market insights - immunities.co.il · global economy o the nine-year economic recovery continues as...

TRANSCRIPT

Market Insights

June 2018

Global Economy

o The nine-year economic recovery continues as global economy is expected to grow at 3.9% for 2018. The US economy

is the engine behind the robust growth as the rest of the world struggle to keep up

o The differences between monetary policies of the US and the rest of the world are getting sharper as the Fed continues

to tighten .This could further increase volatility in global financial markets

o Political turmoil from Turkey to Italy and Spain is adding to the burden investors face as they grapple with the end of

easy money conditions

o After trade war fears eased due to postponement of tariffs, Trump’s revival of a plan to slap tariffs on $50 billion of

Chinese imports has cast the talks between two country's into turmoil

o Higher borrowing costs in the US and USD appreciation expose weaknesses in emerging markets, as big chunk of their

debt is denominated in USD

o Oil retreated last month after Saudi Arabia and Russia said they are discussing reviving output

United Stateso US real GDP growth in Q1 was revised down to 2.2% from 2.3%. This deceleration in GDP growth was mainly due to

weak consumer spending and residential investment. However, it was a strong quarter for business, with

investment perhaps getting a boost from this year's corporate tax cut

o Inflation is stabilizing as the core PCE deflator, the fed preferred gauge of inflation, rose 0.2% in April and 1.8%

YOY. The Federal Open Market Committee minutes of its last meeting emphasized that a little overshooting is still

consistent with their policy, hence the fed in no hurry to accelerate the pace of rate hikes

o The labor market is strong as Nonfarm payroll rose 223K in May while the unemployment rate moves down to a

new expansion low of 3.8%. Average hourly earnings was up 0.3% and 2.7% YOY. It seems like available slack in the

labor force is disappearing and in turn raising the potential of wage inflation

o The Dollar Index has advanced more than 4 percent through April and May, on track for the best two-month run

since November 2016

o Dollar funding costs eased a little bit as rising demand for short-term debt has been fueled by inflation concerns

that promoted investors to ETF and money market funds

Core Economic IndicatorUSA

Economic Indicator Latest Figure Reference Period

Growth Rate 2.2% Q1-2018

Unemployment Rate 3.8% May-2018

Inflation Rate (Core PCE, YoY) 1.8% April-2018

FED Funds Target Range 1.5%-1.75% June-2018

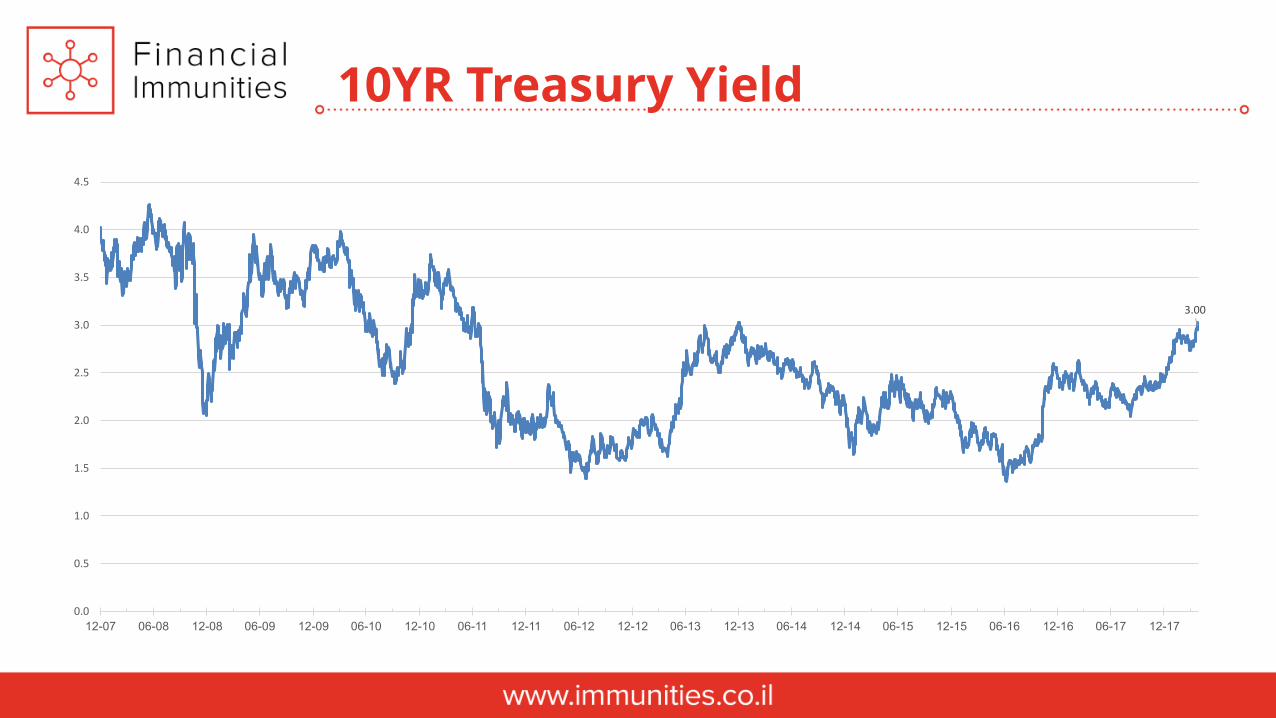

10 Year Treasury Yield to Maturity 2.9% June-2018

Ratio of Current Account Balance to GDP -2.36% Q4-2017

Ratio of Public Debt to GDP 103.74% October-2017

Economic Growth GDP (Annualized)

1.4

-2.7

2

-1.9

-8.2

-5.4

-0.5

1.3

3.9

1.7

3.9

2.7 2.5

-1.5

2.9

0.8

4.6

2.7

1.9

0.50.1

2.8

0.8

3.1

4

-0.9

4.6

5.2

2

3.22.7

1.6

0.5 0.6

2.2

2.8

1.8

1.2

3.1 3.22.9

2.2

-9.0

-8.0

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Economic SentimentManufacturing and Non-Manufacturing PMI

30

35

40

45

50

55

60

65

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Manufacturing Non- Manufacturing

Labor MarketUnemployment Rate (Left) and Under Unemployment Rate (Right)

6

8

10

12

14

16

18

3.5

4.5

5.5

6.5

7.5

8.5

9.5

10.5

12-07 06-08 12-08 06-09 12-09 06-10 12-10 06-11 12-11 06-12 12-12 06-13 12-13 06-14 12-14 06-15 12-15 06-16 12-16 06-17 12-17

Unemployment U6- Unemployment

InflationCore PCE (YoY) and 5Y Inflation Forecast

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

12-07 06-08 12-08 06-09 12-09 06-10 12-10 06-11 12-11 06-12 12-12 06-13 12-13 06-14 12-14 06-15 12-15 06-16 12-16 06-17 12-17

US Breakeven 5 Year Inflation Core PCE Rate (YoY) Inflation Target

Fed Inflation Target

10YR Treasury Yield

3.00

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

12-07 06-08 12-08 06-09 12-09 06-10 12-10 06-11 12-11 06-12 12-12 06-13 12-13 06-14 12-14 06-15 12-15 06-16 12-16 06-17 12-17

US Treasury Yield Curve

0

0.5

1

1.5

2

2.5

3

0Y 2Y 4Y 6Y 8Y 10YCurrent 3-Months Ago 6-Months Ago

Fed Funds Projection

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

2018 2019 2020

FOMC Dots Median OIS - Latest Value

Probability of a 4th FED Funds Hike in 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

5/31/20185/15/20184/27/20184/11/20183/26/20183/8/20182/20/20182/2/20181/17/20181/1/201812/14/2017

US Dollar Index (DXY)

75.0

80.0

85.0

90.0

95.0

100.0

105.0

12-12 06-13 12-13 06-14 12-14 06-15 12-15 06-16 12-16 06-17 12-17

Citi Economic Surprise

-100

-80

-60

-40

-20

0

20

40

60

80

100

12-12 03-13 06-13 09-13 12-13 03-14 06-14 09-14 12-14 03-15 06-15 09-15 12-15 03-16 06-16 09-16 12-16 03-17 06-17 09-17 12-17 03-18

o Economic growth in Europe lost further momentum in the past month. Hopes that the first quarter cooling in GDP

would prove short-lived are looking increasingly optimistic

o The Eurozone labor market continues to tighten as unemployment rate fell to 8.5%. Although, there are Signs of

some pick-up in wage growth further advances will probably be needed for wages growth to pick up significantly

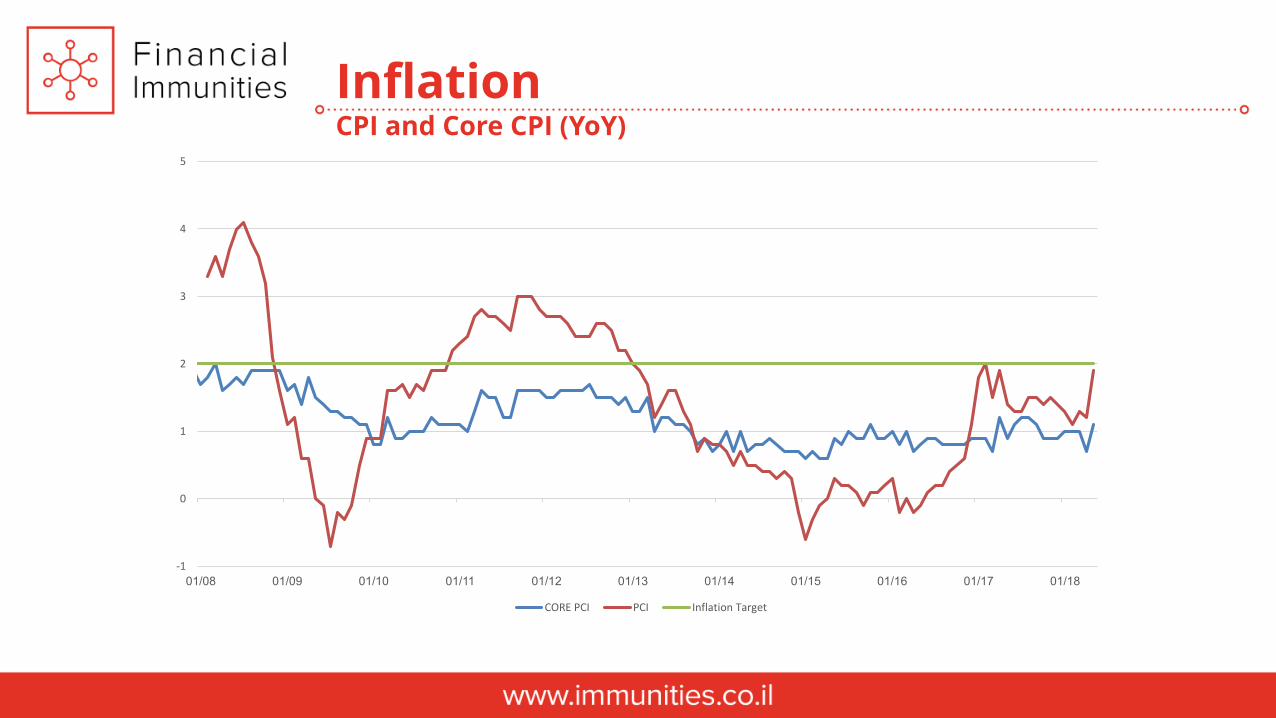

o Euro-area inflation hit the fastest pace in more than a year at 1.9% YOY. The reading was 0.7% above April reading

and much stronger than expected. The core measure rose to 1.1%, also better than anticipated

o Political uncertainty in Italy and Spain revives memories of the debt crisis and sent financial markets into turmoil.

The change at the top of the euro region’s third and fourth-biggest economies calmed the markets, although the

new government in Italy threatens to further challenge the EU on budget rules and immigration

o The central bank is likely to remain quite cautious in its updated economic forecasts at the next policy meeting

scheduled June 14. The inflation report may increase the chances of ending the asset purchase program in

September but it certainly does not guarantee it

Eurozone

Core Economic IndicatorEurozone

Economic Indicator Latest Figure Reference Period

Growth Rate (YoY) 1.6% Q1-2018

Unemployment Rate 8.5% April-2018

Inflation Rate (Core, YoY) 1.1% May-2018

Central Bank deposit rate 0.00% April-2018

10 Year Government Bond Yield (Germany) 0.38% June-2018

Ratio of Surplus in Current Account to GDP 3.51% Q4-2017

Ratio of Public Debt to GDP 86.7% Q4-2017

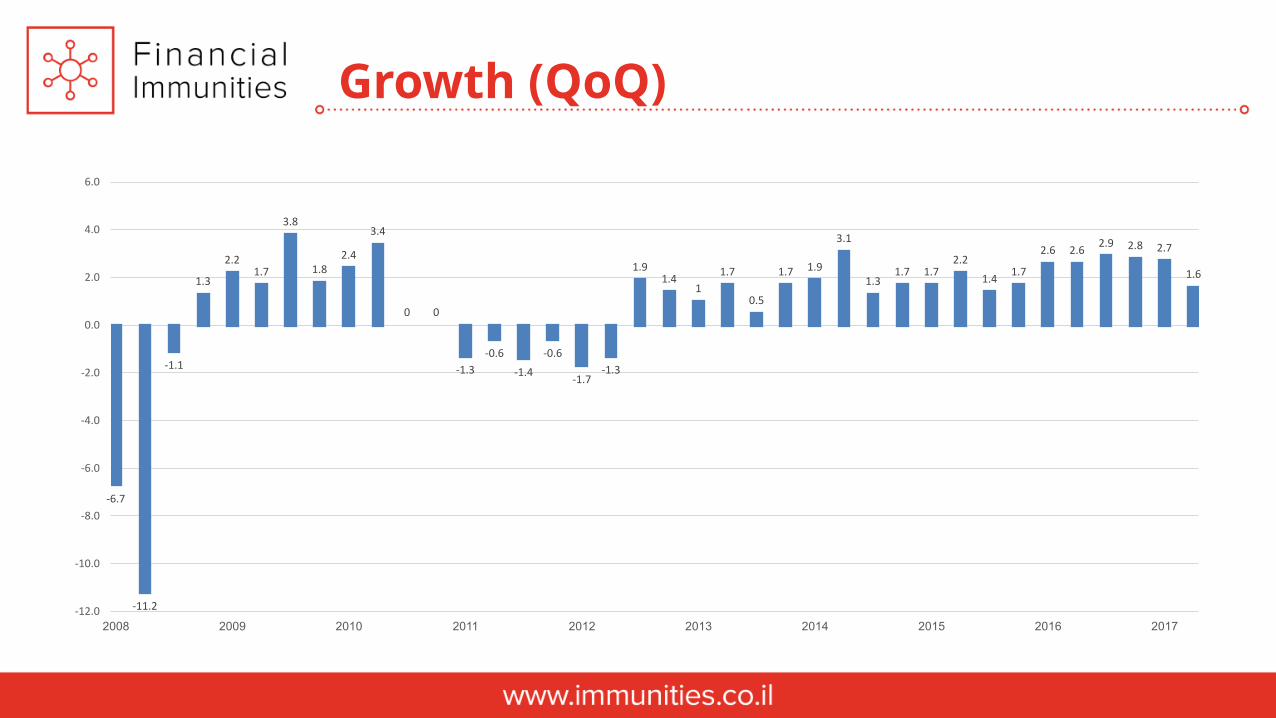

Growth (QoQ)

-6.7

-11.2

-1.1

1.3

2.21.7

3.8

1.82.4

3.4

0 0

-1.3

-0.6

-1.4

-0.6

-1.7-1.3

1.91.4

1

1.7

0.5

1.7 1.9

3.1

1.31.7 1.7

2.2

1.41.7

2.6 2.62.9 2.8 2.7

1.6

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Economic SentimentManufacturing and Non-Manufacturing PMI

48.0

50.0

52.0

54.0

56.0

58.0

60.0

62.0

08-15 11-15 02-16 05-16 08-16 11-16 02-17 05-17 08-17 11-17 02-18 05-18

Manufacturing Non-Manufacturing

Labor MarketUnemployment Rate

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

12-07 06-08 12-08 06-09 12-09 06-10 12-10 06-11 12-11 06-12 12-12 06-13 12-13 06-14 12-14 06-15 12-15 06-16 12-16 06-17 12-17

InflationCPI and Core CPI (YoY)

-1

0

1

2

3

4

5

01/08 01/09 01/10 01/11 01/12 01/13 01/14 01/15 01/16 01/17 01/18

CORE PCI PCI Inflation Target

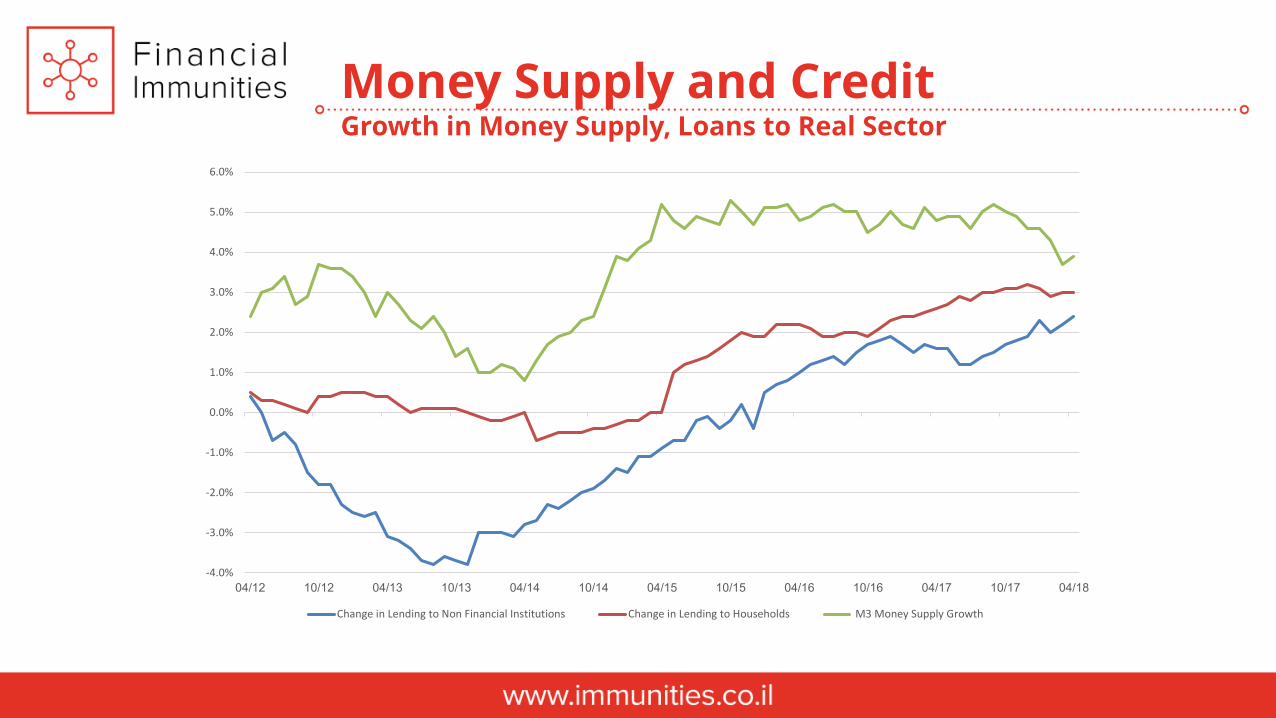

Money Supply and CreditGrowth in Money Supply, Loans to Real Sector

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

04/12 10/12 04/13 10/13 04/14 10/14 04/15 10/15 04/16 10/16 04/17 10/17 04/18

Change in Lending to Non Financial Institutions Change in Lending to Households M3 Money Supply Growth

10YR Government Bond Yield

-0.5

0.5

1.5

2.5

3.5

4.5

12-13 03-14 06-14 09-14 12-14 03-15 06-15 09-15 12-15 03-16 06-16 09-16 12-16 03-17 06-17 09-17 12-17 03-18

Germany Italy France Spain

Exchange RateEuro Index (Right) EURUSD (Left)

1

1.05

1.1

1.15

1.2

1.25

1.3

1.35

1.4

1.45

75

80

85

90

95

100

31/12/2012 30/06/2013 31/12/2013 30/06/2014 31/12/2014 30/06/2015 31/12/2015 30/06/2016 31/12/2016 30/06/2017 31/12/2017

Euro Index EURUSD

Citi Economic Surprise

-150

-100

-50

0

50

100

12-12 03-13 06-13 09-13 12-13 03-14 06-14 09-14 12-14 03-15 06-15 09-15 12-15 03-16 06-16 09-16 12-16 03-17 06-17 09-17 12-17 03-18

o The economy continues to grow at a rate slightly higher than 4%

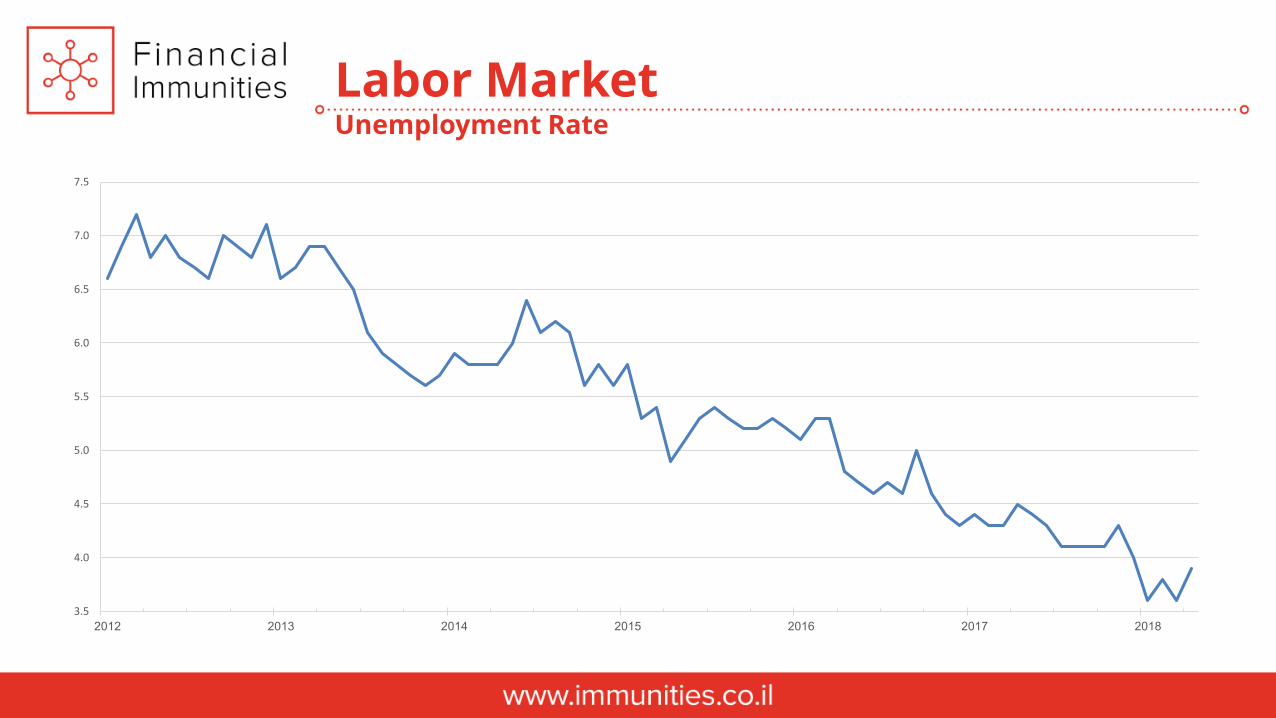

o The unemployment rate is at 3.9%, reflecting a slight increase for the first time since last September

o The inflation rate continues to rise, supported by increasing commodity prices and wages, but it is still

below the target

o The Monetary Committee decided to leave the interest rate unchanged at 0.1% and it is expected to

remain unchanged at least until the beginning of 2019

o The stagnation in housing market continues as house prices fell by 2.7% on the last 6 months

o During the last month, interest rate differential between the USD and ILS continued to widen to 2.7%

(close to 1,000 pips)

o The divergence between local and US monetary policy is expected to deepen. This will further

extend the interest rates differential and make ILS financial assets less attractive

Israel

Core Economic IndicatorIsrael

Economic Indicator Latest Figure Reference Period

Growth Rate 4.2% Q1-2018

Unemployment Rate 3.9% April-2018

Inflation Rate (YoY) 0.4% April-2018

Central Bank Interest Rate 0.1% June-2018

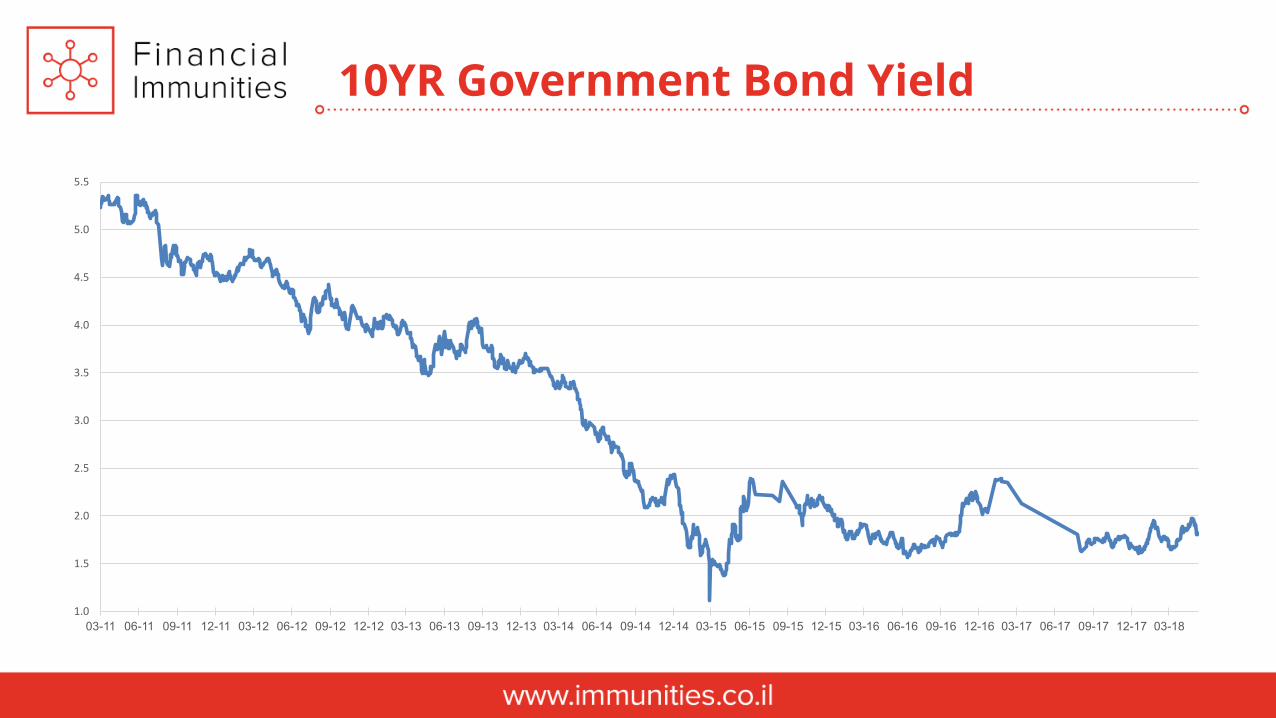

10 Year Government Bond Yield 1.84% June-2018

Ratio of Surplus in Current Account to GDP 2.94% Q4-2017

Ratio of Public Debt to GDP 59.5% Q4-2017

Economic Growth (Annualized)

5.3

2.9

10.8

-2.4

0.3

3.6

55.4

66.3

3.7

5.9

6.4

5.1

6.6

1.7

00.2

4.13.9

4.3

6.8

3.7

2.3

3.73.3

1.8

6.2

2.2

0.2

1.5

4.24.5

5.5

4.1

4.6

0.8

2.9

4.3 4.44.2

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

12-07 06-08 12-08 06-09 12-09 06-10 12-10 06-11 12-11 06-12 12-12 06-13 12-13 06-14 12-14 06-15 12-15 06-16 12-16 06-17 12-17

Labor MarketUnemployment Rate

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

2012 2013 2014 2015 2016 2017 2018

InflationCPI (YoY)

0.4

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

10YR Government Bond Yield

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

03-11 06-11 09-11 12-11 03-12 06-12 09-12 12-12 03-13 06-13 09-13 12-13 03-14 06-14 09-14 12-14 03-15 06-15 09-15 12-15 03-16 06-16 09-16 12-16 03-17 06-17 09-17 12-17 03-18

Government Bond Yield Curve

0

0.5

1

1.5

2

2.5

0Y 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y

Current 3-Months Ago 6-Months Ago

Hedging CostsUSDILS 1YR Forward Premium

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

Exchange RateUSDILS (Left) BOI Nominal Effective Rate (Right)

75

80

85

90

95

100

105

01-13 07-13 01-14 07-14 01-15 07-15 01-16 07-16 01-17 07-17 01-18

3

3.2

3.4

3.6

3.8

4

4.2

USDILS BoI Nominal Effective Exchange Rate