loan pricing a key driver in the - amazon s3 · 2016-09-19 · loan pricing –a key driver in the...

TRANSCRIPT

#SageworksSummit

Loan Pricing – A Key Driver in the

Success of your Bank’s Strategy

September 16 · 2016

#SageworksSummit

Agenda.

• Banks currently have a number of methods they use to price loans

» How does your bank price loans?

» How important is a loan pricing strategy?

• What are the factors of a successful loan pricing model

» Case study: Risk ratings & loan pricing

• How loan pricing will help you meet your strategic goals and make your investors happy

» Sample loan pricing model scenarios

2

#SageworksSummit

Agenda.

• Banks currently have a number of methods they use to price loans

» How does your bank price loans?

» How important is a loan pricing strategy?

• What are the factors of a successful loan pricing model

» Case study: Risk ratings & loan pricing

• How loan pricing will help you meet your strategic goals and make your investors happy

» Sample loan pricing model scenarios

3

#SageworksSummit

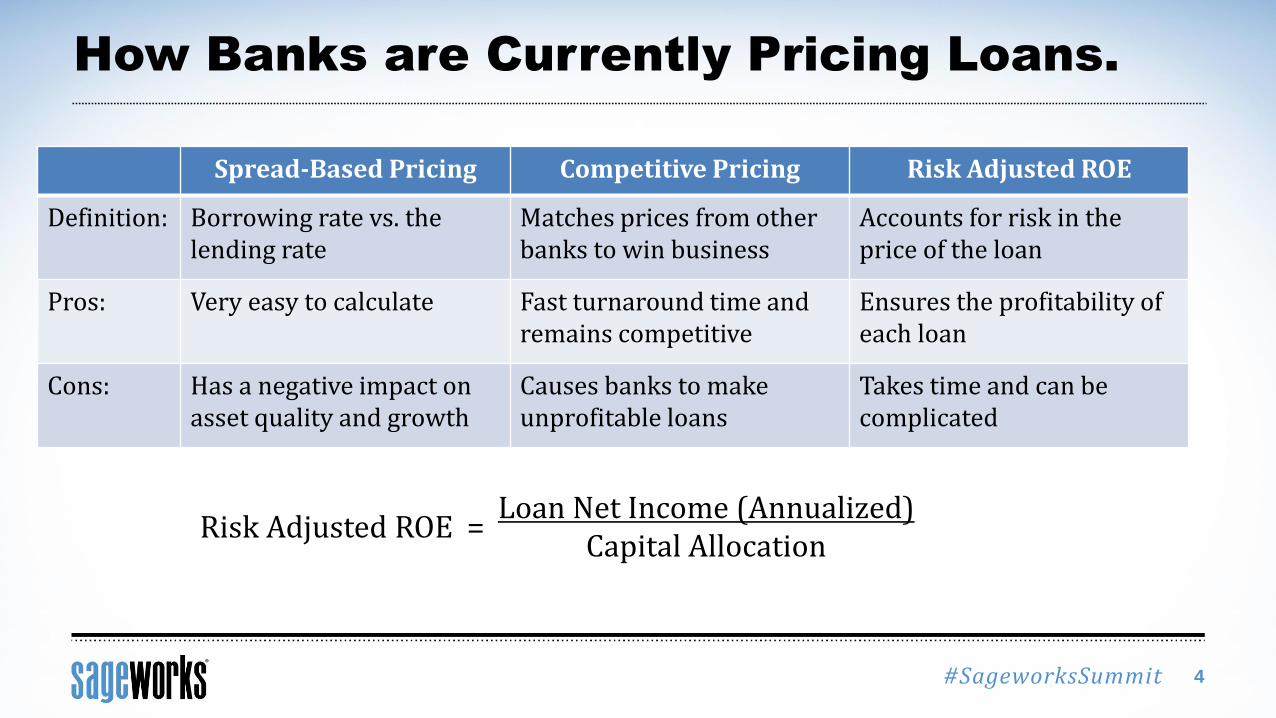

How Banks are Currently Pricing Loans.

Spread-Based Pricing Competitive Pricing Risk Adjusted ROE

Definition: Borrowing rate vs. the lending rate

Matches prices from other banks to win business

Accounts for risk in the price of the loan

Pros: Very easy to calculate Fast turnaround time and remains competitive

Ensures the profitability of each loan

Cons: Has a negative impact on asset quality and growth

Causes banks to make unprofitable loans

Takes time and can be complicated

4

Risk Adjusted ROE = Loan Net Income (Annualized)

Capital Allocation

#SageworksSummit

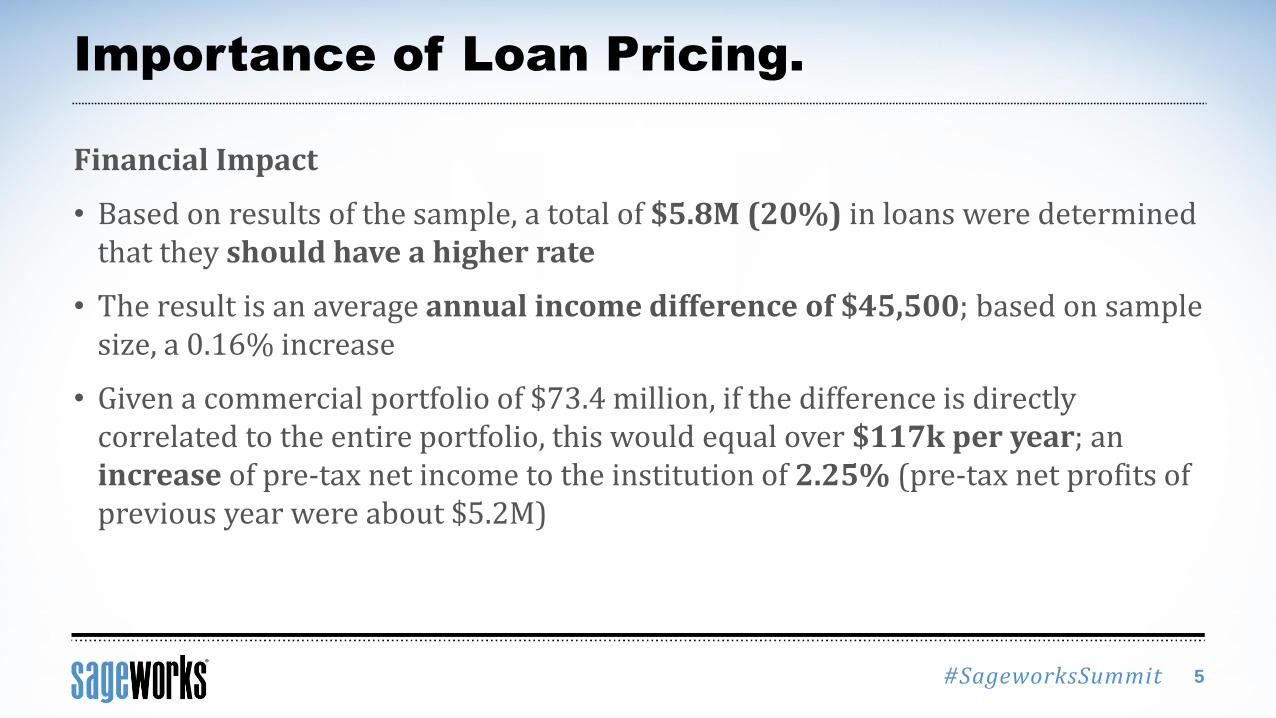

Importance of Loan Pricing.

Financial Impact

• Based on results of the sample, a total of $5.8M (20%) in loans were determined that they should have a higher rate

• The result is an average annual income difference of $45,500; based on sample size, a 0.16% increase

• Given a commercial portfolio of $73.4 million, if the difference is directly correlated to the entire portfolio, this would equal over $117k per year; an increase of pre-tax net income to the institution of 2.25% (pre-tax net profits of previous year were about $5.2M)

5

#SageworksSummit

Importance of Loan Pricing.

Non-Financial Impact

• Identify supply and demand imbalances in the markets

» Loans whose rates more than cover the risk will generate more revenue

• Risk pricing can assist the institution in problem loan situations

» Pricing risk within the loan agreement and covenants provides potential additional income, but it also disincentives borrowers from engaging in riskier activities

• The system will provide additional data and documented trend analysis on risk within the loan portfolio that can be used to inform and justify more subjective aspects of the ALLL

6

#SageworksSummit

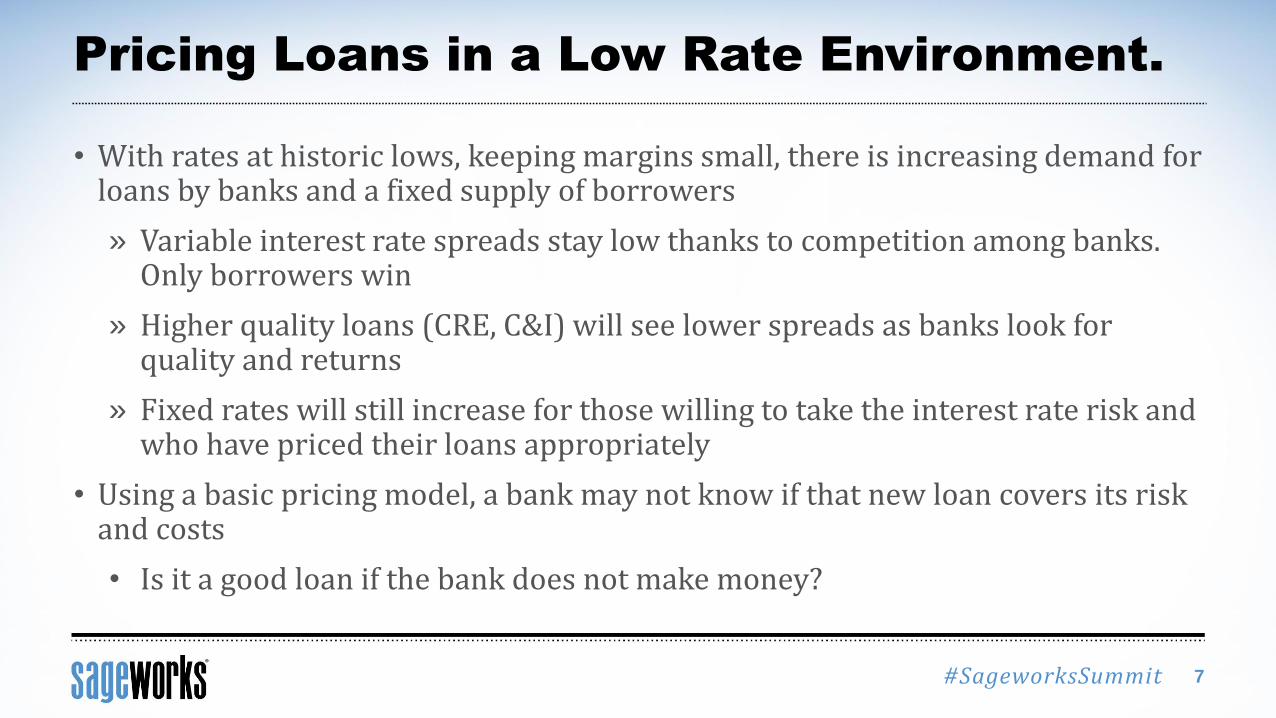

Pricing Loans in a Low Rate Environment.

• With rates at historic lows, keeping margins small, there is increasing demand for loans by banks and a fixed supply of borrowers

» Variable interest rate spreads stay low thanks to competition among banks. Only borrowers win

» Higher quality loans (CRE, C&I) will see lower spreads as banks look for quality and returns

» Fixed rates will still increase for those willing to take the interest rate risk and who have priced their loans appropriately

• Using a basic pricing model, a bank may not know if that new loan covers its risk and costs

• Is it a good loan if the bank does not make money?

7

#SageworksSummit

Agenda.

• Banks currently have a number of methods they use to price loans

» How does your bank price loans?

» How important is a loan pricing strategy?

• What are the factors of a successful loan pricing model

» Case study: Risk ratings & loan pricing

• How loan pricing will help you meet your strategic goals and make your investors happy

» Sample loan pricing model scenarios

8

#SageworksSummit

Factors of a Successful Loan Pricing Strategy.

• A strong credit culture and defined risk appetite

• An objective risk rating process

» 59% of bankers surveyed by Sageworks said their current risk rating process was too subjective, not applied uniformly, or both

» Often determines credit approval process and price for the loan; incorrect ratings could lead to undue risk in the portfolio

• Corporate income strategy

» Defined thresholds for expected returns (ROE and ROA)

• Relationship mentality

» Bankers and borrowers should both win when you have their relationship

• Defined servicing costs

9

#SageworksSummit

The Cost of Servicing a Customer.

Typical loan expenses:

» Funding Cost - The cost the institution will incur in securing funds to make the loan that is being priced

» Credit Risk Expense - The risk of default on the loan that may arise from the borrower failing to make required payments.

» Origination Expense – The up front cost to the bank for underwriting and originating the loan

Watch out for these expenses:

» Servicing Expense – The cost to maintain the loan over the duration of the relationship

» Overhead Expense - The institution's general and administrative costs associated with this loan in the loan pricing decision.

10

#SageworksSummit

Using Risk Ratings to Quantify Credit Risk.

11

#SageworksSummit

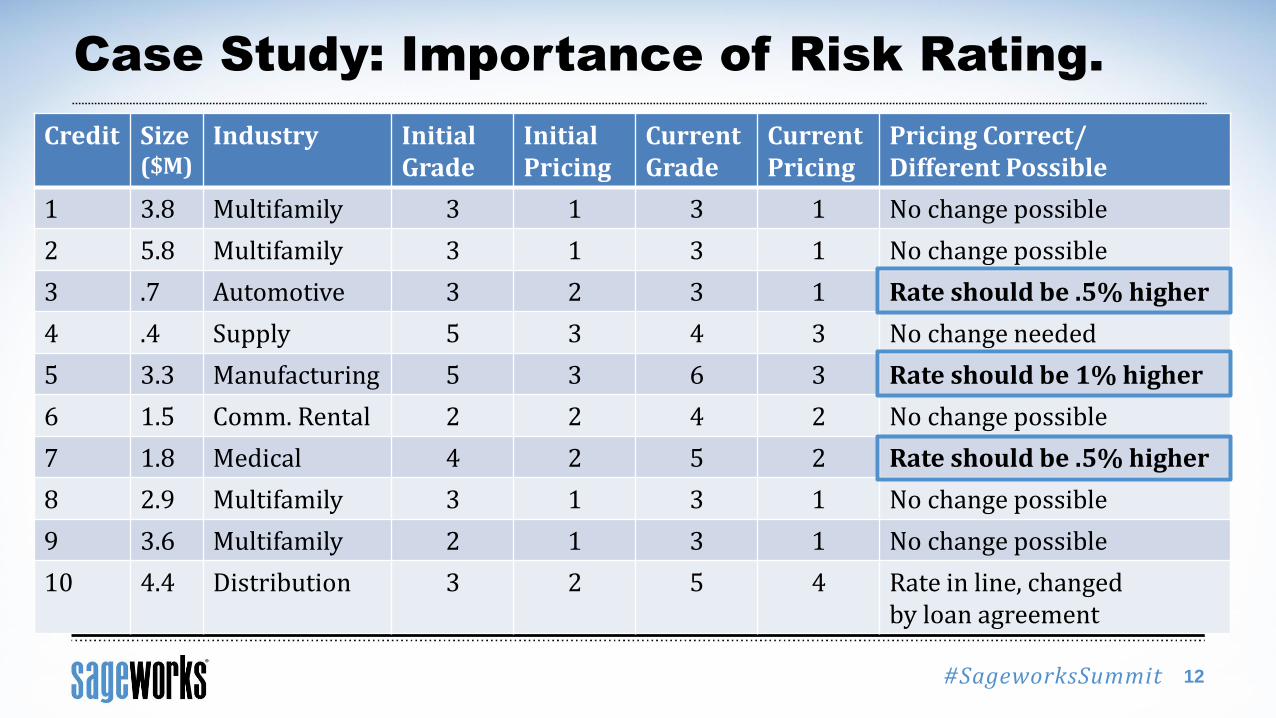

Case Study: Importance of Risk Rating.

12

Credit Size ($M)

Industry Initial Grade

InitialPricing

CurrentGrade

Current Pricing

Pricing Correct/Different Possible

1 3.8 Multifamily 3 1 3 1 No change possible

2 5.8 Multifamily 3 1 3 1 No change possible

3 .7 Automotive 3 2 3 1 Rate should be .5% higher

4 .4 Supply 5 3 4 3 No change needed

5 3.3 Manufacturing 5 3 6 3 Rate should be 1% higher

6 1.5 Comm. Rental 2 2 4 2 No change possible

7 1.8 Medical 4 2 5 2 Rate should be .5% higher

8 2.9 Multifamily 3 1 3 1 No change possible

9 3.6 Multifamily 2 1 3 1 No change possible

10 4.4 Distribution 3 2 5 4 Rate in line, changed by loan agreement

#SageworksSummit

Revisiting the Importance of Loan Pricing.

Financial Impact

• Based on results of the sample, a total of $5.8M (20%) in loans were determined that they should have a higher rate

• The result is an average annual income difference of $45,500; based on sample size, a 0.16% increase

• Given a commercial portfolio of $73.4 million, if the difference is directly correlated to the entire portfolio, this would equal over $117k per year; an increase of pre-tax net income to the institution of 2.25% (pre-tax net profits of previous year were about $5.2M)

13

#SageworksSummit

Revisiting the Importance of Loan Pricing.

Non-Financial Impact

• A clear risk rating system helps to minimize subjectivity and variability of grading an individual loan between all loan officers

» Confusion and frustration from the lack of consistency is minimized

• Objective and updated risk ratings provide documentation for the justification of a loan within the smaller grades

• Risk pricing can assist the institution in problem loan situations

» Pricing risk within the loan agreement and covenants provides potential additional income, but it also disincentives borrowers from engaging in riskier activities

• The system will provide additional data and documented trend analysis on risk within the loan portfolio that can be used to inform and justify more subjective aspects of the ALLL

14

#SageworksSummit

How to Appropriately Price Risk Into Loans.

• Loans with high LTV and low debt service coverage ratios should be priced higher to account for charge-offs

• High loan prices allow the bank to put more money into ALLL augment capital to support risks being taken

15

Overpriced(High Price/Low Risk)

Strategic(Priced Correctly)

Routine(Priced Correctly)

Underpriced(Low Price/High Risk)

Risk

Pri

ce

#SageworksSummit

Agenda.

• Banks currently have a number of methods they use to price loans

» How does your bank price loans?

» How important is a loan pricing strategy?

• What are the factors of a successful loan pricing model

» Case study: Risk ratings & loan pricing

• How loan pricing will help you meet your strategic goals and make your investors happy

» Sample loan pricing model scenarios

16

#SageworksSummit

Loan pricing helps meet your strategic goals.

• Priced loans will generate an ROE and ROA for both the loan and the relationship

» After accounting for credit risk, servicing costs, relationship income and contributed capital

• A positive ROE, for instance, means the bank is making money on the loan, but is it making enough money for the bank?

» A 5% ROE may not cover taxes and other variable costs

» If all loans had an average ROE of 5%, could the bank actually make money?

» Consider setting minimum thresholds for ROE, ROA or both

17

#SageworksSummit

Variable factors that drive changes to ROE.

• When structuring loans to be priced, these factors can have considerable impact on the price as well as ROE and ROA

» Risk rating

» Funding curve

» Structure (Fixed payment, balloon, line of credit etc)

» Term/Amortization

» Relationship income

• Bringing pricing into the process earlier might help optimize final structure and term

18

#SageworksSummit

Variable factors continued.

• Bankers will find that using specific structures and term will likely mean successful pricing

» Standardizing structures will also benefit borrowers (“our best rates are for 6 year terms right now”)

• Relationship income is one of the largest drivers of profitability, asking for their business or their deposit WILL get them a lower rate

• Consider holding interest bearing deposits for the term of the loan

• Does your bank offer treasury, insurance, trust or brokerage products?

19

#SageworksSummit

Best Practices for ROE and ROA Thresholds.

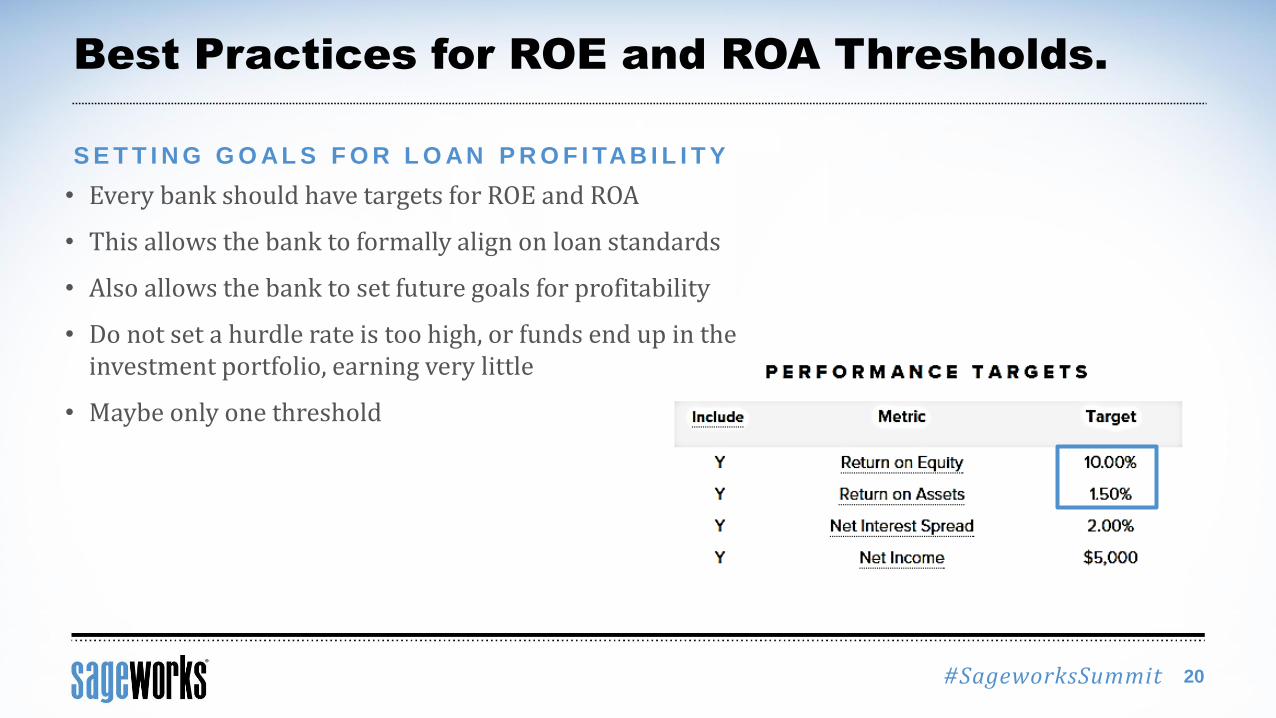

• Every bank should have targets for ROE and ROA

• This allows the bank to formally align on loan standards

• Also allows the bank to set future goals for profitability

• Do not set a hurdle rate is too high, or funds end up in the investment portfolio, earning very little

• Maybe only one threshold

20

S E T T I N G G O AL S F O R L O AN P R O F I TAB I L I T Y

#SageworksSummit

Best Practices for ROE and ROA Thresholds.

21

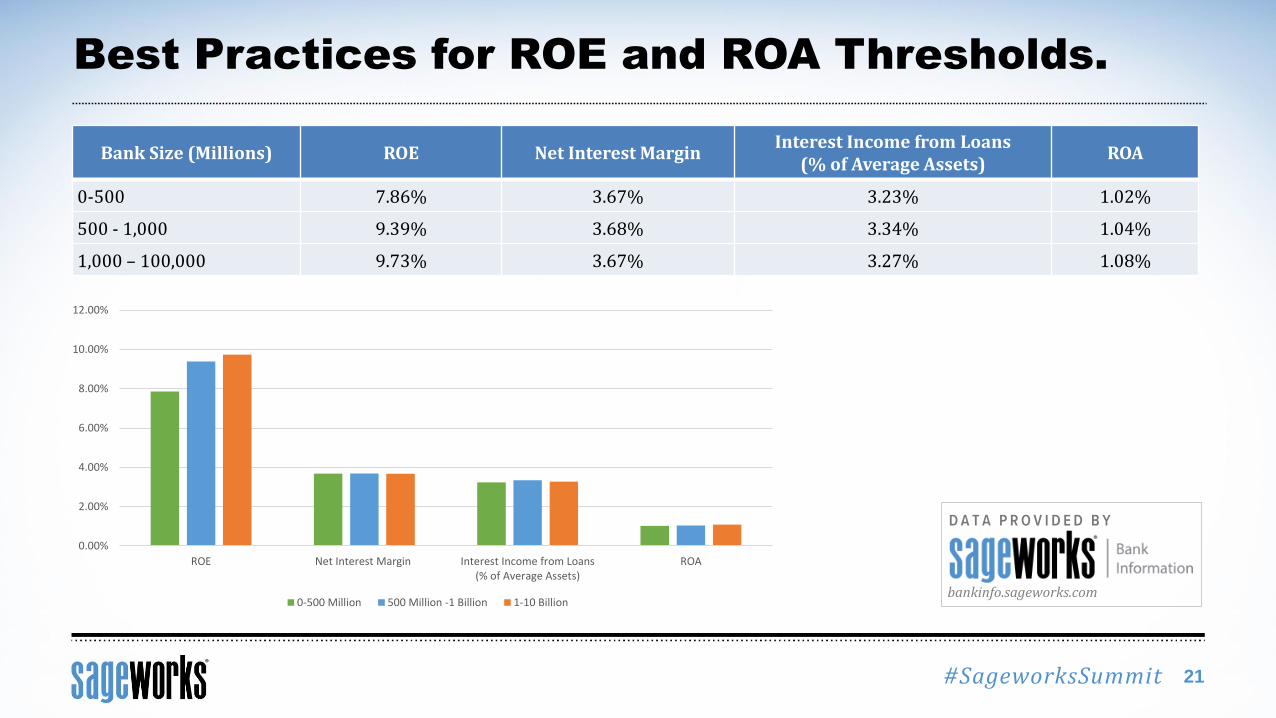

Bank Size (Millions) ROE Net Interest Margin Interest Income from Loans

(% of Average Assets)ROA

0-500 7.86% 3.67% 3.23% 1.02%

500 - 1,000 9.39% 3.68% 3.34% 1.04%

1,000 – 100,000 9.73% 3.67% 3.27% 1.08%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

ROE Net Interest Margin Interest Income from Loans(% of Average Assets)

ROA

0-500 Million 500 Million -1 Billion 1-10 Billion

D A T A P R O V I D E D B Y

bankinfo.sageworks.com

#SageworksSummit

RISK RATING = 5(MARGINALLY ACCEPTABLE)

RISK RATING = 4(ACCEPTABLE RISK)

RISK RATING = 1(MINIMAL RISK)

Example: Impact of Risk Ratings on Profitability.

22

TERMS