m e s s a g e f r o m t h e - dmf.go.th · dmf’s responsibilities divided into divisional level 5...

TRANSCRIPT

1 2002AnnualR

eport

The year 2002 was a transitional year for government agency in energy sector to berelocated under Ministry of Energy in the line of Bureaucratic Reform. With co-oper-ation between these agencies, the state policy would be able to be implementedmore efficiently to bring great benefit to the people of Thailand.

The Department of Mineral Fuels (DMF) was established to be responsible for theexploration and production of mineral fuels throughout the Kingdom of Thailand aswell as Thailand-Malaysia Joint Development Area. Apart from that, DMF has beenworking on the development and management of the Thailand-Cambodia OverlappingClaimed Area. Negotiation between two countries is going on with satisfactoryprogress.

Thailandûs indigenous resources are very important for energy security. Provenreserve and Production Ratio (R/P) is widely used to monitor how long we can dependon our own resources. On the supply side, gas reserve of Thailand stands at about33.5 Tcf, and on the production side, the daily gas consumption is about 2,000million cubic feet from indigenous production and about 600 million cubic feet fromMyanmar. These give the R/P of about 19. DMF has been enhancing the co-operationbetween government sector and private sector in order to maximize the use of petro-leum fields and, managing the petroleum production. These would maintain the R/Pat a satisfactory level for the sustainable use of indigenous resources.

With dedication and working efficiently under the new strategies, DMF wouldguarantee the energy security and put Thailand on its prestigious position within theASEAN region.

M e s s a g e f r o m t h e

Nopadon Mantajit

Director-GeneralDepartment of Mineral Fuels

Director-General

2 2002AnnualR

eport

Message from the Director-General 1

Contents 2

Highlights 3

The Department of Mineral Fuels 4

● DMF’s obligations and responsibilities 4

● Mission 5

● Vision 5

● DMF’s responsibilities divided into divisional level 5

Benefits 7

Petroleum Balance 12

Petroleum Concessions 16

Petroleum Investment 26

Petroleum Exploration 28

Field Development 30

Petroleum Production 38

Petroleum Enviromental Activities 40

Activities in the Malaysia-Thailand 43

Joint Development Area (MTJDA)

Petroleum Resources && Reserves 47

Coal Activities 51

List of Petroleum Concessionaires 56

Government Agencies, State Enterprises and Institutes 61

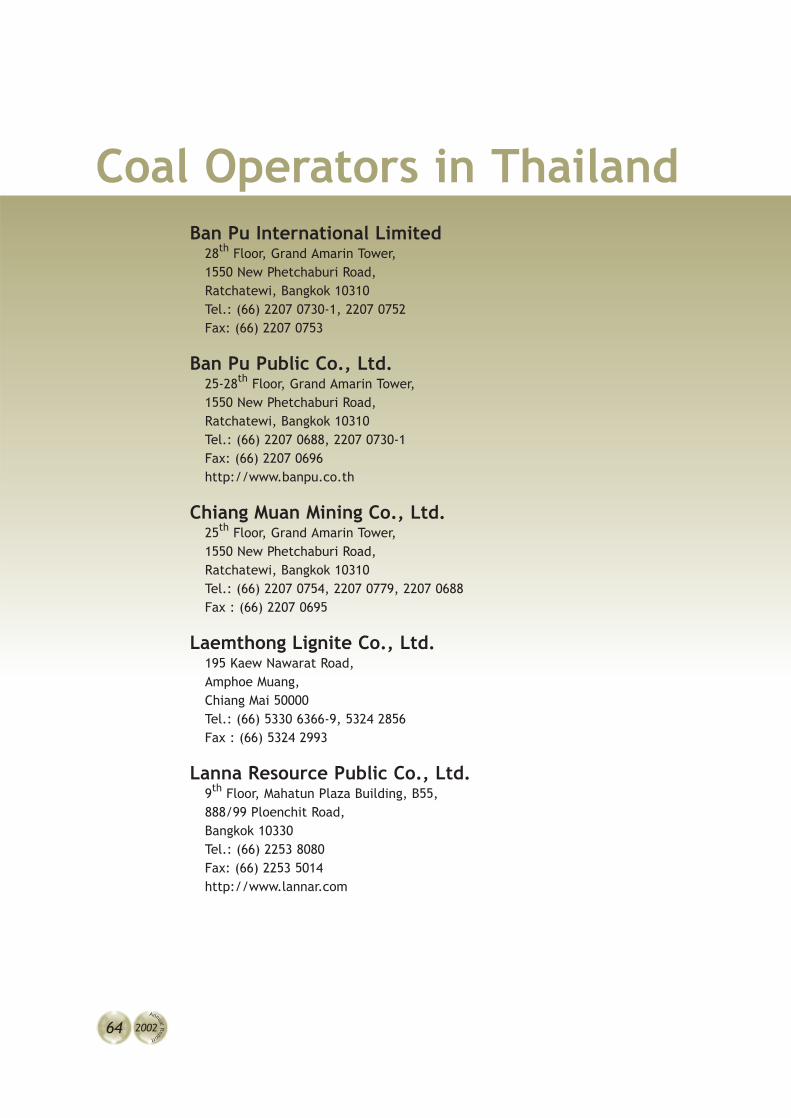

Coal Operations in Thailand 64

Abbreviation 66

Contents

3 2002AnnualR

eport

HighlightsActivities 1999 2000 2001 2002 Unit

Geophysical Surveys• 2D seismic 2,534 493 - 1,128.6 line-km• 3D seismic 1,658 134 827.82 481.5 sq. km

Drilling• exploratory *35 *47 *43 *22 well• development 165 179 155 339 well

New Prospects• number of new prospects 8 7 11 **3

Production (Total Sale)• by 8 8 8 8 concessionaire• from 26 25 26 30 field

• natural gas 678 713 693 726 Bcf• condensate 17.8 19.1 18.9 19.6 MMbbl• oil 12.0 20.9 22.4 27.7 MMbbl

• values 68.58 107.27 116.29 123.49 billion baht• royalties 8.50 13.47 14.6 15.7 billion baht

• royalty allocation to the sub-district 203.43 330.63 342.51 273.48 million bahtadministration organization

• royalty allocation to the provincial 305.14 495.94 434.51 273.48 million bahtadministration organization

Concessions• number of concessions 26 25 25 22• number of concession blocks 33 32 32 29

* Include appraisal wells

** Phuhom-3, Pikul-2x and 11A-2

4 2002AnnualR

eport

For a long time, energy has been an indispensable necessity of dailylife and alsoplayed as an essential catalyst for Thailandûs economic, social and security development.The Thai government, realising the importance of efficient energy management, has initiatedpolicies that enhance domestic supply in order to reduce the degree of reliance of energyimports (especially, promoting natural gas as major energy supply). The policies also emphasizenational energy management to increase the competitiveness of the production sector andcreate energy price stability. To visualize the government policies, the Ministry of Energy wasformed by the unification of all governmental organizations involved in energy sector.

The Mineral Fuels Division was set up under the Department of Mineral Resources,Ministry of Industry, on 17 January 1972 with the obligation to develop Thailandûs energyresources. Thailandûs upstream petroleum industry has been continually developed overthe past 30 years with continual success and, consequently, petroleum has become a majorenergy resource for the nationûs development.

The Mineral Fuels Division, as the only organization managing petroleum explorationand production, was repositioned on 3 October 2002 to be the Department of Mineral Fuelsunder the Ministry of Energy as formalized by the Government Restructuring Act (NO 24) B.E.2545 with obligations and responsibilities to manage the up-stream petroleum industries.

DMFûs obligations and responsibilitiesAccording to the Ministerial Regulation on Reorganization of the Ministry of Energy

B.E.2545, the DMFûs obligations and responsibilitiesare given as follows;

DMF has the duty to promote and accelerate domestic petroleum exploration andproduction, and also to encourage collaboration with neighboring countries.

Such responsibilities include the following matters;

1. Managing and monitoring petroleum concession awards, exploration, production, storage,transportation and selling.

2. Collecting petroleum royalty payments and any other benefits.

3. To co-ordinate with concessionaires, operators and government agencies to ensure thatconcessionaires and operators are working in accordance to the Thai law and regulations.

4. Coal and oil shale exploration and potential evaluation

5. Mineral fuels research and development

6. Collaborating in developing petroleum fields in joint development areas, overlapping areasand other countries in the region.

7. Other matters as assigned by the ministry or the cabinet.

T h e D e p a r t m e n t o f

Mineral Fuels

5 2002AnnualR

eport

MissionTo promote the integration of petroleum exploration, development, production and

management, with more environmentally friendly and international standardized technologies.

VisionThe Department of Mineral Fuels is a first-grade organization administrating and

managing mineral fuel resources to secure and maintain the energy supply.

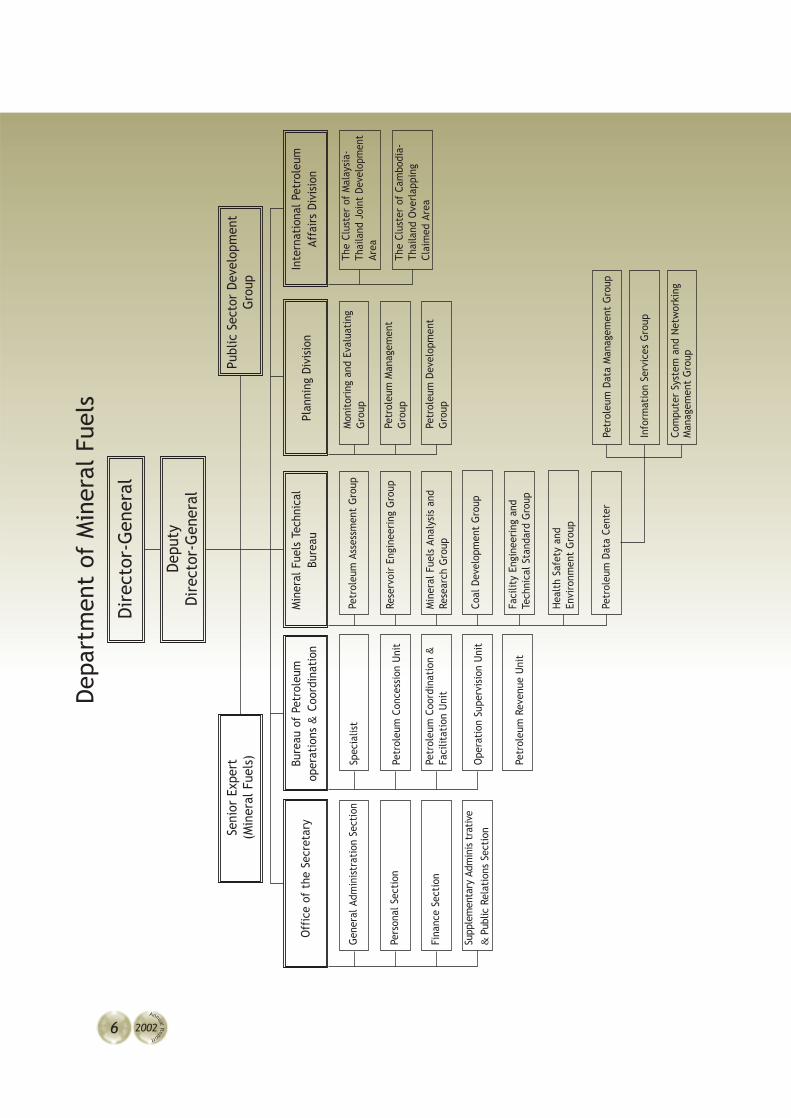

DMFûs responsibilities are divided into divisional levels as follows :• Office of the Secretary

Support executive and internal management who are responsible for departmentalpolicies and plans.

• Bureau of Petroleum Operations and Coordination

Promote and regulate all domestic petroleum exploration and production activitiesincluding concession awards, exploration and production supervision, concessionmanagement and facilitate concessionaireûs affairs as stipulated by law.

• Mineral Fuels Technical Bureau

Technically support the departmentûs responsibilities such as concession awards,exploration and production activities and natural fuels utilization by assessingdomestic natural fuels fields and study safety and environmental impact ofoperations.

• Petroleum Planning Division

Cooperate departmentûs policies and plans leading to effective service and accordingto natural policies by formulate strategic plans which address direction, strategiesand plan assessment.

• International Petroleum Operations Division

Endorse international collaboration in explorationand development of energy resources in the jointdevelopment areas andover-lapping areas bymanaging the operationsin accordance with thelaws and regulations ofThailand.

6 2002AnnualR

eport

Dep

artm

ent

of M

iner

al F

uels

Seni

or E

xper

tPu

blic

Sec

tor

Deve

lopm

ent

(Min

eral

Fue

ls)

Gro

up

Bure

au o

f Pe

trol

eum

oper

atio

ns &

Coor

dina

tion

Spec

ialis

t

Petr

oleu

m C

once

ssio

n U

nit

Petr

oleu

m C

oord

inat

ion

&Fa

cilit

atio

n U

nit

Ope

rati

on S

uper

visi

on U

nit

Petr

oleu

m R

even

ue U

nit

Min

eral

Fue

ls T

echn

ical

Bure

au

Petr

oleu

m A

sses

smen

t G

roup

Rese

rvoi

r En

gine

erin

g G

roup

Min

eral

Fue

ls A

naly

sis

and

Rese

arch

Gro

up

Coal

Dev

elop

men

t G

roup

Faci

lity

Engi

neer

ing

and

Tech

nica

l Sta

ndar

d G

roup

Hea

lth

Safe

ty a

ndEn

viro

nmen

t G

roup

Petr

oleu

m D

ata

Cent

er

Plan

ning

Div

isio

n

Mon

itor

ing

and

Eval

uati

ngG

roup

Petr

oleu

m M

anag

emen

tG

roup

Petr

oleu

m D

evel

opm

ent

Gro

up

Inte

rnat

iona

l Pet

role

umAf

fair

s Di

visi

on

The

Clus

ter

of M

alay

sia-

Thai

land

Joi

nt D

evel

opm

ent

Area

The

Clus

ter

of C

ambo

dia-

Thai

land

Ove

rlap

ping

Clai

med

Are

a

Petr

oleu

m D

ata

Man

agem

ent

Gro

up

Info

rmat

ion

Serv

ices

Gro

up

Com

pute

r Sy

stem

and

Net

wor

king

Man

agem

ent

Gro

up

Dir

ecto

r-G

ener

al

Depu

tyDi

rect

or-G

ener

al

Off

ice

of t

he S

ecre

tary

Gen

eral

Adm

inis

trat

ion

Sect

ion

Pers

onal

Sec

tion

Fina

nce

Sect

ion

Supp

lem

enta

ry A

dmin

is t

rati

ve

& P

ublic

Rela

tion

s Se

ctio

n

7 2002AnnualR

eport

Royalties from petroleum production in 2002 contributed 15.662 billion baht to thecountry. These royalties broke down into 61%, 15% and 24% collected from gas, condensate andoil, respectively. From 2001 to 2002 royalties increased by 7%.

Royalty payments made by onshore concessionaires from onshore blocks are devided asfollows;

• 20% is divided amongst the Sub-District Administration Organizations (SDAO) in the concession areas to be use by the local communities. (Table 1)

• 20% is divided amongst the others SDAOs throughout the country.

• 20% is divided amongst the Provincial Administration Organizations (PAO) within the concession areas.(Table 2)

• The remaining 40% is sent to the treasury.

100% of royalty payments made by concessionaires from offshore blocks are sent to thetreasury.

Benefits

Table 1 :

Block Province Sub-District Administration No. of SDAO Royalty allocation (baht)Organizations (SDAO) Each Subtotal

S1 Kamphaeng Phet Lan Krabu, Nong Luang*, 4 17,802,479 71,209,917Chonglom, Bueng Tab Rat, Non Pluang 1 17,802,479 17,802,479Tesaban Lan Krabu** 1 17,802,479 17,802,479

Phitsanulok Kui Muang, Chum Saeng Songkhram, 4 17,802,479 71,209,917Bung Kok, Nong Kula

Sukhothai Kong, Nong Tum 2 17,802,479 35,604,958NC Kamphaeng Phet Nong Luang* 1 1,197,920 1,197,920

Sukhothai Nong Chik 1 1,197,920 1,197,920E5 Khon Kaen Kudnamsai, Muang Wan, Nam Phong 3 18,389,404 55,168,213

PTTEP 1 Nakhon Pathom Thung Luk Nok 1 597,449 597,449Suphan Buri Suan Taeng, Chedi 2 597,449 1,194,899

SW Phetchabun Si Thep, Na Sanun, Bo Rang 3 122,475 367,425Ta Rong 1 122,475 122,475Total 23 273,476,051

8 2002AnnualR

eport

Block Province No. of Royalty allocation (baht)PAO Each Subtotal

S1 Kamphaeng Phet, Phitsanulok, Sukhothai 3 71,209,917 213,629,751

NC Kamphaeng Phet, Sukhothai 2 1,197,920 2,395,840

E5 Khon Kaen 1 55,168,213 55,168,213

PTTEP 1 Nakhon Pathom, Suphan Buri 2 896,174 1,792,348

SW Phetchabun 1 489,899 489,899

Total 7 273,476,051

Remarks : S1 Thai Shell Exploration and Production Co., Ltd. PTT Exploration and Production Public Co., Ltd.

NC Sino- U.S. Petroleum Inc.Combined Oil and Gas (Thailand) Inc.Thai Energy Resources Ltd.Sino Thai Energy Ltd.

E : Esso Exploration and Production Khorat Inc. PTT Exploration and Production Public Co., Ltd.

PTTEP1 PTTEP International Ltd.SW Pacific Tiger Energy (Thailand) Ltd.* Nong Luang SDAO has been allocated royalty from block S1 and NC.** Tesaban Lan Krabu and Ta Rong SDAO have been allocated royalty

since July, 2002

Table 2 :

9 2002AnnualR

eport

Sales, Value and Royalty of Crude Oil

Petroleum Field 1981-1985 1986-1990 1991-1995 1996-2000 2001 2002 Total

Sirikit (LPG)Sales (MMkg) * 41.10 489.74 107.61 109.60 108.89 1,277.77Value (million baht) 251.51 3,043.86 584.83 1,130.77 985.77 9,224.30Royalty (million baht) 31.44 380.48 73.10 141.35 123.22 1,153.02

Platong Sales (Mbbl) 196.06 888.20 1,084.25Value (million baht) 147.70 984.58 1,132.28Royalty (million baht) 18.46 123.07 141.53

KaphongSales (Mbbl) 176.51 216.28 392.79Value (million baht) 132.28 222.77 355.06Royalty (million baht) 16.54 27.85 44.38

Plamuk Sales (Mbbl) 158.38 1,570.97 1,729.35Value (million baht) 119.28 1,711.34 1,830.62Royalty (million baht) 14.91 213.92 228.83

SuratSales (Mbbl) 2.11 196.15 198.26Value (million baht) 1.67 210.47 212.13Royalty (million baht) 0.21 26.31 26.52

Yala U3Sales (Mbbl) 1,322.88 1,322.88Value (million baht) 1,500.73 1,500.73Royalty (million baht) 187.59 187.59

Sirikit et al.Sales (Mbbl) 14,663.18 35,528.54 39,319.39 6,800.62 7,803.85 7,450.19 142,587.03Value (million baht) 9,616.95 14,942.29 16,217.34 3,174.15 7,570.90 7,142.35 80,093.79Royalty (million baht) 1,202.11 1,867.79 2,027.23 396.77 946.36 892.79 10,011.77

Nang NuanSales (Mbbl) 475.75 1,687.87 1,908.64 0.00 0.00 4,506.46Value (million baht) 156.14 670.76 919.00 0.00 0.00 2,054.03Royalty (million baht) 19.52 83.84 114.88 0.00 0.00 256.74

Kamphang Saen + U-Thong + SangkrajaiSales (Mbbl) 1,826.07 350.91 213.01 215.77 3,525.83Value (million baht) 637.55 154.97 184.43 192.28 1,697.27Royalty (million baht) 31.88 7.75 9.22 9.61 84.37

Bung Ya + Bung MuangSales (Mbbl) 315.70 151.16 314.90 278.58 1,841.20Value (million baht) 112.75 66.96 276.58 247.06 1,183.33Royalty (million baht) 5.64 3.35 13.83 12.35 59.14

Wichian BuriSales (Mbbl) 54.70 101.66 69.01 59.46 572.88Value (million baht) 16.81 37.92 59.09 54.66 328.92Royalty (million baht) 0.84 1.90 2.94 2.73 16.23

TantawanSales (Mbbl) 2,947.39 2,111.64 13,541.97Value (million baht) 3,076.56 2,251.04 12,305.37Royalty (million baht) 413.93 304.13 1,590.90

BenchamasSales (Mbbl) 10,719.23 12,962.01 33,257.47Value (million baht) 11,166.79 13,751.43 36,337.45Royalty (million baht) 1,484.85 1,863.12 4,838.26

TotalSales (Mbbl) 14,663.18 36,004.29 43,203.73 60,816.62 22,600.44 27,272.11 204,560.37Value (million baht) 9,616.95 15,349.94 20,699.06 49,468.80 23,866.06 29,254.47 148,255.29Royalty (million baht) 1,202.11 1,918.74 2,529.91 6,139.24 3,062.60 3,786.70 18,639.29

* LPGû s sales not included in total salesPlatong, Kaphong, Kaphong, Plamuk and Surat started in 2001

10 2002AnnualR

eport

Sales, Value and Royalty of Condensate

Petroleum Field 1981-1985 1986-1990 1991-1995 1996-2000 2001 2002 Total

ErawanSales (Mbbl) 9,494.31 12,607.63 16,550.49 16,693.46 3,260.08 2,942.76 61,548.73Value (million baht) 6,625.16 5,632.17 7,457.98 11,219.09 3,348.09 2,910.39 37,192.88Royalty (million baht) 828.17 688.84 932.25 1,402.37 418.51 363.80 4,633.93

BaanpotSales (Mbbl) 1,005.31 2,106.17 727.86 963.40 83.96 122.28 5,008.98Value (million baht) 693.72 920.18 426.28 632.60 86.43 119.19 2,878.40Royalty (million baht) 86.71 113.21 53.28 79.06 10.80 14.90 357.98

Satun + South SatunSales (Mbbl) 976.98 9,309.86 14,301.36 14,334.32 1,869.01 1,546.32 42,337.85Value (million baht) 731.41 4,193.19 6,382.73 9,345.74 1,920.37 1,518.78 24,092.22Royalty (million baht) 91.42 552.07 797.83 1,168.19 240.06 189.85 3,039.41

Platong + KaphongSales (Mbbl) 1,119.40 7,290.49 4,548.15 7,432.73 560.54 174.90 21,126.21Value (million baht) 835.33 3,196.25 2,075.23 4,905.50 617.05 177.16 11,806.52Royalty (million baht) 104.42 392.53 259.40 613.13 77.13 22.14 1,468.78

FunanSales (Mbbl) 8,950.21 8,268.55 1,922.32 2,385.35 21,526.43Value (million baht) 3,912.72 5,606.69 1,946.91 2,366.93 13,833.24Royalty (million baht) 489.08 700.82 243.36 295.87 1,729.13

JakrawanSales (Mbbl) 362.64 3,395.74 491.70 441.12 4,691.20Value (million baht) 148.31 2,411.96 623.79 431.65 3,615.71Royalty (million baht) 18.53 301.47 77.97 53.96 451.94

SuratSales (Mbbl) 979.75 620.63 0 0 1,600.38Value (million baht) 412.12 364.68 0 0 776.81Royalty (million baht) 51.52 45.84 0 0 97.36

GominSales (Mbbl) 63.31 3,330.37 221.68 228.13 3,843.48Value (million baht) 25.45 2,060.29 226.39 222.69 2,534.83Royalty (million baht) 3.18 257.51 27.14 27.84 315.67

Pladang + TratSales (Mbbl) 2,430.88 1,291.11 1,152.83 4,874.83Value (million baht) 2,068.41 1,319.19 1,133.93 4,521.53Royalty (million baht) 258.53 164.90 141.74 565.18

PlamukSales (Mbbl) 146.36 0.90 0 147.27Value (million baht) 119.60 0.93 0 120.53Royalty (million baht) 14.94 0.12 0 15.06

PailinSales (Mbbl) 5,290.09 2,956.11 4,044.38 12,290.58Value (million baht) 4,879.21 3,066.88 4,150.15 12,096.24Royalty (million baht) 609.51 383.36 518.77 1,511.64

BongkotSales (Mbbl) 3,242.56 20,561.10 6,098.33 5,666.41 35,568.40Value (million baht) 1,303.19 14,464.83 6,168.21 5,584.53 27,520.76Royalty (million baht) 162.89 1,808.09 771.03 698.07 3,440.07

TotalSales (Mbbl) 12,595.99 31,314.14 49,726.33 83,467.63 18,755.73 18,704.48 214,564.34Value (million baht) 8,885.63 13,941.79 22,144.01 58,078.60 19,324.23 18,615.40 140,989.67Royalty (million baht) 1,110.72 1,746.65 2,767.98 7,259.46 2,414.37 2,326.94 17,626.15

11 2002AnnualR

eport

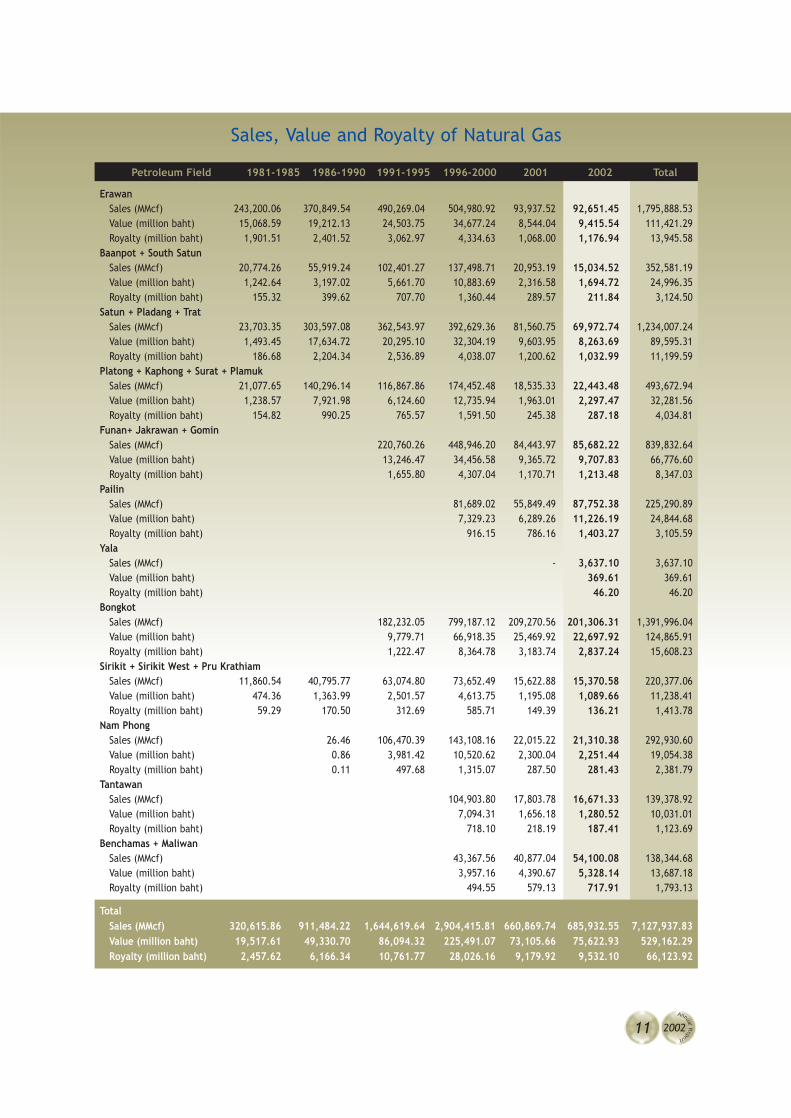

Sales, Value and Royalty of Natural Gas

Petroleum Field 1981-1985 1986-1990 1991-1995 1996-2000 2001 2002 Total

ErawanSales (MMcf) 243,200.06 370,849.54 490,269.04 504,980.92 93,937.52 92,651.45 1,795,888.53Value (million baht) 15,068.59 19,212.13 24,503.75 34,677.24 8,544.04 9,415.54 111,421.29Royalty (million baht) 1,901.51 2,401.52 3,062.97 4,334.63 1,068.00 1,176.94 13,945.58

Baanpot + South SatunSales (MMcf) 20,774.26 55,919.24 102,401.27 137,498.71 20,953.19 15,034.52 352,581.19Value (million baht) 1,242.64 3,197.02 5,661.70 10,883.69 2,316.58 1,694.72 24,996.35Royalty (million baht) 155.32 399.62 707.70 1,360.44 289.57 211.84 3,124.50

Satun + Pladang + TratSales (MMcf) 23,703.35 303,597.08 362,543.97 392,629.36 81,560.75 69,972.74 1,234,007.24Value (million baht) 1,493.45 17,634.72 20,295.10 32,304.19 9,603.95 8,263.69 89,595.31Royalty (million baht) 186.68 2,204.34 2,536.89 4,038.07 1,200.62 1,032.99 11,199.59

Platong + Kaphong + Surat + PlamukSales (MMcf) 21,077.65 140,296.14 116,867.86 174,452.48 18,535.33 22,443.48 493,672.94 Value (million baht) 1,238.57 7,921.98 6,124.60 12,735.94 1,963.01 2,297.47 32,281.56Royalty (million baht) 154.82 990.25 765.57 1,591.50 245.38 287.18 4,034.81

Funan+ Jakrawan + GominSales (MMcf) 220,760.26 448,946.20 84,443.97 85,682.22 839,832.64Value (million baht) 13,246.47 34,456.58 9,365.72 9,707.83 66,776.60Royalty (million baht) 1,655.80 4,307.04 1,170.71 1,213.48 8,347.03

PailinSales (MMcf) 81,689.02 55,849.49 87,752.38 225,290.89Value (million baht) 7,329.23 6,289.26 11,226.19 24,844.68Royalty (million baht) 916.15 786.16 1,403.27 3,105.59

YalaSales (MMcf) - 3,637.10 3,637.10Value (million baht) 369.61 369.61Royalty (million baht) 46.20 46.20

BongkotSales (MMcf) 182,232.05 799,187.12 209,270.56 201,306.31 1,391,996.04Value (million baht) 9,779.71 66,918.35 25,469.92 22,697.92 124,865.91Royalty (million baht) 1,222.47 8,364.78 3,183.74 2,837.24 15,608.23

Sirikit + Sirikit West + Pru KrathiamSales (MMcf) 11,860.54 40,795.77 63,074.80 73,652.49 15,622.88 15,370.58 220,377.06Value (million baht) 474.36 1,363.99 2,501.57 4,613.75 1,195.08 1,089.66 11,238.41Royalty (million baht) 59.29 170.50 312.69 585.71 149.39 136.21 1,413.78

Nam PhongSales (MMcf) 26.46 106,470.39 143,108.16 22,015.22 21,310.38 292,930.60Value (million baht) 0.86 3,981.42 10,520.62 2,300.04 2,251.44 19,054.38Royalty (million baht) 0.11 497.68 1,315.07 287.50 281.43 2,381.79

TantawanSales (MMcf) 104,903.80 17,803.78 16,671.33 139,378.92Value (million baht) 7,094.31 1,656.18 1,280.52 10,031.01Royalty (million baht) 718.10 218.19 187.41 1,123.69

Benchamas + MaliwanSales (MMcf) 43,367.56 40,877.04 54,100.08 138,344.68Value (million baht) 3,957.16 4,390.67 5,328.14 13,687.18Royalty (million baht) 494.55 579.13 717.91 1,793.13

TotalSales (MMcf) 320,615.86 911,484.22 1,644,619.64 2,904,415.81 660,869.74 685,932.55 7,127,937.83Value (million baht) 19,517.61 49,330.70 86,094.32 225,491.07 73,105.66 75,622.93 529,162.29Royalty (million baht) 2,457.62 6,166.34 10,761.77 28,026.16 9,179.92 9,532.10 66,123.92

12 2002AnnualR

eport

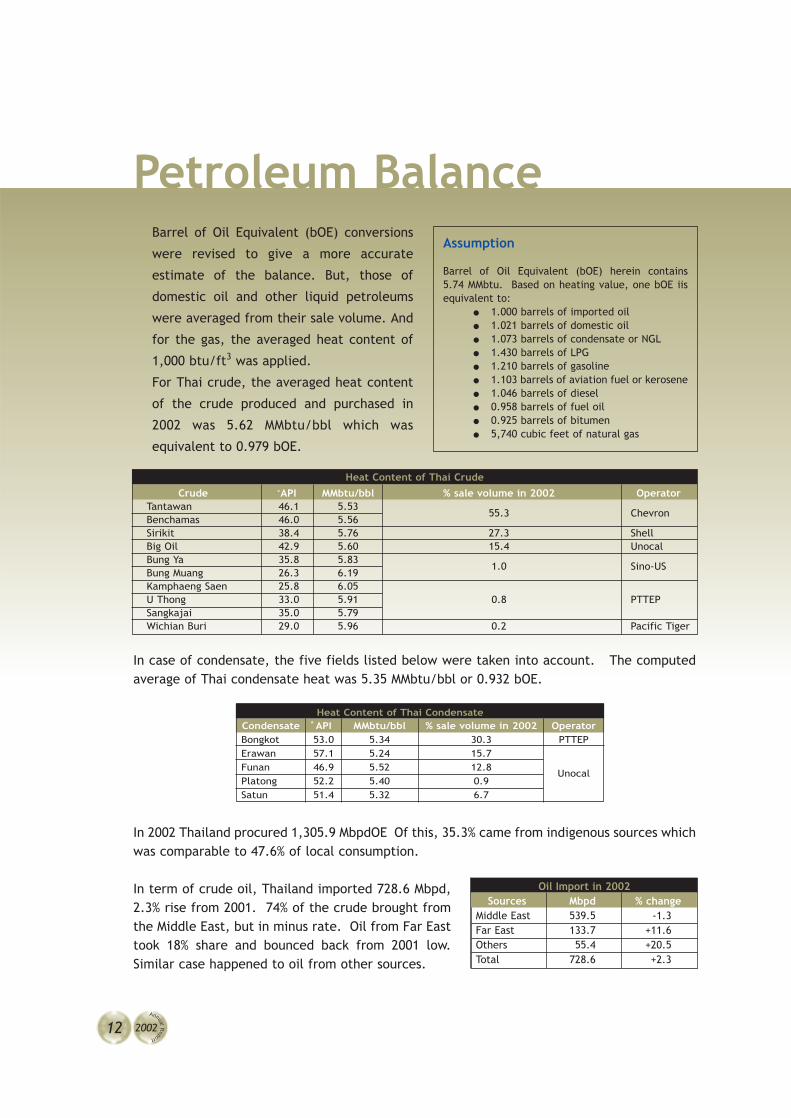

Petroleum BalanceAssumption

Barrel of Oil Equivalent (bOE) herein contains5.74 MMbtu. Based on heating value, one bOE iisequivalent to:

● 1.000 barrels of imported oil● 1.021 barrels of domestic oil● 1.073 barrels of condensate or NGL● 1.430 barrels of LPG● 1.210 barrels of gasoline● 1.103 barrels of aviation fuel or kerosene● 1.046 barrels of diesel● 0.958 barrels of fuel oil● 0.925 barrels of bitumen● 5,740 cubic feet of natural gas

Barrel of Oil Equivalent (bOE) conversions

were revised to give a more accurate

estimate of the balance. But, those of

domestic oil and other liquid petroleums

were averaged from their sale volume. And

for the gas, the averaged heat content of

1,000 btu/ft3 was applied.

For Thai crude, the averaged heat content

of the crude produced and purchased in

2002 was 5.62 MMbtu/bbl which was

equivalent to 0.979 bOE.

In case of condensate, the five fields listed below were taken into account. The computedaverage of Thai condensate heat was 5.35 MMbtu/bbl or 0.932 bOE.

Heat Content of Thai CondensateCondensate ÌAPI MMbtu/bbl % sale volume in 2002 OperatorBongkot 53.0 5.34 30.3 PTTEPErawan 57.1 5.24 15.7

UnocalFunan 46.9 5.52 12.8Platong 52.2 5.40 0.9Satun 51.4 5.32 6.7

Oil Import in 2002Sources Mbpd % change

Middle East 539.5 -1.3Far East 133.7 +11.6Others 55.4 +20.5Total 728.6 +2.3

In term of crude oil, Thailand imported 728.6 Mbpd,2.3% rise from 2001. 74% of the crude brought fromthe Middle East, but in minus rate. Oil from Far Easttook 18% share and bounced back from 2001 low.Similar case happened to oil from other sources.

In 2002 Thailand procured 1,305.9 MbpdOE Of this, 35.3% came from indigenous sources whichwas comparable to 47.6% of local consumption.

Heat Content of Thai Crude

Crude ÌAPI MMbtu/bbl % sale volume in 2002 OperatorTantawan 46.1 5.53

55.3 ChevronBenchamas 46.0 5.56Sirikit 38.4 5.76 27.3 ShellBig Oil 42.9 5.60 15.4 UnocalBung Ya 35.8 5.83

1.0 Sino-USBung Muang 26.3 6.19Kamphaeng Saen 25.8 6.05

0.8 PTTEPU Thong 33.0 5.91Sangkajai 35.0 5.79Wichian Buri 29.0 5.96 0.2 Pacific Tiger

13 2002AnnualR

eport

By country, the number of suppliers decreased from 23 to 18 in 2001. Middle East was still amajor source of oil for Thailand, but, in lower rate. In contrast, oil coming from Africa wasapparently growing, especially from Angola. Three of the new oil suppliers this year wereEquatorial Guinea, South Africa and Myanmar.

Oil Import by Country of Origin

No. Country2001 2002

Million liters % Million liters %1 UAE (1) 9,072 22.0 8,934 21.132 Oman (2) 7,942 19.2 8,452 19.993 Saudi Arabia (3) 6,149 14.9 5,586 13.214 Yemen (4) 4,582 11.1 4,735 11.205 Brunei (6) 2,977 7.2 3,075 7.276 Malaysia (5) 3,677 8.9 3,013 7.137 Qatar (8) 1,362 3.5 2,746 6.498 Indonesia (11) 505 1.2 1,738 4.119 Angola (14) 302 0.7 1,169 2.76

10 Iraq (9) 608 1.5 544 1.2911 Kuwait (7) 1,739 4.2 495 1.1712 Nigeria (16) 157 0.4 468 1.1113 Australia (10) 555 1.3 412 0.9714 Equatorial Guinea - - 314 0.7415 Vietnam (12) 372 0.9 230 0.5416 South Africa - - 164 0.3917 Pakistan (20) 33 0.1 138 0.3318 Myanmar - - 67 0.1619 Congo (former Zaire) (13) 324 0.8 - -20 Papua New Guinea (15) 212 0.5 - -21 Ecuador (17) 145 0.4 - -22 Russia (18) 140 0.3 - -23 China (19) 84 0.2 - -24 Japan (21) 29 0.1 - -25 Ukraine (22) 27 0.1 - -26 Singapore (23) 27 0.1 - -

Total 41,329 100.0 42,280 100.00

Number in bracket is the rank in 20011 barrel = 158.99 liters

Source: PTIT

Domestic production was up by 22%, and export alsogrew up 37%, compared to the total import, itûs netimport continued expanding.

After reaching zero export in 2001, again Thailandshipped out around 5,000 barrels a day of condensateduring the year.

Net Oil Import2000 2001 2002

Total import 643.5 680.0 728.6Total export 27.5 36.5 47.9Net import 616.0 643.5 680.5

Unit in MbpdOE

14 2002AnnualR

eport

Gas production increased by 4%. The increment was less than of the imported gas (16%).Deducted from petrochemical use, gas for fuelling shrinked around 3%. Most reductionmainly caused by 11% down of IPP and SPP consumption.

Refined Products

ItemImport Production Consumption Export

2001 2002 2001 2002 2001 2002 2001 2002LPG - - 101.4 101.6 76.4 78.8 24.2 21.7Gasoline 2.5 3.9 143.3 142.2 118.2 126.2 25.5 21.2Kerosene - - 10.1 9.5 1.0 1.1 6.8 5.5Jet Fuel 0.1 0.9 71.4 80.4 64.0 65.1 8.4 15.9Diesel 5.5 12.2 286.5 299.4 262.3 277.1 28.4 40.2Fuel Oil - - 110.1 102.8 78.1 82.4 26.5 13.2Bitumen 0.0 0.0 19.4 16.1 14.7 14.0 5.0 2.5

Unit in Mbpd

In terms of refined products, Thailand seemed to be a producer, importing crude oil, refiningit and using most of the production domestically. Thailand has exported petroleum productsmuch more than of its import for many years.

In 2002, changes varied differently in many items. LPG has no import for third year in a row.Its production as well as consumption went up in the same direction.

Gasoline and diesel, extensively used in transportation, kept growing. Uses nationwide wentup by 7% for gasoline and around 6% for diesel. Growth in consumption, production, importand export of diesel exceeded any other refined product in 2002.

Acted obviously as a kerosene supplier, Thailand used domestically only one fifth of its pro-duction in 2002.

Domestic Petroleum Substitution1997 1998 1999 2000 2001 2002

Domestic Production 333.6 350.9 385.6 429.1 429.7 461.1

Local Consumption 897.0 840.2 863.6 940.3 952.6 967.9

% Substitution 37.2 41.8 44.7 45.6 45.1 47.6

Unit in MbpdOE

The development of petroleum resources clearly benefit Thailand, as has been evidenced.

15 2002AnnualR

eport

THAI

LAN

Dû s

PETR

OLE

UM

BAL

ANCE

S (J

anua

ry-D

ecem

ber

2002

)

Uni

t :

Mbp

dOE

Sour

ce :

PT

IT

16 2002AnnualR

eport

Petroleum ConcessionsChronology of the 18th Petroleum Concession Bidding Round

For the 18th Bidding Round as announced on 11 July 2000, international oil companies wereinvited to apply for rights to explore and produce petroleum in any of 87 exploration blocksin Thailand. The submission period will be 3 years from the date of the Announcement (11 July2000 - 10 July 2003). Round of submission will be before the 15th of each month.

15 August 2000 5 oil companies submitted their applications as follows:Thai Shell/PTTEP applied for onshore Blocks L10/43, L11/43, L21/43and L22/43Harrods Energy applied for offshore Block G4/43CNPC (Hong Kong) applied for onshore Block L21/43Pacific Tiger applied for onshore Block L44/43Chevron applied for offshore Block G4/43Status Submitting for final approval by the Cabinet, 4 Blocks shall

be awarded to 4 oil companies as follows:L22/43 to Thai Shell/PTTEPL21/43 to CNPCL44/43 to Pacific TigerG4/43 to Chevron

15 March 2002 SVS Energy applied for onshore Block L71/43NuCoastal applied for offshore Block G5/43Pacific Tiger applied for onshore Block L33/43Status Submitting for final approval by the Cabinet, 3 Blocks shall

be awarded to 3 oil companies as follows:L71/43 to SVS EnergyG5/43 to NuCoastalL33/43 to Pacific Tiger

15 September 2002 NuCoastal applied for onshore Blocks L15/43 and L27/43Status Under the consideration of the Petroleum Committee

New Production Areas8 PLAs were granted to 6 Concessionaires as follows:

PLA Concessionaire Block Sq. Km. Approved Date

West YalaUnocal

B10 105.99 23 Apr 02

Greater Funan B12, B13 426.82

Jasmine Harrods B5/27 48.6388 30 Sep 02

Ton Rang PTT E&P B15 18.2784 30 Sep 02

Sang KajaiPTTEP Intû l

PTTEP1 1.98 8 May 02

Pikul B13/38 1.9264 30 Sep 02

South Pradoo Tao Thai Shell S1 90.4340 30 Sep 02

Wichian Buri Licence II Pacific Tiger SW1A 8.6411 30 Sep 02

17 2002AnnualR

eport

Unocal Thailand Limited planned to produce natural gas from West Yala at the rate of9 MMscf/d toward to the peak rate of 65 MMscf/d in 2005. The production of condensateand oil are expected at the peak rate of 4,300 bbl/d in first year. The production periodwill be 16 years. With regard to Greater Funan, Unocal planned to produce natural gas andcondensate at the rate of 185 MMscf/d and 6,200 bbl/d respectively. The production periodwill be 17 years.

Harrods Energy (Thailand) Limited planned to produce oil from Jasmine at the rate of 12,000bbl/d in early 2005 toward to the peak rate of 22,000 bbl/d in April 2006. The productionwill then decline and be completed in 2010.

PTT Exploration and Production Public Company Limited planned to share the productionfacilities with Bongkot Field for Ton Rangûûs production. The production of natural gas andcondensate are expected at the rate of 85 MMscf/d and 847 bbl/d respectively in 2003 thendecline and be completed in 2008.

PTTEP International Limited planned to produce oil with natural pressure from Sang Kajai atthe rate of 420 bbl/d for one year then using rod pump until completed the production in mid2006. With regard to Pikul, PTTEP planned to share the production facilities with BongkotField. The production of natural gas and condensate are expected at the rate of 20 MMscf/dand 200 bbl/d respectively in 2004 then decline and be completed in 2008.

Thai Shell Exploration and Production Company Limited planned to produce oil from SouthPradoo Tao with existing production equipment at the rate of 1,300 bbl/d toward the peakrate of 2,700 bbl/d. The production will then decline and be completed in 2013.

Pacific Tiger Energy (Thailand) Limited planned to produce oil from Wichian Buri Licence IIat the peak rate of 110 bbl/d in 2005. The production period will be 10 years.

18 2002AnnualR

eport

Bidding Areas

19 2002AnnualR

eport

Gulf of Thailand

1/ 2514 Thailand Blocks 5 and 6 LLC 50.00 B5 4,645.00 - -26 Nov 71 Idemitsu Oil & Gas Co., Ltd. 50.00 B6 5,510.00 - -

1/2515/5 Gas Sale Agreement No.2 (Unit Area I)1 Mar 72 Unocal Thailand, Ltd. (Operator) 70.00 B10 - 277.62 637.8924

Mitsui Oil Exploration Co., Ltd. 30.00 B11 - 213.02 977.6055

Gas Sale Agreement No.2 (Supplementary) (Unit Area II)Unocal Thailand, Ltd. (Operator) 71.25Mitsui Oil Exploration Co., Ltd. 23.75PTT Exploration and Production Public Co., Ltd. 5.00

Thailand-Cambodia Overlapping AreaUnocal Thailand, Ltd. (Operator) 60.00 B10 1,382.90 - -Mitsui Oil Exploration Co., Ltd. 40.00 B11 1,401.49 - -

17 Dec 97 Unocal Thailand, Ltd. (Operator) 60.00 B10A 166.00 - -Sup.No 9 Mitsui Oil Exploration Co., Ltd. 40.00 B11A 88.00 - -

2/2515/6 Gas Sale Agreement No.11Mar 72 Unocal Thailand, Ltd. (Operator) 80.00 B12 - 1,077.45 196.71

Mitsui Oil Exploration Co., Ltd. 20.00 B13 - 292.88 896.375

Gas Sale Agreement No.2 (Unit Area I)Unocal Thailand, Ltd. (Operator) 70.00Mitsui Oil Exploration Co., Ltd. 30.00

Gas Sale Agreement No.2 (Supplementary) (unit Area II)Unocal Thailand, Ltd. (Operator) 71.25Mitsui Oil Exploration Co., Ltd. 23.75PTT Exploration and Production Public Co., Ltd. 5.00

8 Jun 99 Thailand-Cambodia Overlapping AreaSup.No6 Unocal Thailand, Ltd. (Operator) 80.00 B12 (A) 294.00 - -

Mitsui Oil Exploration Co., Ltd. 20.00 B12 (B) 125.00 - -B13

3/2515/7 PTT Exploration and Production Public Co.,Ltd.(Operator) 44.45 B16 - 421.66 981.458 Mar 72 Total FinaElf E&P Thailand 33.33 B17 - 105.00 413.38

British Gas Thailand PTE Ltd. 22.22

1 June 98 PTT Exploration and Production Public Co., Ltd.(Operator) 80.00 B16A 719.00 - -Unocal Thailand, Ltd. 16.00Moeco Thailand Co.,Ltd. 4.00

4/2515/8 Thailand-Cambodia Overlapping Area9 Mar 72 British Gas Asia Inc. (Operator) 50.00 B7 4,760.00 - -

Chevron Overseas Petroleum Thailand Ltd. 33.33 B8 3,400.00 - -Petroleum Resources (Thailand) Pty., Ltd. 16.67 B9 2,260.00 - -

5/ 2515/9 PTT Exploration and Production Public Co.,Ltd.(Operator) 44.45 B15 - 272.2784 1,006.7210 Mar 72 Total FinaElf E&P Thailand 33.33

British Gas Thailand PTE Ltd. 22.22

1 June 98 PTT Exploration and Production Public Co., Ltd.(Operator) 80.00 B14A 1,887.00 - -Unocal Thailand, Ltd. 16.00Moeco Thailand Co., Ltd. 4.00

1 June 98 PTT Exploration and Production Public Co.,Ltd.(Operator) 80.00 B15A 1,460.00 - -Unocal Thailand ,Ltd. 16.00Moeco Thailand Co.,Ltd. 4.00

3/2528/28 Thai Shell Exploration and Production Co.,Ltd. 100.00 B6/27 - 4.00 1,302.606 Feb 85

Petroleum Concessionaires in Thailand(as of 31 December 2002)

Concess. No.Concessionaire (s) (as of Jan 2003)

ShareBlock

Concession area (sq. km)

Date of Issue (%) Exploration Production Reserves

20 2002AnnualR

eport

1/2529/33 Unocal Thailand, Ltd. (Operator) 35.00 B12/27 - 1,429.73 1,687.7115 Jan 86 PTT Exploration and Production Public Co.,Ltd. 45.00

Amerada Hess (Thailand) Co., Ltd. 15.00MOECO Thai Oil Development Co.,Ltd. 5.00

1/2532/35 Harrods Energy (Thailand) Ltd. 100.00 B5/27 - 48.6388 -9 Aug 89

6/2534/41 Chevron Offshore (Thailand) Ltd. (Operator) 31 2/3 B8/32 - 1,282.85 1,330.9211 Sep 91 Thaipo Ltd. 31 2/3

B 8/32 Partners Ltd. 31 2/3Palang Sophon Limited 5.00Tantawan Production AreaChevron Offshore (Thailand) Ltd. (Operator) 46.34 B8/32 - 274.70 -Thaipo Ltd. 46.34Palang Sophon Limited 7.32

6/2534/41 Unocal Petroleum Ltd. (Operator) 80.00 B10/32 - 5.06 252.286411 Sep 91 Mitsui Oil Exploration Co., Ltd. 20.00

1/2535/45 Harrods Energy (Thailand) Ltd. (Operator) 74.07 B12/32 2,715.08 121.92 -12 Mar 92 Songkhla Resources Ltd. 25.93

2/2539/49 PTTEP International Ltd. (Operator) 44.45 B13/38 161.63 1.9264 -27 Jun 96 TotalFinaElf E&P Thailand 33.33

Thai Energy Co., Ltd. 22.223/2539/50 Soco Exploration (Thailand) Co., Ltd. 50.00 B8/38 2,394.28 - -24 Oct 96

4/2539/51 Harrods Energy (Thailand) Ltd. 100.00 B11/38 2,165.00 - -28 Oct 96

1/2542/57 Devon Energy (Thailand) Ltd. 100.00 B7/38 9,238.00 - -03 Mar 99Onshore

1/2522/16 Thai Shell Exploration and Production Co.,Ltd.(Operator) 75.00 S1 - 189.604 1,136.6115 Mar 79 PTT Exploration and Production Public Co., Ltd. 25.00

2/2522/17 Namphong Area16 Mar 79 ExxonMobil Exploration and Production Khorat Inc. 80.00 E5 - 34.40 34.54

(Operator)PTT Exploration and Production Public Co., Ltd. 20.00Outside Namphong AreaAmerada Hess (Thailand) Co., Ltd. (Operator) 80.00 E5 - - 39.31PTT Exploration and Production Public Co., Ltd. 20.00

1/2524/19 Amerada Hess (Thailand) Co., Ltd. 100.00 EU1 - 1.96 190.933 Jun 81

1/2526/23 Sino-U.S. Petroleum Inc. (Operator) 33.33 NC - 11.244 -12 Apr 83 Combined Oil and Gas (Thailand) Inc. 33.33

Thai Energy Resources Ltd. 16.67Sino Thai Energy Ltd. 16.67

1/2527/24 Pacific Tiger Energy (Thailand) Ltd. 100.00 SW1A - 14.4611 -24 Jul 84

2/2528/27 PTTEP International Ltd. 100.00 PTTEP1 - 9.04 -5 Feb 85

Concess. No.Concessionaire (s) (as of Jan 2003)

ShareBlock

Concession area (sq. km)

Date of Issue (%) Exploration Production Reserves

Joint Development Area (MTJA)1. CTOC Block A-182. CPOC Block B-17, C-19

Area Concessions BlocksGulf of Thailand 16 23Onshore 6 6Total 22 29

Exploration Production ReserveOnshore - 260.7091 1,401.39Gulf of Thailand 45,243.38 5,828.73 10,708.65Total 45,243.38 6,089.44 12,110.0411

Total Concession Areas (sq.km.)

Total Petroleum Concessions In Thailand (as of 31 December 2002)

21 2002AnnualR

eport

Thailand Onshore Petroleum Concession Map (As of January 2003)

22 2002AnnualR

eport

Thailand Offshore Petroleum Concession Map (As of January 2003)

23 2002AnnualR

eport

Granted Petroleum Production Areas in Thailand(as of 31 December 2002)

Operator Production Area Name Issued Area IssuedConcession No. No. Block (sq. km) Date

Offshore (Gulf of Thailand)

PTT Exploration && Production Public Co., Ltd.3/2515/7 1 Bongkot 16B B16 280.0000 18 Mar 83

2 Bongkot 16E 40.0000 17 May 833 Bai Bua - 1 101.6590 16 Sep 974 Bongkot 17E B17 105.0000 17 May 83

PTT Exploration && Production Public Co., Ltd.5/2515/9 5 Bongkot 15B B15 254.0000 16 Aug 82

6 Tonsak 187.0900 6 Feb 017 Ton Rang 18.2784 30 Sep 02

Chevron Offshore (Thailand) Ltd1/2534/36 8 Tantawan B8/32 274.6670 23 Aug 95

9 Benchamas & Pakrakrong 411.1500 16 Jun 9710 Maliwan 368.5000 3 Nov 9711 North Jarmjuree 503.2000 2 Nov 00

Thai Shell Exploration && Production Co., Ltd.3/2528/28 12 Nang Nuan A02 B6/27 2.0000 24 Nov 87

13 Nang Nuan B01 2.0000 10 Feb 93

Unocal Thailand, Ltd.1/2515/5 14 Platong Area 1 B10 49.4800 29 Oct 82

15 Kaphong Area 2 32.8000 24 Oct 8316 Platong Area 0.2500 4 Dec 8417 Kaphong Area 2-Extension 17.0000 17 May 8918 Surat Area 3 7.5800 8 Apr 9119 Platong F Platform 1.7540 22 Apr 9420 Surat Area 5 1.9920 27 May 9421 Plamuk Area 6 50.0710 15 Sep 9722 Platong H Platform Area 7 7.1370 3 Nov 9723 Kaphong A Platform Area 8 3.3868 3 Mar 9924 West Yala 105.99 23 Apr 0225 North Pladang Area 2 B11 2.0000 29 Oct 8226 Pladang Area 3 40.2400 29 Oct 8227 Satun Area 1 3.2200 29 Oct 8228 Platong Area 2 11.0900 29 Oct 8229 Trat Area 5 2.0000 11 Jan 8330 Pakarang Area 6 2.0000 11 Jan 8331 Platong Area 2-Extension 1.7500 4 Dec 8432 Satun Area 1-Extension 20.5300 27 Dec 8433 Platong Area 7 9.7030 25 Dec 8734 North Satun 20.2380 30 Mar 9235 Platong F Platform 6.0260 22 Apr 9436 Pladang A & PDD-2 Area 10 18.7600 23 Jun 9737 Plamuk Area 11 9.7270 15 Sep 9738 Platong E Area 11 0.6740 3 Mar 9939 Trat Area 13 65.2198 26 Jul 99

Unocal Thailand, Ltd.2/2515/6 40 Erawan Area 1 B12 109.1600 26 Dec 79

41 Erawan Area 2 31.6700 24 Feb 8142 Satun Area 3 53.9800 29 Oct 8243 Erawan Area 1-2-Extension 17.9600 3 May 84

24 2002AnnualR

eport

Operator Production Area Name Issued Area IssuedConcession No. No. Block (sq. km) Date

44 Erawan Area 1-Extension 15.2100 3 May 8445 Satun Area 3-Extension (1) 16.2800 27 Dec 8446 Satun Area 3-Extension (2) 22.0500 27 Dec 8447 Erawan Area-Extension (1) 57.6000 29 Apr 8548 Erawan Area 1-Extension (M) 10.5600 11 Apr 8849 Erawan Area 1-Extension (N) 4.0000 13 Oct 8850 Jakrawan Area 4 3.2300 15 Nov 8951 Satun Area 5 10.3500 18 May 9052 Erawan Area 1-Extension (P) 2.3200 9 Aug 9053 Satun Area 6 18.5900 29 Oct 9054 Erawan Area 1-Extension (R & Q) 25.5030 3 Nov 9355 Funan G 2.7450 4 Oct 9456 Erawan S & T Platforms 30.8890 22 Nov 9457 Jakrawan B, C & D 50.0770 3 Apr 9658 Satun L Platform Area 10 23.4323 24 Feb 9759 Jakrawan E & I Area 11 5.5721 23 Sep 9760 Jakrawan F & H Area 12 8.7485 23 Sep 9761 East Dara Area 13 129.7000 6 Dec 00

Unocal Thailand, Ltd.2/2515/6 62 Erawan Area 1 B13 5.4200 26 Dec 79

63 Baanpot Area 2 35.4300 29 Oct 8264 Funan Area 4 2.0000 11 Jan 8365 Baanpot Area 3 7.9900 14 Dec 8366 Erawan Area 1-N-Extension 7.3200 29 Apr 8567 Erawan Area 1-Extension (s) 1.6900 3 Oct 8668 Baanpot Area 5 2.5360 20 Aug 8769 Baanpot Area 5-Extension 11.0000 26 Feb 8870 Jakrawan Area 3 12.7100 15 Nov 8971 Funan Area 4-Addition 99.0610 28 Aug 9172 Jakrawan Area 6 1.9380 6 Oct 9373 Funan G 6.3000 4 Oct 9474 Gomin A & B Area 8 20.1090 10 Jul 9575 Funan H & I 23.0110 22 Apr 9676 Jakrawan E & I Area 10 9.4498 23 Sep 9777 Jakrawan F & H Area 11 5.9641 23 Sep 9778 Funan J Platform (Area 12) 11.3900 26 Apr 0079 Funan B & H Infill Platform 9.6600 2 Nov 0080 Funan K Area 14 19.9000 2 Nov 0081 Greater Funan 426.82 23 Apr 02

Unocal Petroleum, Ltd.5/2534/41 82 West Dara B 10/32 5.0600 6 Dec 00

Unocal Thailand, Ltd.1/2529/33 83 Main Pailin Area 1 452.6200 5 Jan 94

84 North Pailin Area 2 325.4930 3 Nov 9785 South Pailin Area 3 B12/27 118.6290 27 Aug 9886 West Pailin Area 4 149.8510 27 Aug 9887 Moragot Area 5 383.1400 27 Aug 98

Harrods Energy (Thailand) Ltd.

1/2532/35 88 Jasmine B5/27 48.6388 30 Sep 02

Harrods Energy (Thailand) Ltd.

1/2535/45 89 Bussabong B12/32 121.9200 6 Feb 01

PTTEP International Ltd.

2/2539/49 90 Pikul B13/38 1.9264 30 Sep 02

25 2002AnnualR

eport

Operator Production Area Name Issued Area IssuedConcession No. No. Block (sq. km) Date

Onshore

ExxonMobil Exploration && Production Khorat Inc.

2/2522/17 1 Nam Phong E5 34.4000 5 Feb 88

Amerada Hess (Thailand) Co.Ltd.

1/2524/19 2 Phu Horm-1 EU1 1.9600 15 May 89

Pacific Tiger Energy (Thailand) Ltd.

1/2527/24 3 Wichian Buri SW1A 2.0000 24 Jan 924 Na Sanun 1.9720 12 May 955 Si Thep 1.8480 13 May 976 Wichian Buri Licence II 8.6411 30 Sep 02

PTTEP International Ltd.

2/2528/27 7 U-Thong PTTEP 1 5.0600 10 Aug 908 Kamphaeng Saen 2.0000 10 Aug 909 Sang Kajai 1.98 8 May 02

Sino-U.S. Petroleum Inc.

1/2526/23 10 Bung Ya Structure NC 5.4189 15 Jan 9111 Bung Muang-2 1.9970 5 Jan 9412 Bung Muang & Bung Ya Area I 0.9100 22 Jul 9613 Bung Muang & Bung Ya Area II 2.0020 12 Jul 9614 Bung Muang & Bung Ya Area III 0.9160 12 Jul 96

Thai Shell Exploration && Production Co., Ltd.

1/2522/16 15 Sirikit S1 25.0000 11 Jan 8316 Sirikit F01 10.7000 13 May 8317 Sirikit South 14.7500 20 Aug 8418 Sirikit West 2.9120 9 Oct 8419 Pru Krathiam 16.1172 15 Dec 8620 Wat Taen 2.0000 4 Mar 8821 Thap Rat 1.9490 27 Jan 8922 Nong Tum 1.9733 23 Feb 9023 Pratu Tao 1.9954 24 Mar 8924 Sirikit East 1.9300 10 Feb 9325 Nong Makhaam E 1.8600 19 Apr 9326 Sirikit T 2.4960 27 Aug 9827 Nong Makhaam 15.4920 19 Oct 9928 South Pradoo Tao 90.4340 30 Sep 02

Source : Bureau of Petroleum Operations and Coordination, DMF

26 2002AnnualR

eport

Petroleum InvestmentThere has been an enormous amount of money spent on petroleum exploration and productionactivities in Thailand. The expenditures can be grouped under three categories:

1. Exploration Costs include the cost of geological survey, seismic survey either 2D or 3D,exploratory drilling, development of drilling techniques.

2. Development Costs include cost of construction, installation platform, facilities, pipeline,tanker, infrastructure, research and development.

3. Operating Costs include the cost of maintaining the operation, acquisition cost, productioncost, administration, overhaead charge and royalty.

For 30 years in conducting petroleum operation, total petroleum expenditures were as follows:47% operating cost, 28% development cost and 25% exploration cost. Compared to year 2002,slightly increased for operating cost (49%) followed by exploration cost (31%) and developmentcost reduced to 20% as shown in the figures.

Cummulative 1981-2001

Cummulative 12002

Operating Cost

47 %

Exploration Cost

25 %

Development Cost

28 %

Operating Cost

49 %

Exploration Cost

31 %

Development Cost

20 %

27 2002AnnualR

eport

For more than 30 years, concessionaires have invested 536,668 million baht in upstreampetroleum activities. 17% onshore and 83% offshore investment cost. Petroleum productionmainly came from gas fields in offshore areas. Annual petroleum expenditures both onshoreand offshore area were summarized as illustrated in the following table.

Year Onshore Offshore Total1971 - 1991 35,412 92,597 128,008

1992 3,025 13,603 16,6281993 2,860 14,981 17,8411994 3,227 16,171 19,3991995 2,638 20,290 22,9281996 3,587 23,384 26,9711997 4,746 37,404 42,1501998 6,264 44,072 50,3351999 5,382 35,999 41,3822000 7,362 38,384 45,7462001 6,774 53,999 60,7732002 7,327 57,180 64,507

88,603 448,065 536,668

28 2002AnnualR

eport

Petroleum ExplorationSeismic surveyIn the year 2002, no extensive onshore seismic survey has been done as in previous years.There were only offshore seismic surveys. The main reasons were no new block awarded andthe seismic survey in the existing block itself was almost in mature stage. However, there wassome seismic acquisition in the gulf of Thailand for either complementing exploratorycommitment or future field development.Soco has contracted Multiwave Geological Company for further 2D seismic survey required inblock B8/38 to total recording distance of 1,128.6 km.Unocal has completed additional 3D seismic survey in North Surat Area (block B10) and NorthDara Area (block B12&B10/32) total area of 481.5 sq. km.Chevron hired Fugro Airborne Surveys Limited conducting gravity and magnetic survey in blockB8/32, total recording of 1,766 km. and 13,213 km. respectively.

Exploration DrillingExploration activities have been mainly focused on offshore areas with only one well beingdrilled onshore. Altogether 22 exploratory and delineation wells were drilled in 2002, just onlyhalf the number drilled in the previous year. All wells, except one reported hydrocarbons.

Amerada Hess drilled the onshore well Phu Horm-3 (located in the Watershed Area, Class 1Aof the National Reserved Forest) in June 2002. A sever gas kick was observed and shortly afterdrilling operations were suspended. Amerada Hess intend to resume drilling operations in early2003.

Chevron drilled 6 delineation wells, 2 in Benchamas, Tantawan and Jamjuree field. All wellsfound oil which well contribute to further field development.

PTTEP drilled 2 exploration wells, one in Arthit project another in Pikul structure both weregas well. Arthit-14-6X was the last well of Arthit drilling campaign and has convinced PTTEPof getting sufficient informative datas which essential for final field assessment prior totender production area application.Pikul-2X was the second well drilled in Pikul structure inblock B13/38 and the result proved economic viability for field development. In addition, twodelineation wells were drilled in Bongkot and Tonsak area and found gas as well, encouragingmore field development.

Unocal drilled 11 delineation wells to get more information from several existing fielddevelopments i.e. plamuk, 11A-2, Erawan, Moragot and Pailin in block B10, B11A, B12 &B12/27 respectively. Only one of the wells drilled was dry.

29 2002AnnualR

eport

Operator Block Well name Duration TD (m) Result

Onshore

Amerada Hess E5 Phu Horm-3 9 Jun-24 Aug 02 2,478 Suspended

Gulf of Thailand

Chevron B8/32 Benchamas North-4 1-13 Jul 02 3,538 Oil

Benchamas-26 14-20 Jul 02 2,399 Oil

Jamjuree-9 21-27 Jul 02 2,914 Oil

Jamjuree-10 23 Aug-2 Sep 02 2,860 Oil

Tantawan-21 28 Jul-7 Aug 02 3,333 Oil

Tantawan-22 9-21 Aug 02 3,546 Oil

PTTEP B14A Arthit-14-6x 7-17 Jan 02 3,325 Gas

B15 Tonsak-6 2-12 Jun 02 2,770 Gas

B16 BK-Del-22 27 Jan-4 Feb 02 3,064 Gas

B13/38 Pikul-2X 17-22 Jan 02 2,186 Gas

Unocal B10 Plamuk-6 15-22 Sep 02 3,528 Oil&Gas

B11A 11A-2 17-22 Apr 02 3,267 Oil&Gas

B12 Erawan12-48 27 Jul-4 Aug 02 3,403 Gas

Erawan12-49 21-27 Sep 02 3,440 Gas

B12/27 Moragot-05 24 Apr-1 May 02 3,284 Gas

Pailin-40 12-19 Mar 02 3,438 Gas

Pailin-41 3-8 May 02 3,404 Gas

Pailin-42 20-26 Mar 02 3,414 Gas

Pailin-43 9-14 Apr 02 2,712 Dry

Pailin-44 28 Mar-5 Apr 02 4,263 Gas

Pailin-45 25 Jul-2 Aug 02 3,637 Gas

Exploration Drilling in 2002

30 2002AnnualR

eport

Field DevelopmentDevelopment wellThis year field development has been dominated by the offshore sector with 310 offshore wellsbeing drilled and only 29 wells onshore.The number of wells drilled this year is nearly double when compared to the last year, due toimproved drilling practices and attractive petroleum prices.

Sino-U.S. drilled 4 wells in Bung Muang structure in order to regain the production rate whichdeclined rapidly after a few months of production.

Thai Shell drilled 21 development wells in block S1 which is still focusing on Sirikit main andNong Makhaam area of which 13 and 5 wells drilled respectively. The rest were drilled inGraeter Pratu Toa area. The production mechanism of some wells were changed over fromconventional artificial gaslift to Electrical Submersible Pump according to high base sedimentwater (BS&W). All produced water has been re-injected in to the depleted formation forflooding purpose. The waterflood project in order to fully develop Sirikit West area has beenstarted by drilling 4 water injection wells in the appropriately desired location. Also,2 shallow water source wells were drilled to support further the full scale waterflood projectof the whole area in the future.

PTTEP drilled only 16 development wells on the existing platforms due to rig inavailability. Inaddition, the latest wellhead platform, WP-14 is under construction and will be completedby early next year.

Chevron added 4 development wells in Tantawan and 5 platforms of Benchamas field havebeen drilled with 46 development wells to enhance its production rate. Furthermore, 6 waterinjection wells for the waterflood project in Benchamas field have been drilled back to back.After months of flooding, the increment of production rate on each targeted producer wellwas clearly observed.

Unocal is still the main producer in the gulf of Thailand. A large number of 343 developmentwells were drilled to boost up its gas and oil production especially in Erawan field followed byNorth Pailin and Plamuk with the number of well drilled 132, 59 and 42 respectively. To avoiddischarging produced water directly into the sea, 3 more water injection wells were employedin Pailin central production platform (PACPP) enhancing water disposal capacity.

Pacific Tiger has maitained its business by adding 4 development wells in the block andenhancing production performance by means of downhole device, called the progressivecavity pump(PCP) instead of beam pumping due to high viscosity of crude oil.

The existing small production field without drilling activities are Nam Phong, Authong andKhamphang Saen.

31 2002AnnualR

eport

Development Drilling in 2002Operator Block Well name Duration Active Days TD (m) Result

OnshorePacific Tiger SW1A Wichian Buri North-3 10 Jan-2 Feb 02 23 1,033 Oil

Wichian Buri North-4 11-14 Oct 02 4 1,565 OilWichian Buri North-5 5-8 Oct 02 4 1,284 OilWichian Buri North-6 8-11 Oct 02 4 1,312 Oil

Sino-U.S. NC Bung Muang 2-12 1-19 Feb 02 19 3,010 OilBung Muang 2-13 22 Feb-8 Mar 02 14 2,938 OilBung Muang 2-14 1-25 Nov 02 25 2,845 OilBung Muang 2-15 29 Nov-12 Dec 02 14 2,828 Oil

Thai Shell S1 Lan Krabu-W05 8-12 Jan 02 4 2,238 OilLan Krabu-CA02 14-21 Jan 02 7 2,566 OilNong Makhaam-C10 24-28 Jan 02 5 2,213 OilNong Tum-A02 31 Jan-13 Feb 02 14 3,792 OilNong Tum-A03 13-28 Feb 02 15 3,755 OilPratu Tao-A05 12-23 Apr 02 12 3,872 OilLan Krabu-A11 27 Apr-2 May 02 5 2,398 OilLan Krabu-A12 2-6 May 02 5 2,414 OilLan Krabu-A13 7-12 May 02 6 2,176 OilLan Krabu-A14 13-21 May 02 8 2,507 OilLan Krabu-A15 22-27 May 02 5 2,330 OilLan Krabu-S05 11-18 Jun 02 7 2,401 OilLan Krabu-S06 18-26 Jun 02 8 2,476 OilLan Krabu-R08 29 Jun-5 Jul 02 7 2,528 OilLan Krabu-R09 5-12 Jul 02 7 2,432 OilNong Makhaam-E02 15-20 Jul 02 6 2,325 OilLan Krabu-G07 21-27 Oct 02 6 2,490 OilLan Krabu-L15 30 Oct-3 Nov 02 5 2,706 OilNong Makhaam-C11 21-25 Nov 02 5 2,027 OilNong Makhaam-C14 9-14 Dec 02 5 2,367 OilNong Makhaam-F12 24-28 Dec 02 4 1,757 Oil

Gulf of ThailandChevron B8/32 Benchamas B-30 2-15 Jan 02 10 3,603 Oil

Benchamas B-32 5-21 Jan 02 9 3,362 Oil&GasBenchamas B-31 7 Feb-22 Mar 02 8 3,181 Oil&GasBenchamas H-1 7 Apr-2 May 02 11 3,162 GasBenchamas H-2 6 Apr-7 May 02 9 3,319 Oil&GasBenchamas H-3 13 Apr-11 May 02 8 2,918 GasBenchamas H-4 8 Apr-14 May 02 7 2,923 Oil&GasBenchamas H-5 14 Apr-17 Jun 02 8 2,802 OilBenchamas H-6 14 Apr-20 Jun 02 7 2,214 OilBenchamas H-7 9 Apr-24 May 02 16 3,296 Oil&GasBenchamas H-7ST2 9 Apr-27 Jun 02 27 3,338 Oil&GasBenchamas H-8ST1 9 Apr-12 Jun 02 25 4,316 OilBenchamas E-1 19 May-29 Jun 02 10 2,995 GasBenchamas E-2 22 May-24 Jun 02 17 2,818 Oil&GasBenchamas E-4 24 May-9 Jul 02 8 2,890 Oil&GasBenchamas E-5 21 May-12 Jul 02 7 3,291 Oil&GasBenchamas E-6ST1 28 May-29 Jul 02 14 3,723 Oil&Gas

32 2002AnnualR

eport

Operator Block Well name Duration Active Days TD (m) Result

Benchamas E-7 29 May-19 Jul 02 10 4,201 Oil&GasBenchamas E-9 19 May-1 Aug 02 8 2,688 Oil&GasBenchamas I-1 16 Aug-14 Sep 02 12 3,266 Oil&GasBenchamas I-2 21 Aug-18 Sep 02 6 2,948 Oil&GasBenchamas I-3 22 Aug-21 Sep 02 6 3,255 Oil&GasBenchamas I-4 11 Aug-26 Sep 02 9 2,817 Oil&GasBenchamas I-5ST1 15 Aug-24 Oct 02 15 3,628 Oil&GasBenchamas I-7 13 Aug-4 Oct 02 12 2,933 Oil&GasBenchamas I-8 9 Aug-8 Oct 02 10 3,112 Oil&GasBenchamas I-9 22 Aug-13 Oct 02 8 3,536 Oil&GasBenchamas I-10 14-27Oct 02 7 3,370 Oil&GasBenchamas G-1 9 Sep-10 Oct 02 10 3,364 Oil&GasBenchamas G-2 8 Sep-2 Oct 02 12 3,503 Oil&GasBenchamas G-3 11 Sep-20 Oct 02 7 3,033 Oil&GasBenchamas G-4 8 Sep-13 Oct 02 8 3,326 Oil&GasBenchamas G-5 12 Sep-6 Nov 02 11 2,664 Oil&GasBenchamas G-6 13 Sep-24 Oct 02 7 2,898 Oil&GasBenchamas G-7 7 Sep-5 Oct 02 7 3,568 Oil&GasBenchamas G-8 9 Sep-17 Oct 02 8 3,029 Oil&GasBenchamas G-9 7-15 Nov 02 7 2,898 Oil&GasBenchamas G-10 7-18 Nov 02 6 2,805 Oil&GasBenchamas D-1 9 Nov-3 Dec 02 12 3,254 Oil&GasBenchamas D-2 2 Nov-7 Dec 02 10 3,198 Oil&GasBenchamas D-3 5 Nov 02-7 Jan 03 8 3,722 Oil&GasBenchamas D-4 7 Nov-11 Dec 02 8 3,112 Oil&GasBenchamas D-5 3 Nov-17 Dec 02 12 3,173 Oil&GasBenchamas D-6 6 Nov-24 Dec 02 12 3,490 Oil&GasBenchamas D-7 11 Nov-30 Dec 02 10 3,285 Oil&GasBenchamas D-8 11 Nov 02-4 Jan 03 9 3,542 Oil&GasTantawan E-9 28 Nov-22 Dec 02 9 4,612 Oil&GasTantawan E-10 25 Nov-17 Dec 02 8 3,354 Oil&GasTantawan E-11 30 Nov-12 Dec 02 7 2,780 Oil&GasTantawan E-12 2-26 Dec 02 7 3,437 Oil&Gas

PTTEP B15 BK-11-J 28 Feb-12 Mar 02 12 3,420 GasBK-11-A 14 Aug-2 Oct 02 10 3,300 GasBK-11-B 13-22 Mar 02 10 3,035 GasBK-11-C 15-29 Aug 02 10 3,690 GasBK-11-D 19 Aug-18 Sep 02 8 3,645 GasBK-11-E 11 Aug-10 Oct 02 11 3,910 GasBK-11-F 16 Aug-11 Sep 02 9 3,910 GasBK-11-H 17 Aug-4 Sep 02 8 3,125 GasBK-11-K 9 Aug-25 Sep 02 9 3,662 GasBK-10-AE 18 May-4 Jun 02 9 2,610 GasBK-10-BW 21-29 May 02 8 2,775 GasBK-9-BWR 10-23 Jun 02 13 3,636 GasBK-9-JE 23 Jun-1 Jul 02 8 3,278 GasBK-9-FE 3-20 Jul 02 7 3,685 GasBK-9-FW 3-14 Jul 02 12 3,330 GasBK-9-BER 20 Jul-1 Aug 02 12 3,655 Gas

33 2002AnnualR

eport

Operator Block Well name Duration Active Days TD (m) Result

Unocal 10 Plamuk B -01 2 Jan-4 Feb 02 8 3,628 Oil&GasPlamuk B -02 21 Feb-3 Mar 02 10 3,477 Oil&GasPlamuk B -04 3-18 Mar 02 15 2,507 Oil&GasPlamuk B -07 5-18 Feb 02 8 3,552 Oil&GasPlamuk B -08 4-13 Feb 02 9 3,709 Oil&GasPlamuk B -15 3-30 Jan 02 8 3,589 Gas/Oil ?Plamuk B -16 3-16 Jan 02 7 3,826 Gas/OilPlamuk B -18 3-24 Jan 02 10 4,048 GasPlamuk C -01 24 Mar-14 Apr 02 8 3,951 Oil&GasPlamuk C -06 25 Mar-30 Apr 02 6 3,527 Oil&GasPlamuk C -07 25 Mar-8 Apr02 10 3,594 Oil&GasPlamuk C -10 7-30 May 02 8 3,537 Oil&GasPlamuk C -11 26 Mar-26 Apr 02 8 3,788 Oil&GasPlamuk C -12 7 May-6 Jun 02 9 4,203 Oil&GasPlamuk C -13 22 Mar-20 Apr 02 9 3,014 Oil&GasPlamuk C -14 8 May-11 Jun 02 8 3,174 Oil&GasPlamuk C -15 7-24 May 02 7 3,325 Oil&GasPlamuk C -16 11-18 Jun 02 8 3,523 Oil&GasPlamuk C -3 7-19 May 02 8 3,600 Oil&GasPlamuk C -8 26 Mar-6 May 02 8 3,912 Oil&GasPlamuk D-1 23 Jun-11 Jul 02 8 3,304 Oil&GasPlamuk D-10 23 Jun-18 Jul 02 9 3,252 Oil&GasPlamuk D-11 25 Jul-8 Aug 02 8 3,268 Oil&GasPlamuk D-12 26 Jul-22 Aug 02 8 2,975 Oil&GasPlamuk D-13 23 Jun-21 Jul 02 7 2,941 Oil&GasPlamuk D-14 26Jul-25 Aug 02 6 3,220 Oil&GasPlamuk D-2 26 Jul-17 Aug 02 6 3,195 Oil&GasPlamuk D-3 26 Aug-1 Sep 02 5 3,053 Oil&GasPlamuk D-6 26 Jul-13 Aug 02 7 3,217 Oil&GasPlamuk D-7 22 Jun-5 Jul 02 9 3,526 Oil&GasPlamuk D-9 22 Jun-25 Jul 02 9 2,758 Oil&GasPlatong G-21 27 May-2 Jun 02 7 1,902 GasPlamuk C-02 7-26 Oct 02 9 3,960 Oil&GasPlamuk C-04 7-16 Oct 02 8 3,303 Oil&GasPlamuk C-09 26 Oct-8 Nov 02 12 3,312 Oil&GasPlamuk C-17 7-31 Oct 02 8 3,914 Oil&GasPlamuk C-24 7-20 Oct 02 7 4,072 Oil&GasPlamuk D-15 12-24 Nov 02 8 3,193 Oil&GasPlamuk D-16 13-20 Nov 02 6 3,226 Oil&GasPlamuk D-17 13 Nov-7 Dec 02 6 2,740 Oil&GasPlamuk D-18 24-30 Nov 02 6 3,177 Oil&GasPlamuk D-19 24 Nov-3 Dec 02 6 3,216 Oil&GasSurat A-09 28 Oct-11 Nov 02 8 2,947 Oil&GasSurat A-10 28 Oct-16 Nov 02 7 2,822 Oil&GasSurat A-11 28 Oct-7 Nov 02 9 2,705 Oil&GasSurat A-12 27 Oct-20 Nov 02 7 3,065 Oil&GasYala B-04 9 Oct-3 Nov 02 8 3,864 Oil&GasYala B-05 10-24 Oct 02 8 3,609 Oil&GasYala B-06 10-20 Oct 02 7 3,625 Oil&Gas

34 2002AnnualR

eport

Operator Block Well name Duration Active Days TD (m) Result

Yala B-07 3-25 Nov 02 8 3,886 Oil&GasYala B-1 1 Jul-13 Aug 02 7 3,563 Gas&OilYala B-13 30 Jun-9 Aug 02 7 3,501 Gas&OilYala B-14 1-31 Jul 02 8 3,764 Oil&GasYala B-15 10-29 Oct 02 8 3,479 Oil&GasYala B-16 30 Jun-26 Jul 02 8 4,167 Oil&GasYala B-17 1 Jul-6 Aug 02 9 3,924 Gas&OilYala B-2 1-20 Jul 02 8 3,818 Oil&GasYala B-24 3-20 Nov 02 8 3,895 Oil&GasYala B-25 4-13 Nov 02 7 3,989 Oil&GasYala B-26 28 Jun-18 Aug 02 9 3,437 Gas&OilYala B-27 3-30 Nov 02 8 3,530 Oil&GasYala B-3 30 Jun-15 Jul 02 8 3,488 Oil&Gas

11 Pladang A-14 15-30 Aug 02 8 4,305 GasPladang A-15 21 Aug-3 Sep 02 8 4,421 GasPladang A-16 25 Aug-6 Sep 02 6 3,399 GasPladang A-17 16 Aug-10 Sep 02 6 4,355 GasPladang A-18 17 Aug-12 Sep 02 5 3,360 GasPladang A-19 20 Aug-17 Sep 02 8 3,463 GasTrat A-14 7-29 Dec 02 6 3,190 GasTrat A-19 14 Dec 02-1 Jan 03 6 3,214 GasTrat A-20 12 Dec 02-3 Jan 03 4 2,623 GasTrat A-21 8 Dec 02-11 Jan 03 17 3,989 GasTrat A-23 11-26 Dec 02 8 3,897 Gas

12 Erawan R-19 21 Apr-11 May 02 7 3,224 GasErawan R-20 21 Apr-7 May 02 9 4,073 GasErawan R-25 2-10 Apr 02 7 3,471 GasErawan R-26 31 Mar-16 Apr 02 9 4,028 GasErawan R-27 30 Mar-21 Apr 02 8 3,367 GasErawan R-29 21-30 Apr 02 7 3,635 GasErawan U-1 10-21 Apr 02 9 3,659 GasErawan U-2 10-26 Apr 02 7 3,968 GasErawan U-11 15-31 May 02 9 4,281 GasErawan U-12 15-21 Jun 02 7 3,865 GasErawan U-3 8 May-6 Jun 02 9 3,952 GasErawan U-4 10 Apr-8 May 02 7 3,417 GasErawan U-6 10-27 Jun 02 9 4,016 GasErawan U-7 9 May-10 Jun 02 8 3,716 GasErawan U-8 14-26 May 02 10 3,716 GasErawan F-14 8-17 Jun 02 6 3,700 GasErawan F-17 6 Jun-4 Jul 02 6 3,607 GasErawan F-18 13-28 Jul 02 6 4,331 GasErawan F-19 8-26 Jun 02 7 4,444 GasErawan F-20 9 Jun-8 Jul 02 6 3,667 GasErawan F-21 9-30 Jun 02 6 3,518 GasErawan F-22 14 Jul-5 Aug 02 8 2,638 GasErawan F-23 9-21 Jun 02 7 4,020 GasErawan F-24 13-24 Jul 02 8 4,141 GasErawan F-25 14 Jul-1 Aug 02 6 4,026 Gas

35 2002AnnualR

eport

Operator Block Well name Duration Active Days TD (m) Result

Erawan U-10 3-20 Sep 02 6 3,446 GasErawan U-13 26 Aug-29 Sep 02 6 4,284 GasErawan U-14 25 Aug-13 Sep 02 6 3,751 GasErawan U-15 26 Aug-26 Sep 02 6 3,582 GasErawan U-19 4-17 Sep 02 7 3,616 GasErawan U-22 26 Aug-10 Sep 02 7 3,521 GasErawan U-9 27 Aug-23 Sep 02 6 3,634 GasSatun J-11 30 Apr-12 May 02 6 3,790 GasSatun J-12 1-14 May 02 6 3,937 GasSatun J-13 1-18 May 02 7 3,191 GasSatun J-14 30 Apr-20 May 02 5 3,776 GasSatun J-15 1-23 May 02 6 3,115 GasSatun M-13 10-15 Jul 02 5 3,584 GasSatun M-14 26 Jun-21 Jul 02 6 3,839 GasSatun M-16 9-18 Jul 02 6 3,172 GasSatun M-17 5-24 Jul 02 7 3,212 Gas

12/27 North Pailin A - 01 15-27 Jan 02 4 3,096 GasNorth Pailin A - 02 16 Jan-1 Feb 02 5 2,851 GasNorth Pailin A - 04 15-30 Jan 02 6 3,277 GasNorth Pailin A - 05 2-11 Feb 02 5 3,471 GasNorth Pailin A - 06 3-13 Feb 02 4 2,818 GasNorth Pailin A - 08 2-9 Feb 02 5 2,887 GasNorth Pailin A - 09 3-18 Feb 02 4 2,523 GasNorth Pailin A - 10 3-16 Feb 02 5 2,877 GasNorth Pailin A - 13 3-14 Feb 02 4 3,003 GasNorth Pailin A - 15 16 Jan-2 Feb 02 4 2,850 GasNorth Pailin A - 16 16-26 Jan 02 5 2,773 GasNorth Pailin A -12 15-23 Jan 02 5 2,659 GasNorth Pailin B - 03 15 Jan-11 Feb 02 6 3,482 GasNorth Pailin B - 04 14 Jan-7 Feb 02 5 3,479 GasNorth Pailin B - 1 11 Feb-7 Mar 02 4 2,963 GasNorth Pailin B - 14 15-30 Jan 02 5 3,523 GasNorth Pailin B - 20 15 Jan-2 Feb 02 6 3,659 GasNorth Pailin B - 22 12 Feb-11 Mar 02 4 2,981 GasNorth Pailin B -09 12 Jan-5 Feb 02 6 3,338 GasNorth Pailin B -10 13-26 Jan 02 6 3,021 GasNorth Pailin B -11 13-28 Jan 02 6 3,603 GasNorth Pailin B -13 17-22 Mar 02 6 3,749 GasNorth Pailin B -17 13-27 Feb 02 7 3,313 GasNorth Pailin B -2 18 Feb-10 Mar 02 8 3,549 GasNorth Pailin B -23 14 Feb-6 Mar 02 6 3,098 GasNorth Pailin B -25 13 Feb-4 Mar 02 9 3,933 GasNorth Pailin B -27 19 Feb-1 Mar 02 6 3,953 GasNorth Pailin B -8 11-17 Mar 02 7 3,511 GasNorth Pailin C-02 11-24 Feb 02 8 3,219 GasNorth Pailin C-03 14-27 Feb 02 6 3,868 GasNorth Pailin C-06 12 Feb-4 Mar 02 11 3,7558 GasNorth Pailin C-08 13 Feb-12 Mar 02 8 3,5578 GasNorth Pailin C-09 13 Feb-8 Mar 02 5 3,581 Gas

36 2002AnnualR

eport

Operator Block Well name Duration Active Days TD (m) Result

North Pailin C-1 13 Mar-6 Apr 02 6 3,534 GasNorth Pailin C-10 13 Mar-3 Apr 02 5 3,869 GasNorth Pailin C-11 14 Feb-6 Mar 02 5 3,610 GasNorth Pailin C-4 13-25 Mar 02 6 3,609 GasNorth Pailin C-5 13-27 Mar 02 5 3,755 GasNorth Pailin C-7 12-22 Mar 02 6 3,766 GasNorth Pailin D -01 24-28 Jan 02 5 3,269 GasNorth Pailin D -03 15-21 Feb 02 7 3,299 GasNorth Pailin D -06 15-24 Feb 02 6 3,980 GasNorth Pailin D -08 18 Jan-9 Feb 02 7 3,559 GasNorth Pailin D -09 12 Feb-9 Mar 02 6 3,461 GasNorth Pailin D -11 18 Jan-12 Feb 02 6 3,712 GasNorth Pailin D -12 12-27 Feb 02 7 3,873 GasNorth Pailin D -13 16 Jan-6 Feb 02 6 3,795 GasNorth Pailin D -14 15 Jan-3 Feb 02 10 3,846 GasNorth Pailin D -15 12 Feb-5 Mar 02 8 3,942 GasNorth Pailin E-1 11 May-10 Jun 02 8 4,340 GasNorth Pailin E-11 14 May-1 Jun 02 7 3,915 GasNorth Pailin E-12 14 May-10 Jul 02 6 3,886 GasNorth Pailin E-14 16 Jun-15 Jul 02 9 3,760 GasNorth Pailin E-15 14-27 May 02 8 4,452 GasNorth Pailin E-16 14 May-15 Jun 02 8 4,261 GasNorth Pailin E-19 16 Jun-6 Jul 02 8 3,791 GasNorth Pailin E-5 16 Jun-1 Jul 02 10 4,033 GasNorth Pailin E-6 16 Jun-22 Jul 02 9 3,872 GasNorth Pailin E-9 14 May-5 Jun 02 8 4,363 GasPailin F - 14 7-23 Jun 02 11 3,520 GasPailin F -03 27 Apr-27 May 02 9 4,157 GasPailin F -07 28 Apr-13 Jun 02 8 3,995 GasPailin F -08 27 Apr-7 Jun 02 11 4,060 GasPailin F -09 29 Mar-26 Apr 02 9 3,967 GasPailin F -10 29 Mar-14 Apr 02 8 3,924 GasPailin F -11 29 Mar-20 Apr 02 9 4,077 GasPailin F -12 27 Apr-15 May 02 9 3,581 GasPailin F -13 27 Mar-11 Apr 02 5 3,493 GasPailin F -15 27 Apr-22 May 02 10 4,627 GasPailin F -17 27 Apr-1 Jun 02 7 4,130 GasPailin F-1 12 Sep-4 Nov 02 10 3,873 GasPailin F-16 10 Sep -3 Oct 02 14 4,704 GasPailin F-18 11 Sep-8 Oct 02 8 4,233 GasPailin F-4 11 Sep-16 Oct 02 9 3,793 GasPailin F-5 10 Sep-26 Oct 02 13 3,595 GasPailin G-02 28 Nov-21 Dec 02 14 4,347 GasPailin G-06 28 Nov-25 Dec 02 6 3,849 GasPailin G-12 28 Nov-11 Dec 02 10 3,904 Gas

13 Funan G-10 23 Feb-13 Mar 02 6 4,271 GasFunan G-11 23 Feb-22 Mar 02 9 3,127 GasFunan G-12 23 Mar-19 Apr 02 6 3,502 GasFunan G-13 24 Feb-7 Mar 02 7 3,057 Gas

37 2002AnnualR

eport

Operator Block Well name Duration Active Days TD (m) Result

Funan G-14 23 Mar-1 Apr 02 6 3,160 GasFunan G-15 22 Mar-11 Apr 02 13 4,096 GasFunan G-16 24 Mar-26 Apr 02 6 3,233 GasFunan G-17 23 Mar-23 Apr 02 8 3,235 GasFunan G-18 23 Mar-15 Apr 02 7 3,825 GasFunan G-4 24 Feb-10 Mar 02 6 3,482 GasFunan G-7 26 Feb-16 Mar 02 6 2,896 GasFunan F-24 13-23 Aug 02 6 3,252 GasFunan F-25 14-26 Aug 02 6 3,445 GasFunan F-29 14-29 Aug 02 6 3,268 GasFunan F-32 11 Aug-1 Sep 02 6 3,298 GasFunan F-33 15 Aug-5 Sep 02 8 3,322 GasGomin A-13 15 Nov-1 Dec 02 7 4,061 GasGomin A-15 15 Nov-4 Dec 02 7 4,374 GasGomin A-16 14-24 Nov 02 5 4,562 GasGomin A-17 8-14 Dec 02 5 3,694 GasGomin A-18 15-27 Nov 02 6 4,074 GasGomin A-19 14 Nov-7 Dec 02 6 4,177 GasGomin A-20 10-17 Dec 02 8 4,265 GasGomin C-01 22 Dec 02-16 Jan 03 4 3,669 GasGomin C-02 22 Dec 02-9 Jan 03 4 3,536 GasGomin C-04 21 Dec 02-18 Jan 03 4 3,282 GasGomin C-07 22 Dec 02-11 Jan 03 4 3,736 GasGomin C-15 22 Dec 02-13 Jan 03 4 4,012 GasGomin C-16 22 Dec 02-3 Jan 03 4 3,813 GasGomin C-18 23 Dec 02-6 Jan 03 4 3,516 GasGomin C-20 23 Dec 02-1 Jan 03 6 4,139 GasJakrawan F-01 28 Oct-16 Nov 02 6 2,964 GasJakrawan F-03 28 Oct-25 Nov 02 6 3,174 GasJakrawan F-04 5-15 Oct 02 7 3,587 GasJakrawan F-05 26 Nov-3 Dec 02 6 3,150 GasJakrawan F-06 25 Nov-6 Dec 02 6 3,632 GasJakrawan F-07 25 Nov-9 Dec 02 7 3,854 GasJakrawan F-08 4-18 Oct 02 6 3,682 GasJakrawan F-10 29 Dec 02-13 Jan 03 8 3,398 GasJakrawan F-11 5 Oct-19 Nov 02 7 3,709 GasJakrawan F-12 4-21 Oct 02 6 3,394 GasJakrawan F-13 5-27 Oct 02 6 3,097 GasJakrawan F-14 28 Oct -14 Nov 02 11 3,833 GasJakrawan F-15 4-24 Oct 02 6 3,484 GasJakrawan F-16 28 Oct-22 Nov 02 6 3,951 GasJakrawan F-17 9-20 Dec 02 7 3,190 GasJakrawan F-18 10-27 Dec 02 6 3,405 GasJakrawan F-19 9-22 Dec 02 5 3,477 GasJakrawan F-20 29 Dec 02-8 Jan 03 8 3,404 GasJakrawan F-21 10-24 Dec 02 6 3,558 GasJakrawan F-22 10-29 Dec 02 10 3,618 Gas

38 2002AnnualR

eport

Crude Oil Export in 2002

Petroleum ProductionDaily RateIn 2002 Thailand produced petroleum an equivalent to 471,736 boed, or 7.11% increase fromthe previous year. Based on heating content, shares of the produced petroleum were as follows: 74%natural gas, 10% oil and 16% condensate.

Total production of gas was 1,990 MMscfd (or 347,056 boed), 4.8% increase while domestic consumptionhad grown by 7.3%. The gap was filled with Myanmar gas. Main increments came from production ofthe Benchamas field by Chevron and Plamuk, Funan and North Pailin fields by Unocal.

Condensate was produced at 53,656 bcd (or 48,805 boed), 3.7% increase, Production by Unocal wasincreased by 7.6 %, mainly from Funan , Pailin and North Pailin fields while production from Bongkot fieldby PTTEP was decreased by 3.1%.

Crude oil production increased by 22.5% to 75,875 bod. Main increments came from offshore productionof Big Oil Project by Unocal Thailand, while onshore production mostly decreased.

Australia 5,990,406 195,979 6,186,385China 4,065,670 1,246,806 5,312,476Indonesia 4,182,442 0 4,182,442Korea 0 1,284,543 1,284,543U.S.A. 835,131 0 835,131Total 15,073,649 2,727,328 17,800,977

Unit in barrel

Exported ContentExport of petroleum liquids in 2002 was19,629,582 bbl, 47 % increase.

1,828,605 bbl Condensate was exported byUnocal and PTTEP. Unocal shipped 1,747,033bbl condensate out to Korea and PTTEPshipped 81,572 bbl to Vietnam.

Oil exports rose by 33.3%. Chevron shipped 15,073,649 bbl of their products to Australia,China, Indonesiaand U.S.A. (15.25 up) ,and Unocal Thailand delivered more oil from the Big Oil Project to Australia,China and Korea.

Unocal 1,028 1,109 7.9 35,524 37,893 6.7 1,196 11,820 888.3PTTEP 584 566 -3.1 16,208 15,763 -2.7Chevron 170 200 17.6 36,811 41,192 11.9Offshore Total 1,782 1,875 5.2 51,732 53,656 3.7 38,007 53,012 39.5Thai Shell 57 56 -1.8 21,570 20,598 -4.5ExxonMobil 60 59 -1.7PTTEPI 597 627 5.0Sino-US. 903 803 -11.1Pacific Tiger 196 174 -11.2DED 661 661 0.0Onshore Total 117 115 -1.7 0 0 0.0 23,927 22,863 -4.4Grand Total 1,899 1,990 4.8 51,732 53,656 3.7 61,934 75,875 22.5

Petroleum ProductionOperator

Gas (MMcfd) Condensate (bbl) Crude Oil (bbl)

2001 2002 Change(%) 2001 2002 Change(%) 2001 2002 Change(%)

New Production FieldsUnocal Thailand started up production from Yala and North Pailin since Q2 2002. Average productionof Yala were 15 MMscfd of natural gas and 5,900 bbld of crude oil and of North Pailin were 137 MMscfdof natural gas and 5,900 bbld of condensate in 2002.

Chevron Unocal Total

39 2002AnnualR

eport

FIELD Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec TOTALNATURAL GAS (MMscf)

Erawan 7,654.041 7,608.805 8,880.322 8,128.427 8,425.515 7,889.112 8,284.741 8,644.840 8,460.778 7,565.749 7,262.339 8,189.726 96,994.395Baanpot 152.435 353.396 523.381 383.989 394.811 360.637 276.997 219.135 281.096 328.175 199.882 137.155 3,611.089South Satun 817.689 1,140.487 1,062.360 1,034.701 1,179.134 1,096.132 883.653 871.697 804.023 808.277 855.249 956.590 11,509.992Satun 3,479.506 3,373.344 3,888.893 3,817.604 3,947.178 3,709.817 3,304.049 3,518.712 2,989.053 3,152.615 2,926.297 3,593.165 41,700.233Pladang 582.349 495.675 557.657 597.156 465.269 461.218 319.086 62.629 95.634 506.625 654.810 1,140.960 5,939.068Trat 2,666.130 1,979.887 2,312.353 1,852.120 1,490.547 1,617.556 1,919.324 1,557.516 1,370.437 1,364.139 1,082.960 1,603.456 20,816.425Platong 579.924 618.596 758.707 684.973 350.152 426.257 380.540 512.144 673.594 701.151 809.581 667.421 7,163.040Kaphong 425.965 241.906 315.166 339.530 323.768 395.816 387.149 463.484 335.594 303.780 236.867 254.156 4,023.181Surat 49.159 62.234 80.700 55.060 54.378 45.938 38.458 35.672 34.503 25.820 26.062 31.172 539.156Plamuk 457.612 546.128 700.199 1,193.310 1,365.021 1,040.255 933.741 637.612 987.263 1,333.421 1,395.584 1,395.915 11,986.061Funan 4,996.357 4,559.149 5,230.105 4,983.411 5,445.363 5,779.964 4,359.675 5,110.580 5,068.546 5,903.557 5,236.152 5,450.247 62,123.106Jakrawan 314.267 250.776 282.636 267.602 328.567 278.283 220.245 202.808 200.151 200.844 214.603 252.579 3,013.361West Jakrawan 1,566.106 1,706.238 2,133.980 2,203.915 2,257.470 2,311.080 1,301.408 1,140.656 1,127.407 1,185.390 928.086 1,631.129 19,492.865Gomin 413.699 510.868 491.441 351.933 385.214 220.238 102.830 88.145 222.074 113.382 101.864 115.726 3,117.414Pailin 5,590.657 6,121.840 7,146.060 7,347.880 7,805.240 6,492.504 7,410.283 6,842.989 7,308.363 7,429.420 4,799.342 5,023.377 79,317.955Yala 0.000 0.000 0.000 14.070 366.417 460.903 645.626 319.213 366.973 697.163 537.910 433.247 3,841.522North Pailin 0.000 0.000 0.000 0.000 0.000 1,569.732 5,837.736 5,895.096 5,245.539 3,737.631 3,758.982 3,378.811 29,423.527Bongkot 17,069.961 15,470.221 20,028.731 18,353.118 18,764.820 18,520.502 18,054.978 19,460.426 17,433.361 16,911.807 14,656.987 11,905.342 206,630.254Tantawan 1,591.187 1,173.027 1,039.853 1,616.606 1,608.937 1,753.679 2,184.087 1,668.412 1,284.652 1,105.419 1,334.394 1,150.865 17,511.118Benchamas 4,117.697 3,992.746 5,003.735 4,396.902 4,893.047 4,325.737 4,502.053 4,634.816 4,586.531 4,854.923 4,548.063 5,462.069 55,318.319Maliwan 0.000 0.000 0.000 0.000 0.000 0.000 160.680 130.002 27.598 0.000 0.000 0.000 318.280Sirikit 1,700.086 1,736.865 1,763.534 1,742.297 1,732.745 1,613.284 1,741.399 1,770.787 1,682.397 1,723.997 1,646.006 1,738.999 20,592.396Nam Phong 1,899.444 1,720.327 1,902.405 1,832.446 1,830.994 1,705.629 1,742.010 1,833.997 1,736.841 1,778.196 1,691.662 1,692.749 21,366.700Total 56,124.271 53,662.515 64,102.218 61,197.050 63,414.587 62,074.273 64,990.748 65,621.368 62,322.408 61,731.481 54,903.682 56,204.856 726,349.457CONDENSATE (bbl)Erawan 238,081 235,603 269,275 232,571 239,544 236,041 322,170 328,685 344,480 293,054 283,414 272,852 3,295,770Baanpot 7,017 12,974 17,431 14,797 17,219 141,598 12,704 8,571 11,660 13,299 12,900 3,329 273,499South Satun 21,884 28,614 29,469 26,689 31,293 26,051 26,317 30,880 21,466 22,913 21,990 22,626 310,192Satun 104,434 130,740 134,973 112,937 115,790 98,268 80,124 80,382 66,835 82,151 79,292 138,037 1,223,963Pladang 31,737 15,866 38,461 24,849 20,734 27,368 11,296 1,505 1,743 24,337 23,211 54,662 275,769Trat 95,750 57,204 69,231 80,069 62,101 73,384 83,069 80,384 74,704 68,169 66,072 31,437 841,574Platong 12,398 8,510 14,581 8,659 8,240 8,596 18,224 24,810 35,847 35,715 34,448 13,171 223,199Funan 161,958 161,580 214,844 217,714 227,416 258,467 212,814 189,176 188,080 261,893 253,874 199,186 2,547,002Jakrawan 0 1,000 673 566 1,025 287 896 745 774 70 70 2,649 8,755West Jakrawan 34,270 36,901 46,704 51,372 51,338 50,825 33,886 34,770 33,563 27,616 26,585 31,236 459,066Gomin 30,254 31,277 13,165 11,132 23,166 11,972 9,404 25,807 40,471 11,288 10,993 17,100 236,029Pailin 220,006 238,031 287,845 295,226 315,929 258,939 223,026 235,807 221,561 282,993 273,489 203,549 3,056,401North Pailin 0 0 0 0 0 53,761 201,782 219,546 205,254 131,663 127,249 139,749 1,079,004Bongkot 440,511 423,313 551,141 505,833 502,922 482,933 522,928 496,299 477,809 492,664 476,353 380,749 5,753,455Total 1,398,300 1,381,613 1,687,793 1,582,414 1,616,717 1,728,490 1,758,640 1,757,367 1,724,247 1,747,825 1,689,940 1,510,332 19,583,678CRUDE OIL (bbl)Platong 41,707 25,124 61,597 42,097 19,579 56,299 104,052 83,637 112,318 110,656 103,892 130,596 891,554Kaphong 60,730 22,639 15,015 12,476 8,738 13,679 14,611 14,932 14,887 10,730 8,443 7,577 204,457Surat 16,305 17,510 24,430 26,063 16,728 14,622 10,972 12,016 16,756 13,969 15,871 18,442 203,684Plamuk 79,609 99,690 140,983 159,483 159,325 105,224 133,599 114,602 93,229 155,032 143,333 184,602 1,568,711Yala 0 0 0 0 103,193 141,051 210,490 144,827 168,164 238,569 222,464 217,022 1,445,780Tantawan 213,995 174,065 132,090 173,992 198,992 229,499 198,959 175,625 154,269 125,378 150,642 133,225 2,060,731Benchamas 1,117,644 1,002,234 1,062,826 941,990 1,046,819 974,112 1,175,279 1,173,900 1,159,615 1,149,978 943,564 1,149,823 12,897,784Maliwan 0 0 0 0 0 0 33,233 33,048 10,267 0 0 0 76,548Sirikit 590,647 570,518 594,579 620,844 650,805 666,362 687,716 694,648 601,773 626,198 600,843 613,467 7,518,400Kamphangsaen 864 501 817 801 789 794 758 851 876 887 918 943 9,799U-Thong 15,394 13,831 14,506 13,796 14,117 16,731 12,872 11,776 11,530 11,456 12,079 15,904 163,992SanKrajai 0 0 0 0 0 0 13,618 6,227 9,159 9,044 8,481 8,411 54,940Bung Ya 8,801 7,329 7,991 7,030 7,225 6,744 7,362 7,044 8,000 7,688 6,448 6,872 88,534Bung Muang 14,476 12,270 12,251 24,357 23,358 20,029 17,112 17,827 16,875 14,965 13,562 17,416 204,498Wichianburi 4,535 4,369 4,658 4,596 4,695 3,557 3,234 3,235 3,661 4,224 7,563 9,940 58,267Srithep 453 379 668 386 397 391 386 405 382 366 356 360 4,929Fang 21,302 20,460 18,466 18,995 17,189 14,623 14,609 21,454 22,868 23,042 24,979 23,140 241,127Total 2,186,462 1,970,919 2,090,877 2,046,906 2,271,949 2,263,717 2,638,862 2,516,054 2,404,629 2,502,182 2,263,438 2,537,740 27,693,735Sirikit (LPG,Tons) 9,085 8,379 9,041 8,801 9,143 9,194 9,439 9,705 8,934 9,051 8,831 9,327 108,930

Monthly Petroleum Production in Thailand in 2002

40 2002AnnualR

eport

Environmental Impacts Assessment (EIA) ReportsAs the result of the Notice (given on 22nd January 1996) from the Minister of Science,Technology, and Environment (MOSTE) No 3 (1996) concerning prescription of typesand capacity of projects or activities of government agencies, state enterprises orprivate sector requiring a submission for approval of report on environmental impactsassessment given on 22 January 1996, the upstream oil and gas activities are requiredto submit an environmental impacts assessment report (EIA) for çall capacitiesé.

In 2002, there were 2 Environmental Impact Assessment (EIA) reports for upstreamoil and gas activities submitted to the Department of Mineral Fuels (DMF) and Officeof Natural Resources and Environmental Policy and Planning (ONEP), as the approvalregulator authority, as follows: ● an EIA report for onshore development project of South Pratu Toa oil field, block S1,

Bang Rakham district, Phitsanuloak Province, implemented by Thai Shell Explorationand Production Ltd., conducted by Pro-En Technology Ltd. (Pro-En). The report wassubmitted to ONEP in November 2002 and was approved in February 2003.

● an EIA report for offshore hydrocarbon exploration and drilling project of çHong Fawellé, block B7/38 in the coastal area of the Gulf of Thailand , implemented byDevon Energy (Thailand) Ltd., conducted by International EnvironmentalManagement Co.Ltd. (IEM). The report was submitted to ONEP in February 2002 andwas approved in March 2003. See detail in table as below.

Upstream Oil && Gas Activity Environmental Impact Assessment Reports in 2002Concessionaire

Project name ConsultantSubmitted

(Project owner) date/Approved date

Devon Energy(Thailand) Ltd.

Thai ShellExploration andProduction Ltd.

Hydrocarbon Exploration & Drilling çHong Fa Wellé Project ,Block B7/38, Gulf of Thailand● Main Report (1 Thai copy)● Executive Summary Report (1 Thai, 1 English copy)● Appendices Report (1 English copy)● 1

stAdditional Information Report (2 Thai, 1

Englishcopies)● 2

ndAdditional Information Report (2 Thai, 1

English copies)

çSouth Pratu Toaé Development Project, Block S1, BangRakham District, Phitsanuloak Province ● Main Report (3 Thai copies)● Executive Summary Report (3 Thai copies)● Appendices Report (1 English copy)

IEM Ltd.

Pro-En Technology Ltd

27 February 2002

19 December 200210 February 2003/11 March 2003(Approved)

29 Nov 2002/ 12 February 2003

Environmental Monitoring ReportsIn conformance with the Environmental Regulation related to EIA requirement for theall capacities of upstream oil and gas activities, the concessionaire is required to followthe conditional approval i.e., several environmental impact prevention and correctionmeasures by ONEP. These conditions includes the requirement that environmentalmonitoring surveys be conducted by the concessionaire, and reported to ONEP and DMF.