misys changing role of transaction monitoring

TRANSCRIPT

8/8/2019 MiSys Changing Role of Transaction Monitoring

http://slidepdf.com/reader/full/misys-changing-role-of-transaction-monitoring 1/4

experiencesolutions

results

The changing role of transaction monitoring

in Anti Money Laundering compliance

Misys Executive Brief

8/8/2019 MiSys Changing Role of Transaction Monitoring

http://slidepdf.com/reader/full/misys-changing-role-of-transaction-monitoring 2/4

In 2008, all financial services organisations aroundthe world are now primary targets for a far tougher

regime of global regulatory scrutiny, as regulatorsincreasingly identify and respond to changesintroduced by new, far reaching Anti MoneyLaundering (AML) and Countering the Financingof Terrorism (CFT) controls.

The unprecedented changes taking place in theregulatory environment are being driven by:

+ The 3rd EU Money Laundering Directive for

European banks and their global branchnetwork

+ The new Financial Action Task Force (FATF)responses

+ The US extra territorial reach for any organisation wishing to trade in US dollars

Furthermore, changes to the financial industry –

the increasingly international nature of banking,the greater complexity of banking products andgrowing investment in emerging markets – aresignificantly adding to the difficulties faced bybanks when applying these regulations.

Misys Executive Brief

The changing role of transaction monitoringin Anti Money Laundering compliance

Estimated money laundering flows arereported to be in excess of US$1 trillionbeing laundered every year by drug dealers,arms traffickers and other criminals.

Founding principlesWe should perhaps remember the initialreasons for AML legislation: it was toprovide banks with a legal conduit theycould, and should, use to provideinformation on the transfer of funds bycustomers that they had reasonablegrounds to believe was illegal.

Today, banks are required to behonourable custodians and guardiansof their customers’ and their ownfinancial assets. With regard to AMLand CFT, banks are not required to beforensic investigation teams of anInterpol nature.

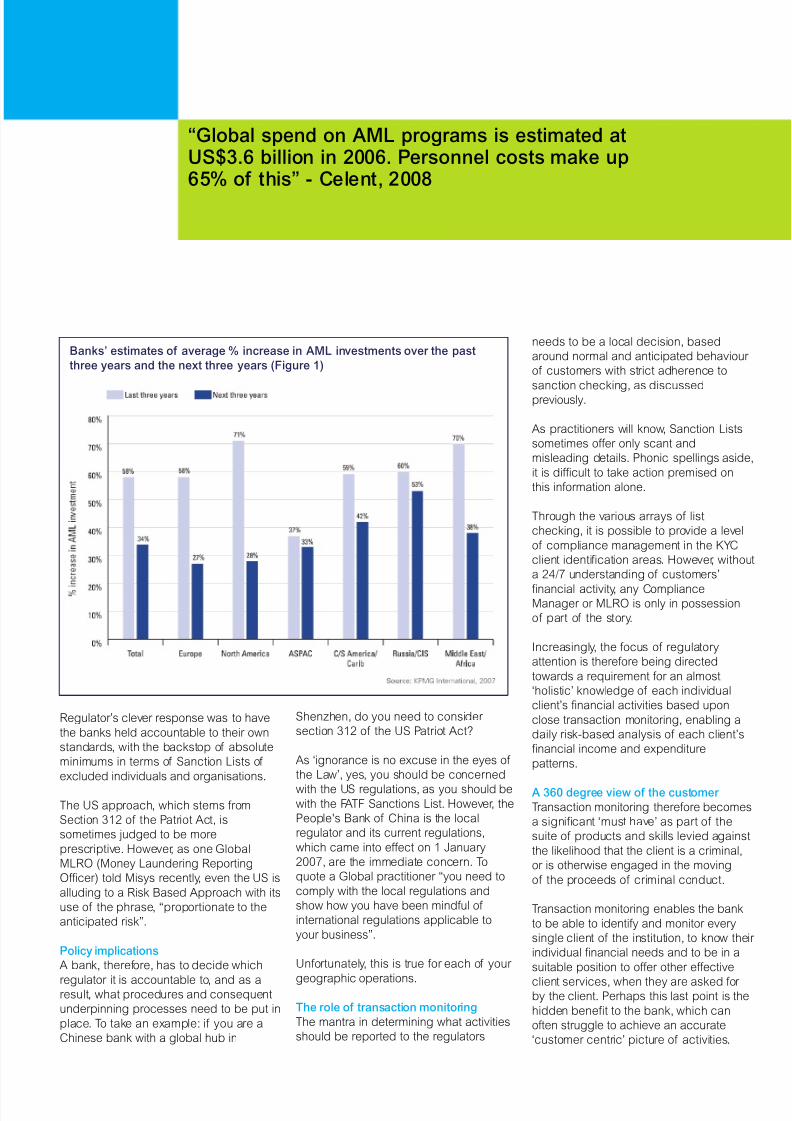

Banks may go to extreme lengths toprevent fraud against their ownorganisations, but that is a separateissue and one where the cost can beevaluated against the received reward.No such return-on-investment (ROI)scenario exists for regulatory practice.This becomes particularly relevant whenyou consider the escalating costs of compliance as highlighted by KPMG’sGlobal Anti-Money Laundering Survey2007. The costs of AML compliancehave proved to far exceed expectations,with an estimated 58% increase since2004 (see Figure 1).

Which regulation matters more?The challenge as perceived by manybanks is that there are potentiallymultiple sets of differing regulatoryrequirements. The European banks arenow being held accountable to the RiskBased Approach, which was firstpioneered in the UK and then adoptedat an EU level.

This approach moves away from having

prescriptive mandates about what youshould and should not do and was aresponse to accusations by banks thatthe regulatory requirements were tooonerous and often not applicable. The

8/8/2019 MiSys Changing Role of Transaction Monitoring

http://slidepdf.com/reader/full/misys-changing-role-of-transaction-monitoring 3/4

Regulator’s clever response was to havethe banks held accountable to their ownstandards, with the backstop of absoluteminimums in terms of Sanction Lists of excluded individuals and organisations.

The US approach, which stems fromSection 312 of the Patriot Act, issometimes judged to be moreprescriptive. However, as one GlobalMLRO (Money Laundering ReportingOfficer) told Misys recently, even the US isalluding to a Risk Based Approach with itsuse of the phrase, “proportionate to theanticipated risk”.

Policy implicationsA bank, therefore, has to decide which

regulator it is accountable to, and as aresult, what procedures and consequentunderpinning processes need to be put inplace. To take an example: if you are aChinese bank with a global hub in

Shenzhen, do you need to consider section 312 of the US Patriot Act?

As ‘ignorance is no excuse in the eyes of the Law’, yes, you should be concerned

with the US regulations, as you should bewith the FATF Sanctions List. However, thePeople's Bank of China is the localregulator and its current regulations,which came into effect on 1 January2007, are the immediate concern. Toquote a Global practitioner “you need tocomply with the local regulations andshow how you have been mindful of international regulations applicable toyour business”.

Unfortunately, this is true for each of your

geographic operations.

The role of transaction monitoringThe mantra in determining what activitiesshould be reported to the regulators

needs to be a local decision, basedaround normal and anticipated behaviour of customers with strict adherence tosanction checking, as discussedpreviously.

As practitioners will know, Sanction Listssometimes offer only scant andmisleading details. Phonic spellings aside,it is difficult to take action premised onthis information alone.

Through the various arrays of listchecking, it is possible to provide a levelof compliance management in the KYCclient identification areas. However, withouta 24/7 understanding of customers’

financial activity, any ComplianceManager or MLRO is only in possessionof part of the story.

Increasingly, the focus of regulatoryattention is therefore being directedtowards a requirement for an almost‘holistic’ knowledge of each individualclient’s financial activities based uponclose transaction monitoring, enabling adaily risk-based analysis of each client’sfinancial income and expenditurepatterns.

A 360 degree view of the customer Transaction monitoring therefore becomesa significant ‘must have’ as part of thesuite of products and skills levied againstthe likelihood that the client is a criminal,or is otherwise engaged in the movingof the proceeds of criminal conduct.

Transaction monitoring enables the bankto be able to identify and monitor everysingle client of the institution, to know their individual financial needs and to be in asuitable position to offer other effective

client services, when they are asked for by the client. Perhaps this last point is thehidden benefit to the bank, which canoften struggle to achieve an accurate‘customer centric’ picture of activities.

“Global spend on AML programs is estimated atUS$3.6 billion in 2006. Personnel costs make up65% of this” - Celent, 2008

Banks’ estimates of average % increase in AML investments over the pastthree years and the next three years (Figure 1)

8/8/2019 MiSys Changing Role of Transaction Monitoring

http://slidepdf.com/reader/full/misys-changing-role-of-transaction-monitoring 4/4

Future trends and ramificationsMoney laundering regulations haveattracted a significant degree of USattention, and breaches of regulations,particularly in dollar-denominatedtransactions, will always pose specialrisks for non-US practitioners.

Where those firms fall foul of US laws,they will increasingly find themselves thesubject of extra territorial intervention bythe US Justice Department, and evidenceof regulatory breaches will be submittedand used in evidence in any extraditionapplication made by the US FederalAuthorities. The ‘NatWest Three’ are ahigh profile example of this.

In 2008 and beyond, we shall see a far greater emphasis being placed oninvestigations into dealings with PEPsand charitable organisations. Corruptionallegations will assume increasedimportance as the US brings its extraterritorial powers to bear on executivesof foreign companies whom they deemto be guilty of involvement in thepayment of commissions to foreignagents to win business.

To find out how Misys canhelp you effectively meet

your compliance objectives,

please contact your Misys

account representative or

visit :

www.misys.com/banking

As a consequence, transaction monitoringbecomes the most significant weapon inthe armoury of the efficient complianceprofessional. It enables them to remainproactive in the surveillance of their clients’ affairs and to remain focusedon the delivery of a proportionaterisk-based approach.

By calibrating the rule-sets of atransaction monitoring system as closelyas possible to the risk level definitions theindividual institution is willing to accept, aconsistent and documented strategy canbe adopted by the bank. A strategy that isaudited and demonstrable to each and allregulatory practice.

"the world's 'shadow economy' now accountsfor between 15 and 20 % of global turnover"excerpt from McMafia, by Misha Glenny

'Misys' is a trade mark of Misys Plc, a mark registered in various

countries worldwide. All other product and company names may

be trade marks of their respective owners.

Copyright © 2007 Misys Services Limited. All rights reserved.

Misys Services Limited is a member of the Misys group of

companies.

Registered in England, No. 01941076 Registered Office: Burleigh

House, Chapel Oak, Salford Priors, Evesham, WR11 8SP

Automated transaction monitoringAutomated transaction monitoringsystems review thousands, if not

millions, of transactions to find theone incident representing a truecase of money laundering, fraud or market abuse.

These systems aim to reduce theamount of time spent by analyst teamson manually monitoring and identifyingsuspicious activity. Two types of potential issues can be flagged: a falsepositive, marking a ‘clean’ transactionor account as a financial crime alert;and a false negative, missing a realfinancial crime incident.

The balance a bank achieves betweenthe two, through risk-based rules, iscritical. A system that produces anexcessive number of false positiveswill require a large number of analyststo investigate the high volume of alerts, leading to higher costs. On theother hand, monitoring systems mustbe comprehensive and sensitiveenough to find cases of financial crimethat do exist.

Transaction monitoring technologiesshould provide a full audit trail for record keeping and internal reporting,as well as immediate access to allinformation for an analyst to investigatea case. Additional considerationsinclude the creation of intuitiveinvestigation workflows and adequatereporting for regulators.