mandatory savings and retirement adequacy: a portfolio simulation of epf in sri lanka wasana...

Post on 21-Dec-2015

218 views

TRANSCRIPT

Mandatory Savings and Mandatory Savings and Retirement Adequacy: A Retirement Adequacy: A Portfolio Simulation of Portfolio Simulation of

EPF in Sri LankaEPF in Sri Lanka

Wasana Wasana KarunarathneKarunarathneThe University of MelbourneThe University of Melbourne

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 22

AgendaAgenda

The Employees Provident Fund (EPF) The Employees Provident Fund (EPF)

EPF’s Investment PerformancesEPF’s Investment Performances

Empirical FindingsEmpirical Findings Does EPF Provide Sufficient Member Balances?Does EPF Provide Sufficient Member Balances?

Member Balances under Different Portfolio Member Balances under Different Portfolio InvestmentsInvestments

Parametric Reform OptionsParametric Reform Options

Policy RecomendationsPolicy Recomendations

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 33

The EPF SchemeThe EPF Scheme

EPF is implemented in 1958

Major vehicle for private sector employees

Covers around 30% of the labour force (80% of the private sector employees)

Fully funded, defined contributory (DC) type

Centrally managed by the Central Bank of Sri Lanka on behalf of the government

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 44

Contribution Rate: 20% of gross salaryContribution Rate: 20% of gross salaryMandatory for both employers (12%) Mandatory for both employers (12%) and employees (8%)and employees (8%)

Benefits: lump sum PaymentBenefits: lump sum Payment

Retirement age: 55 years Retirement age: 55 years

Pre-retirement withdrawals: allowed Pre-retirement withdrawals: allowed for housing purposesfor housing purposes

EPF Scheme cont.

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 55

EPF Scheme cont.

4

6

8

10

12

14

16

18

20

1995 1996 1997 1998 1999 2000 2001 2002

cont / GDS (%)

EPF Sav / GDS (%)

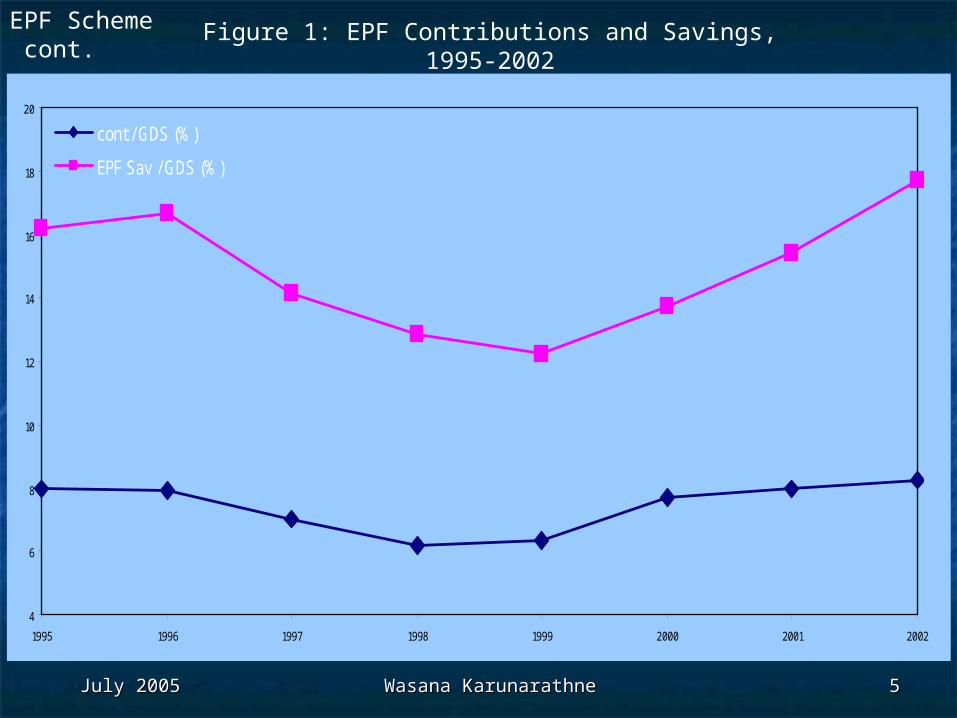

Figure 1: EPF Contributions and Savings, 1995-2002

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 66

Investment PerformanceInvestment Performance

EPF investments are highly regulated EPF investments are highly regulated and restricted to invest in and restricted to invest in government securitiesgovernment securities

in briefin brief

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 77

35.50%

61.03%

0.50%

Rupee Loans

T. Bonds

Equity Shares

Inv. Performance cont.

Figure 2: EPF, Investment Allocation, 2002

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 88

2.0000

4.0000

6.0000

8.0000

10.0000

12.0000

14.0000

16.0000

1959 1964 1969 1974 1979 1984 1989 1994 1999 2004

-20

-15

-10

-5

0

5

10

15

Nominal

Real

Figure 2: EPF, Real and Nominal rates Return, 1960-2002

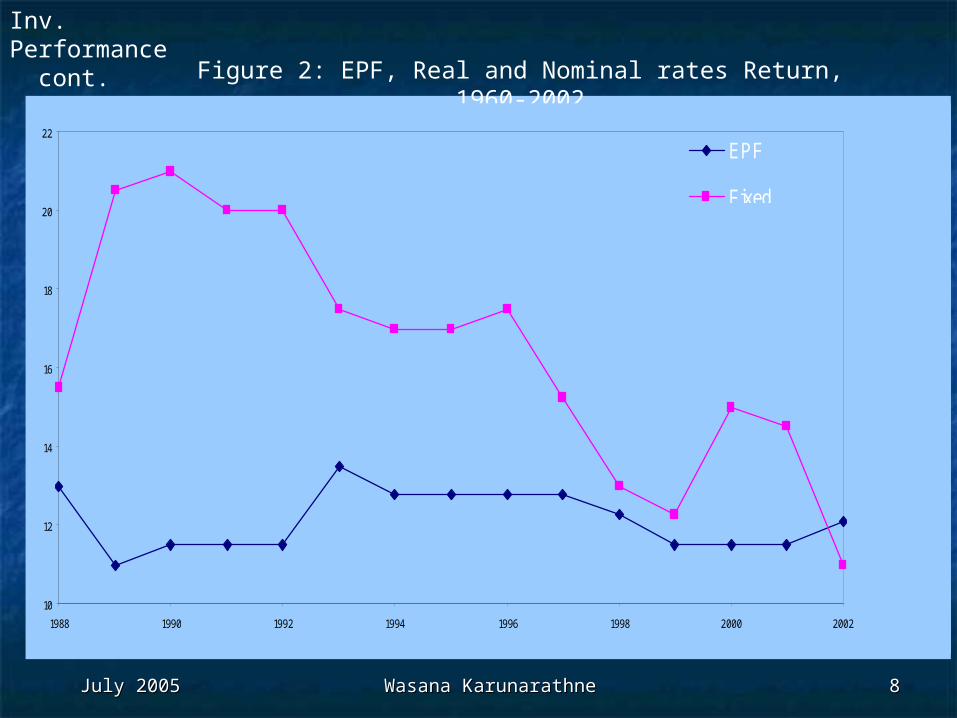

Inv. Performance cont.

10

12

14

16

18

20

22

1988 1990 1992 1994 1996 1998 2000 2002

EPF

FixedDeposits

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 99

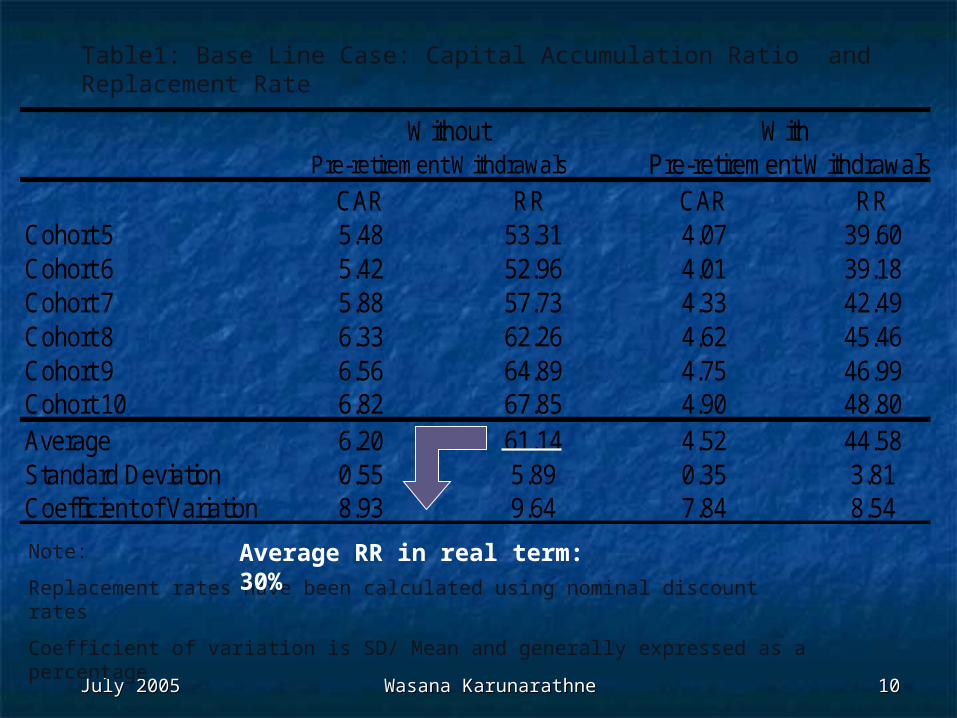

Empirical Findings:Empirical Findings:

Does EPF provide adequate balances? Does EPF provide adequate balances?

The paper calculates The paper calculates

The Capital Accumulation Ratio The Capital Accumulation Ratio (CAR)(CAR)

Replacement Rate (RR)Replacement Rate (RR)

Next slide provides the results under Next slide provides the results under the baseline scenariothe baseline scenario

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 1010

Pre-retirement Withdrawals Pre-retirement WithdrawalsCAR RR CAR RR

Cohort 5 5.48 53.31 4.07 39.60Cohort 6 5.42 52.96 4.01 39.18Cohort 7 5.88 57.73 4.33 42.49Cohort 8 6.33 62.26 4.62 45.46Cohort 9 6.56 64.89 4.75 46.99Cohort 10 6.82 67.85 4.90 48.80Average 6.20 61.14 4.52 44.58Standard Deviation 0.55 5.89 0.35 3.81Coefficient of Variation 8.93 9.64 7.84 8.54

Without With

Note:

Replacement rates have been calculated using nominal discount rates

Coefficient of variation is SD/ Mean and generally expressed as a percentage

Table1: Base Line Case: Capital Accumulation Ratio and Replacement Rate

Average RR in real term: 30%

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 1111

Could the situation be changed, if Could the situation be changed, if EPF used diversified portfolios? EPF used diversified portfolios?

Empirical Findings cont.

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 1212

R Loans T- Bills Stocks Balance 1 Balance 2 Balance 3

100-0-0 0-100-0 0-0-100 60-30-10 20-40-40 10-30-60

Cohort 1 5.58 6.15 19.38 6.87 10.63 13.37 4.50Cohort 2 5.98 6.87 18.06 7.32 10.91 13.30 4.84Cohort 3 6.14 6.87 10.18 6.81 8.84 9.68 4.69Cohort 4 6.14 7.56 8.69 7.16 8.74 9.14 5.06Cohort 5 6.49 7.91 9.42 7.54 9.24 9.73 5.48Cohort 6 6.30 7.74 6.99 7.14 8.10 8.08 5.42Cohort 7 6.79 8.37 6.49 7.57 8.20 7.95 5.88Cohort 8 7.20 9.36 4.92 7.90 7.84 7.08 6.33Cohort 9 7.48 9.74 6.17 8.36 8.77 8.21 6.56Cohort 10 7.76 9.83 7.30 8.69 9.45 9.12 6.82Average 6.58 8.04 9.76 7.54 9.07 9.56 5.56Range 2.18 3.68 14.46 1.88 2.79 6.29 2.32Standard Deviation 0.70 1.27 4.98 0.62 1.02 2.15 0.81Coefficient of Variation 10.69 15.86 51.07 8.22 11.28 22.49 14.63

Base lineCase

Table2: CAR under Diversified portfolio Investments

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 1313

Empirical Findings cont.

Parametric Reform OptionsParametric Reform Options

Available OptionsAvailable Options Reform the investment functionReform the investment function

Increase retirement ageIncrease retirement age

Increase contribution rateIncrease contribution rate

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 1414

Table2: CAR under Diversified portfolio Investments

A. B. C.

Increase Increase Investment

Retirement Contribution Function

Age to 60 Rate Reforms

Balance 2

Cohort 1 4.50 5.84 4.95 10.63 9.17 11.69 6.43 10.09Cohort 2 4.84 6.33 5.33 10.91 9.28 12.00 6.96 10.21Cohort 3 4.69 6.80 5.16 8.84 8.86 9.73 7.47 9.75Cohort 4 5.06 7.03 5.56 8.74 9.89 9.61 7.73 10.88Cohort 5 5.48 7.30 6.03 9.24 10.65 10.17 8.03 11.72Average 4.91 6.66 5.40 9.67 9.57 10.64 7.33 10.53Standard Deviation 0.38 0.58 0.41 1.02 0.71 1.13 0.64 0.78Coefficient of Variation 7.67 8.70 7.67 10.57 7.41 10.57 8.70 7.41

A, B andC together

A and ctogether

B and Ctogether

A and Btogether

Base LineCase (No Pre-retirement Withdrawals)

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 1515

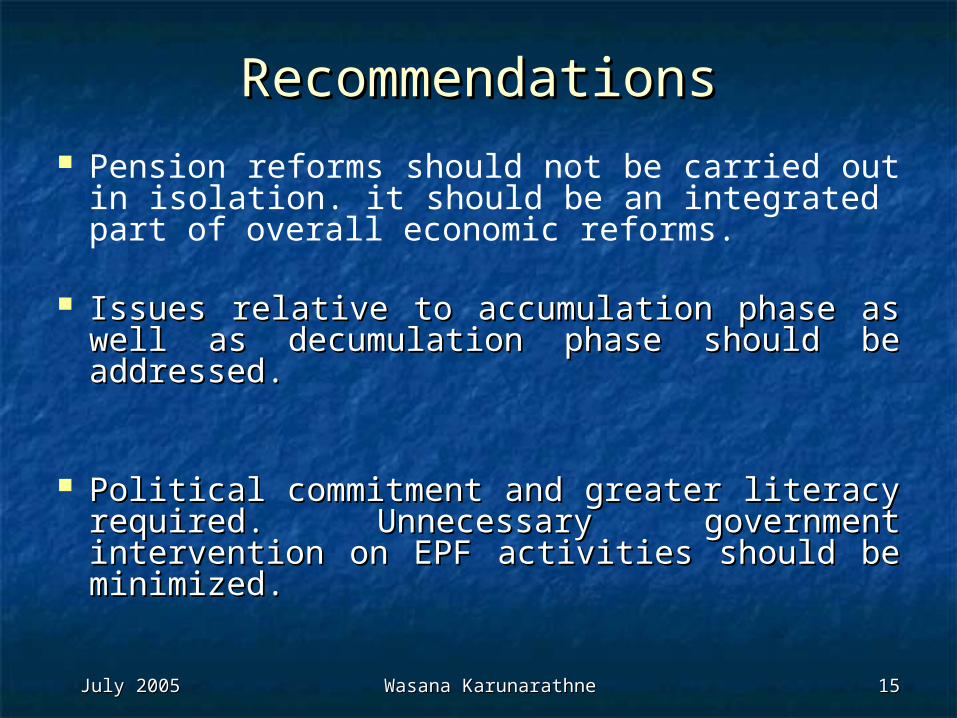

RecommendationsRecommendations Pension reforms should not be carried out in

isolation. it should be an integrated part of overall economic reforms.

Issues relative to accumulation phase as Issues relative to accumulation phase as well as decumulation phase should be well as decumulation phase should be addressed.addressed.

Political commitment and greater literacy Political commitment and greater literacy required. Unnecessary government required. Unnecessary government intervention on EPF activities should be intervention on EPF activities should be minimized. minimized.

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 1616

RecommendationsRecommendations

Enhance the professionalism of the Enhance the professionalism of the management. management.

Improve the investment function. Improve the investment function. Diversify portfolios. Gradually de-link Diversify portfolios. Gradually de-link provident funds from budgetary provident funds from budgetary financing financing

Limit pre-retirement withdrawalsLimit pre-retirement withdrawals

July 2005July 2005 Wasana KarunarathneWasana Karunarathne 1717

Thank Thank you!you!Contacts:Contacts:

Wasana KarunarathneWasana KarunarathneDepartment of EconomicsDepartment of EconomicsUniversity of Melbourne,University of Melbourne,

Economics and Commerce BuildingEconomics and Commerce BuildingVictoria, 3010, AustraliaVictoria, 3010, Australia

Phone: 61 3 8344 5397Phone: 61 3 8344 5397Email: Email: [email protected]@unimelb.edu.au

I would like thank National University of Singapore for financial support provided for my PhD research.