motor vehicle & trailer excise manual - amazon s3

TRANSCRIPT

Motor Vehicle &Trailer ExciseManualPrepared by the Property Tax Bureau, September 1995

Massachusetts Department of Revenue Division of Local ServicesMitchell Adams, Commissioner Robert H. Marsh, Deputy Commissioner

This first comprehensive Motor Vehicle & Trailer Excise

Manual is due to the efforts of Bruce Stanford, Tax

Counsel in the Division of Local Services’ Property Tax

Bureau. We believe this manual will be of inestimable

value to assessors, collectors and taxpayers. Special

thanks go to David Lewis and Kerry Conard of the

Registry of Motor Vehicles for their invaluable

assistance.

Robert H. Marsh

Deputy Commissioner

Motor Vehicle & TrailerExcise ManualTABLE OF CONTENTS

1 THE ASSESSMENT PROCESS

Motor Vehicles Subject to Excise . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Definition of “Motor Vehicle”. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Basis of the Excise Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Period of Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Calendar Year Basis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Registration Requirements of:

Non-Residents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Owers Who Acquire Residence or Place of Business . . . . . . . . . . . . . . . . . . . . . . 2

Calculation of the Excise Amount . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Role of the Registry of Motor Vehicles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Electronic Valuation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Non-Electronic Valuation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Preparation of Bills or Billing Information . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Obtaining Authorization to Print Bills. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Distribution of Bills or Billing Information . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Role of the Division of Local Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Place of Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Assessment by the Commissioner of Revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Proration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Vehicles Registered after January 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Registration Canceled before December 1. . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Minimum Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Payment Due Date . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Bill Mailed After Date of Issue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Date of Mailing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Person to Whom Excise Should Be Assessed . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Assessment in Case of Death of Registrant . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Address to Which Bill Should Be Mailed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Failure to Receive Bill . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Bill Mailed to Wrong Address . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Registrant Moves to New Address . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Methods to Effectuate a Change of Address . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Form #10094 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Change of Address Labels; Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Liability if Notice Not Given to Registry . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Relief if Address Given but Not Effectuated . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Place Where Payment Is Due . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Bill Mailed to Wrong Person . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Recommitment of Bills . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Assessors Discretion to Recommit Assessments . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Machinery Attached to a Motor Vehicle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Common Carriers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2 EXEMPTIONS

Vehicles Owned by:

Government . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Church . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Charity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Vehicles Leased by Charity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Former Prisoner of War . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Spouse of Former Prisoner of War . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Handicapped Persons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Veterans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Non-Veterans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Vehicles Operated with Section 5 Plates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 3

Penalty for Improper Use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 3

Assessment on Vehicle, Not Plate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 3

Vehicles Jointly Registered in Two States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 4

Vehicles Owned by:

Non-Domiciliary Servicemen . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 4

Foreign Dignitaries. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 4

Liability of Motor Vehicles for Personal Property Tax . . . . . . . . . . . . . . . . . . . . . . 1 5

Farm Plates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 5

Limitation of Use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 5

Use on Farm Tractors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 5

Use on Farm Trailers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 6

Operation of Unregistered Vehicles for Farm Purposes. . . . . . . . . . . . . . . . . . . . . . 1 6

3 ABATEMENTS

Application for Abatement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Proration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Cancellation of Registration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Minimum Abatement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Chapter 58 §8 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Circumstances Authorizing Assessors to Abate

Overvaluation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Transfer of Title and Cancellation of Registration . . . . . . . . . . . . . . . . . . . . . . . 18

Move Out of State and Register There . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Subsequent Registration Same Year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Transfer of Registration. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Theft of Motor Vehicle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Processing an Abatement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Abatement of Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Appeal of Assessors’ Decision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Refund of Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Notifying Registry of Valuation Corrections . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

4 COLLECTION PROCEDURES

Collection Remedies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Demand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Deputy Collectors and Other Collection Officers . . . . . . . . . . . . . . . . . . . . . . . . . 23

Issuance of Warrant . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Notice of Warrant . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Exhibition of Warrant . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Partial Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Non-Renewal Procedure. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Use of a Deputy Collector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Use of a Collection Agency. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Time Limitation of Placement of Marks . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Information Required to Place Marks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Clearing Marks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

License . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Registration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Persons Who May Place Marks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

In-Office Alternatives to Deputies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Collectors Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

On-Line Access to Non Renewal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Refunds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Interest on Abatements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Abatement of Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Uncollectible Excises. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

5 MISCELLANEOUS

Antique Automobiles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Abatement Application is a Public Record . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Special Plates. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Statute of Limitations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Mobile Homes/Manufactured Housing. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Located in Manufactured Housing Community . . . . . . . . . . . . . . . . . . . . . . . . 30

Not Located in Manufactured Housing Community . . . . . . . . . . . . . . . . . . . . . 30

Bankruptcy. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Automatic Stay . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Debts Not Discharged . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Proof of Claim . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Non-Renewal Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Minimum Refund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Death of a Spouse . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

INDEX . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

MOTOR VEHICLES SUBJECT TO

EXCISE

Pursuant to Ch. 60A of the MassachusettsGeneral Laws, every motor vehicle andtrailer1 registered in the Commonwealth issubject to the motor vehicle excise unless ex-pressly exempted. See Chapter 2 for a listingand discussion of each exemption.

DEFINITION OF “MOTOR VEHICLE”The term “motor vehicles” is defined in Ch.90 §1. The statute broadly defines motor vehi-cles as “all vehicles constructed and designedfor propulsion by power other than muscularpower including such vehicles when pulledor towed by another motor vehicle.” Thestatute, however, proceeds to limit this defini-tion by excluding the following:

• trains and trolleys, including tracklesstrolleys.

• vehicles used for other purposes thantransportation of property and incapableof being driven at a speed exceedingtwelve miles per hour and

1. used exclusively for the building, re-pair and maintenance of highways or

2. designed especially for use elsewherethan on the traveled part of ways.

• wheelchairs owned and operated by in-valids and operated or guided by a per-son on foot.

• motorized bicycles.

BASIS OF THE EXCISE ASSESSMENT

The motor vehicle excise is imposed for theprivilege of registering a motor vehicle. Reg-

istering a motor vehicle automatically triggersthe assessment of the excise.

PERIOD OF ASSESSMENT

Motor vehicle registrations are issued for ei-ther one or two years. The following regis-trations are issued for one year:

1. Vanity plates.

2. Section 5 plates. (Section 5 plates are thoseregistration plates authorized by Ch. 90 §5and which may be issued to automobilemanufacturers, dealers, repairmen, farmers,owner-contractors, transporters and har-vesters of forest products. See definitionsCh. 90 §1.)

3. Commercial registrations for vehicles of6,000 pounds or more.

All other plates and registrations are issuedfor two years.

CALENDAR YEAR BASIS

Section 5 plates and registrations for com-mercial vehicles of 6,000 pounds or more areissued on a calendar year basis. Black’s LawDictionary, Fourth Edition, defines calendaryear, “The period from January 1 to Decem-ber 31, inclusive.”

All other registration periods are staggered.For example, the registration of a passengervehicle registered on March 3rd of someparticular year will expire on March 2nd ofthe second following year. A vanity platefirst effective on November 15th of someyear will expire on November 14th of thefollowing year.

1The rules relating to trailers are identical to those relating to motor vehicles. Therefore, where this manual refers to motor vehicles,the reference, where appropriate, is also to trailers, as well.

The Assessment Process 1

Massachusetts Department of Revenue Division of Local ServicesMitchell Adams, Commissioner Robert H. Marsh, Deputy Commissioner

REGISTRATION REQUIREMENTS

OF (1) NON-RESIDENTS AND (2) OWNERS

WHO ACQUIRE A REGULAR PLACE OF

BUSINESS OR ABODE IN THE COMMONWEALTH

A non-resident of Massachusetts may, for alimited period of time, operate within theCommonwealth a motor vehicle registeredin some other state or country, so long as hehas complied with the laws relating to oper-ation and registration in the other state orcountry. G.L. Ch. 90 §3 limits the durationof such operation to not more than thirtydays in the aggregate in any one year.

Whenever a non-resident owner of a motorvehicle acquires a regular place of abode orbusiness or employment in Massachusetts,that person must either:

• register that vehicle in Massachusettswithin thirty days or

• maintain in full force a policy of liabilityinsurance at least in the amount or limitsset out in Ch. 90 §34A.

CALCULATION OF THE EXCISE

AMOUNT

The amount of the motor vehicle excise dueon any particular vehicle or trailer in anyregistration year is calculated by multiply-ing the value of the vehicle by the motor ve-hicle excise rate. That rate is fixed at $25.00per thousand dollars of value. The value ofa vehicle for the purpose of the excise is theapplicable percentage for that year of themanufacturer’s suggested retail price forthat vehicle. The applicable percentages areset out in Ch. 60A §1 as follows:

The manufacturer’s list price for any particu-lar vehicle is the price recommended by themanufacturer as the selling price of that vehi-cle when new. It is the manufacturer’s listprice rather than the actual purchase pricewhich will control for purposes of calculatingthe motor vehicle excise. The following mod-els illustrate calculations of amounts due forrepresentative automobiles.

Model 1

2 The Assessment Process

In the year preceding the year of manufacture. . . . .50%In the year of manufacture . . . . . . . . . . . . . . . . . 90%In the second year . . . . . . . . . . . . . . . . . . . . . . . 60% In the third year. . . . . . . . . . . . . . . . . . . . . . . . . . 40% In the fourth year. . . . . . . . . . . . . . . . . . . . . . . . . 25%In the fifth and succeeding years. . . . . . . . . . . . 10%

Model 1 assumes a motor vehicle (a) purchased in the year preceding the year of manufacture [e.g., a 1990model year vehicle purchased in calendar 1989] (b) with a manufacturer’s list price of $15,000.

Manufacturer’s Ch. 60A Value for Rate Excise AmountList Price Percentage Excise Purposes

Year of Purchase: $15,000 x 50% = $7,500 x .025 = $187.50Second Year: $15,000 x 90% = $13,500 x .025 = $337.50Third Year: $15,000 x 60% = $9,000 x .025 = $225.00Fourth Year: $15,000 x 40% = $6,000 x .025 = $150.00Fifth Year: $15,000 x 25% = $3,750 x .025 = $93.75Sixth: $15,000 x 10% = $1,500 x .025 = $37.50(and all ensuing years)

ROLE OF THE REGISTRY OF

MOTOR VEHICLES IN

ADMINISTRATION OF THE

MOTOR VEHICLE EXCISE

I. ELECTRONIC VALUATION

The Registry of Motor Vehicles annually cal-culates the value of all registered motor ve-hicles for the purpose of excise assessment.For most motor vehicles, the calculations areperformed electronically using valuationtapes. For automobiles and light trucks, thevaluation tape is created by the NationalAutomobile Dealers Used Car Guide Co.(N.A.D.A.); for heavy trucks and school buses,the tape is created by Maclean Hunter Mar-ket Reports, Inc., publisher of The Truck BlueBook; and for motorcycles, the tape is createdby Hap Jones, publisher of the MotorcycleBlue Book. In each case, it is the vehicle’sidentification number (VIN) which drivesthe electronic valuation process.

II. NON-ELECTRONIC VALUATION: TRAILERS,FIXED EQUIPMENT

While most vehicles are valued electroni-cally, valuation programs are not availablefor all motor vehicles or motor vehicle com-ponents. For example, various equipmentcommonly mounted on the cab chassis, suchas cement mixers or pumpers, garbage com-pactors, home delivery oil trucks, welldrillers, etc., cannot be valued electronically.Also, tapes do not exist which value the

myriad varieties of trailers on the market.For these kinds of items, as well as for thosemotor vehicles which cannot be valuedusing the available tapes, the Registry ofMotor Vehicles annually ascertains valua-tions (default valuations) and mails notice ofthese valuations to all board of assessors inthe fall of every year.

Assessors possess authority to abate a Reg-istry default value in any case in which theybelieve it is excessive. Assessors may alsoobtain the manufacturer’s list price of anyparticular motor vehicle by either (a) callingan automobile dealer who regularly sellsthat brand of vehicle, (b) requesting the ve-hicle’s registrant to provide the windowpricing sticker of the car when new or (c)calling the manufacturer’s customer servicenumber.

III. PREPARATION OF BILLS OR BILLING

INFORMATION

In addition to calculating the value of allmotor vehicles registered in the Common-wealth, the Registry, at each municipality’soption, either (a) prepares actual excise billsfor the city or town or (b) enters billing in-formation on a computer tape for the use ofthe city or town to produce its own bills.Any community which chooses to receiveactual bills is assessed a Cherry Sheet chargeof 15¢ per bill for this service.

Model 2

Motor Vehicle & Trailer Excise Manual 3

Model 2 assumes a motor vehicle (a) purchased two years succeeding the year of manufacture (b) with amanufacturer’s list price of $19,000.

Manufacturer’s Ch. 60A Value for Rate Excise AmountList Price Percentage Excise Purposes

Year of Purchase: $19,000 x 40% = $7,600 x .025 = $190.00Second Year: $19,000 x 25% = $4,750 x .025 = $118.75Third Year: $19,000 x 10% = $1,900 x .025 = $47.5(and all ensuing years)

IV. OBTAINING AUTHORIZATION TO PRINT BILLS

Any city or town which wishes to print itsown bills must submit to the Registry a No-tice of Intent to Print Motor Vehicle ExciseBills. The format for making this request isset out annually in the IGR on the require-ments for motor vehicle excise bills for thatyear. No assessment is made to those com-munities that receive billing information ona computer tape.

V. DISTRIBUTION OF BILLS OR BILLING

INFORMATION

Because of the volume and variety of typesof vehicles, the Registry is unable to providebills or billing information for all vehicles atthe same time. Rather, bills and billing tapesare prepared and distributed in batches sub-sequent to January first. The first batch, usu-ally mailed out in early January of each year,is comprised of passenger motor vehicleswhich were registered as of the precedingJanuary first. Vehicles registered after Janu-ary first are contained in a later batch orbatches. Another batch is comprised oftrucks; still another, of motorcycles.

ROLE OF THE DIVISION OF LOCAL

SERVICES IN THE ADMINISTRATION

OF THE MOTOR VEHICLE EXCISE

The Division of Local Services is available toassist local officials in the administration ofthe motor vehicle excise by responding toquestions which relate to legal or technicalaspects of the excise. In addition, the Com-missioner of Revenue will authorize asses-sors to abate excises, under G.L. Ch. 58 §8,in appropriate cases, when the assessors donot possess jurisdiction to make an abate-ment on their own. See Chapter 3 for a fur-ther discussion of Ch. 58 §8 abatements.

The Division, however, possesses neither thestaff nor the other necessary resources to as-sist municipalities in valuing motor vehicles.

All assessors should ensure, therefore, thatthey have available in their offices up-to-date copies of the N.A.D.A. Official UsedCar Guide, the Truck Blue Book, the Motor-cycle Blue Book and the Registry’s annualletter setting out valuations of motor vehi-cles and components which it is unable tovalue electronically. With these resources,assessors will be able to process abatementapplications based upon claims of overvalu-ation. The Massachusetts Association of As-sessing Officers (M.A.A.O.) annuallyorganizes bulk purchasing of these valua-tion materials to assist cities and towns toreduce costs. Therefore, municipalitiesshould coordinate their purchases throughthe Association.

PLACE OF ASSESSMENT

The excise on any particular vehicle is to beassessed at the place where that vehicle isprincipally kept, i.e., garaged. The relevantstatute, Ch. 60A §6, provides:

“The excise…shall be laid and collectedat the residential address of the owner, ifan individual, or at the principal place ofbusiness in the commonwealth, if a part-nership, voluntary association or corpo-ration, as determined by the owner’sregistration, except that if a motor vehi-cle…is customarily kept in some othermunicipality, the excise shall be laid andcollected in such other municipality.”

This statute was drafted with a presumptionthat any particular motor vehicle is kept forexcise purposes at the residence or principalbusiness address of its owner. On the basisof this presumption, the statute sets out twoalternatives. It instructs that the excise forthe vehicle is to be imposed and collected bythe city or town where its owner (a) if an in-dividual, lives, or (b) if a partnership, volun-tary association or corporation, maintains itsprincipal place of business UNLESS themotor vehicle is customarily kept in someother city or town.

4 The Assessment Process

It is only when the Registry is specificallynotified that a vehicle is principally kept insome other municipality that the Registrywill include the excise for that vehicle in thecommitment for the other municipality. Oth-erwise, the excise will be included in thecommitment of the municipality where theindividual lives or the principal place ofbusiness is located.

The place where a motor vehicle is princi-pally kept is not identified on the registra-tion certificate for that vehicle. However,that place is identified on the registrant’s in-surance coverage selection sheet. Therefore,where an issue arises concerning the placeof garaging, the assessors should request acopy of this insurance document.

ASSESSMENT BY COMMISSIONER

OF REVENUE

In the case of motor vehicles which are notcustomarily kept in any Massachusetts cityor town, i.e., vehicles registered in Mass-achusetts but customarily kept out of state,the excise is levied and collected by the Ex-cise Bureau within the Department of Rev-enue. For answers to questions respectingsuch excises, call the Excise Bureau at (617)626-3060 or 3086.

PRORATION

I. VEHICLES REGISTERED AFTER JANUARY 1

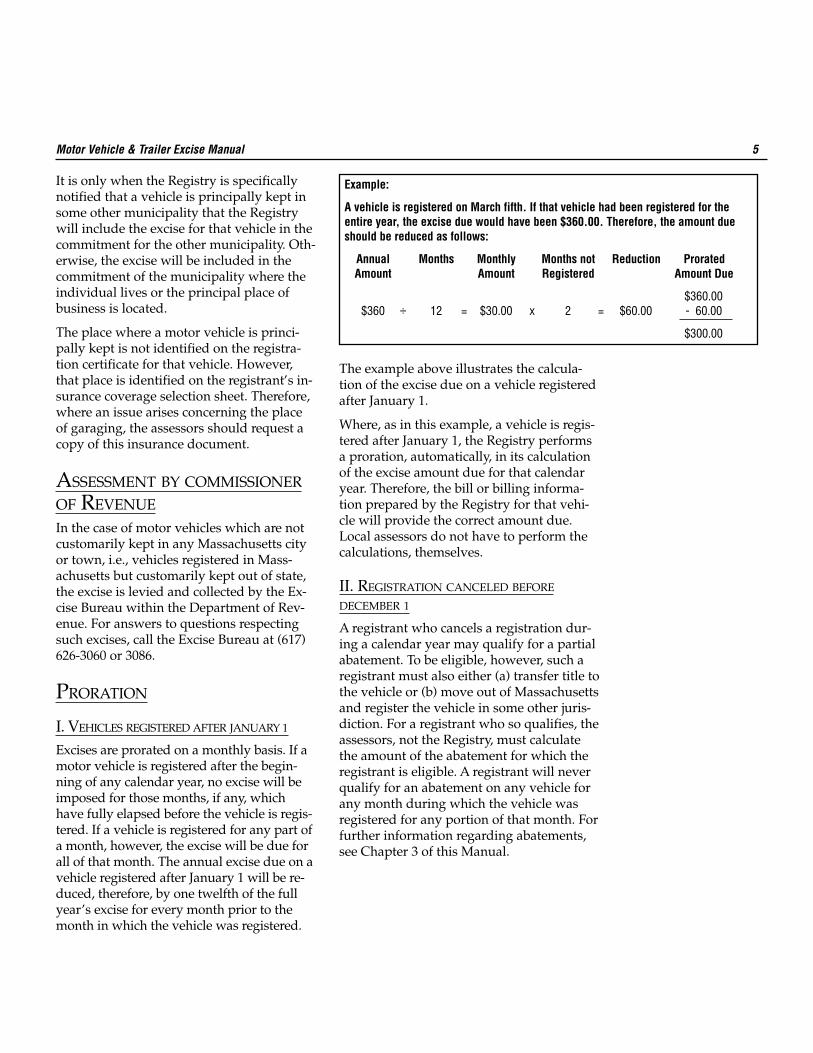

Excises are prorated on a monthly basis. If amotor vehicle is registered after the begin-ning of any calendar year, no excise will beimposed for those months, if any, whichhave fully elapsed before the vehicle is regis-tered. If a vehicle is registered for any part ofa month, however, the excise will be due forall of that month. The annual excise due on avehicle registered after January 1 will be re-duced, therefore, by one twelfth of the fullyear’s excise for every month prior to themonth in which the vehicle was registered.

The example above illustrates the calcula-tion of the excise due on a vehicle registeredafter January 1.

Where, as in this example, a vehicle is regis-tered after January 1, the Registry performsa proration, automatically, in its calculationof the excise amount due for that calendaryear. Therefore, the bill or billing informa-tion prepared by the Registry for that vehi-cle will provide the correct amount due.Local assessors do not have to perform thecalculations, themselves.

II. REGISTRATION CANCELED BEFORE

DECEMBER 1

A registrant who cancels a registration dur-ing a calendar year may qualify for a partialabatement. To be eligible, however, such aregistrant must also either (a) transfer title tothe vehicle or (b) move out of Massachusettsand register the vehicle in some other juris-diction. For a registrant who so qualifies, theassessors, not the Registry, must calculatethe amount of the abatement for which theregistrant is eligible. A registrant will neverqualify for an abatement on any vehicle forany month during which the vehicle wasregistered for any portion of that month. Forfurther information regarding abatements,see Chapter 3 of this Manual.

Motor Vehicle & Trailer Excise Manual 5

Example:

A vehicle is registered on March fifth. If that vehicle had been registered for theentire year, the excise due would have been $360.00. Therefore, the amount dueshould be reduced as follows:

Annual Months Monthly Months not Reduction ProratedAmount Amount Registered Amount Due

$360.00$360 ÷ 12 = $30.00 x 2 = $60.00 - 60.00

$300.00

MINIMUM ASSESSMENT

The minimum motor vehicle assessmentwhich may be made is five dollars. There-fore, if the value of a vehicle produces an ex-cise amount less than five dollars, anassessment of five dollars must be made.

PAYMENT DUE DATE

Excise bills must show the date upon whichthe bills were issued and must contain thestatement: “Due and Payable in Full Within30 Days of Issue.” (See annual IGR on theformat of motor vehicle excise bills.) A pay-ment, to be timely, must be received in thecollector’s office on or before the close ofbusiness on the thirtieth day following thedate shown on the bill as the date of issue.As is the case with property taxes, mailingthe payment on or before the due date doesnot satisfy the requisite for timely paymentif it is not received until after the due date.

EXCISE BILL MAILED AFTER THE

DATE OF ISSUE

If an excise bill is mailed after the printeddate of issuance, the bill is due and payableat the expiration of thirty days from the datethe bill was mailed by the tax collector.Again, to be timely paid, the payment mustbe received in the collector’s office on or be-fore the close of business on the thirtieth dayfollowing the date of mailing.

DATE OF MAILING

The date of mailing of a motor vehicle excisebill is not necessarily the postmarked date.Rather, it is the date certified by the collec-tor, on the affidavit of sending, executed inaccordance with G.L. Ch. 60 §3, as the datethe bill was mailed. The collector shouldcertify the mailing date on the affidavit to bethe date the bill was delivered into the cus-tody of the post office. It is irrelevant

whether a bill is postmarked on the date it isturned over to the post office. For the pur-pose of determining whether a bill is timelypaid, that bill is deemed to have beenmailed on the turnover date.

INTEREST

If a motor vehicle excise bill is not timelypaid, interest accrues on any unpaid amountat the rate of 12% per year, simple interest,not compounded, from the date the pay-ment was due until the date it is paid.

PERSON TO WHOM EXCISE BILL

SHOULD BE ASSESSED

Ch. 60A §2 directs that the motor vehicle ex-cise “shall be assessed to the owner of thevehicle or trailer registering the same.” Thisstatute deems a person who registers amotor vehicle to be that vehicle’s owner forexcise purposes. Moreover, pursuant to Ch.90 §2, the statute which sets out rules andprocedures relating to the registration ofmotor vehicles, motor vehicles may only beregistered to their owners.

This requirement is corroborated by Ch. 90D§4 which establishes that, except for certainvehicles expressly exempted under Ch. 90D§2, the Registrar shall accept no new appli-cation for registration pertaining to a motorvehicle or trailer under the provisions of Ch.90 until the owner thereof makes applicationto the registrar for a certificate of title.

The Supreme Judicial Court dealt with theissue of vehicle ownership in Casey v. Gal-lagher, 326 Mass. 746, 750 (1950) where itfound registration of a motor vehicle to con-note ownership. The Court declared,“[R]egistration in the name of a person asowner is evidence of ownership by him.”

The word “owner,” as used in Ch. 90 §2, isnot confined to a person having absolute in-terest in the vehicle; a motor vehicle may beregistered by a person having a part owner-ship in the vehicle. It may, also, be registeredby a corporation, association, partnership orother legal entity.

6 The Assessment Process

By the express provisions of Ch. 90 §2A,motor vehicles may be registered to minors.

In the case of a leased vehicle, the bill mustbe assessed to the lessor (leasing company)since the lessor, not the lessee, is the ownerof the vehicle.

In sum, assessors should assess the excisefor any particular motor vehicle to theowner of that vehicle who, of necessity, willbe the registrant.

ASSESSMENT IN THE CASE OF

THE DEATH OF THE REGISTRANT

I. REGISTRANT DIES AFTER ASSESSMENT

BUT PRIOR TO PAYMENT

If an excise is assessed to a registrant whodies prior to payment, the collector shouldseek payment from the decedent’s executoror administrator. Pursuant to Ch. 197 §9, thecollector must make the claim within oneyear after the date of the decedent’s death. Ifthe executor or administrator does not pay,the collector should commence an action tocollect in the appropriate probate court.

II. REGISTRANT DIES BEFORE ASSESSMENT

If an excise is assessed after a registrant dies,the assessment should be made to the dece-dent’s executor or administrator. If an ex-ecutor or administrator has not yet beenappointed, the assessment should be madeto the decedent’s estate. Upon subsequentappointment, the executor or administratorbecomes responsible to pay the assessmentas though it had been to him.

III. LIABILITY OF EXECUTOR OR ADMINISTRATOR

Pursuant to Ch. 60 §36, a decedent’s execu-tor or administrator, who receives or haspossession of money applicable to a motorvehicle excise assessed upon the deceased

person’s estate, must pay the excise forth-with. If the executor or administrator fails todo so, he will, if a demand has been made,become personally liable for that excise. Tocollect upon such a liability, the collectormust commence an action within six years.

ADDRESS TO WHICH BILL

SHOULD BE MAILED

For individuals, the excise for each particu-lar motor vehicle should be mailed to theowner’s residential address as that addressappears on the individual’s registration, un-less that owner has expressly specified inwriting a different mailing address.

For corporations, partnerships or voluntaryassociations, the excise should be mailed tothe owner’s principal place of business inthe Commonwealth, if any, as that addressappears on the owner’s registration. If theowner has no principal place of business inthe Commonwealth, the bill should bemailed to the owner’s principal place ofbusiness outside the Commonwealth.

FAILURE TO RECEIVE BILL

So long as a municipality mails an excise billto a registrant and the bill is sent to the reg-istrant’s address, as that address appears onthe vehicle’s registration or as the personhas otherwise specified in writing, the regis-trant is presumed to have received the bill,regardless whether he received it in fact. Ifthe registrant fails to receive such a bill, heis, nevertheless, liable for its timely pay-ment, and interest and fees will accrue if thebill is not paid on or before the due date.

BILL MAILED TO WRONG ADDRESS

If a motor vehicle excise bill is not sent tothe registrant’s address, as that address ap-pears on the vehicle’s registration or asexpressly designated by the registrant, col-lection cannot be enforced. In the case of abill sent to the right city or town but to the

Motor Vehicle & Trailer Excise Manual 7

wrong street address, the bill should be reis-sued by the collector to the correct street ad-dress without the addition of any interest orfees. In the case of a bill sent to the wrongcity or town, that bill should be abated inthe incorrect municipality and recommittedin the correct city or town. (See discussion ofassessors discretion to recommit excise as-sessment, below.) If the assessors lack juris-diction to so abate, they may seek jurisdictionunder Ch. 58 §8. (See Chapter 2; see alsoI.G.R. 94-202.)

REGISTRANT MOVES TO NEW

ADDRESS

If a registrant moves to some other addressthan that shown on his excise bill, that regis-trant should take steps to ensure that his ad-dress is changed on his license andregistration. G.L. Ch. 90 §26A states:

“Every person in whose name a motorvehicle…has been registered…shall re-port any change of his name, residentialaddress or mailing address in writing tothe registrar within thirty days after thedate on which such change was made.”

METHODS TO EFFECTUATE A

CHANGE OF ADDRESS

I. FORM #10094A convenient way for a person to make achange of address in the Registry’s databank is to fill out and submit an orange“Change of Address — License/ Registra-tion” card, Form #10094. A registrant mayalso change the address on his registrationby calling the Registry of Motor Vehicles at(617) 351-4500, although this procedure doesnot technically comply with the statute’s re-quirement that the change be made in writ-

ing. Assessors, too, can alter or update infor-mation in the Registry’s excise data bank bycalling (617) 351-9380; however, the Registrywould prefer the assessors to effect thesechanges in writing, using the standard formentitled Request for Records Change.

II. CHANGE OF ADDRESS LABELS; FEES:Upon a request made either in writing or byphone, the Registry will provide change ofaddress labels upon which licensee/regis-trants may enter address changes. Theselabels may then be affixed, as appropriate,to previously issued licenses and registra-tions. The Registry provides change of ad-dress labels at no charge. Alternatively, aregistrant/licensee who changes his addressmay obtain from the Registry an amendedlicense and/or registration(s) displaying thenew address. For each amended document,the Registry will assess a $15.00 fee pur-suant to the authority of Ch. 90 §33.

III. LIABILITY IF NOTICE OF CHANGE OF

ADDRESS IS NOT GIVEN TO THE REGISTRY:If a registrant moves and does not changehis address, the excise bill will be mailed tothe registrant’s former address, and the billmight not be forwarded by the post office tothe new address. So long as a municipalitymails the excise bill to the address that ap-pears on a person’s registration, the munici-pality fulfills its duty to give notice to theregistrant. The registrant becomes subject tointerest and fees if the excise is not timelypaid. If a bill does not reach a registrant be-cause that person moved and did not notifythe Registry of his change of address, theregistrant is not entitled to any relief.

8 The Assessment Process

IV. AVAILABLE RELIEF IF CHANGE OF

ADDRESS IS GIVEN BUT NOT EFFECTUATED

DUE TO REGISTRY ERROR

On the other hand, if a person moves andproperly notifies the Registry of the movebut, notwithstanding, does not receive anexcise bill, that person may be entitled to re-lief. Two particular circumstances should af-ford such relief:

1. A registrant properly files a change ofaddress; however, due to a clerical error,the change is either not entered, at all, oris incorrectly entered into the Registry’srecords.

2. A registrant’s license and registrationare not integrated in the Registry’srecords. The registrant properly files anaddress change which effects a change inhis license file. However, the address inhis registration file is not concurrentlyupdated, and the excise bill goes to theincorrect address. (This is an infrequentcircumstance since the vast majority ofthe Registry’s records are integrated.)

In both of the above circumstances, the as-sessors are not legally obligated to grant anabatement, if they possess jurisdiction, or toseek authority to grant an abatement underCh. 58 §8, if they lack such jurisdiction. Theypossess full discretion in these matters.However, the Department of Revenue be-lieves an abatement is fair and equitable insuch situations.

PAYMENT DUE TO MUNICIPALITY

WHERE VEHICLE WAS

ORIGINALLY REGISTERED

The excise for any particular year is due tothe municipality in which a vehicle was reg-istered on January first of that year. For a ve-hicle not registered on January first, theexcise is due to the municipality in whichthe vehicle was registered after January first.Therefore, in the case of any person who

moves during any particular registrationyear, the excise will be due to the city ortown where the vehicle was originally regis-tered for that calendar year.

BILL MAILED TO WRONG PERSON

Ch. 60A §2 expressly requires motor vehiclebills to be mailed to the vehicles’ owners.Therefore, collection cannot be enforced inthe case of a bill sent to the wrong person.Such a bill should be abated. If a municipal-ity sends a bill to the wrong person, itshould, when it discovers the error, reissuethe bill to the proper person. That bill wouldbe due thirty days from the date of mailing.

RECOMMITMENT OF MOTOR

VEHICLE EXCISE BILLS

A motor vehicle excise bill committed to theincorrect city or town is not enforceable andmust, upon a written request timely submit-ted by the registrant, be abated by the asses-sors of that city or town. Assessors grantingsuch an abatement should, forthwith, notifythe assessors in the municipality where thecommitment should have been made. Uponreceipt of such notification, these assessorsmust recommit that bill to their tax collectorfor mailing to the registrant, regardlesswhen the earlier commitment was made.

ASSESSORS DISCRETION TO

RECOMMIT EXCISE ASSESSMENT

Assessors must commit any and all exciseassessments which are due to their respec-tive municipalities. They lack the discretionto do otherwise. Ch. 60A §2 states that, ex-cept for vehicles which are expressly ex-empt, “[T]he board of assessors shall assessthe excise imposed by [Ch. 60A] section one,and commit the same to the collector oftaxes with their warrant for the collectionthereof.” (Emphasis supplied.) Assessorshave no authority to refuse to commit an ex-cise for some earlier calendar year because

Motor Vehicle & Trailer Excise Manual 9

the commitment for that year has been ex-tinguished or for any other reason.

ASSESSMENT OF MACHINERY

ATTACHED TO A MOTOR VEHICLE

Machinery which is permanently attachedto a motor vehicle or trailer and which can-not feasibly be removed and sold separatelyfor its intended purpose should be assessedas part of the value of the motor vehicle ortrailer under the motor vehicle excise. Whenso assessed, it is exempt from personal prop-erty tax in the same manner as the rest of themotor vehicle or trailer under Ch. 59 §5(35).

COMMON CARRIERS

Common carriers are subject to the motorvehicle excise. A common carrier is onewho, as a regular business, transports per-sons and/or goods from place to place forthose who employ him and who pay hischarges. Therefore, unless a carrier is ex-empt from the excise as a transportation au-thority or otherwise, city and town assessorsand collectors should assess and levy, in theusual way, an excise on all vehicles ownedby that common carrier which are customar-ily kept in their municipalities.

10 The Assessment Process

Ch. 60A §1 exempts the following vehiclesfrom the motor vehicle excise:

I. Vehicles owned and registered by theCommonwealth or any political subdivisionof the Commonwealth. Political subdivi-sions include cities, towns, counties, districtsand authorities.

II. Vehicles owned and registered by anycorporation whose personal property is ex-empt from taxation under Ch. 59 §5, ClausesThird and Tenth. Clause Third exempts thepersonal property owned by literary, benev-olent, charitable and scientific corporations.Clause Tenth exempts the personal propertyowned by religious organizations.

In making a determination about the excisestatus of vehicles owned by a charitable cor-poration, the assessors must ascertainwhether a charity satisfies the Clause Thirdrequisites. Clause Third exempts the:

“[p]ersonal property of a charitable orga-nization, which term, as used in thisclause, shall mean (1) a literary, benevo-lent, charitable or scientific institution ortemperance society, incorporated in thecommonwealth, and (2) a trust for liter-ary, benevolent, charitable, scientific ortemperance purposes if it is establishedby a declaration of trust executed in thecommonwealth or all its trustees are ap-pointed by a court or courts in the com-monwealth and if its principal literary,benevolent, charitable, scientific or tem-perance purposes are principally andusually carried out within the common-wealth.” (Emphasis added.)

The documents a charity should provide,therefore, are, for a corporation, a copy ofthe articles of incorporation, and for a trust,

a copy of its declaration of trust. These doc-uments, alone, should be sufficient to deter-mine whether a charity qualifies forexemption on automobiles it owns and reg-isters. (To determine a charity’s tax status re-garding real property, additional documentswould be necessary to establish how theproperty was occupied and used on thequalification date.)

III. Vehicles leased for a full calendar year toany charitable corporation except a charita-ble educational corporation which eithergrants degrees or awards diplomas. (Vehi-cles owned by such educational corpora-tions which satisfy the exemption requisitesfor a charitable corporation, cited above, areexempt from the excise.)

A. Only a vehicle leased for a full calen-dar year may qualify for an exemption.Therefore, a vehicle leased from Febru-ary first of one year through Januarythirty-first of the next year would notqualify for an exemption. A vehicleleased from February first of one yearthrough January thirty-first of the secondfollowing year could only qualify for thefull calendar year contained within thetwenty-four months of the lease.

B. The Legislature’s purpose in restrict-ing the excise exemption on vehiclesleased to charities to full calendar yearsis the fact that the excise, itself, is as-sessed on a calendar year basis. Withoutthis restriction, a leasing company couldobtain a calendar year exemption on thebasis of a lease which terminated atsome time during a calendar year.

C. Vehicles leased to private schoolswhich are organized as charities are notexempt from the motor vehicle excise.

Exemptions 2

D. To determine the eligibility of lessorsunder this provision, assessors shouldrequire:

1. A copy of the lease agreement orsome other documentation which dis-closes the dates the lease commencesand terminates.

2. The name, address and sales tax ex-emption number of the non-profitlessee.

IV. Vehicles owned and registered by formerprisoners of war or the surviving spouses offormer prisoners of war.

A. This exemption is available only atlocal option. It must be accepted by avote of the city council with the approvalof the mayor, in a city, and by vote of thetown meeting or town council, in a town.

B. To qualify as a former prisoner of war,a person must have been regularly ap-pointed, enrolled, enlisted or inductedinto the military forces of the UnitedStates and been captured, separated andincarcerated by an enemy of the UnitedStates during an armed conflict.

C. At the time of the initial filing of anapplication for this exemption, the appli-cant must supply sufficient evidence ofthe former prisoner of war’s earlier in-carceration, either through documenta-tion by the Veterans Administration orby providing a copy of the veteran’s dis-charge papers. In future years, only theapplication for exemption must be filed.

D. A surviving spouse of a deceased for-mer prisoner of war is entitled to this ex-emption until such time as thatsurviving spouse remarries.

E. Prisoner of war registration plates arenot necessary for entitlement to this ex-emption.

V. Vehicles owned and registered by handi-capped persons.

A. Handicapped veterans:

1. To qualify as a veteran, a personmust have been honorably dischargedfrom the armed services and haveserved in either World War I, World II,the Korean Emergency, the Viet-namese War, the Lebanese PeaceKeeping Force, the Panamanian Inter-vention Force or the Persian Gulf.

2. In addition, the person must, byreason of such service, have sufferedeither (a) an actual loss of or a perma-nent and complete loss of use of, oneor both feet or one or both hands or(b) a permanent vision impairment, ofthe magnitude set out in Ch. 60A §1,of one or both eyes. As used in thisstatute, loss of use is the constructiveequivalent of an actual loss. No mag-nitude of loss which is less than totalloss of use qualifies an individual forexemption.

3. This loss must be documented bythe records of the Veterans Adminis-tration.

4. This exemption is restricted for eachhandicapped veteran to one vehicle,owned and registered by the veteranfor personal, non-business use. A vet-eran who owns more than one vehiclehas the right to choose the vehicleupon which to obtain an exemption.

5. If any vehicle is jointly owned by ahandicapped veteran with some otherperson, the veteran qualifies only forthat percentage of the excise amountwhich corresponds to his or her per-centage ownership of the vehicle.

B. Handicapped non-veterans:

1. This exemption is available to a per-son who has suffered either (a) an ac-

12 Exemptions

tual loss of or a permanent and com-plete loss of use of both legs or botharms (b) a permanent vision impair-ment of both eyes of the magnitudeset out in Ch. 60A §1. As with the ex-emption for handicapped veterans,loss of use is the constructive equiva-lent of an actual loss.

2. A board of assessors may require anapplicant for this exemption to pro-vide a certification by a physician ofthe existence of the requisite loss.

3. This exemption is restricted for eachhandicapped person to one vehicle,owned and registered by that personfor personal, non-business use. A per-son who owns more than one vehiclehas the right to choose upon whichvehicle to obtain an exemption.

If a vehicle is jointly owned by ahandicapped person with some otherperson, the handicapped person qual-ifies only for that percentage of the ex-cise amount which corresponds to hisor her percentage ownership of thevehicle.

C. Handicap Plates:A person need not have a handicap plateto be eligible for this exemption. Alterna-tively, one who has a handicap plate isnot per se entitled to an exemption. Therequisite loss must still be demonstrated.

VI. Vehicles operated with Section 5 platesand owned or controlled by manufacturers,farmers or dealers. (See discussion of farmvehicles, below.)

Formerly, vehicles operated with repairplates also qualified for an exemption fromthe excise. However, this exemption was re-pealed, commencing with calendar year1991. Frequently, tow trucks are operatedwith repair plates. Such trucks are not ex-empt from the motor vehicle excise.

The exemption for vehicles operated withthese special plates is conditional, however.It should only be granted if:

A. the vehicles are operated exclusivelyfor business purposes. The statute for-bids the use of such vehicles for the per-sonal use or convenience of the holder ofthe special plates or some other person.Such activities as commuting or runningerrands, which are clearly for the “con-venience” of some person, is a non-ex-empt use. The statute makes noallowance for even minimal personaluse. Any degree of personal use, how-ever slight, disqualifies a motor vehiclefrom an excise exemption.

B. the manufacturer, farmer or dealerfiled an application with the assessors onor before December thirty-first of thepreceding year using State Tax Form126A requesting the exemption. The ap-plication must contain a statement “sub-scribed under penalties of perjury” bythe owner or controller of the vehiclethat it will not be operated for any per-sonal use.

PENALTY FOR UTILIZING VEHICLE

WITH SECTION 5 PLATE FOR

PERSONAL USE

If assessors discover that a vehicle operatedwith special plates and upon which an ex-emption was allowed is, notwithstanding,utilized for personal use, the assessors must,forthwith, assess the excise upon that vehi-cle. In addition, they shall assess a penaltyof $100.00. An excise assessed in such cir-cumstances cannot be subsequently abatedfor any part of the year of assessment, re-gardless whether title to the vehicle assessedis transferred.

Motor Vehicle & Trailer Excise Manual 13

ASSESSMENT SHOULD NOT BE

MADE ON REGISTRATION PLATES

Making assessments on vehicles operatedwith special plates is problematic for asses-sors because such plates may be movedfrom vehicle to vehicle. Since officials pos-sess no efficient means to know what vehi-cles these are, frequent assessment practicehas been to assess the plates, themselves,rather than the vehicles to which they are at-tached. This practice, however, is inconsis-tent with the holding of the SupremeJudicial Court in Board of Assessors ofNeedham v. E. J. Bleiler Equipment Co., Inc.,364 Mass. 834 (1974), a case which dealtwith dealer plates. The Court stated, “An as-sessment of a motor vehicle excise ondealer’s plates, as opposed to vehicles, is notauthorized by G.L. Ch. 60A §1.”

VII. Vehicles jointly registered in Massachu-setts and some other state, and customarilykept in the other state, provided:

A. the individual or business that ownsthe vehicle resides in another state, andhas no principal place of business in theCommonwealth, and

B. the other state does not impose ahigher (1) excise, (2) privilege or prop-erty tax, (3) registration fee or (4) fee inlieu of or in addition to a registration feeon Massachusetts vehicles:

1. customarily kept in Massachusetts and

2. registered:

a) by a resident of Massachusetts

b) both in Massachusetts and inthat other state.

Upon a request by a board of assessors, theCommissioner of Revenue will determinethe exemption eligibility of any particularregistrant. For a Supreme Judicial Court caseapplying the eligibility requisites for this ex-emption, see Akers Motor Lines, Inc. v. StateTax Commissioner, 344 Mass. 359 (1962).

VIII. Vehicles owned and registered bynon-domiciliary servicemen.

A. This exemption is available to servicemen:

1. whose domicile is not in Massachusetts,

2. who are in residence in Massachu-setts pursuant to military orders,

3. and who register their motor vehi-cles in this state.

B. The serviceman need not be stationedin Massachusetts. For example, he maybe stationed in a border state. So long ashe is absent from his domicile by reasonof compliance with military orders, he isexempt from the motor vehicle excise inevery state except that of his domicile.(Soldiers’ and Sailors’ Civil Relief Act, 50USCA §574 App.)

C. To determine the eligibility of a ser-viceman who seeks an exemption as anon-domiciliary, the assessors should re-quire a letter from the serviceman’s com-manding officer establishing that he isabsent from his domicile by reason ofcompliance with military orders, identi-fying the place of the serviceman’s as-signment.

D. A Massachusetts domiciliary who issent to some other state pursuant to mili-tary orders but does not cancel his Mass-achusetts registration is not eligible for amotor vehicle exemption.

E. A non-domiciliary serviceman mayqualify for an exemption on two or morevehicles. However, for each exemptionsought, the serviceman must be able toprove that he owns the subject vehicle.

F. A serviceman is not exempt for a vehi-cle registered to his spouse or to someother person. If a vehicle is ownedjointly by a serviceman and some otherperson(s), the serviceman is eligible foran exemption of only that percentage ofthe excise amount that corresponds tohis ownership share of the vehicle.

14 Exemptions

IX. Vehicles owned and registered by for-eign dignitaries, diplomats, consular officersor employees.

A. No Massachusetts statute grants amotor vehicle exemption for diplomats,etc. However, numerous tax exemptionsare granted by treaties and conventionswhich have the authority of federal lawand preempt any state law to the con-trary. For example, Article 49 of the Vi-enna Convention exempts diplomats ofsignatory nations and members of theirfamilies from all “dues and taxes, per-sonal or real, national, regional or mu-nicipal,” with exceptions not relevant tomotor vehicle excise.

B. In order to verify the status as a diplo-mat of a person claiming an exemption,assessors can contact:

Registration and Titling UnitDiplomatic Motor Vehicle OfficeU.S. Department of State Office ofForeign MissionsWashington, D.C. 20520

LIABILITY OF MOTOR VEHICLES

FOR A PERSONAL PROPERTY TAX

The motor vehicle excise is an assessment inlieu of a personal property tax. Vehicleswhich are exempt from the motor vehicleexcise are not subject to a personal propertytax, pursuant to Ch. 59 §5(35), which ex-empts from taxation motor vehicles whichare either subject to or exempt from the ex-cise under Ch. 60A.

Conversely, any vehicle which is not subjectto or exempt from the motor vehicle exciseis subject to taxation as personal propertyunder the provisions of Ch. 59 §18. Theowner of any such vehicle should reportthat property to the assessors on a form oflist, using either State Tax Form 2 or 2HF, asappropriate.

VALUATION OF VEHICLES SUBJECT

TO PERSONAL PROPERTY TAX

While Ch. 60A directs that vehicles be val-ued for excise in conformance with the for-mula set out in Section 1, Ch. 59 §38prescribes that assessors value personalproperty at “fair cash value.” In order to de-termine the fair cash value of unregisteredmotor vehicles, assessors should use valua-tion manuals, such as N.A.D.A.’s OfficialUsed Car Guide. Such manuals provide av-erage retail prices, as well as manufacturer’ssuggested list prices used for excise pur-poses. In addition, while the purchase priceof a motor vehicle is irrelevant for purposesof excise valuation, that price is pertinent forpersonal property valuation. So long as asale is arms length, some weight should begiven to the sales price in determining thevalue of the subject vehicle for purposes ofpersonal property tax assessment.

FARM PLATE EXEMPTION ISSUES

I. LIMITATION OF USE OF PLATES

A farm plate may not be used on a passen-ger vehicle. A pickup truck is not a passen-ger vehicle for purposes of this provision.Therefore, farm plates may properly be usedon pickup trucks.

II. USE OF PLATES ON FARM TRACTORS

While farm plates may be used on farm trac-tors, such use does not qualify those tractorsfor an exemption from the motor vehicle ex-cise. The exemption is available only for“motor vehicles and trailers” operated withfarm plates. Pursuant to Ch. 90 §1, vehicleswhich are (a) used for other purposes thantransportation of property, (b) incapable ofbeing driven at a speed exceeding twelvemiles per hour and (c) designed especiallyfor use elsewhere than on the traveled partof ways are expressly exempted from the

Motor Vehicle & Trailer Excise Manual 15

definition of motor vehicles. Since a farmtractor does not satisfy the definition of amotor vehicle, it is not subject to the motorvehicle excise in the first place. Rather, suchequipment should be assessed as personalproperty.

Where the owner of a tractor is “principallyengaged in agriculture,” that tractor may beeligible for assessment as farm machineryunder Ch. 59 §8A. This statute extends a taxadvantage to qualifying farmers. Under itsprovisions, the farm animals, machineryand equipment of a person principally en-gaged in agriculture is assessed “at the rateof five dollars per one thousand dollars ofvaluation.”

Alternatively, an owner of a tractor not qual-ifying for assessment under this statute issubject to taxation under the personal prop-erty provisions of Ch. 59 §18.

III. USE OF PLATES ON FARM TRAILERS

Farm trailers, also, do not qualify for ex-emption from the motor vehicle excise. Thedefinition of “trailer” in Ch. 90 §1 expressly

excludes “farm machinery or implementswhen used in connection with the operationof a farm or estate…[and] any vehicle whentowed behind a farm tractor and used inconnection with the operation of a farm orestate.” Therefore, farm trailers, like farmtractors, above, should be assessed either aspersonal property or as farm machinery.

IV. OPERATION OF UNREGISTERED VEHICLES

USED EXCLUSIVELY FOR AGRICULTURAL

PURPOSES

Ch. 90 §9 authorizes the operation of an un-registered tractor, trailer or truck for a dis-tance not exceeding one half mile, ifuninsured, or two miles, if insured, so longas it is used exclusively for agricultural pur-poses. Evidence of such insurance must befiled with the Registrar of Motor vehicles.

16 Exemptions

The rules and laws relating to abatements ofthe motor vehicle excise are set out in Ch.60A §1.

The authority to abate an excise lies in theboard of assessors. No other person maygrant an abatement.

While assessors possess authority to abatemotor vehicle excises, they may only do soonly within the limitations and consistentwith the specific circumstances which areset out in the statute. These limitations andcircumstances are discussed below.

APPLICATION FOR ABATEMENT

Assessors possess jurisdiction to abate amotor vehicle excise only if an applicationfor abatement is timely filed. To be timelyfiled, an application must be received by theassessors on or before December thirty-firstof the year following the year to which theexcise relates. If an excise bill is sent after De-cember first of the year following the year towhich an excise relates, then an applicationfor abatement, to be timely filed, must be re-ceived by the assessors on or before the thir-tieth day following the mailing of the bill.

PRORATION

As was explained in Chapter 1, motor vehi-cle excises are prorated on a monthly basis.For each month that the assessors allow anabatement on a motor vehicle, the excise dueon that vehicle is reduced by an amount

equal to one twelfth of the annual amountwhich would otherwise have been due, mul-tiplied by the number of months duringwhich the vehicle was not registered. Exceptin the case of an overvaluation, a conditionprecedent to the granting of an abatement isthe cancellation of the registration on a motorvehicle. Where a requisite for an abatement issuch cancellation, an abatement cannot begiven for any month during the vehicle wasregistered for any period of time.

CANCELLATION OF

REGISTRATION

Canceling the insurance policy on a motorvehicle does not effect a contemporaneouscancellation of the registration on that vehi-cle. Rather, to cause a cancellation, a regis-trant should deal directly with the Registryof Motor Vehicles, either in person, byphone or by mail.

To effectuate a cancellation on a particularvehicle, a registrant should return the li-cense plates to the Registry and receive aPlate Return Receipt. A registrant who doesnot have possession of those plates shouldobtain from the Registry a Form C19, “LostPlate Affidavit for Cancellation of Registra-tion.” Obtaining either a Plate Return Re-ceipt or a processed Form C19 willeffectuate a cancellation of the registrationon that vehicle.

An insurer, in order to cancel or revoke aninsurance policy on a motor vehicle, mustgive electronic notice to the Registry. If theRegistry does not receive a new certificate ofinsurance covering the same vehicle withinthe following twenty-three days, it will mailnotice to the registrant that unless a newcertificate is provided within the ensuingten days, the registration on that motor ve-hicle will be revoked.

Abatements 3

ExamplesFor an excise bill for calendar 1994 mailed at anytime during 1994, the deadline for submitting an ap-plication for abatement would be December 31, 1995.

For an excise bill for calendar 1994 mailed onMarch 4, 1996, the deadline for submitting the ap-plication would be April 3, 1996. (March has thirty-one days.)

MINIMUM ABATEMENT

The minimum motor vehicle abatementwhich may be made is five dollars. If a regis-trant otherwise qualifies for an abatementbut the amount of that abatement is less thanfive dollars, no abatement may be made.

CH. 58 §8If an application for abatement is not timelyfiled, the assessors, subsequently, have nojurisdiction to abate. If they wish, neverthe-less, to grant an abatement, their only legalrecourse is to seek authority from the Com-missioner of Revenue to grant the abate-ment. The Commissioner possessesauthority to authorize abatements underthis statute in circumstances where extraor-dinary or clearly mitigating circumstancesare demonstrated which justify a taxpayer’sfailure to have utilized the standard abate-ment process and the assessors do not,themselves, otherwise have authority toabate. For details regarding the submissionfor abatement authority under this statute,assessors should consult InformationalGuideline Release 92-206.

CIRCUMSTANCES WHICH ALLOW

ASSESSORS TO EXERCISE

ABATEMENT AUTHORITY

Where assessors possess jurisdiction tomake abatements, they may exercise thatauthority in the following circumstances:

I. A VEHICLE IS OVERVALUED

As is explained in Chapter 1 of this Manual,Ch. 60A §1 of the General Laws sets out theprocedure whereby motor vehicles are to bevalued for the purpose of the excise. Thisprocedure is based upon the manufacturer’slist price for that vehicle, discounted by thedesignated percentage which accords withthe age of the vehicle. However, the statutepermits the assessors to abate that value if,in their opinion, the value so determined isexcessive.

Assessors should rarely exercise this abate-ment authority and, then, only in the case ofsome extraordinary circumstance unique toa particular vehicle. If, for example, a vehi-cle were substantially damaged due to anaccident or other cause and were not re-paired, the assessors could lawfully abate itsvalue.

In the absence of some extraordinary cir-cumstance, however, a value properly calcu-lated should not be altered because valuingall motor vehicles using a uniform proce-dure ensures equity and regularity in the as-sessment process.

II. A REGISTRANT TRANSFERS TITLE TO A

VEHICLE AND CANCELS THE REGISTRATION

ON THAT VEHICLE

Ch. 60A §1 makes an abatement available if“during a calendar year ownership of amotor vehicle…is transferred by sale or oth-erwise and its registration is surrendered.

Two actions are necessary for qualificationfor this abatement eligibility. A vehicleowner must both (a) convey title to the vehi-cle and (b) cancel the registration on that ve-hicle. The performance of one of theseactions, alone, does not qualify a person foran abatement. Therefore, a person who can-cels the registration on a vehicle during acalendar year but does not convey title tothe vehicle is not entitled to an exciseabatement for any part of that year. For thesucceeding fiscal year, the vehicle should beassessed as personal property. See Chapter2, “Liability of motor vehicles for a personalproperty tax.”

A transfer of title may be made by gift, sale,repossession or any other action which con-veys ownership from the registrant to someother person. In processing an applicationfor abatement under this provision, asses-sors should require that they be presentedwith a copy of a bill of sale or some otherdocument which establishes that a transferhas occurred. If a registrant claims abandon-ment of a vehicle at a junk yard or someother place of disposition, that registrant

18 Abatements

must present evidence thereof, such as a re-ceipt from the owner of the junk yard. If aninsured vehicle is totaled in an accident andsettlement is made for the full value of thevehicle, title passes to the insurance com-pany by right of subrogation (legal doctrineof substituting one creditor for another). Insuch a case, the month the insurance com-pany makes payment to the insured is themonth that title transferred.

Generally, the assessors should require aplate return receipt to show evidence of can-cellation of registration. However, in somecircumstances, such as when a vehicle is to-taled in an accident and the vehicle is re-moved to a junk yard, it may not be possiblefor the owner to retrieve the plates. In suchcircumstances, the registrant should cancelthe registration on that vehicle using Reg-istry of Motor Vehicle Form C19 (See copyin Appendix.). Filing this form with the Reg-istry will eliminate future billings on the ve-hicle. Otherwise, excise bills will issue untilthe registration expires.

Whenever the performance of more thanone activity is required to establish eligibil-ity for an abatement, the proper date for usein calculating the amount of the abatementis that date when the final one of the activi-ties is performed.

III. A REGISTRANT MOVES OUT OF STATE AND

REGISTERS IN SOME OTHER STATE OR COUNTRY

A registrant is eligible for an excise abate-ment who “during a calendar year…re-moves to another state and registers suchmotor vehicle or trailer in such other stateand surrenders or does not renew his regis-tration in this state.” (G.L. Ch. 60A §1. Em-phasis supplied.)

As above, two actions are also necessary forabatement eligibility under this provision. Aperson must have (1) registered his vehiclein some other state and (2) surrendered hisMassachusetts registration.

Although, assessors should generally re-quire a person to present to them a plate re-turn receipt as evidence of cancellation of

his Massachusetts registration, this require-ment should be abandoned in the case of astate (e.g., Arizona and California) which,when issuing a registration, confiscates theplates of any other state in which the vehiclemay be registered at the time. In such a case,proof of registration in that state is sufficientevidence of the registrant’s cancellation ofhis Massachusetts registration. The date ofregistration in the other state could appro-priately be deemed the date of surrender ofthe Massachusetts registration for purposesof the relevant abatement provision underCh. 60A §1. Of course, if a person does notcancel his registration in Massachusettsusing a Form C19, excise bills will continueto issue until the registration expires.

IV. A PERSON CANCELS THE REGISTRATION ON

A VEHICLE AND SUBSEQUENTLY REREGISTERS

THAT VEHICLE IN THE SAME YEAR

No excise shall be due if assessed on thesame vehicle more than once in any calen-dar year by reason of the reregistration ofthat vehicle, except as outlined above in thecase of a transfer of that vehicle or a moveout of the state by its owner. If a person can-cels the registration on a motor vehicle inany particular year but does not transfertitle to that vehicle or does not move tosome other state and register the vehicle inthe other state and the person subsequentlyreregisters the vehicle in the same year, theexcise imposed for the months of the secondregistration should be abated. Otherwise,the person would be liable for two exciseson the same vehicle for the same year.

V. A PERSON SELLS OR TRADES A MOTOR

VEHICLE, CANCELS THE REGISTRATION ON

THAT VEHICLE AND SUBSEQUENTLY TRANSFERS

THE REGISTRATION TO SOME OTHER VEHICLE

IN SAME MONTH

If a person sells or trades a vehicle, cancelsthe registration on that vehicle and transfersthat registration to another motor vehicle inthe month of cancellation, the excise may befully abated on the transferred vehicle forthat month. Otherwise, the person would be

Motor Vehicle & Trailer Excise Manual 19

liable for two excises on the same registra-tion for the same month.

Such a person is not liable for a minimum$5.00 assessment on the transferred vehicle.

VI. A VEHICLE IS STOLEN

A. A registrant is eligible for an abatementof the excise on a vehicle which is stolen,provided that the registrant:

1. notifies the police within 48 hours ofdiscovery of the theft,

2. surrenders the certificate of registra-tion (not sooner than 30 days after thetheft), and

3. presents a certificate of cancellation ofregistration from the Registrar of MotorVehicles verifying that the vehicle hasbeen stolen. If the plates are lost with thestolen vehicle, the registrar will issue aForm C19, “Lost Plate Affidavit for Can-cellation of Registration.” The abatementwill be issued for the months followingthe month of cancellation of the certifi-cate of registration.

B. Vehicle subsequently recovered

If a motor vehicle which had been stolenand for which an abatement of the excisehas been granted is subsequently recoveredand registered in the same calendar year bythe same owner, that owner is liable to pay aproportionate part of the excise for thosemonths of the remaining year.

False report of the theft of a motor vehicle

If a registrant makes a false report of thetheft of a motor vehicle and seeks or obtains,thereby, an abatement of the excise on thatvehicle, the registrant is subject to a penaltyof up to three times the excise due on the ve-hicle for the entire year. To recover thispenalty, the city or town to which the excisewas payable must bring a civil actionagainst the registrant.

PROCESSING AN ABATEMENT

Upon granting an excise abatement, asses-sors must prepare an abatement certificate(State Tax Form 146) and provide a copy tothe tax collector and a copy to the registrant.Upon receipt of a certificate, a registrantmay go to the tax collector to request a re-fund, if the excise has been paid, or to havethe bill adjusted, if it has not.

The board must maintain copies of all abate-ments granted as permanent records. A ma-jority of the board must sign the abatementcertificates. In addition, the assessors mustregularly prepare a monthly report of all ex-cise abatements granted, using State TaxForm 156, and forward the report for eachparticular month to the collector as soon asreasonably possible following the end ofthat month.

ABATEMENT OF INTEREST

The Supreme Judicial Court, in Bordeau v.Registry of Motor Vehicles, 373 Mass. 429(1977), held that the abatement procedure isavailable to contest costs and fees, as well asthe amount of the excise assessed. TheCourt stated:

“Our construction of the scope of the remedyavailable in the abatement procedure re-quires an interpretation of the term “excise”broad enough to allow an aggrieved tax-payer the right to correct a possible injurydue to a wrongful assessment of any chargeassociated with the excise tax.”

Moreover, Ch. 60 §20 provides that when itis found, in any particular case, that no tax isdue, costs or fees should not be collected.

Therefore, when a tax collector receivesfrom the assessors a certificate which abatesall of an excise assessment, the collectorshould abate all the collection fees, enumer-ated in Ch. 60 §15, as well as all other inter-est and charges. These fees include fees forthe services of a deputy collector.

20 Abatements

APPEAL OF ASSESSORS’ DECISION

Pursuant to Ch. 58A §6, the Appellate TaxBoard has express jurisdiction to decide ap-peals of assessors’ decisions regardingmotor vehicle excise assessments. Ch. 60A§2 expressly authorizes aggrieved parties totake an appeal from any decision by the as-sessors relating to the motor vehicle exciseto the Appellate Tax Board.

REFUND OF INTEREST

If the Appellate Tax Board (or the CountyCommissioners) orders an abatement, Ch.60A §2 mandates that the municipality payinterest on the refund of any overpayment, atan annual rate of six percent, calculated fromthe date of payment. No interest shall bepaid on account of an overpayment upon anabatement granted by the board of assessors.

NOTIFICATION OF VALUATION

CORRECTION TO REGISTRY

Upon adjusting the value of a motor vehicle,assessors should forward an Assessors-Col-lectors Report of Record Change to the Reg-istry, thereby notifying the Registry of thevalue which is to be subsequently assignedto that vehicle. This assigned value shouldbe the manufacturer’s list price, not the cur-rent depreciated value.

Motor Vehicle & Trailer Excise Manual 21

COLLECTION REMEDIES

Pursuant to Ch. 60A§3, a tax collector, in the col-lection of the motor vehicle excise, “shall haveall the remedies provided by chapter sixty.”

DEMAND

A prerequisite to the use of most collectionremedies is the mailing of a demand. A de-mand must be “made more than one dayafter an excise becomes due and payable.”Therefore, if a bill were due on February first,the earliest a demand could properly bemailed would be February third. Just as withan initial excise bill, the law does not requirethat a demand bill be received; it requiresonly that demand be “made.” (Ch. 60A §1states that “failure to receive notice [of anoriginal excise bill] shall not affect the valid-ity of the excise. Ch. 60 §16 states, “failure toreceive [a demand] shall not invalidate a taxor any proceedings for the enforcement orcollection of the same.”)

DEPUTY TAX COLLECTORS OR

OTHER COLLECTION OFFICERS

Pursuant to Ch. 60 §92, a tax collector mayappoint a deputy tax collector to assist incollecting delinquent motor vehicle excises.(See I.G.R. 90-219 for requirements govern-ing deputy collectors.)

ISSUANCE OF A WARRANT

If an excise bill remains unpaid for fourteendays after the issuance of a demand, the taxcollector may issue a warrant to a deputycollector or other officer, thereby grantingauthority to that person to collect the delin-quent excise. The Commissioner of Rev-enue’s prescribed warrant form is State TaxForm 266 (updated 11/92). No other form is

to be used for this purpose without the ex-press permission of the Commissioner. Forthe issuance of a warrant, a $5.00 fee isadded to the delinquent bill.

NOTICE OF WARRANT

A deputy tax collector or other officer whoreceives a warrant authorizing the collectionof an overdue excise may give notice to thedelinquent of the receipt of that warrant.The Commissioner of Revenue’s prescribednotice form is State Tax Form 275 (updated11/92). No other form is to be used for thispurpose without the express permission ofthe Commissioner. For sending notice of theissuance of a warrant, a $9.00 fee is added tothe delinquent bill.

EXHIBITION OF WARRANT