monetizing the internet through sales and advertising

TRANSCRIPT

Monetizing the Internet Through Sales and Advertising

Gian Fulgoni

Executive Chairman and Co-Founder, comScore Inc.

2© comScore, Inc. Proprietary and Confidential.

comScore is a Global Market Research Company and Leader in

Measuring the Digital World

NASDAQ SCOR

Founded August 1999

Clients 1,750 worldwide

Employees 1,000+

Headquarters Reston, VA

Global Coverage170+ countries under

measurement;43 markets reported

Local Presence 30+ locations in 21 countries

V0910

3© comScore, Inc. Proprietary and Confidential.

comScore Leverages Rich Panel Data to Deliver Unique and Broad

Digital Business Analytics

2 Million Person Panel with 360°View of Person Behavior

V0910

4© comScore, Inc. Proprietary and Confidential.

The Internet as a Sales Channel

5© comScore, Inc. Proprietary and Confidential.

In 2010, Consumers Spent $228 Billion Online. With the Advantages of Lower Prices

and Convenience, E-commerce Continued to Grow in Importance in Q1 2011 and to

Rebound from Recession

$42 $53 $67$82

$102 $123 $130 $130

$142

$38

$30$40

$51

$61

$69

$77 $84 $80

$85

$22

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

$72$93

$117$143

Retail

Travel

+29%

+26%

+22%

+19%

+26%

+33%

+26%

+28%

+20%

+24%+24%

+13%

$171

$200

+17%

+20%

+12%

+6%

+9%

+7%

$214

0%

-5%

$209

-2%

U.S. E-commerce Dollar Sales Growth ($ Billions)Source: comScore e-Commerce Measurement

+10%

+6%

+9%

$228

+12%

+9%

Q1

6© comScore, Inc. Proprietary and Confidential.

E-commerce continues to gain share of retail spending on an apples-

to-apples basis and is approaching 10%

*Note: e-Commerce share is shown as a percent of DOC’s Total

Retail Sales excluding Food Service & Drinking, Food & Bev. Stores,

Motor Vehicles & Parts, Gasoline Stations and Health & Personal

Care Stores.

e-Commerce Share of Corresponding Retail Spending*Source: comScore for e-Commerce & U.S. Department of Commerce (DOC) for Retail

e-C

om

me

rce

Sh

are

e-Commerce share peaks in

colder seasons (Q4 & Q1)

4.3%

3.7%4.0%

4.6%

5.1%

4.3%4.5%

5.3%

5.9%

5.0%5.3%

6.4%

6.7%

5.9%

6.3%

7.4% 7.3%

6.5% 6.6%

7.6% 7.7%

6.8%6.9%

7.7%8.1%

7.1% 7.1%

8.0%

8.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

7© comScore, Inc. Proprietary and Confidential.

Rising gas prices have historically had a negative impact on e-

commerce spending growth. Will that re-occur?

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Y/Y % Change in Retail E-Commerce SpendingSource: comScore E-Commerce Measurement, Jan-07 - Mar-11

$2.96/gallon $4.14/gallon

8© comScore, Inc. Proprietary and Confidential.

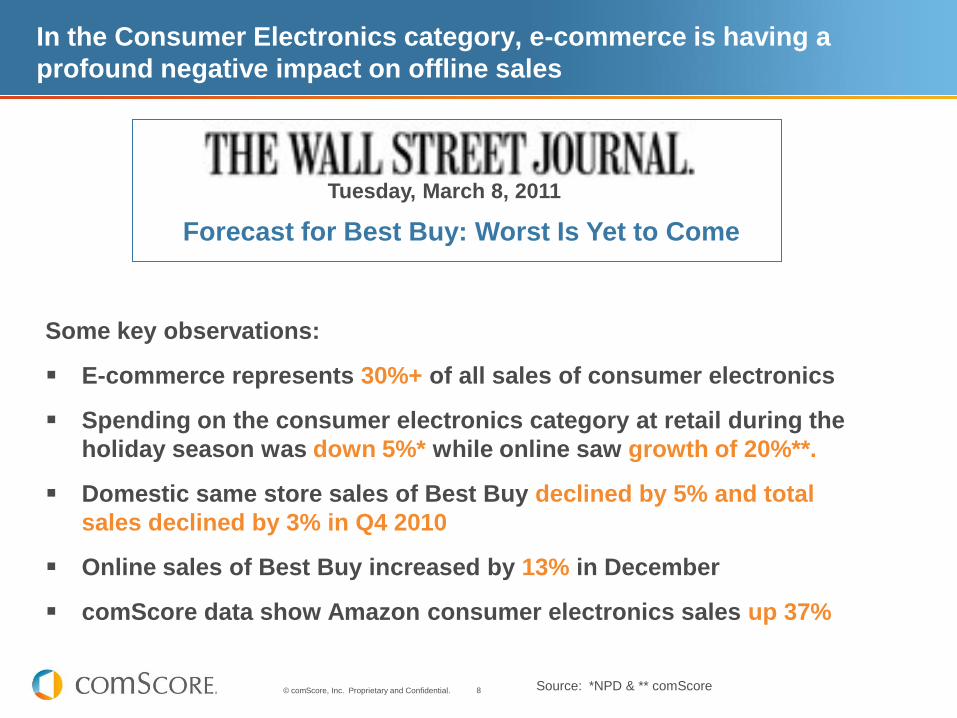

In the Consumer Electronics category, e-commerce is having a

profound negative impact on offline sales

Some key observations:

E-commerce represents 30%+ of all sales of consumer electronics

Spending on the consumer electronics category at retail during the

holiday season was down 5%* while online saw growth of 20%**.

Domestic same store sales of Best Buy declined by 5% and total

sales declined by 3% in Q4 2010

Online sales of Best Buy increased by 13% in December

comScore data show Amazon consumer electronics sales up 37%

Source: *NPD & ** comScore

Forecast for Best Buy: Worst Is Yet to Come

Tuesday, March 8, 2011

9© comScore, Inc. Proprietary and Confidential.

2010 free shipping patterns resembled 2009 until late November

when free shipping surged to 55%. For the remainder of the season,

2010 outpaced 2009 by 7-12 percentage points

41% 41%

47%50%

46%44% 45%

40%44%

41%

44% 45%45%

50%

55%

51% 52%52%

54%

50%

30%

35%

40%

45%

50%

55%

60%

31

-Oct-

10

2-N

ov-1

0

4-N

ov-1

0

6-N

ov-1

0

8-N

ov-1

0

10

-No

v-1

0

12

-No

v-1

0

14

-No

v-1

0

16

-No

v-1

0

18

-No

v-1

0

20

-No

v-1

0

22

-No

v-1

0

24

-No

v-1

0

26

-No

v-1

0

28

-No

v-1

0

30

-No

v-1

0

2-D

ec

-10

4-D

ec

-10

6-D

ec

-10

8-D

ec

-10

10-D

ec-1

0

12-D

ec-1

0

14-D

ec-1

0

16-D

ec-1

0

18-D

ec-1

0

20-D

ec-1

0

22-D

ec-1

0

24-D

ec-1

0

26-D

ec-1

0

28-D

ec-1

0

30-D

ec-1

0

1-J

an

-11

2009 2010

Percentage of e-Commerce Transactions with Free ShippingSource: comScore e-Commerce Measurement

Average Order Value on free shipping purchases was $110 during holiday

season 2010. For non-free shipping purchases it was $95.

2010 outpaced 2009 by

12 percentage points the

final Monday before

Christmas

10© comScore, Inc. Proprietary and Confidential.

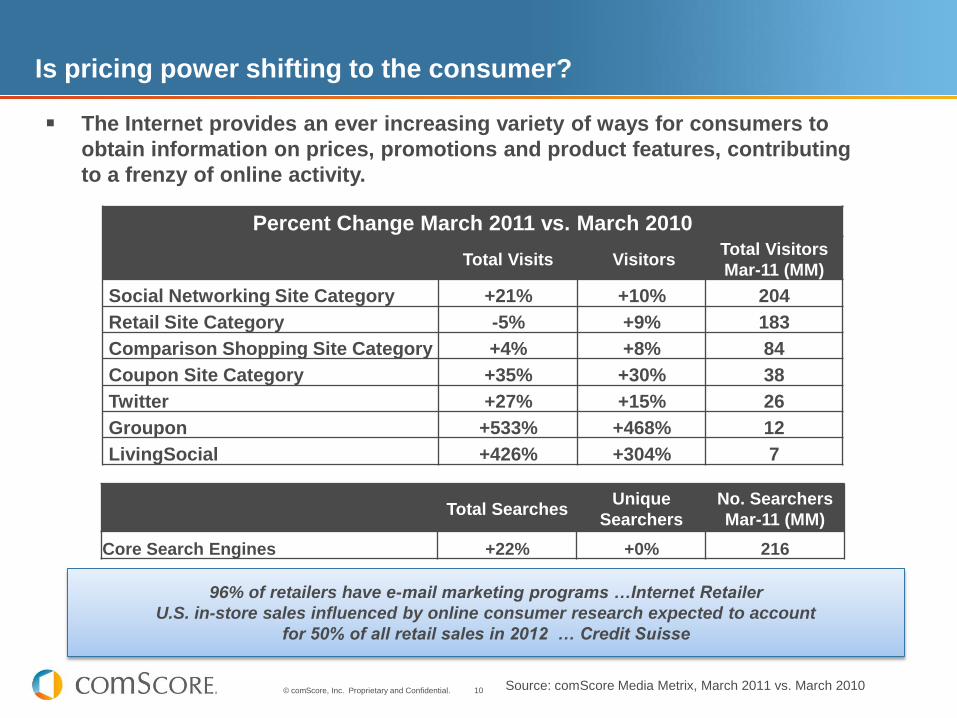

Is pricing power shifting to the consumer?

Percent Change March 2011 vs. March 2010

Total Visits VisitorsTotal Visitors

Mar-11 (MM)

Social Networking Site Category +21% +10% 204

Retail Site Category -5% +9% 183

Comparison Shopping Site Category +4% +8% 84

Coupon Site Category +35% +30% 38

Twitter +27% +15% 26

Groupon +533% +468% 12

LivingSocial +426% +304% 7

96% of retailers have e-mail marketing programs …Internet Retailer

U.S. in-store sales influenced by online consumer research expected to account

for 50% of all retail sales in 2012 … Credit Suisse

Source: comScore Media Metrix, March 2011 vs. March 2010

Total SearchesUnique

Searchers

No. Searchers

Mar-11 (MM)

Core Search Engines +22% +0% 216

The Internet provides an ever increasing variety of ways for consumers to

obtain information on prices, promotions and product features, contributing

to a frenzy of online activity.

11© comScore, Inc. Proprietary and Confidential.

And there‟s more: 31% of consumers now own or use some form of

smartphone or Internet-capable digital media device. This is

significantly higher among higher-income consumers

Smartphone Ownership and Usage

Q. Do you own or use a smartphone or digital media device, such as an iPhone, iPad, Droid, Blackberry or

similar device? Source: comScore Survey – January 2011

31%

67%

2%

Yes No Not sure

19%

32%

47%

Under $50k

$50k - $99k

$100k+

% who own or use a smartphone

Smartphone Ownership/usage (by income)

12© comScore, Inc. Proprietary and Confidential.

72 Million People (31% of 234 Million U.S. Mobile Subscribers) Now

Use a Smartphone to Access a Wide Variety of Content

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Social Networking

Classifieds Online Retail

General Reference

Maps Shopping Guides

Restaurant Info

Weather Auction Sites

Personal Email

Un

iqu

e U

se

r (0

00

)

Fastest Growing Mobile Site Content Categories by Total Audience (000)Source: comScore MobiLens, 3 mo. avg. ending Dec-2010 versus Dec-2009

Dec-09 Dec-10

+ 55% + 53%+ 47%

+ 46%

+ 46%

+ 45%

+ 45%

+ 45%

+ 39%

+ 56%

When it Comes to Mobile Content Consumption, Social Networking Ranks as Fastest Growing

Category, Followed by Classifieds and Retail

13© comScore, Inc. Proprietary and Confidential.

Building Sales with Online Marketing:

Lessons Learned

14© comScore, Inc. Proprietary and Confidential.

2010 U.S. Measured Media Spend

$149 BillionD

ire

ct

Re

sp

on

se

Bra

nd

ing

$91B

$58B

2010 U.S. Online Media Spend

$26 Billion

$6B

$20B

Internet is lagging in capturing branding dollars. Online spend in 2010

accounted for 34% of all media direct response spend, while online spend for

branding remained unchanged at $6B, or only 6% of all media branding ad

dollars.

61%

39%

6% of

branding

dollars

34% of direct

response

dollars

Source: Brand.net analysis based on Barclays Capital and DMA

$18Billion

in 2009

$6 Billion

in 2009

15© comScore, Inc. Proprietary and Confidential.

What We‟ve Learned About Online Advertising

The Click is at Best an Incomplete and at Worst a

Misleading Metric

Accurate Delivery of Media Plan is Critical

Creative Remains Extremely Important

Digital Ad Campaigns Lift In-Store Sales

In CPG: “Is Online the New Print”

Video Holds the Key to Powerful Online Branding

Campaigns

16© comScore, Inc. Proprietary and Confidential.

Clicks are at Best an Incomplete and at Worst a

Misleading Metric

17© comScore, Inc. Proprietary and Confidential.

Clickers Represent a Small and Declining Segment of Internet Users

July 2007 March 2009

• There are 50% fewer clickers today (16%) than in July 2007 (32%)

• 8% of all Internet users account for 85% of all clicks

• Optimizing against clicks means ignoring 84 percent of Internet users

Non-Clickers

68%

Clickers 32%

Non-Clickers

84%

Clickers16%

Source: comScore, Inc. custom analysis, Total US Online

Population, persons, July 2007 and March 2009 data periods

18© comScore, Inc. Proprietary and Confidential.

Global Click Rates on Individual Campaigns are Pitifully Low. In the

U.S., Only One in a Thousand Ads in a Campaign are Clicked

Source: DoubleClick DART for Advertisers, a cross section of regions,

January – December 2008

0.07%

0.08%

0.08%

0.08%

0.09%

0.10%

0.10%

0.10%

0.10%

0.11%

0.11%

0.12%

0.12%

0.12%

0.13%

0.14%

0.14%

0.14%

0.15%

0.16%

0.17%

0.18%

0.18%

0.20%

0.20%

0.21%

0.26%

0.29%

Norway

Ireland

Luxembourg

United Kingdom

Finland

Australia

Canada

Sweden

United States

Hungary

Switzerland

Denmark

France

Italy

Germany

New Zealand

Spain

Turkey

Austria

Netherlands

Belgium

China

Greece

India

Singapore

Hong Kong

United Arab Emirates

Malaysia

0.07%

0.08%

0.08%

0.08%

0.09%

0.10%

0.10%

0.10%

0.10%

0.11%

0.11%

0.12%

0.12%

0.12%

0.13%

0.14%

0.14%

0.14%

0.15%

0.16%

0.17%

0.18%

0.18%

0.20%

0.20%

0.21%

0.26%

0.29%

Norway

Ireland

Luxembourg

United Kingdom

Finland

Australia

Canada

Sweden

United States

Hungary

Switzerland

Denmark

France

Italy

Germany

New Zealand

Spain

Turkey

Austria

Netherlands

Belgium

China

Greece

India

Singapore

Hong Kong

United Arab Emirates

Malaysia

Worldwide Click-Through Rates*

*Click-through rates across Static Image, Flash, and Rich Media formats

19© comScore, Inc. Proprietary and Confidential.

The Meddlesome Click ….Some Agencies Get It

“A click means nothing. A click earns no revenue and creates

no brand equity. Your online advertising has some goal – and

it’s surely not to generate clicks. Regardless of whether they

clicked an ad or not, the key is to determine how that ad unit

influenced a consumer to think, feel, or do something they

wouldn’t have done otherwise.”

John Lowell

SVP Director, Research & Analytics

Starcom

“I spend a lot of time fighting against media metrics that

don’t matter”

Kate Sirkin

EVP Global Research

Starcom MediaVest Group

20© comScore, Inc. Proprietary and Confidential.

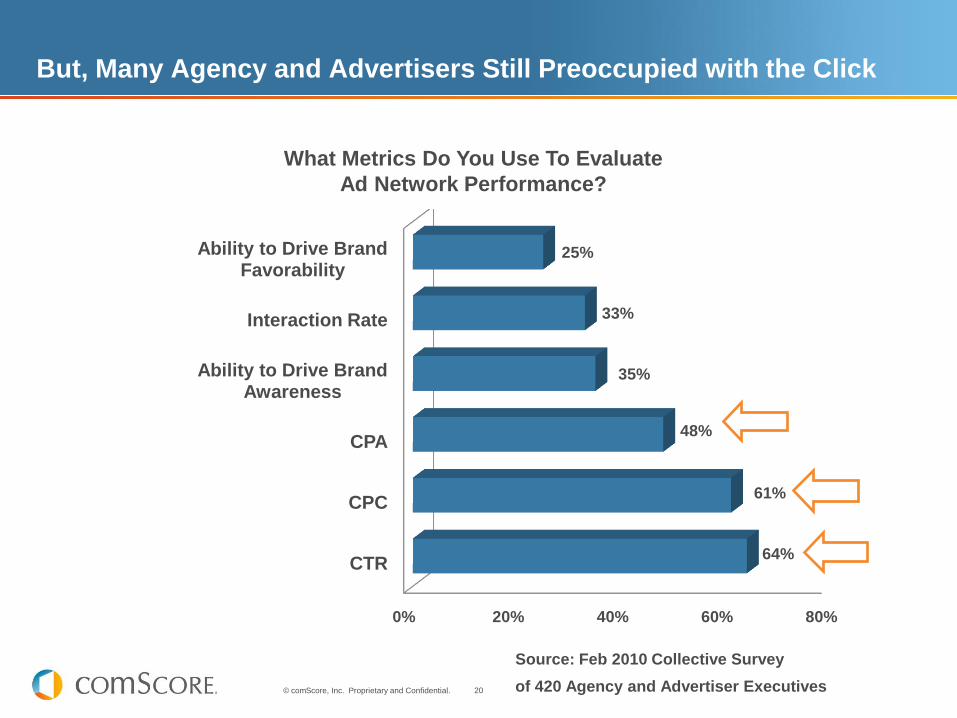

But, Many Agency and Advertisers Still Preoccupied with the Click

Source: Feb 2010 Collective Survey

of 420 Agency and Advertiser Executives

0% 20% 40% 60% 80%

CTR

CPC

CPA

Ability to Drive Brand Awareness

Interaction Rate

Ability to Drive Brand Favorability

64%

61%

48%

35%

33%

25%

What Metrics Do You Use To Evaluate

Ad Network Performance?

21© comScore, Inc. Proprietary and Confidential.

Journal Of Advertising Research:

comScore‟s “Whither the Click?”

Journal of Advertising Research, June 2009

“What We Know About Advertising: 21 Watertight Laws for

Intelligent Advertising Decisions”

comScore‟s “Whither the Click?”

– 200+ comScore studies conducted in the U.S. to assess

behavioral impact of paid search and online display ads.

21

Even with Minimal Clicks,

Display Advertising Proven to Lift:

• Site visitation

• Trademark search queries

• Online and offline sales

Prof. Byron Sharp, Ehrenberg Bass Institute, University of South Australia

Prof. Jerry Wind, The Wharton School

22© comScore, Inc. Proprietary and Confidential.

22

We Now Know Online Ads Incite Action Beyond the Click….

Results from 139 comScore Campaign Effectiveness Studies

2.1%

3.1%

3.9%

4.5%

3.5%

4.8%

5.8%

6.6%

Week of f irst exposure

Weeks 1-2 af ter f irst exposure

Weeks 1-3 af ter f irst exposure

Weeks 1-4 af ter f irst exposure

Advertiser Site Reach

Control Test

% Lif t: 65.0% % Lif t: 53.8% % Lif t: 49.1% % Lif t: 45.7%

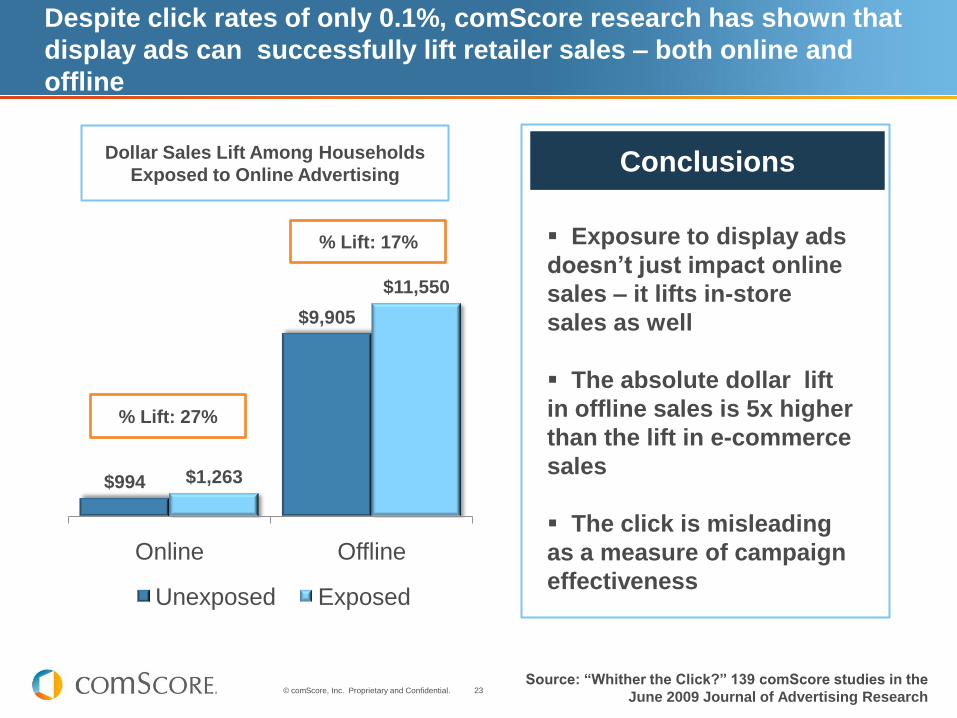

23© comScore, Inc. Proprietary and Confidential.

$994

$9,905

$1,263

$11,550

Online Offline

Unexposed Exposed

Dollar Sales Lift Among Households

Exposed to Online Advertising

% Lift: 17%

% Lift: 27%

Despite click rates of only 0.1%, comScore research has shown that

display ads can successfully lift retailer sales – both online and

offline

Source: “Whither the Click?” 139 comScore studies in the

June 2009 Journal of Advertising Research

Exposure to display ads

doesn‟t just impact online

sales – it lifts in-store

sales as well

The absolute dollar lift

in offline sales is 5x higher

than the lift in e-commerce

sales

The click is misleading

as a measure of campaign

effectiveness

Conclusions

24© comScore, Inc. Proprietary and Confidential.

Accurate Delivery of Media Plan is Critical

25© comScore, Inc. Proprietary and Confidential.

Cookie Deletion is a Global Reality … and a Global Challenge

Ad Server Cookies Web Site Cookies

Country

Percent of

computers

deleting

Average # of

cookies per

computer

for same

campaign

Percent of

computers

deleting

Average # of

cookies per

computer

for same

web site

Australia 37% 5.7 28% 2.7

Brazil 40% 6.6 33% 2.5

U.K. 35% 5.9 27% 2.7

U.S. 35% 5.4 29% 3.5

26© comScore, Inc. Proprietary and Confidential.

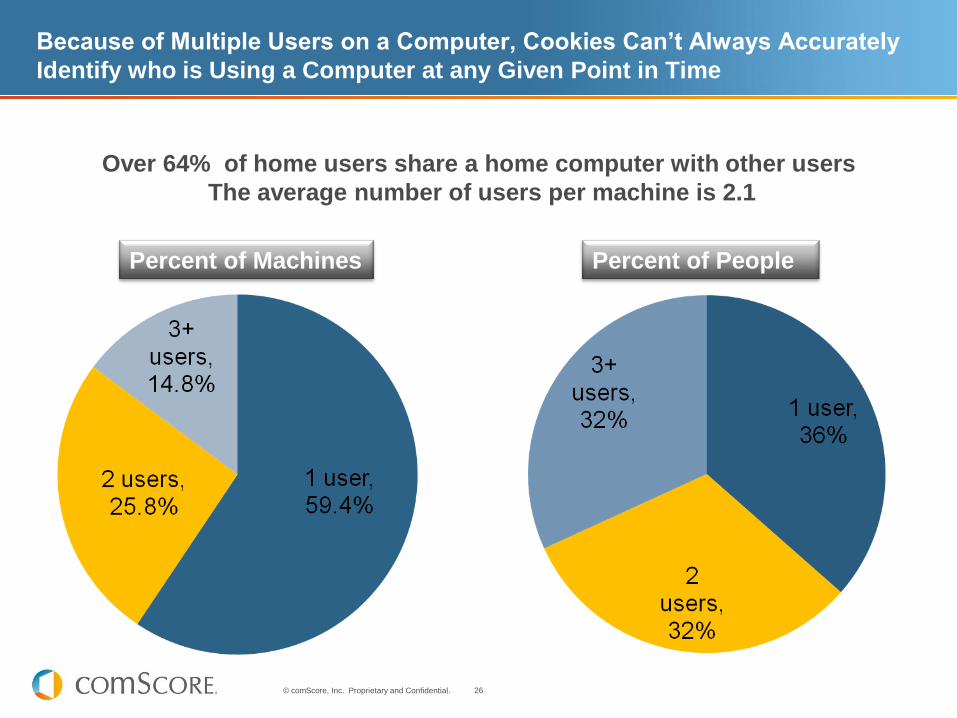

Because of Multiple Users on a Computer, Cookies Can‟t Always Accurately

Identify who is Using a Computer at any Given Point in Time

Over 64% of home users share a home computer with other users

The average number of users per machine is 2.1

Percent of Machines Percent of People

27© comScore, Inc. Proprietary and Confidential.

Ad frequency needs to be closely monitored:

Ad server delivery can be problematic

0

10

20

30

40

50

60

70

65%

17%

7%11%

Percent of PeopleBy Frequency of Exposure

-

10

20

30

40

50

60

21%

14%11%

54%

Percent of ImpressionsBy Frequency of Exposure

1 to 2 3 to 5 6 to 9 10+

1 to 2 3 to 5 6 to 9 10+

28© comScore, Inc. Proprietary and Confidential.

Campaign Delivery Can Miss Targeted Audiences.

Target for this Health & Well Being product was females age 35-54

Male40%

% C

om

po

sit

ion

of

Ex

po

se

d A

ud

ien

ce

Female

60%

40% of exposed consumers outside of planned gender target

14.4%

17.3%

25.3%

22.4%

20.6%

55+

Only 43% of females

exposed to the

campaign met the

targeted age group

Only 25% of all exposed consumers met planned targeting criteria

45-54

35-44

25-34

15-24

29© comScore, Inc. Proprietary and Confidential.

comScore‟s „Campaign Essentials‟ Real Time Reporting Dashboard

“How Many, Who, Which, Where?”

30© comScore, Inc. Proprietary and Confidential.

Creative is Extremely Important:

Proven Strategic Elements are a Must

31© comScore, Inc. Proprietary and Confidential.

The value of creative: In TV and Print, over 50% of the impact of

advertising is driven by the strength of creative

Ad Quality 52%

Media Plan13%

Other35%

*Quality of creative is based on ARS Persuasion Score which measures changes in

consumer preference through a simulated purchase exercise with and without

exposure to the creative .

comScore ARS Global Validation Summary includes an evaluation of 396 TV ad

campaigns, utilizing sales data from R. L. Polk New Vehicle Registration, IMS

HEALTH, IRI InfoScan, Markettrack, Nielsen SCANTRACK or Nielsen Retail Index.

Media Plan = Elements such as GRPs, wearout & continuity/flighting of airing

Ad Quality = Quality of the creative based on ARS Persuasion Score*.

Other = Price, promotion and distribution

% Influence on shifts in brand sales Source: Source: comScore ARS Global Validation Summary

Creative is 4x More

Impactful in

Influencing Sales

Than

The Media Plan

Numbers represent the percent variance in sales shifts explained by the corresponding factors.

32© comScore, Inc. Proprietary and Confidential.

Digital Campaigns Lift In-Store Sales for CPG:

• Is “Online the New Print?”

33© comScore, Inc. Proprietary and Confidential.

Short Term Offline Lift in CPG Brand Sales From Online Advertising

Matches Longer Term TV Impact: Is Online the New Print?

TV (BehaviorScan) Internet (comScore)

+8%+9%

BehaviorScan tests conducted over one year period

comScore studies over three months*

*Assumes 40% HH Internet Reach Against Target

Hypothesis 1: More precise targeting on the Internet allows more impressions to be

delivered against target audience in a given period of time

Hypothesis 2: Online ads include more messages about price and promotion than TV ads,

which tend to be mainly focused on branding

34© comScore, Inc. Proprietary and Confidential.

Offline Sales Lift in 3-Months from Online Advertising for CPG Brands

Not Surprisingly, Purchase-Based Targeting Has Been Shown To Drive

Even Higher Lifts In In-store Sales Than Non-Behaviorally Targeted

Campaigns

*Source: comScore Offline Sales Lift Norms, 2011

**Source: comScore Audience Advantage, which leverages sophisticated predictive

targeting algorithms that are created using anonymous panel and census data sources;

targeting was deployed on the Microsoft Network sites

Note: Retail sales is measured by linking the comScore panel of 1 million U.S. Internet

users to their retailer loyalty card data from dunnhumby, which provides a measure of the

panelist‟s in-store buying activity.

9%

22%

38%

40% Internet Reach Against Internet

Population*

100% Internet Reach Against Internet

Population*

Purchase-Based Targeting**

35© comScore, Inc. Proprietary and Confidential.

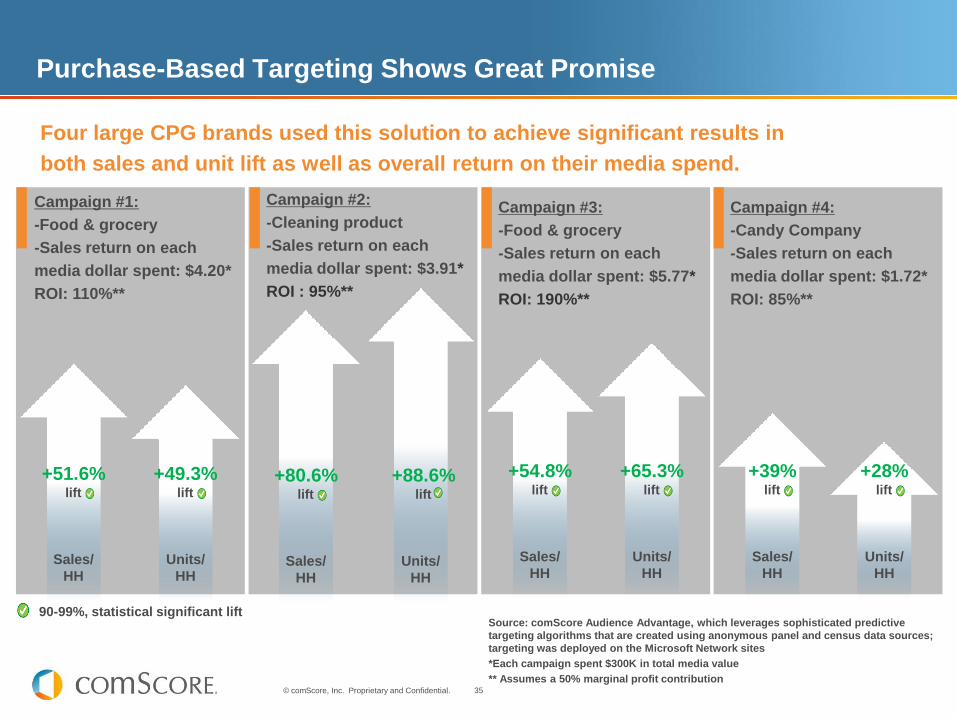

Purchase-Based Targeting Shows Great Promise

Four large CPG brands used this solution to achieve significant results in

both sales and unit lift as well as overall return on their media spend.

Campaign #1:

-Food & grocery

-Sales return on each

media dollar spent: $4.20*

ROI: 110%**

Campaign #2:

-Cleaning product

-Sales return on each

media dollar spent: $3.91*

ROI : 95%**

Sales/

HH

+80.6%lift

Units/

HH

+88.6%lift

Campaign #3:

-Food & grocery

-Sales return on each

media dollar spent: $5.77*

ROI: 190%**

Sales/

HH

+54.8%lift

Units/

HH

+65.3%lift

Sales/

HH

+51.6%lift

Units/

HH

+49.3%lift

90-99%, statistical significant lift

Campaign #4:

-Candy Company

-Sales return on each

media dollar spent: $1.72*

ROI: 85%**

Sales/

HH

+39%lift

Units/

HH

+28%lift

Source: comScore Audience Advantage, which leverages sophisticated predictive

targeting algorithms that are created using anonymous panel and census data sources;

targeting was deployed on the Microsoft Network sites

*Each campaign spent $300K in total media value

** Assumes a 50% marginal profit contribution

36© comScore, Inc. Proprietary and Confidential.

1Cases drawn from comScore ARS test databases and balanced by category (n=100 for digital display ads, n=3,681 for Television Ads)

Proven Strategic Branding Drivers are Used at a Much Lower Rate in Digital Ads

Proven Branding Element

Digital Display Ads1

(Rich Media, Banners,

Rectangles)

Television Ads1

Brand Differentiating Key Message 17% 31%

New Product/New Feature Information 19% 44%

Product Convenience (explicit & stated) 0% 9%

Competitive Comparison 10% 24%

Superiority Claim 13% 26%

Percent of Ads Containing Element

37© comScore, Inc. Proprietary and Confidential.

Elements

present

…But, Campaign Sales Are More Likely When Strategic Drivers Are

Used in Digital

Source: comScore blinded case studies

September 2010

-20.6

0.06.0 7.3

21.8

31.1 32.0 33.4

48.0 48.4

75.0 75.980.0

-25

0

25

50

75

100

Percent Lift in Sales (Exposed vs. Control)

Elements not

present

38© comScore, Inc. Proprietary and Confidential.

But Price / Promotion Used Much More Frequently

ElementDigital Display Ads1

(Rich Media, Banners, )Television Ads1

Brand Differentiating Key Message 17% 31%

New Product/New Feature Information 19% 44%

Product Convenience (explicit & stated) 0% 9%

Competitive Comparison 10% 24%

Superiority Claim 13% 26%

Price Reductions / Coupons / Samples 44% 8%

Percent of Ads Containing Element

1Cases drawn from comScore ARS test databases and balanced by

category (n=100 for digital display ads, n=3,681 for Television Ads)

39© comScore, Inc. Proprietary and Confidential.

Inclusion of promotion / price incentives in online ads

helps lift offline sales

Source: comScore blinded case studies

September 2010

26.8%28.4%

39.5%

48.9%

0.0%

20.0%

40.0%

60.0%

No Value Information Coupon Only Free Sample Explicit Value Claim

Percent Lift in Sales (Exposed vs. Control)

40© comScore, Inc. Proprietary and Confidential.

Video Holds the Key to Capturing Branding Dollars

41© comScore, Inc. Proprietary and Confidential.

Online Viewing of Video in February 2011 Reached 83% of Online

Users

NUMBER OF VIEWERS 173 Million

% OF INTERNET AUDIENCE 83%

VIDEOS VIEWED 31 Billion

VIDEOS PER PERSON 179

VIEWING TIME PER PERSON 13.5 hrs

Source: comScore Video Metrix, February 2011

88 million Americans

will watch

an online

video today!

42© comScore, Inc. Proprietary and Confidential.

Rapid Growth in Long-form TV Programming Online Over Past Year

Yearly growth in videos viewed on long-form TV programming sites

Source: comScore Video Metrix, February 2011 vs. February 2010

105%

Videos per Viewer

71%increase increase

Videos Viewed

43© comScore, Inc. Proprietary and Confidential.

Driven by Rapid Growth, Time Spent Viewing Online Video is Now

Equivalent to 8% of TV Viewing

Source: Nielsen for TV. comScore for Online Video

TV Viewing Online Video

36

3

Hours Watched Per Viewer Per Week

+4% vs. YA

+15% vs. YA

44© comScore, Inc. Proprietary and Confidential.

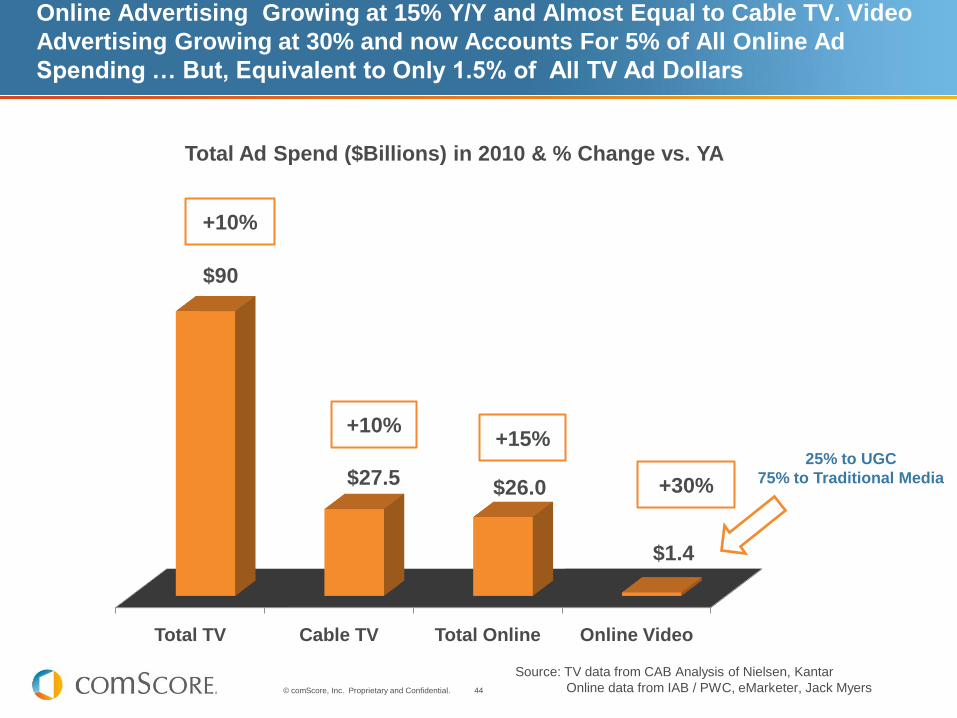

Online Advertising Growing at 15% Y/Y and Almost Equal to Cable TV. Video

Advertising Growing at 30% and now Accounts For 5% of All Online Ad

Spending … But, Equivalent to Only 1.5% of All TV Ad Dollars

Source: TV data from CAB Analysis of Nielsen, Kantar

Online data from IAB / PWC, eMarketer, Jack Myers

Total TV Cable TV Total Online Online Video

$90

$27.5 $26.0

$1.4

Total Ad Spend ($Billions) in 2010 & % Change vs. YA

25% to UGC

75% to Traditional Media

+10%

+10%+15%

+30%

45© comScore, Inc. Proprietary and Confidential.

Brands Trying to Reach their Target with TV Alone Hit A

Plateau of Diminishing Returns

85.1 87.9

67.874.1

0

10

20

30

40

50

60

70

80

90

100

0 2,500 5,000 7,500 10,000 12,500 15,000Cost ($000)

Total Reach

Effective Reach

Total Reach and Effective Reach for a TV

Campaign as a Function of Cost

Typically 30%+ of Target Audience is not Effectively reached

46© comScore, Inc. Proprietary and Confidential.

Adding Branding Advertising With Online Video Builds

Reach with Identical Investment

Media Plan GRPs Cost Total ReachEffective

Reach

TV Only 1,000 $10,000 85.1% 67.8%

TV + Internet Combination

TV (90%) 900 $9,000 83.7% 65.8%

Online (10%) 500 $1,000 63.8% 44.0%

TV + Online 1,400 $10,000 90.2% 83.7%

TV Only vs.

90% TV + 10% Online400 0 5.1% 15.9%

Impact of a 90/10 Budget Allocation

47© comScore, Inc. Proprietary and Confidential.

What We‟ve Learned

E-commerce is growing strongly and gaining share of consumers‟

wallets

– Has pricing power moved to the consumer?

Online advertising is effective, both as a direct response and

branding strategy

– The click is at best an incomplete and at worst a misleading metric

– Accurate delivery of media plan is critical

– Digital ad campaigns lift in-store sales

– Creative remains extremely important

– For CPG: “Is Display Advertising the New Print?”

– Video holds the key to more powerful online branding campaigns

47

Thank You!