medical devices market overview and degree 36 first impression

TRANSCRIPT

Build · Compete · Grow

MEDICAL DEVICES MARKET OVERVIEW AND DECREE 36 FIRST IMPRESSION

June 2017

Build · Compete · Grow

Contents

Contents:1. Healthcare infrastructure 2. Medical device market3. Decree 36 and its influences4. Market entry

Build · Compete · Grow3 [email protected]

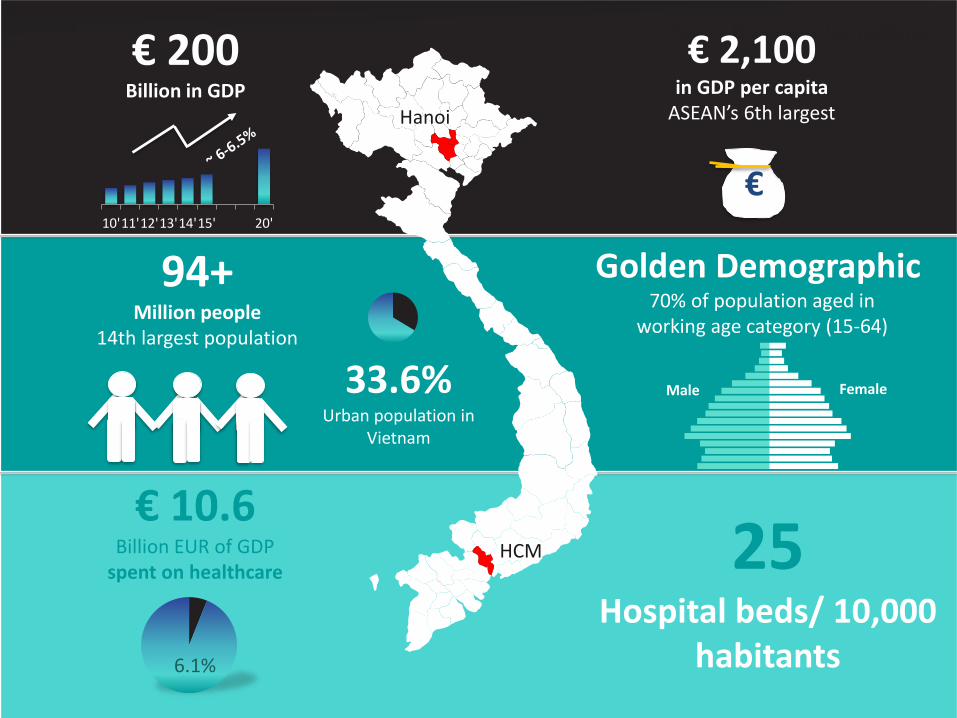

€ 200Billion in GDP

10'11'12'13'14'15' 20'

€ 2,100in GDP per capita

ASEAN’s 6th largest

€

94+ Million people

14th largest population

Golden Demographic70% of population aged in

working age category (15-64)

Male Female

€ 10.6Billion EUR of GDP

spent on healthcare 25Hospital beds/ 10,000

habitants6.1%

33.6%Urban population in

Vietnam

Hanoi

HCM

Build · Compete · Grow

Vietnam’s Healthcare Infrastructure

Build · Compete · Grow5 [email protected]

Health Establishments by TypeThe level of facility investment, professional capacity, and complexity of treatment are the differentiating factors for each healthcare facilities

Source: Statistical MoH report

Small Private Polyclinics(SPriPC)

Medium Private Polyclinics (MPriPC)

Private Specialized Clinics(PriSC)

District Polyhospitals(DPH)

Health Stations (HS)

Private Polyhospitals(PriPH)

Specialized Hospitals(SH)

Provincial Polyhospitals(ProPH)

Private Specialized Hospitals (PriSH)

Specific health problems. Public facility More popular in big cities. SPH is operated by a number of professionals including doctors and specialists

assigned by MoH, with very high level of investment in modern technologies

Specific health problems. Private facility Privately owned by one or a group of doctors or a medical group/corporation. SPH has specialized equipment

that can cure serious cases and perform complex surgeries

Various health problems. Private facility Privately owned by one or a group of doctors or a medical group/corporation. Some PHs are perceived as

better than public hospitals but more expensive and mostly not public insurance applicable

Various health problems. Public facility Present in every provincial unit with large number of beds and constructed in populous area. PH welcomes

hundred patient visits everyday, providing a broad range of treatment

Various health problems. Public facility Well-equipped state-owned facility with moderate to high capacity and public insurance applicability that

provides healthcare service to a large portion of community within an area The presence is deemed important as it helps to ease overcrowding of central / provincial hospitals

Specific health problems. Private facility Facility that is specialized in one field (otorhinolaryngology, obstetric, cardiology, etc) with modern equipment

(ultrasound device, X-ray device, etc) to perform complex diagnosis and treatment

Private facility. Able to treat in-patients MPP is moderately invested with equipment to perform higher diagnosis, treatment and minor surgeries

A few health problems. Private facility Simply equipped with 1 or 2 doctors in charge of treating patients with minor health problems such as flu,

coughing, stomachache, etc. SPP has flexible working hours and is convenient for quick health check-up

A few minor health problems. Public facility State-owned and present in every commune or ward. Physicians take main charge of diagnosing and

prescribing simple health problems

Public sector Private sector

~65 facilities

~51

~119

~629

~492

~11,743

~10,000

~10,000

~10,000

~43,099 facilities

Build · Compete · Grow6 [email protected]

2,787 2,970

3,280

859 1,031

1,858

686 687 531 379

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Red RiverDelta

Northernmidlands

andmountain

areas

NorthernCentral areaand Centralcoastal area

CentralHighlands

South East MekongRiver Delta

Hanoi Thanh Hoa Nghe An Ho Chi MinhCity

Region Key cities

No

. of

hea

lth

est

ablis

hm

en

ts

Number of health establishments by regions and by key cities in 2014 (*)

• Hanoi, the capital, is expected to receive the largest share of the central funding for purchasing new and advanced medical devices, given its preferential budget allocation from the MoH.

71% of healthcare establishments are situated in Northern Vietnam

(*) excluding private health establishments

Source: GSO

Healthcare Facilities by Regions and Cities

Build · Compete · Grow7 [email protected]

Inadequate number of public hospital to serve rising demand in healthcare needs, coupled with government encouragement are driving the growth of private hospital

• Public and Private hospitals are not sharing the patients burden:• 40% capacities/facilities are under-utilized• Public facilities are under constant overloaded

• Public hospitals’ overcapacity due to:• Affordable prices • Accessibility• Lack of well-trained and experienced staff with the private sector

Source: MoH Report (2011-2015), GSO and Ipsos Analysis 7

Private hospitals

7%

Public hospitals

93%

Patient Visits by Public vs. Private Hospitals 2015

Total patients visit = over 146 Mn

91% 88% 88% 88% 86%

9% 12% 12% 13% 14%

Private

Public

Vietnam Hospital Classification & Growth, 2011 – 2015

1,224 1,232 CAGR

13.6%

1,142 1,197

0.7%

1,241

Hospital Infrastructure vs. Demand

Build · Compete · Grow

Vietnam’s Medical Device Market

Build · Compete · Grow9 [email protected]

IPSOS KNOWLEDGE AND EXPERTISE

Source: [email protected]

459.0

668.7 698.0 747.1 815.8

892.3 977.8

0

200

400

600

800

1,000

1,200

2010 2014 2015e 2016f 2017f 2018f 2019f

EUR

mn

Medical equipment market value, 2010-19f

85.1

43.5

14.2 7.2 2.6 2.1

0

20

40

60

80

100

Singapore Malaysia Thailand Vietnam Philippines Indonesia

EUR

Medical equipment market value per capita, 2015

Vietnam’s medical devices market has observed a stable growth to estimated €977.8 million in 2019 with CAGR projected around 7%, which is considered one of the fastest growing markets in Asia

Medical Equipment Market Value, 2010 – 2019

Build · Compete · Grow10 [email protected]

Vietnam’s Medical Equipment by Segments, 2014 – 2019

• Consumables and diagnostic imaging segments are accounted for near half of the market.

• Dominated by imported goods with nearly 95% of the medical devices are from overseas, especially in high-end segments such as diagnostic imaging products. Local manufacturers can only meet the market demand for basic equipment such as hospital beds, rubber health products and disposable supplies.

23%

22%

5%5%

15%

30%

2014

25%

23%

5%6%

15%

26%

2019

Consumables

Diagnostic Imaging

Dental Products

Orthopaedics &Prosthetics

Patient Aids

Other Medical Devices

€668.7mn €977.8mn

Medical equipment market structure, 2014-19f

Source: BMI

Vietnam’s medical equipment sector is expected to record a 46% increase to reach nearly €1 bn in 2019 with nearly 95% of devices are imported

Build · Compete · Grow11 [email protected]

Medical equipment imports reached €631 million in 2014 with Diagnostic Imaging and Consumables segments account for over 45% of the total export value. Singapore and Japan were the top two suppliers of medical equipment to Vietnam in 2014

14%

27%

5%5%13%

36%

2010

23%

23%

5%5%

14%

30%

2014

Consumables

Diagnostic Imaging

Dental Products

Orthopaedics &ProstheticsPatient Aids

Other MedicalDevices

€437.8mn €631.3mn

Medical equipment’s import structure, 2010-2014

Source: BMI

24.0%

19.2%

12.8%10.8% 10.6% 8.9%

7.0%3.1% 2.8% 2.8% 2.5% 2.5%

17.0%

0%

5%

10%

15%

20%

25%

30%

Vietnam’s medical equipment import by main countries, 2015

Total import value = €631.3mn

Vietnam’s Medical Equipment Import Structure (2014 – 2019)

Build · Compete · Grow12 [email protected]

Experiment with the latest andmost innovative technologies andsystems. These end-users can be considered potential partners for EU investors to strategically market their products in Vietnam.

Major buyers but tend to purchase equipment from their country of origin.

Government-funded

hospitals, clinics and healthcare

centres

Foreign-owned and

joint-venture hospitals,

clinics, and healthcare

centres

Local private hospitals

Medical education and

research institutions

Purchase the largest quantity of medical equipment (70% of the market). Funded by the Government, this group of buyers often look for advanced and brand name medical devices made in G-8 countries

Expected to show the strongest growth as a result of the development of private healthcare in Vietnam in order to compete with public and foreign-owned healthcare centres.

Profile of End ConsumersGovernment-funded healthcare centers (hospitals, clinics and others) are considered the biggest purchaser of medical equipment

Build · Compete · Grow

Decree 36 and Its Influences

Build · Compete · Grow14 [email protected]

Decree 36: New Regulation For Medical Device Management

01/07/2016 01/01/2017

Effective date of Decree 36

•Complete announcement toeligible organizations totrade medical devices

•Receive the declarations ofapplicable standards for typeA medical devices

01/07/2017

•Complete the declaration ofeligibility to produce medical devices

•Complete submission of applicationfor declaration of eligibility toprovide technical advisory servicesand to conduct theinspection/calibration

•Effective date of receipt notes forapplicable standards of type Amedical devices

•Receive application for registrationof free sale of Type B, C or D medicaldevices

01/01/2018

• Effective date ofregistration number offree sale of type B, Cand D medical devices

• Medical devicemanufacturerscomplete application ofthe ISO 9001 qualitycontrol system

01/01/2020

• Medical devicemanufacturerscompleteapplication of theISO 13485 qualitycontrol system

Timeline:

Management System

Pre Decree 36 Post Decree 36

Medical devices market was managed under two separatelegislation systems: Local products: are required to be registered for Marketing

Authorization (MA) licenses for circulation in Vietnam Foreign products: are required to obtain import licenses for

circulation in Vietnam. In fact, only 49 out of 10,500 medicaldevices were required to get import licenses, whereas theremaining products can be imported under the generalconsumer goods and other categories.

No clear responsibilities of stakeholders, especially ones ofsuppliers.

Medical devices market was managed under an uniformlegislation systems: Both local and foreign products are required to registered

for MA licenses to be circulated in Vietnam Rights and responsibilities of stakeholders are regulated

clearly. Suppliers must provide their products’ informationand take responsibilities for whole products’ life cycle fromsupplying to after sale services.

Decree 36 on medical devices management will bring the medical devices market under an uniform legislation system and enhance the market transparency with existence of qualified suppliers and products

Source: Ipsos’ Research and Analysis, MoH

Build · Compete · Grow15 [email protected]

Impact LevelStakeholders Impacts

Suppliers in High-end segment

Low • With valid MA licenses, importation activities will be simplified without requirement of importlicense or import quota for each shipment

• Exemption from certain certificates (for example, certificates of quality control standards,summary of clinically testing data and others) for companies having the certificate for free sale(CFS) from countries or organizations such as: EU, Japan, Canada, TGA of Australia, FDA of USA,which will simplify the registration procedure and reduce the workload for the suppliers.

• More administrative tasks for suppliers to conform with the new regulations, especially theMA license requirement.

Suppliers in Mid-end and

Low- end segments

High

• With the valid MA licenses, importation activities will be simplified without requirement ofimport license or import quota for each shipment.

• Qualified suppliers can be benefited from tighter control and governance when disqualifiedsuppliers are eliminated leaving room for growth for this current oversupplied marketsegment.

• More administrative tasks for suppliers to conform with the new regulations, especially theMA license requirement.

• Existing companies without the CFS who provide unqualified or substandard products will facea new barrier with new certificate requirements (e.g. certificates of quality control standards,summary of clinically testing data, importation, manufacturing, circulation and tradingactivities).

• New and existing unqualified product suppliers will also face difficulties with additional humanresources and infrastructure (storage facilities, logistic requirement, employee’s technicalqualification in medical device technology) to operate.

Positive impact Negative impact

Source: Ipsos’ Research and Analysis via secondary research, primary research

Decree 36: Influences to Stakeholders

Build · Compete · Grow16 [email protected]

Impact LevelStakeholders Impacts

Healthcare practitioners

Low • Removal of substandard products and unqualified suppliers will give healthcare practitionersmore chances to procure high quality products from qualified suppliers

• They have more rights to request for suppliers’ responsibilities for their products’ life cycle,from supply to after-sale services

• The procurement bidding results must be published online as part of the new transparencyinitiative; hence, healthcare practitioners will be able to select the best fit suppliers

• The more stringent control of unqualified/substandard medical devices will lead to fewerchoices of cheaper products which will put new strain to the current financial budget formedical devices

Positive impact Negative impact

• Removal of substandard products and unqualified suppliers will give patients more chances touse high quality products from qualified suppliers

• Patients’ out of pocket payment may increase to cover the rise in payment for higher qualitymedical devices.

• Challenges in finding additional sources of finance to cover the rise in payment for medicaldevices as well as sufficient resources to implement and maintain the new Decree 36effectively and accurately.

• More workload, administrative and management jobs as well as challenges in theimplementation process to ensure the timeline, effectiveness and compliances of stakeholders.

• Top-down approach with clear responsibility and governance from the government and allrelevant authorities to control products quality throughout their lifecycle and ensure markettransparency

Patients Low

GO and Other Organizations

High

Source: Ipsos’ Research and Analysis via secondary research, primary research

Decree 36: Influences to Stakeholders

Build · Compete · Grow17 [email protected]

Key Growth Drivers of Vietnam’s Medical Equipment Sector

Key Drivers

Increasing population and life expectancy

Modernizing public

healthcare facilities

Encouraging International

initiatives

A significant expected surge of the 60-79 age group, exposes the healthcare infrastructure to higher demands and potentially also leads to increased investments to meet these needs. Furthermore, the rapid urbanisation also facilitates the emergence of hospitals, reducing the access to healthcare service in economical-disadvantaged areas.

To achieve this objective, it is estimated that the Government will need to spend approximately €1.06 billion per year. In addition, the expansion of the private healthcare sector in Vietnam has been facilitated by the lifting of the ban on private practice in 1989. More than 200 private facilities are in operation across the country to cater to the increasing demands of the emerging middle class.

Some international initiatives have been launched to support Vietnam’s plans in the healthcare sectors. For example, the 2nd phase of the EU Health Sector Policy Support Programme (EU-HSPSP-2) or the bilateral agreements with South Korea, Japan and the EU. This creates a momentum for the increase of import and export of medical equipment, while also opening new avenues for domestic manufacturers.

Build · Compete · Grow18 [email protected]

About Ipsos Business Consulting

Ipsos Business Consulting is the specialist consulting division of

Ipsos, which is ranked third in the global research industry.

With a strong presence in 88 countries, Ipsos employs more

than 16,000 people.

We have the ability to conduct consulting engagements in more

than 100 countries. Our team of consultants has been serving

clients worldwide through our 21 consulting "hubs" since 1994.

Our suite of solutions has been developed using over 20 years

experience of working on winning sales and marketing

strategies for developed and emerging markets. There is no

substitute for first-hand knowledge when it comes to

understanding an industry. We draw on the detailed industry

expertise of our consultants, which has been accumulated

through practical project execution.

Founded in France in 1975, Ipsos is controlled and managed by

research and consulting professionals. They have built a solid

Group around a multi-specialist positioning. Ipsos is listed on

Eurolist - NYSE-Euronext. The company is part of the SBF 120

and the Mid-60 index and is eligible for the Deferred Settlement

Service (SRD).ISIN code FR0000073298, Reuters ISOS.PA,

Bloomberg IPS:FP

Build · Compete · Grow

At Ipsos Business Consulting we focus on maintaining our position as a leading provider of high quality consulting solutions for sales and marketing professionals. We deliver information, analysis and recommendations that allow our clients to make smarter decisions and to develop and implement winning market strategies.

We believe that our work is important. Security, simplicity, speed and substance applies to everything we do.

Through specialisation, we offer our clients a unique depth of knowledge and expertise. Learning from different experiences gives us perspective and inspires us to boldly call things into question, to be creative.

By nurturing a culture of collaboration and curiosity, we attract the highest calibre of people who have the ability and desire to influence and shape the future.

Our Solutions:Go-to-Market Market SizingBusiness Unit Strategy PricingCompetitive Intelligence ForecastingPartner Evaluation Brand Strategy & ValueInnovation Scouting B2B Customer SegmentationOptimal Channel Strategy Sales Detector

Build · Compete · Grow19 [email protected]

Local knowledge with a global reach

Ipsos Business Consulting Hubs Ipsos Offices

New York

London

Lagos Nairobi

DubaiNew Delhi

MumbaiBangkok

Kuala Lumpur

Jakarta

Singapore

Ho Chi Minh City

Manila

Hong Kong

Shanghai

BeijingSeoul

Tokyo

Sydney

Wuhan

Johannesburg

CONTACT US

AUSTRALIA

Level 13, 168 Walker StreetNorth Sydney 2060NSW, AustraliaE. [email protected]. 61 (2) 9900 5100

GREATER CHINA

BEIJING12th Floor, Union PlazaNo. 20 Chao Wai AvenueChaoyang District, 100020Beijing, ChinaE. [email protected]. 86 (10) 5219 8899

SHANGHAI31/F Westgate Mall1038 West Nanjing Road 200041Shanghai, ChinaE. [email protected]. 86 (21) 2231 9988

WUHAN10F HongKong & Macao Center118JiangHan RoadHanKou Wuhan, 430014Wuhan, ChinaE. [email protected]. 86 (27) 5988 5888

HONG KONG22/F Leighton CentreNo 77 Leighton RoadCauseway BayHong KongE. [email protected]. 852 3766 2288

INDIA

MUMBAILotus Corporate Park1701, 17th Floor, F WingOff Western Express HighwayGoregoan (E), Mumbai – 400063, IndiaE. [email protected]. 91 (22) 6620 8000

GURGAON801, 8th Floor, Vipul Square B-Block, Sushant Lok, Part-1Gurgaon – 122016, HaryanaE. [email protected]. 91 (12) 4469 2400

INDONESIA

Graha Arda, 3rd FloorJl. H.R. Rasuna Said Kav B-6, 12910KuninganJakarta, IndonesiaE. [email protected]. 62 (21) 527 7701

JAPAN

Hulic Kamiyacho Building4-3-13, ToranomonMinato-ku, 105-0001Tokyo, JapanE. [email protected]. 81 (3) 6867 8001

KENYA

Acorn House97 James Gichuru Road LavingtonP.O. Box 6823000200 City SquareNairobi, KenyaE. [email protected]. 254 (20) 386 2721-33

MALAYSIA

18th Floor, Menara IGBNo. 2 The BoulevardMid Valley CityLingkaran Syed Putra, 59200Kuala Lumpur, MalaysiaE. [email protected]. 6 (03) 2282 2244

NIGERIA

Block A, Obi Village Opposite Forte OilMM2 Airport Road, IkejaLagos, NigeriaE. [email protected]. 234 (806) 629 9805

PHILIPPINES

1401-B, One Corporate CentreJulia Vargas cor. Meralco AveOrtigas Center, Pasig City, 1605Metro Manila, PhilippinesE. [email protected]. 63 (2) 633 3997

SINGAPORE

3 Killiney Road #05-01Winsland House I, S239519SingaporeE. [email protected]. 65 6333 1511

SOUTH AFRICA

Wrigley Field The Campus 57 Sloane Street BryanstonJohannesburg, South AfricaE. [email protected]. 27 (11) 709 7800

SOUTH KOREA

12th Floor, Korea EconomicDaily Building, 463 Cheongpa-RoJung-Gu 100-791Seoul, South KoreaE. [email protected]. 82 (2) 6464 5100

THAILAND

21st and 22nd Floor, Asia Centre Building173 Sathorn Road SouthKhwaeng TungmahamekKhet Sathorn 10120Bangkok, ThailandE. [email protected]. 66 (2) 697 0100

UAE

4th Floor, Office No 403Al Thuraya Tower 1P.O. Box 500611Dubai Media City, UAEE. [email protected]. 971 (4) 4408 980

UK

3 Thomas More SquareLondon E1 1YW United KingdomE. [email protected]. 44 (20) 3059 5000

USA

Time & Life Building1271 Avenue of the Americas15th FloorNew York, NY10020United States of AmericaE. [email protected]. 1 (212) 265 3200

VIETNAM

Level 9A, Nam A Bank Tower201-203 CMT8 Street, Ward 4District 3HCMC, VietnamE. [email protected]. 84 (8) 3832 9820

www.ipsosconsulting.com