march 2016 u.s. employment update and outlook

TRANSCRIPT

U.S. employment situation: September 2013

Release date: October 22, 2013

Healthier growth returned in February,

but variance remains

U.S. employment situation: February 2016 March 4, 2016

February 2016 employment summary

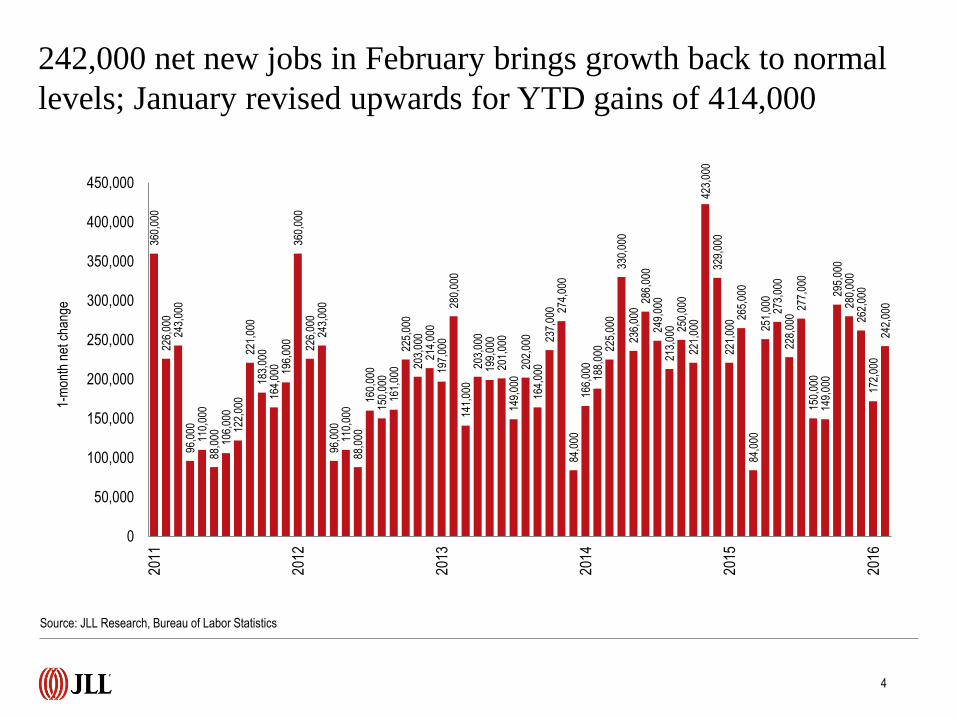

• After a slow January, February returned back to normal levels of grow with 242,000 net new jobs. Although year-to-date figures are down

compared to 2015, January saw significant upward revisions to 172,000 jobs, improving the year’s initial performance. Despite global tensions

and economic shifts, the U.S. economy seems to be holding its own, although certain sectors such as energy and trade could be impacted by

fluctuations in domestic and international demand.

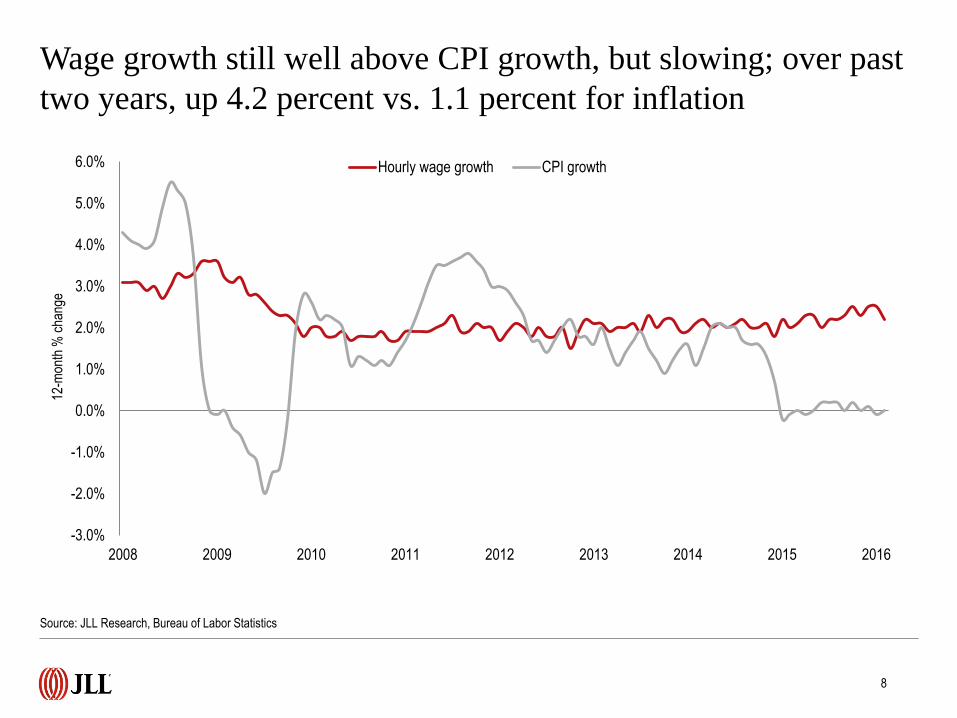

• Hourly wage growth fell slightly to 2.2 percent, but is still outperforming inflation at 0.0 percent. Over the past two years, wages have

increased 3.8 times faster than inflation; while this should be increasing consumer spending, the personal consumption expenditures

component of GDP has fallen in seasonally adjusted annual terms to 1.5 percent, compared to the 2015 average of 1.8 percent.

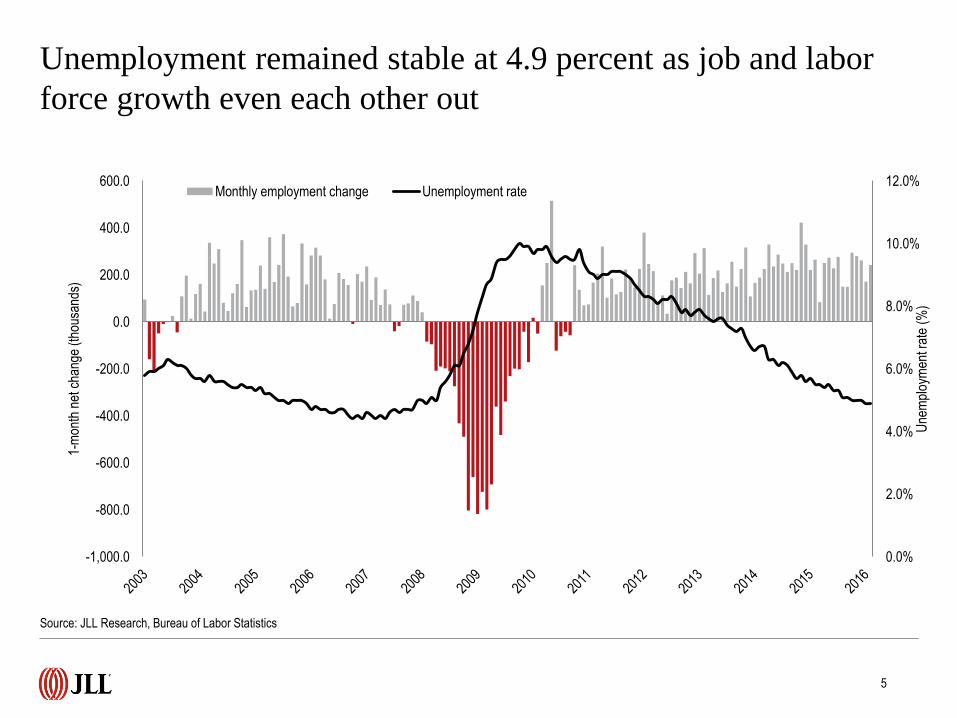

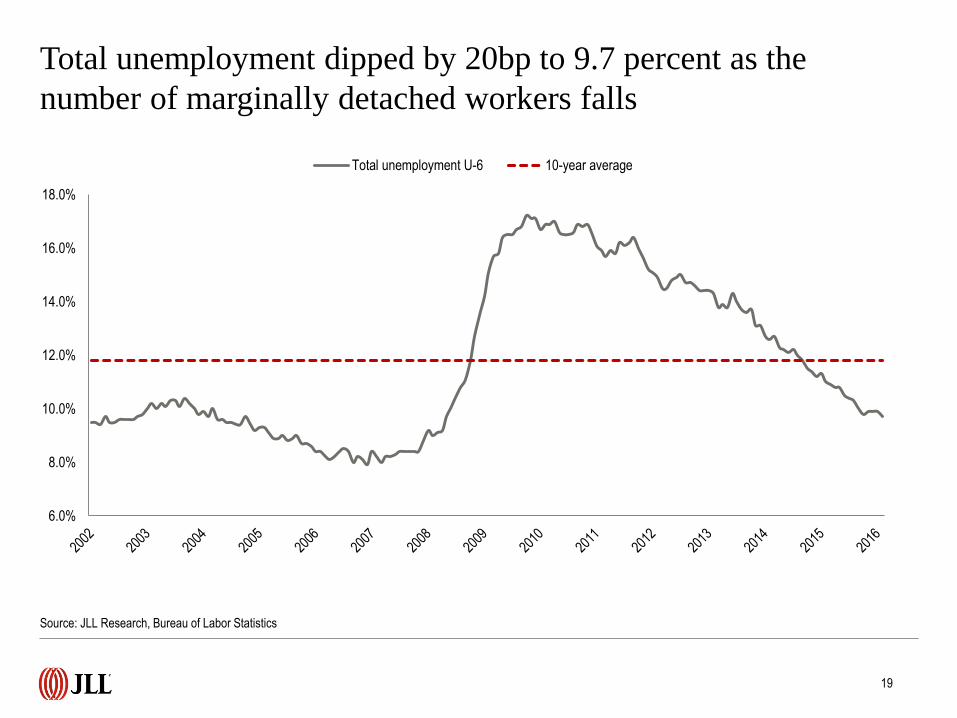

• Unemployment remained steady at 4.9 percent in February, keeping it below 5.0 percent for the second month since before the recession. On

the other hand, total unemployment dipped by 20 basis points to 9.7 percent as the number of marginally detached workers continues to

decline.

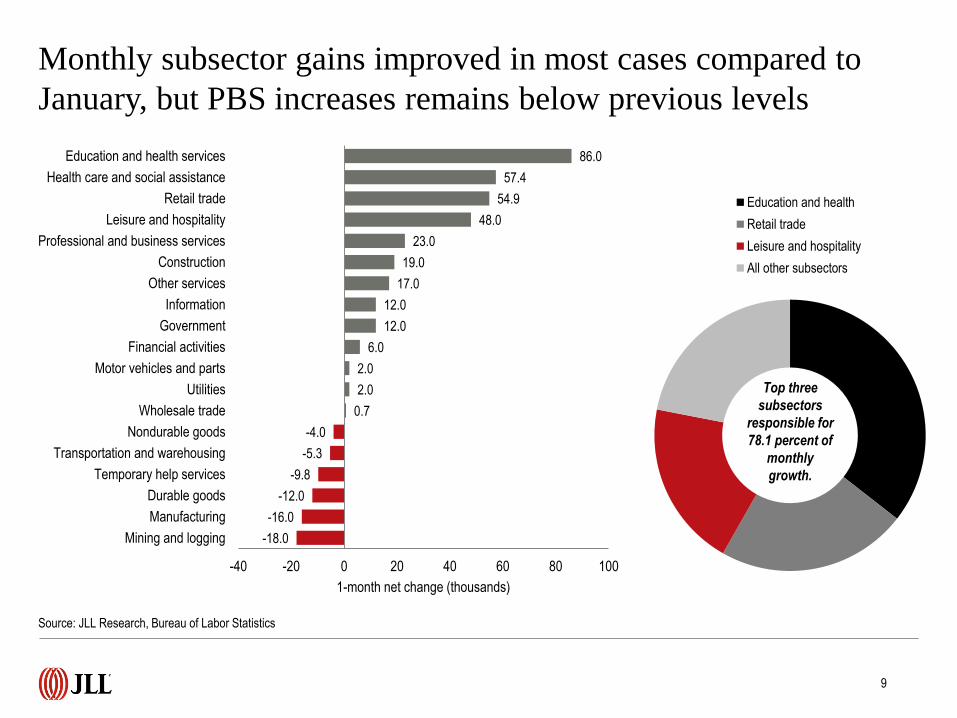

• At the industry level, most subsectors witnessed some level of improvement, while mining and logging contracted yet again by 18,000. More

volatile was manufacturing, which dropped into negative territory in February as well, along with transportation and warehousing. Professional

and business services (PBS), previously the consistent leader in the recovery, is still growing, albeit at a slower rate than education and

health, retail trade and leisure and hospitality, in turn bringing down office-using industries’ contributions to monthly gains.

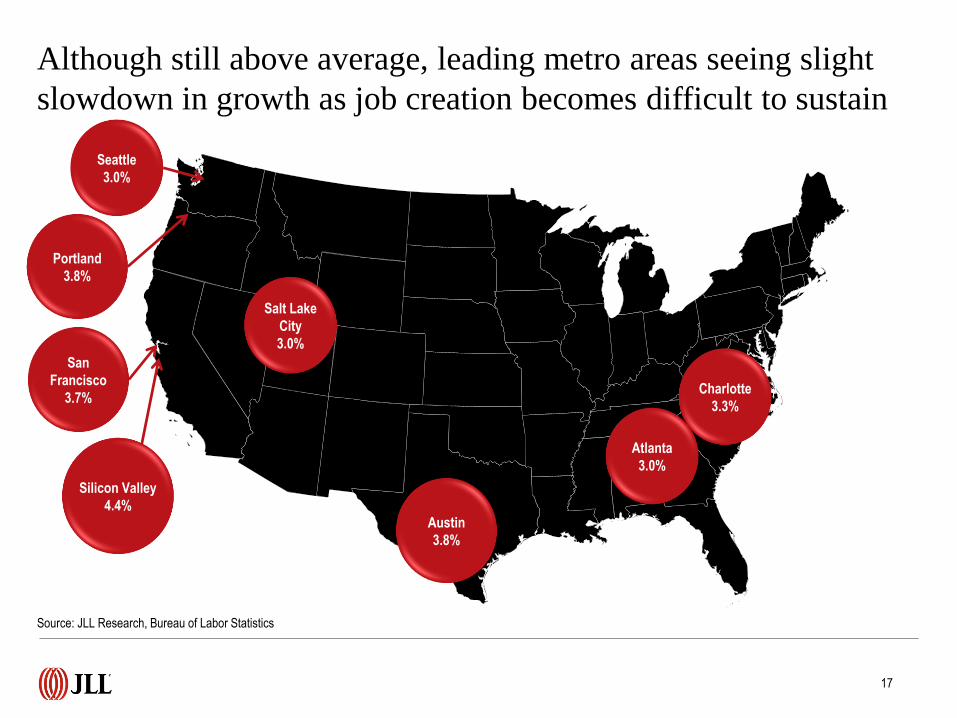

• High-performing local markets continue to add jobs at a blistering pace, although their rates of growth have begun to soften as talent

shortages and a lack of slack in the labor market make current absolute levels of growth more difficult. Silicon Valley once again led the pack

with 4.4-percent growth, while tech hubs such as San Francisco and Portland aren’t far behind at 3.7 and 3.8 percent, respective ly. At 3.0 and

2.9 percent, Atlanta and Dallas continue to witness the positive effects of diverse corporate expansion and migration, as rapid employment

growth is translating into demand for space, aided by structurally high vacancy providing increased and more affordable options for tenants.

Source: JLL Research, Bureau of Labor Statistics

February 2016 labor market at a glance

+242,000(65 consecutive months

of growth)1-month net change

+2,672,000(+1.9% y-o-y)

12-month change

+779,00010-year average annual growth

Source: JLL Research, Bureau of Labor Statistics

4.9%Unemployment rate

-60bp12-month change in unemployment

7.0%10-year average unemployment

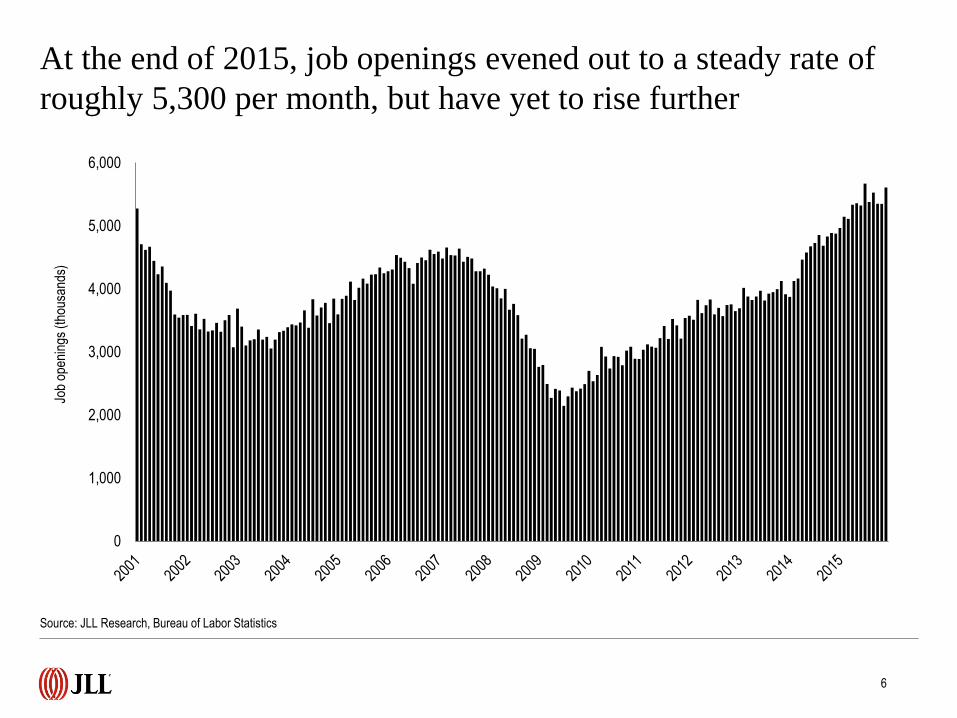

5,607,000(+3.8% y-o-y)

Job openings

5,361,000(+2.3% y-o-y)

Hires

3,055,000(+2.1% y-o-y)

Quits

242,000 net new jobs in February brings growth back to normal

levels; January revised upwards for YTD gains of 414,000

360,

000

226,

000

243,

000

96,0

0011

0,00

088

,000 10

6,00

012

2,00

022

1,00

018

3,00

016

4,00

0 196,

000

360,

000

226,

000

243,

000

96,0

0011

0,00

088

,000

160,

000

150,

000

161,

000

225,

000

203,

000

214,

000

197,

000

280,

000

141,

000

203,

000

199,

000

201,

000

149,

000

202,

000

164,

000

237,

000 27

4,00

084

,000

166,

000

188,

000 22

5,00

033

0,00

023

6,00

028

6,00

024

9,00

021

3,00

0 250,

000

221,

000

423,

000

329,

000

221,

000 26

5,00

084

,000

251,

000

273,

000

228,

000

277,

000

150,

000

149,

000

295,

000

280,

000

262,

000

172,

000

242,

000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2011

2012

2013

2014

2015

2016

1-m

onth

net

cha

nge

4

Source: JLL Research, Bureau of Labor Statistics

Unemployment remained stable at 4.9 percent as job and labor

force growth even each other out

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-1,000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

Une

mpl

oym

ent r

ate

(%)

1-m

onth

net

cha

nge

(tho

usan

ds)

Monthly employment change Unemployment rate

Source: JLL Research, Bureau of Labor Statistics

5

At the end of 2015, job openings evened out to a steady rate of

roughly 5,300 per month, but have yet to rise further

Source: JLL Research, Bureau of Labor Statistics

6

0

1,000

2,000

3,000

4,000

5,000

6,000

Job

open

ings

(th

ousa

nds)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Con

sum

er c

onfid

ence

inde

xAlthough consumer confidence dropped to 92.2 in February, it

has stayed within a similar range for past six months

Source: JLL Research, Bureau of Labor Statistics

7

Wage growth still well above CPI growth, but slowing; over past

two years, up 4.2 percent vs. 1.1 percent for inflation

Source: JLL Research, Bureau of Labor Statistics

8

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016

12-m

onth

% c

hang

e

Hourly wage growth CPI growth

-18.0

-16.0

-12.0

-9.8

-5.3

-4.0

0.7

2.0

2.0

6.0

12.0

12.0

17.0

19.0

23.0

48.0

54.9

57.4

86.0

-40 -20 0 20 40 60 80 100

Mining and logging

Manufacturing

Durable goods

Temporary help services

Transportation and warehousing

Nondurable goods

Wholesale trade

Utilities

Motor vehicles and parts

Financial activities

Government

Information

Other services

Construction

Professional and business services

Leisure and hospitality

Retail trade

Health care and social assistance

Education and health services

1-month net change (thousands)

Monthly subsector gains improved in most cases compared to

January, but PBS increases remains below previous levels

Source: JLL Research, Bureau of Labor Statistics

9

Education and health

Retail trade

Leisure and hospitality

All other subsectors

Top three

subsectors

responsible for

78.1 percent of

monthly

growth.

-141.0

-34.0

11.2

12.0

27.3

41.0

46.0

51.7

66.0

68.0

75.0

86.0

142.0

253.0

338.6

446.0

610.0

634.5

698.0

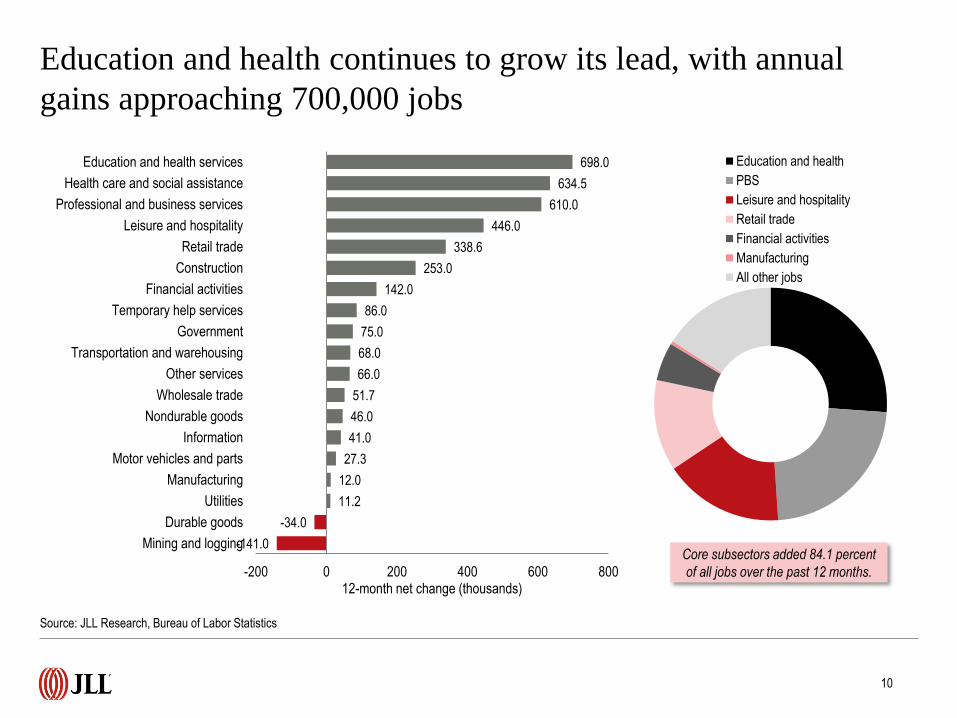

-200 0 200 400 600 800

Mining and logging

Durable goods

Utilities

Manufacturing

Motor vehicles and parts

Information

Nondurable goods

Wholesale trade

Other services

Transportation and warehousing

Government

Temporary help services

Financial activities

Construction

Retail trade

Leisure and hospitality

Professional and business services

Health care and social assistance

Education and health services

12-month net change (thousands)

Education and health

PBS

Leisure and hospitality

Retail trade

Financial activities

Manufacturing

All other jobs

Education and health continues to grow its lead, with annual

gains approaching 700,000 jobs

Source: JLL Research, Bureau of Labor Statistics

10

Core subsectors added 84.1 percent

of all jobs over the past 12 months.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Une

mpl

oym

ent r

ate

(%)

For the seventh consecutive month, bachelor’s degree

unemployment remains at natural low of 2.5 percent

Source: JLL Research, Bureau of Labor Statistics

11

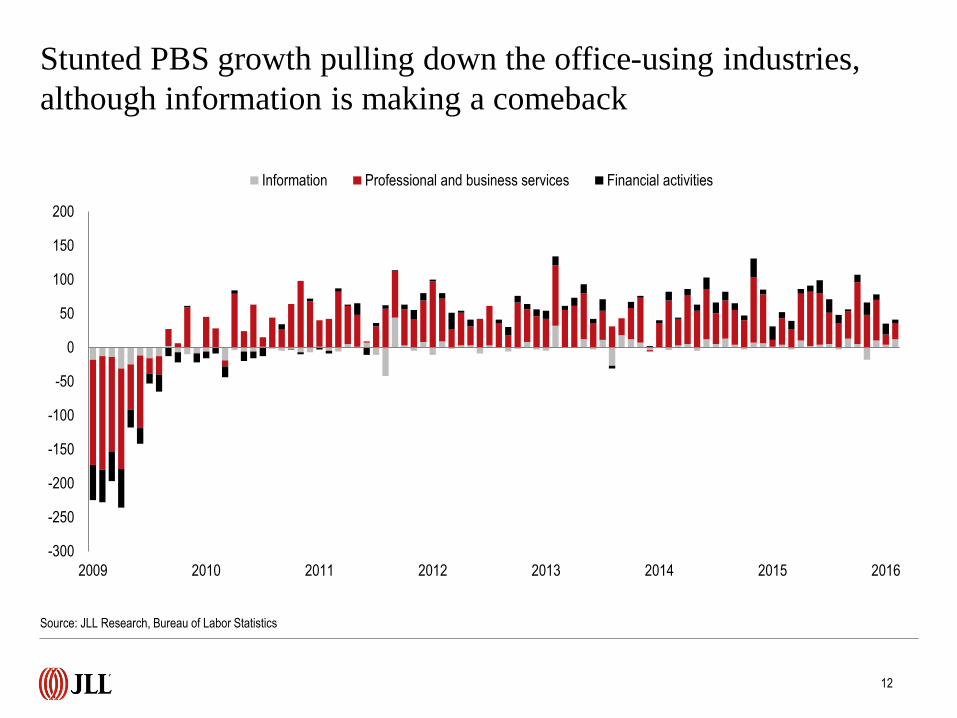

Stunted PBS growth pulling down the office-using industries,

although information is making a comeback

-300

-250

-200

-150

-100

-50

0

50

100

150

200

2009 2010 2011 2012 2013 2014 2015 2016

Information Professional and business services Financial activities

Source: JLL Research, Bureau of Labor Statistics

12

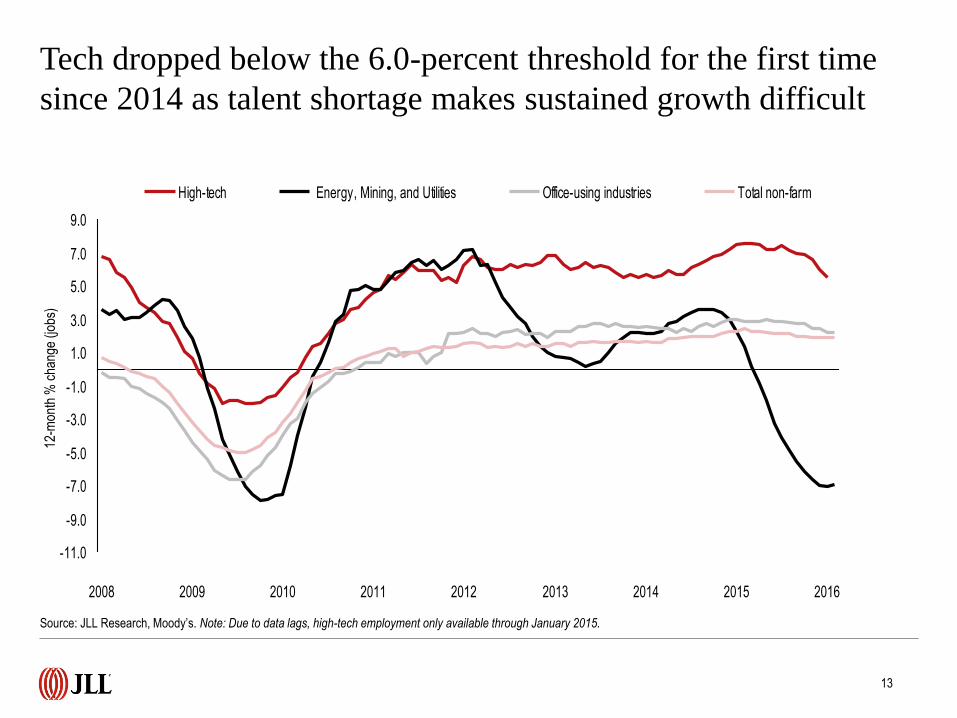

Tech dropped below the 6.0-percent threshold for the first time

since 2014 as talent shortage makes sustained growth difficult

-11.0

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

2008 2009 2010 2011 2012 2013 2014 2015 2016

High-tech Energy, Mining, and Utilities Office-using industries Total non-farm

Source: JLL Research, Moody’s. Note: Due to data lags, high-tech employment only available through January 2015.

13

12-m

onth

% c

hang

e (jo

bs)

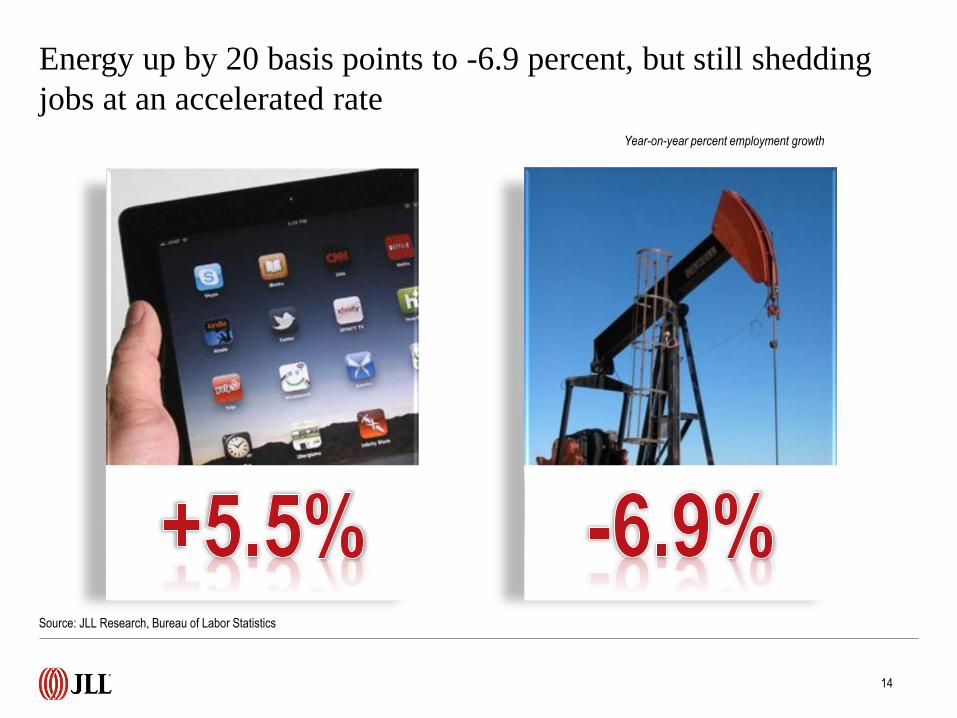

Energy up by 20 basis points to -6.9 percent, but still shedding

jobs at an accelerated rate Year-on-year percent employment growth

Source: JLL Research, Bureau of Labor Statistics

14

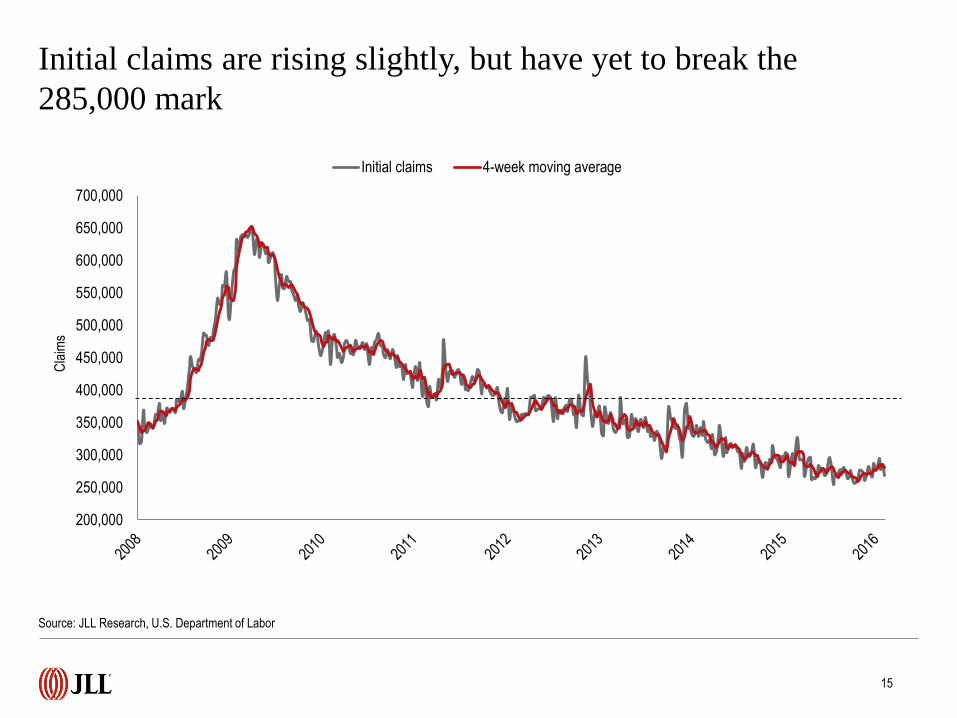

Initial claims are rising slightly, but have yet to break the

285,000 mark

Source: JLL Research, U.S. Department of Labor

15

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

Cla

ims

Initial claims 4-week moving average

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 2011 2012 2013 2014 2015

Hire

s an

d qu

its (

thou

sand

s)

Hires Quits

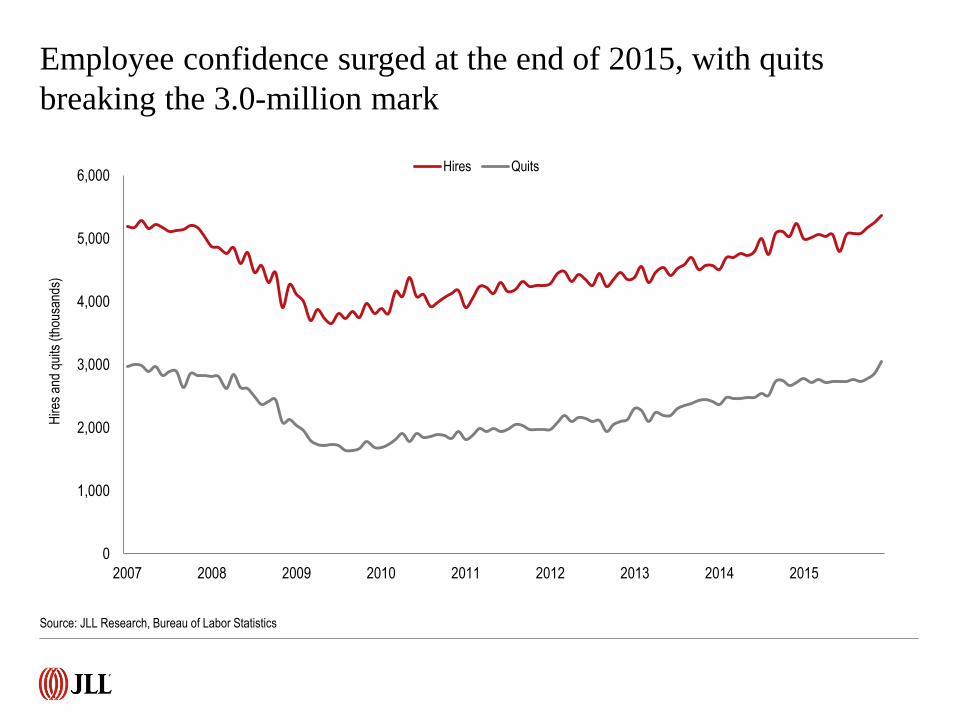

Employee confidence surged at the end of 2015, with quits

breaking the 3.0-million mark

Source: JLL Research, Bureau of Labor Statistics

Although still above average, leading metro areas seeing slight

slowdown in growth as job creation becomes difficult to sustain

Source: JLL Research, Bureau of Labor Statistics

17

Silicon Valley

4.4%

San

Francisco

3.7%

Atlanta

3.0%

Austin

3.8%

Salt Lake

City

3.0%

Portland

3.8%

Seattle

3.0%

Charlotte

3.3%

0.6%

0.8%

1.3%

1.7%

1.7%

2.2%

2.2%

2.2%

2.9%

3.0%

3.0%

4.4%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% 5.0%

Chicago

Houston

Philadelphia

Boston

New York

Los Angeles

Washington, DC

South Florida

Dallas

Seattle

Atlanta

San Francisco

12-month % change

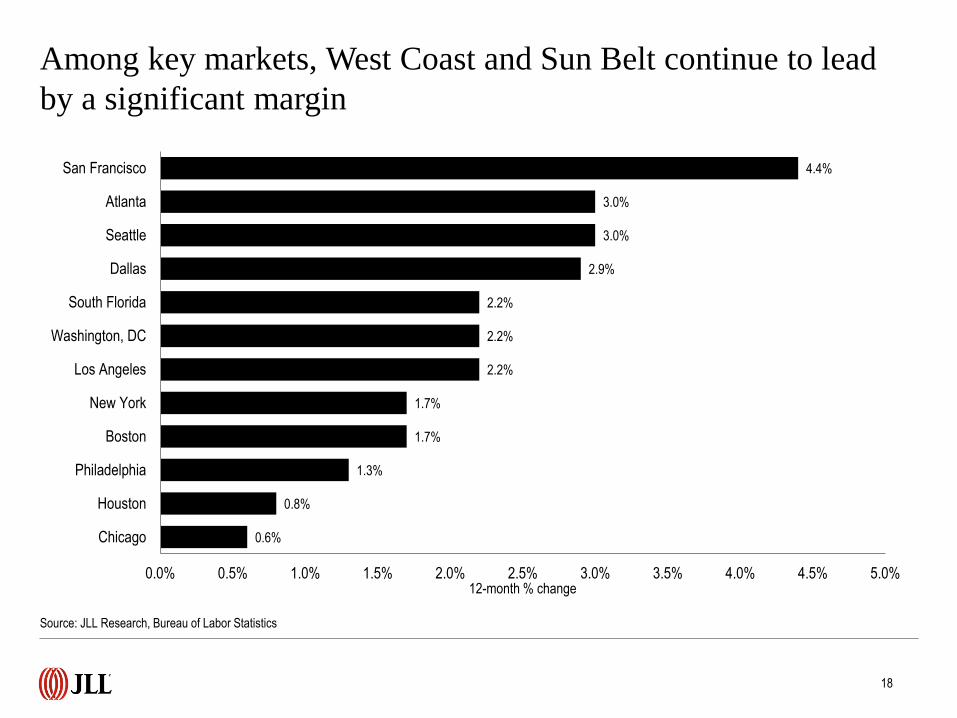

Among key markets, West Coast and Sun Belt continue to lead

by a significant margin

Source: JLL Research, Bureau of Labor Statistics

18

Total unemployment dipped by 20bp to 9.7 percent as the

number of marginally detached workers falls

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Total unemployment U-6 10-year average

Source: JLL Research, Bureau of Labor Statistics

19

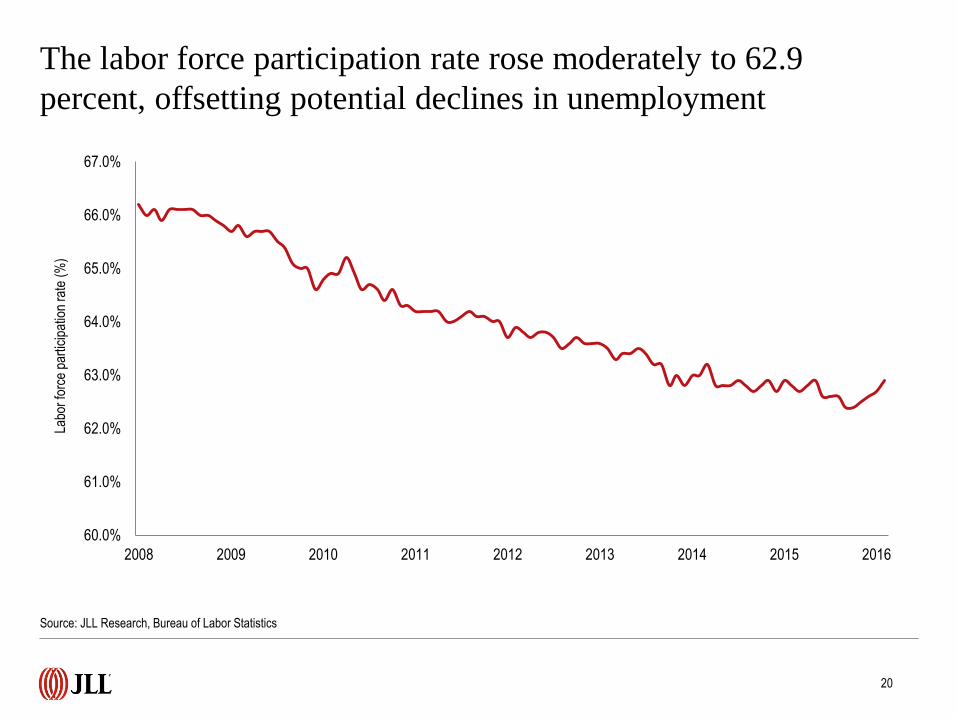

The labor force participation rate rose moderately to 62.9

percent, offsetting potential declines in unemployment

Source: JLL Research, Bureau of Labor Statistics

20

60.0%

61.0%

62.0%

63.0%

64.0%

65.0%

66.0%

67.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016

Labo

r fo

rce

part

icip

atio

n ra

te (

%)

©2015 Jones Lang LaSalle Research IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

For more information, please contact:

Ben Breslau

Managing Director - Americas Research

Phil Ryan

Research Analyst – Office and Economy Research

Or, find more employment, business and real estate research at jll.com.

>>> Click here to check it out.