metro altanta transit project delivery and cost … m... · metro atlanta transit project delivery...

TRANSCRIPT

Metro Atlanta Transit

Project Delivery Assessment and Cost Estimate Review

George M. Hitchcock III, PE, PMP, DBIA

Hatch Mott MacDonald

Atlanta, GA

ABSTRACT

Major public transit projects, including heavy rail,

light rail, bus rapid transit, and commuter rail represent a

significant capital investment by Federal, State, and local

governments. Major public transit projects have been

delivered late and over budget. Determining a project’s

ability to meet both schedule and budget is therefore a

difficult and important task. The development and/or

evaluation of project schedules, risk assessments, and cost

estimates during the concept/feasibility stage and the

inclusion of sufficient contingency remains critical to

establishing and maintaining the public’s trust. The first

questions that sponsors must answer are invariably how

much will the project cost and when will it be completed?

Introduction

The State of Georgia’s Transportation Investment

Act of 2010 (TIA) is used to refer to H.B. 277, legislation

which establishes a transportation sales tax referendum for

each of the twelve regions of the State of Georgia to be held

in the summer of 2012. The length of the sales tax

collection and distribution for each region, if approved,

will be 10 years.

A list of financially unconstrained projects was to

be developed for each region by Georgia Department of

Transportation’s (GDOT) Director of Planning. From that

list, elected officials from the region were to select the

projects to be placed on the financially constrained list for

voter consideration at the summer 2012 ballot referendum.

All the projects on the financially constrained list should

be constructible within the 10-year period of the sales tax.

The Georgia Regional Transportation Authority (GRTA)

and Atlanta Regional Commission (ARC) were tasked with

performing a delivery assessment, cost review, and

performance evaluation of the proposed transit projects

within the metropolitan Atlanta region.

The TIA allowed for funding of transit capital

projects and up to 20 years operating funds for those

projects, as prescribed by H.B. 277:

Any portion of a region’s revenues may be used

for transit capital and maintenance & operations (M&O)

(except for MARTA which may only pay for M&O of new

capital outlays made after January 1, 2011). Revenues may

be used to fund a 20-year reserve for a region’s transit

maintenance & operations.

With the significant growth in the Atlanta metro

region and the on-going congestion on the freeways,

transportation alternatives that can bypass that automobile

congestion, such as rail transit projects, are very appealing

to the region. Since very few new major capital transit

projects have been built in the past decade within the

Atlanta region, there is considerable interest by many

transit agencies in obtaining funding for new transit

projects and extensions of existing transit facilities.

There is also interest in getting funds to improve

existing transit systems and perform deferred maintenance

projects, known as State-of-Good-Repair projects. H.B.

277 allows for the funds raised through the sales tax to also

be used for M&O funds, which is a benefit to many transit

agencies suffering from the prolonged effects of the

difficult economic conditions since 2008 recession.

GRTA’s Role

TIA assigned GRTA the role of ensuring delivery of

public transit projects for the Atlanta region (on time and

on budget). As the list was developed by the GDOT

Director of Planning and the locally elected officials,

GRTA supported the effort by analyzing rail-transit capital

projects submitted within the Atlanta region for project

delivery during the ten-year time frame of TIA. The

Delivery Evaluation consisted primarily of an analysis of

schedule risk elements and the review/development of

sponsor’s project schedule.

Overview

The study was initially scoped as a deliverability

screening and assessment of the non-roadway projects for

the Atlanta region from the unconstrained list developed by

GDOT for the August 2012 TIA ballot measure.

Therefore, the first part of the study was termed the Project

Delivery Assessment. Midway through the study, the need

to review and validate the project sponsors capital and

operating costs estimates was added. This information,

along with other performance criteria data supplied by

ARC, was prepared to assist decision makers in

determining the project for the fiscally constrained list.

The evaluation began in March 2011 and was completed

by June 2011.

APTA 2014 Rail Conference

Metro Atlanta Transit

Project Delivery Assessment and Cost Estimate Review 2

GDOT received 62 funding requests for non-

roadway improvements from nine project sponsors. Table

1 provides a summary of the applications by mode.

PROJECT DELIVERY ASSESSMENT

The goal of the deliverability analysis was to help

provide a realistic expectation of the schedule for each

major capital public transit project and to assess potential

delays (risk) in order to ensure on–time delivery of the

selected projects within a ten year period, which includes

beginning of revenue service and operations. This portion

of the study focused on nineteen applications which

represented fifteen major capital rail projects, illustrated in

Figure 1, as all other public transit capital projects

submitted were expected to be completed within the 10

year period.

Process

During the scoping phase, GRTA determined that a

transparent process was needed that included significant

sponsor engagement to avoid public disagreements

regarding the assessments. A detailed process flowchart

and schedule was developed and shared with the sponsors.

Significant sponsor engagement was established in three

main phases: data collection, methodology /analysis, and

results.

The process started with a one-day Risk

Workshop where a group of national and local

professionals that comprised the project team, along with

GRTA, met to develop a risk worksheet and draft

methodology. Project sponsors were then requested to

prepare a presentation and to participate in an interview

where the project team had the opportunity to discuss the

sponsor’s projects. A draft methodology was distributed to

the project sponsors, prior to the presentation/interview.

After the sponsor’s presentation and receipt of comments

from both GRTA and the sponsors, the methodology was

completed. The project team then performed a draft risk

assessment of the 15 major capital projects. After the first

evaluation, the project team developed a list of clarification

questions for the sponsors and held a follow-up meeting

with each of the sponsors prior to developing the final risk

assessment. Parallel to this process was the development

of program schedules. The draft results of the risk

assessment and program schedules were presented

individually to each of the sponsors, and finalized prior to

the public presentation of final draft results to the Regional

Roundtable. Feedback was received from the project

sponsors and various outside stakeholders and incorporated

into the final results.

Risk Analysis

The project team and GRTA identified a

comprehensive list of evaluation criteria that were

incorporated into the draft methodology that was then

shared with project sponsors. The risk assessment

methodology used a typical risk matrix with both

likelihood and severity indices, as shown in Figure 2. The

final Risk Rating categories utilized the identical five tier

scale that FTA used for overall project ratings under

SAFETEA-LU for New Starts or Small Starts projects.

The risk assessment was performed

independently by five project team members whose draft

assessments were aggregated and evaluated to identify

major differences between evaluators. These areas of

discrepancy were discussed among the members, and then

a final evaluation was completed. The individual risk

criteria scores were categorized into one of six major

categories based upon the major phases:

Procurement | Agreements

Planning | Environmental

Engineering & Architectural Design

Right-of-Way Acquisition

Construction

Commissioning & Testing

Table 1. Transit Applications

Figure 1. Major Capital Projects Map

APTA 2014 Rail Conference

Metro Atlanta Transit

Project Delivery Assessment and Cost Estimate Review 3

An unweighted final composite risk score was

derived for each project and formed the basis for the

development of recommendations.

Program Schedule

CPM schedules were independently developed

for each project using Microsoft Project and utilized the

same major phases identified for the Risk Analysis. The

project procurement method was assumed to be Design-

Bid-Build to capture the longest anticipated delivery time

and the schedule risk assessment was performed using the

Program Evaluation and Review Technique (PERT)

Analysis

PERT Analysis

A sample of the PERT analysis is shown in Table

2. This illustrates the various task durations and the

derivation of standard deviation (Sigma) and calculation of

the project variance (Sigma times Confidence value). The

project variance is a schedule contingency to account for

variation in the durations of each task.

The final completion date was established by adding an

identified task identified and associated “Project Variance”

to the schedule. The duration of the individual tasks were

based upon the variability of the overall schedule using a

95% confidence interval. The Microsoft Project® (MSP)

input form for the calculation of the task duration utilizing

the PERT methodology was used. Table 3 and Figure 3

present the input table for the calculation of the task

duration, and the Gantt chart view of the resulting

schedule. Without the project variance task, the program

finish date would be December 2017. However, the

addition of the project variance task (8.8 months)

established an expected finish date of September 2018.

Monte Carlo Analysis

A subsequent Monte Carlo modeling was

performed for each project schedule utilizing Microsoft

Project and @Risk® software. The Monte Carlo modeling

was done to create a comparison baseline to confirm the

validity of the PERT models. The project completion

(finish) date results are displayed graphically in Figure 4 in

the form of a Histogram, S-curve and Tornado Diagram.

Figure 2. Risk Matrix

Table 2. PERT Worksheet

Table 3. MSP PERT Tool

Figure 3. MSP Schedule

Figure 4. Monte Carlo Output

APTA 2014 Rail Conference

Metro Atlanta Transit

Project Delivery Assessment and Cost Estimate Review 4

Schedule Duration Comparison

A comparison of the results of the PERT Analysis

and Monte Carlo simulation model indicate that the

duration of total project varied by less than 4% overall,

inclusive of the project variance task. Table 4 summarizes

the results for the above project finish dates and duration

by model.

Results

Each project was assigned a Project Delivery

Score. The Project Delivery Score was defined as the

product of the Risk Score and the remaining project

duration in years. The remaining project duration was

derived by subtracting the completion date based upon the

PERT analysis from the January 1, 2013 anticipated start

of the sales tax collection. The results of the analysis were

sorted based on the Project Delivery Score and presented

as shown in Figure 5. The figure included the key metrics

for Delivery, Schedule and Risk. A risk rating along with

the presence of a default risk was also provided.

Additionally a new term was identified, the Default Risk.

The Default Risk was added to account for risks that had

the potential being a fatal flaw or an unrecoverable risk that

would lead to project failure.

Table 4. Finish Date Comparison

Figure 5. Project Delivery Results

APTA 2014 Rail Conference

Metro Atlanta Transit

Project Delivery Assessment and Cost Estimate Review 5

COST ESTIMATE REVIEW

During the Program Delivery Assessment, it was

determined that the project sponsor cost information

provide in their applications did not provide sufficient

information for evaluation. GRTA initiated the Cost

Estimate Review phase in mid-May 2011 and was

completed by the end of July 2011.

The purpose of this study was to perform a review

the capital and operations cost estimates for transit projects

from the Atlanta region on the unconstrained projects’ list.

The primary goal of the assessment was to

evaluate the sponsor’s cost estimate to verify the

reasonableness of their budget requests utilizing following

three principals:

Completeness – estimate included a complete

scope of work.

Reasonableness – estimate fairly represented

reasonable costs.

Consistent – estimate utilized appropriate soft

cost factors.

Process

The process of evaluating the project sponsor cost

estimate began with a review of the documentation

provided during the Project Delivery Assessment. Noting

that there was not a consistent approach and/or format for

the estimates, the project team developed a set of cost

estimating guidelines for capital and operating costs based

on the FTA’s SCC methodology. The project team

prepared a capital and operating cost methodology. The

methodology addressed the development of capital cost

and operating cost models by mode (commuter rail, heavy

rail, light rail/streetcar, bus rapid transit). The

methodology included information from FTA’s Capital

Cost Database and National Transit Database (NTD)

information. The methodology and the FTA’s SCC for

capital projects workbook was provided to the sponsors so

that each sponsor could submit a standardized cost

proposal.

Concurrent with the sponsor’s estimating process;

the project team began an independent cost estimate for

each project.

Upon receipt of the project sponsors revised

estimates; the project team performed an evaluation of the

submittal to determine the completeness of the sponsor’s

estimate. A comparison was done between the project

sponsors’ estimates and the project team’s independent

estimates. This information was shared with each project

sponsor and meetings were held with each project sponsor

to reconcile and differences, either in unit costs and/or

scope. While there were differences between the estimates,

GRTA and the project sponsors were able to achieve

consensus on a single estimate of maximum probable cost

for utilization by the Regional Roundtable to develop the

fiscally constrained project list.

FTA SCC Unit Cost Development

The Capital Costs used in the independent

estimates were developed in the FTA SCC format using the

SCC 2010 Database. Similarly, the Operating costs were

based upon the 2009 NTD data. The analysis presented

here focuses solely on the capital cost analysis.

FTA SCC Database Unit Costs

Utilization of the FTA SCC database required the

application of engineering judgment and the use of other

data sources to validate the applicable unit cost. While the

database is based on as-built verified costs, the difference

between some of unit costs can be significant and not every

project includes all the various cost categories. The project

team analyzed each cost item in the SCC prior to

incorporating the average cost into the independent

estimates. The analysis indicated that the use of the raw

unfiltered averages caused erroneous estimates.

For some items the range (span) of values

reported was greater than the average cost, and the

associated standard deviation was often greater than the

average. The project team adjusted the data for each item.

Some data was culled based upon knowledge of specific

projects where items may have been reported in unusual

categories (parking decks reported as parking lots as an

example). Other items were adjusted by culling the

furthest outliers (both high and low) until the median an

average costs were within on standard deviation. Table 5

provide representative examples for some of the raw

database cost statistics and illustrate the variability of LRT

cost data. Similar issues existed with the HRT cost data,

and the process was repeated with the HRT data.

Final FTA SCC Unit Costs

After a thorough review and refinement of the raw

FTA SCC cost database values, a final unit cost table was

develop for both HRT and LRT. Table 6 provides the final

Table 5. SCC Unit Cost Variation

APTA 2014 Rail Conference

Metro Atlanta Transit

Project Delivery Assessment and Cost Estimate Review 6

unit costs that formed the basis of the development of cost

estimates for the 15 major capital projects.

Capital Cost Estimates

With a scrubbed SCC unit cost table for each

mode, the project team began review and evaluation of the

project sponsors cost estimates and the development of an

independent cost estimate. The process involved three

basic phases, the harmonization of sponsor data, the

computation of analogous system cost, and the independent

scope verification and estimate of maximum probable cost.

Harmonization of Sponsor Data

The project team requested that sponsors submit

their cost estimates in the FTA SCC format, but few of the

projects were submitted as requested. This required that

the project team harmonize the data to match the SCC

format based upon database average line item formats. The

process consisted to two steps, the first was the direct

conversion of line times, and the second was the expansion

of line items to match the SCC format. This process was

cost neutral, because the total sponsor’s cost remained

unchanged. An example of this expansion would be in

station costs. Sponsor’s typically had a single value for a

station, while section 20 has several line items. The station

cost broken down into the various subcategories using the

FTA SCC database average unit costs to determine the

distribution, and theoretical quantities were developed.

Additionally, none of the project sponsors included the

required 1% of construction cost for Arts in Transit.

Typical missing quantities were computed for obvious

missing items such as track without any costs for

guideway. Thirty percent contingency on construction cost

was added at the phase.

SCC Line Item Comparison of Analogous Systems

The project team took the harmonized data

(quantities) and applied the FTA SCC cost data to develop

a theoretical comparison cost between the sponsor’s

submission and a hypothetical “average” FTA project.

Also, quantities were added were missing. Table 7 is a

partial example of this analysis.

Independent Cost Estimate

The project team did independent scope

verification on each sponsor’s estimate. The team

developed/verified the quantity takeoff from the plans and

concepts documents submitted by the project sponsors.

These plans and documents varied considerably. The first

activity was a review of the project scope and verification

of the team’s data with the project sponsors. Project

sponsors were provide the above information regarding

their individual projects and given the opportunity to

provide additional information and/or clarifications.

Contingency Analysis

During the development of the capital cost

estimates, the subject of contingency was examined.

Project sponsors cost estimates included a range of

contingencies, both allocated and unallocated, in Table 8.

Statistic Allocated Unallocated Total

Minimum 0.0% 0.0% 16.1%

Average 15.1% 9.3% 24.4%

Maximum 20.0% 16.1% 30.7%

Table 8. Sponsor Contingency

Table 6. GRTA Unit Costs

Table 7. Analogous Costs

APTA 2014 Rail Conference

Metro Atlanta Transit

Project Delivery Assessment and Cost Estimate Review 7

All of the projects are in the early stages of project

development and to effectively evaluate projects, it was

necessary to establish a uniform approach to contingency.

During the project review process, the projects sponsor and

GRTA agreed to 30% unallocated contingency on SCC 10-

50 costs.

During a Regional Roundtable meeting, the

representative responsible for the selection of the fiscally

constrained project list were exploring the distribution of

region sales tax revenue between transit and highway,

observed that approximately $3 billion dollars would be

allocated to transit, and of that 30% or $1 billion dollars

would be allocated to project contingency. ARC, GRTA

and GDOT were asked to review the policy of contingency

and provide additional information and justification of that

value. As part of the additional analysis, both a statistical

analysis and a Monte Carlo simulation model was

developed utilizing the unit costs and standard deviation to

calculate the contingency. The result of the statistical

analysis was a range of contingencies based on project and

mode. The cost weighted average for all projects is 31.5%

while HRT was 35.4% and LRT was 28.6%. Finally, Table

9 provides an example of the statistical contingency cost

worksheet used to calculate the actual contingency % using

the standard deviation (σ) developed in the LRT SCC Unit

Cost analysis.

Statistical Unallocated Contingency

Rail Mode HRT LRT

Minimum 32.4% 24.3%

Median 35.5% 28.8%

Average 37.6% 29.0%

Maximum 45.8% 33.2%

Table 9. Unallocated Contingency

Monte Carlo Simulations

There were significant discussions regarding

contingency due to the magnitude of the dollars identified

as contingency, and the desire to develop as many projects

as fiscally possible. The project team used the results of

the independent costs estimates and performed a statistical

analysis and Monte Carlo model to establish a confidence

in the overall results. Figure 6 is a graphic example of the

results including a Histogram, S-Curve and Tornado

Diagram. Table 10 presents the results in a tabular format,

while Table 11 illustrates the actual @Risk model

worksheet.

A comparison of the results between the various

methodologies resulted in an insignificant variation

between the various methods, and confirmed the utilization

of 30% contingency for all capital projects. The various

results for the above example project are summarized in

Table 12.

Project 10: LRT NE I-85

Total Project Cost | Model Type Total Capital

Cost

Total Project Cost | 30% Contingency $1,227,865,079

Total Project Cost | Statistical Analysis 95% CL $1,220,300,389

Total Project Cost | Monte Carlo Model 85% $1,216,748,139

Table 12. Contingency by Model

Figure 6. Monte Carlo Output

Table 10. Tabular Results

Table 11. @Risk Model

APTA 2014 Rail Conference

Metro Atlanta Transit

Project Delivery Assessment and Cost Estimate Review 8

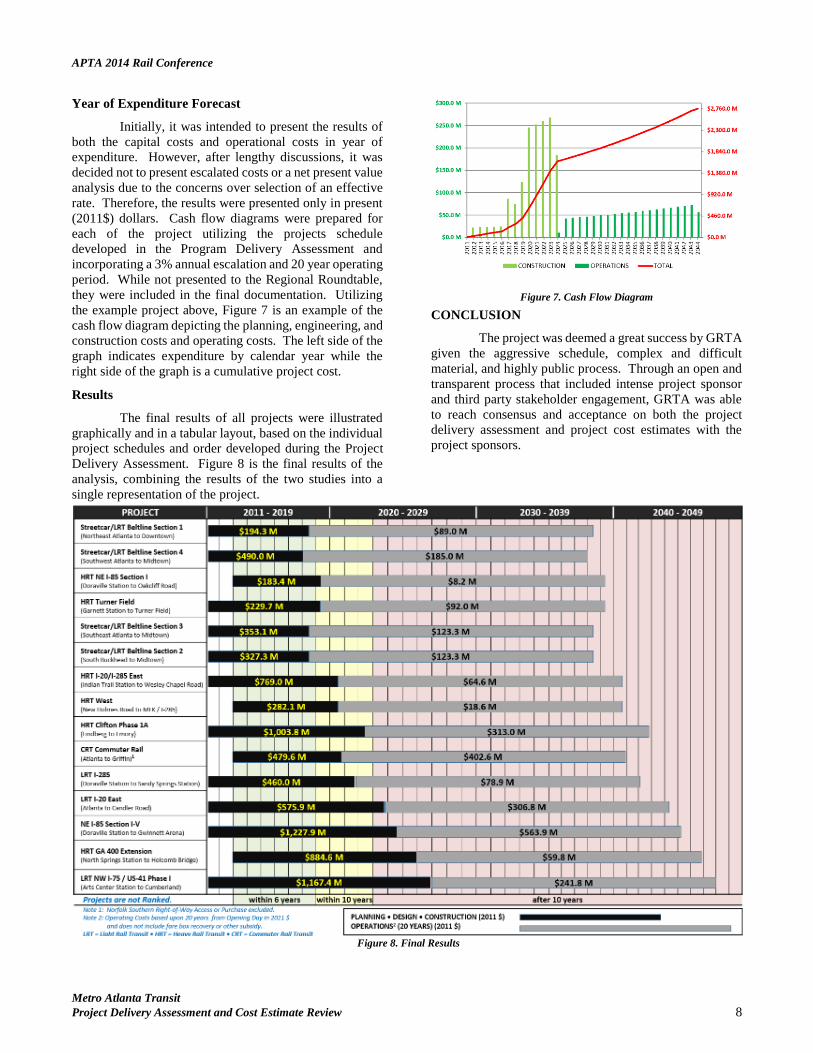

Year of Expenditure Forecast

Initially, it was intended to present the results of

both the capital costs and operational costs in year of

expenditure. However, after lengthy discussions, it was

decided not to present escalated costs or a net present value

analysis due to the concerns over selection of an effective

rate. Therefore, the results were presented only in present

(2011$) dollars. Cash flow diagrams were prepared for

each of the project utilizing the projects schedule

developed in the Program Delivery Assessment and

incorporating a 3% annual escalation and 20 year operating

period. While not presented to the Regional Roundtable,

they were included in the final documentation. Utilizing

the example project above, Figure 7 is an example of the

cash flow diagram depicting the planning, engineering, and

construction costs and operating costs. The left side of the

graph indicates expenditure by calendar year while the

right side of the graph is a cumulative project cost.

Results

The final results of all projects were illustrated

graphically and in a tabular layout, based on the individual

project schedules and order developed during the Project

Delivery Assessment. Figure 8 is the final results of the

analysis, combining the results of the two studies into a

single representation of the project.

CONCLUSION

The project was deemed a great success by GRTA

given the aggressive schedule, complex and difficult

material, and highly public process. Through an open and

transparent process that included intense project sponsor

and third party stakeholder engagement, GRTA was able

to reach consensus and acceptance on both the project

delivery assessment and project cost estimates with the

project sponsors.

Figure 7. Cash Flow Diagram

Figure 8. Final Results