17% increase)

• Couple/+ 1 or more adults 3+ children households: over 3% growth (16% increase)

• Lone parent/+ 1 or more adults 1-2 children households: over 43% growth (18% increase)

• Lone parent/+ 1 or more adults 3+ children households: over 32% growth (7% increase)

• Other households: almost 6% decline (6% increase)

28

29

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

% of tota l 2011 36.45% 27.78% 15.93% 2.80% 12.19% 1.19% 3.66%

% of tota l 2031 41.48% 24.09% 13.79% 2.16% 14.70% 1.15% 2.64%

% change 2011 to 2031 23.81% -5.68% -5.81% -16.09% 31.20% 4.97% -21.57%

One personCouple/+1 or more

adults no chi ldren

Couple/+ 1 or more

adults 1-2 chi ldren

Couple/+ 1 or more

adults 3+ chi ldren

Lone parent/+ 1 or

more adults 1-2

chi ldren

Lone parent/+ 1 or

more adults 3+

chi ldren

Other households

Derived Forecast - Households

Natural Change - Corby 2011 - 2031

30

31

32

Key findings for the period 2011-2031 Natural Change

• One person households: growth of almost 24%

• Couple/+1 or more adults no children households: 6% decline

• Couple/+ 1 or more adults 1-2 children households: 6% decline

• Couple/+ 1 or more adults 3+ children households: 16% decline

• Lone parent/+ 1 or more adults 1-2 children households: over 30% growth

• Lone parent/+ 1 or more adults 3+ children households: 5% growth

• Other households: 22% decline Migration-led Recalibrated

• One person households: growth of over 42% (18% increase on Natural Change)

• Couple/+1 or more adults no children households: almost 9% growth (15% increase)

• Couple/+ 1 or more adults 1-2 children households: almost 22% growth (28% increase)

• Couple/+ 1 or more adults 3+ children households: 6% growth (22% increase)

• Lone parent/+ 1 or more adults 1-2 children households: over 57% growth (27% increase)

• Lone parent/+ 1 or more adults 3+ children households: almost 26% growth (21% increase)

• Other households: 14% decline (8% increase)

33

34

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

% of tota l 2011 29.28% 41.90% 16.17% 3.15% 5.41% 0.68% 3.41%

% of tota l 2031 34.47% 38.98% 13.37% 2.89% 6.30% 1.25% 2.75%

% change 2011 to 2031 28.10% 1.26% -10.03% -0.15% 26.63% 99.29% -12.07%

One personCouple/+1 or more

adults no chi ldren

Couple/+ 1 or more

adul ts 1-2 chi ldren

Couple/+ 1 or more

adul ts 3+ chi ldren

Lone parent/+ 1 or

more adults 1-2

chi ldren

Lone parent/+ 1 or

more adults 3+

chi ldren

Other hous eholds

Derived Forecast - Households

Natural Change - East Northants 2011 - 2031

35

36

37

Key findings for the period 2011-2031 Natural Change

• One person households: 28% growth;

• Couple/+1 or more adults no children households: 1% decline;

• Couple/+ 1 or more adults 1-2 children households: 10% decline

• Couple/+ 1 or more adults 3+ children households: stability

• Lone parent/+ 1 or more adults 1-2 children households: 27% growth

• Lone parent/+ 1 or more adults 3+ children households: almost 100% growth

• Other households: 12% decline Migration-led Recalibrated

• One person households: growth of over 37% (9% increase on Natural Change)

• Couple/+1 or more adults no children households: over 19% growth (20% increase)

• Couple/+ 1 or more adults 1-2 children households: almost 3.5% decline (13.5% increase)

• Couple/+ 1 or more adults 3+ children households: 1.25% decline (1.25% decline)

• Lone parent/+ 1 or more adults 1-2 children households: over 41% growth (14% increase)

• Lone parent/+ 1 or more adults 3+ children households: over 60% growth (40% decline)

• Other households: over 4% growth (16% increase)

38

39

40

41

42

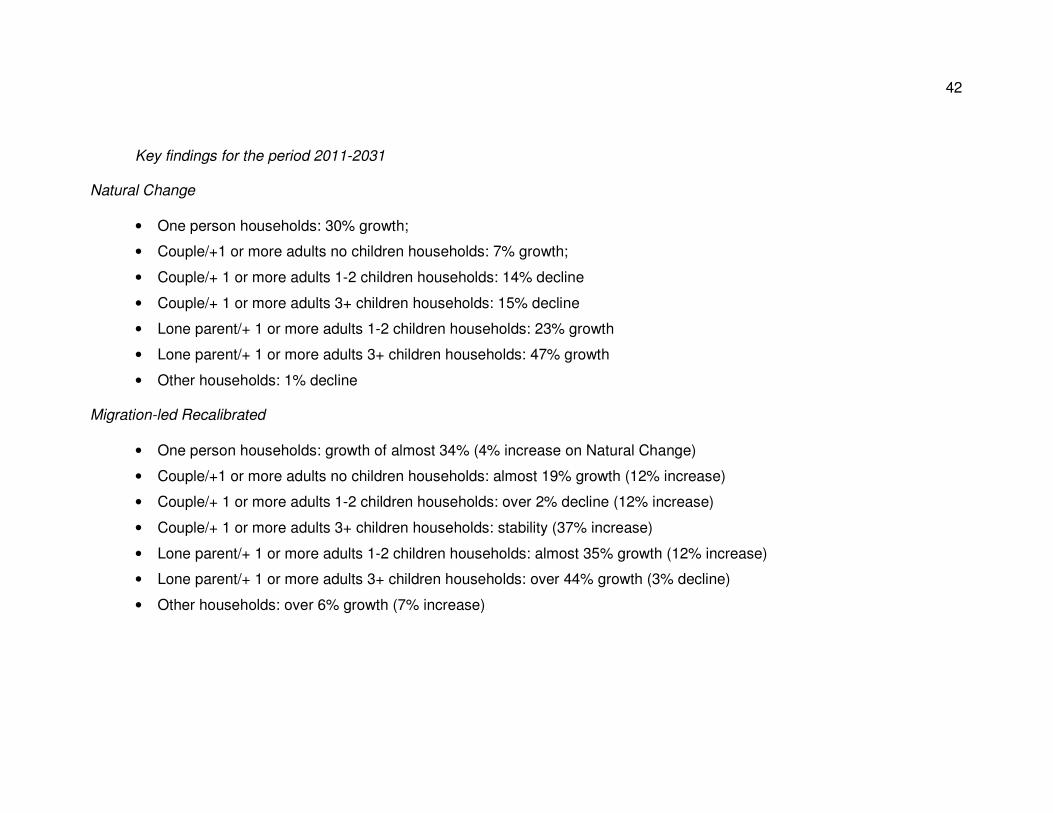

Key findings for the period 2011-2031 Natural Change

• One person households: 30% growth;

• Couple/+1 or more adults no children households: 7% growth;

• Couple/+ 1 or more adults 1-2 children households: 14% decline

• Couple/+ 1 or more adults 3+ children households: 15% decline

• Lone parent/+ 1 or more adults 1-2 children households: 23% growth

• Lone parent/+ 1 or more adults 3+ children households: 47% growth

• Other households: 1% decline Migration-led Recalibrated

• One person households: growth of almost 34% (4% increase on Natural Change)

• Couple/+1 or more adults no children households: almost 19% growth (12% increase)

• Couple/+ 1 or more adults 1-2 children households: over 2% decline (12% increase)

• Couple/+ 1 or more adults 3+ children households: stability (37% increase)

• Lone parent/+ 1 or more adults 1-2 children households: almost 35% growth (12% increase)

• Lone parent/+ 1 or more adults 3+ children households: over 44% growth (3% decline)

• Other households: over 6% growth (7% increase)

43

44

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

% of tota l 2011 33.03% 35.59% 15.70% 3.70% 7.53% 0.88% 3.57%

% of tota l 2031 36.54% 36.19% 11.93% 3.03% 8.58% 0.85% 2.88%

% change 2011 to 2031 19.99% 10.29% -17.62% -11.12% 23.68% 3.96% -12.65%

One personCouple/+1 or more

adults no chi ldren

Couple/+ 1 or more

adults 1-2 chi ldren

Couple/+ 1 or more

adults 3+ chi ldren

Lone parent/+ 1 or

more adults 1-2

chi ldren

Lone parent/+ 1 or

more adults 3+

chi ldren

Other households

Derived Forecast - Households

Natural Change - Kettering 2011 - 2031

45

46

47

Key findings for the period 2011-2031 Natural Change

• One person households: 20% growth;

• Couple/+1 or more adults no children households: 10% growth;

• Couple/+ 1 or more adults 1-2 children households: 18% decline

• Couple/+ 1 or more adults 3+ children households: 11% decline

• Lone parent/+ 1 or more adults 1-2 children households: 24% growth

• Lone parent/+ 1 or more adults 3+ children households: 4% growth

• Other households: 13% decline Migration-led Recalibrated

• One person households: growth of over 29% (9% increase on Natural Change)

• Couple/+1 or more adults no children households: almost 19% growth (9% increase)

• Couple/+ 1 or more adults 1-2 children households: over 3% decline (15% increase)

• Couple/+ 1 or more adults 3+ children households: over 6% growth (17% increase)

• Lone parent/+ 1 or more adults 1-2 children households: almost 38% growth (14% increase)

• Lone parent/+ 1 or more adults 3+ children households: over 25% growth (19% increase)

• Other households: over 8% decline (5% increase)

48

49

50

51

52

Key findings for the period 2011-2031 Migration-led Recalibrated

• One person households: growth of almost 49% (25% increase on Natural Change – see below)

• Couple/+1 or more adults no children households: almost 34% growth (26% increase)

• Couple/+ 1 or more adults 1-2 children households: almost 11% growth (32% increase)

• Couple/+ 1 or more adults 3+ children households: almost 20% growth (35% increase)

• Lone parent/+ 1 or more adults 1-2 children households: over 59% growth (33% increase)

• Lone parent/+ 1 or more adults 3+ children households: almost 41% growth (38% increase)

• Other households: over 4% decline (14% increase) Natural Change (for charts see Appendix X)

• One person households: 24% growth;

• Couple/+1 or more adults no children households: 8% growth;

• Couple/+ 1 or more adults 1-2 children households: 21% decline

• Couple/+ 1 or more adults 3+ children households: 15% decline

• Lone parent/+ 1 or more adults 1-2 children households: 26% growth

• Lone parent/+ 1 or more adults 3+ children households: 3% growth

• Other households: 18% decline.

53

54

55

56

57

Key findings for the period 2011-2031 Migration-led Recalibrated

• One person households: growth of over 29% (3% increase on Natural Change – see below)

• Couple/+1 or more adults no children households: over 8% growth (3% increase)

• Couple/+ 1 or more adults 1-2 children households: almost 11% decline (8% increase)

• Couple/+ 1 or more adults 3+ children households: almost 6% decline (9% increase)

• Lone parent/+ 1 or more adults 1-2 children households: almost 31% growth (8% increase)

• Lone parent/+ 1 or more adults 3+ children households: over 26% growth (no change)

• Other households: over 10% decline (1% increase) Natural Change (for charts see Appendix X)

• One person households: 26% growth;

• Couple/+1 or more adults no children households: 5% growth;

• Couple/+ 1 or more adults 1-2 children households: 19% decline

• Couple/+ 1 or more adults 3+ children households: 15% decline

• Lone parent/+ 1 or more adults 1-2 children households: 23% growth

• Lone parent/+ 1 or more adults 3+ children households: 26% growth

• Other households: 11% decline

58

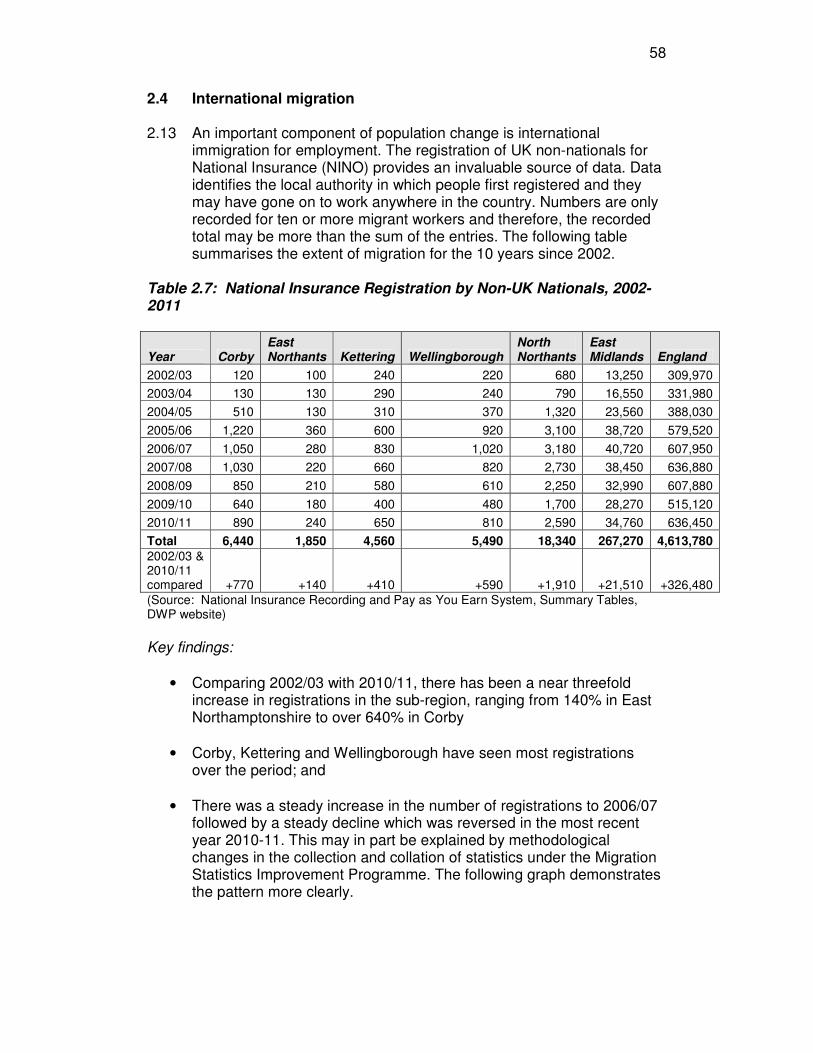

2.4 International migration 2.13 An important component of population change is international

immigration for employment. The registration of UK non-nationals for National Insurance (NINO) provides an invaluable source of data. Data identifies the local authority in which people first registered and they may have gone on to work anywhere in the country. Numbers are only recorded for ten or more migrant workers and therefore, the recorded total may be more than the sum of the entries. The following table summarises the extent of migration for the 10 years since 2002.

Table 2.7: National Insurance Registration by Non-UK Nationals, 2002-2011

Year Corby East Northants Kettering Wellingborough

North Northants

East Midlands England

2002/03 120 100 240 220 680 13,250 309,970

2003/04 130 130 290 240 790 16,550 331,980

2004/05 510 130 310 370 1,320 23,560 388,030

2005/06 1,220 360 600 920 3,100 38,720 579,520

2006/07 1,050 280 830 1,020 3,180 40,720 607,950

2007/08 1,030 220 660 820 2,730 38,450 636,880

2008/09 850 210 580 610 2,250 32,990 607,880

2009/10 640 180 400 480 1,700 28,270 515,120

2010/11 890 240 650 810 2,590 34,760 636,450

Total 6,440 1,850 4,560 5,490 18,340 267,270 4,613,780

2002/03 & 2010/11 compared +770 +140 +410 +590 +1,910 +21,510 +326,480

(Source: National Insurance Recording and Pay as You Earn System, Summary Tables, DWP website) Key findings:

• Comparing 2002/03 with 2010/11, there has been a near threefold increase in registrations in the sub-region, ranging from 140% in East Northamptonshire to over 640% in Corby

• Corby, Kettering and Wellingborough have seen most registrations over the period; and

• There was a steady increase in the number of registrations to 2006/07 followed by a steady decline which was reversed in the most recent year 2010-11. This may in part be explained by methodological changes in the collection and collation of statistics under the Migration Statistics Improvement Programme. The following graph demonstrates the pattern more clearly.

59

National Insurance Registrations by Non UK Nationals by Year

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/2011

Nu

mb

er

of

Re

gis

tra

tio

ns

Corby

East Northants

Kettering

Wellingborough

North Northants

60

2.14 The following table identifies the main countries from which people have migrated.

Table 2.8: NINO Registrations of 500 people or more in North Northants. from 1st January 2002 to September 2011

Total Poland Slovak Rep

Rep of Latvia

India Hungary Rep of Lithuania

Romania

Area

(000s) 000s) (000s) 000s) (000s) 000s) 000s) 000s)

Corby 6.96 2.65 0.84 0.74 0.09 0.4 0.33 0.32

East Northants

1.95 0.41 0.08 0.04 0.15 0.11 0.04 0.11

Kettering 4.86 1.49 0.46 0.09 0.41 0.15 0.23 0.06

Wellingborough 5.86 2.67 0.18 0.47 0.42 0.26 0.14 0.09

North Northants

19.63 7.22 1.56 1.34 1.07 0.92 0.74 0.58

(Source: DWP Tabulation Tool, DWP website)

Key findings:

• 6 of 8 the central/east European countries which acceded to the EU in 2004 are featured, and account for almost two thirds of those registering between 2002 and 2011; the only other country from which 500 or more people migrated was India.

2.15 A new data source available from ONS concerns Indicative Immigration

Estimates for Short Term Migrants (workers and students) and data is available for the three years to June 2010.

Table 2.9: immigration estimates for short term migrants, 2007-2010 Area 2007/08 2008/09 2009/10 Totals

Corby 122 47 81 250

East Northamptonshire 28 21 21 70

Kettering 73 25 49 147

Wellingborough 92 26 58 176

Totals 315 119 209 643 (Source: National Insurance Recording and Pay as You Earn System, Summary Tables, DWP website) Key findings:

• A total of 643 short term migrants have been allocated to the sub-region, with the largest number in Corby.

61

2.5 Internal migration 2.16 Internal migration refers to population movement within England and

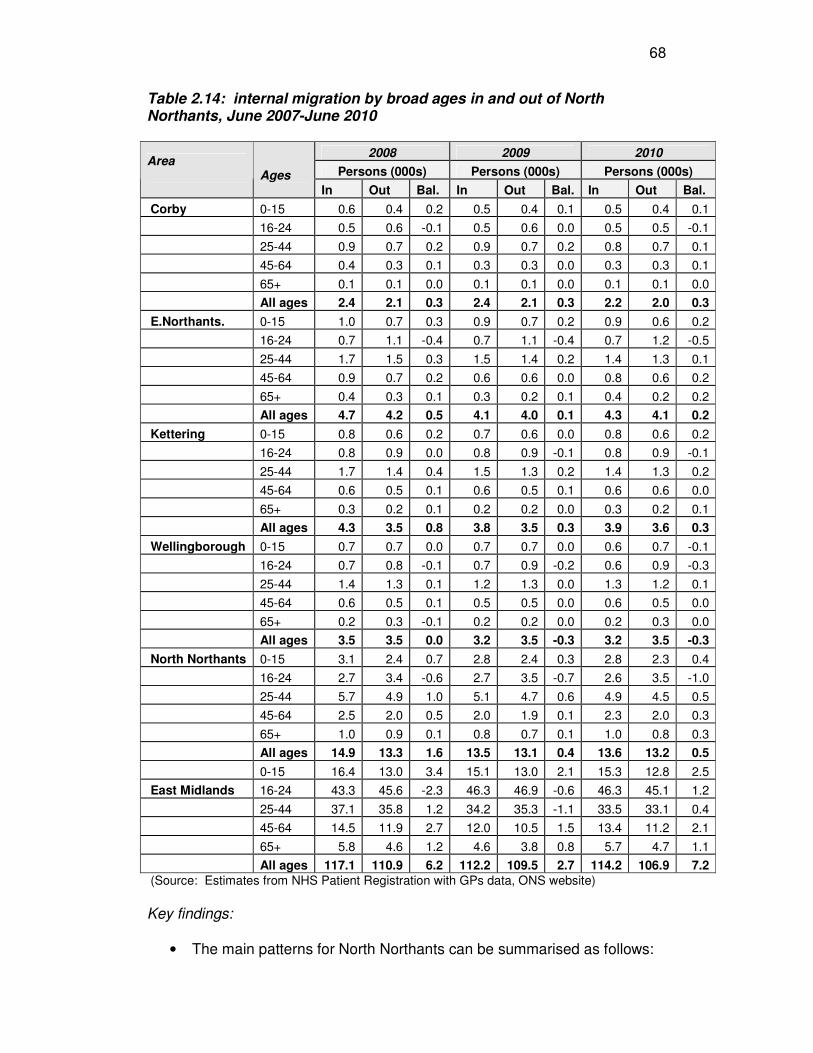

Wales. Movement between North Northamptonshire, regions and local authority areas can be monitored using NHS patient registration data. Such data is reliant on people registering with a GP and those groups who are recognised to register at lower rates include students, especially male students and young men, but conversely, families and older people are more likely to register. Please note that figures are rounded to the nearest 10 or 100 by NHSCR and therefore, totals may vary from the sum. The following table provides a starting point for understanding patterns of internal migration by examining the movement of people into North Northants. by region for the most recent year to June 2010.

Table 2.10: internal migration into North Northants from regions for the year ending June 2010

Origin Number of In-migrants

Those Moving within North Northants.

In-migrants Excluding those Moving within North Northants.

North East 150 150

North West 380 380

Yorkshire and The Humber 500 500

East Midlands 6,740 3,360 3,380

West Midlands 620 620

East 2,290 2,290

London 860 860

South East 1,260 1,260

South West 450 450

Wales 180 180

(Source: Estimates from NHS Patient Registration with GPs data, ONS website)

Key findings:

• Not surprisingly, most movement is from within North Northants and the East Midlands but this is followed by the East region then the south east. It is interesting to note that even when London and the South East are combined (2,140 people), this is still less than migration from the East region. These patterns are more clearly seen on the following map.

62

2.17 The following table reviews the movement of people out of North

Northants. by region for the most recent year to June 2010.

63

Table 2.11: internal migration out of North Northants to regions for the year ending June 2010

Destination Number Out Migrants

Those Moving within North Northants.

Out Migrants Excluding those Moving within North Northants.

North East 180 180

North West 420 420

Yorkshire and The Humber 580 580

East Midlands 6,410 3,360 3,050

West Midlands 700 700

East 1,830 1,830

London 730 730

South East 1,200 1,200

South West 620 620

Wales 230 230

(Source: Estimates from NHS Patient Registration with GPs data, ONS website)

Key findings:

• Not surprisingly, most movement out is within North Northants and the East Midlands and this is followed by the East region then the south east. It is interesting to note that when London and the South East are combined (1,930 people), this is almost the same as migration to the East region. These patterns are more clearly seen on the following map.

64

65

2.18 The following table and map identify the net effect of regional migration patterns.

Table 2.12: net migration into and out of North Northants from/to regions for the two years ending June 2010

Regions In 2009 In 2010 Out 2009 Out 2010 Net Migration

East 2,190 2,290 1,750 1,830 +900

London 1,000 860 720 730 +410

South East 1,300 1,260 1,130 1,200 +230

East Midlands 3,000 3,380 3,170 3,050 +160

North West 480 380 450 420 -10

North East 190 150 180 180 -20

Yorkshire and The Humber 460 500 510 580 -130

West Midlands 670 620 730 700 -140

South West 400 450 600 620 -370 (Source: Internal Migration Statistics, Office for National Statistics) Note: Excludes LAs within North Northants

Key findings:

• The strongest gains were from the East then the London regions; the main losses were to the south west region, a favourite location for retirement.

66

67

2.19 The following table turns to the local authority level and focuses on the

net effect of internal migration into and out of North Northants and constituent local authority areas for the 3 years June 2007-10.

Table 2.13: in and outmigration by district, June 2007-June2010

2007-08 2008-09 2009-10

Persons (000s) Persons (000s) Persons (000s) Local Authority In Out Balance In Out Balance In Out Balance

Corby 2.4 2.1 +0.3 2.4 2.1 +0.3 2.2 2.0 +0.3

East Northants. 4.7 4.2 +0.5 4.1 4.0 +0.1 4.3 4.1 +0.2

Kettering 4.3 3.5 +0.8 3.8 3.5 +0.3 3.9 3.6 +0.3

Wellingborough 3.5 3.5 +0.0 3.2 3.5 -0.3 3.2 3.5 -0.3

North Northants 14.9 13.3 +1.6 13.5 13.1 +0.4 13.6 13.2 +0.4

East Midlands 117.1 110.9 +6.2 112.2 109.5 +2.7 114.2 106.9 +7.2

(Source: Estimates from NHS Patient Registration with GPs data, ONS website)

Key findings:

• North Northants gained 1,600 people in 2007-08 but this fell to 400 in each of the following years, an overall gain of 2,400 people.

• The effect for constituent local authorities was net gains over 3 years of:

o 900 people in Corby; o 800 people in East Northants.; o 1,400 people in Kettering;

• but a loss of:

o 600 people in Wellingborough. 2.20 Data on internal migration by age enables limited profiling of the types

of people and households moving in and out of North Northants for example, those aged 0-15 can be associated with parents aged 25-44 to indicate families with children; those aged 16-24 will include students and those aged 65+ are pensioner households. The following table summarises patterns for the 3 years 2007-10.

68

Table 2.14: internal migration by broad ages in and out of North Northants, June 2007-June 2010

2008 2009 2010

Persons (000s) Persons (000s) Persons (000s) Area

Ages In Out Bal. In Out Bal. In Out Bal.

Corby 0-15 0.6 0.4 0.2 0.5 0.4 0.1 0.5 0.4 0.1

16-24 0.5 0.6 -0.1 0.5 0.6 0.0 0.5 0.5 -0.1

25-44 0.9 0.7 0.2 0.9 0.7 0.2 0.8 0.7 0.1

45-64 0.4 0.3 0.1 0.3 0.3 0.0 0.3 0.3 0.1

65+ 0.1 0.1 0.0 0.1 0.1 0.0 0.1 0.1 0.0

All ages 2.4 2.1 0.3 2.4 2.1 0.3 2.2 2.0 0.3

E.Northants. 0-15 1.0 0.7 0.3 0.9 0.7 0.2 0.9 0.6 0.2

16-24 0.7 1.1 -0.4 0.7 1.1 -0.4 0.7 1.2 -0.5

25-44 1.7 1.5 0.3 1.5 1.4 0.2 1.4 1.3 0.1

45-64 0.9 0.7 0.2 0.6 0.6 0.0 0.8 0.6 0.2

65+ 0.4 0.3 0.1 0.3 0.2 0.1 0.4 0.2 0.2

All ages 4.7 4.2 0.5 4.1 4.0 0.1 4.3 4.1 0.2

Kettering 0-15 0.8 0.6 0.2 0.7 0.6 0.0 0.8 0.6 0.2

16-24 0.8 0.9 0.0 0.8 0.9 -0.1 0.8 0.9 -0.1

25-44 1.7 1.4 0.4 1.5 1.3 0.2 1.4 1.3 0.2

45-64 0.6 0.5 0.1 0.6 0.5 0.1 0.6 0.6 0.0

65+ 0.3 0.2 0.1 0.2 0.2 0.0 0.3 0.2 0.1

All ages 4.3 3.5 0.8 3.8 3.5 0.3 3.9 3.6 0.3

Wellingborough 0-15 0.7 0.7 0.0 0.7 0.7 0.0 0.6 0.7 -0.1

16-24 0.7 0.8 -0.1 0.7 0.9 -0.2 0.6 0.9 -0.3

25-44 1.4 1.3 0.1 1.2 1.3 0.0 1.3 1.2 0.1

45-64 0.6 0.5 0.1 0.5 0.5 0.0 0.6 0.5 0.0

65+ 0.2 0.3 -0.1 0.2 0.2 0.0 0.2 0.3 0.0

All ages 3.5 3.5 0.0 3.2 3.5 -0.3 3.2 3.5 -0.3

North Northants 0-15 3.1 2.4 0.7 2.8 2.4 0.3 2.8 2.3 0.4

16-24 2.7 3.4 -0.6 2.7 3.5 -0.7 2.6 3.5 -1.0

25-44 5.7 4.9 1.0 5.1 4.7 0.6 4.9 4.5 0.5

45-64 2.5 2.0 0.5 2.0 1.9 0.1 2.3 2.0 0.3

65+ 1.0 0.9 0.1 0.8 0.7 0.1 1.0 0.8 0.3

All ages 14.9 13.3 1.6 13.5 13.1 0.4 13.6 13.2 0.5

0-15 16.4 13.0 3.4 15.1 13.0 2.1 15.3 12.8 2.5

East Midlands 16-24 43.3 45.6 -2.3 46.3 46.9 -0.6 46.3 45.1 1.2

25-44 37.1 35.8 1.2 34.2 35.3 -1.1 33.5 33.1 0.4

45-64 14.5 11.9 2.7 12.0 10.5 1.5 13.4 11.2 2.1

65+ 5.8 4.6 1.2 4.6 3.8 0.8 5.7 4.7 1.1

All ages 117.1 110.9 6.2 112.2 109.5 2.7 114.2 106.9 7.2

(Source: Estimates from NHS Patient Registration with GPs data, ONS website) Key findings:

• The main patterns for North Northants can be summarised as follows:

69

o a gain of 1,400 people aged 0-15 and 2,100 aged 25-44

suggests that families with children are being attracted to the area;

o a loss of 2,300 people aged 16-25 suggests that more students and those of first working age are leaving the area; and

o gains of 900 in those aged 45-64 and 500 in those aged 65+ indicates that the area is also proving attractive to older age groups.

• For Corby, East Northants and Kettering, the same patterns are evident though Kettering made only very small gains in the older age groups.

• Wellingborough is the exception with only a small gain in those aged 25-44 (+200); small losses in other age groups and half the total loss accounted for by those aged 16-25.

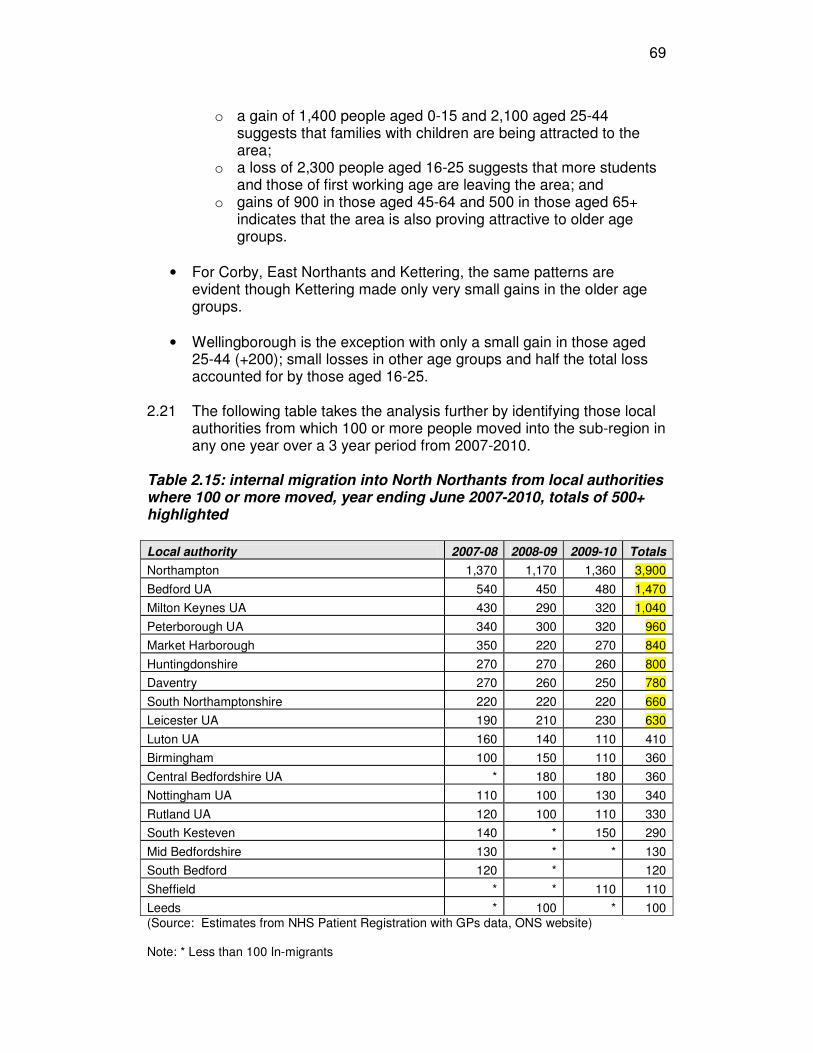

2.21 The following table takes the analysis further by identifying those local

authorities from which 100 or more people moved into the sub-region in any one year over a 3 year period from 2007-2010.

Table 2.15: internal migration into North Northants from local authorities where 100 or more moved, year ending June 2007-2010, totals of 500+ highlighted

Local authority 2007-08 2008-09 2009-10 Totals

Northampton 1,370 1,170 1,360 3,900

Bedford UA 540 450 480 1,470

Milton Keynes UA 430 290 320 1,040

Peterborough UA 340 300 320 960

Market Harborough 350 220 270 840

Huntingdonshire 270 270 260 800

Daventry 270 260 250 780

South Northamptonshire 220 220 220 660

Leicester UA 190 210 230 630

Luton UA 160 140 110 410

Birmingham 100 150 110 360

Central Bedfordshire UA * 180 180 360

Nottingham UA 110 100 130 340

Rutland UA 120 100 110 330

South Kesteven 140 * 150 290

Mid Bedfordshire 130 * * 130

South Bedford 120 * 120

Sheffield * * 110 110

Leeds * 100 * 100

(Source: Estimates from NHS Patient Registration with GPs data, ONS website) Note: * Less than 100 In-migrants

70

Key findings:

• Northampton provided the largest number of migrants into North Northants followed by Bedford, Milton Keynes, Peterborough, Market Harborough, Huntingdonshire, Daventry, South Northants. and Leicester. These patterns are most clearly seen on the following map which focuses on the larger flows of 200 or more people.

Please note: this data is also available for each local authority area.

71

72

2.22 The following table takes the analysis further by identifying those local authorities from which 100 or more people moved into the sub-region in any one year over a 3 year period from 2007-2010.

Table 2.16: internal migration out of North Northants into local authorities where 100 or more moved, 2007-2010, totals of 500+ highlighted

Local Authority 2007-08 2008-09 2009-10 Totals

Northampton 1,030 1,060 1,030 3,120

Bedford UA 390 310 380 1,080

Daventry 280 270 220 770

Market Harborough 220 270 240 730

Milton Keynes UA 250 240 240 730

Peterborough UA 210 200 220 630

Huntingdonshire 230 220 160 610

South Northamptonshire 210 180 190 580

Leicester UA 190 200 170 560

Nottingham UA 160 180 180 520

Birmingham 120 170 160 450

Rutland UA 140 160 140 440

South Kesteven 130 160 150 440

Sheffield 130 120 150 400

Leeds 120 100 140 360

Central Bedfordshire UA * 110 110 220

Coventry * 100 100 200

Cornwall UA * * 100 100

Source: Estimates from NHS Patient Registration with GPs data, ONS website * Less than 100 Out Migrants Key findings:

• Northampton attracted the largest number of migrants out of North Northants followed by Bedford, Daventry, Market Harborough, Milton Keynes and Peterborough. These patterns are most clearly seen on the following map which focuses on the larger flows of 200 or more people.

Please note: this data is also available for each local authority area.

73

74

2.23 The following table examines the net effect of movement in and out of the sub-region from 2007-2010 for the local authorities identified above. Table 2.17: net effect of internal migration in and out of North Northants into 2007-2010 by main local authority areas, totals of 150+/- highlighted

Local Authority In Out Net effect

Northampton 3,900 Northampton 3,120 +780

Bedford UA 1,470 Bedford UA 1,080 +390

Peterborough UA 960 Peterborough UA 630 +330

Milton Keynes UA 1,040 Milton Keynes UA 730 +310

Luton UA 410 Luton UA 150 +260

Huntingdonshire 800 Huntingdonshire 610 +190

Central Bedfordshire UA 360 Central Bedfordshire UA 220 +140

Market Harborough 840 Market Harborough 730 +110

South Northamptonshire 660 South Northamptonshire 580 +80

Leicester UA 630 Leicester UA 560 +70

Daventry 780 Daventry 770 +10

Birmingham 360 Birmingham 450 -90

Rutland UA 330 Rutland UA 440 -110

South Kesteven 290 South Kesteven 440 -150

Nottingham UA 340 Nottingham UA 520 -180

Leeds 100 Leeds 360 -260

Sheffield 110 Sheffield 400 -290

(Source: Estimates from NHS Patient Registration with GPs data, ONS website) Note: * Less than 100 Out Migrants Key findings:

• The main patterns for North Northants can be summarised as follows:

o Strong net gains from Northampton, Bedford, Peterborough, Milton Keynes, Luton and Huntingdonshire;

o A near equal exchange of population with Daventry; and o Clear net losses of people to Sheffield, Leeds, Nottingham and

South Kesteven. 2.24 The following map highlights net migration of 100 or more people for

the 2 years to June 2010.

75

76

2.6 Commuting/travel to work 2.25 Benchmarks for identifying a housing market catchment area are that

either 75% of people live and work within a defined boundary (known as the ‘live: work’ or ‘Travel to Work Area’) or that 75% of home moves take place within a defined boundary. Catchment areas can be noticeably different according to home moves compared with travel to work. For example, migration patterns are often more extensive from higher cost housing areas whose households have greater equity and vice versa. Consequently, the ‘live: work’ is a useful indicator of housing market.

2.26 Analysis of commuting patterns was at the time of completion of the

report mainly dependent on 2001 Census data and will need updating once the results of the 2011 Census are available. The following table summarises the extent of commuting in and out of North Northamptonshire in 2001.

Table 2.18: travel into and out of North Northamptonshire to work, 2001

Local Authority Corby East

Northants. Kettering Wellingborough North

Northants.

Travel in 4,202 3,666 3,832 5,769 17,469

Travel out 2,483 11,882 8,725 10,761 32,003

Net effect 1,719 -8,216 -4,893 -4,992 -14,534

(Source: Table 107 UK Travel Flows, 2001 Census, NOMIS website) Key findings:

• In 2001, 14,500 more people travelled to work outside the area than travelled in; and

• This pattern was consistent for all local authorities except Corby where the reverse was the case and more people travelled in than out.

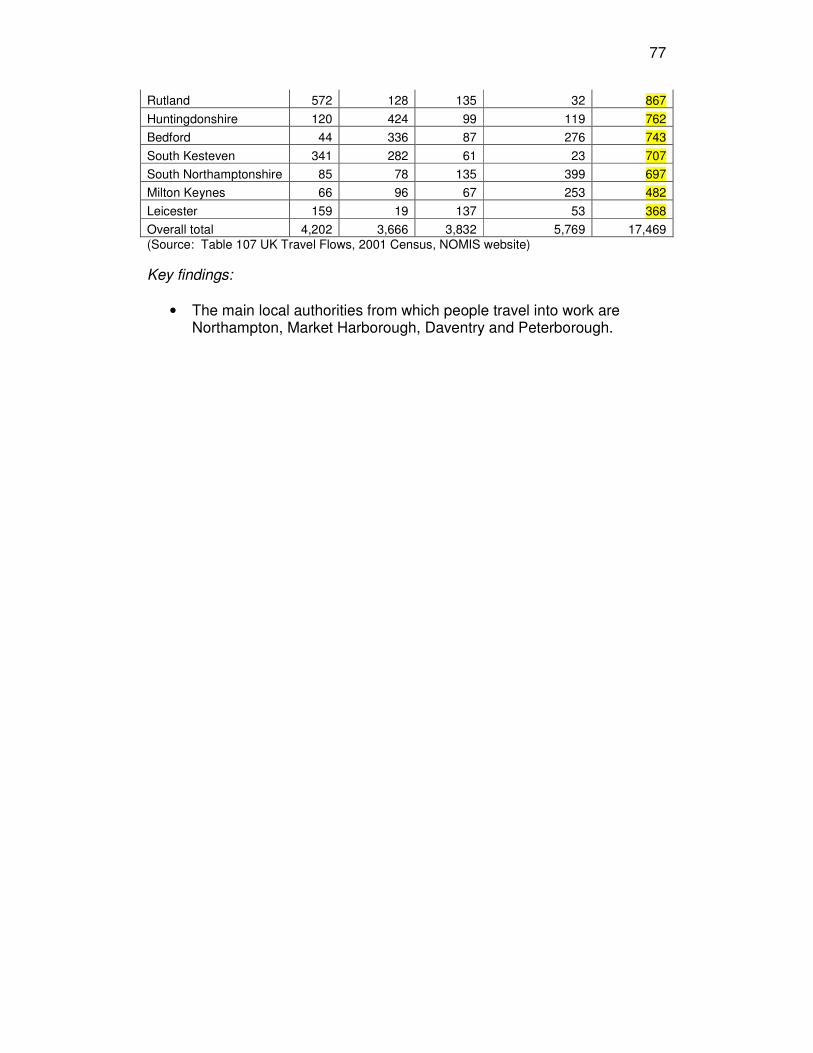

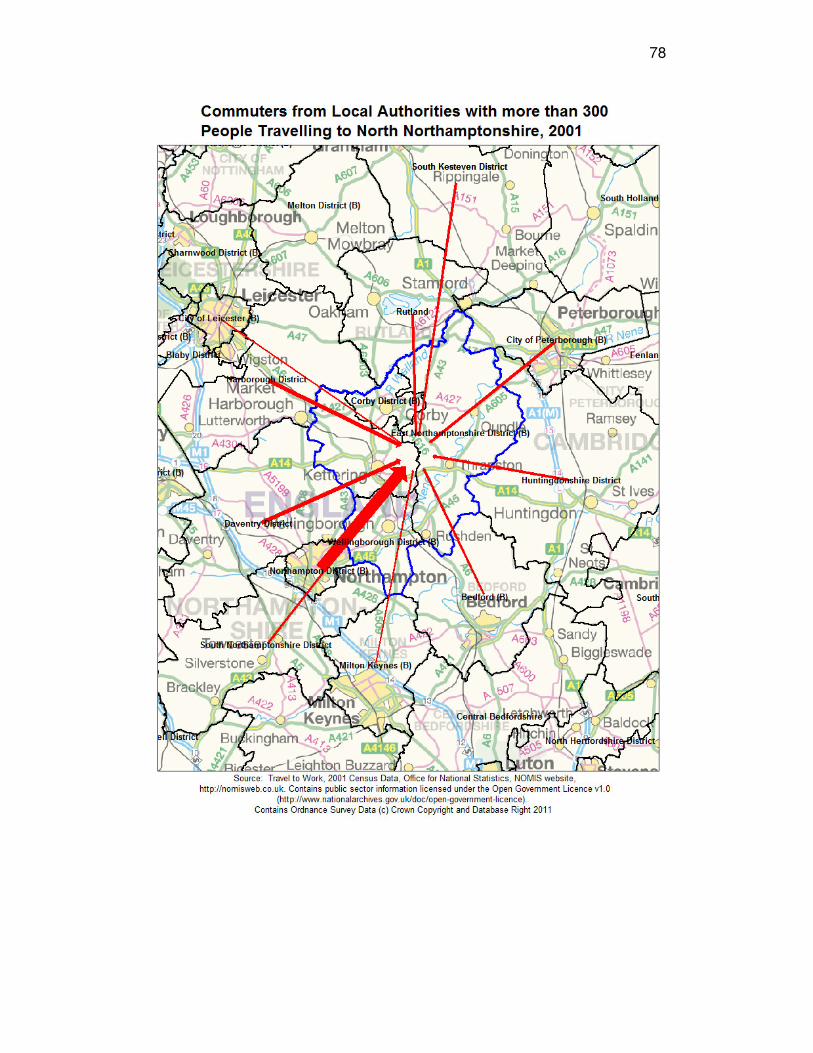

2.27 The following table and map address the question, ‘where do people

work who live in North Northamptonshire’? and identify the principal flows. The 75% level is equivalent to 13,100 people.

Table 2.19: travel into work in North Northamptonshire from local authorities where 300 or more travel, 2001, 75% level identified

Local Authority Corby East

Northants. Kettering Wellingborough North

Northants.

Northampton 466 588 1,000 2,505 4,559

Market Harborough 613 73 597 131 1,414

Daventry 178 120 438 527 1,263

Peterborough 260 579 107 58 1,004

77

Rutland 572 128 135 32 867

Huntingdonshire 120 424 99 119 762

Bedford 44 336 87 276 743

South Kesteven 341 282 61 23 707

South Northamptonshire 85 78 135 399 697

Milton Keynes 66 96 67 253 482

Leicester 159 19 137 53 368

Overall total 4,202 3,666 3,832 5,769 17,469

(Source: Table 107 UK Travel Flows, 2001 Census, NOMIS website)

Key findings:

• The main local authorities from which people travel into work are Northampton, Market Harborough, Daventry and Peterborough.

78

79

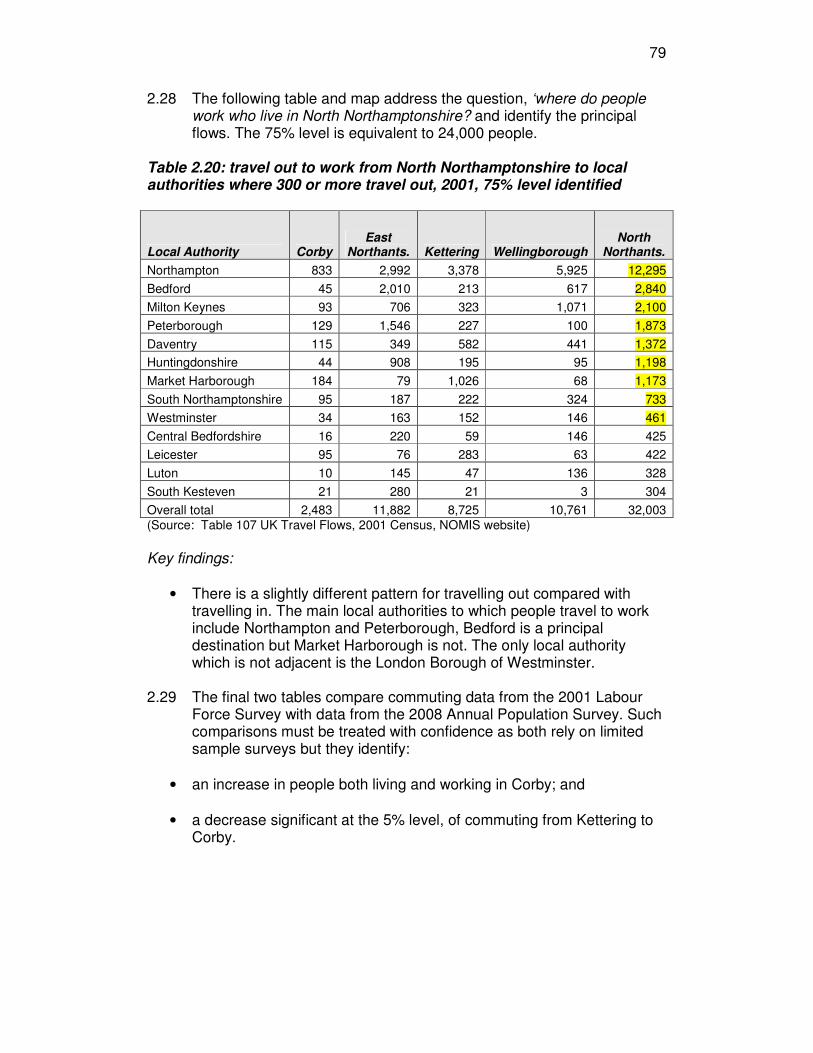

2.28 The following table and map address the question, ‘where do people work who live in North Northamptonshire? and identify the principal flows. The 75% level is equivalent to 24,000 people. Table 2.20: travel out to work from North Northamptonshire to local authorities where 300 or more travel out, 2001, 75% level identified

Local Authority Corby East

Northants. Kettering Wellingborough North

Northants.

Northampton 833 2,992 3,378 5,925 12,295

Bedford 45 2,010 213 617 2,840

Milton Keynes 93 706 323 1,071 2,100

Peterborough 129 1,546 227 100 1,873

Daventry 115 349 582 441 1,372

Huntingdonshire 44 908 195 95 1,198

Market Harborough 184 79 1,026 68 1,173

South Northamptonshire 95 187 222 324 733

Westminster 34 163 152 146 461

Central Bedfordshire 16 220 59 146 425

Leicester 95 76 283 63 422

Luton 10 145 47 136 328

South Kesteven 21 280 21 3 304

Overall total 2,483 11,882 8,725 10,761 32,003

(Source: Table 107 UK Travel Flows, 2001 Census, NOMIS website) Key findings:

• There is a slightly different pattern for travelling out compared with travelling in. The main local authorities to which people travel to work include Northampton and Peterborough, Bedford is a principal destination but Market Harborough is not. The only local authority which is not adjacent is the London Borough of Westminster.

2.29 The final two tables compare commuting data from the 2001 Labour

Force Survey with data from the 2008 Annual Population Survey. Such comparisons must be treated with confidence as both rely on limited sample surveys but they identify:

• an increase in people both living and working in Corby; and

• a decrease significant at the 5% level, of commuting from Kettering to Corby.

80

81

Table 2.21: place of residence commuter flows: where do workers live? (commuters in), 2001 and 2008

Corby East Northamptonshire Kettering Wellingborough

Workplace 2001 2008

Change Significant at 5% level 2001 2008

Change Significant at 5% level 2001 2008

Change Significant at 5% level 2001 2008

Change Significant at 5% level

Residence % % % % % % % %

Corby 59.0 73.2 No 0.0 0.0 n/a 3.4 5.8 No 0.0 0.0 n/a

East Northamptonshire 3.4 4.9 No 66.3 68.3 No 0.0 3.7 n/a 9.6 10.9 No

Kettering 20.0 7.6 Yes 8.6 8.9 No 72.8 67.7 No 8.6 8.3 No

Wellingborough 0.0 0.0 n/a 8.6 5.8 No 6.3 8.8 No 65.8 61.9 No

Peterborough 1.2 2.1 No 2.6 1.6 No 0.0 0.0 n/a 0.0 0.0 n/a

Rutland 3.0 1.8 No 0.0 0.0 n/a 0.0 0.0 n/a 0.0 0.0 n/a

Northampton 0.0 0.0 n/a 0 0 n/a 0.0 0 n/a 4.9 8.7 No

(Source: 2001 Labour Force Survey and 2008 Annual Population Survey, APS Commuter Flow, Neighbourhood Statistics Website) Note: Some data shows a commuting linkage but estimates are not reliable

82

Table 2.22: workplace commuter flows: where do residents work? (commuters out), 2001 and 2008

Corby East Northamptonshire Kettering Wellingborough

Residence 2001 2008

Change Significant at 5% level 2001 2008

Change Significant at 5% level 2001 2008

Change Significant at 5% level 2001 2008

Change Significant at 5% level

Workplace % % % % % % % %

Corby 81.1 77.1 No 2.4 3.3 No 12.8 5.1 Yes 0.0 0.0 n/a

East Northamptonshire 0.0 0.0 n/a 43.3 40.9 No 5.0 5.3 No 5.9 4.0 No

Kettering 5.8 7.6 n/a 0.0 3.1 n/a 58.2 56.7 No 5.9 8.5 No

Wellingborough 0.0 0.0 n/a 9.2 8.7 No 7.3 6.6 No 66.0 56.7 No

Peterborough 0.0 0.0 n/a 0.0 0.0 n/a 0.0 0.0 n/a 0.0 0.0 n/a

Rutland 0.0 0.0 n/a 0.0 0.0 n/a 0.0 0.0 n/a 0.0 0.0 n/a

Northampton 0.0 0.0 n/a 6.3 9.0 No 5.9 8.1 No 12.0 8.7 No

Milton Keynes 0.0 0.0 n/a 0.0 3.7 n/a 0.0 0.0 n/a 4.3 6.7 No

North Hertfordshire 0.0 0.0 n/a 0.0 5.7 n/a 0.0 0.0 n/a 0.0 3.7 n/a

Leicester 0.0 0.0 n/a 0.0 0.0 n/a 0.0 2.8 n/a 0.0 0.0 n/a

Bedford 0.0 0.0 n/a 5.1 7.2 No 0.0 0.0 n/a 0.0 0 n/a

(Source: 2001 Labour Force Survey and 2008 Annual Population Survey, APS Commuter Flow, Neighbourhood Statistics Website) Note: Some data shows a commuting linkage but estimates are not reliable

83

3.0 What choices do consumers have in the housing market? A

profile of housing stock and supply 3.1 Introduction 3.1 This section reviews patterns and trends in the housing market across

the area as the basis for understanding the balance between supply and demand and the future requirement for housing. A distinction is made between housing stock - the number of dwellings - and housing supply - the number of dwellings available annually to rent or purchase due to turnover from the existing stock and new supply from construction, conversions and bringing empty homes back into use.

3.2 Setting the baseline: patterns and trends in the housing stock Property type 3.2 An authoritative and up-to-date breakdown of the dwelling stock by

type will need to be added once 2011 Census data is released. The following table summarises the baseline position by accommodation type in 2001 and the sub-section closes with a detailed estimate of stock by tenure. Table 3.24 provides a detailed estimate of the current position.

84

Table 3.1: accommodation type, 2001

Corby E.Northants. Wellingborough Kettering N. Northants E.Midlands England

Property Type No % No % No % No % No % % %

Whole house or bungalow: Detached 3,958 17.4 11,546 35.4 10,424 29.2 8,108 26.1 34,036 27.9 32.2 22.5

Whole house or bungalow: Semi-detached 8,362 36.8 11,162 34.2 12,697 35.6 10,715 34.5 42,936 35.2 36.3 31.6

Whole house or bungalow: Terraced (including end terrace) 7,495 33.0 7,377 22.6 9,078 25.4 9,054 29.2 33,004 27.1 21.3 25.8

Flat; maisonette or apartment: Purpose Built block of flats or tenement 2,507 11.0 1,819 5.6 2,676 7.5 2,304 7.4 9,306 7.6 7.2 14.0

Flat; maisonette or apartment: Part of a converted or shared house (including bed-sits) 211 0.9 274 0.8 468 1.3 457 1.5 1,410 1.2 1.7 4.6

Flat; maisonette or apartment: In commercial building 135 0.6 293 0.9 270 0.8 202 0.7 900 0.7 0.9 1.1

Caravan or other mobile/temporary structure 42 0.2 138 0.4 59 0.2 178 0.6 417 0.3 0.4 0.4

Total Dwellings 22,710 100.0 32,609 100.0 35,672 100.0 31,018 100.0 122,009 100.0 100.0 100.0

(Source: KS16 2001 Census)

Key findings:

• Compared with the national pattern, the main differences are the higher proportions of detached and semi-detached houses and the lower proportions of flats. These difference are less marked when compared with the regional pattern; and

• Corby has the most distinctive housing profile with below average proportions of detached houses and above average proportions of terraced houses.

85

Tenure 3.3 The following table summarises the baseline position in 2001 and is followed by the current estimate. Table 3.2: tenure type, 2001

Corby E.Northants. Wellingborough Kettering N. Northants E. Midlands England

Tenure No % No % No % No % No % % %

Owner occupied: Owns outright 4,597 20.9 9,030 28.9 8,172 27.2 10,079 29.3 31,878 27.1 30.8 29.2

Owner occupied: with a mortgage or loan 9,132 41.5 14,699 47.0 13,307 44.2 16,313 47.4 53,451 45.4 40.8 38.9

Owner occupied: shared ownership 73 0.3 1,425 4.6 255 0.8 84 0.2 497 0.4 0.6 0.7

Rented from: a local authority 6,127 27.8 0 0 4,885 16.2 3,726 10.8 16,078 13.7 13.8 13.2

Rented from: Housing Association 696 3.2 3,127 10.0 1,004 3.3 964 2.8 5,791 4.9 3.7 6.1

Rented from: Private landlord or letting agency 747 3.4 1,948 6.2 1,565 5.2 2,204 6.4 6,464 5.5 7.3 8.8

Rented from: Other 641 2.9 1,015 3.2 894 3.0 1,072 3.1 3,622 3.1 3.0 3.2

All Households 22,013 100.0 31,244 100.0 30,082 100.0 34,442 100.0 117,781 100.0 100.0 100.0

(Source: KS18 2001 Census) Note: Although recorded as such, there were no local authority homes in East Northants at the time of the 2001 Census and need. This is a common inaccuracy arising from former local authority tenants continuing to record themselves as local authority tenants and these figures have been added to the housing association total.

Key findings:

86

• Compared with the national pattern, the main difference is the lower proportion of private rented housing. This difference is less marked when compared with the regional pattern; and

• Corby has the most distinctive housing profile with below average proportions of home ownership and private renting and above average proportions of social renting.

87

3.4 The following table summarises the estimated position by tenure at 2011 but owner occupation and private renting are not separated.

Table 3.3: tenure at 2011

Local authority

Housing association

Other Public Sector

Owner Occupied &

Private Rented Total

Area No. % No. % No. % No. % No. %

Corby 4,808 18.4 809 3.1 0 0.0 20,490 78.5 26,100 100.0

East Northants. 0 0.0 4,933 13.4 10 0.0 31,770 86.5 36,710 100.0

Kettering 3,812 9.4 1,593 3.9 5 0.0 35,110 86.6 40,520 100.0

Wellingborough 12 0.0 5,848 17.6 0 0.0 27,390 82.4 33,250 100.0

North Northants 8,632 6.3 13,183 9.7 15 0.0 114,760 84.0 136,580 100.0

East Midlands - 9.5 - 6.4 0.2 - 83.8 - 100.0

England - 7.9 - 9.9 0.3 - 82.0 - 100.0

(Source: Table 100, Dwelling Stock by District, CLG website)

Key findings

• As the owner occupied and private rented totals are not disaggregated, it is difficult to compare this breakdown with that of 2001 above, other than to identify a fall in the proportion of social housing from 18.5-16% of the stock total. A further and more detailed estimate of stock by tenure is provided at Table 3.24 below.

88

Number of rooms and bedrooms

3.5 A key indicator when profiling the supply of housing is the number of bedrooms. Whilst this data will be available from the 2011 Census, only the number of habitable rooms was recorded in 2001, i.e. excluding bathrooms, toilets, halls or landings. The following table summarises the baseline position by number of rooms in 2001.

Table 3.4: number of rooms

Corby E.Northants. Kettering Wellingborough N. Northants E.Midlands England

Rooms No % No % No % No % No % % %

1 room 127 0.6 64 0.2 176 0.6 106 0.3 473 0.4 0.4 0.9

2 rooms 503 2.3 336 1.1 581 1.9 463 1.3 1,883 1.6 1.6 2.5

3 rooms 1,705 7.7 1,453 4.7 1,987 6.6 2,023 5.9 7,168 6.1 6.5 9.2

4 rooms 3,631 16.5 5,086 16.3 4,955 16.5 6,550 19.0 20,222 17.2 18.1 20.0

5 rooms 7,656 34.8 8,861 28.4 9,524 31.7 10,093 29.3 36,134 30.7 30.2 27.1

6 rooms 5,244 23.8 6,805 21.8 6,582 21.9 7,515 21.8 26,146 22.2 22.3 20.5

7 rooms 1,825 8.3 3,519 11.3 2,873 9.6 3,573 10.4 11,790 10.0 9.7 9.2

8 or more rooms 1,322 6.0 5,120 16.4 3,404 11.3 4,119 12.0 13,965 11.9 11.3 10.6

All Occupied Household Spaces 22,013 100.0 31,244 100.0 30,082 100.0 34,442 100.0 117,781 100.0 100.0 100.0

(Source: UV57 2001 Census)

89

Key findings:

• The number of rooms was close to the regional average but, when compared with the national pattern, there are fewer homes with a smaller number of rooms and a larger proportion with more rooms.

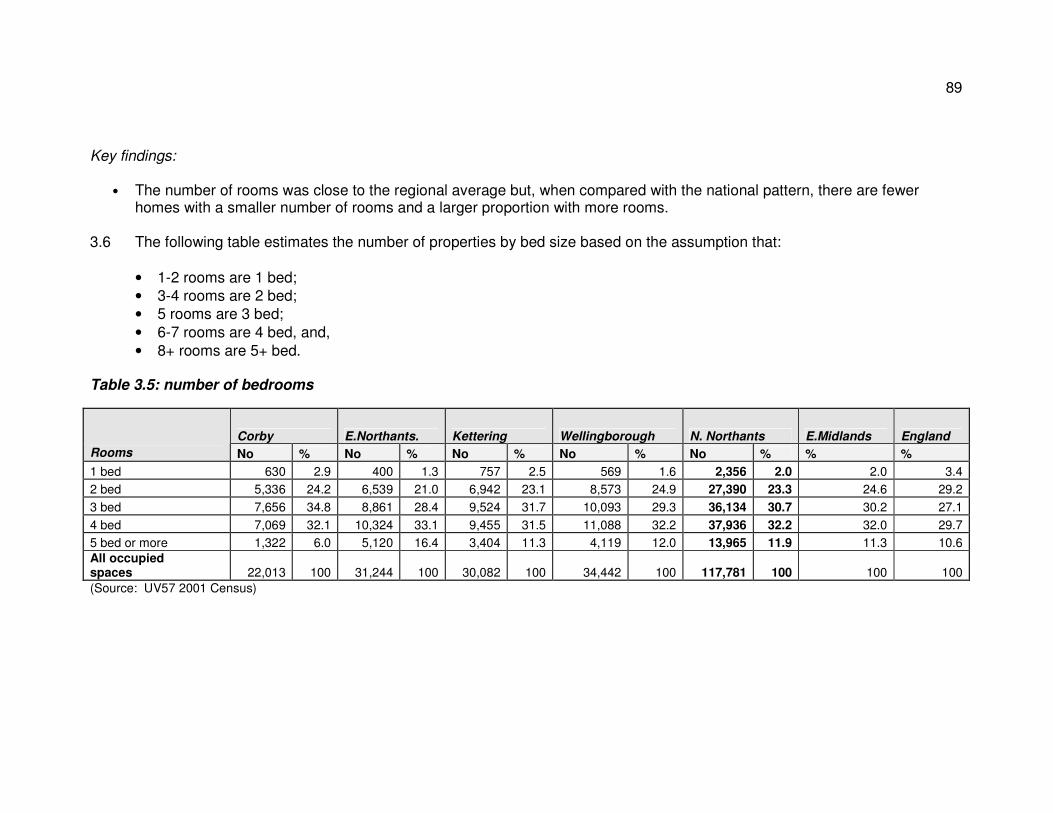

3.6 The following table estimates the number of properties by bed size based on the assumption that:

• 1-2 rooms are 1 bed;

• 3-4 rooms are 2 bed;

• 5 rooms are 3 bed;

• 6-7 rooms are 4 bed, and,

• 8+ rooms are 5+ bed.

Table 3.5: number of bedrooms

Corby E.Northants. Kettering Wellingborough N. Northants E.Midlands England

Rooms No % No % No % No % No % % %

1 bed 630 2.9 400 1.3 757 2.5 569 1.6 2,356 2.0 2.0 3.4

2 bed 5,336 24.2 6,539 21.0 6,942 23.1 8,573 24.9 27,390 23.3 24.6 29.2

3 bed 7,656 34.8 8,861 28.4 9,524 31.7 10,093 29.3 36,134 30.7 30.2 27.1

4 bed 7,069 32.1 10,324 33.1 9,455 31.5 11,088 32.2 37,936 32.2 32.0 29.7

5 bed or more 1,322 6.0 5,120 16.4 3,404 11.3 4,119 12.0 13,965 11.9 11.3 10.6

All occupied spaces 22,013 100 31,244 100 30,082 100 34,442 100 117,781 100 100 100

(Source: UV57 2001 Census)

90

Key findings:

• Whilst there will be wide variations at ward level, this table confirms that, when compared with the national pattern, there are fewer smaller and more larger homes across the area.

• The main differences by district from regional or national averages are:

o In Corby, the larger proportion of 3 bed and smaller proportion of 5 bed homes or larger; and o In East Northants, the smaller proportion of 1 bed and larger proportion of 5 bed properties;

Dwellings by Council Tax band 3.7 The following table summarises dwellings by Council Tax band in 2011. It must be remembered that as the property values

on which these bandings have been based have not been updated since 1st April 1991 and may no longer be a valid indication of relative market values.

Table 3.6: dwellings by Council Tax band, 2011

Corby East Northants. Kettering Wellingborough North

Northants East Mids

England & Wales

Band No % No % No % No % No % % %

A 13,650 52.2 9,136 24.6 12,940 31.2 10,384 31.3 46,110 33.4 37.7 24.3

B 5,625 21.5 10,131 27.2 11,487 27.7 9,473 28.5 36,716 26.6 22.5 19.7

C 3,026 11.6 5,922 15.9 7,781 18.8 6,509 19.6 23,238 16.8 18.0 21.8

D 2,367 9.1 4,783 12.9 4,609 11.1 3,559 10.7 15,318 11.1 10.7 15.4

E 1,052 4.0 3,536 9.5 2,751 6.6 2,079 6.3 9,418 6.8 6.3 9.7

F 251 1.0 2,226 6.0 1,244 3.0 761 2.3 4,482 3.2 3.0 5.2

G 142 0.5 1,328 3.6 635 1.5 416 1.3 2,521 1.8 1.7 3.5

91

H 18 0.1 133 0.4 51 0.1 38 0.1 240 0.2 0.2 0.6

I 0 0.0 0 0.0 0 0.0 0 0.0 0 0.0 0.0 0.0

Total 26,131 100.0 37,195 100.0 41,498 100.0 33,219 100.0 138,043 100.0 100.0 100.0

(Source: Dwellings by Council Tax Band, Neighbourhood Statistics website) Key findings:

• This confirms that, when compared with the national pattern, there are more lower value and less higher value homes.

92

Underoccupation and overcrowding 3.8 The Occupancy Rating provides a measure of both under-occupancy

and overcrowding and is based on the concept of the Room Requirement which is calculated as follows:

• a one-person household is assumed to require three rooms (two common rooms and a bedroom); and

• where there are two or more residents, it is assumed that they require a minimum of two common rooms plus one bedroom for:

• each couple (as determined by the relationship question)

• each lone parent

• any other person aged 16 or over

• each pair aged 10 to 15 of the same sex

• each pair formed from a remaining person aged 10 to 15 with a child aged under 10 of the same sex

• each pair of children aged under 10 remaining

• each remaining person (either aged 10 to 15 or under 10). 3.9 The Occupancy Rating relates the actual number of rooms in a

property to the number of rooms ‘required’ by the members of that household (based on an assessment of the relationship between household members, their ages and gender) and provides the following outcomes which are used here as proxy indicators of under-occupation and overcrowding:

• An occupancy rating of +2 or more suggests there are 2 or more rooms more than are 'required' according to the definition, i.e. there is under-occupation; and

• An occupancy rating of -1 suggests there is one less room than is 'required' according to the definition, i.e. there is overcrowding.

3.10 The following table summarises the level of under-occupation and

overcrowding for all households and, in view of its greater incidence among older people, highlights households including one or more pensioners.

Table 3.7: under-occupation and overcrowding, 2001

Indicator Corby East Northants Kettering W/borough

North Northants.

Occupancy rating +2 all households: no. 10,673 19,143 19,403 16,340 65,559 Occupancy rating +2 all households: % 48.48 61.28 56.33 54.32 55.10 Occupancy rating +2 pensioner 3,656 5,615 5,955 5,166 20,392

93

households: no. Occupancy rating +2 pensioner households: % 56.77 61.98 58.11 57.16 58.51 Occupancy rating -1 all households: no. 1,377 862 1,295 1,547 5,081 Occupancy rating -1 all households: % 6.26 2.76 3.76 5.14 4.48 (Source: Table UV59, 2001 Census)

Key findings

• An average of 55% of all households are underoccupying and 59% of pensioner households. The highest rates are in East Northants. and the lowest in Corby.

• An average of almost 5% of all households are overcrowded, the highest rate is in Corby.

Trends in residential completions 3.8 This section reviews trends in residential completions in general, by

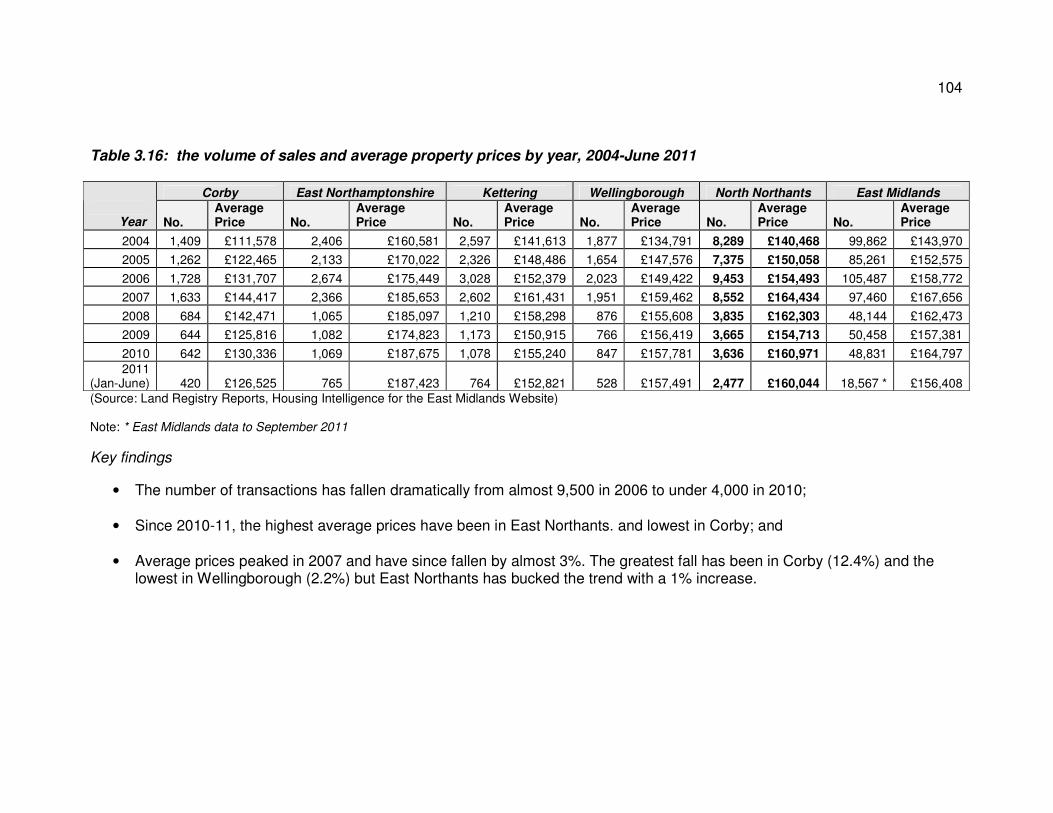

sector and bedsize. The following table summarises trends between 2006 and 2011.

Table 3.7: all residential completions, 2006-2011 Area 2006/07 2007/08 2008/09 2009/10 2010/11 Total % Corby 573 457 476 372 585 2,463 30.5 East Northants 504 536 170 211 217 1,638 20.3

Kettering 572 685 422 395 473 2,547 31.6 Wellingborough 392 474 295 151 110 1,422 17.6 North Northants 2,041 2,152 1,363 1,129 1,385 8,070 100% (Source: North Northants JPU and local authority data)

Key findings:

• Over 8,000 properties have been completed since 2006-07, almost one third each in Corby and Kettering with the lowest proportion in Wellingborough.

Completions by bedsize 3.9 The following table summarises trends in all housing completions by

bedsize between 2006 and 2011 for East Northants and Wellingborough.

94

Table 3.8: all residential completions by bedsize, 2006-2011

Year Corby East Northants Kettering Wellingborough Total no.

Total %

1 bed

2006/07 - 20 - 22 42

2007/08 - 55 - 46 101

2008/09 - 58 - 13 71

2009/10 - NK - 40 40

2010/11 - 7 - 15 22

Totals 140 - 136 276 12.48

2 bed

2006/07 - 108 - 74 182

2007/08 - 217 - 99 316

2008/09 - 48 - 14 62

2009/10 - NK - 64 64

2010/11 - 19 - 81 100

Totals 392 - 332 724 32.75 3 bed

2006/07 - 167 - 17 184

2007/08 - 220 - 14 234

2008/09 - 46 - 8 54

2009/10 - NK - 22 22

2010/11 - 65 - 19 84

Totals 498 - 80 578 26.14

4 bed

2006/07 - 177 - 2 179

2007/08 - 198 - 4 202

2008/09 - 60 - 0 60

2009/10 - NK - 0 0

2010/11 - 42 - 0 42

Totals 477 - 6 483 21.85

5 bed

2006/07 - 0 - 0 0

2007/08 - 0 - 0 0

2008/09 - 0 - 0 0

2009/10 - NK - 0 0

2010/11 - 0 - 1 1

Totals 0 - 1 1 0.05

All housing

2006/07 - 472 - 115 587

2007/08 - 690 - 163 853

2008/09 - 212 - 35 247

2009/10 - 149 - 126 275

2010/11 - 133 - 116 249

Sub-totals - 1.656 - 555 2,211

Overall total 2,463 1.656 2,547 555 7,221

Overall % 34.11 22.93 35.27 7.69 100% 100% (Source: North Northants JPU and local authority data)

95

Key findings:

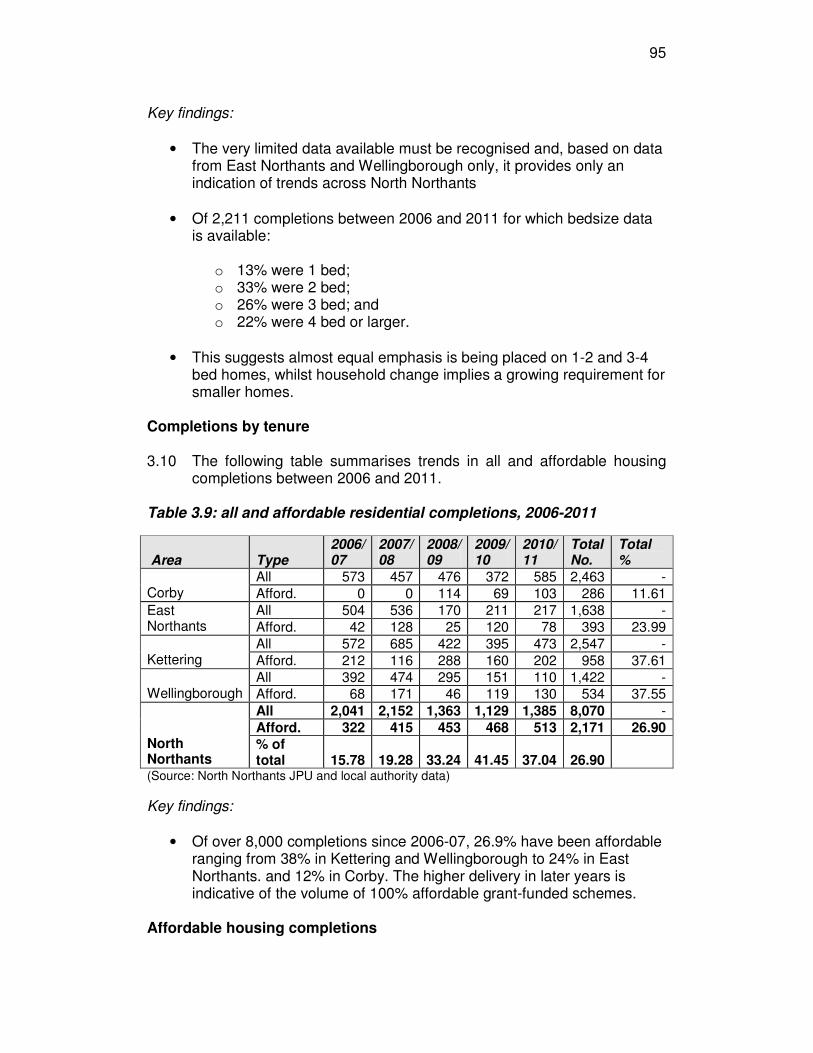

• The very limited data available must be recognised and, based on data from East Northants and Wellingborough only, it provides only an indication of trends across North Northants

• Of 2,211 completions between 2006 and 2011 for which bedsize data is available:

o 13% were 1 bed; o 33% were 2 bed; o 26% were 3 bed; and o 22% were 4 bed or larger.

• This suggests almost equal emphasis is being placed on 1-2 and 3-4 bed homes, whilst household change implies a growing requirement for smaller homes.

Completions by tenure 3.10 The following table summarises trends in all and affordable housing

completions between 2006 and 2011. Table 3.9: all and affordable residential completions, 2006-2011

Area Type 2006/ 07

2007/ 08

2008/ 09

2009/ 10

2010/ 11

Total No.

Total %

All 573 457 476 372 585 2,463 - Corby Afford. 0 0 114 69 103 286 11.61

All 504 536 170 211 217 1,638 - East Northants Afford. 42 128 25 120 78 393 23.99

All 572 685 422 395 473 2,547 - Kettering Afford. 212 116 288 160 202 958 37.61

All 392 474 295 151 110 1,422 - Wellingborough Afford. 68 171 46 119 130 534 37.55

All 2,041 2,152 1,363 1,129 1,385 8,070 -

Afford. 322 415 453 468 513 2,171 26.90 North Northants

% of total 15.78 19.28 33.24 41.45 37.04 26.90

(Source: North Northants JPU and local authority data)

Key findings:

• Of over 8,000 completions since 2006-07, 26.9% have been affordable ranging from 38% in Kettering and Wellingborough to 24% in East Northants. and 12% in Corby. The higher delivery in later years is indicative of the volume of 100% affordable grant-funded schemes.

Affordable housing completions

96

3.11 The following table summarises trends in affordable housing completions between 2006 and 2012.

Table 3.10: affordable residential completions, 2006-2011

Year Tenure Corby East Northants Kettering Wellingborough

North Northants

2006/07 Social 0 10 91 23 124

2007/08 Social 0 66 66 113 245

2008/09 Social 42 5 145 39 231

2009/10 Social 51 109 96 66 322

2010/11 Social 95 56 156 85 392

Totals Social 188 246 554 326 1,314

2006/07 Intermediate 0 32 121 32 185

2007/08 Intermediate 0 62 50 58 170

2008/09 Intermediate 72 4 98 33 207

2009/10 Intermediate 18 11 64 53 146

2010/11 Intermediate 8 22 46 45 121

Totals Intermediate 98 131 379 221 829

2006/07 All affordable 0 42 212 68 322

2007/08 All affordable 0 128 116 171 415

2008/09 All affordable 114 9 243 72 438

2009/10 All affordable 69 120 160 119 468

2010/11 All affordable 103 78 220 130 531

Totals All affordable 286 377 951 560 2,174

2011/12 All affordable 138 51 87 58 334 (Source: North Northants JPU and local authority data)

Kettering data includes Intermediate and ‘other’.

Key findings:

• 60% of affordable completions were social rented and one third intermediate housing including intermediate rent and shared ownership.

3.3 The private rented sector 3.12 The following section uses current data to profile the private rented

sector and uses a range of data sources:

• The property websites ‘rightmove’ and ‘findaproperty’;

• The Valuation Office Agency database; and

• Interviews with lettings agents.

97

3.13 The following table profiles the average number of private rented properties available for letting by type for February - May 2012, details of property type was not available for all properties advertised.

Table 3.11: the supply of private rented sector properties by type, February - May 2012 Type of accommodation Corby

East Northants Kettering Wellingborough

Total. No.

Total %

Flats/apartments 37 57 106 65 265 31.7 Terraced 59 29 85 45 218 26.1 Detached 31 56 54 25 166 19.9

Semi-detached 36 30 54 44 164 19.6 Bungalows 2 4 10 7 23 2.8

Sub-total 165 176 309 186 836 100% Sub-total % 19.7 21.1 37.0 22.3 Total advertised 178 178 321 183 860

(Source: rightmove.co.uk)

Key findings

• An average of 860 properties were advertised in February - May 2012, more than a third of the total in Kettering and almost exactly the same proportions in the 3 other local authority areas;

• The main property types advertised were flats and terraced houses though one fifth were detached houses.

3.14 The following table profiles the average monthly rentals of properties

available by type for February – May 2012. Table 3.12: private rented sector, average monthly rentals by property type and bedsize, February - May 2012, rounded to £5 Type of accommodation Corby

East Northants Kettering Wellingborough

North Northants.

Studio flats - - - £330 -