microcredit project (loan 1327-ino) in indonesia · microcredit project (loan 1327-ino) in...

TRANSCRIPT

PCR: INO 26471

Microcredit Project (Loan 1327-INO) In Indonesia January 2005

Asian Development Bank

Project Completion Report

ADB

CURRENCY EQUIVALENTS

Currency Unit – rupiah (Rp)

At Appraisal At Project Completion (June 1994) (July 2002)

Rp1.00 = $0.000108 $0.000112 $1.00 = Rp9,269 Rp9,195

ABBREVIATIONS ADB – Asian Development Bank BI – Bank Indonesia BPD – Bank Pembangunan Daerah (regional development bank) BPR – Bank Perkreditan Rakyat (village bank) CGAP – Consultative Group to Assist the Poorest GNP – gross national product LDKP – Lembaga Dana Kredit Pedesaan (small nonbank financial institution) MFI – Microfinance institution NGO – nongovernment organization PAM – project administration memorandum PCR – project completion report or project completion review PIU – project implementation unit SFI – small financial institution SHG – Self-help group TA – technical assistance

NOTES

(i) The fiscal year (FY) of the Government and its agencies ends on 30 March. FY before a calendar year denotes the year in which the fiscal year ends; for example, FY2000 ends on 30 March 2000.

(ii) In this report, "$" refers to US dollars.

CONTENTS

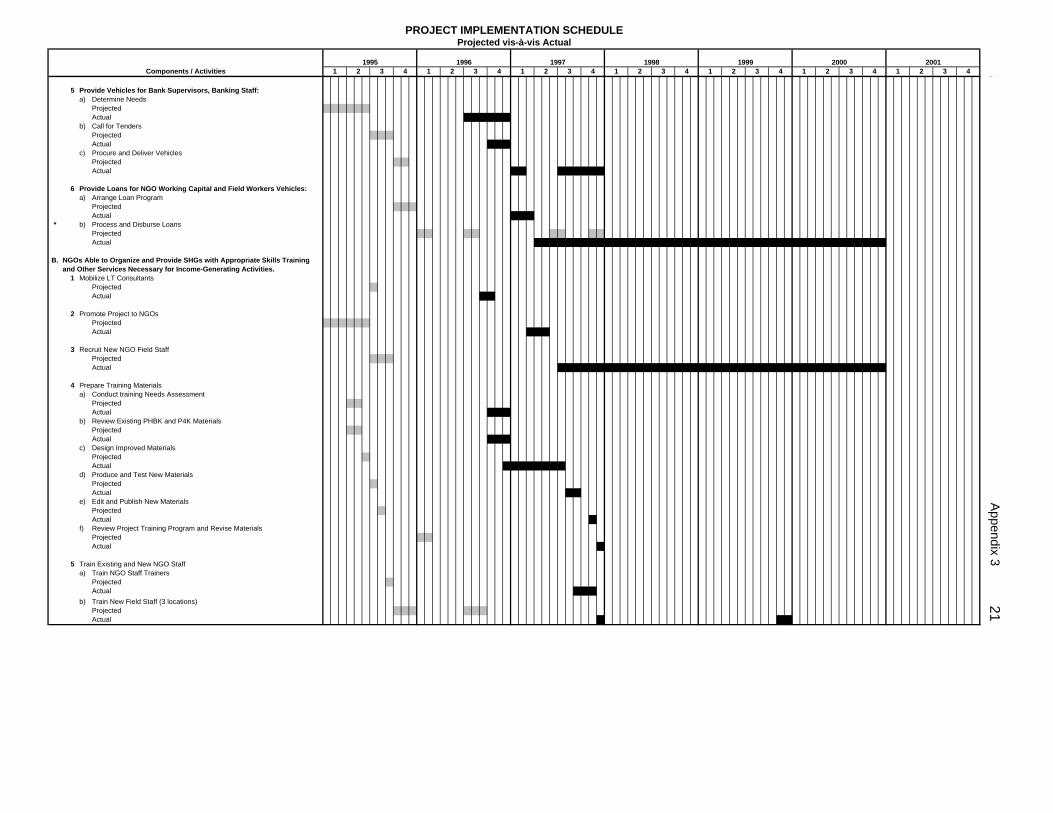

Page

BASIC DATA i I. PROJECT DESCRIPTION 1 II. EVALUATION OF DESIGN AND IMPLEMENTATION 1

A. Relevance of Design and Formulation 1 B. Project Outputs 3 C. Project Costs 6 D. Disbursements 6 E. Project Schedule 7 F. Implementation Arrangements 7 G. Conditions and Covenants 7 H. Related Technical Assistance 8 I. Consultant Recruitment and Procurement 8 J. Performance of Consultants, Contractors, and Suppliers 9 K. Performance of the Borrower and the Executing Agency 9 L. Performance of the Asian Development Bank 10

III. EVALUATION OF PERFORMANCE 10 A. Relevance 10 B. Efficacy in Achievement of Purpose 11 C. Efficiency in Achievement of Outputs and Purpose 11 D. Preliminary Assessment of Sustainability 11 E. Environmental, Sociocultural, and Other Impacts 12

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS 12 A. Overall Assessment 12 B. Lessons Learned 12 C. Recommendations 14

APPENDIXES 1. Project Framework 16 2. Project Poverty Indicators 19 3. Project Implementation Schedule: Projected vs. Actual 20 4. Consultant Staffing Schedule 23 5. Project Loan Sizes in Perspective 24 6. List of Subloans 25 SUPPLEMENTARY APPENDIXES (available on request) A. Bank Indonesia Project Completion Report B. Bank Indonesia Report: Social Impacts on Subborrowers

BASIC DATA

A. Loan Identification 1. Country Indonesia 2. Loan Number 1327-INO 3. Project Title Microcredit Project 4. Borrower Republic of Indonesia 5. Executing Agency Bank Indonesia 6. Amount of Loan SDR17,469,000 7. Project Completion Report Number B. Loan Data

1. Appraisal − Date Started − Date Completed

6 June 1994 15 June 1994

2. Loan Negotiations − Date Started − Date Completed

22 September 1994 23 September 1994

3. Date of Board Approval 25 October 1994 4. Date of Loan Agreement 10 January 1995

5. Date of Loan Effectiveness − In Loan Agreement − Actual − Number of Extensions

10 April 1995 21 July 1995

6. Closing Date

− In Loan Agreement − Actual − Number of Extensions

30 June 2000 5 July 2002 Three

7. Terms of Loan − Service Charge − Maturity (number of years) − Grace Period (number of years)

1% per year 35 10

8. Terms of Relending − Interest Rate − Maturity (number of years) − Grace Period (number of years)

1% per year 35 10

ii

9. Disbursements a. Dates Initial Disbursement

10 January 1997

Final Disbursement

25 April 2002

Time Interval

64.4 months

Effective Date

21 July 1995

Original Closing Date

30 June 2000

Time Interval

60.3 months

b. Amount (SDR ‘000)

Category Number Category

Original Allocation

Last Revised

Allocation Amount

Canceled Amount

Disbursed

01 02 03 04 05a 05b 05c 06 07 08

Computers Vehicles Other Equipment Consulting Services Credit Facilities Training Consulting Services Service Charge during Construction Prior TA Cost Unallocated

108 663 35

810 13,277

1,362 646 263 140 165

550 782

0 596

14,774 30

418 263 56 0

(190) (153)

0 415

(1,234) 0

(418) (16)

0 0

360 629

0 1,011

13,540 30 0

247 56 0

Total 17,469 17,469 (1,596) 15,873 TA = technical assistance C. Project Data

1. Project Cost ($’ 000) Cost Appraisal Estimate Actual Foreign Exchange 3,700 3,159 Local Currency 38,800 17,710 Total 42,500 20,869 2. Financing Plan ($’ 000) Cost Appraisal Estimate Actual Financing Plan ($ million) Borrower Financed ADB Financed Other External Financing Total IDC Costs Borrower Financed ADB Financed Other External Financing Total

16,800 25,700

0 42,500

263

0 0

263

7,271 13,598

0 20,829

321

0 0

321 ADB = Asian Development Bank, IDC = interest and other charges during implementation.

iii

3. Cost Breakdown by Project Component (SDR’ 000)

Component Appraisal Estimate Actual

01 Computers 02 Vehicles 03 Other Equipment 04 Consulting Services 05a Credit Facilities 05b Training 05c Consulting Services 06 Service Charge During Construction 07 Prior TA Cost 08 Unallocated Total

108 663 35

810 13,277

1,362 646 263 140 165

17,469

360 629

0 1,011

13,540 30 0

247 56 0

15,873 TA = technical assistance.

4. Project Schedule

Item Appraisal Estimate Actual

I. Sustainable Small Financial Institutions (SFIs) (i) Identify SFIs and Disburse Credit Funds (ii) Prepare SFI Training Materials (iii) Trains SFI Staff (iv) Computerize SFI Activities (v) Provide Vehicles for Bank Supervisors,

Banking Staff (vi) Provide Loans for NGOs’ Working

Capital and Field Worker Vehicles II. NGOs Able to Organize and Provide Self-

Help Group (SHD) with Appropriate Skills, Training, and Other Services Necessary for Income-Generating Activities

(i) Mobilize LT Consultants (ii) Promote Project to NGOs (iii) Recruit New NGO Field Staff (iv) Prepare Training Materials (v) Train Existing and New NGO Staff (vi) Computerize NGO Activities III. Bank Indonesia Able to Implement, Monitor,

and Supervise a Range of SFIs and NGOs (i) Project Start-Up (ii) Conduct Special Studies to Support NGO

Component (iii) Produce Project Reports (iv) Determine and Procure Vehicles (v) Design and Conduct Baseline Survey (vi) Collect and Process Follow-Up BME and

Impact Data (vii) Analyze Impact Data for Completion

Report

Feb 1995−Dec 1999 Jul 1995−Jun 1997 Jan 1996−Nov 1997 Jul 1995−Oct 1996 Jan 1996−Nov 1995 Oct 1995−Dec 1997 Jul 1995 Jan 1995−Jun 1995 Jul 1995−Sep 1995 Apr 1995−Feb 1996 Sep 1995−Sep 1996 Oct 1995−Mar 1996

Jan 1995−Jun 1995 Oct 1995−Dec 1998 Jul 1995−Dec 1999 Jan 1995−Jun 1995 Jul 1995−Dec 1995 Jan 1996−Sep 1999 Oct 1999−Dec 1999

BME = benefit monitoring and evaluation, NGO = nongovernment organization, SFI = small financial institution, SHG = self-help group.

iv

5. Project Performance Report Ratings

Ratings

Implementation Period Development Objective Implementation Progress

1 January–31 December 1999 S S 1 January–31 December 2000 S S 1 January–31 January 2001 HS HS 1 February–30 April 2001 S PS 1 May– 31 December 2001 S S 1 January–31 June 2002 S S HS = highly satisfactory, PS = partly satisfactory, S = satisfactory. D. Data on Asian Development Bank Missions Name of Mission

Date No. of Persons

No. of Person-Days

Specialization of Members

Loan Appraisal 6−15 Jun 1994 3 30 project economist, senior counsel, financial analyst

Loan Review 1−21 Dec 1998 3 63 senior economist, loan administration, staff consultant

Loan Review 30 Aug−1 Sep 1999 1 3 manager, AEAR Loan Review 4−18 Dec 2000 1 15 senior economist Loan Review 24 May −9 Apr 2001 2 32 project specialist, associate project

analyst PCR 1 18−22 Sept 2004 1 5 credit specialist PCR = project completion report, AEAR = Agriculture and Rural Development Division (East). 1 The project completion report was prepared by Roger Thomas Moyes, Credit Specialist.

I. PROJECT DESCRIPTION 1. The goal of the Project was to increase income and employment in rural areas, and the objectives were to alleviate poverty and promote the participation of women in development activities. The Project proposed to achieve these through four related components:

(i) lending to the poor and near-poor for the development of small, simple, low-cost microenterprises through a credit line to small financial institutions (SFIs);

(ii) strengthening of SFIs to provide efficient and cost-effective small-scale financial services for the development and sustainable operation of microenterprises;

(iii) strengthening nongovernment organizations (NGOs) to organize and provide self-help groups (SHGs) with skills training and other services necessary for income-generating activities; and

(iv) strengthening of Bank Indonesia’s (BI) capacity to implement, monitor, and supervise a range of SFIs and NGOs that provide small-scale financial services in rural areas.1

2. A four-fold rationale was presented for the Project:

(i) loans from SFIs to microenterprises help create jobs and increase incomes, and SFIs have real funding constraints;

(ii) SFIs are overly dependent on short-term funding sources and need long-term funding to provide efficient and cost-effective small-scale financial services for the development and sustainable operation of microenterprises;

(iii) NGOs provide a valuable service in organizing poor people into groups, and preparing them to receive small amounts of credit, and NGOs lack resources; and

(iv) institutional strengthening is required to build sustainable providers of microfinance.

II. EVALUATION OF DESIGN AND IMPLEMENTATION

3. The Project was designed around a credit line to SFIs and NGOs, and loan-funded technical assistance (TA) was incorporated to meet institutional capacity-building requirements. Implementation was managed by a project implementation unit (PIU) at BI, the Executing Agency. 4. The credit line could be accessed by different kinds of SFIs, which for the purposes of the Project include Bank Pembangunan Daerah (BPDs) (regional development banks), Lembaga Dana Kredit Pedesaan (LDKP) (small non-bank financial institutions, usually found at the village level), and Bank Perkreditan Rakyat (BPRs) (village banks). Proceeds of borrowing by BPDs would be for onlending to LDKPs, representing a wholesale arrangement. Borrowing by LDKPs would be primarily for onlending to individual microenterprises or to groups. Similarly, BPRs could borrow for onlending to microenterprises or to groups. Both LDKPs and BPRs could borrow for fixed assets or for training, which would allow them to expand and/or

1 ADB. 1994. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to the

Republic of Indonesia for the Microcredit Project. Manila. Project coverage initially was limited to five provinces, including West Java, Central Java, East Java, Nusa Tenggara Barat, and South Kalimantan. Ten additional provinces were later added, including Aceh, North Sumatra, West Sumatra, Bengkulu, Riau, Lampung, Yogjakarta, Bali, South Sulawesi, and North Sulawesi.

2

improve their operations. NGOs could borrow from either BPRs or LDKPs and use the funds for internal capacity building or for group onlending. A. Relevance of Design and Formulation 5. The Project, designed in 19942 was consistent with ADB's country program and strategy and development objectives of that time, and also was consistent with the Government’s concurrent goals and policies, which were to direct development assistance to projects that improve the lives of the poor.3 To a great degree, the Project anticipated refocusing ADB’s operations towards poverty alleviation. This project was one of ADB’s first microfinance projects, and the first such project in Indonesia. The design team drew lessons from the economic and sector work undertaken in Indonesia by World Bank and the United States Agency for International Development. At the time the Project was conceived, knowledge of microfinance was generally poor among the donor community and developing countries. ADB had no microfinance strategy, there was no Consultative Group to Assist the Poor (CGAP)4, significantly less understanding of the impacts and benefits of microfinance, and no internal consensus on how best to measure a microfinance project’s success or failure. At the time, ADB’s agricultural divisions viewed microfinance as a rural poverty intervention that must demonstrate quantifiable poverty impacts. 6. Project design assumed that lack of access to financial services by poor rural dwellers acts as a genuine constraint on real incomes and reduces employment opportunities, reasonable assumptions then and now. Key to evaluating design relevance is demonstrating the linkage between access to credit and positive impacts on real incomes and employment. This is challenging in that financial services such as loans only allow people to take advantage of economic opportunities; financial services do not create new economic opportunities or generate wealth. Also, money is fungible. SFIs have multiple sources of funding and individual borrowers and microenterprises mix funds between family and business. It is difficult to isolate economic impacts and ascribe specific benefits to funds provided through a credit line. 7. The project design was highly relevant from the point of view of outputs and relevant in terms of the goal and objectives, although the way in which these were stated was problematic. It was sensible to formulate the project as an effort to provide microloans to poor people through SFIs, with poorer clients assisted by NGO intermediaries to access credit. There was a large, unmet demand for funds from microenterprises and the rural working poor, a need for additional funding sources from the SFIs, and a willingness on the part of all participants to pay market interest rates. It was reasonable to expect that a microfinance project’s impact on incomes and employment would be positive and relevant to evaluate poverty and social impacts. However, the specific targeted amounts by which incomes were to be increased was not appropriate. In addition, the objective related to employment generation was assigned a measurable target, expressed as a specific number of person-days of work to be created. So, increased employment was expected to be an outcome of the project, but the RRP does not state explicitly that the project was expected to create positions for new wage-earning employees within MSEs, though this is a reasonable inference. Ultimately, it appears that the project did create

2 ADB. 1993. Project Preparatory Technical Assistance to the Republic of Indonesia for Microcredit Design Study.

Manila (TA 1849-INO). 3 IMPRES Desa Tertinggal (IDT) (Presidential Instruction for Backward Villages) was a $200 million concurrent

government project, implemented starting in fiscal year 1994/1995, designed to reach the 20,000 poorest rural villages. The Microcredit Project initially targeted areas not covered by IDT.

4 CGAP is an agency organized and funded by the World Bank that promotes pro-poor financial system development. ADB is a member and a senior ADB staff member sits on its board.

3

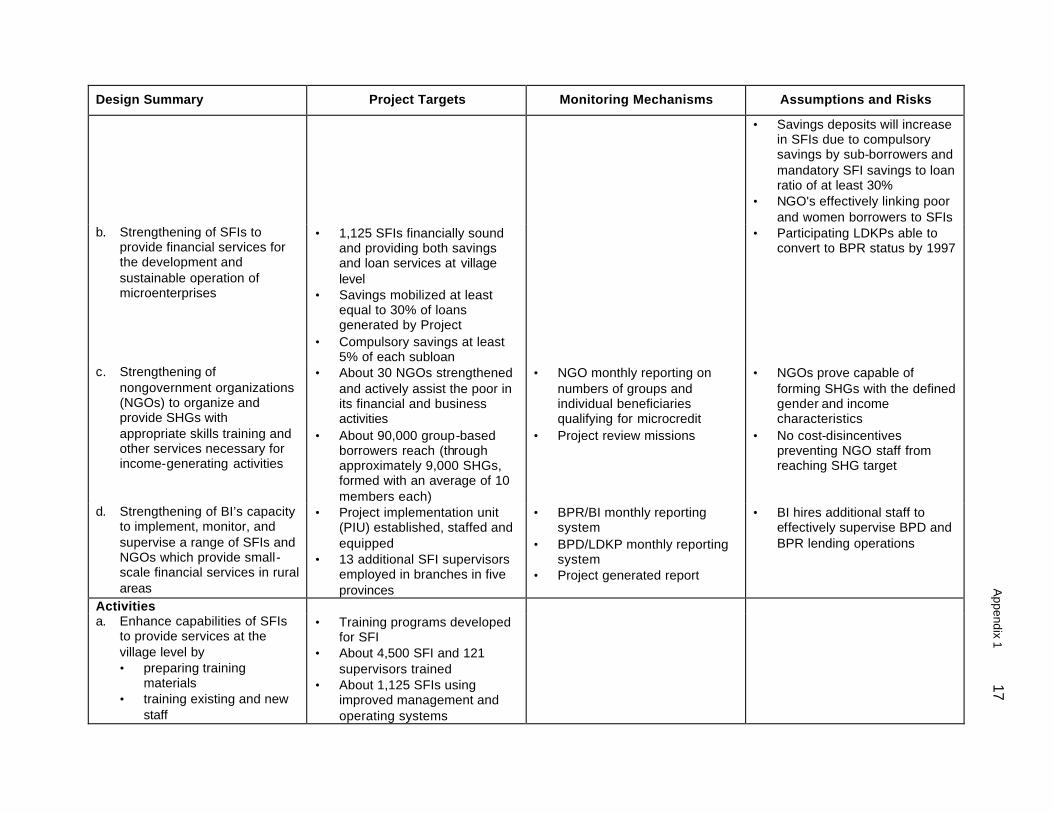

employment, but in an indirect way, as impact surveys showed that microenterprise borrowers were able to spend more time working in their businesses (measured in person days), and, in some cases, to get other family members involved in the business. 8. Another problematic feature of project design was the assumption that a standardized banking software program could be developed and shared among all participating SFIs. This proved overly ambitious because (i) different SFIs had varying product offerings and differing methods for calculating, interest rates, fees, and other items; (ii) the ability to absorb banking software varied widely among more than 1,000 SFIs; (iii) BPRs could not meet the value proposition for banking software even at very low subsidized prices; and (iv) one local information technology (IT) consultant was insufficient to create, effectively market, install, and provide ongoing service for banking software. 9. The Project was designed as a poverty intervention with implications for the financial sector. In hindsight, it might have been more appropriate to consider it a financial sector intervention with poverty impacts. The present view promoted through CGAP and embodied in ADB’s microfinance strategy is that the purpose of microfinance interventions is best defined as financial deepening, or providing greater access to financial services to poor people or those with low incomes. It is now considered axiomatic that increasing access to financial services by poor people can provide tangible economic benefits, although it is difficult to quantify precisely microfinance’s economic and social impacts on poor people. Microfinance projects should be evaluated based upon (i) expanded outreach to microenterprises, measured by activity indicators such as the number of borrowers and savers, number of women borrowers and savers, average loan size (with very low loan sizes serving as a proxy for lending to the poor), and total amount of microlending; and (ii) increased sustainability of microfinance institution (MFI), as measured by, among other indicators, the capacity of an MFI to cover operational costs (operational sustainability), cover financial costs (financial sustainability), achieve high loan recovery rates, and generate returns on assets and equity that approach those at commercial financial institutions. B. Project Outputs 10. The table below compares the original project target outputs5 with actual results. Unless otherwise indicated actual figures presented are as of 31 December 2001, just prior to project closure.

Table 1: Project Target Output6 Indicators and Actual Results

Project Targets Component (i)

Projected § 300,000 new borrowers reached § 66% of SHG members are poor § 50% of SHG members are women

Actual § 801,103 borrowers participate, of which 484,625 were new borrowers § 64% of SHG borrowers were poor or near poor § 53% of SHG borrowers were women

Component (ii) Projected § 1,125 SFIs financially sound and providing both savings and loan services at

the village level

5 Detailed reviews of outputs, outcomes, and impacts are contained in Supplementary Appendixes 1 and 2. 6 The Project Framework is presented in Appendix 1.

4

Project Targets § Savings mobilized at least equal to 30% of project loans § Compulsory savings at least 5% of each subloan

Actual § 982 (87% of target) SFIs participated in the Project, including 843 BPRs and 139 LDKPs in 15 provinces. LDKPs were not allowed to participate unless they converted to BPR by 1999. BI’s survey of financial results at 90 participating BPRs during 1998 and 1999 found: § Percentage of BPRs achieving a sound rating increases from 47% to 73%

(highest BI rating, based on CAMEL7 analysis); § Loan recovery rates improved (87.3% before, 90.7% after), and

nonperforming loans (NPL) declined from 12.7% to 9.35%; § BPRs expanded lending by more than 150% (in nominal terms); § BPRs increased the number of microenterprise borrowers served by 33.8%,

while microenterprise borrowers accounted for a larger share of BPR clients, 67%, than prior to the Project, when 53% of their borrowers were microenterprises; § 170% increase in deposits at surveyed BPRs, indicating that the target of

30% of project loans has been achieved many times over; § Number of overall borrowers increased by 9.7%; number of savings

customers rose by 23.4%; and the average savings amount rose by 75%; § BPR overall productivity and profitability increased substantially.

Component (iii) Projected § 30 NGOs strengthened to provide financial and business help to the poor

§ 90,000 group-based borrowers in 9,000 SHGs linked to BPRs and LDKPs Actual § 65 NGOs participated in the Project, 37 of which BI deemed “active” as of 30

June 2001 (still in the business of working with SHGs); § 147,020 group-based borrowers in 5,367 SHGs linked to SFIs; § BPRs/LDKPs created SHGs on their own, with 84,109 total group borrowers

as of 30 June 2001; § BI survey found that among BPRs providing funding to SHGs, only about

41% lent to SHGs formed by NGOs, while more than 75% of BPRs formed their own SHGs for lending.

Component (iv) Projected § PIU established

§ 13 additional SFI supervisors employed at BI branches Actual § PIU established four BI staff seconded to PIU; three international and six

local consultants retained § 13 project cars, 13 computers purchased for 13 BI branches; 24

nonpermanent staff and 3 consultants recruited for participating BI branches. BI = Bank Indonesia, BPR = Bank Perkreditan Rakyat (village bank), LDKP = Lembaga Dana Kredit Pedesaan (small nonbank financial institution), NGO = nongovernment organization, NPL = nonperforming loan, SFI = small financial institution, SHG = self-help group. Source: ADB. 1994. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to

Indonesia for the Microcredit Project. Manila (Loan 1327); Bank Indonesia, Final Report of the Microcredit Project, 2002.

11. The number of new borrowers reached was 162% of the targeted figure, and the number of project beneficiaries (BPR borrowers receiving funds onlent through the project credit line) was 267% of the target. The target for participating SFIs was substantially met, with the final figure for SFI participation 87% of the target. Indicators for participation by women and poor people were met or exceeded. In one exceptional case, 66% of SHG borrowers were to be classified as poor, but the final survey found that only 64% could be classified that way. This

7 CAMEL refers to a rating system for banks that evaluates and grades five factors including capital, assets,

markets, earnings, and liquidity.

5

case still represents substantial fulfillment of the initial project target. This is particularly remarkable because of the financial, economic, and political crises that rocked Indonesia from 1997 through 1999 and whose effects lasted for years. The rupiah was severely devalued, inflation spiked dramatically, and several large banks failed. 12. The Project’s institutional development outputs appear to have been achieved. It is not clear, however, if the improvement in soundness of SFIs may be attributed to project capacity-building activities or other factors. No control group of SFIs was available for comparison and only the strongest SFIs were selected to participate. SFIs were able to raise their loan interest rates substantially while increasing their deposit rates more modestly. SFIs enjoy significant pricing power in their local areas, and they were able to increase their spreads and improve their bottom lines. A significant number of NGOs participated in the Project—more than originally targeted—and a high number remain engaged with groups still. The project organized and funded a significant amount of NGO capacity building activities, yet it is difficult to ascertain to what degree the project strengthened NGOs. Many NGOs participated in another project8 that worked with groups, and thus were already engaged in the business of group formation. 13. Achievement of the targeted outputs was matched to a great degree by achievement of higher-level outcomes and impact. The following table reviews the Project’s goal and objective.

Table 2: Project Goal and Purpose

Goal Projected § 300,000 families in five provinces will see income levels increase by an

average of Rp633,000. 33% of beneficiaries are women and 33% are poor Actual § Project survey data shows that incomes in the original five provinces

increased by Rp1,824,579 per family from 1997 to 1998, but the nominal increase, 57%, was less than the inflation rate of 78% over the same period. A survey during 1998–2001 showed that incomes increased 81% in nominal terms to Rp9,047,195, greater than cumulative inflation of 21% over this 3-year period. Real incomes did rise over the period of the two surveys. § 85% of surveyed borrowers report nominal increase in money income. § Baseline survey data show 60% of individual borrowers were poor or near

poor, rising to 68% at the final survey; 70% group borrowers were poor or near poor at the baseline survey and 64% at the final survey (see Supplementary Appendix 2, p.18). § Women represented 50% of all individual borrowers, and 53% of all group

borrowers (see Supplementary Appendix 2, p. 43). Objective (Purpose)

Projected § 125 person-days of jobs created in each of 300,000 microenterprises § 156,000 full-time equivalent jobs created for subborrowers, of which 33% are

for women, and 33% are for the poor Actual § The social survey found that 47% of subborrowers increased their average

number of working days per year from an initial 178 days per year to 262 days per year. Applying this to all subborrowers (801,103) the projected figure for full-time equivalent jobs would be 184,363. If we consider only the new borrowers reached by the Project (484,625) the number of new full-time equivalent jobs created would be 111,530.

Source: ADB. 1994. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to Indonesia for the Microcredit Project. Manila (Loan 1327); Bank Indonesia, Final Report of the Microcredit Project, 2002.

8 PHBK, or “Linking Banks and Self-Help Groups Project,” begun in 1988, was supported with $9 million from GTZ,

and was completed in 1996.

6

14. The employment objective was achieved: the Project created employment equal to 110,000 to 180,000 full-time equivalent jobs (projected from survey data). These were not, however, in the form of new positions for wage employees. According to the project social survey, only 4% of subborrowers hired paid workers. Borrowing from SFIs resulted in an increase in the activity of the microenterprise owner/operator (which could be characterized as a reduction in underemployment), and, in many cases, of his or her family members. The project goal appears to have been achieved, though the employment impact is best described as indirect, rather than direct, as would be the case if new jobs were created. Beneficiaries saw an increase in real incomes, although the true picture is clouded by inflation, and, to a certain degree, currency devaluation. The nominal increase in beneficiary incomes was certainly greater than Rp633,000, which was the projected goal.9 Both goal and purpose were expressed with a specificity that was not based on empirical data. The project framework’s outcomes and impacts were relevant, but the specific numbers were not necessarily appropriate as targets for the goal and purpose. C. Project Costs

15. The Project did not experience any significant cost overruns or underruns, nor were there any major shifts between foreign and local costs. D. Disbursements

16. Disbursements were delayed by slow startup and by controversy surrounding the passage of the new Central Bank Law. The initial implementation and disbursement delays were largely related to slow recruitment of consultants. Negotiations with the consulting firm initially selected broke down before a contract was signed. The point margin separating the second- and third-ranking firms was so narrow that ADB staff recommended a re-evaluation, and the second-ranked firm ultimately selected was forced to replace its candidate for team leader well into the negotiation process (see Appendixes 3 and 4 for projected schedule vs. actual timing of project activities and consulting services inputs, respectively). The drafting of onlending agreements with SFIs took much more time than anticipated. These negotiations and arrangements were further slowed by an internal reorganization of BI. Finally, BI did not have sufficient personnel to administer the Project during the first 3.5 years of implementation. 17. For approximately 3.5 years (from loan effectiveness to midterm review mission), no ADB loan review missions were fielded. ADB and BI communicated constantly during this time, but the prolonged period without a visit from ADB headquarters undoubtedly contributed to disbursement delays. 18. The Central Bank Law, enacted 17 May 1999, prohibited BI from disbursing funds under the Project after 16 November 1999, and confusion related to the legal basis for BI continuing as Executing Agency slowed disbursement and briefly suspended consulting services. By the end of 1998, 3.5 years into a 5-year project, disbursements amounted to only 13% of the total loan. Starting in early 1999, well in advance of the November 1999 deadline, BI accelerated its

9 Attempts to measure incomes of a similar group of poor people who did not have access to finance appear to have

provided unclear results. “Nonbeneficiaries ” (poor or near-poor people in the project area that did not borrow from BPRs and did not have any contact with a local NGO) were interviewed during the baseline and midterm social surveys, but no results or analysis of their responses were presented in the report. BI staff available at the time of the PCR mission report that the results, in terms of income growth, were similar for nonbeneficiaries as for beneficiaries because nonbeneficiaries often had access to alternative sources of finance.

7

disbursements under the Project, meeting 100% of project financing needs for this period in order to meet its overall 40% counterpart funding obligation under the Project. BI made no loan disbursements after November 1999. ADB’s loan disbursements were effectively suspended during this time. The Ministry of Finance informed ADB on 8 August 2000 that the new Central Bank Law would “grandfather” BI as the Executing Agency, so there would be no disruption in management for ongoing projects even though BI would be legally blocked from disbursing its own funds in support of future projects. To overcome the initial disbursement delays, BI recommended and ADB approved the expansion of the project area (footnote 1). BI also held down the interest rate charged to SFIs, many of which were not prepared to pay the high rates that were the product of the Project’s calculations. These two decisions, combined with the mobilization of additional project personnel by BI, put disbursements back on track by 2000, ensuring a high rate of utilization for the credit line. E. Project Schedule

19. In response to the delays discussed above, the Project was extended on three occasions, which has also resulted in changes to the amortization schedule. F. Implementation Arrangements

20. Project implementation arrangements were generally appropriate, and the machinery for disbursing the credit line, delivering capacity building, and measuring project impacts and benefits proved to operate as designed. In addition to the issue of BI’s role as lender and Executing Agency, other issues arose related to implementation arrangements. 21. The minimum loan size for onlending by SFIs to microenterprises was set at an initial maximum value of Rp250,000, with the maximum (ceiling) for follow-on loans not to exceed Rp500,000. At the time of project design, the equivalent US dollar values were about $120 and $240, respectively. The Asian financial crisis and ensuing inflation meant that the initial maximum value and the ceiling value of loans for microenterprises were dramatically reduced in real terms. By mutual agreement, BI and ADB periodically adjusted upwards these amounts (see the table in Appendix 5 that traces the periodic increases in allowable loan sizes). At project completion, 31 December 2001, the initial amount was raised to Rp2,000,000 ($190), and the ceiling amount reached Rp5,000,000 ($480). 22. Substantial implementation delays resulted in much lower disbursement than projected during the initial 3.5 years of the Project. BI recommended in November 1998 that the number of provinces be increased in order to achieve full disbursement within the project timeframe. The midterm review mission fielded in December 1998 recommended and ADB approved in January of 1999 the expansion of the Project to 15 provinces. After the midterm review, BI delegated a significant amount of authority for project management to the BI branches, which were allowed, for example, to determine the amount each SFI could borrow. BI branches by early 1999 appear to have been fully staffed, and BI head office began to evaluate branches’ performance in managing the microcredit project their periodic performance reviews. These changes rapidly accelerated loan disbursements. Appendix 6 is the list of subloans. G. Conditions and Covenants

23. There were no significant delays in meeting the conditions for loan effectiveness. The covenants included in the Loan Agreement were relevant, and BI complied with almost all of them throughout the Project. The main exception concerned the interest rate for onlending to

8

SFIs. The calculation of the interest rate for onlending to SFIs became a significant issue in the wake of the Asian financial crisis, the impact of which began to be felt in Indonesia in December of 1997. From 1 July through 31 December 1998, BI did not comply with this covenant.10 ADB staff notified BI of noncompliance in early 1999 and initiated a dialogue with BI to bring them back into compliance on this issue. BI, dealing at the time with a full-blown economic crisis, saw the project interest rate—as calculated according to the Loan Agreement—spike from 11% per year to more than 30% per year. With disbursements already well behind schedule, BI feared that SFIs would not be willing to borrow at such rates in the long term (BPR deposit rates had been observed during the same to be significantly below 30%, meaning that project funds would not have been attractively priced). For 1998 and 1999, BI set the interest rate at 15% without reference to the formula in the Loan Agreement. This issue was finally resolved by the end of 1999 when market conditions allowed BI to revert to the original calculation of interest rates. ADB staff demonstrated initiative in attempting on several occasions to devise an alternative interest rate calculation, showed patience and understanding, and a reasonable level of forbearance under difficult circumstances. 24. The minor exceptions related to covenant compliance concerned the stipulation requiring compulsory savings by each subborrower of 5% of the total subloan amount. This covenant was effectively abandoned when SFIs were found subtracting the 5% compulsory savings from the initial subloan amounts. The covenant in theory would help SFIs build up savings for the benefit of both themselves and their poor borrowers, but in practice it served to increase the SFIs’ effective lending rates with no compelling economic benefit to borrowers. H. Related Technical Assistance

25. Technical assistance (TA) was built into the Project and funded under the loan. The TA provided capacity building for the SFIs and NGOs, and was divided into two packages. Under the first package, two international and six domestic consultants were involved in developing and delivering specific training modules to support project activities. The Government of Norway provided a $1 million grant for training and consulting services to the Project in 1996, which was fully disbursed by March 2002. These funds supported the second package of consulting services, which focused on NGO capacity building and benefit monitoring and evaluation. The start-up of TA efforts was substantially delayed, as mentioned above. Several individual consultants (all of the them national consultants) had their inputs extended and were paid out of cost savings. 26. The team under the first package produced training materials for SFIs, trained trainers, and developed a series of software tools for project monitoring and for SFI operations. The project completion review (PCR) mission was unable to verify whether the training materials were still in use, or if the local trainers that were qualified under the Project were still available to provide further training. The training activities were a main subject of periodic reports from consultants under this package, and loan review missions commented on these activities extensively. The PCR mission found the consultant reports to be neither incisive nor particularly well prepared; the mission memoranda reveal that ADB staff raised issues related to the relevance and quality of the training material produced, as well as the prospects for sustainability of the training efforts after the Project. Evaluating the outcome of consulting services related to training is difficult. Certainly staff were trained, but there are no participant

10 Loan Agreement, Section 1.02 (b,m, o), Article 1, for definitions of terms, and Schedule 6, paras 9–11 for

calculation of the interest rate.

9

evaluations of training exercises or detailed satisfaction surveys from SFI managers who might have been in a position to evaluate the efficacy of the training. 27. Consultants under the second package carried out most of their assigned tasks, although ADB has no record of NGO capacity-building activities. The PCR mission verified that these activities did take place, at least in places the mission visited. The measurement of outcomes for package II consultants is also difficult, as there is no record of training evaluations. I. Consultant Recruitment and Procurement

28. TA consultants were selected and contracted in accordance with ADB’s Guidelines on the Use of Consultants. Project-related procurement was carried out in accordance with ADB's Guidelines on Procurement. J. Performance of Consultants, Contractors, and Suppliers

29. BPR staff said SFI training was interesting and useful, but consultants did not require course participants to fill out post-course evaluations that might have provided more insight. Efforts to develop standardized banking software program did not fully bear fruit (some project monitoring and financial analysis packages were developed), and could not have been expected to as the design was flawed in this respect. The PCR mission concluded that the TA package for NGOs was not particularly effective, which might explain why some BI and SFI staff said they were disappointed in the work of many NGOs. Overall, the consultants’ performance is rated as less than satisfactory. 30. NGOs did not fully achieve the outputs related to group formation and linking of groups to BPRs. Specific targets here were based upon the limited experience of the PHBK project. The project offered fairly limited incentives for NGOs, and provided no compelling incentives for BPRs to work with NGOs. Incentives for NGO participation were limited mainly to local BI offices’ reimbursement of the cost of hiring new NGO staff to form SHGs. Some NGOs sought to participate solely because they could get funding for new staff, although their expertise or fundamental mission may have had little to do with group formation. Some BPRs reported bad experiences with such NGOs, and 75% of BPRs simply took on the task of group development on their own, many with good results. NGOs’ contributions were still significant, and clearly some NGOs stood out as good stewards of groups. Group formation on the one hand and acceptance of the group’s credit risk on the other hand created natural tension between NGOs and SFIs. Only in isolated cases did NGOs assume any responsibility for repaying group loans to SFIs. There were successful cases where NGOs did indeed guarantee their groups’ loan repayment to SFIs, cementing close working relationships between NGOs and SFIs. Many of these relationships continue long after project completion. The NGOs performed satisfactorily. 31. BPRs were clearly appropriate vehicles for offering microloans and providing savings and deposit services. The improvement in the soundness ratings for participating BPRs, revealed in the SFI survey above (see Table 1), demonstrates that BPRs responded positively to the Project despite difficult economic circumstances. This, in turn, provided both attractive funding and useful technical assistance. The criteria that BI developed for project participation raised expectations for BPRs’ performance: the availability of the credit line, which provided a welcomed new source of funding, provided a powerful incentive for BPRs to reach the BI-mandated CAMEL rating. This was the first time BPRs were participating in a credit line project of this type. BI was very careful about SFI selection and closely monitored SFI participants. Local BI offices also organized the training courses for the BPRs. Overall, the training program

10

may have helped to enhance the skills and professionalism of BPR staff, despite issues related to quality of some course offerings and sustainable training delivery mechanisms. The BPRs and BI forged a closer working relationship through the Project. This had a substantially positive impact on BPRs’ financial performance. SFI performance is rated highly satisfactory. K. Performance of the Borrower and the Executing Agency 32. The Borrower, the Ministry of Finance, was regularly informed of the project progress, but was not assigned and did not play an active role in the Project. None of the implementation issues required borrower intervention as BI and ADB developed a cordial working relationship despite initial delays and some disagreements. The Borrower’s performance is rated satisfactory. 33. After prolonged implementation delays, BI did finally demonstrate resolute leadership and competent project management. SFI monitoring was particularly conscientious. Reporting was initially a problem, but it became more timely and thorough after the midterm review. The social surveys were carried out carefully. BI proved proactive in identifying solutions to the disbursement challenge. Expanding the project area was pursued enthusiastically, even though it entailed a substantial increase in BI resources. When the new Central Bank Law was passed in 1999, BI had an opportunity to pass the Project off to another agency. BI insisted on remaining the Executing Agency, a clear demonstration of their dedication to the Project, which was considered successful and a source of institutional pride. BI’s appraisal as competent and capable of managing the Project was fully borne out in implementation. 34. BI has passed the project portfolio (including the credit and foreign exchange risk) to Bank Mandiri, a state-owned commercial bank that now manages the credit line’s continuing operations. BI’s role in the Project has now officially ended, and according to law, it cannot assume a similar role in future projects. This is fully consistent with international best practice, where the central bank’s role is confined to monetary policy and supervision. BI did, however, prove itself fully up to the task of managing a complex, multi-faceted project under the most difficult of economic circumstances. BI’s performance as Executing Agency was satisfactory. L. Performance of the Asian Development Bank

35. The project was very slow to start. The lack of an inception mission and the subsequent failure to field a mission at the time when the consultants were initially mobilized undoubtedly delayed the Project further. ADB staff ultimately demonstrated a high level of engagement in the Project. Project staff provided leadership in working through key issues, including the interest rate controversy, and was flexible in adapting to changing circumstances. Monitoring was adequate, although BI might have benefited from a more detailed and critical appraisal of the reporting systems and survey techniques used under the Project. Because of the failure to field missions in the crucial early period, ADB’s performance is rated less than satisfactory.

III. EVALUATION OF PERFORMANCE A. Relevance 36. The Project addressed microenterprises’ and poor rural dwellers’ large unmet demand for financial services through an appropriate set of financial intermediaries. It also built upon successful group lending methodologies pioneered in an earlier project and provided needed TA for capacity building at SFIs and NGOs. The project was consistent with government policies to

11

reduce rural poverty. Setting a specific, nominal target for an increase in incomes was not appropriate as a project goal because borrowers had differing socioeconomic characteristics and worked in various sectors. Poverty is multidimensional, so increases in nominal incomes may not reflect social impacts accurately. The numerical specificity of income impact does not seem to be based upon similar experience, research data, or other information that would indicate a specific nominal amount or percentage of increased income could be achieved through a microfinance intervention. The purpose of generating substantial amounts of new employment was also relevant, although the Project demonstrated that the employment impact is more indirect than direct, as the number of microenterprise employees did not increase substantially. Considering the soundness of the project design, and the essential relevance of poverty reduction (interpreted as increased incomes and employment), it is fair to judge the Project relevant. B. Efficacy in Achievement of Purpose

37. The achievement of the income- and employment-related goals and purposes can certainly be considered an indicator of project efficacy. Incomes did rise measurably in real terms. The purpose of generating employment appears to have been met and exceeded, though, as noted, the employment effect was more indirect than direct, and practically all project outputs were substantially exceeded. Many microenterprises and poor people had access to financial services on a sustainable basis for the first time through the Project. Participating SFIs demonstrably improved their financial performance and expanded their outreach to new smaller customers, many of them experimenting successfully with group lending. The project expanded the frontiers of microfinance at a time of unprecedented financial and economic difficulty. Impact of externalities is difficult to assess, however, and there are problems related to attribution of project benefits. The project is rated efficacious. C. Efficiency in Achievement of Outputs and Purpose

38. Fulfillment of component output indicators—particularly the targets related to expansion of outreach by SFIs—represents a signal achievement. It is difficult, however, to attribute the improvement in BPRs’ soundness ratings to project activities such as training, which did not appear to have been very high quality. BPR performance improvements likely had more to do with (i) the imperative to improve CAMEL indicators in order to tap into the credit line; (ii) strong monitoring by BI, bolstered by dedicated project staff; and (iii) the skill of SFI managers who took advantage of a rising interest rate environment. Project TA resources were not efficiently leveraged. Both BI and ADB wasted a lot of time and demonstrated an unusually high level of tolerance for inactivity. BI and ADB finally reacted with much energy and professionalism in late 1998 and salvaged the Project. In the final analysis, BI branches, the SFIs, and the NGOs deserve credit for the achievement of output indicators, and these participants’ efforts to reach targets were boosted when the project area expanded from 5 to 15 provinces. The Project was less efficient than it should have been in achieving component outputs. D. Preliminary Assessment of Sustainability

39. A commercial bank has taken over management of the credit line, a clear indication of potential sustainability. The Project also expended significant resources in helping NGOs form groups, then in linking those groups to BPRs. A significant number of NGOs are continuing these operations. Many SFIs have learned how to successfully lend to groups on their own, and all participating SFIs were challenged to serve poorer clients. The project laid the foundation for commercial banks to lend to BPRs and has clearly demonstrated the BPRs’ capacity to manage

12

borrowed funds. Many participating BPRs still lend to the same borrowers that they reached under the Project, and are expanding their lending to new microenterprises based upon positive experiences gained under the Project. Bank Mandiri only took over the credit line in 2004, and it is still early to evaluate sustainability. The Project is likely to be sustainable. E. Environmental, Sociocultural, and Other Impacts

40. There are a series of impacts worth noting, particularly institutional ones. The Project incorporated gender targets into the project framework, seeking explicitly to empower women through greater access to microloans. The Project surpassed its gender targets, namely, the percentage of women participating. The survey shows that women did benefit financially from the Project and that their incomes rose. Bank Mandiri taking over the project loan portfolio is an unexpected positive development. Essentially, the Project has created a financial product—the portfolio of BPR loans—with a positive yield and a measurable financial value. Good BI stewardship, strong incentives for improved SFI performance, and the willingness of SFIs to experiment and learn produced substantial institutional impacts (para. 31). Participating BPRs are sounder today, have access to commercial funding in amounts previously unavailable, and have larger markets. The Project had no adverse environmental impact and generated significant institutional impacts.

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS

A. Overall Assessment

41. The Project is rated successful. The project was implemented as conceived during a period of extraordinary economic difficulty, overcoming substantial delays. The project outputs were appropriate, readily measurable, and directly linked to project activities. Higher-level impacts and outcomes, as well as increased income and employment, were also achieved. 42. This is a successful project that has achieved substantial outreach to poor and near-poor borrowers, many of whom had access to bank lending for the first time. The Project has demonstrated good prospects for sustainability as SFIs continue to serve their newly acquired clients, and the project portfolio has proved attractive to a commercial financial institution. Social impact surveys show that most borrowers’ incomes improved measurably over a 5-year period. B. Lessons Learned

43. The lessons learned apply both to further operations by ADB in Indonesia and lessons that have more general applicability.

1. Lessons for Indonesia Operations

44. BPRs Can Benefit from Continued Assistance. BPRs are well suited to microfinance, and in fact meet CGAP criteria for being considered MFIs because the average loan size of most BPRs is below 150% of GNP per capita (see Appendix 5). Sound BPRs are profitable and well capitalized but have funding constraints that limit lending outreach. BPRs are confined geographically and cannot easily expand deposit-taking activities to expand loans. They cannot move up market because of competition from larger financial institutions, legal lending limits, and funding constraints. They are, however, well positioned to move down market. BPRs’ competitive advantage is in their closeness and attentiveness to their customers, who are generally individuals, microenterprises, and small businesses. BPRs, however, often lack the

13

desire or the funds to invest in computer systems and software, and they have no easy way to link with the payments system or wider payment networks. BPRs’ geographical and size limitations also have negative implications for asset/loan portfolio diversification. In some cases they are not well equipped to design new products that might facilitate moving down market to serve poorer clients with smaller loans. 45. BPRs need to develop appropriate new products, diversify and better manage asset and loan portfolio risk, and improve their information technology. Commercial banks are now clearly moving down market, and this intensified competition adds greater urgency to the need to address BPRs’ institutional weaknesses. Larger commercial banks enjoy advantages in terms of lower funding costs, operating cost structures with scale economies (notably promotional, training, research and development, and IT cost advantages), richer product offerings, and technological superiority. External interventions targeting BPRs might consider creating more formal linkages of BPRs and commercial banks—where a marketing/product channeling symbiosis is likely—and strengthening of supporting institutions that help BPRs enhance their competitiveness or reduce their risks by providing treasury management services. BPRs need external assistance to overcome their operational weaknesses and have proven that they can manage and benefit from access to additional sources of funding like commercial lines of credit. There is broad scope for follow-on programming by ADB. 46. Interventions Should Promote Commercialization of Microfinance. Commercial microfinance has arrived in Indonesia, highlighting new possibilities for private-sector operations. The project demonstrates that with the proper oversight, a portfolio of loans to BPRs—established, profitable, well-capitalized businesses—can carry low risk and earn a commercial yield. At the very least, it is possible to reduce the scope of public-sector activity in future microfinance projects/loans. Future ADB funding should further catalyze private-sector participation in microfinance, meaning that ADB funds should be leveraged with private funding.

2. General Lessons

47. Use Outreach and Institutional Sustainability as Main Indicators. Because incomes are subject to various unquantifiable externalities, success or failure of microfinance is best measured by outreach and financial sustainability. Loan size can serve as a useful proxy for depth of outreach to poor clients. It is important to gather survey data related to poverty and incomes of project participants. It is necessary to understand poverty in all its dimensions—not simply in terms of income—so well-designed social impact surveys should rightfully be incorporated into microfinance projects. Still, an increase or decrease in income by participating microenterprises should not be considered the central indicator of success of a microfinance project. There is solid evidence to suggest that a well-designed microfinance intervention will benefit those who were hitherto denied access to affordable financial services. Project frameworks should elevate sustainable financial deepening to the outcome or impact level. 48. Don’t Expect Microenterprises to Hire New Employees. Expansion of microfinance activity does not necessarily contribute to creation of new wage earning jobs. With access to loans, a microentrepreneur can spend more time developing her/his business, and perhaps support the participation of additional family members in the business. The impact of microfinance on employment is mainly indirect, therefore, and the most significant impact of microfinance can expected to be on family incomes. 49. Leave Client Se lection to the MFI. If challenged, and with access to effective technical assistance, many financial institutions can move down market and adopt new methods of

14

reaching poorer clients. The key factors were the fact that (i) the SFIs set their own interest rates to charge clients; and (ii) the Project did not limit lending to a certain sector, only a certain size. Maximum loan sizes were attractive mainly to poorer clients, and also helped serve large numbers of microenterprises run by poor and near-poor women because they matched the size of their businesses. Client selection is the MFI’s business and should not be interfered with by any project or agency. 50. Promote Diversification of Funding Sources. In most cases, SFIs were allowed to borrow no more than 5% of their overall funding (based upon discussions with BI and BPR personnel, reinforced by BI survey data). The project created no dependency on the part of SFIs; BPRs needed to continue gathering funds in the form of savings and time deposits from traditional customers. Sustainability of microfinance depends upon MFIs’ ability to attract and retain readily available commercial sources of funding. Credit line availability should be strictly limited so as not to create dependence on the part of the MFI. The success of a credit line intervention might best be measured in lending outreach to new borrowers combined with a substantial increase in the amount of local funding gathered by the MFI. 51. Expand the Frontiers of Microfinance. There is a natural limit to how far down market SFIs can go with lending without (i) increasing operating expenses to such a point that the lending business is no longer attractive, or (ii) finding insufficient demand for such small loan amounts. This level will be different for each SFI. There was friction between ADB, BI, and the SFIs during the Project over the maximum initial loan size; the Project performed a constant and difficult balancing act to push downward the frontiers of microcredit while keeping the SFIs interested in exploring those frontiers.11 Microfinance projects should determine a range for commercial microlending, challenge SFIs to move down market, provide proven new methodologies to assist SFIs to move down market, and allow SFIs some leverage to push back from the bottom end of the range to ensure commercial sustainability. The Project demonstrates that ADB can successfully expand the frontiers of microfinance. C. Recommendations

1. Project Related

52. Future Monitoring. Monitoring should take the form of quarterly project reports that include details of lending activity, and should be prepared by Bank Mandiri. ADB has developed core indicators for monitoring MFIs that include measures of outreach, efficiency, portfolio quality, profitability, and social impact. These indicators should be incorporated into Bank Mandiri’s management information systems on the ongoing credit line. BI should also use its regulatory leverage to ensure that BPRs report in a timely and proper manner to Bank Mandiri. 53. Covenants. An agreement between Bank Mandiri and the Ministry of Finance governs continued onlending and incorporates many of the covenants in the Loan Agreement. These covenants should be maintained by Bank Mandiri, particularly those related to BPR eligibility and the setting of the initial and maximum loan size. The initial and maximum allowable loan 11 For the purpose of discussion, the frontier of commercial microlending in Indonesia might be loosely defined as

somewhere between Rp1 million and Rp2 million for individual loans. These values represent the approximate average loan size of outstanding BPR project loans, and the present maximum initial project loan value, respectively. These values represented about 10% to 20% of GNP per capita. The Project demonstrated that microfinance in Indonesia can be commercially viable at loan levels dramatically below the international benchmark. If the CGAP benchmark had been available at the time of project design, would the Project have been so ambitious in pushing downward the frontiers of microlending? This example shows that future projects should be so bold.

15

size is likely to be revisited, and should be reviewed and adjusted annually by mutual agreement between the MOF, Bank Mandiri, and ADB. 54. Cataloguing Lessons. The project worked with more than 800,000 borrowers, a thousand SFIs, and dozens of NGOs, sparking a great deal of creative activity and innovation. Monitoring activity has been restricted to the quantification of project outputs and surveys of borrowers’ economic status. The PCR Mission uncovered during a short time many innovations that need to be more fully explored and understood. ADB should process an advisory technical assistance in 2005 (maximum 6 months’ duration) to identify the Project’s more promising financial innovations in group lending and new products.

2. General

55. ADB has an important institutional interest in seeing that social impact surveys are carried out consistently and rigorously. It is important to monitor the social impacts of microfinance interventions on poor people. CGAP has produced a number of publications related to measuring poverty and social impacts of microfinance, and these standard survey tools and methodologies should be applied in future ADB microfinance projects. Social impact surveys should be consistent and comparable across projects and countries. Resources to carry out these surveys need to be built into projects and funded by loans. 56. The form and content of microfinance project reporting must be mandated by ADB after close consultation with all stakeholders, in particular the Executing Agencies and implementing agencies and institutions. In this project, the Executing Agency and consultants appear to have developed the reporting formats; no project administration memorandum (PAM) was prepared, which in this case resulted in reporting of irrelevant data as well as incomplete reporting of relevant data. PAMs are both useful and necessary. PAMs related to microfinance projects should incorporate ADB's monitoring indicators for microfinance projects, which were developed and published during 2003. The use of standard indicators will allow for more consistent project evaluations and facilitate cross-project comparisons. 57. Further Action or Follow-Up. No follow up actions are needed to complete the Project. Outstanding loan balances have been cancelled and no additional assistance is required. The project performance audit report should not be prepared until after a substantial period of time has elapsed, allowing Bank Mandiri to continue its performance. We recommend that the Operations Evaluation Department wait 2–3 years before fielding a mission, at which time sustainability can be properly evaluated.

16 A

ppendix 1

PROJECT FRAMEWORK

Design Summary Project Targets Monitoring Mechanisms Assumptions and Risks

Goal Assumptions To increase incomes in rural areas, to reduce poverty, and to improve the economic opportunities for rural poor and rural women

Income level of about 300,000 families increased by an average of Rp633,000 of which at least 33% are women and 33% are poor

• Baseline and periodic follow-up social surveys

• Project review mission • Midterm review

• General economic conditions of growth continue

About 100,000 poor beneficiaries' income levels will increase by as much as 50%

• Bank Indonesia (BI) and Bank Pembangunan Daerah (BPD's) benefit monitoring and evaluation (BME) system for small financial institution (SFI) compliance with lending to poor

• Without the Project, the poor and women remain excluded from many economic opportunities

Purpose Increased employment and income-generating activities among the poor, near-poor, and women by promoting microenterprises and facilitating their sustained access to financial services

• An average of 125 person-days of jobs created in each of the 300,000 microenterprises

• About 156,000 equivalent full-time jobs created for the sub-borrowers, of which at least 33% are for women and 33% for the poor

• Baseline and periodic follow-up social survey

• Rural wages do not decline • High rate of loan recovery and

low rate of default

Outputs a. Lending to the poor and near-

poor for the development of microenterprises

• A total of about 300,000 new borrowers reached. At least 25% of the subborrower credit line provided for small, non-collateral loans to at least 100,000 poor and near-poor small borrowers

• At least two thirds of the self-help group (SHG) members are poor beneficiaries

• At least 50% of the SHG members are women

• Bank Indonesia Bank Perkreditan Rakyat (BPR) and Lembaga Dana Kredit Pedesaan (LDKP) monthly reporting system including data loan size, volume of savings, and number of customers

Risks • Credit line do not reach the

poor and women • Savings are not mobilized • Microenterprise failure and

loan default Assumptions • SFIs effectively supervised to

meet beneficiary subloan targets

Appendix 1

17

Design Summary Project Targets Monitoring Mechanisms Assumptions and Risks

• Savings deposits will increase in SFIs due to compulsory savings by sub-borrowers and mandatory SFI savings to loan ratio of at least 30%

• NGO's effectively linking poor and women borrowers to SFIs

b. Strengthening of SFIs to provide financial services for the development and sustainable operation of microenterprises

• 1,125 SFIs financially sound and providing both savings and loan services at village level

• Savings mobilized at least equal to 30% of loans generated by Project

• Compulsory savings at least 5% of each subloan

• Participating LDKPs able to convert to BPR status by 1997

c. Strengthening of nongovernment organizations (NGOs) to organize and provide SHGs with appropriate skills training and other services necessary for income-generating activities

• About 30 NGOs strengthened and actively assist the poor in its financial and business activities

• About 90,000 group-based borrowers reach (through approximately 9,000 SHGs, formed with an average of 10 members each)

• NGO monthly reporting on numbers of groups and individual beneficiaries qualifying for microcredit

• Project review missions

• NGOs prove capable of forming SHGs with the defined gender and income characteristics

• No cost-disincentives preventing NGO staff from reaching SHG target

d. Strengthening of BI’s capacity to implement, monitor, and supervise a range of SFIs and NGOs which provide small-scale financial services in rural areas

• Project implementation unit (PIU) established, staffed and equipped

• 13 additional SFI supervisors employed in branches in five provinces

• BPR/BI monthly reporting system

• BPD/LDKP monthly reporting system

• Project generated report

• BI hires additional staff to effectively supervise BPD and BPR lending operations

Activities a. Enhance capabilities of SFIs

to provide services at the village level by • preparing training

materials • training existing and new

staff

• Training programs developed for SFI

• About 4,500 SFI and 121 supervisors trained

• About 1,125 SFIs using improved management and operating systems

18

Appendix 1

Design Summary Project Targets Monitoring Mechanisms Assumptions and Risks

• improving outreach and reporting functions

• providing long-term funds to support loans to target beneficiaries

• Improved service to customer through village posts

• $30 million long-term funds provided to participating SFIs for onlending to target beneficiaries

• Training program developed for NGO staff

• 135 field staff trained and employed by NGOs

b. Enhance the capabilities of NGOs to assist SHGs to access financial services by • preparing training

materials • training existing and new

staff • assisting SHG member

microenterprises in formulating business plans

• NGOs with computerized systems and motorcycles

• Special project reports • Project BME Baseline Survey,

Impact Assessment, and Special Reports

• Core NGO staff sustainable/ low turnover of personnel

• NGOs prepared to employ and manage much larger number of field staff

• Willingness and ability of regional NGOs to hold sufficient courses

• BI improves reporting mechanisms with BPDs for LDKP supervision

c. Establish monitoring and evaluation systems including BME, baseline survey, midterm review, impact assessment, and special studies.

Inputs Resources by component total project cost ($ million) • microenterprises 30.0 • SFIs 4.2 • NGOs/SHGs 2.8 • supervision/monitoring 4.9 • others 0.6

Total 42.5

BI = Bank Indonesia, BME = benefit and monitoring evaluation, BPD = Bank Pembangunan Daerah (regional development bank), BPR = Bank Perkreditan Rakyat (village bank), LDKP = Lembaga Dana Kredit Pedesaan (small nonblank financial institution), NGO = nongovernment organization, PIU = project implementation unit, SFI = small financial institution, SHG = self-help group.

Append

ix 2 19

PROJECT POVERTY INDICATORS

Official Poverty Line2

Urban Rural Social Survey

"Working Poor"

Poverty Line1

CPI (1996=100)

Real Annual Income, Working

Exchange Rate: Rp/$

at Year End

Value of Nominal Poverty

Line ($)

Rp $ Rp $

Baseline: 1997 2,714,760 112 2,428,446 4,650 584 504,384 108 376,392 81

Midterm: 1998 5,495,460 198 2,768,912 8,025 685 1,163,508 145 873,360 109 Final Survey: 2001 6,600,000 249 2,649,007 10,400 635 1,200,132 115 964,584 93 1 Amount represents nominal annual income of "working poor" hous ehold as defined by the Bank Indonesia (BI) social survey. 2 Official Government poverty line as per Biro Pusat Statistik (BPS); figures for annual income per capita. Source: Bank Indonesia.

A. Sustainable SFIs1 Identify SFIs and Disburse Credit Funds:

a) Mobilize Project ConsultantsProjectedActual

b) Determine Participating SFIs Based on CriteriaProjectedActual

c) Discuss SFIs for Participation with BI OfficersProjected `Actual

* d) Promote Projects to BPDs and Potential SFIs; Solicit SFI ApplicationsProjectedActual

* e) Review BPR applications for Funds; Perform Due Diligence ReviewProjectedActual

* f) Review BPD/LDKP Applications for Funds; Perform ReviewProjectedActual

* g) Disburse Loans to SFIsProjectedActual

2 Prepare SFI Training Materials:a) Review Existing Materials and Practices

ProjectedActual

b) Formulate Curricula, Obtain ApprovalProjectedActual

c) Write MaterialsProjectedActual

d) Produce and Test New MaterialsProjectedActual

e) Edit and Publish New MaterialsProjectedActual

* f) Review and Revise Training MaterialsProjectedActual

3 Train SFI Staff:* a) Train BPD & SFI Managers and Supervisors

ProjectedActual

* b) Train SFI StaffProjectedActual

4 Computerize SFI Activities:a) Mobilize Consultants

ProjectedActual

b) Review Existing SystemsProjectedActual

c) Write SoftwareProjectedActual

* d) Test Software in Field LocationsProjectedActual

* e) Revise Computer SoftwareProjectedActual

* f) Train Software UsersProjectedActual

20A

ppendix 3Components / Activities

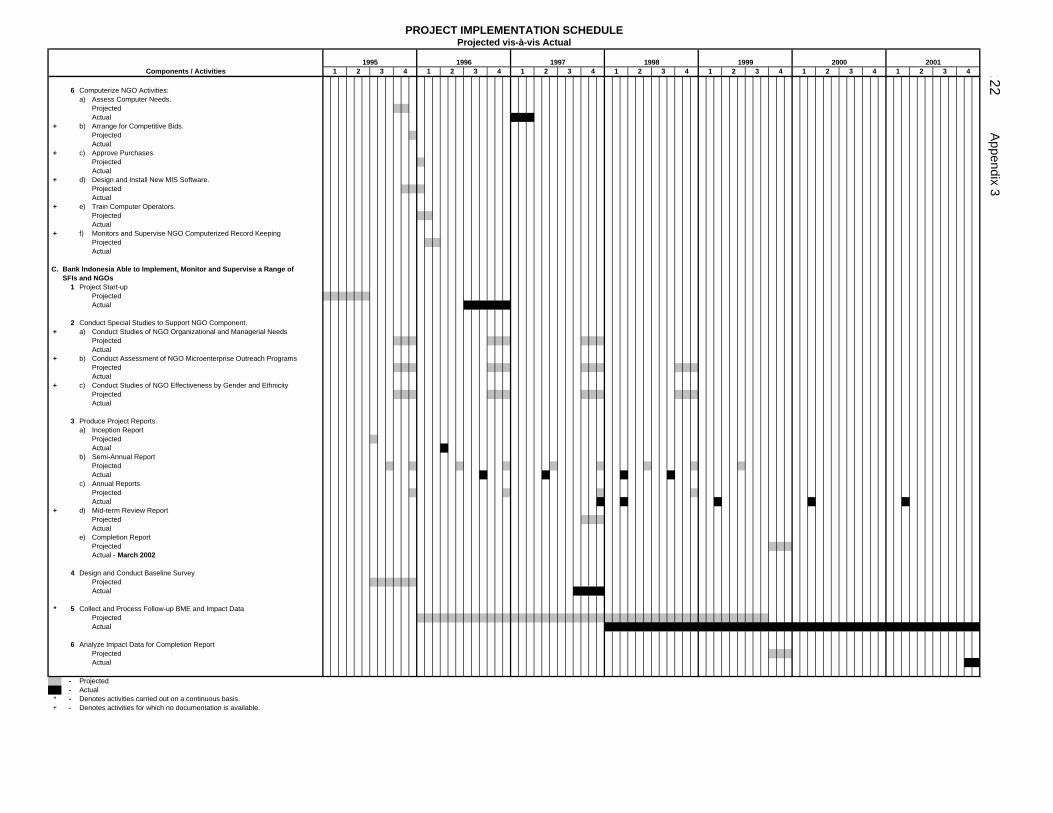

PROJECT IMPLEMENTATION SCHEDULEProjected vis-à-vis Actual

20011 2 3 4

20001 2 3 4

19991 2 3 4

19981 2 3 4

19971 2 3 4

1995 19961 2 3 41 2 3 4

20Components / Activities

PROJECT IMPLEMENTATION SCHEDULEProjected vis-à-vis Actual

20011 2 3 4

20001 2 3 4

19991 2 3 4

19981 2 3 4

19971 2 3 4

1995 19961 2 3 41 2 3 4

5 Provide Vehicles for Bank Supervisors, Banking Staff:a) Determine Needs

ProjectedActual

b) Call for TendersProjectedActual

c) Procure and Deliver VehiclesProjectedActual

6 Provide Loans for NGO Working Capital and Field Workers Vehicles:a) Arrange Loan Program

ProjectedActual

* b) Process and Disburse LoansProjectedActual

B. NGOs Able to Organize and Provide SHGs with Appropriate Skills Trainingand Other Services Necessary for Income-Generating Activities.

1 Mobilize LT ConsultantsProjectedActual

2 Promote Project to NGOsProjectedActual

3 Recruit New NGO Field StaffProjectedActual

4 Prepare Training Materialsa) Conduct training Needs Assessment

ProjectedActual

b) Review Existing PHBK and P4K MaterialsProjectedActual

c) Design Improved MaterialsProjectedActual

d) Produce and Test New MaterialsProjectedActual

e) Edit and Publish New MaterialsProjectedActual

f) Review Project Training Program and Revise MaterialsProjectedActual

5 Train Existing and New NGO Staffa) Train NGO Staff Trainers

Projected Actual

b) Train New Field Staff (3 locations)Projected Actual

21A

ppendix 3

20Components / Activities

PROJECT IMPLEMENTATION SCHEDULEProjected vis-à-vis Actual

20011 2 3 4

20001 2 3 4

19991 2 3 4

19981 2 3 4

19971 2 3 4

1995 19961 2 3 41 2 3 4

6 Computerize NGO Activities:a) Assess Computer Needs.

ProjectedActual

+ b) Arrange for Competitive Bids.ProjectedActual

+ c) Approve Purchases.ProjectedActual

+ d) Design and Install New MIS Software.ProjectedActual

+ e) Train Computer Operators.ProjectedActual

+ f) Monitors and Supervise NGO Computerized Record KeepingProjectedActual

C. Bank Indonesia Able to Implement, Monitor and Supervise a Range ofSFIs and NGOs

1 Project Start-upProjectedActual

2 Conduct Special Studies to Support NGO Component.+ a) Conduct Studies of NGO Organizational and Managerial Needs

ProjectedActual

+ b) Conduct Assessment of NGO Microenterprise Outreach ProgramsProjectedActual

+ c) Conduct Studies of NGO Effectiveness by Gender and EthnicityProjectedActual

3 Produce Project Reports.a) Inception Report

ProjectedActual

b) Semi-Annual ReportProjectedActual

c) Annual ReportsProjectedActual

+ d) Mid-term Review ReportProjectedActual

e) Completion ReportProjectedActual - March 2002

4 Design and Conduct Baseline SurveyProjectedActual

* 5 Collect and Process Follow-up BME and Impact DataProjectedActual

6 Analyze Impact Data for Completion ReportProjectedActual

- Projected- Actual

* - Denotes activities carried out on a continuous basis.+ - Denotes activities for which no documentation is available.

Appendix 3

22

No. ofPerson-Months

A. Financial and Credit Aspects1 Foreign

a) Rural Banking Specialist (Team Leader) 48 ProjectedActual

b) SFI Training Specialist 9 ProjectedActual

2 Domestica) SFI Mngmt and Supervision Specialist 24

ProjectedActual (extended 24 months)

b) SFI Computer Specialist 24 ProjectedActual (extended 24 months)

c) SFI Curriculum and Training Specialist 12 ProjectedActual

d) Loan Management Materials Specialist 2 ProjectedActual

e) Funds Management Materials Specialist 3 ProjectedActual

f) Bookkeeping Materials Specialist 4 ProjectedActual

B. Social and BME Aspects1 Foreign

a) BME Specialist 6 ProjectedActual

2 Domestica) BME Specialist 19

ProjectedActual

b) Social Survey Specialist 6 ProjectedActual

c) WID/Gender Specialist 4 ProjectedActual

d) NGO Mngmnt and Training Specialist 24 ProjectedActual

e) Microenterprise Development Specialist 12 ProjectedActual

- Projected- Actual- Extended

Consultant

CONSULTANT STAFFING SCHEDULEProjected vis-à-vis Actual

20011 2 3 4

20001 2 3 4

19991 2 3 4

19981 2 3 43 4

19971 2 3 4

Appendix 4

23

1995 19961 2 3 41 2

24 A

ppendix 5

PROJECT LOAN SIZES IN PERSPECTIVE Project Loan Size in Perspective 1996 1997 1998 1999 2000 2001

Initial Maximum Loan Amount 1 250,000 500,000 1,000,000 1,000,000 1,000,000 2,000,000

Maximum Loan Amount 2,000,000 2,000,000 2,000,000 2,000,000 2,000,000 5,000,000

Average Project Loan Amount 326,000 372,000 369,000 525,000 438,000 1,151,000

GNP per Capita 2,633,523 3,049,187 4,492,385 5,008,936 5,780,405 6,859,207

150% of GNP per Capita 2 3,950,285 4,573,781 6,738,578 7,513,404 8,670,608 10,288,811

Rupiah/$ Exchange Rate 2,383 4,650 8,025 7,100 9,595 10,400

GNP per Capita ($) 1,105 656 560 705 602 600

As a Percentage of GNP per Capita

Initial Maximum Loan Amount (%) 9 16 22 20 17 29

Maximum Loan Amount (%) 76 66 45 40 35 73

Average Project Loan Amount (%) 12 12 8 10 8 17

1 For initial year, Bank Indonesia (BI) allowed the initial maximum value of loans made under the Project to be Rp500,000 by year-end. 2 Consultative Group to Assist the Poorest (CGAP) benchmark for microlending. Loans below this amount can be considered microloans. Source: Bank Indonesia.

Appendix 6 25

LIST OF SUBLOANS

Disbursement Subloan AmountSubloan Authorization Amount Disbursed Equivalent

No. Sub-Borrower Date (SDR) (SDR)

001 Urusan Credit - BI 1 Sep 97 145,409 145,409 219,032

002 Urusan Credit - Jakarta 29 Jun 98 117,421 117,421 176,874

003 Various 10 Sep 98 264,107 264,107 354,490

004 Various 5 Oct 98 458,702 458,702 629,027

005 Various 8 Apr 99 2,325,896 2,325,896 3,162,224

006 Various 9 Aug 01 4,567,177 4,567,177 5,877,135

007 Various 21 May 02 1,544,389 1,544,389 1,950,973

008 Bank Indonesia 1 Apr 02 857,832 857,832 1,104,100

009 Bank Indonesia 25 Apr 02 3,259,109 3,259,109 4,191,347

Total 13,540,043 13,540,043 17,665,201 BI = Bank Indonesia, SDR = special drawing rights.Source: Bank Indonesia.