leveraging technology in a down economy - ncr...

TRANSCRIPT

Like many businesses, retail and hospitality organiza-

tions may be tempted to cut their information tech-

nology budgets during tough times. Companies

struggling with slow sales and high fixed costs may

see large-scale IT investments as a logical target for

belt-tightening. In reality, technology investments

that enable operational efficiency, reduce labor costs

and improve customer service capabilities are some

of the best business moves retail and hospitality

companies can make. They can mitigate the worst

effects of economic downturns, and also position

these organizations to quickly gain market share,

increase sales and boost profits when times begin to

improve. Customer-facing applications, such as self-

service technology, and applications offering a fast

ROI, such as lifecycle pricing, are just two IT invest-

ments that can pay handsome returns during eco-

nomic downturns.

Leveraging Technologyin a Down EconomyMANAGING COSTS AND IT INVESTMENTS

SO YOU EMERGE STRONGER WHEN TIMES IMPROVE

A RIS NEWS AND HOSPITALITY TECHNOLOGY WHITEPAPER

PRODUCED BY

SPONSORED BY

®

LEVERAGING TECHNOLOGY IN A DOWN ECONOMY

Corporate investments in IT have surged sincethe mid-1990s—from about $3,500 spent perworker in 1994 to about $8,000 in 2004,according to the Bureau of Economic Analysis.“At the same time, annual productivity growthin U.S. companies roughly doubled, after plod-ding along at about 1.4% for nearly 20 years,”write Andrew McAfee and Erik Brynjolfssonin the July-August 2008 Harvard BusinessReview article, “Investing in the IT That Makesa Competitive Difference.”

Since this IT intensification took place, tech-nology has become embedded in every aspectof business—and has become one of the mostimportant ways companies compete. The

authors write: “Our field research suggests thatbusinesses entered a new era of increased com-petitiveness in the mid-1990s not because theyhad so many IT innovations to choose from butbecause some of these new technologiesenabled improvements to companies’operatingmodels and then made it possible to replicatethose improvements much more widely.”

IT’s mission-critical relevance during bothgood and bad economic times translates intotwo important messages for the current eco-nomic crisis. First, if tough times demand thatIT budgets must be cut, these cuts must bedone with a scalpel rather than a chainsaw.Indiscriminate slashing or across-the-boardreductions can affect not only day-to-day oper-ational efficiency but a company’s competitivedifferentiation, leaving it in a far weaker posi-tion when the economy rebounds.

Second, smart IT investment and careful man-agement can be powerful tools to not onlyweather economic storms but to actuallyimprove a company’s capabilities, allowingthese businesses to improve their position rela-tive to their competitors.

There are some strong indications that IT exec-utives throughout the business world alreadyhear this message loud and clear. While currentglobal economic problems are affecting ITbudgets, research firm Gartner Inc. said inOctober 2008 that reductions will not be assevere as they were during the dot-com bust in2001. At that time, budgets were slashed frommid double-digit growth to low single-digitgrowth. However, Gartner’s “worst-case sce-nario” for today indicates an IT spendingincrease of 2.3 percent in 2009, down from anearlier projection of a 5.8 percent increase.Gartner analysts speaking at the October 2008Gartner Symposium/ITxpo predicted that ITspending in the U.S. and Japan would be flat in2009, while Europe would experience negativegrowth. While emerging regions would not beas severely affected as developed areas, theywould not be immune.

In addition, Marianne Kolbasuk McGee

2

Tough economic times provide an uptick in at leastone area: metaphors to describe the turmoil. Falling dominoes, houses of cards and perfect stormsare being countered with tin cups, bailouts and Hail Mary passes. However, it’s the job of businessand information technology professionals to lookbeyond both colorful metaphors and short-term fixes. Sober assessments of the value of IT reveal its absolutely crucial role in every aspect of today’seconomy—a role that will continue to grow in importance well into the 21st century.

JULY 2008 MARCH 2008

New Hires 72% 76%

Infrastructure upgrades 60% 55%

New application development 46% 45%

New outsourcing engagements 29% 28%

End-user technology 25% 30%

Other 5% 2%

LEVERAGING TECHNOLOGY IN A DOWN ECONOMY

recently wrote in InformationWeek that “Thereare plenty of business technology executivesgoing forward with big projects, even adding totheir IT workloads—and budgets—with newprojects, backed by managements that see achance to invest in technology-driven efforts toleap ahead of weakened competitors.” McGeeadded that customer-facing projects were onlyhalf as likely to be cut as those that didn’t touchcustomers, and that “smart CIOs are lookingfor ways to use the IT tools at their disposal tocut costs in their organizations and in otherparts of their companies.”

How Are Retail and Hospitality Dealingwith the Downturn?Obviously, hard times have different impactson different parts of the retail and hospitalityindustries. High-end retail and luxury resortsare likely to take more of a hit than other seg-ments, while supermarkets, do it yourself(DIY) retailers and quick service restaurants(QSRs) may actually benefit from a slowdown.

Several leading analysts see the same generalbusiness strategies—cautious budget cuttingand close examination of IT projects—takingplace in the retail and hospitality industries. Inaddition, the focus on customer-facing tech-nologies, especially those that enhance the cus-tomer experience or improve operational effi-ciency, or both, seems strong. Self-servicetechnology, which allows retail and hospitalitycompanies to more effectively allocate laborwhile meeting both existing and new customerneeds, fits these criteria well.

Overall, however, caution is today’s byword.“There’s certainly been an impact on how com-panies are spending their IT dollars,” saysKevin Sterneckert, Director-Research Analystat AMR Research. “We’ve seen that the largeERP (Enterprise Resource Planning) deals aretough to come by, and that sales cycles for tech-nology are lengthening. Retailers know thatthey need these technologies, but their budgetsmay not allow it at this point—they are in a‘wait and see’ mode.

“What we do see, however, is significant activ-

3

9%

14%

10%

7% 28%

13%

19%

Up more than 10%

Up 5% to 10%

Up less than 5%

FlatDown lessthan 5%

Down5% to 10%

Down morethan 10%

SOURCE: InformationWeek Research State of the Economy Survey of 612 business technology profession-als, 2008

SOURCE: InformationWeek Research State of the Economy Survey of 612 business technology profession-

als; 386 respondents in July and 208 in March experiencing IT spending cutbacks

WHICH TYPES OF PROJECTS OR INVESTMENTSARE YOU MOST LIKELY TO SCALE BACK?

HOW WILL YOUR COMPANY’S IT SPENDING THIS YEAR COMPARE WITH LAST YEAR?

ity around solutions that have implementationtimes of six to nine months, maybe a year, andthat have a direct impact on the balance sheet,”Sterneckert adds. “We’re actually seeing someacceleration if a project offers a quantifiablebenefit or ROI that will improve sales, reducecosts or improve margins.”

Shorter, More Quantifiable ROIs SoughtSterneckert’s colleague Mike Griswold, VicePresident for Retail at AMR, notes that manycompanies had already gone through their2008 budgeting process and earmarked fundsby the time the worst of the financial storm hitin the fall. “Companies are still spending

money this year, and will be into early 2009,”says Griswold. However, he adds that retailersare establishing a series of three “hurdles” thatany IT project must clear in order to beapproved and implemented.

“The first hurdle is that projects need to havea very quantifiable ROI,” notes Griswold.“The second hurdle has to do with timeframe. Retailers that had been comfortablewith 18- to 24-month paybacks are now look-ing at six to nine months, 12 at the most.Projects don’t need to have a complete pay-back in that time, but they do need to startshowing value.”

The third hurdle involves business adoptabil-ity. “Companies are asking about the amountof change management involved in a project,”Griswold says. “Those with huge changemanagement or training components arebeing postponed, because the companies feelthey can’t afford to have that many peopledisrupted or distracted.”

Griswold cites lifecycle pricing applicationsas particularly attractive to retailers. “There’sa lot of value around intelligently setting your

LEVERAGING TECHNOLOGY IN A DOWN ECONOMY

4

58%

36%

38%

39%

40%

58%

36%

30%

24%

18%

PCI compliance

Providing associates with better tools

Loss prevention

Inventory visibility

Advanced CRM/loyalty programs

Kiosks

Cross-channel integration

Workforce management

Reduce out-of-stocks

Speed through checkout

5

SOURCE: RIS News/IHL Group 2009 Store Systems Study

TOP STORE SYSTEM PRIORITIES FOR 2009

base price,” he notes. “Most retailers have afairly aggressive competitor pricing program,but it’s very manual, and there’s not a lot ofscience behind it to help them understandhow sharp they need to be with their competi-tors. Retailers need to get credit for beingpriced better than their competition, but theycan’t gouge themselves so much that they’regiving away their gross margins.

“This is especially true in the area of promo-tions,” he adds. “Retailers need to bring peo-ple in with promotional pricing but not togive away the store. Using the science behindlifecycle pricing, they can figure out that theycan get just as much traffic if they promote anitem at 99 cents as they would if they promot-ed it at 89 cents. Typically what had happenedwas that the retailer would price it at 89 centsjust because that’s how they’ve always pricedit, so the science is a huge benefit in terms ofsaving gross margins.”

Could Downturn be a Mini Tech Boomfor Hospitality?In the hospitality industry, the current crisismay actually be a spur to technology invest-ment, according to Pearl Brewer, PhD,

Professor and Executive Director of GraduateStudies at the William F. Harrah College ofHotel Administration at the University ofNevada, Las Vegas. Historically a recessionwould have been a cue to make across-the-board cutbacks in technology spending. Butshe notes that some hospitality executives areviewing this crisis as “an opportunity to putinto place technologies that had been on theback burner.”

She adds that the hospitality industry has his-torically been slow to adopt new technolo-gies, so hotels and restaurants may be takingadvantage of lower prices to introduce newapplications—not new to the world in gener-al, but new to the industry. And as in the retailindustry, any technology implementationneeds to meet tough criteria—in this case toreduce costs, increase revenues, or enhancecustomer service. “What I’m hearing is thatnow a technology may need to accomplishtwo of those things before it will be looked atseriously,” says Dr. Brewer.

Jeff Roster, Research Vice President forRetail at Gartner, notes that this downturn isshowing several important differences fromprevious ones. “Historically many retailershave responded to bad economic data byacross-the-board spending cuts,” says Roster.“A few retailers, Wal-Mart being the bestexample, continued on with their strategic ITinitiatives, because they wanted to be in a bet-ter position to take advantage of the rebound-ing economy when the downturn ended.”

Roster adds that he expects overall IT budg-ets to remain mostly intact. “E-commerceintegration, business intelligence, CRM, sup-ply chain visibility and many others are justtoo critical to the retailers’ overarching strate-gies to slow down or cancel,” he notes.“Many of these projects had passed aggres-sive ROI hurdles before launching, so theyshould continue.”

Roster adds that while he has not seen manylayoffs in retail IT, “obviously a lot hinges onChristmas 2008. If it lives up to (or down to)

21%

21%

21%

14%

13%

6%

6%

6%

17%

31%

18%

18%

20%

In-room entertainment systems

Wi-Fi hotspots

In-room checkout

Infrastructure for handheld

Internet kiosk in lobby

Check-in/out kiosks in lobby

Online check-in/out

VOIP

Kiosk for airline check-in/boarding pass

Wireless check-in available offsite

Support for slingbox

RFID

Biometrics for payment, security

LEVERAGING TECHNOLOGY IN A DOWN ECONOMY

5

53%Enhanced customer experience

41%

20%

16%

6%

Generate revenue

Differentiate from competition

Lower expenses

Increase security

SOURCE: Spring 2008 study for the American Hotel Lodging Association Foundation, by University of

Nevada, Las Vegas

HOTELIERS’ MOST IMPORTANT IT GOALS FOR THE NEXT 5 YEARS

SOURCE: Spring 2008 study for the American Hotel Lodging Association Foundation, by University of

Nevada, Las Vegas

PERCENTAGE OF PROPERTIES PLANNING TO OFFER EACH TECHNOLOGY WITHIN 5 YEARS

some of the apocalyptic predictions some aremaking, I think layoffs are a given.”

Enhancing Customer Service a Crucial IT Test in HospitalityAs with virtually all other IT investments, cus-tomer-facing technologies such as self-serviceare being subjected to stringent analysis byretail and hospitality organizations.

In hospitality, self-service technology needs toprovide some combination of lower labor costs,increased revenue or increased customer satis-faction. The last element is particularly impor-tant to hoteliers, who identified enhancing thecustomer experience as their top IT goal for thenext five years, in the spring 2008 study for theAmerican Hotel Lodging AssociationFoundation conducted by the University ofNevada, Las Vegas.

Brewer, one of the study’s authors, gave theexample of self-service concierge kiosks fea-turing user-friendly, intuitive interfaces thattake advantage of recent advances in searchtechnology. Such technology could accom-plish multiple goals: answering guests’queries and providing the hotel withupselling opportunities without having toemploy a concierge at all times.

Other self-service possibilities include lobbyor front desk kiosks that allow guests tocheck in or check out of hotels, as well asunits that let travelers print airline boardingpasses. Brewer notes that increasing numbersof hotels are placing such self-service kiosksin prominent locations, banking on guests’increasing comfort level with self-service ingeneral and these technologies in particular.

The AHLA foundation study identified avariety of kiosk types among technologieshoteliers plan to offer within five years,including Internet kiosk in lobby (20 per-cent of respondents); check-in/out kiosks inlobby (18 percent); and kiosks for airlinecheck-in/boarding pass (14 percent).

In restaurants, especially the quick service

Continued on page 8

Q: Given the current turmoil anduncertainty in the marketplace,is it realistic to expect thatretail and hospitality compa-nies will continue to invest intechnology?

WEBSTER: Technology is suchan important enabler for retail-

ers, restaurants and hotels that we do expect themto continue to invest. What has changed is thefocus on sustainable cost reductions, and deliver-ing a better return on invested capital (ROIC). Thisis where self-service is different from other infra-structure investments, in that is has a proven abili-ty to reduce operating costs. Self-service is aboutmigrating high frequency, low value transactions toa more convenient channel—for example, enteringan order at the deli or restaurant, or dispensing aroom key. By automating these transactions withself-service, companies can reduce and re-allo-cate staff and create additional capacity. Self-serv-ice delivers a superior ROIC.

Q: Will tighter times mean that retail and hospitalitycompanies will be more interested in deployingself-service in order to save on labor costs?

WEBSTER: That will likely be the case, as self-serv-ice is a proven method to drive productivity and laborsavings. But this is only one element of the value

proposition. Retailers not only get lower operatingcosts when deploying self-service, but they alsoget the ability to create a better experience for theircustomers. For example with self-checkout, busi-nesses are able to redeploy labor hours to otherareas of the store, while reducing the amount oftime customers spend waiting in line by 40 percent,and getting them through the checkout 20 percentfaster. Imagine the impact this has on customerattraction and retention.

We’ve seen some self-service vendors get this bal-ance of labor costs and customer service wrong—they say that self-service technology allows con-sumers to reduce contact with store associates. AtNCR, we philosophically and fundamentally dis-agree with that approach. Self-service is all aboutcreating a new world of interaction; one that isfaster, easier and transforms the way that yourstaff and customers work together.

Q: How do you see consumer behavior being shapedby economic conditions?

WEBSTER: Now more than ever, consumers want amultichannel experience. They are time starved,and demand choice, convenience and speed ofservice. Consumers want the ability to browseonline, review products, and get pricing informa-tion. They want to be able to find information viatheir mobile device, regardless of their location. In

LEVERAGING TECHNOLOGY IN A DOWN ECONOMY

6

Self-Service Technology Provides a Customer Connection in Tough TimesMIKE WEBSTER, CHIEF STRATEGY AND COMMUNICATIONS OFFICER, NCR CORPORATION

“Self-service is all about creating a new world of interaction; one that is faster, easier and transforms the

way that your staff and customers work together.”

LEVERAGING TECHNOLOGY IN A DOWN ECONOMY

7

“Self-service is about migrating high frequency,low value transactions to a more convenient channel—for example, entering an order at the deli or restaurant,

or dispensing a room key. By automating these transactions with self-service, companies can reduce and re-allocate staff and create additional capacity.”

For more information visit www.ncr.com oremail [email protected].

this economic environment, the real winners willensure that these channels are seamlessly inte-grated and consistent. NCR surveyed consumersabout their multichannel preferences, and 97 per-cent of respondents said they would use a combi-nation of self-service channels in their interactionswith retailers.

Q: What advice can you give businesses that hadlengthy technology agendas and now need to prior-itize based on the economy’s impact?

WEBSTER: While traditional financial metrics arecertainly relevant and important, companies shouldlook beyond mere operating costs. They should lookat investments that change the way they connectwith their customers. Economic uncertainty createsboth risk and opportunity. Prioritizing investmentsthat directly impact the customer experience willmove to the top.

Q: How can NCR help retailers and hospitality com-panies weather this economic storm?

WEBSTER: NCR has a significant role to play in help-ing our retail and hospitality customers make deci-sions about their technology investments during thisdifficult time. NCR has 125 years of experience inhow best to take advantage of change, in both goodtimes and bad. We understand how consumers wantto interact, connect and transact with companies,and our history and solutions can help companiesnavigate this period as well as possible. We havemore than 20,000 professionals in over 100 coun-tries that are mobilized to help retailers ride out thisstorm. ●

segment, self-service kiosks that are integrat-ed into point of sale and kitchen managementsystems may help restaurateurs control laborcosts, a key factor in maintaining margins. Inaddition, self-service technology may relievethe pressure on QSRs’ perennially highemployee turnover rates, reducing theexpense of frequently hiring and trainingnew employees.

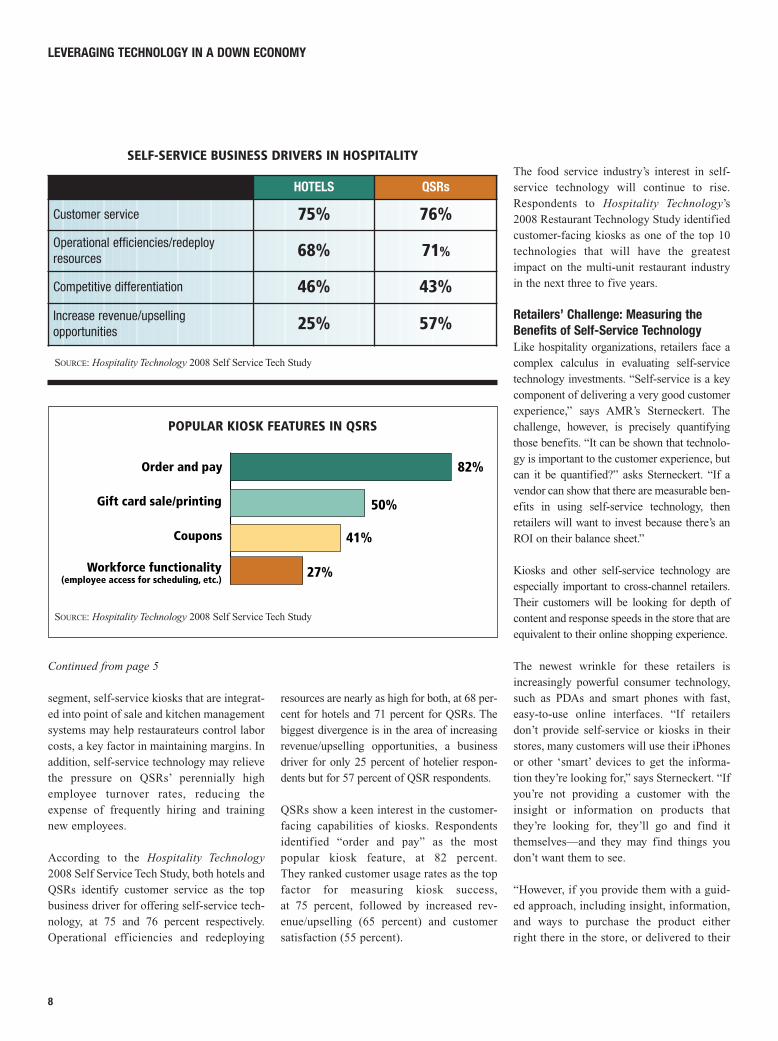

According to the Hospitality Technology2008 Self Service Tech Study, both hotels andQSRs identify customer service as the topbusiness driver for offering self-service tech-nology, at 75 and 76 percent respectively.Operational efficiencies and redeploying

LEVERAGING TECHNOLOGY IN A DOWN ECONOMY

8

resources are nearly as high for both, at 68 per-cent for hotels and 71 percent for QSRs. Thebiggest divergence is in the area of increasingrevenue/upselling opportunities, a businessdriver for only 25 percent of hotelier respon-dents but for 57 percent of QSR respondents.

QSRs show a keen interest in the customer-facing capabilities of kiosks. Respondentsidentified “order and pay” as the most popular kiosk feature, at 82 percent. They ranked customer usage rates as the topfactor for measuring kiosk success, at 75 percent, followed by increased rev-enue/upselling (65 percent) and customersatisfaction (55 percent).

The food service industry’s interest in self-service technology will continue to rise.Respondents to Hospitality Technology’s2008 Restaurant Technology Study identifiedcustomer-facing kiosks as one of the top 10technologies that will have the greatestimpact on the multi-unit restaurant industryin the next three to five years.

Retailers’ Challenge: Measuring theBenefits of Self-Service TechnologyLike hospitality organizations, retailers face acomplex calculus in evaluating self-servicetechnology investments. “Self-service is a keycomponent of delivering a very good customerexperience,” says AMR’s Sterneckert. Thechallenge, however, is precisely quantifyingthose benefits. “It can be shown that technolo-gy is important to the customer experience, butcan it be quantified?” asks Sterneckert. “If avendor can show that there are measurable ben-efits in using self-service technology, thenretailers will want to invest because there’s anROI on their balance sheet.”

Kiosks and other self-service technology areespecially important to cross-channel retailers.Their customers will be looking for depth ofcontent and response speeds in the store that areequivalent to their online shopping experience.

The newest wrinkle for these retailers isincreasingly powerful consumer technology,such as PDAs and smart phones with fast,easy-to-use online interfaces. “If retailersdon’t provide self-service or kiosks in theirstores, many customers will use their iPhonesor other ‘smart’ devices to get the informa-tion they’re looking for,” says Sterneckert. “Ifyou’re not providing a customer with theinsight or information on products thatthey’re looking for, they’ll go and find itthemselves—and they may find things youdon’t want them to see.

“However, if you provide them with a guid-ed approach, including insight, information,and ways to purchase the product eitherright there in the store, or delivered to their

HOTELS QSRs

Customer service 75% 76%

Operational efficiencies/redeployresources 68% 71%

Competitive differentiation 46% 43%

Increase revenue/upselling opportunities 25% 57%

SOURCE: Hospitality Technology 2008 Self Service Tech Study

SELF-SERVICE BUSINESS DRIVERS IN HOSPITALITY

82%Order and pay

50%

41%

27%Workforce functionality(employee access for scheduling, etc.)

Coupons

Gift card sale/printing

SOURCE: Hospitality Technology 2008 Self Service Tech Study

POPULAR KIOSK FEATURES IN QSRS

Continued from page 5

LEVERAGING TECHNOLOGY IN A DOWN ECONOMY

9

home via ‘white glove’ delivery, you havethe opportunity to further improve the expe-rience for the customer,” he adds. “It may bedifficult to quantify the benefits of self-service technology, but it’s easy to see that ifyou don’t offer it, there’s a very visibledownside risk. People will find some way toget the information they need, and theorganization loses the opportunity to influ-ence their experience.”

Consumers’ Own Technology a GrowingFactor in Self-ServiceAMR’s Griswold agrees that advanced con-sumer technology needs to be taken intoaccount. “We’re quickly reaching a pointwhere retailers across all segments will needto acknowledge that consumers will havebetter technology than the store itself, andthat shoppers are more in tune with how touse it than store associates,” he says. “I thinkthat means that retailers will be movingaway from store proprietary-type technolo-gy, to getting consumers to ‘opt in’ and usetheir own device while they’re in the store.”

Griswold noted that systems involving shop-pers’ mobile phones have already seen wide-spread success in the Asia/Pacific region andare moving into Europe. “There are three bil-lion mobile phones in the world, and only 1.4billion people with credit cards. We have toconnect with people with their cell phones, anduse technology to turn the mobile device into apayment vehicle,” he says.

That said, Griswold still thinks there’s astrong role for kiosks and other self-servicetechnology. “It needs to be a well-thought-out strategy that’s linked to the retailer’sbrand. A high-end retailer that prizes one-on-one, personalized interactions with shop-pers may not use kiosks, but for others itmakes perfect sense,” he says. “It can beused for a checking-in process, to downloadoffers or coupons, or to provide information.In grocers like Safeway and Kroger, they’repiloting deli ordering via kiosk, where cus-tomers place the order and then circle backto pick it up.”

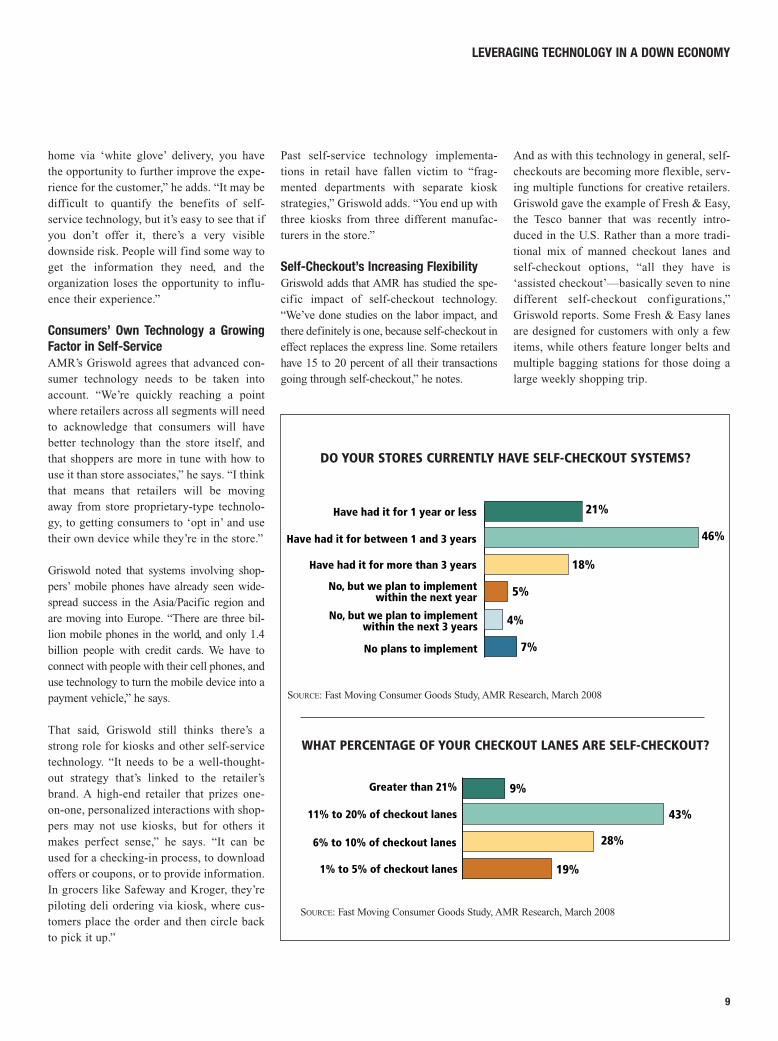

21%Have had it for 1 year or less

18%

46%

5%

4%

7%

Have had it for between 1 and 3 years

Have had it for more than 3 years

No, but we plan to implementwithin the next year

No, but we plan to implementwithin the next 3 years

No plans to implement

9

DO YOUR STORES CURRENTLY HAVE SELF-CHECKOUT SYSTEMS?

9%

43%

28%

19%

Greater than 21%

11% to 20% of checkout lanes

6% to 10% of checkout lanes

1% to 5% of checkout lanes

SOURCE: Fast Moving Consumer Goods Study, AMR Research, March 2008

WHAT PERCENTAGE OF YOUR CHECKOUT LANES ARE SELF-CHECKOUT?

Past self-service technology implementa-tions in retail have fallen victim to “frag-mented departments with separate kioskstrategies,” Griswold adds. “You end up withthree kiosks from three different manufac-turers in the store.”

Self-Checkout’s Increasing FlexibilityGriswold adds that AMR has studied the spe-cific impact of self-checkout technology.“We’ve done studies on the labor impact, andthere definitely is one, because self-checkout ineffect replaces the express line. Some retailershave 15 to 20 percent of all their transactionsgoing through self-checkout,” he notes.

And as with this technology in general, self-checkouts are becoming more flexible, serv-ing multiple functions for creative retailers.Griswold gave the example of Fresh & Easy,the Tesco banner that was recently intro-duced in the U.S. Rather than a more tradi-tional mix of manned checkout lanes andself-checkout options, “all they have is‘assisted checkout’—basically seven to ninedifferent self-checkout configurations,”Griswold reports. Some Fresh & Easy lanesare designed for customers with only a fewitems, while others feature longer belts andmultiple bagging stations for those doing alarge weekly shopping trip.

SOURCE: Fast Moving Consumer Goods Study, AMR Research, March 2008

LEVERAGING TECHNOLOGY IN A DOWN ECONOMY

10

“Fresh & Easy’s model is customer service,so they have anywhere from one to threeassociates to help customers through theprocess, either ringing things up for them orguiding them to the right units,” saysGriswold. “It’s a recognition that many differ-ent types of shoppers will use self-check-out—it’s no longer just the person with onlyfour or five items.”

Another indication that self-checkout is nowan accepted part of the mix for retailersemphasizing customer service is a pilot atsupermarket retailer Wegman’s, known for itsintense focus on enhancing the customerexperience.

“They’re responding to the desire of someshoppers to get in and get out quickly with self-service,” says Griswold. “It’s being seen asanother way to provide good customer service.There’s an increasing comfort level with self-service among consumers, and even an expec-tation that there will be a self-checkout optionwhen shoppers go to a big box-type store.”

The technology itself has become more user-friendly, he adds. “In early versions the desirewas to just get the person through the check-out quickly,” says Griswold. “Now the ver-sions out there are easier to use—it’s easier todo fruits and vegetables, and there’s morevisual stimulation about what button to pushin what order, and where the money goes.We’re seeing a focus on the user experience.”

AMR’s studies indicate how widespread self-checkout technology has become in the retailindustry, especially in the fast moving con-sumer goods (FMCG) verticals of grocery,convenience and chain drug stores. Across allthree verticals, 93 percent have had self-check-out technology for at least one year, accordingto AMR’s March 2008 FMCG study.

Of those retailers who do have the technology,43 percent offer it in between 11 to 20 percentof their total checkout lanes. Convenience andgrocery stores have higher penetrations thanchain drug stores: 92 percent of convenience

store respondents have self-checkout in morethan 5 percent of their checkout lanes, as do 85percent of grocery respondents; for chain drugstores, the figure is 64 percent.

Risks of Drastic IT CutsWith industries as diverse as retail and hospital-ity, individual companies’ IT investment strate-gies will undoubtedly vary widely. However,some advice that’s applicable across the boardis that companies need to be extremely carefulif IT budget cuts are deemed necessary.

“Losing focus on your strategic initiatives inthe midst of a financial storm is the footballequivalent of throwing away your playbookbecause you’re a touchdown behind, and draw-ing your plays in the sand,” says Gartner’sRoster. “That might work on a grammar schoolplayground but it’s not going to lead you to theSuper Bowl. You get to the promised land byexecuting flawlessly in January what you hadenvisioned in August.”

In the retail arena, the day-in, day-out devo-tion to IT by the industry’s giant, Wal-Mart, isanother key reason to carefully monitor andmaintain IT investment levels.

“The big difference in this recession comparedto recessions past is that 100 percent of theretail industry knows Wal-Mart will stay ontask and continue to press their advantage,”says Roster. “Wal-Mart will be very happyindeed if their competition curls up in a balland tries to wait this out.”

While not downplaying the seriousness oftoday’s economic crisis, AMR’s Griswoldalso advocates a careful approach to IT budg-ets. As tempting as it may be to slash duringsuch difficult times, it’s still a mistake. “Youcan’t just cut IT spending in this environ-ment. If you do, what you offer your cus-tomers will grow stagnant very quickly,” hesays. This is especially dangerous as theeconomy affects consumers’ behavior.“Customers will gravitate to a couple ofretailers who satisfy their needs; they won’tbe bopping all over town for items.”

Too much cutting can also have negativeinternal effects. “The real risk people run iscutting out intellectual property that they’llnever get back,” says Griswold. “This mightbe a particular part of their IT group work-ing on cutting-edge technology. It mayseem attractive to cut this at first and go‘back to basics.’ But things will get better,and organizations need to be as intact aspossible when that happens. If you cut toodeep, and cut areas that will provide youwith your differentiation, you create resent-ment—and you may not get those internalpeople back, which makes restarting thatmomentum very difficult.”

Griswold also feels that across-the-boardcuts can be as dangerous as cutting R&Dtoo sharply. “Simply cutting 10 percentfrom everyone is not a sound approach.You have to admit that within an organiza-tion, there are parts that are more impor-tant than others. Some you cut 10 percent,others can be cut 20 percent. You have toask what you want the organization to looklike when things recover, and then how youshape the organization so that it does lookthat way when things do get better.”

According to UNLV’s Brewer, successfulcompanies are those that stay calm andkeep their eyes open. “I think it’s true ingeneral that people who succeed at the endof the day are those who take downturns asopportunities,” she says. “And people whodo the best with technology are those thatcan see through both the technology andits application—to the things that are soobvious that when you see them done, youask ‘Why didn’t someone think of thatbefore?’”

Retail and hospitality organizations will facedifficult decisions in the months ahead.Those who view their information technolo-gy investments as tools to weather the eco-nomic storm, rather than simply as cost cen-ters that need to be trimmed, are likely to bein a better position when the clouds finallyclear away. ■